The Review of Economics and Statistics

VOL. CV

MARCH 2023

NUMBER 2

THE TWO-MARGIN PROBLEM IN INSURANCE MARKETS

Michael Geruso, Timothy J. Layton, Grace McCormack, and Mark Shepard*

Abstract—Insurance markets often feature consumer sorting along both an

extensive margin (whether to buy) and an intensive margin (which plan

to buy). We present a new graphical theoretical framework that extends a

workhorse model to incorporate both selection margins simultaneously. A

key insight from our framework is that policies aimed at addressing one

margin of selection often involve an economically meaningful trade-off on

the other margin in terms of prices, enrollment, and welfare. 使用数据

from Massachusetts, we illustrate these trade-offs in an empirical sufficient

statistics approach that is tightly linked to the graphical framework we

发展.

我.

介绍

SOME of the most important problems in health insurance

markets stem from adverse selection, or the tendency of

sicker consumers to exhibit higher demand for insurance.

Concerns about adverse selection have motivated a variety

of regulatory interventions in the United States and around

the rest of world, including insurance mandates, penalties for

being uninsured, subsidies for purchasing insurance, risk ad-

justment transfers, benefit regulation, and reinsurance. 政策

discussions about how to address adverse selection have be-

come salient in the United States as many public programs

have shifted toward providing health insurance via regulated

市场 (Gruber, 2017).

But a deeper look reveals that not all policies combating

adverse selection are targeted at the same problem. 上

Received for publication June 8, 2020. Revision accepted for publication

二月 19, 2021. Editor: Benjamin R. Handel.

∗Geruso: University of Texas at Austin and NBER; Layton: 哈佛大学-

versity and NBER; McCormack: 哈佛大学; Shepard: 哈佛

University and NBER.

We thank Sebastian Fleitas, Bentley MacLeod, Maria Polyakova, 和

Ashley Swanson for serving as discussants for this paper. We also thank

Kate Bundorf, Marika Cabral, Amitabh Chandra, Vilsa Curto, Leemore

Dafny, Keith Ericson, Amy Finkelstein, Jon Gruber, Tom McGuire, Neale

Mahoney, Joe Newhouse, Evan Saltzman, Brad Shapiro, and Pietro Tebaldi;

participants at NBER Health Care, NBER Insurance Working Group,

CEPRA/NBER Workshop on Aging and Health, 这 2019 Becker Friedman

Institute Health Economics Initiative Annual Conference at the University

of Chicago, 这 2019 American Economic Association meetings, 这 2018

American Society of Health Economists meeting, 这 2018 Annual Health

Economics Conference, 这 2018 Chicago Booth Junior Health Economics

Summit; and seminars at the Brookings Institution and the University of

Wisconsin for useful feedback. We gratefully acknowledge financial sup-

port for this project from the Laura and John Arnold Foundation, the Eunice

Kennedy Shriver National Institute of Child Health and Human Develop-

ment Center grant P2CHD042849 awarded to the Population Research Cen-

ter at UT-Austin, the Agency for Healthcare Research and Quality (K01-

HS25786-01), and the National Institute on Aging, grant T32-AG000186.

No party had the right to review this paper prior to its circulation.

A supplemental appendix is available online at https://doi.org/10.1162/

rest_a_01070.

一只手, policies such as mandates and subsidies combat

selection on the extensive margin (or “against the market”).

This type of selection is characterized by sicker people be-

ing more likely to buy insurance. It leads to higher insurer

costs and higher consumer prices and causes some healthy

people to opt out. Policies such as risk adjustment and ben-

efit regulation, 另一方面, combat selection on the

intensive margin (or “within the market”). This type of se-

lection is characterized by sicker people being more likely

to purchase more generous plans within the market. Inten-

sive margin selection drives up the price of generous plans

relative to skimpy ones and results in too many consumers

choosing skimpy plans. 在某些情况下, selection within the

market may be so strong that generous contracts cannot be

sustained, and the market for them unravels entirely (卡特勒

& Reber, 1998).

Prior work has recognized these two problems and has

studied policies targeted at each. 然而, this literature has

largely considered these two forms of selection in isolation—

either assuming all consumers buy insurance and focusing on

the intensive margin (Handel, Hendel, & Whinston, 2015) 或者

assuming all contracts within the market are identical and

focusing on the extensive margin (Hackmann, Kolstad, &

Kowalski, 2015). By ignoring one margin or the other, 这

selection problem is usefully simplified. In empirical work,

it becomes amenable to a sufficient statistics approach based

on demand and cost curves defined in reference to a single

price—either the price of insurance or the price difference be-

tween a generous versus a skimpy plan (Einav, Finkelstein,

& Cullen, 2010). 然而, this simplification does not al-

low for potential interactions between these two margins of

选择.

在本文中, we generalize the canonical insurance mar-

ket framework to address both margins simultaneously. 这

benefit of doing so is not merely a technical curiosity. 它有

first-order policy importance in settings like the ACA mar-

ketplaces where both the generosity of coverage and rates of

uninsurance are serious concerns. To see why, consider an

insurance mandate—a policy that aims to correct extensive

margin selection by bringing healthy marginal consumers

into the market. Our framework shows how a mandate that

succeeds in increasing rates of insurance coverage will likely

worsen selection on the intensive margin. 直观地, 这

mandate brings more healthy and low-cost consumers into

the market. Because these new consumers tend to select the

The Review of Economics and Statistics, 行进 2023, 105(2): 237–257

© 2021 The President and Fellows of Harvard College and the Massachusetts Institute of Technology

https://doi.org/10.1162/rest_a_01070

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

238

THE REVIEW OF ECONOMICS AND STATISTICS

lower-price (and lower-quality) 计划, the risk pools of those

plans will get even healthier. In equilibrium, these plans will

further reduce prices, siphoning additional consumers away

from higher-quality plans on the intensive margin, causing

prices for high-quality coverage to spiral upward. These two

offsetting effects (improving take-up and inducing within-

market unraveling) represent a clear example of the inten-

sive/extensive margin interactions that are the focus of our

paper.1

One of our main contributions is to provide a graphical

demand-cost framework that lets economists visualize (和

teach) the two-margin selection problem in a transparent way.

这样做, we build on the influential work of Einav et al.

(2010) and Einav and Finkelstein (2011), who show how to

visualize selection markets in terms of demand, average cost,

and marginal cost curves. We generalize their model to allow

for two plans—a more generous H plan and a less generous

L plan—plus an outside option of uninsurance (U ). 虽然

stylized, our vertical model captures the core intuition of the

two selection margins: an intensive margin difference in gen-

erosity (H versus L) and an extensive margin option to exit

the market (by choosing U ). It also captures the key feature

of adverse selection: that higher-risk consumers have greater

willingness to pay for generous coverage—both for H relative

to L, and for L relative to U . Our vertical model is the sim-

plest framework that captures these features and is useful for

developing intuition around a potentially multidimensional

problem by allowing the market to be represented in stan-

dard two-dimensional graphs with familiar demand and cost

curves. Equilibrium prices, market shares, and social surplus

can all be easily visualized. We also show the extent to which

the core intuitions hold as various assumptions on the model

are relaxed, 包括, 例如, allowing for horizontal

differentiation across plans.

As in Einav et al. (2010), there is a tight link between

our model and the estimation of sufficient statistics used to

characterize equilibrium and welfare. Econometric identifi-

cation is analogous, though exogenous price variation along

two margins is required—for example, independent variation

in the price of a skimpy plan and in the price of a generous

plan.2

After developing the graphical framework, we use it to

show how policies and regulatory actions that counteract

selection on one margin can interact with the other. The rel-

evance of these cross-margin interactions is the key concep-

tual message of our paper. We show that a mandate’s im-

pact on plan generosity is, 实际上, an instance of a broader

phenomenon that encapsulates many relevant policy inter-

ventions currently in place in insurance markets. These in-

1Recent theoretical insights from Azevedo and Gottlieb (2017) and em-

pirical findings from Saltzman (2021) indicate that this is an important

omission in contexts like the ACA marketplaces. We similarly find that

these interactions are first-order for plan choices and welfare.

2Or alternatively, variation in a market-wide subsidy for selecting any

plan and independent variation in the price difference between bare bones

and generous plans.

clude plan benefits requirements, network adequacy rules,

risk adjustment, reinsurance, subsidies, and behavioral in-

terventions like plan choice architectures or autoenrollment.

Each involves a potential trade-off: Policies that aim to ad-

dress intensive margin selection tend to worsen extensive

margin selection, and vice versa.

The graphical model helps show why these cross-margin

interactions occur. The key insight is that for each plan, 不-

ther its demand or average cost curve is not a price-invariant

model primitive (as is true in a two-option model) but an

equilibrium object that depends on the other plan’s price.

Policies that target one selection margin typically influence

market prices (例如, the mandate lowers PL relative to PH ),

which in turn shifts demand or cost curves that determine the

other margin (例如, the lower PL reduces demand for H). 这

cross-plan dependence of demand and average costs is the

key missing piece when the two margins are analyzed sepa-

率地. We show how the geometry of the demand and cost

curves generates this dependence. We also develop a more

general nongraphical version of our model that allows for

horizontal differentiation and use it to show that many of the

key intuitions will hold with a modest amount of horizon-

tal differentiation (IE。, consumers on the margin between H

and U ).

With the intuition and price theory in place, we analyze

the model’s insights empirically using demand and cost es-

timates from the Massachusetts Commonwealth Care pro-

公克, a subsidized insurance exchange that was a precursor to

the ACA health insurance marketplace. We draw on demand

and cost estimates from Finkelstein et al. (2019) to simulate

equilibrium in counterfactuals where we vary benefit design

规则, mandate penalties, and risk adjustment strength.3 Be-

yond demonstrating how our framework can be used, 这

empirical exercise generates several policy insights. The size

of the unintended cross-margin effects can be quite large. 我们

find that a strong mandate sufficient to move all consumers

into insurance—increasing enrollment by around 25 百分-

age points—can reduce the market share of generous plans by

多于 15 百分点, 或者 35% of baseline market

分享. In the other direction, strengthening risk-adjustment

transfers until the market “upravels” to include only gener-

ous coverage can substantially reduce market-level consumer

participation—in our setting, by as much as 15 percentage

points or 60% of the baseline uninsurance rate. With the ad-

ditional assumption that consumer choices reveal plan valu-

ations, we find that the cross-margin welfare impacts can be

similarly large (and often first order).

更远, we show that in some settings, cross-margin in-

teractions are critical for determining optimal policy. 什么时候

intensive margin policies (such as risk adjustment) are weak,

it can be optimal to also have weak extensive margin policies

3Finkelstein et al. (2019) use a regression discountinuity design to doc-

ument significant adverse selection both into the market and within the

market between a narrow-network, lower-quality option and a set of wider-

网络, higher-quality plans.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

THE TWO-MARGIN PROBLEM IN INSURANCE MARKETS

239

(such as an uninsurance penalty). But when intensive mar-

gin policies are strong, it can be optimal to also have strong

extensive margin policies. These results show that in these

市场, regulators are operating in a world of the second-

best and must consider interactions between the two margins

of selection in order to determine constrained optimal policy.

This is true whether optimality is viewed from a formal so-

cial surplus perspective or reflects a political preference over

rates of insurance coverage on the one hand and insurance

quality on the other. While we stop short of prescribing the

optimal policy in a given market, our results indicate that

when extensive margin policies become stronger, 密集的

margin policies should often strengthen (and vice versa).

Our paper contributes to a growing literature on adverse

selection in health insurance markets. Our main contribution

is to provide a graphical model that unites two key strands

of this literature. The first strand focuses on extensive mar-

gin selection and stems from the seminal work of Akerlof

(1970).4 The second strand focuses on intensive margin se-

lection, studying either consumer sorting across a fixed set

of contracts within a market5 or how consumer selection is

endogenously reflected in the characteristics of the contracts

offered.6

The most directly connected work is a prior theoretical

contribution by Azevedo and Gottlieb (2017) that points out

the potential cross-margin effects of a mandate in a setting

with vertically differentiated contracts that differ in their

coinsurance rates. Our framework maintains the vertical as-

sumption of Azevedo and Gottlieb (2017) while allowing

differentiation to be more flexible (IE。, based on factors

other than cost sharing) in a two-contract setting. 类似于

Azevedo and Gottlieb (2017), our paper also takes a step to-

ward bridging the gap between the Akerlof (1970) and Einav

等人. (2010) fixed-contracts approach and the Rothschild and

斯蒂格利茨 (1976) endogenous-contracts approach to modeling

adverse selection in insurance markets by allowing some con-

tracts to death-spiral out of existence in equilibrium while

others remain available. This possibility that policies can af-

fect which contracts are ultimately offered in equilibrium is

a key feature of our model that was originally highlighted by

Rothschild and Stiglitz (1976) but is generally overlooked by

the Einav et al. (2010) workhorse model. 最后, Saltzman

(2021) provides a complementary analysis (concurrent with

ours) that investigates cross-margin effects using a structural

model estimated with ACA data from California.

Our insights about cross-margin interactions are relevant

for active policy debates in the ACA and other insurance set-

tings. 例如, within the last 5 年, 联邦政府-

4Recent theoretical advances in this strand include Hendren (2013) 和

Mahoney and Weyl (2017) and empirical applications by Bundorf, 莱文,

and Mahoney (2012), Hackmann et al. (2015), Tebaldi (2017), 和别的.

5看, 例如, Handel et al. (2015); Shepard (2022).

6看, 例如, Glazer and McGuire (2000); Veiga and Weyl (2016); 凯里

(2017); Lavetti and Simon (2018); and Geruso, Layton, and Prinz (2019).

Geruso and Layton (2017) provide an overview comparing the fixed- 和

endogenous-contracts approaches to modeling intensive margin selection.

ernment has gone back-and-forth with respect to the level

of flexibility it provides to states to weaken ACA Essential

Health Benefits or risk adjustment transfers (intensive margin

政策). The stated goal of more flexibility has been to lower

plan prices and reduce uninsurance, and the stated goal of less

flexibility has been to increase the quality of ACA insurance

计划 (cross-margin effects). 然而, state efforts to sim-

plify enrollment (Domurat, Menashe, & Yin, 2021) or enact

mandate penalties (all extensive margin policies) may cre-

ate unintended consequences on the intensive margin. 更多的

宽广地, our model is also relevant to other settings with two

selection margins, including the Medicare program (with its

Medicare Advantage option), employer programs with a plan

choice decision and a participation decision (例如, CalPERS),

national health insurance systems with an opt-out (例如, 格尔-

许多), and other selection markets (outside health insurance)

with both an extensive and intensive margin choice.

The rest of the paper is organized as follows. Section II

presents the graphical vertical model. Section III applies the

model to show two-margin impacts of various policies. 秒-

tions IV to VI apply the model with simulations: section IV

discusses methods; section V shows price and enrollment

结果; and section VI shows welfare results. Section VII

concludes.

二. 模型

在这个部分, we develop a theoretical and graphical

model that depicts insurance market equilibrium and wel-

fare in the spirit of Einav et al. (2010, hereafter EFC), 尽管

allowing for the possibility that interventions affecting se-

lection on one margin may affect selection on another. 这

requires an insurance plan choice set with at least three op-

系统蒸发散. Consider two fixed contracts, j = {H, L}, where H is

more generous than L on some metric, and an outside op-

的, U . In the focal application of our model to the ACA’s

individual markets, U represents uninsurance.

Each plan j ∈ {H, L} sets a single community-rated price

Pj that (along with any risk adjustment transfers; 见下文)

must cover its costs. Consumers make choices based on these

prices and on the price of the outside option, PU = M.7 In our

focal example, M is a mandate penalty. The distinguishing

feature ofU is that its price is exogenously determined; it does

not adjust based on the consumers who select into it. 这是

natural for the case where U is uninsurance or a public plan

like Traditional Medicare.8 P = {PH , PL, PU } is the vector of

prices in the market.

In the most general formulation, demand in this market

cannot be easily depicted in two-dimensional figures. 到

make the cross-margin effects of interest clearer, we impose

a vertical model of demand, which assumes contracts are

identically preference-ranked across consumers. 虽然

the strict vertical assumption is not necessary for many of

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

7以下, we allow that consumers may receive a subsidy, S, so that choices

are based on post-subsidy prices, Pcons

= Pj − S.

j

8We adapt the model to the case of Medicare in appendix B.2.

240

THE REVIEW OF ECONOMICS AND STATISTICS

our main insights to hold, it captures the key features of the

issues raised by simultaneous selection on two margins in a

simple way that allows for graphical representation. We next

present the vertical model, then add the cost curves, and fi-

nally show how to find equilibrium and welfare. Throughout

the paper, we discuss the implications of relaxing the vertical

demand assumption for our findings.

A. Demand

L(s) < 0 and W (cid:6)

The model’s demand primitives are consumers’ willing-

ness to pay (WTP) for each plan. Let Wi,H be WTP of con-

sumer i for plan H, and Wi,L be WTP for L, both defined as

WTP relative to U (Wi,U ≡ 0). We impose the following two

assumptions on demand:

Assumption 1. Vertical ranking: Wi,H > Wi,L for all i

Assumption 2. Single dimension of WTP heterogeneity:

There is a single index s ∼ U [0, 1] that orders consumers

based on declining WTP, such that W (西德:6)

H (s) -

瓦 (西德:6)

L(s) < 0 for all s.

These assumptions, which are a slight generalization of the

textbook vertical model,9 involve two substantive restrictions

on the nature of demand. First, the products are vertically

ranked: all consumers would choose H over L if their prices

were equal and would similarly prefer L to U if their prices

were equal.10 This is a statement about the type of setting

to which our model applies. The vertical model applies best

when plan rankings are clear—for example, a low- versus

high-deductible plan, or a narrow versus complete provider

network plan. Importantly, these are precisely the settings

where intensive margin risk selection is most relevant. When

plans are horizontally differentiated (such as in the Covered

California market; see Tebaldi, 2017), it is less likely that

high-risk consumers will heavily select into a single plan or

type of plan. In such cases, the existing EFC framework can

capture the main way risk selection matters: in versus out of

the market (the extensive margin). Our model is designed to

study the additional issues that arise when both intensive and

extensive margins matter simultaneously.11

Second, consumers’ WTP for H and L—which in general

could vary arbitrarily over two dimensions—are assumed to

collapse to a single-dimensional index, s ∈ [0, 1]. Higher s

types have both lower WL and a smaller gap between WH and

9Our vertical model follows the format of Finkelstein et al. (2019). It is

a generalization of the textbook vertical model in which products differ on

quality (Q j) and consumers differ on taste for quality (βi), so that WTP

equals: Wi, j = βiQ j and utility equals Ui, j = Wi, j − Pj = βiQ j − Pj.

10See appendix B.2 for an alternative case where the outside option is

preferred to H and L.

11Even in settings without apparent vertical differentiation across plans

within the market, our model can be useful in assessing counterfactual

policies that might generate this type of differentiation. In particular, our

examples below imply that a regulator encouraging better entrants may gen-

erate unintended cross-margin effects on the rates of uninsurance. Further,

an apparent lack of vertical differentiation may itself be an equilibrium out-

come in a vertical model, reflecting a situation where generous coverage

has already unraveled.

WL. Lower s types care more about having insurance (L versus

U ) and more about the generosity of coverage (H versus L).

This assumption is a natural approximation that captures the

primary pattern of selection in many cases; indeed it holds

exactly in a model where plans differ purely in their coin-

surance rate (see Azevedo & Gottlieb, 2017). Substantively,

assumption 2 restricts consumer sorting and substitution pat-

terns among options when prices change. The primary con-

sequence of this assumption is that consumers are only on

the margin between adjacent-generosity options—between

H and L or between L and U . No consumer is on the mar-

gin between H and U , so if the price of U (the mandate

penalty) increases modestly, the newly insured all buy L (the

cheaper plan), not H. This restriction captures in a strong

way the general (and testable) idea that these are the main

ways consumers substitute in response to price changes. With

this restriction in place (and under a price vector at which

all options are chosen), consumers sort into plans with the

highest-WTP types choosing H, intermediate types choos-

ing L, and low types choosing U . We show that weakening

this assumption—allowing an H-U margin—does not change

the key implications of the model as long as most consumers

exhibit vertical preferences. We describe a more general

(nongraphical) model in appendix A that allows for both hor-

izontal and vertical differentiation. As we describe, horizon-

tal differentiation tends to dampen the cross-margin effects

we study. Throughout, we provide supplementary (theoreti-

cal and empirical) results that show the extent to which the

relative degree of horizontal differentiation affects our main

results.

Figure 1a plots a simple linear example of WH (s) and

WL(s) curves that satisfy these assumptions. The x-axis is

the WTP index s, so WTP declines from left to right as usual.

Let sLU (P) be the extensive-marginal type who is indiffer-

ent between L and U at a given set of prices P. Assum-

ing for now that PU ≡ M = 0, this cutoff type is defined by

the intersection of L’s WTP curve WL and L’s price, where

WL (sLU ) = PL. Consumers to the right of sLU go uninsured.

Those to the left buy insurance. Therefore, WL(s) represents

the (inverse) demand curve for any formal insurance (H or

L).12

Let sH L(P) be the intensive-marginal type who is indiffer-

ent between H and L. This cutoff type is defined by

(cid:2)WH L(sH L ) ≡ WH (sH L ) − WL (sH L ) = PH − PL.

(1)

Consumers to the left of sH L buy H because their incremen-

tal WTP for H over L—which we label (cid:2)WH L—exceeds

the incremental price. With demand for H and for H + L

thus determined by these cutoffs, demand for L equals the

12In the more general case where consumers receive subsidies for pur-

chasing insurance or pay a penalty when choosing U , WL (s) and the

(inverse) demand curve for insurance will diverge. Specifically, DL (s) =

WL (s) + S + M. For simplicity, we ignore the subsidy and penalty terms

here but fully incorporate consumer subsidies when we use the model to

study the effects of common policies (section III) as well as in the empirical

exercise (section V).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

a

_

0

1

0

7

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE TWO-MARGIN PROBLEM IN INSURANCE MARKETS

241

FIGURE 1.—ENROLLEE SORTING AND COST UNDER VERTICAL MODEL

at a slope equal to that of (cid:2)WH L and its intersection with PH

determines sH L. DH (s; PL ) is flatter than WH because its slope

equals that of (cid:2)WH L(s).

Most important, DH (s; PL ) is not a pure primitive that could

be identified off of exogenous price variation but instead de-

pends on both WTP primitives (WH , WL) and, critically, on

PL. Because demand for H depends on the price of L, policies

targeted at altering the allocation of consumers on the exten-

sive margin of insurance/uninsurance can affect the sorting of

consumers across the intensive H/L margin if these policies

affect the price of L. The dependence of demand for H on

the price of L generates an interaction between the intensive

and extensive margins, a key theme of this paper.

B. Costs

(cid:3)

The model’s cost primitives are expected insurer costs for

consumers of type s in each plan j.15 These “type-specific

(cid:2)

costs” are defined as C j (s) = E

Ci j | si = s

. C j (s) is analo-

gous to “marginal cost” in the EFC model—so called because

it refers to consumers on the margin of purchasing at a given

price. However, to avoid confusion in our model where there

are two purchasing margins, we refer to C j (s) as type-specific

costs, or simply costs. In addition, we define CU (s) as the ex-

pected costs of uncompensated care of type-s consumers if

they were uninsured. Along with adverse selection, exter-

nal uncompensated care costs motivate subsidy and mandate

policies.

Plan-specific average costs are defined as the average

of C j (s) for all types who buy plan j at a given set of

prices: AC j (P) = 1

s∈D j (P) C j (s)ds, where (abusing no-

tation slightly) s ∈ D j (P) refers to s-types who buy plan j at

prices P.

D j (P)

(cid:4)

Panel a shows demand and consumer sorting under the vertical model. WH (s) and WL (s) are willingness

to pay for the H and L plans. DH (s; PL ) is the demand curve for H (as a function of PH ), which depends

on the value of PL . See the body text for additional description. Panel b shows the cost curves for H and

L plans under the vertical model. CH (s) and CL (s) are the consumer type-s specific costs. ACH (sHL ) and

ACL (sLU ; sHL ) are the average cost curves for H and L given that the intensive margin type is sHL and

the extensive margin type is sLU . Adverse selection makes the price difference PH − PL larger than the

causal cost difference.

difference between the two.13 Rearranging equation (1) yields

the (inverse) demand for H, given a fixed PL:

DH (s; PL ) ≡ WH (s) − WL(s) + PL.

(2)

Figure 1a shows DH (s; PL ) with a dashed line. One can draw

DH by noting that it intersects the WH curve at the cutoff

type sLU (since WL(sLU ) = PL).14 It then proceeds leftward

13Formally, the demand functions for the general case where M (cid:7)=

0 are defined by the following equations, where (cid:2)P ≡ PH − PL:

DH (P) = sH L ((cid:2)P); DL (P) = sLU (PL − M ) − sH L ((cid:2)P); DU (P) = 1 −

sLU (PL − M ).

14DH is not defined to the right of sLU , since if PH falls further than its

level at this point, nobody buys L. As a result, the demand curve for H

thereafter equals WH (s).

We illustrate the construction of these cost curves in fig-

ure 1b. We show a case where cost curves CH and CL are

downward sloping, indicating adverse selection. The gap be-

tween the two curves for a given s-type equals the difference

in plan spending if the s-type consumer enrolls in H versus

L. We refer to this as the “causal” plan effect, since it re-

flects the true difference in insurer spending for a given set of

people.16

We start by deriving ACH (P), the average cost curve for

the H plan. To avoid ambiguity later, it is helpful to rede-

fine the argument of ACH as the marginal type that buys

15A key insight of the EFC model is that—while costs may vary widely

across consumers of a given WTP type—it is sufficient for welfare to con-

sider the cost of the typical consumer of each type. The reason is that with

community-rated pricing, consumers sort into plans based only on WTP.

There is no way to segregate consumers more finely than WTP type, and

since insurers are risk neutral, only the expected cost within type matters.

We note, however, that this argument breaks down when leaving the world

of community-rated prices, as pointed out by Bundorf et al. (2012), Geruso

(2017), and Layton et al. (2017). Our model (like the model of EFC) thus

cannot be used to assess the welfare consequences of policies that allow for

consumer risk rating.

16As in EFC, the causal plan effect reflects both a difference in coverage

(e.g., lower cost sharing) conditional on behavior, and any behavioral effect

(or moral hazard) of the plans.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

a

_

0

1

0

7

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

242

THE REVIEW OF ECONOMICS AND STATISTICS

H at price P, sH L(P). We use this notation in figure 1b.

ACH integrates over individual costs (CH ) from the left. For

sH L = 0, the only consumers enrolled in H are the very sick-

est consumers. For these consumers, s = 0, implying that

ACH (sH L = 0) = CH (s = 0). Then, as sH L increases, mov-

ing right along the horizontal axis, H includes more relatively

healthy consumers, resulting in a downward-sloping average

cost curve. Eventually, when sH L = 1 and all consumers are

enrolled in H, ACH (sH L = 1) is equal to the average cost in H

across all consumers. Because H only has one marginal con-

sumer type (the intensive margin), the derivation of ACH (sH L )

is identical to that of the average cost curve in EFC. For each

value of sH L, there is only one possible value of ACH . This im-

plies that the curve can be calculated directly from a market

primitive (by integrating over CH (s)) and is not an equilib-

rium object.

The average cost curve for L is more complicated because

it is an average over a range of consumers, s ∈ [sH L, sLU ],

with two endogenous margins. For each value of sLU that

defines sorting between U and L, there are many possible

values of ACL, depending on consumer sorting between H

and L. This fact makes it impossible to plot a single fixed

ACL curve as we did with ACH . Nonetheless, it is possible to

plot ACL(sLU ) conditional on sH L(P). We denote this curve

ACL(sLU ; sH L ) and illustrate it with a dashed line in figure

1b. There are many such iso-sH L plots of ACL (not pictured)

that hold PH fixed at various levels. The left-most point of the

ACL curve depends on the sH L cutoff type determined by PH .

Higher values of sH L imply that ACL(sLU ; sH L ) starts from

a higher point. Just as ACH equals CH at s = 0, ACL equals

CL at s = sH L. Moving rightward from s = sH L, plan L adds

more relatively healthy consumers, resulting in a downward-

sloping average cost curve.

In summary, while ACH is fixed and does not depend on the

price of L, ACL is an equilibrium object in that it changes as

PH , and therefore sH L, changes. This implies that the average

cost of L and thus the price of L in equilibrium depends on the

price of H. Recognizing such dependencies is critical for an-

alyzing policy interventions. For example, a subsidy targeted

to H that results in a lower (net) PH and a larger H enrollment

(a rightward-shifted sH L) would cause the left-most point on

ACL to shift down and rightward and would cause the curve

to have a less-steep slope. In a competitive market, this would

likely result in a lower PL, causing additional consumers to

enter the market.

C. Competitive Equilibrium

We consider competitive equilibrims where plan prices, P,

exactly equal their average costs:

PH = ACH (P)

and PL = ACL (P) ,

(3)

In some settings, multiple price vectors will satisfy this defi-

nition of equilibrium, including vectors that result in no en-

rollment in one of the plans or no enrollment in either plan.

Because of this, we follow Handel et al. (2015) and limit

attention to equilibria that meet the requirements of the Ri-

ley equilibrium (RE) notion. A policy satisfies the RE no-

tion if there exists no “Riley deviation policy,” a compet-

ing policy that if offered, would earn a profit, render the

old policy unprofitable, and for which there is no “safe re-

sponse” that would render the Riley deviation unprofitable.

A safe response is a policy offering that does not incur a

loss when offered with the other existing policies in the mar-

ket and renders the potential Riley deviation unprofitable.

When we apply these requirements in our simulations, we

find a unique equilibrium for all empirical settings that we

simulate.17

Perfect competition is of course an approximation that will

be imperfect in many relevant markets. We maintain this as-

sumption, consistent with much prior work, to simplify the

problem and provide a benchmark for thinking about cross-

margin interactions.18

With the outside option of uninsurance, the equilibration

process for the prices of H and L differs somewhat from the

more familiar settings explored by EFC and Handel et al.

(2015). In those settings, it is assumed that all consumers

choose either H or L. Assuming full insurance conveniently

simplifies the equilibrium condition from two expressions to

one: namely, that the differential average cost must be set

equal to the differential price.

To provide intuition for equilibrium in our setting, we build

up from the classic case in EFC, which includes only H and

U as plan options.19 The EFC equilibrium can be seen in

figure 2a if one ignores the WL curve. It is defined by the in-

tersection of WH and ACH , which determines the competitive

equilibrium price. Absent an L plan, any s-type whose WTP

for H exceeds the price of H will buy H, and all other s-types

will opt to remain uninsured.

We next add L to the EFC choice set. To illustrate the equi-

librium, we proceed in four steps, corresponding to the four

panels in figure 2. Figures 2a and 2b show how PH is de-

termined, given a fixed price of L. Figure 2a shows that the

fixed PL implies a given extensive margin cutoff, sLU . Figure

2b shows that this in turn implies an H plan demand curve,

DH (PL ) (dashed). The intersection of DH (PL ) with H’s aver-

age cost curve determines PH and the intensive margin cutoff

17A detailed discussion of these requirements and an algorithm for em-

pirically identifying the RE are provided in appendixes C.3 and C.4,

respectively.

18If there is free entry into both the H and the L contracts, prices will equal

average costs in equilibrium, and there will be no cross-subsidization across

the H and L contracts within a single firm. See the proofs in appendix A of

Handel et al. (2015) and Azevedo and Gottlieb (2017). The intuition is that

in such a setting, if one firm tried to cross-subsidize the adversely selected

H contract with the L contract, another firm would enter the market and

provide only the L contract at a lower price, with no need to cross-subsidize.

This intuition would work less well in settings with a single fixed cost of

firm entry, regardless of how many plans are offered.

19The correct analogy from EFC to our framework is a choice between H

and U (rather than H and L) because the key feature of U is that its price is

exogenously determined, like the lower coverage option in the EFC setting.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

a

_

0

1

0

7

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE TWO-MARGIN PROBLEM IN INSURANCE MARKETS

243

FIGURE 2.—DETERMINATION OF EQUILIBRIUM WITH H, L, AND OUTSIDE OPTION

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

a

_

0

1

0

7

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Figures show how competitive equilibrium is determined in the vertical model with H and L plans and an outside option (uninsurance). Panels a and b show the determination of PH (PL ): a value of PL implies the

extensive margin (sLU ), which in turn implies the demand curve for H and the equilibrium PH . Panels c and d show the determination of PL (PH ): a value of PH implies the intensive margin (sHL ), which implies ACL

and the equilibrium value of PL .

sH L. This process determines the reaction function Pe

the break-even price of H for a given price of L.

H (PL ),

Figures 2c and 2d show how PL is determined, given a

fixed PH . Figure 2c shows that the fixed PH implies a given

intensive margin cutoff (sH L), which in turn fixes the ACL

curve. Figure 2d shows how the intersection of ACL with

WL determines PL and the extensive margin cutoff sLU . This

process determines the reaction function Pe

L (PH ), which gives

the break-even price of L for each price of H.

H (PL ) and PL = Pe

In equilibrium, the reaction functions must equal each

other: PH = Pe

L (PH ). Figure 3 depicts the

equilibrium, including the ACL and DH curves as dashed lines.

These dashed lines are themselves equilibrium outcomes,

even holding fixed consumer preferences and costs. In other

words, there were many possible “iso-sH L” ACL curves and

many possible “iso-PL” DH curves. The equilibrium vectors

of prices are the prices at which demand for L generates the

equilibrium DH (Pe

L ) and this demand for H simultaneously

implies the equilibrium ACL(sH L ) curve.

D.

Social Welfare

We now show how our framework can be used to assess

the welfare consequences of different policies. We define so-

cial welfare in the conventional way, as total social surplus

(willingness-to-pay minus social resource cost). In order to

make the figures simpler and more intuitive, we set CU , the

social cost of uninsurance, equal to 0. We nonetheless al-

low for a positive social cost of uninsurance in our empirical

application below.

To build intuition, we start in figure 4a by illustrating the

case where L is a pure cream skimmer. That is, L has low

244

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 3.—FINAL EQUILIBRIUM

FIGURE 4.—WELFARE

The graph shows the final equilibrium under the vertical model with two plans (H and L) and an outside

option (U ). The dots mark the key intersections defining equilibrium prices and sorting. The intersection

of ACL and WL determines PL and the extensive margin type (sLU ). The DH curve starts at this extensive

margin (where it equals WH ), and its intersection with ACH determines PH and the intensive margin type

(sHL ). This sHL type marks the start of the ACL curve (where it equals CL ).

average costs because it attracts low-cost individuals, but it

has no causal effect on costs, so CL = CH for any individual.

For this case, given WH , WL, and CL = CH , we can find total

social surplus for any allocation of consumers across plans

described by the equilibrium cutoff values se

H L and se

LU .

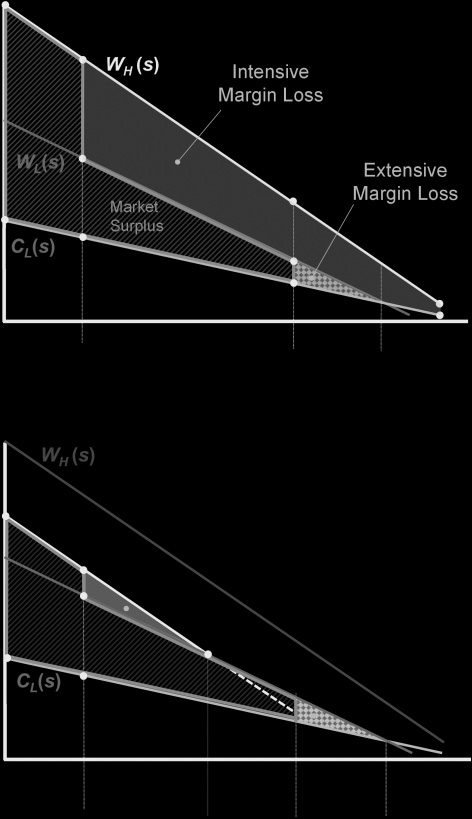

Figure 4a shows that social surplus consists of two pieces.

The first piece (ABHG) is the social surplus for consumers

purchasing H, given by the area between WH and CL = CH

for consumers with s < sH L. The second piece (E F IH) is the

social surplus for consumers purchasing L, given by the area

between WL and CL = CH for consumers with s ∈ [sH L, sLU ].

Figure 4a also illustrates forgone surplus for the allocation of

consumers across plans. Here, the forgone surplus consists of

three components. The first is the forgone surplus due to the

fact that consumers with s ∈ [sH L, sLU ] purchased L when

they would have generated more surplus by purchasing H,

and it is described by the area between WH and WL for these

consumers (BCF E ). The second component is the forgone

surplus due to the fact that consumers with s > sLU did not

purchase insurance when they would have generated positive

surplus by purchasing H, and it is described by the area be-

tween WH and max{WL, CL} (CDJF ). We refer to these two

components as “intensive margin loss.” The third component

is the forgone surplus due to the fact that consumers with

s ∈ [sLU , s∗

LU ] did not purchase insurance when they would

have generated positive surplus by purchasing L, and it is de-

scribed by the area between WL and CL for those consumers.

The figure thus shows how our graphical framework can

be used to estimate welfare for any allocation of consumers

across H, L, and U . 更远, the framework makes it easy

to determine the optimal allocation of consumers between

insurance and uninsurance and between H and L. In the case

of the particular demand and cost primitives drawn in figure

4A, the optimal allocation of consumers across plans is for

all consumers to be in H. If H were not available, 然而,

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

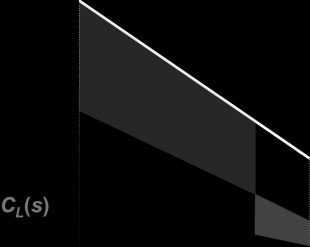

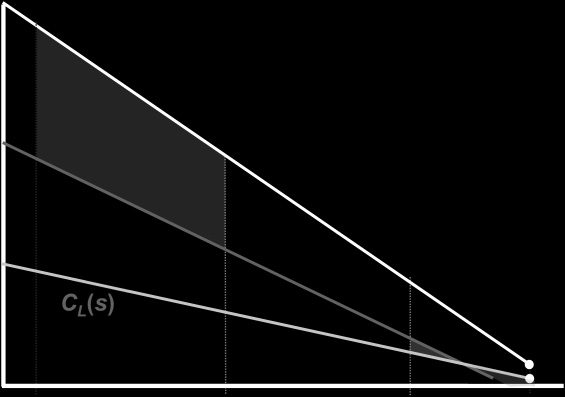

The graphs show welfare given equilibrium prices Pe and implied consumer sorting between H , L, 和

uninsured. Panel a shows the case where the L plan is a pure cream skimmer ((西德:2)CHL = CH (s) − CL (s) = 0),

while panel b shows the case where L has a causal cost advantage ((西德:2)CHL > 0). The market surplus is

阴影 (光); the loss due to intensive margin misallocation (between H and L) is shaded (黑暗的); 和

loss due to extensive margin misallocation (between L and U ) is shaded in thatched (darkest).

the optimal allocation of consumers across L and U would

consist of all consumers with s < s∗

LU purchasing L and all

other consumers remaining uninsured.

In figure 4b, we apply our framework to the case where

it is efficient for some consumers to be in L rather than in

H and for others to remain uninsured. To do this, we change

the assumption that L is a pure cream skimmer and instead

assume that costs in H are higher than in L for each con-

sumer and that the cost gap is constant across consumers:

(cid:2)CH L(s) ≡ CH (s) − CL(s) = δ > 0. 直观地, in this sce-

成员, consumers prefer H because it provides more or better

services—at a higher cost to the insurer. It is convenient to

H (s) = WH (s) - (西德:2)CH L(s), or WTP

define a new curve W Net

for H net of the incremental cost of H versus L. Under the

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

THE TWO-MARGIN PROBLEM IN INSURANCE MARKETS

245

shifts further down.20

assumption that δ is constant, W Net

H (s) will be parallel to and

below WH . This is shown in figure 4b: as L’s cost advantage

over H increases, W Net

H

Given this new W Net

H curve, social welfare is still fully char-

acterized by the three curves, W Net

H , WL, and CL, 和社会的

surplus and forgone surplus are defined in a similar manner

to figure 4a. Social surplus still consists of two components.

The first is the surplus generated by the consumers enrolled

in H, and it is characterized by ABHG, the area between

and CL for consumers with s < sH L.21 This component

W Net

H

is smaller than it was in figure 4a due to the fact that now H

has higher costs than L. In figure 4b, it is thus less socially

advantageous for these consumers to be enrolled in H versus

L. The second component is the surplus generated by the con-

sumers enrolled in L, and it is characterized exactly as before

by E F IH, the area between WL and CL for consumers with

se

LU . Forgone surplus is illustrated in figure 4b,

H L

similar to the illustration in figure 4a.22 In summary, figure 4

shows how our model can accommodate settings in which it

is not socially efficient for all consumers to be enrolled in H

or even in L, such as settings where there is moral hazard or

administrative costs, for example.

< s < se

Appendix B.3 derives a formal expression for welfare, al-

lowing for cases whereCU is non-0, for example, if the outside

option involves social costs like uncompensated care. This

derivation formalizes what is shown graphically in figure 4.

III. Two-Margin Impacts of Risk Selection Policies

In this section, we use our model to assess the conse-

quences of three policies commonly used to combat adverse

selection in insurance markets: benefit regulation, the man-

date penalty on uninsurance, and risk adjustment transfers.

Each of these policies is targeted at one margin of adverse

selection, but our model shows how they affect the other. We

discuss each policy in turn and provide graphical illustra-

tions for their consequences. We conclude with a discussion

of other policies where cross-margin impacts on selection

may be relevant, including behavioral interventions targeting

take-up.

A. Benefit Regulation

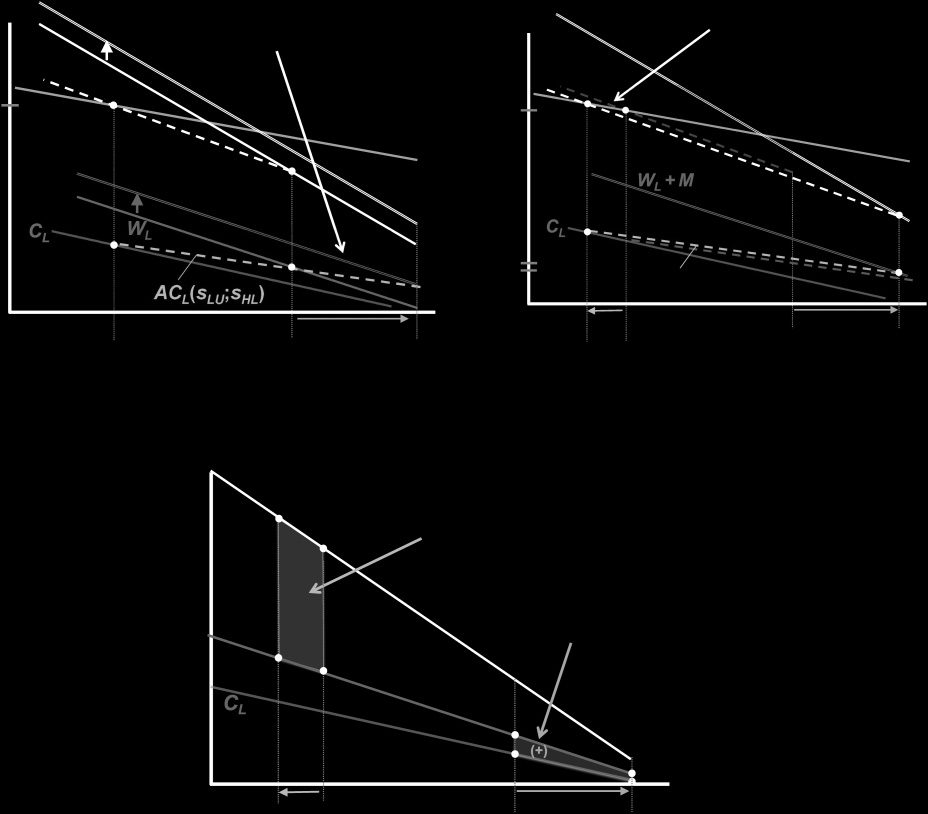

We start by examining benefit regulation. In figure 5, we

consider a rule that eliminates L plans from the market. This

20Heterogeneity in L’s cost advantage across s types could also be accom-

modated and would result in W Net

H

not being parallel to WH .

21To see this, note that this gap is equal to W Net

(CH (s) − CL (s)) − CL (s) = WH (s) − CH (s).

H (s) − CL (s) = WH (s) −

H L

, s∗

22Here, forgone surplus again consists of two components. The first is

the forgone intensive margin surplus due to the fact that consumers with

s ∈ [se

H L] are enrolled in L but would generate more surplus if they

were enrolled in H. It is characterized by the area between W Net

and WL

for these consumers (BKE ). (Unlike in figure 4a, with H’s higher costs,

it is now inefficient for any consumer with s > s∗

H L to enroll in H.) 这

second component represents the extensive margin forgone surplus, and it

is identical to the extensive margin forgone surplus in figure 4a.

H

thought experiment captures a variety of policies that set a

binding floor on plan quality—for example, network ade-

quacy rules, caps on out-of-pocket limits, and the ACA’s

“essential health benefits.” These policies seek to address

intensive margin adverse selection problems by eliminating

low-quality, cream-skimming plans. But as we show, they can

also have unintended extensive margin consequences.

Figure 5a shows the baseline equilibrium with both H and

L plans, while figure 5b shows equilibrium with L plans

eliminated, which reduces to the classic EFC equilibrium.

Figure 5c shows the welfare impact of benefit regulation.

This involves two competing effects: some consumers for-

merly in L shift to H (the intended consequence), 还有一些

consumers formerly in L become uninsured (the unintended

consequence).

In the textbook cream-skimming case, where H is the so-

cially efficient plan for everyone (though most consumers still

generate more social surplus in L versus U ), these two effects

have opposing welfare consequences. 第一个 (intended) 埃夫-

fect increases social surplus by shifting people out of L—an

inefficient plan that exists only by cream skimming—and

into H. 第二 (unintended) 影响, 然而, lowers so-

cial surplus by shifting some L consumers into uninsurance.

因此, even in this textbook case where the L plan is an in-

efficient cream skimmer, banning it has ambiguous welfare

consequences.23

What explains this counterintuitive result? This can be

thought of as an example of “theory of the second best”-style

interactions that emerge with two margins of selection. Reg-

ulation that bans a pure cream-skimming L plan addresses an

intensive margin selection problem. But it has the unintended

side effect of worsening the extensive margin selection prob-

lem of too much uninsurance. Put differently, a pure cream-

skimming L plan adds no social value within the market, 但

by segmenting the healthiest people into a low-price plan,

it can improve welfare by bringing new consumers into the

market.24

乙. Mandate Penalty on Uninsurance

Next we consider the consequences of a mandate penalty

for remaining uninsured (choosing U ). The analysis is also

applicable for analyzing the effect of providing larger insur-

ance subsidies, which reduce consumers’ net price of buying

insurance relative to remaining uninsured.

The mandate penalty has both a direct effect and an indi-

rect effect through equilibrium price adjustments. The direct

23The net welfare impact depends on the market primitives (WH , WL, CH ,

CL) and the social cost of uninsurance,CU . Section II presents the framework

for how these can be measured and the net welfare impact quantified.

24当然, this reasoning depends on the market stabilizing to a separat-

ing equilibrium where both H and L survive. If the market unravels to the L

plan, insurance coverage will typically not be higher: the price of L will not

be low (since it attracts all consumers), and because the quality of L is lower,

uninsurance will typically be higher than in an H-only equilibrium where

L is banned. Whether the market stabilizes to a separating equilibrium or

unravels to L or upravels to H depends on the market primitives.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

246

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 5.—IMPACT OF BENEFIT REGULATION

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

r

e

s

t

/

我

A

r

t

我

C

e

–

p

d

F

/

/

/

/

1

0

5

2

2

3

7

2

0

7

3

2

3

0

/

r

e

s

t

_

A

_

0

1

0

7

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The figure shows the impact on equilibrium (panels a and b) and welfare (panel c) of a benefit regulation that eliminates the L plan. This thought experiment captures a variety of policies that set a binding floor on plan

质量, thus eliminating low-quality plans. For welfare impacts, we show the textbook case where H is the efficient plan for all consumers and L is more efficient than U .

effect of a mandate penalty is to increase the demand for in-

surance. Figure 6a shows this via an upward shift in WL and