The Long-Run Determinants of Indian

Government Bond Yields

Tanweer Akram and Anupam Das∗

This paper investigates the long-term determinants of the nominal yields

of Indian government bonds (IGBs). It examines whether John Maynard

Keynes’ supposition that the short-term interest rate is the key driver of the

long-term government bond yield holds over the long run, 控制后

key economic factors. It also appraises if the government fiscal variable has

an adverse effect on government bond yields over the long run. The models

estimated in this paper show that in India the short-term interest rate is the

key driver of the long-term government bond yield over the long run. 然而,

the government debt ratio does not have any discernible adverse effect on IGB

yields over the long run. These findings will help policy makers to (我) 使用

information on the current trend of the short-term interest rate and other

key macro variables to form their long-term outlook about IGB yields, 和

(二) understand the policy implications of the government’s fiscal stance.

关键词: government bond yields, 印度, interest rates, monetary policy

JEL codes: E43, E50, E60, G10, O16

我. 介绍

John Maynard Keynes (1930) contends that the central bank’s monetary

policy is the most important driver of the long-term interest rate. He believes

that the central bank’s actions influence the long-term interest rate primarily

through the effect of policy rates on the short-term interest rate and other tools

of monetary policy. In The General Theory of Employment, Interest, and Money,

Keynes (2007 [1936]) reiterates the importance of the central bank’s influence

on the long-term interest rate, even though he acknowledges that interest rates

have psychological, 社会的, and conventional foundations, and arise from investors’

liquidity preferences.

∗Tanweer Akram (corresponding author): Director of Global Public Policy and Economics, Thrivent Financial,

明尼阿波利斯, 美国. 电子邮件:

tanweer.akram@thrivent.com; Anupam Das: 教授, Department of

经济学, 正义, and Policy Studies at Mount Royal University, 艾伯塔省, 加拿大. 电子邮件: adas@mtroyal.ca. 这

authors’ institutional affiliations are provided for identification purposes only. The views expressed are solely those

of the authors and are not necessarily those of Thrivent Financial, Thrivent Asset Management, or any of its affiliates.

This is for information purposes only and should not be construed as an offer to buy or sell any investment product

or service. The authors would like to thank the managing editor and two anonymous referees for helpful comments

and suggestions. The usual ADB disclaimer applies.

Asian Development Review, 卷. 36, 不. 1, PP. 168–205

https://doi.org/10.1162/adev_a_00127

© 2019 Asian Development Bank and

Asian Development Bank Institute.

在知识共享下发布

归因 3.0 国际的 (抄送 3.0) 执照.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 169

This paper examines whether Keynes’ supposition that the short-term interest

rate is the key driver of the long-term government bond yield holds in India over

the long run after controlling for various key economic factors, such as inflationary

pressure and measures of economic activity. It also appraises if government fiscal

变量, such as the ratio of government debt to nominal gross domestic product

(GDP), have an adverse long-run effect on government bond yields in India. Akram

and Das (2015a and 2015b) report that Keynes’ conjectures hold in India for the

short-run horizon. They also find that government fiscal variables do not appear

to exert upward pressure on Indian government bond (IGB) yields. 然而, 他们

do not examine if these results hold over a long-run horizon. This paper fills that

critical lacunae.

Understanding the determinants of government bond yields in India over the

long-run horizon is important not just for scholarly reasons but also for policy

purposes and policy modeling, particularly for discerning the effects of fiscal

and monetary policy on IGB yields. Understanding the drivers of government

bond yields in emerging markets such as India has crucial

implications for

the government’s fiscal and macroeconomic policy mix. It is also relevant for

fixed income investment and portfolio allocation, as well as the management of

government debt.

India’s institutional features, its economic rise, and the evolution of its

financial system make it worthwhile to examine the long-run trends in its

government bond market. 第一的, India’s financial markets are in the development

阶段. While India has liberalized its economy and many aspects of its financial

系统, there are still various restrictions. Its bond market is not as deep as those

of advanced capitalist economies such as Japan, 英国, 和

美国 (我们). The country’s banking system is dominated by state-owned or

state-controlled financial institutions, and its fixed income investors in the local

currency bond market are largely confined to investing in government securities

since the depth and liquidity of corporate bonds and other fixed income securities

are limited. 这是, 因此, appropriate to inquire whether Keynes’ supposition

regarding the link between the short-term interest rate and the long-term interest

rate holds in the institutional and structural circumstances of emerging market

economies such as India. 第二, whether the central bank’s setting of the policy

速度(s) and other monetary policy actions influence the long-term interest rate over

the long run in India has meaningful policy implications for monetary transmission

mechanisms. If the evidence suggests that the central bank can decisively affect

the long-term interest rate, not just in the short run but also over the long run,

this would show that the Government of India has considerable policy space. If no

such relationship can be established, then this would mean that its policy space is

rather restrictive and narrow. 因此, it is important to examine what conjectures are

empirically warranted in India and other emerging markets.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

170 Asian Development Review

The paper is organized as follows. Section II sets the foundation for the

empirical investigation. 第一的, it discusses Keynes’ view on interest rates and

provides the theoretical framework. 第二, it summarizes Keynes’ stance on the

loanable funds theory and explains why he rejects this theory. 第三, it presents a

simple two-period model of government bond yields. 第四, it recounts the stylized

facts about government bond yields and government debt ratios. 第五, it briefly

reviews the relevant literature on government bond yields in emerging market

经济体. Section III describes the data, the behavioral equations to be estimated,

and the econometric methodology applied here. Section IV reports the empirical

findings. Section V analyzes the policy implications of the results and concludes.

附录 1 presents the details of the simple two-period model of government bond

yields used in the paper. 附录 2 presents additional regressions to examine the

effects of credit growth, global investors’ risk appetite, and the nominal effective

exchange rate on government bond yields.

二. Theoretical Framework, 模型, Institutional Background, Stylized Facts,

and Brief Review of the Literature

A.

The Keynesian Framework

This paper investigates the long-run determinants of IGB yields based on

Keynes’ (1930 和 2007 [1936]) 意见. Keynes holds that the central bank’s actions

play the decisive role in setting the long-term interest rate on government bonds

(Kregel 2011). He argues against the classical view of interest rates based on the

loanable funds theory as represented in Cassel (1903), 马歇尔 (1890), Taussig

(1918), and the classical economists.

The central bank’s ability to influence the long-term interest rate arises from

its ability to set the policy rate and anchor the short-term interest rate around the

policy rates, and to use various other tools of monetary policy (Keynes 1930). 他

acknowledges that interest rates have a foundation based on human psychology,

social conventions, herd mentality, and liquidity preferences (Keynes 2007 [1936]).

尽管如此, the most immediate and important driver of long-term government

bond yields are the central bank’s actions as manifested through its ability to

(我) influence the short-term interest rate by setting the policy rate, 和 (二) use a wide

range of tools of monetary policy including expanding and contracting its balance

sheet as it deems appropriate. Keynes relies on Riefler’s (1930) pioneering empirical

analysis of the behavior of interest rates on US government securities (Kregel 2011).

He also observes that current conditions and the investor’s near-term outlook affect

the investor’s long-term outlook. Keynes believes that since the investor does not

have a firm basis for estimating the mathematical expectations of the unknown and

uncertain future, the investor resorts to forming an outlook of the future based on

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 171

past and current conditions. 因此, the factors that affect the short-term interest

rate also affect the long-term interest rate.

Keynes’ view on the drivers of long-term government bond yields is

in contrast to that of conventional views in macroeconomics and finance. 这

conventional view is that government debts and deficits have a decisive effect on

government bond yields. Other things held constant, if government debts and/or

government deficits (both as a share of nominal GDP) 增加 (减少), 然后

government bond yields will rise (衰退). This view relies on the loanable funds

theory of interest rates. For Keynes, liquidity preferences and the central bank’s

actions are largely responsible for interest rates as manifested in the yield curve

for gilt-edged (政府) securities and other fixed income instruments in an

经济.

Among others, Ardagna, Caselli, and Lane (2007); Baldacci and Kumar

(2010); Gruber and Kamin (2012); Lam and Tokuoka (2013); Poghosysan (2014);

and Tokuoka (2012) represent the conventional view. 相比之下, Akram (2014);

Akram and Das (2014A, 2014乙, 2015A, 2015乙, 2017A, 2017乙, and 2017c); 和

Akram and Li (2016, 2017A, and 2017b) have argued that the short-term interest

rate and pace of inflation are the key drivers of interest rates on government

bonds. 而且, they argue that if other things are held constant, the government

fiscal variable has hardly any influence on government bond yields. This view is

based on their interpretation of Keynes. It is supported with empirical work on the

determinants of government bond yields in the eurozone, 印度, 日本, and the US.

As mentioned earlier, Akram and Das’ (2015a and 2015b) empirical work on India

has merely explored the short-run dynamics. This paper examines whether the same

hypothesis holds true for India in the long run.

乙.

Keynes’ Stance on the Loanable Funds Theory of Interest Rates

Keynes rejected the loanable funds theory of interest rates. 根据

the proponents of this theory, the interest rate is primarily determined by the

demand and supply of loanable funds. The loanable funds theory has a distinguished

pedigree. It is endorsed in classical economics such as Cassel (1903), Böhm-Bawerk

(1959), 哈耶克 (1933 和 1935), 马歇尔 (1890), Pigou (1927), Ricardo (1817),

von Mises (1953), and Wicksell (1962 [1936]). Keynes rejects the loanable funds

theory because he believes it is insufficient to determine interest rates solely on

the basis of knowledge of the demand for investment and the supply of savings.

He criticizes the loanable funds theory for neglecting the roles of national income,

the marginal propensity to consume, and liquidity preference in the determination

of interest rates. In his view, the “rate of interest is the reward for parting with

liquidity for a specified time” (Keynes 2007 [1936], p. 167). It follows that the

interest rate is “a measure of the unwillingness of those who possess money to part

with their liquid control over it.” Liquidity preference is quite central to Keynes’

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

172 Asian Development Review

view on the interest rate. Liquidity preference arises from fundamental uncertainty

about future economic and financial conditions, and the divergence among investors

about their outlook for the future. Interest rates have institutional and behavioral

foundations. 因此, for Keynes, institutions like the central bank and investors’

psychology and social orientation, as manifested in herding and the formation of

long-term expectations, play decisive roles in the determination of the interest rate,

rather than just the demand and supply of loanable funds. The demand and the

supply of loanable funds are outcomes of income, the propensity to consume, 和

liquidity preference, which occur within a context that consists of institutions, 这样的

as the central bank, and amid investors’ psychology that is guided by animal spirits,

本能, and social conventions.

C.

A Simple Two-Period Model of Government Bond Yields

A simple model, based on Akram and Das’ (2014 和 2015) and Akram

and Li’s (2016 and 2017a) interpretations of Keynes’ views, is presented here to

show the connection between the current short-term interest rate and the long-term

interest rate.

To simplify the exposition, a two-period horizon is used. 那里有两个

periods: t = 1, 2. The long-term interest rate on a government bond in period 1

is rLT ; the short-term interest rates on a Treasury bill in period 1 and period 2

是, 分别, r1 and r2; the expected short-term interest rate in period 2 is Er2;

the 1-year, 1-year forward rate is f1,1; the term premium is z; the current rate of

inflation in period 1 is π1; the actual rate of inflation in period 2 is π2; the expected

rate of inflation in period 2 is Eπ2; the current growth rate in period 1 is g1; 这

actual growth rate in period 2 is g2; the expected growth rate in period 2 is Eg2; 这

government fiscal variable in period 1 is ν1; the government fiscal variable in period

2 is ν2; and the expected government fiscal variable in period 2 is Ev2.

It can be shown that the long-term interest rate is a function of either (我) 这

short-term interest rates in period 1 and period 2, and the growth rate and the rate

of inflation in period 2; 或者 (二) the short-term interest rates in period 1 and period

2, and the growth rate, the rate of inflation, and the government fiscal variable in

时期 2. 因此, the models of the determinants of the long-term bond yields take

the following forms:

rLT = F 7 (r1, r2, g2, π2)

rLT = F 8 (r1, r2, g2, π2, ν2)

(1)

(2)

A detailed derivation of the above models is presented in Appendix 1.

It is appropriate to incorporate the government fiscal variable in the model

of the long-term interest rate for several reasons. 第一的, government fiscal variables

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 173

affect the long-term interest rate in the standard IS–LM Keynesian models. 第二,

it is also included in the standard theoretical and empirical literature, 包括

Ardagna, Caselli, and Lane (2007); Baldacci and Kumar (2010); and other studies

cited in section II.A. 第三, since the paper assesses whether Keynes’ conjecture

regarding the importance of the short-term interest rate in driving the long-term

interest rate is more warranted than that of the conventional view, it is necessary

to empirically estimate the effect of government fiscal variables on the long-term

interest rate. Ruling out, a priori, the role of the government fiscal variable on the

long-term interest rate would be arbitrary and could be regarded as an ad hoc and

unjustified maneuver. Undoubtedly, the empirical findings of this and other studies

that find support for the Keynesian perspective can influence the choice of variables

in the construction of models of the long-term interest rate in the future.

D.

Institutional Background

Akram and Das (2015a and 2015b) provide the institutional background

to the monetary policy framework, the government bond market, and monetary–

fiscal coordination in India. Yanamandra (2014) gives additional perspective on

monetary policy making in India in light of economic reforms, modernization,

and recent developments, while Chakraborty (2016) provides a detailed description

and analysis of the country’s monetary–fiscal policy mix and monetary–fiscal

协调. Jácome et al.’s (2012) survey of global practices among central

banks in extending credit and coordinating with the national Treasury includes a

description of Indian laws, 法规, and practices related to its Treasury and

central bank.

India enjoys monetary sovereignty as defined by Wray (2012). 这

Government of India issues its own currency, the rupee. The country’s central

bank, the Reserve Bank of India (RBI), sets the policy rates and can use a wide

range of monetary policy tools. The RBI enjoys a wide range of authority and

control over the country’s financial system. The Government of India has the

legal and political authority to collect taxes from households, 企业, financial

机构, and other organizations. The country’s sovereign debt is predominantly

issued in its own currency, the rupee. The multifaceted roles played by the RBI in the

payment system, monetary policy, financial stability policy, and policy coordination

with the Treasury gives it the operational ability to influence government bonds’

nominal yields by setting and changing the short-term interest rate and using

other tools of monetary policy as it deems appropriate. RBI (2014) 提供了一个

detailed institutional description of the IGB market, while RBI (various years)

Annual Reports give useful summaries of the central bank’s monetary policy and

background. 这 2009 report presents a valuable perspective on the operational

aspects of monetary–fiscal coordination in India.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

174 Asian Development Review

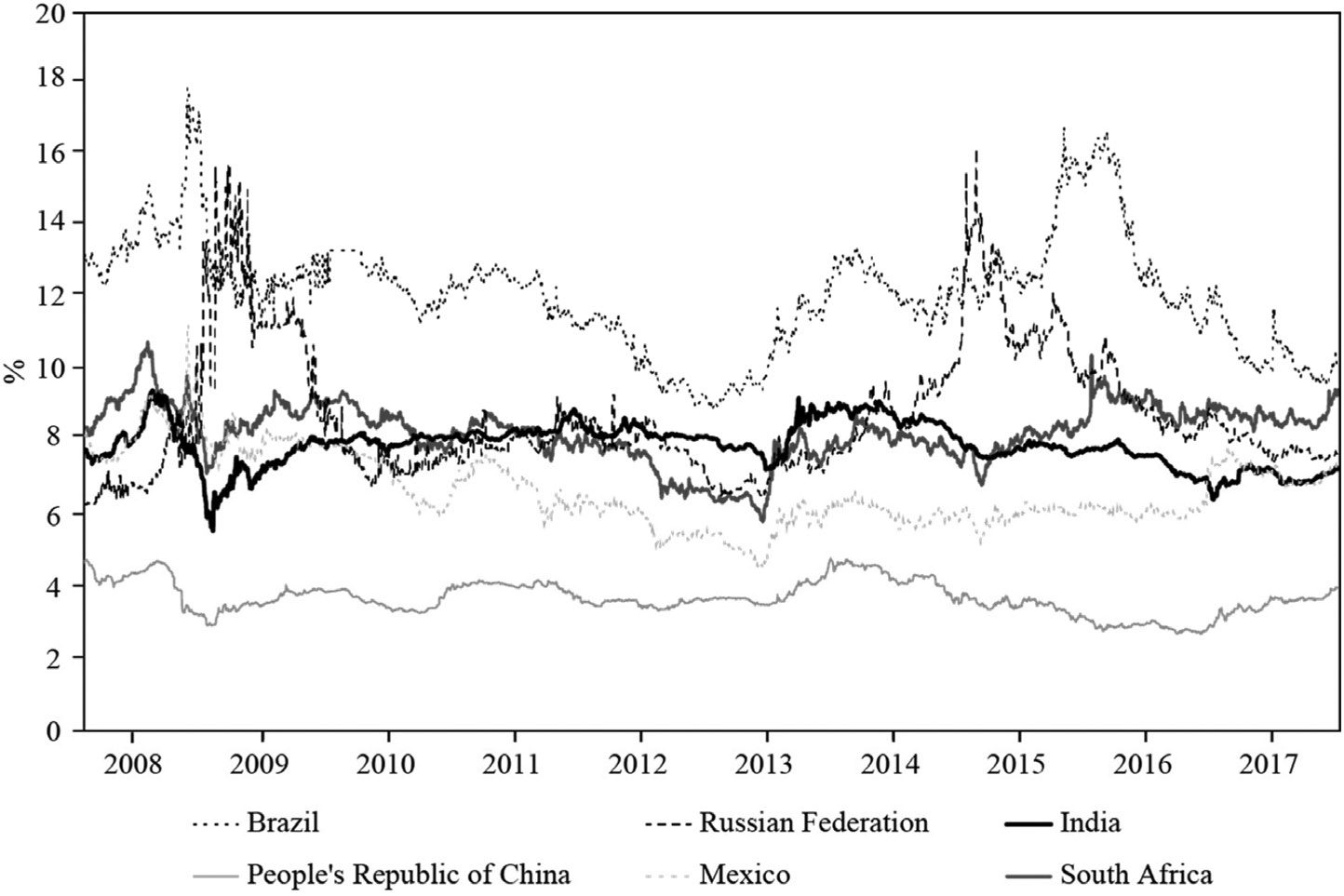

数字 1. The Evolution of 10-Year Government Bond Yields in Selected Emerging

Market Economies

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

来源: Macrobond. Various years. Macrobond subscription services (九月访问 13, 2017).

乙.

Stylized Facts

A set of figures are presented in this section to highlight important stylized

facts related to IGBs and government finance. 数字 1 compares the evolution of

10-year government bond yields in India with that of other major emerging markets,

such as Brazil, 墨西哥, the People’s Republic of China, the Russian Federation, 和

南非. It shows that since the global financial crisis, government bond yields

in India have been generally higher than in the People’s Republic of China and

墨西哥, but lower than in Brazil. Government bond yields in the Russian Federation

and South Africa have been more volatile than those in India. 最近几年, 作为

commodity prices tumbled, financial flows to emerging markets weakened, 和他们的

central bank policy rates increased, and government bond yields in the Russian

Federation and South Africa rose.

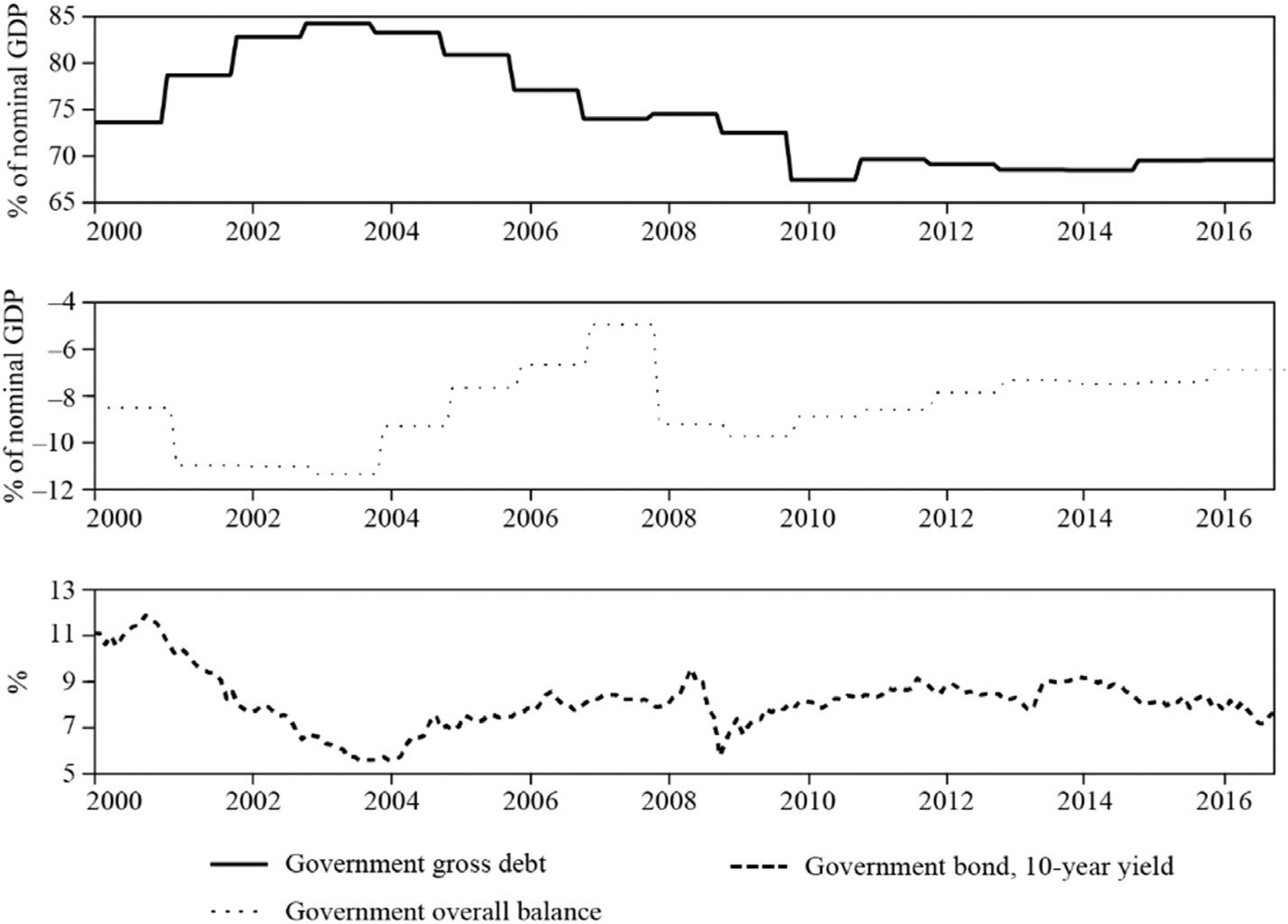

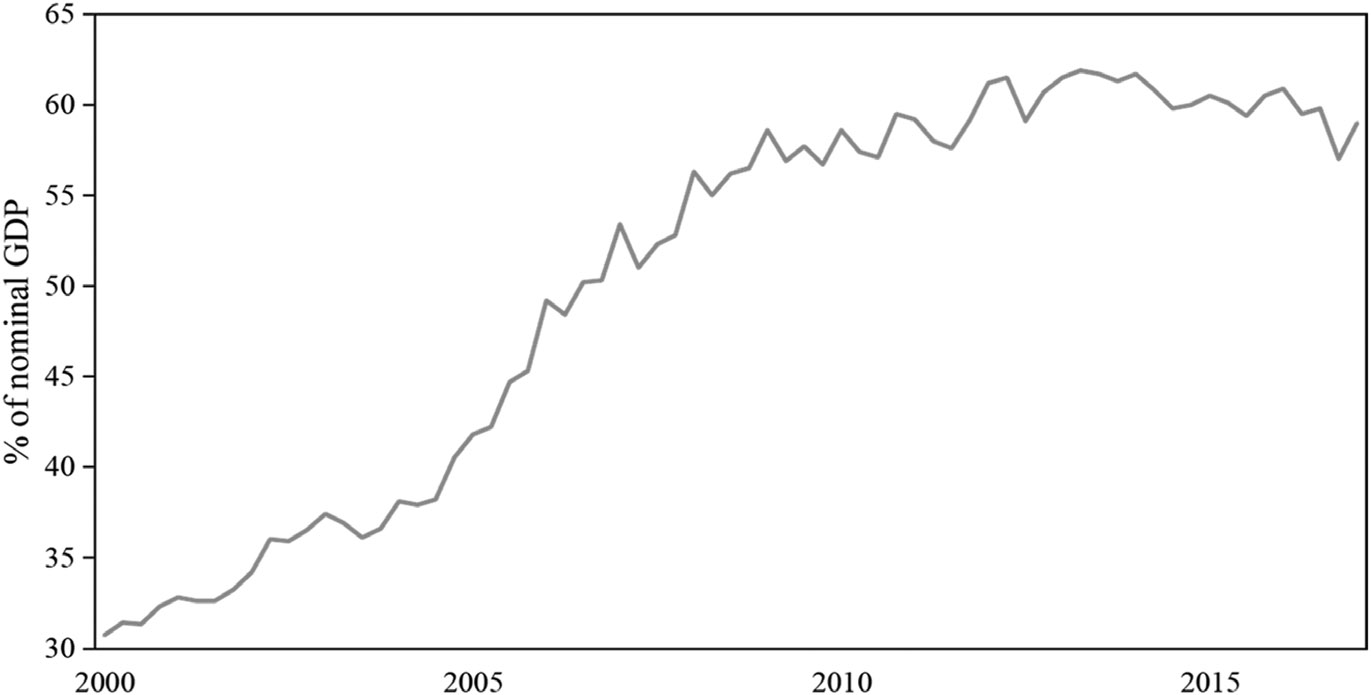

数字 2 shows the evolution of key government fiscal variables in India

例如 (我)

ratio of gross government debt to nominal GDP, (二) 的比率

government fiscal balance to GDP, 和 (三、) 10-year government bond yield. 它

shows that the government debt-to-GDP ratio rose from 70% to nearly 85% 在里面

early 2000s, but subsequently declined to around 70% as the country’s annual fiscal

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 175

数字 2. The Evolution of Key Government Fiscal Variables in India

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

GDP = gross domestic product.

来源: Macrobond. Various years. Macrobond subscription services (九月访问 13, 2017).

balance improved from a deficit of around 11% of GDP in the early 2000s to a

deficit of just 4% of GDP in the 2010s. Since the beginning of the 2010s, India’s

government debt ratio has been stable at around 70%, while its fiscal deficit has

hovered around 7% of GDP. The figure also suggests that, prima facie, the evolution

of government bonds yields in India is not directly affected by government fiscal

状况.

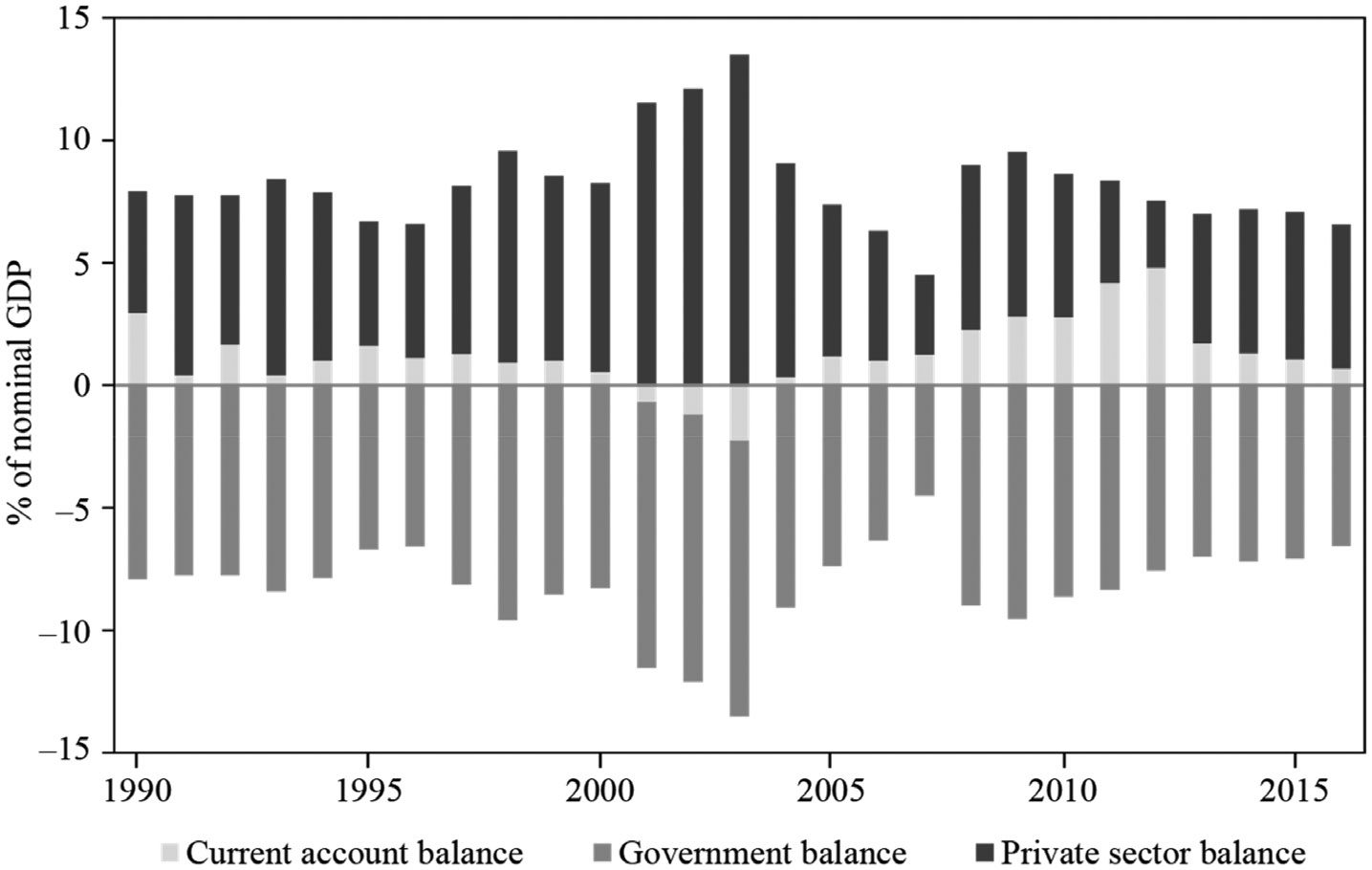

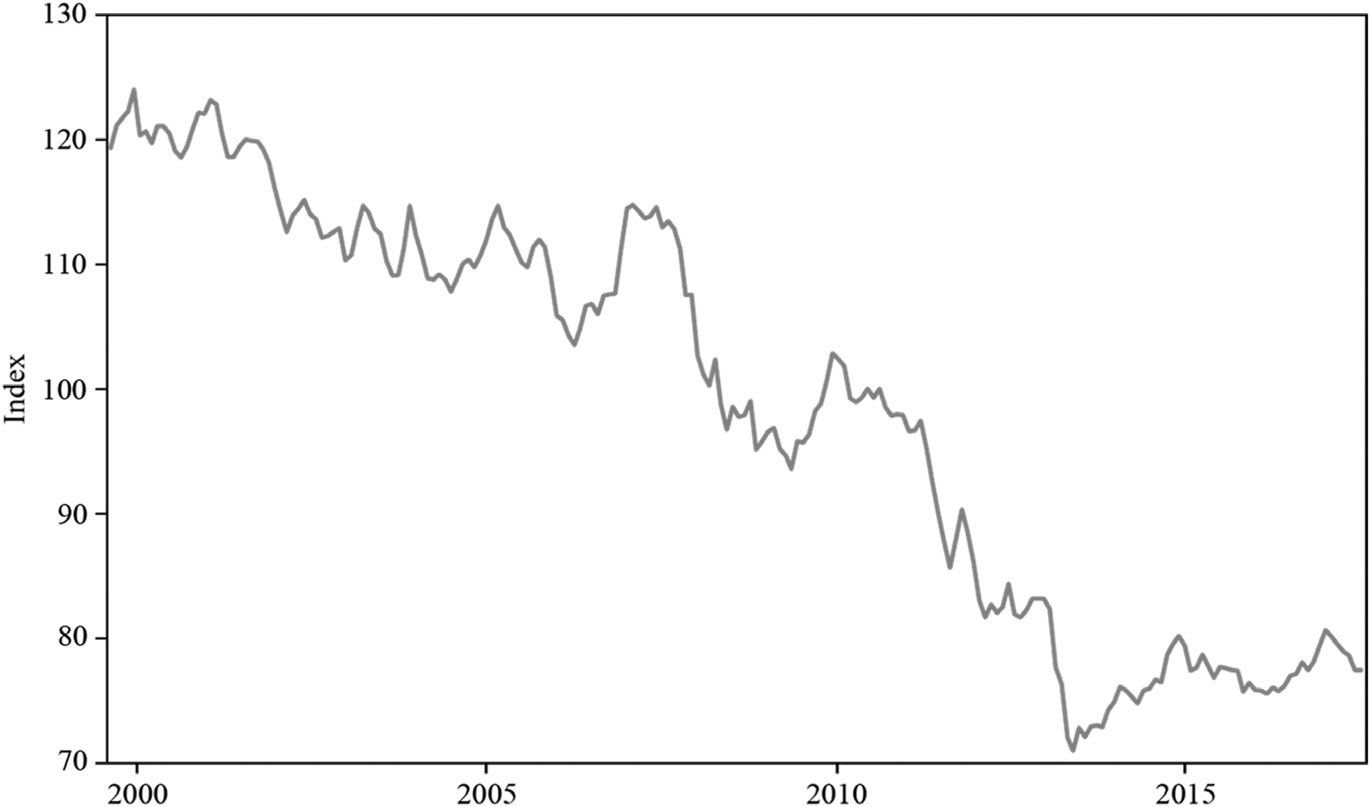

数字 3 shows the evolution of the sector balances as a share of nominal

GDP in India. It uses annual flow data to display (我) the government balance, (二) 这

private sector balance, 和 (三、) the current account balance. It visually shows that

the flow of government dissaving is equal to private sector saving and the rest of the

world’s saving in Indian rupees.

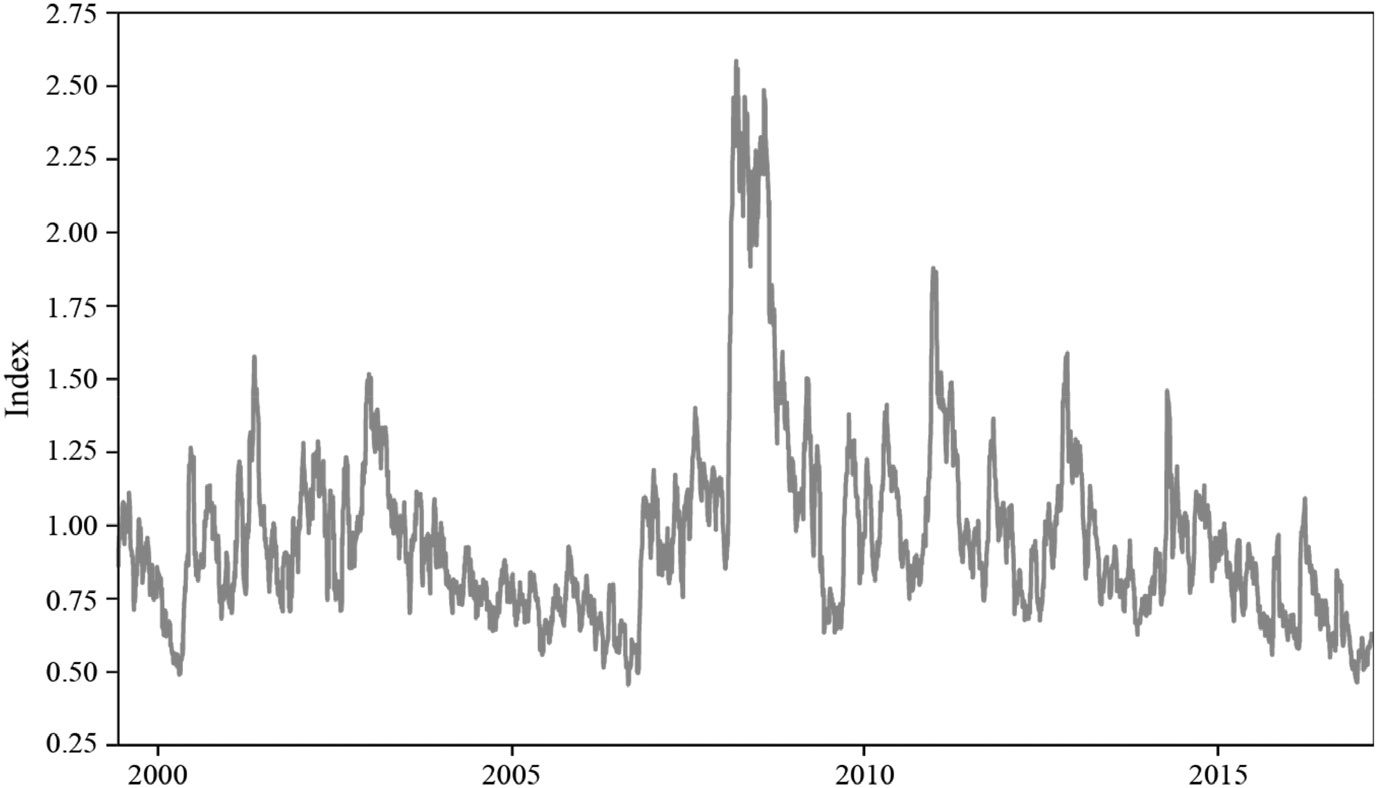

数字 4 displays that the changing relationship between the credit default

swap (CDS) premium on IGBs and the spread between the nominal yields of

10-year IGBs and 10-year US Treasury notes since 2010. It shows that the

correlation can change drastically. 之间 2010 和 2013, the CDS premium

and the yield spread were tightly correlated. 然而, 自从 2014, the correlation

between the CDS premium and the yield spread has been quite weak.

176 Asian Development Review

数字 3. The Evolution of Sector Balances in India

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

GDP = gross domestic product.

来源: Macrobond. Various years. Macrobond subscription services (九月访问 12, 2017).

数字 4. The Evolution of Credit Default Swap Premiums and Yield Spreads

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

CDS = credit default swap, IGB10Yr = 10-year Indian government bond yield, lhs = left-hand side, rhs = right-hand

边, USD = United States (我们) dollar, UST10Yr = 10-year US Treasury note yield.

来源: Macrobond. Various years. Macrobond subscription services (九月访问 12, 2017).

The Long-Run Determinants of Indian Government Bond Yields 177

F.

A Brief Review of the Literature on Government Bond Yields

There is a substantial literature on government bonds yields, including on

the determinants of government bond yields in emerging markets such as India.

尽管如此, the debate on the determinants of bond yields and the relative

importance of the key drivers is still unsettled.

We examine the findings of recent studies on government bond yields to

ascertain how relevant these are to the question that this paper addresses. Andritzky

(2012) provides a useful database on the investor base for government securities

and investigates the effect of the composition of the investor base on government

bond yields. Even though the study relies on G20 advanced economies and the

eurozone, a key finding appears to be relevant for emerging markets. An increase in

the share of bonds held by institutional or nonresidents by 10 百分点

is correlated with a decline in bond yields by about 25–40 basis points (bps).

Asonuma, Bakhache, and Hesse (2015) find that an increase in domestic bank

holdings of government bonds reduces bond yields and provides fiscal space for the

sovereign authorities. Ebeke and Lu (2014) argue that the rise in foreign holdings

of local currency government bonds in emerging markets has led to a decline

in bond yields but a rise in their volatility, particularly since the global financial

crisis. Acharya and Steffen (2015) provide an insightful analysis of the cause of the

divergence of bond yields between the core of the eurozone and its periphery. 他们

also discuss the vital role played by the “carry trade” of eurozone banks in causing

the widening of the spread. The results of Ardagna, Caselli, and Lane (2007) are in

line with the conventional wisdom cited earlier in the introduction. They claim that

an increase of 1 percentage point in the ratio of the primary deficit leads to (我) 一个

increase in the current long-term interest rate by 10 bps and (二) cumulative increases

in the long-term interest rate by 150 bps after 10 年. These and other results in

the conventional literature on government bond yields are interesting. 然而, 这

conventional literature does not probe sufficiently the key role of the central bank

in influencing government bond yields in emerging markets. 因此, a Keynesian

perspective may provide a more insightful analysis of the decisive factors and may

be more pertinent for understanding government bond yields in India.

This view is reinforced by the empirical literature on IGBs, which largely

refutes the conventional view that higher (降低) government debt or government

deficits induce higher (降低) government bond yields. Chakraborty’s (2016)

detailed and careful institutional and empirical study finds that there is no evidence

of any link between fiscal deficit and interest rates in India. Vinod, Chakraborty,

and Karun (2014) use the maximum entropy bootstrap method and report that the

government fiscal deficit ratio is not significant for interest rate determination in

印度. Chakraborty (2012), applying asymmetrical vector autoregressive models,

finds that an increase in the fiscal deficit ratio does not lead to a rise in interest rates.

Akram and Das (2015a and 2015b) show that changes in the short-term interest rate,

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

178 Asian Development Review

after controlling for other crucial variables such as changes in the rates of inflation

and economic activity, take a lead role in driving the changes of the nominal yields

of IGBs. Additional results show that higher fiscal deficits do not appear to exert

upward pressures on government bond yields. Findings from Akram and Das (2015A

and 2015b) 是, 然而, valid solely for the short run. One of the important goals

of the current paper is to examine if the findings from Akram and Das (2015a and

2015乙) hold over the long-run horizon.

The next section introduces behavioral equations, time series data, 和

econometric methods to examine the role of the short-term interest rate, the rate of

inflation, the government fiscal variable, and other key macroeconomics variables

to determine the nominal yields on IGBs over the long-run horizon.

三、. 数据, Behavioral Equations, and Methods

A.

Data1

For the purpose of econometric estimations, time series data on the nominal

yields of long-term IGBs, the short-term interest rate, the rate of inflation, 这

growth of industrial production, and government fiscal variables are used.

Nominal yields on Indian Treasury bills with 3-month maturities are used

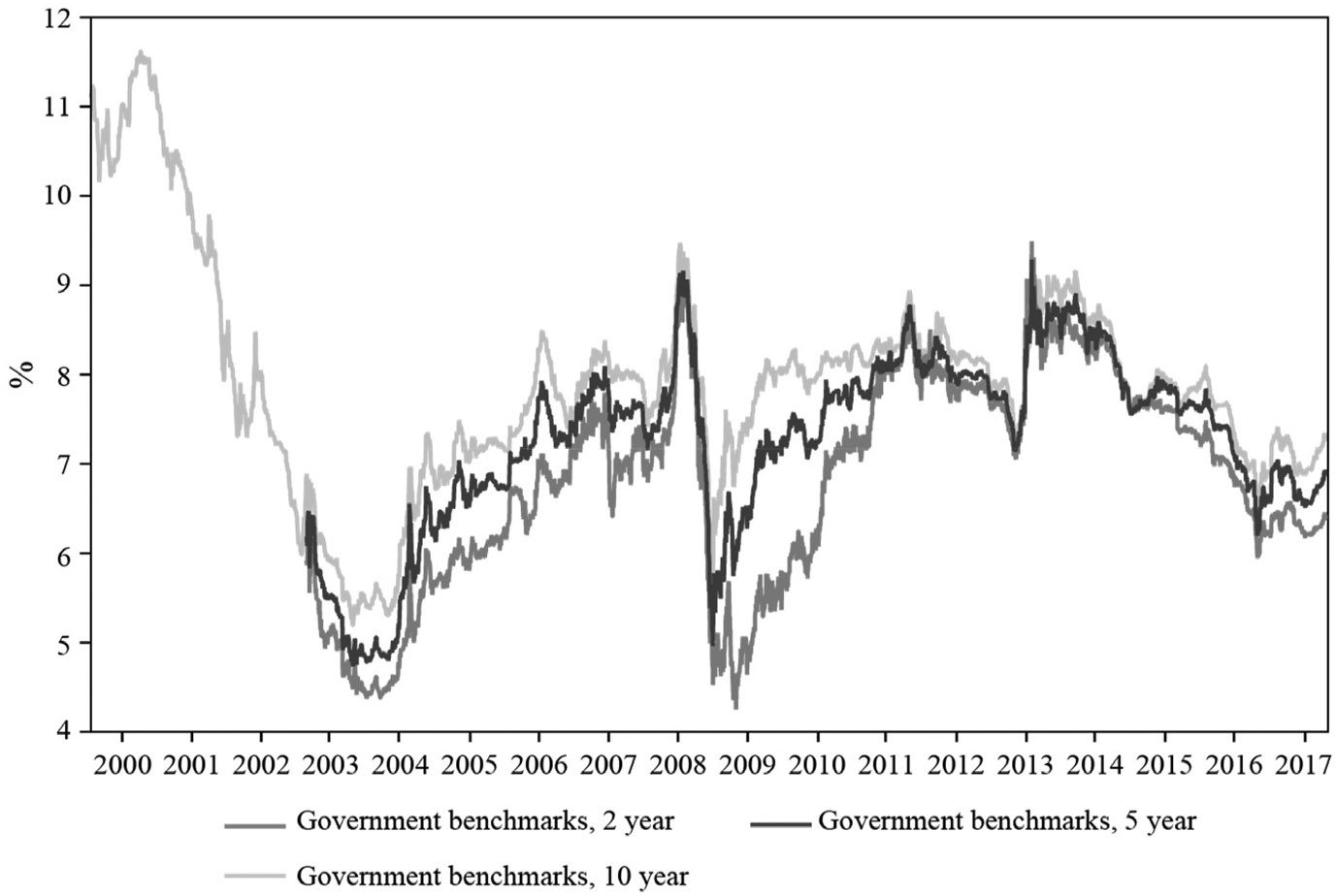

for the short-term interest rate, while the nominal yields on IGBs of various

tenors—including 2-year, 3-年, 5-年, 7-年, and 10-year maturities—are

used to represent long-term government bond yields. The RBI (2014) classifies

government securities with a maturity of less than 1 year as short-term securities,

and those with a maturity of 1 year or more as long-term securities.

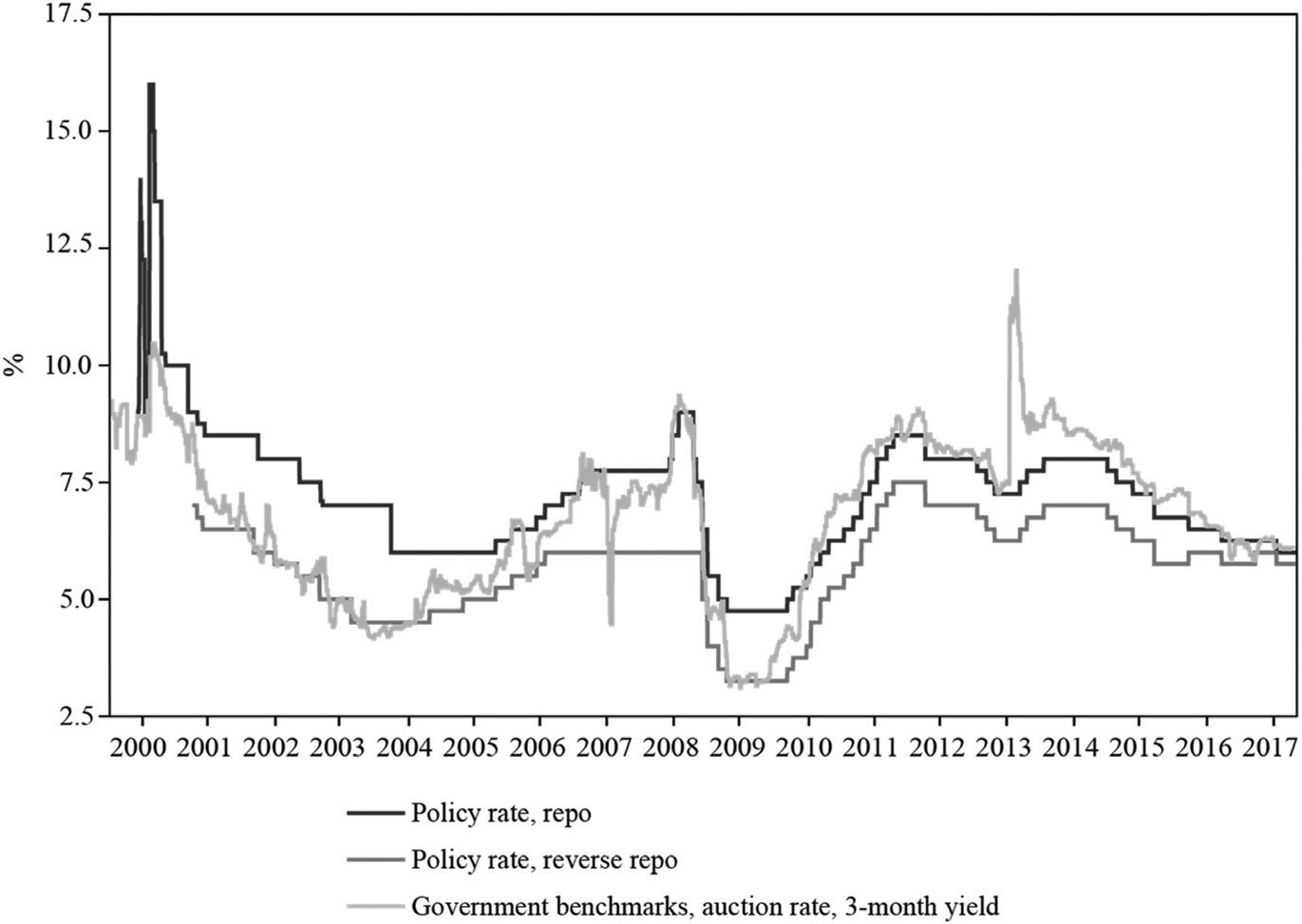

数字 5 shows the evolution of nominal yields of IGBs. 数字 6 节目

the evolution of the short-term interest rate along with the RBI’s policy rates (repo

rates and reverse repo rates). The rate of inflation is defined as the year-on-year

percentage change in the total consumer price index for all items. Growth in

industrial production is the year-on-year percentage change in the index of industrial

activity in India. The ratio of government debt to nominal GDP is used here as

the government fiscal variable. The ratio of private sector credit (from all sectors)

to nominal GDP is used to measure credit growth. The Institute for International

Monetary Affairs’ index of the volatility in global bond markets is a proxy for global

investors’ risk appetite. An increase (减少) in volatility in global bond markets

means that investors’ perception of and appetite for risk has risen (declined).

The nominal effective exchange rate, calculated by the Bank for International

Settlements, is the exchange rate used here. The data of all the variables are

collected from Macrobond’s (various years) data services. 桌子 1 提供了一个

1The dataset used in the empirical part of this paper is available upon request to bona fide researchers for the

replication and verification of the results.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 179

数字 5. The Evolution of Indian Government Bond Yields of Selected Tenors

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

来源: Macrobond. Various years. Macrobond subscription services (七月访问 12, 2017).

数字 6. The Evolution of Policy Rates and Short-Term Interest Rates in India

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

来源: Macrobond. Various years. Macrobond subscription services (七月访问 12, 2017).

180 Asian Development Review

桌子 1. Summary of the Data and Variables

Variable

Labels

Data Description, Date Range

Frequency

来源

Indian Short-Term Interest Rates

TB3M;

TB3M_Q

Government benchmarks,

auction rate, 3-月

% yield; Jan 1999–Oct 2015;

Q1 1999–Q3 2015

日常的; converted to

Reserve Bank of India;

monthly

Macrobond converted to

quarterly

Indian Government Bond Yields

IGB2YR;

Government bond, 2-年

IGB2YR_Q

% yield; Mar 2003–Oct 2015;

Q2 2003–Q3 2015

日常的; converted to

monthly

IGB3YR;

Government bond, 3-年

日常的; converted to

IGB3YR_Q

% yield; Mar 2003–Oct 2015;

Q2 2003–Q3 2015

monthly

IGB5YR;

Government bond, 5-年

IGB5YR_Q

% yield; Mar 2003–Oct 2015;

Q2 2003–Q3 2015

日常的; converted to

monthly; converted

to quarterly

Clearing Corporation of

印度; Macrobond

converted to quarterly

Clearing Corporation of

印度; Macrobond

converted to quarterly

Clearing Corporation of

印度; Macrobond

IGB7YR;

Government bond, 7-年

日常的; converted to

Clearing Corporation of

IGB7YR_Q

% yield; Mar 2003–Oct 2015;

Q2 2003–Q2 2015

monthly; converted

to quarterly

印度; Macrobond

IGB10YR;

Government bonds, 10-年

日常的; converted to

Clearing Corporation of

IGB10YR_Q

Inflation

TCPIYOY;

TCPIYOY_Q

% yield; Jan 1999–Oct 2015;

Q1 1999–Q2 2015

monthly; converted

to quarterly

印度; Macrobond

印度, consumer price index,

Monthly; converted

全部的, % 改变, year on year;

Jan 2007–Oct 2015;

Q1 2007–Q2 2015

to quarterly

The Economist;

Macrobond

Economic Activity

IPIYOY;

Industrial production,

IPIYOY_Q

% 改变, year on year;

Jan 1999–Oct 2015; Q1 1999–

Q2 2015

Government Fiscal Variable

DRATIO_Q

Government debt, % of nominal

GDP; Q1 1999–Q2 2015

Monthly; converted

Central Statistical

to quarterly

Organisation, 印度;

Macrobond

季刊

Indian Ministry of

Commerce and Industry;

Macrobond

Bank for International

Settlements; Macrobond

Credit Growth

CREDIT

Credit from all sectors to the

私营部门, % of nominal

GDP; Jan 1999–Dec 2015

季刊; converted

to monthly using

cubic interpolation

Investors’ Risk Appetite

RISK

Global bond market volatility

指数; Jan 1999–Dec 2015

日常的; converted to

Institute for International

monthly

Monetary Affairs;

Macrobond

Exchange Rate

NEER

Nominal effective exchange rate

Monthly

指数, broad; Jan 1999–

Dec 2015

Bank for International

Settlements; Macrobond

GDP = gross domestic product, Q = quarter.

来源: Authors’ compilation.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 181

summary of the data and detailed descriptions of the variables. The monthly

time series dataset runs from March 1999 to October 2015, while the quarterly

dataset includes time series variables from the third quarter of 2003 to the second

quarter of 2015.

Both monthly and quarterly data are used to examine the determinants of

nominal yields of long-term government bonds. Indian government fiscal data is

available only in quarterly form. 因此, the debt-to-GDP ratio is included only in

the quarterly equations.

乙.

Behavioral Equations

A set of behavioral equations for monthly data and for quarterly data are

constructed in concordance with the model based on the Keynesian framework

presented earlier. These behavioral equations readily lend themselves to empirical

testing. The specific-to-general approach is deployed here. For the monthly dataset,

the long-term government bond yields are first regressed individually with the

short-term interest rate, inflation, and the growth rate of industrial production.

The dependent variables are then regressed with the short-term interest rate and

inflation, and the short-term interest rate and growth rate. In the general form

of the behavioral equation, the long-term interest rate is determined by all three

explanatory variables including the short-term interest rate, rate of inflation, 和

growth rate. The general equation takes the following form:

rLT = α1 + α2r1 + α3π1 + α4g1

(3)

The same approach is used when the quarterly dataset is employed to

examine the determinants of long-term bond yields in India. 然而, 去理解

the effects of the government fiscal variable on government bond yields, the ratio

of government debt to nominal GDP is included in the general equation of the

quarterly dataset. 因此, the behavioral equation can be written in the following

方式:

rLT = z1 + z2r1 + z3π1 + z4g1 + z5v1

(4)

C.

Econometric Methodology

The first step is to examine the nature of the data. The presence of unit roots

in most macroeconomic variables is fairly common (Nelson and Plosser 1982).

因此, estimating the long-run relationships of stationary variables using standard

cointegration techniques (例如, Johansen cointegration) is inconsistent. 所以,

unit root tests on the variables used in this paper are imperative. Conventional

research has used both the Augmented Dickey–Fuller (ADF) (Dickey and Fuller

1979, 1981) and the Phillips–Perron (PP) (Phillips and Perron 1988) tests to

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

182 Asian Development Review

桌子 2. Unit Root Tests for Monthly Variables

Variable

DFGLS

−1.29

−1.76*

−1.26

−2.01**

−1.26

−2.44**

−1.27

−2.74***

−1.57

−2.15**

−1.63*

−9.47***

−1.92*

−0.97

0.30

−0.98

0.48

−0.79*

−4.93***

−0.97

ADF

−1.72

−11.57***

−1.81

−7.60***

−1.95

−7.87***

−2.06

−7.96***

−2.57

−17.09***

−1.89

−9.51***

−4.67***

−9.73***

−1.54

−2.48

−0.52

−11.21***

−4.93***

−17.18***

PP

−1.86

IGB2YR

−11.57***

(西德:5)IGB2YR

−1.97

IGB3YR

(西德:5)IGB3YR

−11.54***

−2.03

IGB5YR

−11.38***

(西德:5)IGB5YR

−2.06

IGB7YR

−11.18***

(西德:5)IGB7YR

−2.58

TB3M

−17.13***

(西德:5)TB3M

−1.99

TCPIYOY

−9.48***

(西德:5)TCPIYOY

−13.66***

IPIYOY

−47.57***

(西德:5)IPIYOY

−1.64

CREDIT

−6.99***

(西德:5)CREDIT

−0.27

NEER

−11.04***

(西德:5)NEER

−4.86***

RISK

−19.01***

(西德:5)RISK

ADF = Augmented Dickey–Fuller, CREDIT = credit to the private sector as percentage of

GDP, DFGLS = Dickey–Fuller Generalized Least Squares, IGB2YR = 2-year government

bond yield, IGB3YR = 3-year government bond yield, IGB5YR = 5-year government bond

yield, IGB7YR = 7-year government bond yield, IPIYOY = year-on-year percentage change

in industrial production, NEER = nominal effective exchange rate, PP = Phillips–Perron,

RISK = global bond market volatility index, TB3M = 3-month government auction rate,

TCPIYOY = year-on-year percentage change in consumer price index.

Notes: ***, **, 和 * indicate statistical significance at 1%, 5%, 和 10% 级别, 分别.

The null hypothesis of all three tests is that the series contains unit roots.

来源: 作者的计算.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

identify the existence of unit roots. Elliott, Rothenberg, and Stock (1996) proposed

the Dickey–Fuller Generalized Least Square (DFGLS) 测试, which is a modified

version of the standard ADF test. According to the DFGLS procedure, the data are

detrended before testing for stationarity. Different versions of the ADF, PP (和

no constant and trend, constant and no trend, and constant and trend), and DFGLS

测试 (with constant but without trend, and constant and trend) are applied in this

纸. All of these versions produce similar results. Due to space constraints, 仅有的

the results with constant but without trend are presented here. All remaining results

are available upon request.2 Unit root results for monthly variables are displayed

表中 2 and the results for quarterly variables are displayed in Table 3. 为了

monthly dataset, most variables are nonstationary at levels and stationary at the first

difference. The year-on-year percentage change in consumer price index is found to

be nonstationary at levels and stationary at the first difference by two out of three

2For additional results, the interested reader may want to consult the working paper version (Akram and Das

2017A) of this study and/or contact the authors.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 183

桌子 3. Unit Root Tests for Quarterly Variables

Variable

DFGLS

−1.51

−6.10***

−1.60

−6.36***

−1.72*

−6.58***

−1.81*

−6.77***

−1.59

−1.87*

−1.93*

−6.46***

−1.70*

−6.55***

−1.27

−0.87

ADF

−2.05

−7.47***

−2.27

−8.06***

−2.54

−8.51***

−2.72

−6.81***

−2.16

−8.52***

−2.36

−6.56***

−4.64***

−6.53***

−2.21

−2.60*

PP

−2.05

IGB2YR_Q

−7.48***

(西德:5)IGB2YR_Q

−2.14

IGB3YR_Q

(西德:5)IGB3YR_Q

−8.36***

−2.30

IGB5YR_Q

−9.59***

(西德:5)IGB5YR_Q

−2.47

IGB7YR_Q

−10.14***

(西德:5)IGB7YR_Q

−2.57

TB3M_Q

−8.60***

(西德:5)TB3M_Q

−2.44

TCPIYOY_Q

−6.65***

(西德:5)TCPIYOY_Q

−4.58***

IPIYOY_Q

−14.18***

(西德:5)IPIYOY_Q

−4.00***

DRATIO_Q

−11.21***

(西德:5)DRATIO_Q

ADF = Augmented Dickey–Fuller, DFGLS = Dickey–Fuller Generalized Least Squares,

DRATIO_Q = government debt as percentage of nominal gross domestic product,

IGB2YR_Q = 2-year government bond yield, IGB3YR_Q = 3-year government bond yield,

IGB5YR_Q = 5-year government bond yield, IGB7YR_Q = 7-year government bond yield,

IPIYOY_Q = year-on-year percentage change in industrial production, PP = Phillips–Perron,

TB3M_Q = 3-month government auction rate, TCPIYOY_Q = year-on-year percentage

change in consumer price index.

Notes: ***, **, 和 * indicate statistical significance at 1%, 5%, 和 10% 级别, 分别.

The null hypothesis of all three tests is that the series contains unit roots.

来源: 作者的计算.

测试. The year-on-year percentage change in industrial production (IPIYOY) 和

the global bond market volatility index are stationary at levels. 因此, most variables

are integrated of order one, 我(1). All three tests suggest that IPIYOY is stationary at

级别; 那是, 我(0). Similar results are found for the quarterly variables. 政府

bond as a percentage of GDP is found to be stationary at levels by the PP test,

and nonstationary at levels by the ADF and DFGLS tests. 所以, all quarterly

variables are either I(0) or I(1).

Given the results from the unit root tests, it is appropriate to estimate

the long-run cointegrating relationships using the autoregressive distributive lag

(ARDL) proposed by Pesaran and Shin (1998) and Pesaran, Shin, 和史密斯

(2001). The ARDL bounds test approach is based on the ordinary least squares

estimation of a conditional unrestricted error correction model for cointegration

分析. The ARDL technique is more appealing than the Johansen cointegration

技术 (Johansen and Juselius 1990) because the latter requires that the variables

are integrated of the same order of I(1). 然而, the ARDL approach is not

constrained by the outcomes of unit root tests. It is applicable irrespective of

whether the regressors in the model are purely I(0), purely I(1), or mutually

cointegrated. In the present case, most variables are I(1) with the exception

of IPIYOY and DRATIO_Q (IE。, government debt as percentage of nominal

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

184 Asian Development Review

桌子 4. Autoregressive Distributive Lag Bounds Test Results for

IGB2YR (monthly data)

方程

4.1) IGB2YR = β 0 + β 1TB3M

4.2) IGB2YR = β 2 + β 3TCPIYOY

4.3) IGB2YR = β 4 + β 5IPIYOY

4.4) IGB2YR = β 6 + β 7TB3M + β 8TCPIYOY

4.5) IGB2YR = β 9 + β 10TB3M + β 11IPIYOY

4.6) IGB2YR = β 12 + β 13TB3M + β 14TCPIYOY + β 15IPIYOY

F-statistic

3.93

2.97

1.46

6.52**

2.99

4.81*

Variable

TB3M

TCPIYOY

IPIYOY

持续的

Time period

Number of observations

Long-Run Relationships

方程 4.4

方程 4.6

0.51***

(0.04)

−0.01

(0.04)

—

3.60***

(0.48)

Dec 2006–

Oct 2015

107

0.51***

(0.05)

−0.00

(0.04)

−0.00

(0.01)

3.60***

(0.54)

Feb 2007–

Oct 2015

105

IGB2YR = 2-year government bond yield, IPIYOY = year-on-year percentage change in

industrial production, TB3M = 3-month government auction rate, TCPIYOY = year-on-year

percentage change in consumer price index.

Notes: ***, **, 和 * represent 1%, 5%, 和 10% levels of significance, 分别. 标准

errors are in parentheses. Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10%

levels of significance, 分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%,

和 10% levels of significance, 分别.

来源: 作者的计算.

GDP), which are I(0). 而且, the ARDL technique allows different variables

to take different optimal numbers of lags, while this is not permitted in the

Johansen cointegration approach. 所以, the ARDL technique, 这将

accommodate both I(0) 和我(1) 变量, is used in this paper to estimate the

long-run relationships between long-term government bond yields and other control

变量.

IV. Empirical Results

A. Monthly Results

The ARDL bounds test results generated from monthly variables are

presented in Tables 4–8. When the short-term interest rate is included with inflation,

in most cases the computed F-statistic based on a Wald test exceeds the upper

bound value at the 5% 等级. In the case of the 2-year government bond yield,

the computed F-statistic exceeds the upper bound value at the 10% level when the

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 185

桌子 5. Autoregressive Distributive Lag Bounds Test Results for

IGB3YR (monthly data)

方程

5.1) IGB3YR = β 16 + β 17TB3M

5.2) IGB3YR = β 18 + β 19TCPIYOY

5.3) IGB3YR = β 20 + β 21IPIYOY

5.4) IGB3YR = β 22 + β 23TB3M + β 24TCPIYOY

5.5) IGB3YR = β 25 + β 26TB3M + β 27IPIYOY

5.6) IGB3YR = β 28 + β 29TB3M + β 30TCPIYOY + β 31IPIYOY

F-statistic

4.60

2.64

2.03

8.37***

3.70

6.20**

Long-Run Relationships

Variable

方程 5.4

方程 5.6

TB3M

TCPIYOY

IPIYOY

持续的

Time period

Number of observations

0.39***

(0.04)

−0.01

(0.04)

—

4.74***

(0.47)

Dec 2006–

Oct 2015

107

0.38***

(0.05)

−0.01

(0.04)

−0.01

(0.01)

4.81***

(0.55)

Feb 2007–

Oct 2015

105

IGB3YR = 3-year government bond yield, IPIYOY = year-on-year percentage change in

industrial production, TB3M = 3-month government auction rate, TCPIYOY = year-on-year

percentage change in consumer price index.

Notes: *** 和 ** represent 1% 和 5% levels of significance, 分别. Standard errors are

in parentheses. Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10% levels of

significance, 分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%, 和 10%

levels of significance, 分别.

来源: 作者的计算.

short-term rate is included in the equation with both inflation and the industrial

production index (方程 4.6). The null hypothesis of no cointegration is rejected

whenever the F-statistic value is higher than the upper bound value. This analysis

confirms the presence of a long-run relationship among long-term government bond

yields, the short-term interest rate, the rate of inflation, and the growth of industrial

生产. It enables the estimation of the long-run coefficients of the short-term

interest rate and other control variables. The coefficients of the short-term interest

rate are always positive and statistically significant at the 1% 等级. The size of this

coefficient tends to be smaller as the tenor of the government bond rises. 这些

results suggest that in the long run the short-term interest rate strongly influences

long-term government bond yields in India.

乙.

Quarterly Results

Estimated results using quarterly data are presented in Tables 9–13. 什么时候

the short-term 3-month interest rate is included with inflation and the ratio of

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

186 Asian Development Review

桌子 6. Autoregressive Distributive Lag Bounds Test Results for

IGB5YR (monthly data)

方程

6.1) IGB5YR = β 32 + β 33TB3M

6.2) IGB5YR = β 34 + β 35TCPIYOY

6.3) IGB5YR = β 36 + β 37IPIYOY

6.4) IGB5YR = β 38 + β 39TB3M + β 40TCPIYOY

6.5) IGB5YR = β 41 + β 42TB3M + β 43IPIYOY

6.6) IGB5YR = β 44 + β 45TB3M + β 46TCPIYOY + β 47IPIYOY

F-statistic

3.84

3.65

2.37

10.56***

4.08

7.74**

Variable

TB3M

TCPIYOY

IPIYOY

持续的

Time period

Number of observations

Long-Run Relationships

方程 6.4

方程 6.6

0.26***

(0.04)

−0.00

(0.04)

—

5.86***

(0.43)

Dec 2006–

Oct 2015

107

0.25***

(0.04)

−0.00

(0.04)

−0.01

(0.01)

5.98***

(0.53)

Feb 2007–

Oct 2015

105

IGB5YR = 5-year government bond yield, IPIYOY = year-on-year percentage change in

industrial production, TB3M = 3-month government auction rate, TCPIYOY = year-on-year

percentage change in consumer price index.

Notes: *** 和 ** represent 1% 和 5% levels of significance, 分别. Standard errors are

in parentheses. Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10% levels of

significance, 分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%, 和 10%

levels of significance, 分别.

来源: 作者的计算.

government debt to nominal GDP, the computed F-statistic value is mostly higher

than the upper bound value. Long-run coefficients of the short-term interest rate

are positive when significant. The magnitude of this coefficient lies between 0.13

和 0.53. The coefficient of the ratio of government debt to nominal GDP is mostly

negative and significant at the 1% 等级, suggesting that in the long run a higher debt

ratio tends to reduce the nominal yields of IGBs. This is contrary to the conventional

智慧. Quarterly data allow the use of government fiscal variables but a clear

limitation is that these results are based on a smaller number of observations.

C.

The Main Finding and Its Relevance

The main finding is that the short-term interest rate is a key driver of the

long-term interest rate on IGBs in both the short run and the long run. This finding

has important policy implications. 例如, it suggests that the RBI’s monetary

policy decisions not only have an immediate effect on the long-term interest

rate and the Treasury yield curve, but also on the direction and the level of the

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 187

桌子 7. Autoregressive Distributive Lag Bounds Test Results for

IGB7YR (monthly data)

方程

7.1) IGB7YR = β 48 + β 49TB3M

7.2) IGB7YR = β 50 + β 51TCPIYOY

7.3) IGB7YR = β 52 + β 53IPIYOY

7.4) IGB7YR = β 54 + β 55TB3M + β 56TCPIYOY

7.5) IGB7YR = β 57 + β 58TB3M + β 59IPIYOY

7.6) IGB7YR = β 60 + β 61TB3M + β 62TCPIYOY + β 63IPIYOY

F-statistic

4.02

5.63

2.59

10.60***

4.09

7.70**

Variable

TB3M

TCPIYOY

IPIYOY

持续的

Time period

Number of observations

Long-Run Relationships

方程 7.2

方程 7.4

方程 7.6

—

0.03

(0.08)

—

7.71***

(0.62)

Dec 2006–

Oct 2015

107

0.19***

(0.03)

0.02

(0.04)

—

6.40***

(0.43)

Dec 2006–

Oct 2015

107

0.18***

(0.04)

0.01

(0.04)

−0.01

(0.01)

6.53***

(0.52)

Feb 2007–

Oct 2015

105

IGB7YR = 7-year government bond yield, IPIYOY = year-on-year percentage change in

industrial production, TB3M = 3-month government auction rate, TCPIYOY = year-on-year

percentage change in consumer price index.

Notes: *** 和 ** represent 1% 和 5% levels of significance, 分别. Standard errors are

in parentheses. Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10% levels of

significance, 分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%, 和 10%

levels of significance, 分别.

来源: 作者的计算.

long-term interest rate over a longer horizon. The results obtained are robust.

Additional regressions estimated in Appendix 2 show that the coefficient of the

short-term interest rate is positive and statistically significant, at least at the 5%

等级, even after controlling for variables such as credit growth, global investors’

risk appetite, and the nominal effective exchange rate. 所以, the main finding

that the short-term interest rate is the most important determinant of long-term bond

yields does not change with adjustments to the specifications.

These results reinforce the findings in Akram and Das’ (2015a and 2015b)

recent studies on IGBs in which they report that changes in the short-term interest

rate are important determinants of changes in long-term government bond yields in

印度. Whereas Akram and Das (2015a and 2015b) established the results for the

short run, the current study extends this for the long run.

V. Policy Implications and Conclusion

The empirical results reported here support Keynes’ conjecture that the

central bank’s actions, through its influence on the short-term interest rate and its use

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

188 Asian Development Review

桌子 8. Autoregressive Distributive Lag Bounds Test Results for

IGB10YR (monthly data)

方程

8.1) IGB10YR = β 64 + β 65TB3M

8.2) IGB10YR = β 66 + β 67TCPIYOY

8.3) IGB10YR = β 68 + β 69IPIYOY

8.4) IGB10YR = β 70 + β 71TB3M + β 72TCPIYOY

8.5) IGB10YR = β 73 + β 74TB3M + β 75IPIYOY

8.6) IGB10YR = β 76 + β 77TB3M + β 78TCPIYOY + β 79IPIYOY

F-statistic

4.73

7.51**

3.60

9.42***

3.07

6.83**

Variable

TB3M

TCPIYOY

IPIYOY

持续的

Time period

Number of observations

Long-Run Relationships

方程 8.2

方程 8.4

方程 8.6

—

0.04

(0.05)

—

7.74***

(0.45)

Dec 2006–

Oct 2015

107

0.14***

(0.04)

0.03

(0.04)

—

6.87***

(0.44)

Dec 2006–

Oct 2015

107

0.13***

(0.04)

0.02

(0.04)

−0.01

(0.01)

6.99***

(0.53)

Feb 2007–

Oct 2015

105

IGB10YR = 10-year government bond yield, IPIYOY = year-on-year percentage change in

industrial production, TB3M = 3-month government auction rate, TCPIYOY = year-on-year

percentage change in consumer price index.

Notes: *** 和 ** represent 1% 和 5% levels of significance, 分别. Standard errors are

in parentheses. Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10% levels of

significance, 分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%, 和 10%

levels of significance, 分别.

来源: 作者的计算.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1

6

4

4

2

2

4

A

d

e

v

_

A

_

0

0

1

2

7

p

d

/

.

桌子 9. Autoregressive Distributive Lag Bounds Test Results for IGB2YR_Q

(quarterly data)

方程

9.1) IGB2YR_Q = γ 0 + γ 1TB3M_Q + γ 2DRATIO_Q

9.2) IGB2YR_Q = γ 3 + γ 4TCPIYOY_Q + γ 5DRATIO_Q

9.3) IGB2YR_Q = γ 6 + γ 7IPIYOY_Q + γ 8DRATIO_Q

9.4) IGB2YR_Q = γ 9 + γ 10TB3M_Q + γ 11TCPIYOY_Q + γ 12DRATIO_Q

9.5) IGB2YR_Q = γ 13 + γ 14TB3M_Q + γ 15IPIYOY_Q + γ 16DRATIO_Q

9.6) IGB2YR_Q = γ 17 + γ 18TB3M_Q + γ 19TCPIYOY_Q + γ 20IPIYOY_Q

+ γ 21DRATIO_Q

F-statistic

2.67

1.68

2.21

1.16

2.03

1.01

DRATIO_Q = government debt as percentage of nominal gross domestic product, IGB2YR_Q = 2-year

government bond yield, IPIYOY_Q = year-on-year percentage change in industrial production, TB3M_Q

= 3-month government auction rate, TCPIYOY_Q = year-on-year percentage change in consumer price

指数.

笔记: Lower bound values are 6.84, 4.94, 和 4.04 为了 1%, 5%, 和 10% levels of significance,

分别. Upper bound values are 7.84, 5.73, 和 4.78 为了 1%, 5%, 和 10% levels of significance,

分别.

来源: 作者的计算.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Long-Run Determinants of Indian Government Bond Yields 189

桌子 10. Autoregressive Distributive Lag Bounds Test Results for IGB3YR_Q

(quarterly data)

方程

10.1) IGB3YR_Q = γ 22 + γ 23TB3M_Q + γ 24DRATIO_Q

10.2) IGB3YR_Q = γ 25 + γ 26TCPIYOY_Q + γ 27DRATIO_Q

10.3) IGB3YR_Q = γ 28 + γ 29IPIYOY_Q + γ 30DRATIO_Q

10.4) IGB3YR_Q = γ 31 + γ 32TB3M_Q + γ 33TCPIYOY_Q + γ 34DRATIO_Q

10.5) IGB3YR_Q = γ 35 + γ 36TB3M_Q + γ 37IPIYOY_Q + γ 38DRATIO_Q

10.6) IGB3YR_Q = γ 39 + γ 40TB3M_Q + γ 41TCPIYOY_Q + γ 42IPIYOY_Q

+ γ 43DRATIO_Q

F-statistic

5.51**

2.19

2.51

6.17**

2.21

1.09

Variable

TB3M_Q

TCPIYOY_Q

IPIYOY_Q

DRATIO_Q

持续的

Time period

Number of observations

Long-Run Relationships

方程 10.1

方程 10.4

0.53***

(0.07)

—

—

−2.39***

(0.82)

7.36***

(1.55)

Q3 2003–

Q2 2015

48

0.44***

(0.03)

0.00

(0.03)

—

0.69

(0.61)

3.21***

(0.85)

Q1 2007–

Q2 2015

34

DRATIO_Q = government debt as percentage of nominal gross domestic product, IGB3YR_Q = 3-year

government bond yield, IPIYOY_Q = year-on-year percentage change in industrial production, TB3M_Q =

3-month government auction rate, TCPIYOY_Q = year-on-year percentage change in consumer price index.

Notes: *** 和 ** represent 1% 和 5% levels of significance, 分别. Standard errors are in parentheses.

Lower bound values are 5.15, 3.79, 和 3.17 为了 1%, 5%, 和 10% levels of significance, 分别. Upper

bound values are 6.36, 5.52, 和 4.14 为了 1%, 5%, 和 10% levels of significance, 分别.

来源: 作者的计算.

of the tools of monetary policy, are the main drivers of the long-term interest rate.

以印度为例, the actions of the RBI affect the long-term interest rate. 这

long-term interest rate on IGBs is positively associated with the short-term interest

rate on Indian Treasury bills after controlling for the relevant variables such as the

rate of inflation, growth of industrial production, and debt ratio. A higher (降低)

long-term interest rate on IGBs is associated with a higher (降低) 短期

interest rate, 更高 (降低) rate of inflation, and faster (slower) pace of industrial

生产. The results show that a higher level of government indebtedness does

not have an adverse effect on IGBs’ nominal yields, contrary to the conventional

看法. These findings concur with the results obtained in Akram and Das’ (2015A

and 2015b) studies of the short-term dynamics of IGBs. The findings also align with

those obtained in studies by Chakraborty (2012 和 2016) and Vinod, Chakraborty,

and Karun (2014), which use quite different econometric and statistical methods.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

6

1

1

6

8

1