The Effects of Formalization on Small and

Medium-Sized Enterprise Tax Payments:

Panel Evidence from Viet Nam

Amadou Boly∗

Do firms pay more taxes after formalization? The answer to this question is

nontrivial. Tax noncompliance can be a persistent behavior among formerly

informal firms. Analyzing the relationship between formalization and tax

payments can also be challenging if nonswitching and switching firms have

different characteristics. I use a panel dataset built from five small and

medium-sized enterprise surveys conducted in Viet Nam from 2005 到 2013.

By comparing nonswitching informal firms to switchers, I show that switchers

are more likely to pay taxes and to pay a higher amount, thereby confirming

heterogeneity. By comparing switchers before and after formalization, I find

that formalization increases tax payment likelihood by 20% and the tax amount

paid by 93%. A control function approach indicates that my results are

robust to potential endogeneity of formalization. 所以, this paper provides

supportive evidence for a key public policy rationale to promote formalization:

increased tax revenues.

关键词: formalization, 税收, Viet Nam

JEL codes: D22, O12, O17

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

我. 介绍

Existing research has mainly focused on the private costs and benefits

of formalization for informal firms, with available evidence suggesting that

formalization can have a positive effect on firm performance (McKenzie and Sakho

2010; Fajnzylber, Maloney, and Montes-Rojas 2011; Rand and Torm 2012; Bruhn

and McKenzie 2014; 博利 2018).1 In contrast to most previous studies, 这篇论文

∗Amadou Boly: African Development Bank, Abidjan, Côte d’Ivoire. 电子邮件: a.boly@afdb.org. This article is

published here with due acknowledgement of UNU-WIDER, Helsinki, which commissioned the original research

under the project Structural Transformation and Inclusive Growth in Viet Nam. I am grateful to the Development

Economics Research Group at the University of Copenhagen for granting access to the Viet Nam data, 尤其

Finn Tarp, and to Christina Kinghan for constructing the panel dataset. I would also like to thank Robert Gillanders,

Anthony Mveyange, and Robert D. Osei, the managing editor and the anonymous referees for helpful comments and

suggestions. The views expressed here are those of the author and do not necessarily reflect those of the African

Development Bank Group. ADB recognizes “Vietnam” as Viet Nam. The usual ADB disclaimer applies.

1Formalization, which is viewed as a deliberate private decision by the firm taken after cost–benefit analysis,

occurs when its perceived net benefits are positive (Maloney 2004; De Mel, 麦肯齐, and Woodruff 2013).

Asian Development Review, 卷. 37, 不. 1, PP. 140–158

https://doi.org/10.1162/adev_a_00144

© 2020 Asian Development Bank and

Asian Development Bank Institute.

在知识共享下发布

归因 3.0 国际的 (抄送 3.0) 执照.

The Effects of Formalization on SME Tax Payments in Viet Nam 141

asks whether a government can also benefit from formalization through additional

tax payments resulting from firms opting out of the informal sector.

Tax payments are costs to firms, and these costs will increase as a direct

consequence of formalization only if there is (partial or full) compliance with

formal tax regulations. 然而, noncompliance with formal tax or labor regulations can

persist among formerly informal firms; noncompliance is a common phenomenon

even among formal firms, including in member countries of the Organisation

for Economic Co-operation and Development (经合组织 2008).2 In consequence,

the claim that formalization increases government revenues is ultimately an

empirical question, the answer to which can strengthen (或不) a key public policy

rationale for promoting the formalization of small and medium-sized enterprises

(中小企业).3

Analyzing the effects of formalization on informal firms is challenging due to

potential firm heterogeneity. Heterogeneity can come from the fact that firms opting

out of the informal sector have different characteristics (例如, owner capabilities and

firm preferences) compared with those that remain informal. 而且, unobserved

characteristics that affect firm outcomes may lead to formalization; 如果, 例如,

more successful firms become more visible, leading to a higher likelihood to register

formally (McKenzie and Sakho 2010; Fajnzylber, Maloney, and Montes-Rojas

2011).

To study the relationship between formalization and tax payments, I applied

regression analysis to a panel dataset compiled using five SME surveys from Viet

Nam. I restricted the dataset to informal firms that remained informal throughout

the survey periods and to informal firms that became formal at a given point

in time (referred to as switching firms or formalized firms). Informality is a

multidimensional concept that is difficult to define. 然而, for my purpose,

formal firms are defined as those that registered to pay tax (obtained a tax code),

which is a commonly used indicator of formality in the literature (McKenzie and

Sakho 2010, Rand and Torm 2012).4

McKenzie and Sakho (2010) hypothesize that a profit-maximizing firm becomes formal if and only if the expected

present discounted value of the net benefits from doing so outweighs the upfront costs:

时间(西德:2)

δt E(πF,t − πI,t ) + θlaw-abiding > CMoney + CTime + CInformation

t=1

where πF,t denotes the firm’s profits if it is formally registered at time t, and πI,t denotes the firm’s profits if it is not

formally registered at time t. θlaw-abiding denotes the utility benefit to firm owners from obeying the law and feeling

they are contributing to national welfare through paying taxes. CMoney, CTime, and CInformation denote the monetary, 时间,

and information costs of registering, 分别.

2See also Basu, Chau, and Kanbur (2010) and Tedds (2010).

3See Bruhn and McKenzie (2014), who consider that the claim that formalization is socially optimal because

it increases government revenues and reinforces a culture of respecting the rule of the law, requires more research.

4An operational definition based on business registration would be consistent with the International Labour

Organization’s (2003) definition of informal sector enterprises, which are basically “unregistered and/or small-scale

private unincorporated enterprises that produce goods or services for sale or barter.” Other criteria of informal

employment include employment contract registration, provision of social security protection, and size of the

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

142 Asian Development Review

然而, the absence of registration does not mean that the informal sector

is not taxed, as a nonnegligible fraction of informal firms pay some sort of taxes

in Viet Nam, albeit mostly local taxes (Cling, Razafindrakoto, and Roubaud 2011,

p. 33).5 It is therefore important to ascertain that formalization leads to additional

tax payments by switching firms beyond and above what was already paid.

Using the formal status variable (status equals 0 if a firm is informal and 1

if formal), I constructed a variable called switcher, which equals 1 for all years in

which a switching firm has been observed in my sample, including the years before

formalization, 和 0 if the firm remained informal throughout the survey periods.

The switcher variable, as firm-type fixed effects, allows for capturing heterogeneity

between firms remaining informal and firms that switched out of the informal

sector at some point. 因此, when included in my regression, the variable

地位, which takes a value of 1 only for switching firms after they have formalized,

captures the net effect of formalization on switching firms.

formalization,

By comparing nonswitching informal firms to switchers,

I confirm

heterogeneity between switching firms and nonswitching firms regarding tax

付款: switchers paid a significantly higher amount of taxes than nonswitchers.

然后, by comparing switchers before and after

I find that

formalization increases the likelihood of tax payment (经过 20%) and the amount

of taxes (经过 93%) relative to preformalization levels. This significant increase

in tax payments persists both in the short and long term. Using a control

function approach, I show that my results are robust to potential endogeneity of

formalization. I also find that the increase in tax payments is mainly driven by

a significant increase in the payment of taxes such as license fees or import and

export taxes, but not in the payment of revenue taxes that are arguably more difficult

to collect. Firm size, previous performance, and compliance inspection all have a

positive relationship with both the amount and likelihood of tax payments.

The remainder of this paper is organized as follows. Section II briefly

literature on the effects of

presents an overview of the existing empirical

formalization. I describe my dataset in section III and explain the empirical

approach in section IV. Section V presents the main results and section VI

concludes.

二. Literature Review

The literature on the relationship between formalization and firm

performance has mainly focused on the private benefits for a firm. Comparing

employer (Henley, Arabsheibani, and Carneiro 2009). 然而, compared to having a tax code, these other definitions

may not be best fits, given that I am seeking whether formalization leads to additional tax payments.

5See also Olken and Singhal (2011) for a discussion of informal taxation in 10 developing economies,

including Viet Nam.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 143

firms that were created immediately before and after a business tax reduction and

simplification scheme in Brazil, Fajnzylber, Maloney, and Montes-Rojas (2011)

find that this scheme led to increased levels of registration and to higher revenues,

profits, and employment among registered firms. 同样地, 夏尔马 (2014) suggests

that registration leads to significant gains in both sales and value added per

employee in India. In Bolivia, McKenzie and Sakho (2010) analyze the effects

of formalization on firm profits, using the physical distance between a firm and

the tax office as an instrument. The assumption is that being closer to a tax office

increases the probability of registration. Their findings suggest that the effect of

tax registration is positive but heterogeneous. Related to the research question in

the current paper, McKenzie and Sakho (2010) also show that registered firms are

more likely to pay taxes, but not significantly more likely to be paying a larger share

of their profits as taxes.

In contrast to most previous cross-section studies, Rand and Torm (2012)

use the same panel data as in this study, but only for 2007 和 2009. 他们的

results indicate that registration leads to an increase in profits and investments for

Vietnamese SMEs. 博利 (2018) shows that becoming formal can further increase

gross profits and the value added of switchers compared with preformalization

级别, both in the short and medium term. The present study is closest to Boly

(2018) as it uses the same dataset and empirical approach, while focusing on

analyzing the relationship between formalization and tax payments. As mentioned

previously, the majority of the existing literature focuses on the private benefits of

formalization for a firm, leaving an evidence gap on the potential social benefits,

specifically those accruing to governments.

三、. 数据

The description of the dataset used in this study parallels that in Boly

(2018), restricted to informal and switching firms. The dataset comes from SME

surveys conducted in Viet Nam in 2005, 2007, 2009, 2011, 和 2013. The surveys,

which were conducted by the Central Institute for Economic Management and the

University of Copenhagen, cover about 2,500 firms in each year. They were carried

out in 10 locations in the cities of Ha Noi and Hai Phong, in Ho Chi Minh City, 和

in the rural provinces of Ha Tay, Khanh Hoa, Lam Dong, Long An, Nghe An, Phu

Tho, and Quang Nam.

The population of nonstate manufacturing enterprises was based on two data

sources from the General Statistics Office of Viet Nam (GSO): the Establishment

Census 2002 (GSO 2004) and the Industrial Survey 2004–2006 (GSO 2008). A

representative sample of registered household and nonhousehold firms was drawn

from this population, using a stratified sampling procedure. The aim was to ensure

the inclusion of an adequate number of enterprises in each province with different

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

144 Asian Development Review

ownership forms. For reasons of implementation, the survey was confined to

specific areas in each province or city. 此外, the GSO enterprise census

focused only on “visible” firms, which are those with fixed professional premises.

Informal household firms were included in the SME surveys based on

random onsite identification within the survey districts observed by the enumerator.

With such an identification approach, the informal firms included in the survey

are those operating alongside officially registered enterprises. These informal firms

may be relatively more competitive (and profitable) compared to informal firms

clustering in areas with no or very few formal firms (Rand and Torm 2012). 在这个

看待, the sample of informal firms in this study may not be fully representative of

the informal sector as a whole in Viet Nam.

Despite the aforementioned weakness, my dataset remains unique by the

number of survey years (5), number of firms, and focus on the informal sector. 我

restricted my sample to firms with at least two observations. I also excluded firms

that were formal when initially entering the sample, given that my interest is in

informal firms and whether they pay more taxes after formalization. The restricted

sample is dominated by informal nonswitchers, which account for 66% of the total

number of firms, while switchers account for 34% of the total number of firms

(Appendix Table A1.1).6

IV. Empirical Approach

To examine the relationship between formalization and tax payments, I use

the following specification:

yit = ρDS

我

+ γ Fit + βXit + λt + μi + εit

(1)

is the dependent variable; DS

where yit

i captures firm-type fixed effects (1 如果

switchers, 0 if nonswitchers); Fit indicates whether a firm has become formal or

不是 (0 if a firm is informal, 和 1 if the firm is formal); Xit represents additional

control variables; λt denotes a full set of time dummy variables; i indexes individual

firms; and t indexes time. As specified, my approach is comparable to a difference-

in-difference approach with varying treatment years.

specification

difference-in-difference

和

nonswitchers) rests on the parallel trend assumption in tax payments before

switching. A graphical check of this assumption suggests that the parallel trend

assumption holds well between 2005 和 2007 和之间 2007 和 2009, 但

switchers

(之间

这

6I assume that once a firm becomes formal it stays formal, and I recode its formality status accordingly. 在

也就是说, I do not allow a switcher to move back to the informal sector. This applies to about 4.2% of observations,

a proportion that I consider negligible. The main justification is that once a firm enters tax authorities’ records by

acquiring a tax code, it becomes very difficult for the firm to move again into informality.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 145

not between 2009 和 2011. As a robustness check, I run the above specification

for different waves of the survey (see section V.C.3).

A key feature of my approach is the construction of a switcher variable

denoted by DS

我 , using the variable Fit (0 if a firm is informal, 和 1 if the firm is

formal). If a firm has shifted out of the informal sector at any time in my survey

periods, the switcher variable equals 1 for all years in which the firm has been

observed in my sample (including the years before formalization); the switcher

variable equals 0 if the firm remained informal throughout the survey periods.

这 (informal) nonswitcher group is used as control group in my regressions. 这

inclusion of firm-type fixed effects in my main regressions (using dummy variable

DS

我 ) enables me to account for time-invariant heterogeneity between nonswitching

and switching firms. 因此, the variable Fit, which takes a value of 1 only for

switching firms after they have formalized, picks up the net effects of formalization.

然而, a known limitation of the fixed-effects approach is that endogeneity due

to time-varying omitted variables is still present, although the bias gets smaller

than with cross-sectional data. I therefore discuss robustness to endogeneity in

section V.C.2.

In addition to the previously mentioned variables, I include several control

variables that could affect firms’ decisions regarding tax payments. These control

variables are summarized in Appendix Table A1.2 for the pooled sample and by

firm type.7 The control variables include (我) gender of the owner or manager (1 如果

male, 0 否则); (二) education level of the owner or manager (0 if secondary

school has not been completed, 1 否则) to proxy for the owner’s or manager’s

人力资本; (三、) firm’s previous performance using previous year’s gross profits;

(四号) number of regular full-time employees (in logarithmic form), as well as the

square, to control for firm-size effects; (v) whether or not the firm holds a certificate

of land use rights to proxy for property rights; (六) government inspections (0 如果

the firm has not been subject to inspections in a given year, 1 否则); 和

(七) dummy variables to control for location and time factors.

V. 结果

After briefly discussing some summary statistics, I present results on the

relationship between formalization and total tax payments, my main variable of

兴趣, using a Tobit regression that considers both the binary participation

decision and the amount paid.8

7See also Rand and Torm (2012).

8The total tax payments variable is constructed as the sum of various taxes and fees, such as taxes on revenues,

license fees, import and export taxes, luxury good taxes, property taxes, and other taxes and fees.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

146 Asian Development Review

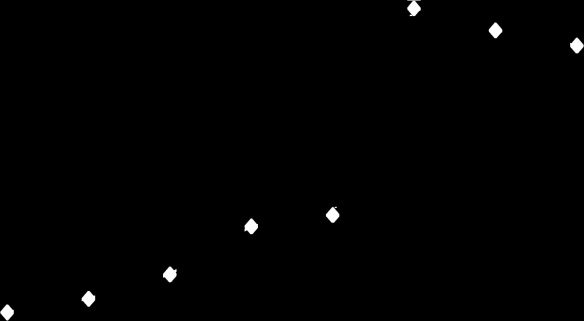

Average Total Tax Payments—Evolution around Formalization Year

笔记: Formalization year is equal to 0.

来源: Author’s calculations.

A.

Summary Statistics

As mentioned earlier, Appendix Table A1.2 describes the dependent

变量 (for the pooled sample) by firm type, 那是, nonswitchers and switchers

(and for switchers: 全面的, before switching, and after switching). I observe that

nonswitchers paid some form of taxes 57% 当时的, while switchers paid taxes

90% 当时的 (全面的), 83% of the time before switching, 和 97% 当时的

after switching. The differences are significant at the 1% level between nonswitchers

and switchers before switching on the one hand, and between switchers before and

after switching on the other hand.

The total tax payments made by switchers before switching (D1,778) 是

significantly higher than that of nonswitchers at the 1% 等级 (D334).9 Switchers

also pay a significantly higher amount of total taxes after joining the formal sector

(D3,792). 全面的, the average total tax payments of switchers (D2,883) 是关于 8.6

times higher than the total tax payments of nonswitchers (D334); switching from the

informal to the formal sector resulted in tax payments increasing more than twofold

from D1,778 to D3,792.

The figure uses an events-study graph to provide an illustration of the

evolution of tax payments for switchers. In this graph, the year of formalization is

set at 0 on the x-axis. Negative numbers refer to years in the preformalization period

and positive numbers to years in the postformalization period. Although there is an

9All monetary values are in real 1,000 Vietnamese dong (D).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

/

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 147

桌子 1. Effects of Formalization on Total Tax Payments (Tobit)

Variables: Log (1 + 税收), (Real D1,000)

模型 1 模型 2

Switcher (from informal to formal)

Switcher (after formalization)

Time since becoming formal (dummy, 2 years or less)

Time since becoming formal (dummy, 4 + 年)

Gender of owner or manager (female = 0, male = 1)

Owner or manager completed secondary school (no = 0, yes = 1)

Gross profits (previous year, 日志)

Firm size (日志 [1 + 就业])

Firm size squared (日志 [1 + 就业])

Share of female employees

Own land use right certificate, (no = 0, yes = 1)

Compliance inspections (no = 0, yes = 1)

持续的

观察结果

Number of panels

Time dummies included

Province dummies included

2.44***

(0.19)

2.36***

(0.21)

1.06***

(0.15)

1.39***

(0.14)

0.58***

(0.17)

0.01

(0.13)

0.21**

(0.09)

0.46***

(0.08)

2.10***

(0.43)

0.01

(0.13)

0.19

(0.14)

0.46***

(0.07)

2.10***

(0.51)

−0.38*** −0.38***

(0.12)

0.39

(0.24)

0.22*

(0.12)

0.73***

(0.10)

−3.87*** −3.94***

(0.73)

4,795

1,306

是的

是的

(0.11)

0.39

(0.24)

0.23*

(0.13)

0.68***

(0.14)

(0.93)

4,795

1,306

是的

是的

D = dong.

Notes: Bootstrapped standard errors in parentheses. ***p < 0.01, **p < 0.05, *p < 0.1.

Source: Author’s calculations.

increasing trend in tax payments in the preformalization period (−8; −2), I observe

a significant jump in the short term, postformalization period (0; +2); this increase

in tax payments persists in the long term (+4; +6) compared to the preformalization

period (−8; −2).

The preliminary analysis above therefore suggests that tax payments increase

after formalization.

B.

Panel Regression

I also study the relationship between formalization and tax payments using a

random effects Tobit regression (left-censored at 0). The results in Table 1 (Model 1)

show that switchers’ total tax payments are significantly higher than nonswitchers.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

/

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

148 Asian Development Review

I therefore find heterogeneity between switching and nonswitching firms; that

is, switchers tend to pay higher taxes while in the informal sector than nonswitchers

do. This heterogeneity has been typically assumed or differenced out in most of the

previous studies on formalization.

I find that

the coefficient of

is analyzed by looking at

The amount of switchers’ tax payments, both before and after they

(after

formalized,

formalization).

tax amounts

significantly compared to preformalization levels (Table 1, Model 1). For switchers,

the mean marginal effects of formalization on the expected value of the censored

outcome is about 93%, and the mean marginal effects of formalization on the

expected value of the truncated outcome is about 73%, controlling for province

and year fixed effects.

formalization increases switchers’

switcher

To study the effects of formalization over the short and long term, I use two

dummy variables that reflect the length of time since formalization. The first dummy

(short term) is 1 for firms that have been formal for 2 years or less, while the second

dummy (long term) is for firms that have been formal for 4 years or more.10 As can

be seen in Table 1 (Model 2), the increase in total tax payments is observed both in

the short and long term. However, the coefficient for total tax payments in the short

term (2 years or less after formalization) is significantly higher than the coefficient

for tax payments in the long term (4 or more years after formalization), suggesting

a decrease in total tax payments over time. Alternatively, the higher coefficients in

the short term for total tax payments may be capturing initial entry costs into the

formal sector.

Several other control variables are noteworthy in Table 1. First, lagged gross

profits have a positive and significant relationship with tax payments at the 1%

confidence level, indicating that more successful firms pay more taxes. Second,

firm size also has a positive and significant relationship with tax payments, likely

explained by the fact that it is more difficult for larger firms to hide their activities.

Finally, undergoing at least one compliance inspection is positively related to the

amount of total taxes.

C.

Robustness Check

In this section, I test the robustness of my results to measurement errors or

possible endogeneity.

10The time since switching to the formal sector is computed as follows. In the first survey year (2005), all

firms were informal. The first switchers are recorded in 2007, with formalization having taken place between 2005

and 2007. For all switching firms, I assume that formalization took place in the year of the survey. As a result, for

firms that were informal in 2005 but formal in 2007, the number of years since switching is 0 in 2007. For these firms

that switched in 2007, the number of years since switching becomes 2 in 2009, 4 in 2011, and 6 in 2013. The same

procedure is applied to firms that switched in 2009, 2011, or 2013.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

.

/

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 149

1.

Likelihood of Tax Payments

An advantage of the dataset used in this paper is the provision of hard

evidence on tax payments made by informal sector firms. However, asking about

tax payments through traditional survey techniques can be problematic as firms may

decide to misreport.11 Given these possible reporting errors, I conduct a robustness

check by using a dummy variable that equals 1 when tax payments are strictly

positive (see summary statistics in Appendix Table A1.2). This dummy dependent

variable reflects the binary participation decision to pay or not to pay taxes; it is

estimated using a random effects logit regression.

Table 2 shows that switchers’ likelihood of paying taxes is significantly

higher than nonswitchers (Model 1). The results also suggest that becoming formal

is positively and significantly associated with an increased likelihood to pay taxes

when looking at the coefficient of switcher (after formalization). Table 2 also shows

that an increased likelihood of paying taxes is observed both in the short and long

term (Model 2).

2.

Endogeneity12

This section analyzes the robustness of my results to potential endogeneity

of formalization, using a control function approach (Wooldridge 2015).

As a first step, I estimate a model of the endogenous explanatory variable:

Fit = 1 [βXit + ωIit + νit] = 1 [δZit + νit]

(2)

where 1[.] is the binary indicator function; Fit, the dependent variable, is a dummy

variable that takes a value of 1 if a firm is formal and 0 otherwise; Xit are control

variables described earlier in section IV; Iit corresponds to a set of exogenous

variables that are omitted from equation (1) and that are partially correlated with

formalization; Zit = (Xit, Iit ); and νit is an error term.

As a second step, I compute generalized residuals, ˆrit, based on results

obtained from equation (2) as follows:

ˆrit = Fitλ

(cid:4)

(cid:3)

ˆδZit

− (1 − Fit )λ

(cid:4)

(cid:3)

− ˆδZit

(3)

where λ(.) = ϕ(.)/(cid:13)(.) is the inverse Mills ratio.

As a third and final step, I reestimate equation (1) by adding ˆrit as an

additional regressor to control for endogeneity.

To construct Iit, I take the annual provincial-level averages for the following

two binary variables: access to powered equipment (1 if with access, 0 otherwise),

11For example, the World Bank Enterprise Surveys ask about “compliance of similar firms to yourself” to

limit the threat of getting wrong responses.

12See also Boly (2018).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

/

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

150 Asian Development Review

Table 2. Effects of Formalization on Total Tax Payments (Logit)

Variables: Dummy Variable (1 if Taxes > 0)

模型 1 模型 2

Switcher (from informal to formal)

Switcher (after formalization)

Time since becoming formal (dummy, 2 年)

Time since becoming formal (dummy, 4 + 年)

Gender of owner or manager (female = 0, male = 1)

Owner or manager completed secondary school (no = 0, yes = 1)

Gross profits (previous year, 日志)

Firm size (日志 [1 + 就业])

Firm size squared (日志 [1 + 就业])

Share of female employees

Own land use right certificate (no = 0, yes = 1)

Compliance inspections (no = 0, yes = 1)

持续的

观察结果

Number of panels

Time dummies included

Province dummies included

笔记: ***p < 0.01, **p < 0.05, *p < 0.1. Source: Author’s calculations. 1.77*** (0.21) 1.72*** (0.21) 1.95*** (0.26) 3.32*** (0.50) 1.23*** (0.30) 0.02 (0.13) 0.12 (0.12) 0.33*** (0.08) 1.36*** (0.41) 0.03 (0.13) 0.10 (0.12) 0.33*** (0.08) 1.39*** (0.41) −0.29*** −0.29*** (0.11) 0.37 (0.24) 0.23* (0.12) 0.66*** (0.15) −4.07*** −4.13*** (0.82) 4,795 1,306 Yes Yes (0.11) 0.37 (0.24) 0.22* (0.13) 0.64*** (0.15) (0.82) 4,795 1,306 Yes Yes and bribe payments (1 if the firm has made any bribe payments in a given year, 0 otherwise). Here, I restrict my sample to only always-formal firms and formalized firms (i.e., switchers once they have switched), with the latter included in the year following formalization. As noted in section III, informal firms in the sample were selected based on random onsite identification in the neighborhoods of formal firms. In Viet Nam, over 80% of formal firms consider that registration is beneficial, while nearly 50% of informal firms do not see any value to it (Cling, Razafindrakoto, and Roubaud 2012). My exclusive restriction assumption is that informal firms are more likely to formalize when they can observe formal firms’ characteristics and potentially attribute those characteristics to formalization. Yet, these formal firms’ observable characteristics will not affect informal firms’ tax payment behavior. l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a d e v / a r t i c e - p d l f / / / / 3 7 1 1 4 0 1 8 4 6 7 6 3 a d e v _ a _ 0 0 1 4 4 p d . / f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 The Effects of Formalization on SME Tax Payments in Viet Nam 151 Table 3. Effects of Formality on Total Tax Payments and Likelihood to Pay Taxes—Control Function Approach Variables Switcher (from informal to formal) Switcher (after formalization) Time since becoming formal (dummy, 2 years) Time since becoming formal (dummy, 4 + years) Generalized residuals Gender of owner or manager (female = 0, male = 1) Owner or manager completed secondary school (no = 0, yes = 1) Gross profits (previous year, log) Firm size (log [1 + employment]) Firm size squared (log [1 + employment]) Share of female employees Own land use right certificate (no = 0, yes = 1) Compliance inspections (no = 0, yes = 1) Access to machinery by formal firms (province-level average of dummy: 0 = no, 1 = yes) Bribe paid by formal firms (province-level average of dummy: 0 = no, 1 = yes) Constant Observations Time dummies included Province dummies included Number of panels Log Tax (Real D1,000), Tobit Logit (1 if Taxes > 0)

(1)

2.36***

(0.19)

1.06***

(0.14)

0.00

(0.17)

0.01

(0.14)

0.19*

(0.10)

0.46***

(0.09)

2.10***

(0.43)

−0.38***

(0.11)

0.39

(0.27)

0.22*

(0.12)

0.73***

(0.16)

(2)

2.45***

(0.19)

1.44***

(0.18)

0.62***

(0.22)

−0.07

(0.17)

0.01

(0.11)

0.21*

(0.12)

0.46***

(0.08)

2.11***

(0.45)

−0.38***

(0.12)

0.39*

(0.24)

0.23*

(0.14)

0.68***

(0.13)

(1)

0.22***

(0.02)

0.06***

(0.02)

0.03

(0.02)

0.01

(0.02)

0.01

(0.01)

0.04***

(0.01)

0.19***

(0.05)

−0.04***

(0.01)

0.05*

(0.03)

0.03*

(0.01)

0.08***

(0.02)

(2)

0.23***

(0.02)

0.10***

(0.02)

0.02

(0.02)

0.02

(0.02)

0.01

(0.01)

0.01

(0.01)

0.04***

(0.01)

0.20***

(0.05)

−0.04***

(0.01)

0.05*

(0.03)

0.03

(0.02)

0.08***

(0.02)

正式的

(No = 0,

Yes = 1),

Probit

−0.12*

(0.07)

0.38***

(0.06)

0.35***

(0.06)

1.01***

(0.22)

−0.16***

(0.05)

−0.28**

(0.12)

0.01

(0.06)

−0.04

(0.06)

8.70***

(0.91)

−0.70***

(0.12)

−13.38***

(0.93)

4,795

是的

不

−3.87***

(0.92)

4,795

是的

是的

1,306

−3.94***

(0.82)

4,795

是的

是的

1,306

−0.28***

(0.10)

4,795

是的

是的

1,306

−0.28***

(0.09)

4,795

是的

是的

1,306

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

D = dong.

Notes: Bootstrapped standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

Source: Author’s calculations

The results of the first-step regression in the first columns of Table 3 (Formal,

Probit) indicate that bribes paid by a formal firm have a negative and significant

effect on the likelihood of formalization, while access to powered equipment has

152 Asian Development Review

a positive and significant effect. As a result, Iit fulfills a requirement of the control

function approach that at least one exogenous variable that is omitted from equation

(1) be partially correlated with the dependent variable in equation (2).

The results of the third step (in the control function approach described

above) are also presented in Table 3, both for the total tax amount and the likelihood

to pay tax. They suggest that endogeneity is not an issue. This provides supportive

evidence that formalization can have a positive effect on switchers’ total tax

payments and that this effect can persist over time for the amount paid but not the

likelihood to pay tax.

3.

Unbalanced Panel

This paper uses an unbalanced panel, which includes only firms with at

least two observations. However, if firms that remain informal are more likely to

drop out of the panel (as formalized firms are more visible and easier to locate

in subsequent rounds), then this would bias the estimates derived from firms that

remain in the panel. As a first robustness check to the unbalanced panel issue, I run

regressions using the full sample, or the sample of firms with at least three, four, or

five observations. In the second check, I keep firms with at least two observations

but vary the number of survey waves, starting with the first two waves in 2005 and

2007.

In all cases, the full model (including controls) is estimated. However, in

Appendix Table A2.1 (varying sample size) and Appendix Table A2.2 (varying

number of waves), I present the coefficients for only the variables switcher (from

informal to formal) and switcher (after formalization) to save space. My results

show that switching firms are different from informal nonswitchers and that the

effect of formalization is positive and significant at conventional levels for all

samples.

D.

Discussion

To explore where the increase in tax payments after formalization comes

from, I make a distinction between revenue taxes and other taxes, with the latter

obtained by excluding revenue taxes from total tax payments. Such a distinction is

motivated by the difficulty to monitor and collect income taxes compared with other

types of taxes such as license fees or import and export taxes. This difficulty partly

explains the use of presumptive taxes for taxing informal sector activities (Joshi,

Prichard, and Heady 2014; Dube and Casale 2016).

Regression analysis indicates that both the likelihood of payments and the

amount paid in revenue-related taxes and other taxes by switchers are significantly

higher after formalization (Appendix Table A2.3). However, a large share of

additional taxes after formalization appears to come from other types of taxes,

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

/

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 153

not revenue-related taxes. Indeed, switchers report only a small increase in revenue

taxes paid before and after switching, based on the sample overall average (D1,152

before switching and D1,175 after switching); while other tax payments appear

to increase significantly at more than double the amount paid in revenue-related

taxes (D625 before switching and D2,616 after switching). Such a result could

suggest that some firms formalize when they realize that in order to start importing

or exporting, they need a tax identification number to make subsequent trade-

related tax payments. To some extent, these results also confirm that revenue-related

taxes can be challenging to collect, even after formalization, compared with other

types of taxes such as license fees or import and export taxes. Arguably, collecting

trade taxes mainly requires being able to control trade flows at major entry points

(e.g., ports, airports, or land borders), while collecting income or sales taxes

requires major investments in enforcement and compliance structures throughout

the entire economy.

Overall compliance with tax obligations is another interesting aspect that

can be considered when analyzing tax payments. To obtain an estimate of the

degree of overall compliance, I compared reported total taxes paid to revenue

levels by switchers, before and after formalization. However, a precise computation

of the level of compliance would require a tax calculator, which is beyond the

scope of this paper. The results on compliance should therefore be treated with

caution.

I find that, using an overall average, the total tax-to-revenue ratio of switchers

slightly increased from 1.26% before formalization to 1.44% after formalization.13

Using fractional regression, given that the ratio of total tax to revenue is between

0 and 1, I find that the increase in the compliance level is significant at the 1%

level.14 Notably, the compliance rate of switchers, even after formalization, remains

below that of always-formal firms, which stands at 3.47% in my sample, suggesting

that switchers may still not be fully compliant with their tax obligations even after

joining the formal sector.

VI. Concluding Remarks

Using a panel dataset consisting of five waves of SME surveys in Viet Nam,

this paper analyzes the relationship between formalization and tax payments. Such

an analysis can be challenging because of potential firm heterogeneity, due to the

fact that firms choosing to formalize can have different underlying characteristics

compared with the ones that remained informal.

13These levels are in line with the lower bound of estimates (1.3%–5% of annual income) provided by

Demenet (2016, p. 40).

14The results of these calculations are available from the author upon request.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

.

/

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

154 Asian Development Review

To control for unobserved heterogeneity, I created dummy variables that

distinguish between two groups of firms in my sample: those that remain informal

and those that switch to the formal sector at some point. As a result, when

the variable status, which takes a value of 1 only for switching firms after they

have formalized, is included in my regression, it picks up only the net effects of

formalization on tax payments.

My results show that switching firms are different

from informal

nonswitching firms regarding total tax payments. Such heterogeneity is typically

assumed in most previous studies on formalization but not explicitly assessed. After

formalization, I observe a significant increase in the amount and likelihood of tax

payments, both in the short and long term. These results are mainly driven by a

significant increase in the payment of other types of taxes—such as license fees,

import and export taxes, and property taxes—not in the payment of revenue taxes.

Overall, my results are supportive of government efforts to reduce the size

of the informal sector by promoting formalization. Such efforts are likely to

result in additional revenues for governments, which is an important assumption

underpinning the public policy rationale for promoting formalization.

References

Basu, Arnab K., Nancy H. Chau, and Ravi Kanbur. 2010. “Turning a Blind Eye: Costly

Enforcement, Credible Commitment, and Minimum Wage Laws.” Economic Journal 120

(543): 244–69.

Boly, Amadou. 2018. “On the Short- and Medium-Term Effects of Formalisation: Panel Evidence

from Vietnam.” Journal of Development Studies 54 (4): 641–56.

Bruhn, Miriam, and David McKenzie. 2014. “Entry Regulation and the Formalization of

Microenterprises in Developing Countries.” World Bank Research Observer 29 (2):186–

201.

Cling, Jean-Pierre, Mireille Razafindrakoto, and François Roubaud. 2011. “The Informal

Economy in Viet Nam.” Ha Noi: International Labour Organization.

_____. 2012. “To Be or Not to Be Registered? Explanatory Factors behind Formalizing Non-

Farm Household Businesses in Vietnam.” Journal of the Asia Pacific Economy 17 (4): 632–

52.

De Mel, Suresh, David McKenzie, and Christopher Woodruff. 2013. “The Demand for, and

Consequences of, Formalization among Informal Firms in Sri Lanka.” American Economic

Journal: Applied Economics 5 (2): 122–50.

Demenet, Axel. 2016. “Insights into a Predominant and Dynamic Informal Sector: The Case of

Vietnam.” Economies and Finances, PSL Research University. English. https://tel.archives-

ouvertes.fr/tel-1587795.

Dube, Godwin, and Daniela Casale. 2016. “The Implementation of Informal Sector Taxation:

Evidence from Selected African Countries.” eJournal of Tax Research 14 (3): 601–23.

Fajnzylber, Pablo, William F. Maloney, and Gabriel V. Montes-Rojas. 2011. “Does Formality

Improve Micro-Firm Performance? Evidence from the Brazilian SIMPLES Program.”

Journal of Development Economics 94 (2): 262–76.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

/

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 155

General Statistics Office of Viet Nam (GSO). 2004. Results of Establishment Census of Vietnam

2002: Vol. 2. Business Establishments. Ha Noi: Statistical Publishing House.

_____. 2008. The Real Situation of Enterprises through the Results of Surveys Conducted in 2005,

2006, 2007. Ha Noi: Statistical Publishing House.

Henley, Andrew, G. Reza Arabsheibani, and Francisco G. Carneiro. 2009. “On Defining and

Measuring the Informal Sector: Evidence from Brazil.” World Development 37 (5): 992–

1003.

International Labour Organization. 2003. “Guidelines Concerning a Statistical Definition of

Informal Employment.” 17th International Conference of Labour Statisticians, Geneva.

Joshi, Anuradha, Wilson Prichard, and Christopher Heady. 2014. “Taxing the Informal

Economy: The Current State of Knowledge and Agendas for Future Research.” Journal

of Development Studies 50 (10): 1325–47.

Maloney, William F. 2004. “Informality Revisited.” World Development 32 (7): 1159–78.

McKenzie, David, and Seynabou Sakho. 2010. “Does It Pay Firms to Register for Taxes? The

Impact of Formality on Firm Profitability.” Journal of Development Economics 91 (1): 15–

24.

Olken, Benjamin A., and Monica Singhal. 2011. “Informal Taxation.” American Economic

Journal: Applied Economics 3 (4): 1–28.

Organisation for Economic Co-operation and Development (OECD). 2008. “Declaring Work

or Staying Underground: Informal Employment in Seven OECD Countries.” In OECD

Employment Outlook 2008. Paris.

Rand, John, and Nina Torm. 2012. “The Benefits of Formalization: Evidence from Vietnamese

Manufacturing SMEs.” World Development 40 (5): 983–98.

Sharma, Smriti. 2014. “Benefits of a Registration Policy for Microenterprise Performance in

India.” Small Business Economics 42 (1): 153–64.

Tedds, Lindsay M. 2010. “Keeping It Off the Books: An Empirical Investigation of Firms that

Engage in Tax Evasion.” Applied Economics 42 (19): 2459–73.

Wooldridge, Jeffrey M. 2015. “Control Function Methods in Applied Econometrics.” Journal of

Human Resources 50 (2): 420–45.

Appendix 1

Table A1.1. Frequency of Sample Firm Types

Overall

Between

Firm Type

Frequency

Percentage

Frequency

Percentage

Informal nonswitchers

Switchers (informal to formal)

Total

3,170

1,859

5,029

63

37

100

896

458

1,354

66

34

100

Source: Author’s calculations.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

.

/

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

156 Asian Development Review

r

e

t

f

A

g

n

i

h

c

t

i

w

S

e

r

o

f

e

B

g

n

i

h

c

t

i

w

S

)

l

a

m

r

o

F

o

t

l

a

m

r

o

f

n

I

(

s

r

e

h

c

t

i

w

S

l

l

a

r

e

v

O

s

r

e

h

c

t

i

w

s

n

o

N

D

S

n

a

e

M

N

D

S

n

a

e

M

N

D

S

n

a

e

M

N

D

S

n

a

e

M

N

e

p

y

T

m

r

i

F

y

b

s

e

l

b

a

i

r

a

V

t

n

e

d

n

e

p

e

d

n

I

d

n

a

t

n

e

d

n

e

p

e

D

f

o

s

c

i

t

s

i

t

a

t

S

y

r

a

m

m

u

S

.

2

.

1

A

e

l

b

a

T

s

e

l

b

a

i

r

a

V

t

n

e

d

n

e

p

e

D

3

1

1

1

1

,

6

2

1

0

.

2

9

7

3

,

9

6

9

0

.

2

3

4

2

3

4

2

7

6

,

5

3

3

3

.

0

8

7

7

,

1

4

3

8

.

0

2

3

4

2

3

4

3

5

4

,

7

2

9

1

.

0

3

8

8

,

2

2

0

9

.

0

2

3

4

2

3

4

0

3

0

,

1

5

7

3

.

0

9

6

5

.

0

9

.

3

3

3

4

7

8

4

7

8

,

0

>

s

e

X

A

t

我

A

t

哦

t

F

我

1

(

s

e

X

A

t

我

A

t

哦

t

y

米

米

你

D

)

0

0

0

,

1

D

我

A

e

r

(

d

我

A

p

s

e

X

A

t

我

A

t

哦

时间

0

0

4

0

.

1

2

7

0

.

2

3

4

5

0

4

.

0

8

4

7

.

0

2

3

4

1

5

3

.

0

3

3

7

.

0

2

3

4

8

8

3

.

0

9

7

6

.

0

6

3

4

0

.

4

7

5

0

.

2

3

4

6

6

4

.

0

4

6

4

.

0

2

3

4

6

8

3

.

0

2

5

.

0

2

3

4

3

0

4

.

0

1

9

3

.

0

5

4

8

6

6

,

1

6

9

7

5

,

2

0

6

5

.

0

6

2

0

.

5

0

4

0

.

1

7

1

6

.

3

3

3

0

.

7

9

6

0

.

2

3

4

2

3

4

2

3

4

2

3

4

6

8

1

0

1

1

,

1

8

1

,

4

4

7

6

5

.

7

1

7

2

.

0

0

4

4

.

0

9

6

0

.

7

6

2

3

.

0

1

7

6

.

0

2

3

4

2

3

4

2

3

4

3

2

4

8

1

9

,

1

6

5

5

1

,

2

5

8

4

0

.

6

7

4

2

.

0

7

3

.

0

7

3

6

.

6

8

2

3

.

0

5

8

6

.

0

2

3

4

2

3

4

2

3

4

2

3

4

6

0

0

.

3

7

5

2

.

0

8

4

3

.

0

3

1

4

.

0

4

3

7

.

0

9

3

.

3

9

0

3

,

7

2

2

8

1

,

3

2

3

3

3

0

.

1

4

2

0

.

2

3

4

7

2

4

.

0

1

8

3

.

0

2

3

4

6

6

2

.

0

6

0

3

.

0

2

3

4

5

0

2

.

0

2

3

1

.

0

4

7

8

4

7

8

4

7

8

4

7

8

4

7

8

4

7

8

4

7

8

,

0

=

e

我

A

米

e

F

(

r

e

G

A

n

A

米

r

哦

r

e

n

w

哦

F

哦

r

e

d

n

e

G

)

1

=

e

我

A

米

)

e

s

我

w

r

e

H

t

哦

0

t

n

e

d

n

e

p

e

d

n

我

y

r

A

d

n

哦

C

e

s

d

e

t

e

我

p

米

哦

C

r

e

G

A

n

A

米

r

哦

r

e

n

w

氧

)

e

s

我

w

r

e

H

t

哦

0

,

d

e

t

e

我

p

米

哦

C

F

我

1

(

我

哦

哦

H

C

s

)

]

t

n

e

米

y

哦

我

p

米

e

+

1

[

G

哦

我

(

e

z

我

s

米

r

我

F

)

r

A

e

y

s

你

哦

我

v

e

r

p

(

s

t

fi

哦

r

p

s

s

哦

r

G

,

0

=

哦

n

(

e

t

A

C

fi

我

t

r

e

C

t

H

G

我

r

e

s

你

d

n

A

我

n

w

氧

s

e

e

y

哦

我

p

米

e

e

我

A

米

e

F

F

哦

e

r

A

H

S

)

1

=

s

e

y

,

0

=

哦

n

(

s

n

哦

我

t

C

e

p

s

n

我

e

C

n

A

我

我

p

米

哦

C

)

1

=

s

e

y

s

s

哦

r

G

,

s

e

X

A

t

F

哦

s

t

n

你

哦

米

A

e

H

t

s

w

哦

H

s

e

我

乙

A

t

s

我

H

t

H

G

你

哦

H

t

我

A

.

d

e

t

你

p

米

哦

C

e

r

A

s

C

我

t

s

我

t

A

t

s

p

你

哦

r

G

e

G

A

r

e

v

A

e

H

t

e

r

哦

F

e

乙

米

r

fi

y

乙

d

e

t

A

我

你

C

我

A

C

t

s

r

fi

s

我

e

我

乙

A

我

r

A

v

H

C

A

e

F

哦

e

G

A

r

e

v

A

s

e

我

r

e

s

e

米

我

t

e

H

时间

:

s

e

t

哦

氮

.

n

哦

我

t

A

我

v

e

d

d

r

A

d

n

A

t

s

=

D

S

,

s

n

哦

我

t

A

v

r

e

s

乙

哦

F

哦

r

e

乙

米

你

n

=

氮

,

G

n

哦

d

=

D

.

s

n

哦

我

s

s

e

r

G

e

r

n

我

s

n

哦

我

t

A

米

r

哦

F

s

n

A

r

t

G

哦

我

r

我

e

H

t

e

s

你

我

,

s

e

e

y

哦

我

p

米

e

F

哦

r

e

乙

米

你

n

e

H

t

d

n

A

,

s

t

fi

哦

r

p

.

s

n

哦

我

t

A

我

你

C

我

A

C

s

’

r

哦

H

t

你

A

:

e

C

r

你

哦

S

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

A

d

e

v

_

A

_

0

0

1

4

4

p

d

.

/

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

The Effects of Formalization on SME Tax Payments in Viet Nam 157

附录 2

Table A2.1. Effects of Formalization on Total Tax Payments (Tobit)—Varying Sample Sizes

Variables: Log (1 + Taxes), (Real D1,000)

1

2

3

4

5

Minimum Observations in Panel

Switcher (from informal to formal)

Switcher (after formalization)

持续的

观察结果

Number of panels

Other controls

Time dummies included

Province dummies included

2.57***

(0.21)

1.12***

(0.17)

2.75***

(0.21)

0.90***

(0.19)

2.72***

(0.31)

0.75***

(0.23)

2.60***

2.31***

(0.21)

(0.18)

1.09***

1.14***

(0.20)

(0.15)

−3.29*** −3.07*** −3.63*** −4.25*** −3.48***

(0.99)

(0.94)

4,240

5,155

1,020

1,666

是的

是的

是的

是的

是的

是的

(1.31)

2,773

570

是的

是的

是的

(1.20)

3,393

731

是的

是的

是的

(0.83)

4,795

1,306

是的

是的

是的

D = dong.

Notes: Bootstrapped standard errors in parentheses. ***p < 0.01, **p < 0.05, *p < 0.1.

Source: Author’s calculations.

Table A2.2. Effects of Formalization on Total Tax Payments (Tobit)—Varying

Survey Waves

Variables: Log

(1 + Taxes),

(Real D1,000)

Switcher (from

informal to

formal)

Switcher (after

formalization)

Constant

Observations

Number of

panels

Other controls

Time dummies

included

Province

2005–

2007

2005–

2009

2005–

2011

2005–

2013

2007–

2009

2007–

2011

2007–

2013

2009–

2011

2009–

2013

2011–

2013

2.71***

(0.26)

2.82***

(0.23)

2.61***

(0.20)

2.57***

(0.21)

2.45***

(0.23)

2.27***

(0.21)

2.32***

(0.21)

1.67***

(0.36)

1.77***

(0.35)

0.79

(0.59)

1.12***

(0.17)

1.54***

(0.14)

1.31***

(0.18)

1.07***

2.40***

(0.57)

(0.20)

−4.23*** −3.67*** −3.81*** −3.07*** −6.67*** −6.04*** −4.41*** −6.40*** −4.43*** −2.35

(1.45)

(1.33)

1,778

1,962

970

1,075

(1.17)

2,128

1,203

(0.83)

4,795

1,306

(1.01)

3,979

1,306

(0.95)

3,017

1,204

(1.06)

3,906

1,305

(0.87)

3,090

1,305

(1.18)

2,833

1,157

(1.12)

2,017

1,157

1.58***

(0.17)

1.90***

(0.23)

1.34***

(0.17)

1.99***

(0.30)

2.32***

(0.33)

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

dummies

included

D = dong.

Notes: Bootstrapped standard errors in parentheses. ***p < 0.01, **p < 0.05, *p < 0.1.

Source: Author’s calculations.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

d

e

v

/

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

3

7

1

1

4

0

1

8

4

6

7

6

3

a

d

e

v

_

a

_

0

0

1

4

4

p

d

/

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

158 Asian Development Review

Table A2.3. Effects of Formalization on Revenue and Other Tax Payments

Revenue-Related Taxes

Other Taxes

Variables

Switcher (after formalization)

Gender of owner or manager (female = 0,

male = 1)

Owner or manager completed secondary school

(1 if completed, 0 otherwise)

Gross profits (previous year)

Firm size (log [1 + employment])

Firm size squared (log [1 + employment])

Share of female employees

Own land use right certificate (no = 0, yes = 1)

Compliance inspections (no = 0, yes = 1)

Constant

Observations

Number of panels

Time dummies included

Province dummies included

Tobit

4.52***