When Fast-Growing Economies Slow Down

When Fast-Growing Economies Slow Down

Barry Eichengreen

经济系

加州大学

伯克利, CA 94720, 美国

eichengr@econ.berkeley.edu

Donghyun Park

Economics and Research

Department

Asian Development Bank

6 ADB Avenue,

Mandaluyong City 1550

Metro Manila, 菲律宾

dpark@adb.org

Kwanho Shin

经济系

Korea University

5-1 Anam-Dong, Sungbuk-Ku

Seoul, 韩国 136-701

khshin@korea.ac.kr

When Fast-Growing Economies Slow

向下: International Evidence and

Implications for China*

抽象的

Using international data starting in 1957, we construct a sample of

cases where fast-growing economies slow down. The evidence

suggests that rapidly growing economies slow down significantly,

in the sense that the growth rate downshifts by at least 2 每-

centage points, when their per capita incomes reach around

美元$ 17,000 in year-2005 constant international prices, a level that China should achieve by or soon after 2015. Among our more provocative findings is that growth slowdowns are more likely in countries that maintain undervalued real exchange rates. 1. Introduction One of the most important developments affecting hu- mankind in the late 20th and early 21st centuries has been the rapid economic growth of large emerging markets, starting with China, extending now through much of Asia, and experienced increasingly in other parts of the devel- oping world. As Lawrence Summers, former Director of the White House National Economic Council, 说, “The dramatic modernization of the Asian economies ranks alongside the Renaissance and the Industrial Revolution as one of the most important developments in economic history.” Rapid economic growth, on the order of 10 每- * 这张纸, prepared for the March 2011 meeting of the Asian Economic Panel at the Earth Institute in New York, draws on joint work with Dwight Perkins, whose input we acknowledge with thanks. We thank Hiro Ito for help with data, and the ADB for ªnancial support. We also thank Jeffrey Sachs, Wing Thye Woo, Louis Kuijs, Myoung-Jae Lee, and Arvind Subramanian for helpful comments and Gayoung Ko and Ji-Soo Kim for their excellent research assistance. Asian Economic Papers 11:1 © 2012 The Earth Institute at Columbia University and the Massachusetts Institute of Technology l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . 来宾来访 0 8 九月 2 0 2 3 When Fast-Growing Economies Slow Down cent per annum in the aggregate and close to that in per capita terms has trans- formed human welfare. Through the miracle of compound interest, it has raised in- comes and living standards by an order of magnitude in a generation.1 The implications extend from the individual to the systemic level. With large emerging markets expanding much faster than the advanced economies, the emerging world has accounted for the majority of the growth of global demand in recent years. The fast growth of emerging markets also means rapid shifts in the relative weight of different regions—East versus West, Asia versus Europe and the United States— something that has geopolitical implications that extend far beyond the narrowly deªned economic realm. That late-developing countries that put a suitable policy framework in place have the capacity to grow more rapidly than early developers is something that econo- mists have known since at least Alexander Gerschenkron.2 Rather than having to pi- oneer new technologies, late-developing countries can import knowhow from abroad. They can reap productivity gains simply by shifting workers from under- employment in agriculture to export-oriented manufacturing, where those imported technologies are utilized. With young generations that are presently engaged in sav- ing enjoying higher incomes than elderly dissavers, such countries are able to ªnance high levels of investment. 但, to invoke that well-known theorist Nelly Furtado, all good things come to an end.3 Periods of high growth in late-developing economies do not last forever. 甚至- tually the pool of underemployment in rural labor is drained. The share of employ- ment in manufacturing peaks, and growth comes to depend more heavily on the difªcult process of raising productivity in the service sector. A larger capital stock means more depreciation, requiring more saving to make this good. As the economy approaches the technological frontier, it must transition from relying on imported technology to indigenous innovation. Can we say exactly when fast growing economies slow down? Can we say anything about the country characteristics and circumstances on which the timing of the slowdown depends? These questions are the focus of this paper. 1 By a factor of 10 在 25 年. 2 Gerschenkron (1964) emphasized the role of an “ideology of growth” (what we refer to in the text as attaching a priority to successful economic development), state policy, and high investment rates as key ingredients in successful catch-up growth. 3 http://www.youtube.com/watch?v(西德:2)4pBo-GL9SRg. 43 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . 来宾来访 0 8 九月 2 0 2 3 When Fast-Growing Economies Slow Down The importance of the answers will be obvious. Signiªcant growth slowdowns in, 说, 中国, 印度, and Brazil would have a major impact on the global economy at a time when the world depends on these large emerging markets and their smaller brethren for incremental demand. There would be a disproportionate impact on markets for energy and raw materials, given the energy- and raw-material-intensity of economic growth in these economies. There could also be implications for social stability where political legitimacy rests on the success of governments in delivering rapid growth. Although the implications of our study are by no means limited to a particular country or countries, these issues have special resonance for China, for at least three reasons. 第一的, the country accounts for a substantial fraction of world population. 所以, the issue of when China slows down will have major implications for the welfare of a signiªcant share of humanity. 此外, the large and fast-growing Chinese economy is increasingly viewed as a key engine of growth for the world economy. The advanced industrial countries, the traditional engines of global growth, have inherited serious problems from the cri- 姐姐: weakened household balance sheets, increased public debts, and still troubled ªnancial systems. 相比之下, China experienced few problems as a result of the cri- 姐姐. There were few bank and enterprise failures. At the height of the crisis in 2009, growth “slowed” just to 9.2 百分. Both advanced and developing countries bene- ªted from China’s resilience. Robust Chinese demand lifted capital goods exports from Germany and Japan and commodity exports from Africa and Latin America. 尤其, demand from China contributed substantially to recovery in East and Southeast Asia, which has close trade linkages with China. l 从http下载 : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . 最后, although China recovered faster than expected from the global crisis, its pol- icymakers are grappling with how to sustain growth in the medium and long terms. The post-crisis external environment is likely to be less benign for a number of rea- 儿子们. The persistent sluggishness of growth in the advanced countries, which are among China’s key export markets, weakens a traditionally important source of demand. The collapse of exports and growth during the global crisis, especially the fourth quarter of 2008 and the ªrst quarter of 2009, highlights the risks of excessive dependence on external demand. This explains why rebalancing growth toward domestic sources of growth has become a priority for Chinese policymakers. And it is not yet clear whether structural adjustment in that direction will be compatible with the maintenance of customary rates of growth. 此外, China faces other medium term structural challenges, notably rapid population aging. 来宾来访 0 8 九月 2 0 2 3 44 Asian Economic Papers When Fast-Growing Economies Slow Down We know of only a few previous studies that address our central question of when fast-growing countries slow down. Probably the closest cousin to our analysis is Ben-David and Papell (1998). They examine a sample of 74 advanced and develop- ing countries spanning the period 1950–90 and look for statistically signiªcant breaks in time series for GDP growth rates. The vast majority of the break-points they identify are associated with decelerations in growth. They ªnd that these cluster in time. For the industrialized countries many of the structural breaks they identify are centered in the 1970s, whereas for developing countries (Latin Ameri- can countries in particular) many of the break points they identify occur in the 1980s. They do not, 然而, utilize criteria related to the magnitude of their growth slowdowns.4 Nor do they examine the income levels at which slowdowns occur or their determinants. There are also some more distant cousins. 普里切特 (2000) examines cases of devel- oping countries where, following a period of sustained growth, growth stagnates or collapses. His is a more restrictive deªnition of growth slowdowns than the one with which we are concerned in this paper. Pritchett is also more concerned with mounting a critique of the typical cross-country growth regression than with identi- fying the determinants of shifts from sustained growth to stagnation or collapse, as here. Reddy and Miniou (2006) similarly study episodes of real income stagnation, which they ªnd to be most prevalent in poor, conºict-ridden, and commodity- exporting countries. 再次, we are not concerned with episodes of stagnation, 如何- 曾经, but only with growth slowdowns. 最后, there are detailed studies of the de- terminants of growth collapses, such as Rodrik (1999), Ros (2005), and Hausmann, 罗德里格斯, and Wagner (2008). But growth collapses are even more radical than epi- sodes of stagnation from the slowdowns that we seek to understand here. The rest of our paper is organized as follows. 部分 2 explains how we identify growth slowdowns. 部分 3 describes the characteristics of the resulting sample. Sections 4 通过 6 take various approaches to identifying the correlates and deter- minants of these slowdowns. 部分 7 attempts to draw out the implications for China, and Section 8 concludes. 2. Identifying slowdowns Our analysis of growth slowdowns builds on a symmetrical analysis of growth ac- celerations by Hausmann, 普里切特, and Rodrik (2005). We identify an episode as a growth slowdown if the rate of GDP growth satisªes three conditions: 4 Very small but statistically signiªcant slowdowns qualify. 45 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . 来宾来访 0 8 九月 2 0 2 3 When Fast-Growing Economies Slow Down gt,t(西德:3)n ≤ 0.035, gt,t(西德:3)n (西德:3) gt,t(西德:4)n ≤ 0.02, (西德:5) 10,000, yt (1) (2) (3) where yt is per capita GDP in 2005 constant international purchasing power parity (PPP) 价格, and gt,t(西德:4)n and gt,t(西德:3)n are the average growth rate between year t and t(西德:4)n and the average growth rate between t(西德:3)n and t, 分别. Following Hausmann, 普里切特, and Rodrik (2005), we set n (西德:2) 7. Data on per capital incomes are from Penn World Tables (PWT) Version 6.3, which covers the period 1957–2007.5 Sources for the other variables are described in the Appendix. The ªrst condition requires that the 7-year average growth rate of per capita GDP is 3.5 percent or greater prior to the slowdown (earlier growth was fast). The second one identiªes a growth slowdown with a decline in the 7-year average growth rate of per capital GDP by at least by 2 百分点 (the slowdown is non- negligible). The third condition limits slowdowns to cases in which per capita GDP is greater than US$ 10,000 在 2005 constant international PPP prices (ruling out

growth crises in not yet successfully developing economies).

桌子 1 lists all the slowdowns identiªed by this approach. In some cases the meth-

odology identiªes a string of consecutive years as growth slowdowns. 例如,

in Greece all years between 1969 和 1978 are identiªed as a slowdown. One way of

dealing with this is to use a Chow test for structural breaks to select only one year

out of the consecutive years identiªed. For Greece we would then select 1973 作为

year of growth slowdown because the Chow test is most signiªcant for that year. 在

桌子 1, the years chosen by the Chow test are denoted in bold.

With this break point in hand, we next assign the value of 1 到 3 years centered

on the year of the growth slowdown, 那是, the dummy equals 1 for t (西德:2) t (西德:3) 1, t and

t (西德:4) 1 and zero otherwise.6 The comparison group consists of the countries that did

not experience a growth slowdown in that same year. The sample includes all coun-

tries for which the relevant data are available including countries that have never

experienced a growth slowdown. We drop all data pertaining to years t (西德:4) 2, . . .

t (西德:4) 7 of the growth slowdown as a way of removing the transition period to which

either a 0 或者 1 may not be clearly assigned.

5 下文中, we report some analysis using data for earlier periods as well.

6 再次, this directly follows Hausmann, 普里切特, and Rodrik (2005).

46

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

桌子 1. Growth slowdown episodes

Growth before slowdown

(t(西德:3)7 through t)

(%)

年

1970

1997

1998

1968

1969

1961

1974

1976

1977

1977

1973

1974

1976

1994

1995

1996

1997

1998

1964

1965

1970

1970

1971

1973

1974

1975

1973

1974

1976

1977

1978

1995

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1978

1988

1989

1990

1991

1992

1993

1994

1978

1979

1972

1973

1974

1975

1976

1979

1980

3.6

4.3

3.7

4.2

3.9

6.4

4.9

4.2

4.0

4.2

4.6

4.8

3.8

5.9

6.5

6.1

6.6

6.1

5.0

5.4

3.9

4.6

4.1

4.6

5.3

5.0

4.5

4.4

6.0

4.2

5.0

3.5

7.4

7.1

6.9

7.0

7.5

5.7

5.5

4.9

3.9

3.6

6.5

5.6

5.5

5.7

5.5

6.1

5.4

4.4

4.7

3.9

9.4

9.5

8.2

5.5

6.2

10.9

7.9

Growth after slowdown

(t through t(西德:4)7)

(%)

(西德:3) 1.5

(西德:3)0.1

(西德:3) 0.5

(西德:3) 1.7

(西德:3) 1.6

(西德:3) 3.5

(西德:3) 2.2

(西德:3) 2.1

(西德:3) 1.5

(西德:3)4.5

(西德:3) 2.5

(西德:3) 1.6

(西德:3) 1.1

(西德:3) 3.9

(西德:3) 2.8

(西德:3) 2.3

(西德:3) 2.3

(西德:3) 2.7

(西德:3) 2.9

(西德:3) 2.8

(西德:3) 1.9

(西德:3) 2.2

(西德:3) 2.0

(西德:3) 2.5

(西德:3) 1.8

(西德:3) 2.3

(西德:3) 2.2

(西德:3) 1.6

(西德:3)2.6

(西德:3)1.7

(西德:3)4.0

(西德:3)2.9

(西德:3) 4.9

(西德:3) 3.9

(西德:3) 3.6

(西德:3) 2.4

(西德:3) 1.3

(西德:3) 2.0

(西德:3) 1.1

(西德:3) 0.0

(西德:3) 0.1

(西德:3)0.3

(西德:3) 4.5

(西德:3) 3.2

(西德:3) 3.2

(西德:3) 3.0

(西德:3) 1.3

(西德:3) 0.9

(西德:3) 1.3

(西德:3) 0.7

(西德:3) 0.8

(西德:3) 1.3

(西德:3)4.7

(西德:3)11.3

(西德:3)11.6

(西德:3)7.3

(西德:3)8.4

(西德:3)6.6

(西德:3)3.5

Difference

in growth

(%)

(西德:3)2.2

(西德:3)4.5

(西德:3)3.2

(西德:3)2.5

(西德:3)2.3

(西德:3)3.0

(西德:3)2.7

(西德:3)2.1

(西德:3)2.5

(西德:3)8.7

(西德:3)2.1

(西德:3)3.2

(西德:3)2.7

(西德:3)2.0

(西德:3)3.7

(西德:3)3.8

(西德:3)4.3

(西德:3)3.4

(西德:3)2.1

(西德:3)2.6

(西德:3)2.0

(西德:3)2.4

(西德:3)2.1

(西德:3)2.1

(西德:3)3.5

(西德:3)2.7

(西德:3)2.3

(西德:3)2.8

(西德:3)8.6

(西德:3)5.8

(西德:3)8.9

(西德:3)6.4

(西德:3)2.5

(西德:3)3.2

(西德:3)3.3

(西德:3)4.5

(西德:3)6.2

(西德:3)3.7

(西德:3)4.4

(西德:3)4.9

(西德:3)3.8

(西德:3)3.9

(西德:3)2.0

(西德:3)2.4

(西德:3)2.4

(西德:3)2.6

(西德:3)4.2

(西德:3)5.1

(西德:3)4.1

(西德:3)3.6

(西德:3)3.9

(西德:3)2.6

(西德:3)14.0

(西德:3)20.8

(西德:3)19.8

(西德:3)12.8

(西德:3)14.6

(西德:3)17.5

(西德:3)11.5

Per capita

GDP at t

10,927

12,778

13,132

15,820

16,326

10,293

17,779

18,615

19,643

28,824

17,041

17,782

18,312

11,145

12,223

13,004

13,736

14,011

13,450

13,944

16,223

13,266

13,481

14,996

15,844

15,777

16,904

17,473

11,270

10,631

11,856

10,161

11,227

12,102

13,024

14,323

15,480

14,248

14,948

15,779

15,874

16,775

13,643

24,523

24,867

25,918

27,273

28,581

29,726

30,822

10,295

10,244

10,690

11,236

11,015

10,040

11,385

11,823

11,129

Asian Economic Papers

国家

阿根廷

澳大利亚

奥地利

Bahrain

比利时

智利

丹麦

芬兰

法国

Gabon

希腊

香港

匈牙利

伊朗

伊拉克

47

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

桌子 1. (Continued)

国家

爱尔兰

以色列

意大利

日本

韩国, Republic of

Kuwait

Lebanon

利比亚

Malaysia

Mauritius

荷兰

新西兰

Growth before slowdown

(t(西德:3)7 through t)

(%)

年

1969

1973

1974

1978

1979

1999

2000

1970

1971

1972

1973

1974

1975

1996

1974

1967

1968

1969

1970

1971

1972

1973

1974

1975

1990

1991

1992

1990

1991

1992

1993

1994

1995

1996

1997

1993

1994

1995

1996

1997

1983

1984

1985

1987

1977

1978

1979

1980

1994

1995

1996

1997

1992

1970

1973

1974

1960

1965

1966

4.4

5.1

4.6

3.8

3.5

7.4

8.3

4.7

5.0

5.5

6.9

7.6

5.5

3.7

4.4

8.7

8.7

9.2

9.5

8.4

8.8

8.4

6.5

5.0

4.2

4.3

3.7

8.6

8.7

8.4

7.9

7.7

7.3

7.2

5.8

6.7

6.3

6.7

4.2

8.5

9.3

6.3

6.2

6.3

5.8

6.4

7.1

5.2

6.7

6.8

6.9

6.5

5.3

4.5

3.7

3.5

3.9

4.2

4.6

Growth after slowdown

(t through t(西德:4)7)

(%)

(西德:3) 2.3

(西德:3) 2.3

(西德:3) 2.5

(西德:3) 0.4

(西德:3)0.3

(西德:3) 4.7

(西德:3) 4.0

(西德:3) 2.3

(西德:3) 1.6

(西德:3) 1.0

(西德:3)0.1

(西德:3) 0.1

(西德:3) 0.1

(西德:3)0.1

(西德:3) 2.3

(西德:3) 6.5

(西德:3) 5.0

(西德:3) 3.8

(西德:3) 2.9

(西德:3) 3.1

(西德:3) 2.8

(西德:3) 2.0

(西德:3) 2.8

(西德:3) 2.9

(西德:3) 1.2

(西德:3) 0.3

(西德:3) 0.2

(西德:3) 5.8

(西德:3) 2.6

(西德:3) 3.7

(西德:3) 4.0

(西德:3) 3.1

(西德:3) 2.9

(西德:3) 2.2

(西德:3) 2.5

(西德:3)2.8

(西德:3)3.0

(西德:3)3.8

(西德:3)1.3

(西德:3) 0.1

(西德:3)6.8

(西德:3)10.1

(西德:3)13.8

(西德:3)14.3

(西德:3)11.3

(西德:3)10.0

(西德:3)12.0

(西德:3)12.4

(西德:3) 3.4

(西德:3) 2.9

(西德:3) 2.4

(西德:3) 2.5

(西德:3) 3.3

(西德:3) 2.1

(西德:3) 1.7

(西德:3) 0.9

(西德:3) 1.7

(西德:3) 1.0

(西德:3) 1.3

Difference

in growth

(%)

(西德:3)2.2

(西德:3)2.8

(西德:3)2.0

(西德:3)3.4

(西德:3)3.8

(西德:3)2.8

(西德:3)4.3

(西德:3)2.5

(西德:3)3.4

(西德:3)4.5

(西德:3)7.0

(西德:3)7.6

(西德:3)5.5

(西德:3)3.8

(西德:3)2.1

(西德:3)2.2

(西德:3)3.7

(西德:3)5.3

(西德:3)6.6

(西德:3)5.3

(西德:3)6.0

(西德:3)6.4

(西德:3)3.7

(西德:3)2.1

(西德:3)3.1

(西德:3)4.0

(西德:3)3.5

(西德:3)2.8

(西德:3)6.1

(西德:3)4.7

(西德:3)3.9

(西德:3)4.5

(西德:3)4.5

(西德:3)5.0

(西德:3)3.2

(西德:3)9.5

(西德:3)9.3

(西德:3)10.5

(西德:3)5.5

(西德:3)8.5

(西德:3)16.1

(西德:3)16.4

(西德:3)20.0

(西德:3)20.7

(西德:3)17.1

(西德:3)16.4

(西德:3)19.1

(西德:3)17.5

(西德:3)3.3

(西德:3)4.0

(西德:3)4.5

(西德:3)4.0

(西德:3)2.0

(西德:3)2.4

(西德:3)2.0

(西德:3)2.7

(西德:3)2.2

(西德:3)3.2

(西德:3)3.2

Per capita

GDP at t

10,033

11,667

11,781

13,469

14,091

29,090

31,389

11,869

12,852

13,861

14,502

14,736

14,986

20,973

15,629

10,041

11,277

12,565

13,856

14,263

15,263

16,326

15,806

15,965

26,385

27,184

27,250

11,908

12,987

13,391

14,050

15,316

16,489

17,613

17,844

44,043

43,031

43,746

42,232

40,164

10,081

15,107

16,192

18,411

56,246

53,273

55,200

46,139

10,987

11,835

12,741

13,297

11,183

17,387

18,642

19,184

12,406

14,456

15,070

48

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

桌子 1. (Continued)

Growth before slowdown

(t(西德:3)7 through t)

(%)

年

1976

1997

1998

1977

1978

1979

1980

1981

1973

1974

1990

1991

1992

2000

1969

1970

1971

1972

1973

1988

1989

1990

1991

2000

1977

1978

1979

1978

1979

1980

1982

1983

1984

1993

1994

1995

1996

1997

1969

1972

1973

1974

1975

1976

1990

1994

1995

1996

1997

1998

1999

1978

1980

1977

1978

1979

1980

1988

1989

1968

4.3

4.0

4.1

5.2

8.7

8.5

8.2

6.6

8.2

7.3

4.4

5.4

5.4

3.6

5.7

5.8

5.5

5.3

4.3

4.7

5.8

5.0

5.1

4.1

9.4

5.5

3.7

6.9

6.4

5.8

6.4

6.8

6.7

6.7

7.0

6.7

6.3

6.2

6.1

5.2

5.3

5.6

4.7

3.8

3.8

6.2

6.0

5.8

5.9

5.6

5.4

4.6

3.6

22.6

20.8

21.4

16.1

3.7

3.7

3.9

Growth after slowdown

(t through t(西德:4)7)

(%)

(西德:3) 2.0

(西德:3) 1.6

(西德:3) 1.7

(西德:3) 2.6

(西德:3) 2.0

(西德:3) 2.3

(西德:3) 4.6

(西德:3) 3.9

(西德:3) 1.4

(西德:3) 1.6

(西德:3) 2.1

(西德:3) 2.5

(西德:3) 2.8

(西德:3) 0.4

(西德:3) 2.1

(西德:3) 2.0

(西德:3) 2.1

(西德:3) 1.4

(西德:3) 1.4

(西德:3) 2.2

(西德:3) 1.9

(西德:3) 2.4

(西德:3) 2.9

(西德:3) 0.1

(西德:3)8.8

(西德:3)8.3

(西德:3)9.7

(西德:3) 4.8

(西德:3) 3.6

(西德:3) 3.3

(西德:3) 4.2

(西德:3) 3.9

(西德:3) 4.0

(西德:3) 4.7

(西德:3) 2.5

(西德:3) 1.9

(西德:3) 0.9

(西德:3) 1.5

(西德:3) 3.8

(西德:3) 1.7

(西德:3) 0.9

(西德:3)0.1

(西德:3) 0.2

(西德:3) 0.0

(西德:3) 1.6

(西德:3) 3.8

(西德:3) 3.6

(西德:3) 3.3

(西德:3) 3.3

(西德:3) 3.3

(西德:3) 3.2

(西德:3)3.4

(西德:3)5.6

(西德:3)4.9

(西德:3)4.1

(西德:3)8.1

(西德:3)9.5

(西德:3) 1.2

(西德:3) 1.3

(西德:3) 1.4

Difference

in growth

(%)

(西德:3)2.3

(西德:3)2.4

(西德:3)2.4

(西德:3)2.6

(西德:3)6.7

(西德:3)6.2

(西德:3)3.6

(西德:3)2.7

(西德:3)6.7

(西德:3)5.7

(西德:3)2.3

(西德:3)2.9

(西德:3)2.6

(西德:3)3.2

(西德:3)3.6

(西德:3)3.8

(西德:3)3.4

(西德:3)3.9

(西德:3)2.9

(西德:3)2.5

(西德:3)4.0

(西德:3)2.6

(西德:3)2.3

(西德:3)4.0

(西德:3)18.2

(西德:3)13.8

(西德:3)13.4

(西德:3)2.1

(西德:3)2.8

(西德:3)2.5

(西德:3)2.2

(西德:3)2.9

(西德:3)2.7

(西德:3)2.0

(西德:3)4.5

(西德:3)4.9

(西德:3)5.4

(西德:3)4.7

(西德:3)2.3

(西德:3)3.5

(西德:3)4.3

(西德:3)5.7

(西德:3)4.6

(西德:3)3.8

(西德:3)2.1

(西德:3)2.4

(西德:3)2.4

(西德:3)2.5

(西德:3)2.7

(西德:3)2.3

(西德:3)2.2

(西德:3)8.1

(西德:3)9.3

(西德:3)27.6

(西德:3)24.9

(西德:3)29.6

(西德:3)25.5

(西德:3)2.4

(西德:3)2.4

(西德:3)2.5

Per capita

GDP at t

21,849

39,503

40,614

14,183

16,083

16,081

13,135

14,638

10,004

10,025

15,045

15,406

15,635

19,606

10,094

10,687

11,205

11,715

11,556

16,901

17,795

18,245

18,588

25,955

43,032

37,541

40,696

11,429

12,369

13,399

14,834

16,271

17,002

25,451

27,555

29,369

30,935

32,986

11,262

12,859

13,830

14,551

14,393

14,673

19,112

16,053

16,936

17,845

18,832

19,526

20,562

12,959

13,671

76,701

65,394

69,445

74,229

21,261

21,733

19,496

国家

Norway

Oman

Portugal

Puerto Rico

Saudi Arabia

新加坡

西班牙

台湾

Trinidad &

Tobago

United Arab

Emirates

英国

美国

49

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

桌子 1. (Continued)

国家

Uruguay

委内瑞拉

Average

年

1996

1997

1998

1974

来源: Authors’ calculation.

Growth before slowdown

(t(西德:3)7 through t)

(%)

3.6

4.3

4.4

3.9

5.6

Growth after slowdown

(t through t(西德:4)7)

(%)

(西德:3)2.0

(西德:3)1.2

(西德:3)1.2

(西德:3)2.2

(西德:3) 2.1

Difference

in growth

(%)

(西德:3)5.6

(西德:3)5.5

(西德:3)5.6

(西德:3)6.1

(西德:3)3.5

Per capita

GDP at t

11,044

11,559

12,097

13,869

16,740

笔记: The per capita GDP data are collected from Penn World Table 6.3. Shaded countries are oil exporters. When we identify a string

of consecutive years as growth slowdowns, we employ a Chow test for structural breaks to select only one year that is most signiªcant.

The selected years by the Chow test are denoted in bold.

In addition to focusing on the dates identiªed here, we also report the results when

we do not employ the Chow test and leave the consecutive years as they are,

即, the dummy indicating a slowdown is set equal to one for the entire run of

consecutive years (和, in addition to the observations for that country 1 year before

and after those selected years of the growth slowdown). In our regression analysis

we report the results both for the sample of all countries covered by PWT when the

manufacturing employment share is not used as an explanatory variable, 也

for a somewhat smaller sample when we employ the manufacturing share. 最后,

because oil-exporting countries exhibit volatile behavior and show growth slow-

downs at per capita incomes differently than other countries (see subsequent discus-

锡安), we also report the results when oil countries are removed. (表中 1, oil ex-

porters are shaded.) Throughout, we report robust standard errors that consider the

panel structure of the probit model.

3. What slowdowns look like

At the bottom of Table 1 we report the average values for all non-oil-exporting coun-

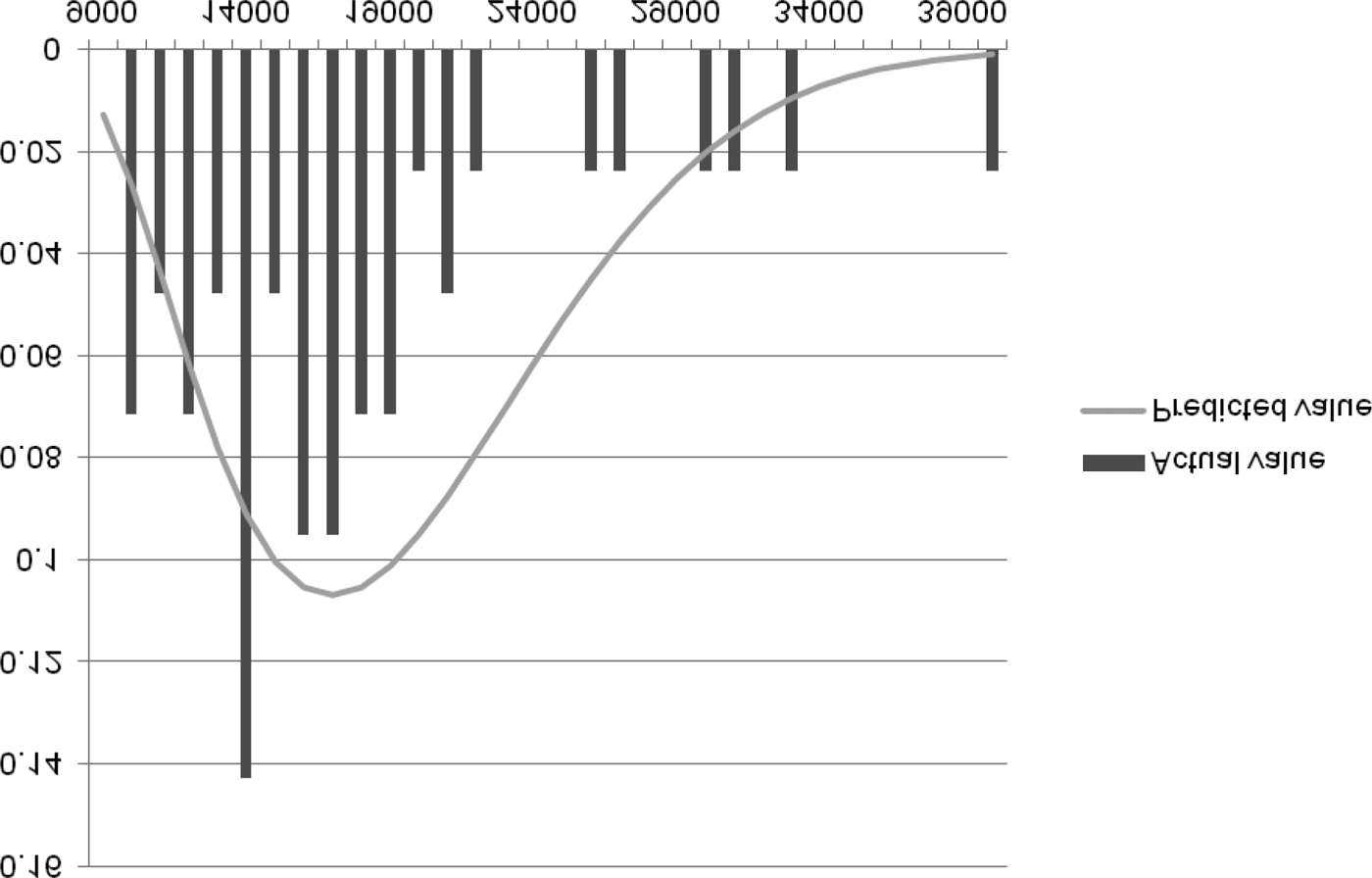

尝试. 平均而言, high growth came to an end at a per capita GDP of US$ 16,740, 在 2005 constant international PPP prices. (The median is US$ 15,058.) At that point the

growth rate slowed from 5.6 到 2.1 percent per annum. For purposes of comparison,

note that China’s per capita GDP, in constant 2005 international PPP prices, 曾是

美元$ 8,511 as of 2007, India’s was US$ 3,826, and Brazil’s was US$ 9,645. These are the latest compatible ªgures provided by Penn World Tables. Around the average of US$ 16,740 per capita GDP there is considerable variation.

数字 1 summarizes the frequency distribution by per capita income in the form of

a bar graph, oil exporters excluded.7 In some cases, explanations for these variations

7 On the exclusion of oil exporters see the subsequent discussion. The reader’s eyes will no

50

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

数字 1. Frequency distribution of growth slowdowns (oil exporters excluded)

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

来源: Authors’ calculation.

笔记: The bars indicate the frequency distribution of actual growth slowdowns by per capita income, and the smooth line is the predicted

values of growth slowdowns derived from a probit model.

are well known, although in others explaining them “will require further study.”

At this point we limit ourselves to a few observations.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

第一的, the list in Table 1 passes the smell test that most of the episodes are well

known and plausible. The methodology locates slowdowns for a number of

European countries in the ªrst half of the 1970s, when the quarter-century-long

“golden age” of rapid economic growth inaugurated by the Marshall Plan and

postwar recovery is widely seen as coming to a close (Crafts and Toniolo 1996). 它

detects a slowdown in Argentina in 1998, just prior to that country’s ªnancial

difªculties coming to a head (as discussed by De la Torre, Levy-Yeyati, and Schmuk-

勒 2002). The slowdown in Korea is centered in 1997, again on the eve of a ªnan-

cial crisis, although in this case we see a steady but signiªcant deceleration

over the course of preceding years (as described in Eichengreen, Perkins, 和

Shin [即将推出]).

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

doubt be drawn to the four high-income slowdowns in the ªgure. These are for Hong Kong,

新加坡, 日本, 和挪威, all of which are discussed further in what follows.

51

Asian Economic Papers

When Fast-Growing Economies Slow Down

A number of countries do not appear in this list, for good reason. Most of these, 喜欢

中国, continue to have per capita incomes below US$ 10,000 在 2005 international PPP prices and are therefore excluded by construction—the idea being that the kind of slower growth with which we are concerned should not simply be a conjectural phenomenon or a reºection of an inability to develop but rather should be associ- ated with increasing economic maturity.8 In practice, this condition does not appear to be especially restrictive. If we reduce the US$ 10,000 threshold to US$ 7,500, we do in fact pick up 15 additional cases, but most of these appear to be reºections of special circumstances that depressed growth relative to trend for an extended pe- riod rather than sustained slowdowns in increasingly mature economies. They in- clude Portugal’s slowdown around the time of its mid–1970s revolution, Romania when President Ceausescu put the economy through the wringer to repay the debt, Mexico’s slowdown at the end of the 1970s and beginning of the 1980s when its foreign-borrowing binge came to an end, and the slowdown in Cuban growth over the course of the 1980s as Soviet aid was curtailed. For what it is worth, the mean income at which slowdowns occur falls from US$ 16,740 to US$ 15,092 when we reduce the minimum-income threshold from US$ 10,000 to US$ 7,500.9 第二, in the majority of the countries experiencing slowdowns, this event is cen- tered at a single point in time and a particular level of per capita income. In a few exceptional cases, growth decelerates in steps. Japan is a well-known example: there is a ªrst slowdown in the early 1970s (our methodology centers this on year 1970 它- 自己, where the difference in the growth rate averages 6.6 percent per annum be- tween the seven preceding and subsequent years), and then a second slowdown in the 1990s (centered on 1992, where the deceleration is an additional 3.5 百分). 明显地, these magnitudes are exceptional; there is no other country where slow- down episodes produce a cumulative deceleration of 10 百分点 (there be- ing no other economy that both experienced such a dramatic economic miracle and then such a complete growth disaster). Qualitatively if not quantitatively, we see a similar pattern in Austria, which experienced a Wirtschaftswunder after World War II before decelerating ªrst in 1961 and then again in 1974, and in Spain, where there is evidence of a two-step deceleration centered around 1974 和 1990. Most other countries for which the methodology picks out more than one growth deceleration are cases where, after an extended period of slower growth, economic reforms lead to a period of faster growth followed by a second deceleration: 考试- ples include Argentina, 香港, 爱尔兰, 以色列, Norway, Portugal, and Singa- 8 Or at least adolescence. 9 The median falls from US$ 15,058 to US$ 13,859. 52 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . 来宾来访 0 8 九月 2 0 2 3 When Fast-Growing Economies Slow Down pore. In Norway the story is oil and natural gas, which led ªrst to a marked uptick in growth in the 1980s and 1990s, giving way subsequently to deceleration. 仍然, in the vast majority of cases it seems appropriate to speak of a speciªc point in time and a particular level of per capita income at which a country’s previously rapid rate of growth slowed down. A ªnal observation concerns outliers. Small open economies like Hong Kong and Singapore appear to experience their growth decelerations at unusually high levels of per capita GDP. It is tempting to also place Israel in this camp. It will be interest- ing to explore whether they are different because they are so small or because they are so open. Oil exporters also are unusual in that they are able to maintain high rates until higher per capita incomes are reached than is customary for other countries. A mo- ment’s reºection suggests that this is obvious: large amounts of oil that can be ex- tracted at low cost shift up the entire per capita income proªle, 其他条件相同. Note that this is not inconsistent with the well-known observation about the poten- tial negative impact on growth of resource abundance (“the resource curse”), 是- cause we focus here on the change in growth rates around the time of the slow- 向下, and not on their earlier absolute rate. All that we require for inclusion in the sample is that per capita income was growing by at least 3.5 percent per an- num over a period prior to the slowdown. But it clearly will be important to distin- guish oil exporters and treat them differently from other countries in the analysis that follows. 4. Proximate sources of slowdowns l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a s e p a r t i c e – 压力 / 的f / / / / / 1 1 1 4 2 1 6 8 3 1 9 5 a s e p _ a _ 0 0 1 1 8 压力 . A ªrst cut at the question of why slowdowns occur asks: which component of the standard growth-accounting framework—capital input, labor input, human capital input, or technical change—accounts for the bulk of the slowdown? To answer this question we use the standard growth-accounting framework, as implemented inter alia by Bernanke and Gurkaynak (2001), whose estimates of labor’s share of income we utilize here. We measure labor input as population between the ages of 15 和 64, from the World Bank’s World Development Indicators, and human capital data are from Barro and Lee (2010). 来宾来访 0 8 九月 2 0 2 3 表中 2 we report two sets of growth accounting results, the ªrst of which uses la- bor share calculated à la Bernanke and Gurkaynak (2001), whereas the second sim- ply sets labor’s share equal to 0.65 for each country. 表中 2.1 we see that the con- tribution of the growth of the capital stock fell from 2.40 百分比到 1.79 百分 53 Asian Economic Papers When Fast-Growing Economies Slow Down around the time of slowdowns. The contribution of labor growth fell more mod- estly, 从 0.89 to just 0.86 百分, whereas that of the growth of human capital ac- tually increased (从 0.44 到 0.51 百分). Much more dramatic is the decline in the contribution of total factor productivity (TFP) 生长, 从 3.04 到 0.09 百分. Growth slowdowns, in a nutshell, are productivity growth slowdowns.10 About 85 percent of the slowdown in the rate of growth of output is explained by the slow- down in the rate of TFP growth. The details in Table 2.2 are different but the story is the same.11 The intuition for this is straightforward. Slowdowns coincide with the point in the growth process where it is no longer possible to boost productivity by shifting addi- tional workers from agriculture to industry and where the gains from importing for- eign technology diminish. But the sharpness and extent of the fall in TFP growth from unusually high levels of 3-plus percent to near zero is striking. Next we consider the determinants of growth slowdowns using a probit model. 是- cause the share of employment in manufacturing is likely to be important for the timing of growth slowdowns, initially we limit the sample to observations for which we have this information. We regress our binary indicator of slowdowns identiªed using the Chow-test methodology on per capita GDP, the ratio of per capita GDP to that in the lead country, the dependency ratio, and the manufacturing share of em- ployment, all of which we enter as quadratics. In addition we include the crude fer- tility rate. In Tables 3.1 和 3.2 we report summary statistics for these variables for the full sample countries, for countries experiencing growth slowdowns, and for China, a country of special interest in this context. Tables 4.1 和 4.2 summarize the basic regressions. Per capita GDP is consistently the most important variable: both per capita GDP and its square are highly signiªcant.12 If we use the regression result in column (1), the peak probability of slowdown occurs when the per capita GDP reaches US$ 15,389

在 2005 international PPP prices, broadly in line with the simple statistics of Table 1.

The ratio measure of per capita income also enters as expected, in column (2). 这

10 The smaller contribution of capital accumulation may not be negligible, but it is dwarfed by

the decline in the contribution of TFP growth.

11 The analogous ªgures are 2.49 到 1.88 percent for capital, 0.91 到 0.86 percent for labor, 0.45

到 0.50 percent for human capital, 和 2.83 到 0.05 percent for TFP.

12 这里, and for that matter in virtually any speciªcation.

54

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

When Fast-Growing Economies Slow Down

0

0

0

.

.

5

5

0

(西德:3)

1

7

0

.

.

2

1

0

(西德:3)

7

4

0

(西德:3)

.

5

0

1

.

8

0

0

.

.

5

2

0

(西德:3)

8

0

0

(西德:3)

.

7

3

.

0

7

1

1

.

3

1

1

.

6

4

0

.

.

0

2

0

(西德:3)

4

1

0

(西德:3)

.

6

5

0

.

7

1

0

.

0

9

.

0

9

4

0

.

2

0

.

0

8

9

2

.

2

1

2

.

4

0

2

.

0

1

1

.

1

2

.

0

2

0

1

.

5

0

0

.

.

3

0

1

(西德:3)

6

9

0

(西德:3)

5

4

1

(西德:3)

.

.

5

0

0

.

.

2

0

0

(西德:3)

0

1

.

1

.

1

0

0

(西德:3)

2

6

2

.

3

2

2

.

5

5

2

.

4

8

.

1

3

6

.

1

7

1

.

3

1

2

3

.

6

0

2

.

2

2

.

4

9

3

.

4

8

7

.

3

1

0

4

.

8

1

3

.

0

1

.

2

0

1

.

2

9

5

.

1

3

1

.

2

1

7

.

2

1

4

2

.

5

4

.

2

7

3

2

.

1

0

6

.

4

6

5

.

8

3

5

.

2

3

5

.

7

6

5

.

3

8

.

3

5

5

.

3

8

9

.

2

2

1

.

2

4

0

.

2

0

6

.

0

2

6

.

0

2

1

.

1

8

3

.

0

5

3

.

0

5

3

.

0

5

5

.

0

3

5

.

0

1

5

.

0

1

3

.

0

2

3

.

0

3

3

.

0

4

3

.

0

6

3

.

0

2

3

.

0

4

3

.

0

8

3

.

0

3

8

.

0

1

8

.

0

7

7

.

0

5

6

.

0

3

5

.

0

1

5

.

0

0

5

.

0

2

2

.

0

7

2

.

0

8

2

.

0

8

2

.

0

8

2

.

0

6

3

.

0

3

4

.

0

0

5

.

0

7

5

.

0

4

6

.

0

4

3

.

0

9

3

.

0

3

2

.

0

8

6

.

0

5

5

.

0

7

4

.

0

8

3

.

0

4

4

.

0

4

5

.

0

7

4

.

0

2

4

.

0

7

3

.

0

3

3

.

0

2

3

.

0

2

2

.

0

3

2

.

0

0

3

.

0

3

6

.

0

7

6

.

0

3

7

.

0

6

7

.

0

9

7

.

0

4

5

.

0

5

5

.

0

3

4

.

0

(西德:3)

1

3

.

0

(西德:3)

4

1

.

0

(西德:3)

4

0

.

0

8

0

.

0

3

1

.

0

7

1

.

0

2

2

.

0

7

2

.

0

8

2

.

0

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

6

4

.

1

(西德:3)

5

3

.

1

(西德:3)

6

0

.

0

(西德:3)

7

4

.

0

(西德:3)

4

6

.

0

7

6

.

0

5

4

.

0

6

4

.

0

7

4

.

0

8

9

.

0

0

0

.

1

1

0

.

1

2

0

.

1

1

0

.

1

3

4

.

0

8

3

.

0

8

2

.

0

9

4

.

0

7

4

.

0

5

3

.

0

3

3

.

0

3

3

.

0

6

5

.

0

1

6

.

0

3

4

.

0

2

6

.

0

5

7

.

0

3

8

.

0

1

9

.

0

9

9

.

0

9

9

.

0

5

9

.

0

9

8

.

0

4

8

.

0

5

4

.

1

1

5

.

1

5

1

.

0

4

2

.

0

0

3

.

0

4

2

.

0

7

2

.

0

7

3

.

0

8

9

.

0

4

9

.

0

2

9

.

0

1

9

.

0

1

9

.

0

8

4

.

0

4

5

.

0

4

4

.

0

3

4

.

0

2

4

.

0

2

4

.

0

3

6

.

0

3

6

.

0

2

2

.

0

2

1

.

0

9

0

.

0

1

1

.

0

2

1

.

0

0

1

.

0

5

2

.

0

3

4

.

0

2

6

.

0

5

7

.

0

1

4

.

1

9

2

.

1

5

9

.

1

5

3

.

1

4

1

.

1

9

9

.

0

8

9

.

0

5

8

.

0

5

6

.

0

9

8

.

2

1

6

.

2

8

3

.

2

8

1

.

2

2

1

.

2

9

6

.

1

2

6

.

1

4

2

.

1

7

4

.

1

9

2

.

1

4

1

.

1

9

9

.

0

8

8

.

0

9

0

.

1

5

9

.

0

6

8

.

1

8

6

.

1

9

4

.

1

5

2

.

1

9

9

.

0

6

8

.

0

3

7

.

0

8

5

.

0

7

4

.

0

7

3

.

0

6

6

.

1

1

7

.

1

2

9

.

1

7

9

.

1

5

8

.

1

9

7

.

1

0

2

.

1

1

2

.

1

3

1

.

1

3

9

.

1

5

3

.

2

3

6

.

2

0

9

.

2

3

1

.

3

0

5

.

1

0

7

.

1

6

7

.

1

0

6

.

1

3

6

.

1

6

5

.

1

4

6

.

1

0

7

.

1

4

7

.

1

2

7

.

1

4

1

.

2

5

1

.

2

0

1

.

2

7

0

.

2

4

1

.

2

9

0

.

2

0

0

.

2

6

8

.

1

8

6

.

1

9

4

.

1

8

6

9

1

9

6

9

1

1

6

9

1

4

7

9

1

6

7

9

1

7

7

9

1

3

7

9

1

4

7

9

1

6

7

9

1

4

9

9

1

5

9

9

1

6

9

9

1

7

9

9

1

8

9

9

1

4

6

9

1

5

6

9

1

0

7

9

1

0

7

9

1

1

7

9

1

3

7

9

1

4

7

9

1

5

7

9

1

3

7

9

1

4

7

9

1

9

6

9

1

0

7

9

1

1

7

9

1

2

7

9

1

3

7

9

1

4

7

9

1

5

7

9

1

6

7

9

1

7

7

9

1

8

7

9

1

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

r

e

t

F

A

r

哦

乙

A

L

e

r

哦

F

e

乙

我

A

t

我

p

A

C

n

A

米

你

H

r

e

t

F

A

e

r

哦

F

e

乙

r

e

t

F

A

r

哦

乙

A

L

e

r

哦

F

e

乙

r

e

t

F

A

我

A

t

我

p

A

C

e

r

哦

F

e

乙

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

r

A

e

是

y

r

t

n

你

哦

C

A

我

我

A

r

t

s

你

A

A

我

r

t

s

你

A

米

你

我

G

我

e

乙

e

我

我

H

C

k

r

A

米

n

e

D

d

n

A

我

n

我

F

e

C

n

A

r

F

e

C

e

e

r

G

d

e

s

你

e

r

A

s

e

r

A

H

s

r

哦

乙

A

我

我

A

你

t

C

A

n

e

H

w

)

%

(

G

n

我

t

n

你

哦

C

C

A

H

t

w

哦

r

G

.

1

.

2

e

我

乙

A

时间

s

t

我

你

s

e

r

G

n

我

t

n

你

哦

C

C

A

H

t

w

哦

r

G

.

2

e

我

乙

A

时间

55

Asian Economic Papers

When Fast-Growing Economies Slow Down

0

8

0

.

0

4

0

.

1

5

0

.

2

4

0

.

.

6

2

1

(西德:3)

2

4

1

(西德:3)

1

0

1

(西德:3)

4

4

1

(西德:3)

.

.

.

3

5

0

.

5

4

0

.

0

7

0

.

.

1

4

1

(西德:3)

2

9

1

(西德:3)

.

1

5

2

.

6

0

.

2

6

3

0

.

.

6

0

0

(西德:3)

7

4

0

(西德:3)

2

3

1

(西德:3)

3

9

0

(西德:3)

1

8

0

(西德:3)

7

1

1

(西德:3)

.

.

.

.

.

2

7

0

.

8

3

2

.

5

1

1

.

6

2

0

.

2

3

0

.

.

8

2

0

(西德:3)

0

2

0

.

.

8

2

0

(西德:3)

3

6

0

.

1

8

0

.

.

4

2

0

(西德:3)

7

8

0

(西德:3)

6

8

0

(西德:3)

.

.

4

2

0

.

1

4

1

.

.

9

1

1

(西德:3)

7

4

2

.

1

3

.

2

0

4

.

2

4

5

.

2

3

4

.

2

1

0

3

.

7

4

2

.

0

5

.

1

8

0

.

3

1

4

.

3

8

7

.

2

6

9

.

1

2

6

.

1

8

0

.

5

8

7

5

.

3

0

.

3

7

1

.

3

3

6

3

.

9

8

.

4

7

4

.

5

2

3

.

3

1

1

2

.

0

9

2

.

8

9

.

3

3

1

.

4

0

7

.

4

8

0

5

.

9

0

4

.

9

4

4

.

2

1

4

.

8

3

.

2

5

1

.

1

5

1

.

2

7

1

.

2

4

5

.

1

1

8

3

.

4

7

3

.

1

4

.

3

2

6

.

0

8

2

.

0

1

2

.

0

4

1

.

0

3

1

.

0

2

1

.

0

1

1

.

0

4

1

.

0

5

5

.

0

1

6

.

0

2

6

.

0

4

6

.

0

1

6

.

0

4

4

.

0

1

4

.

0

8

6

.

0

9

6

.

0

0

7

.

0

0

7

.

0

7

6

.

0

4

6

.

0

3

3

.

0

6

4

.

0

2

5

.

0

2

6

.

0

8

6

.

0

4

7

.

0

9

6

.

0

4

6

.

0

9

5

.

0

6

5

.

0

2

5

.

0

8

3

.

0

8

3

.

0

8

3

.

0

0

7

.

0

5

6

.

0

0

6

.

0

5

5

.

0

9

5

.

0

9

5

.

0

9

5

.

0

4

5

.

0

8

4

.

0

1

4

.

0

4

3

.

0

9

1

.

0

3

3

.

0

0

4

.

0

2

6

.

0

1

6

.

0

1

6

.

0

2

6

.

0

2

4

.

0

7

4

.

0

2

5

.

0

5

5

.

0

7

5

.

0

0

6

.

0

4

3

.

0

5

3

.

0

9

0

.

0

0

1

.

0

0

1

.

0

0

1

.

0

1

2

.

0

2

3

.

0

2

4

.

0

2

5

.

0

2

6

.

0

5

4

.

0

2

4

.

0

0

4

.

0

3

7

.

0

3

7

.

0

3

7

.

0

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

4

5

.

1

6

9

.

0

3

1

.

1

3

2

.

1

1

2

.

1

8

1

.

1

2

1

.

1

1

0

.

1

7

0

.

1

4

2

.

1

2

2

.

1

6

9

.

0

9

7

.

0

3

1

.

1

5

0

.

1

2

6

.

1

7

4

.

1

6

3

.

1

8

2

.

1

1

2

.

1

0

2

.

1

6

7

.

1

5

4

.

0

6

7

.

0

2

7

.

0

8

6

.

0

5

6

.

0

2

6

.

0

9

5

.

0

7

5

.

0

5

5

.

0

4

5

.

0

0

1

.

0

4

0

.

0

2

0

.

0

(西德:3)

0

9

.

0

2

8

.

0

4

7

.

0

5

0

.

2

2

8

.

0

3

7

.

0

5

6

.

0

6

6

.

0

8

6

.

0

3

7

.

0

2

8

.

0

6

3

.

0

7

6

.

0

9

7

.

0

2

2

.

1

7

2

.

1

4

2

.

1

6

2

.

1

5

0

.

2

6

9

.

1

2

9

.

1

4

9

.

1

4

9

.

1

8

8

.

1

5

6

.

2

4

2

.

0

6

3

.

1

8

2

.

1

8

1

.

1

6

0

.

1

5

9

.

0

6

8

.

0

1

8

.

0

6

7

.

0

2

7

.

0

3

6

.

0

9

5

.

0

3

5

.

0

8

3

.

1

4

3

.

1

1

3

.

1

5

7

.

3

5

9

.

2

3

0

.

3

4

1

.

3

7

0

.

3

4

8

.

2

2

7

.

2

6

4

.

2

1

5

.

1

5

4

.

1

9

3

.

1

6

1

.

1

5

9

.

0

5

7

.

1

7

6

.

1

6

2

.

2

0

0

.

2

5

7

.

1

6

4

.

1

1

2

.

1

3

0

.

1

1

3

.

1

0

0

.

1

8

0

.

4

6

7

.

3

1

4

.

3

1

0

.

3

2

7

.

2

7

4

.

2

8

1

.

2

0

0

.

2

8

8

.

1

1

2

.

1

6

0

.

1

2

9

.

0

2

7

.

3

2

2

.

3

3

9

.

2

8

4

.

3

0

0

.

3

1

8

.

2

7

7

.

2

6

7

.

2

4

8

.

2

5

8

.

2

0

9

.

2

6

2

.

1

8

5

.

1

7

6

.

1

3

5

.

1

6

5

.

1

6

2

.

1

1

5

.

1

1

9

.

1

5

9

.

1

5

0

.

2

5

2

.

2

9

4

.

2

7

5

.

2

6

9

.

1

3

6

.

1

2

2

.

4

8

1

.

4

2

2

.

4

1

3

.

4

6

2

.

4

8

2

.

4

7

2

.

4

8

0

.

4

6

7

.

3

1

5

.

1

0

6

.

1

2

6

.

1

2

7

.

3

8

8

.

3

8

9

.

3

8

7

9

1

8

8

9

1

9

8

9

1

0

9

9

1

1

9

9

1

2

9

9

1

3

9

9

1

4

9

9

1

9

6

9

1

3

7

9

1

4

7

9

1

8

7

9

1

9

7

9

1

9

9

9

1

0

0

0

2

0

7

9

1

1

7

9

1

2

7

9

1

3

7

9

1

4

7

9

1

5

7

9

1

6

9

9

1

4

7

9

1

7

6

9

1

8

6

9

1

9

6

9

1

0

7

9

1

1

7

9

1

2

7

9

1

3

7

9

1

4

7

9

1

5

7

9

1

0

9

9

1

1

9

9

1

2

9

9

1

0

9

9

1

1

9

9

1

2

9

9

1

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

1

1

4

2

1

6

8

3

1

9

5

A

s

e

p

_

A

_

0

0

1

1

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

8

S

e

p

e

米

乙

e

r

2

0

2

3

r

e

t

F

A

r

哦

乙

A

L

e

r

哦

F

e

乙

我

A

t

我

p

A

C

n

A

米

你

H

r

e

t

F

A

e

r

哦

F

e

乙

r

e

t

F

A

r

哦

乙

A

L

e

r

哦

F

e

乙

r

e

t

F

A

我

A

t

我

p

A

C

e

r

哦

F

e

乙

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

n

w

哦

d

w

哦

我

s

r

A

e

是

G

n

哦

K

G

n

哦

H

y

r

t

n

你

哦

C

d

n

A

我

e

r

我

我

e

A

r

s

我

y

我

A

t

我

n

A

p

A

J

Asian Economic Papers

F

哦

C

我

我

乙

你

p

e

右

,

A

e

r

哦

K

)

d

e

你

n

我

t

n

哦

C

(

.

1

.

2

e

我

乙

A

时间

56

When Fast-Growing Economies Slow Down

7

8

0

.

8

3

0

.

5

4

0

.

9

0

0

.

2

6

.

0

7

6

0

.

6

5

0

.

8

4

0

.

2

0

.

1

9

2

.

1

5

2

.

0

.

3

0

0

(西德:3)

6

7

0

(西德:3)

.

0

5

0

.

.

9

4

0

(西德:3)

4

1

0

(西德:3)

.

3

2

0

.

2

0

0

.

1

0

0

.

.

1

4

0

(西德:3)

0

2

0

(西德:3)

.

5

4

0

.

3

8

0

.

3

1

1

.

.

5

7

0

(西德:3)

2

4

0

.

.

5

6

0

(西德:3)

5

6

0

(西德:3)

.

0

8

0

.

0

0

1

.

6

4

.

1

6

0

.

2

.

2

0

0

(西德:3)

7

4

0

(西德:3)

8

9

0

(西德:3)

0

1

0

(西德:3)

.

.

.

4

9

0

.

.

9

6

0

(西德:3)

9

2

1

(西德:3)

7

9

1

(西德:3)

2

5

1

(西德:3)

5

5

1

(西德:3)

9

9

0

(西德:3)

.

.

.

.

.

3

9

2

.

6

7

2

.

0

5

2

.

8

4

2

.

1

4

.

1

0

3

3

.

3

0

3

.

3

8

2

.

4

3

.

2

2

4

.

2

3

8

.