Ross Baird

Seed-Stage Investment and Support

Closing the Gap to Growth in Impact Investing

在 2009, Jen Medbery was a techie-turned-teacher with an idea to revolution-

ize American education, but she couldn’t find funding to grow the company.

After graduating from Columbia with a degree in computer science and work-

ing in the trenches as a classroom teacher—first through Teach For America,

then as a founding member of a charter school in New Orleans—Jen grappled

with a dilemma most teachers face today: the time-consuming task of gather-

ing and tracking data. While using student performance metrics has been

proven to improve education, particularly in underserved areas, it often

demands a prohibitive amount of teachers’ time. To help herself and her fellow

teachers deal with this problem, Jen created a software program that she called

Drop the Chalk. Based on feedback about the software, Jen decided to leave

teaching to focus on developing Drop the Chalk into a mainstream solution for

one of the major “pain points” in American education. She now had a product

with great customer feedback and was making a significant impact, but she had

few options for getting financial support or finding investors.

In the salt flats of Gujarat, 印度, Rajesh Shah had been working with

agariyas—salt farmers—for almost 30 年. Agariyas work in some of the most

difficult conditions in the world. They work around the clock for eight months

of the year, standing in 110-degree heat in the middle of the desert, pumping

and raking saltwater until they can produce enough crystallized salt to sell.

These farmers earn less than $1 每天, and must spend almost 50 percent of what they make on the diesel fuel to run their salt pumps. Perhaps most chill- 英利, when agariyas die and their bodies are cremated, their feet do not burn because they are so saturated with salt. After almost three decades working with the salt producers in various capacities, Rajesh had developed a concept called SABRAS, a for-profit company that could do two primary things: process and Ross Baird is the Executive Director of Village Capital, an organization that uses peer cohorts to build seed-stage, high-impact enterprises and accelerate the flow of invest- 蒙特. Ross is also affiliated with First Light, a seed fund that invests in high-impact enterprises worldwide. © 2011 Ross Baird innovations / 体积 6, 数字 3 133 从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Ross Baird sell salt, giving the agariyas access to mainstream markets, and provide afford- able goods and services to the salt workers to improve their quality of life. Rajesh was now ready to launch a business: he had experience, a concept, and an active customer base, but he had nowhere to go for funding. SEED-STAGE IN THE IMPACT INVESTING ECOSYSTEM Jen’s and Rajesh’s stories are not unusual. Thousands of entrepreneurs like them are developing businesses they hope will help change the world, but they struggle to get off the ground because of a lack of funding, operational capac- 性, technical advice, 人手, 和网络. The success of these entrepre- neurs at the seed stage is critical if the impact investing sector is to reach its potential capacity. According to various surveys, the impact investing sector—the subset of investors seeking social and environmental returns in addition to financial returns—is between $25 亿和 $50 billion—a massive market, but still only a tiny fraction of the estimated $200 trillion in the global capital markets.

Early-stage funding for start-up social enterprises, 然而, is rare. Echoing

绿色的, an organization dedicated to funding start-up social entrepreneurs,

received more than 3,000 applications in 2011, but was able to fund fewer than

20. Prominent angel networks for social investors, such as Toniic and Investors’

Circle, still have a limited track record in producing syndicated seed-stage deals

from member investors. 此外, an industry survey of over 100 impact

investment funds, representing $25 billion in capital under management, resulted in only four that would invest $100,000 or less per enterprise.

While there are thousands of promising innovations in the impact invest-

ing world—one only needs to look at the wave of applications submitted to fel-

lowship programs, incubators, and investors—only a handful get funded every

年. This shortfall stunts the growth of impact investing. Most impact invest-

ment funds have capital to deploy, but suffer from a shortage of investable

机会. The Triodos Opportunities Fund, established in the UK to build

and invest in social enterprises, closed in 2010, citing the lack of investable

公司.

Contrast the impact investing sector with the technology entrepreneurship

sector, where seed funding for enterprises, dedicated angel investors, and start-

up grants have been quite common for some time. More than 1,000 angel

investors are registered on AngelList, the most popular website in the technol-

ogy investing universe; almost every major business school holds a business-

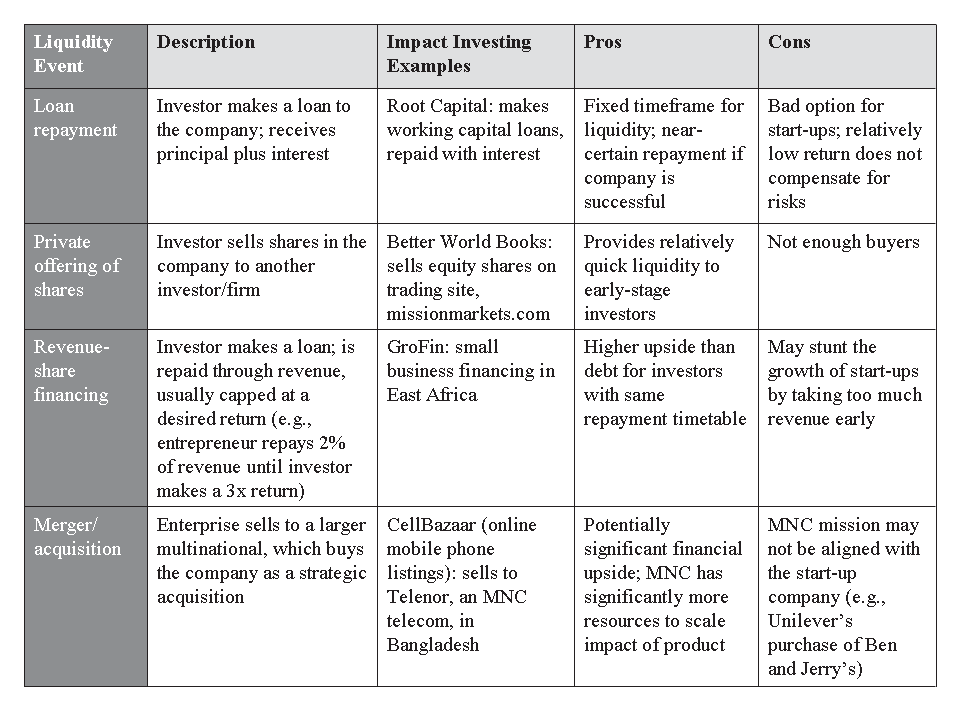

plan competition; and Start Fund, a recent new venture, promises a $150,000 entrepreneur-friendly investment, sight unseen, to all participants in a well- known technology incubator. 134 创新 / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Seed-Stage Investment and Support THE GAP BETWEEN SEED-STAGE ENTREPRENEURS AND IMPACT INVESTORS Jen decided to launch Drop the Chalk as a for-profit company in order to max- imize the impact the company could make. She felt that if she could charge schools for the software, she would be able to ensure that customer schools were deriving value from Drop the Chalk’s solution: if they didn’t find it valu- 有能力的, they wouldn’t renew their subscriptions! She also wanted to build a sus- tainable funding mechanism for the company over the long term. In order to scale to schools nationwide, Jen thought she would need to attract commercial capital, and she struggled to find financing when she decided to turn Drop the Chalk into a commercial innovation. New Orleans only had a small angel investing ecosystem, and most individuals and families with financial resources preferred more risk-averse investment opportunities. Launching as a for-prof- it also disqualified her from many grant opportunities. Jen had a great back- ground and a product with strong customer feedback, but no way to go to scale. Rajesh’s experience put SABRAS on a firm footing at its launch. His net- work of 6,000 salt workers was producing revenue for the company from its first day, and Rajesh had developed an innovation that significantly improved customers’ lives. He designed and prototyped a solar-powered salt pump that replaced the diesel option, cutting production costs as well as the massive pol- lution created by the operation. He also developed an innovative financing mechanism—salt producers would pay loans back in salt! Rajesh began by seeking investment from a handful of the 50+ funds focused on impact invest- ing in India. Although he had not had difficulty raising grant dollars for previ- ous nonprofit efforts serving the agariyas, most of the impact-focused, 为了- profit capital in India was focused on the later stages. Larger funds such as Acumen Fund, LGT Venture Philanthropy, and Aavishkaar typically like to see a track record, a history of revenue, and a fast-growing customer base before investing; an entrepreneur such as Rajesh in the pilot/proof-of-concept stage is typically not far enough along to be a candidate. Despite initial traction, Rajesh had nowhere to go for support. Why did Jen and Rajesh struggle to get off the ground? They were hindered by several structural problems in impact investing that also systematically stunt the growth of seed-stage programs. • Difficult economics behind seed investing and lack of liquidity in the market. Seed investors in the social capital markets are both building a market and investing in it. The traditional path to profitability in the technology sector (bet on 10 risky investments and hope that one becomes a home run, such as Google) becomes more difficult in the seed stage because there is currently limited liquidity in impact investments (那是, a shortage of acquisitions, secondary sales, and IPOs). The cost of hiring a talented team and sourcing, 创新 / 体积 6, 数字 3 135 从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Ross Baird Table 1. Liquidity Options for Entrepreneurs analyzing, and supporting deals has made seed funding prohibitively expen- 西韦. 桌子 1 outlines current liquidity options for entrepreneurs: • Lack of successful entrepreneurs to act as angel investors. Many angel investors are successful entrepreneurs who make investments themselves sim- ply because someone once took a chance on them. Because the sector is so young, social entrepreneurs who have been financially successful are rare— although I’ve noticed, as an investor, that many entrepreneurs in my portfo- lio hope to invest one day, should their company be successful. Kevin Casey of New Avenue Homes, an affordable housing company in the San Francisco Bay Area, 说, “I want to be on the other side of the table!” • Underleveraged grant and government dollars. Since the social capital mar- kets are underdeveloped, some angel investors feel they may be investing a large amount to “de-risk” early-stage enterprises, only to see later investors benefit disproportionately from the financial return. Governments and foun- dations can also play a catalytic role in providing early-stage risk capital for businesses, thus reducing the risk for more commercially focused impact investors. 然而, most seed investment to date is done with private capital. 尽管如此, we are seeing more innovation: the Shell Foundation, 为了考试- 普莱, makes grants directly to for-profit, impact-oriented organizations in the seed stage. They provided early risk capital to notable companies such as 136 创新 / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Seed-Stage Investment and Support d.Light and Husk Power, and they launched a seed-funding accelerator focused on India in conjunction with First Light Ventures, a fund with which I am affiliated. Another example is the New Orleans Startup Fund, a nonprof- it partially funded by the State of Louisiana to put risk equity into high- impact start-ups in the New Orleans area. Current options for enterprise support are incomplete. While a number of complementary efforts worldwide are addressing the seed-stage ecosystem, many current efforts are either effective but currently too expensive to reach significant scale, or still largely experimental. Current options worldwide include: •Business plan competitions: Nowadays, business schools across the United States, from the University of Michigan to Tulane, are hosting competitions focused on social enterprise. 例如, the Global Social Venture Competition at UC Berkeley and the $100K Entrepreneurship Competition

at MIT have been kick-starting social ventures for years. These competitions

can be a great start for any business, but the prizes are relatively small (typi-

卡莉 $25,000 或更少) and can rarely satisfy an entrepreneur’s financial needs. Jen won a business plan competition at Tulane for $10,000 and another at the

University of Pennsylvania for $20,000—financing that was helpful but insuf- 聪明的. •Grant and fellowship programs: 组织机构, most notably Ashoka and Echoing Green, have done remarkable work in supporting seed-stage entre- preneurs. Echoing Green supports an entrepreneur’s personal livelihood for two years at $60,000 每年, and Ashoka provides a similar amount to select-

ed fellows for three years; it has supported almost 3,000 fellows since it began

30 years ago. While these programs have changed the game for seed-stage

支持, they are limited in scalability because of the high cost per fellow.

Echoing Green, 例如, is only able to select 15-20 fellows per year.

•Angel investor collaboratives: Groups such as Investors’ Circle, 其中重点

primarily on U.S.-based businesses, Toniic, which focuses mostly on emerg-

ing market enterprises, and the Europe-based PYMWYMIC (Put Your Money

Where Your Mouth Is Company) gather angel investors and host entrepre-

neurs for pitches and shared diligence. These organizations can be incredibly

catalytic in helping enterprises that need to put together seed-stage rounds.

迄今为止, 然而, the number of seed-stage investments made through these

networks is small: 在 2010, these networks syndicated fewer than five seed

rounds among all members put together. 而且, entrepreneurs sometimes

find the application process opaque and time-consuming.

•Impact investment funds: While over $25 billion has been committed in more than 100 documented social venture funds, according to an industry survey I conducted, four openly invest less than US$100,000 per deal. Groups such as

创新 / 体积 6, 数字 3

137

从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023

Ross Baird

First Light Ventures, Merism Capital, and Investment Development Fund are

blazing the trail, but these funds are still experimental.

•Accelerator and incubator programs: Accelerators are perhaps the first place

for entrepreneurs to turn to seek support. The Hub Network, 最为显着地

Hub Ventures in the San Francisco Bay Area and Hub Venture Labs in

伦敦, provides technical assistance, mentorship, and often seed capital in a

network of 20 cities worldwide. The Unreasonable Institute attracts innova-

tive young entrepreneurs from around the world to Boulder, 科罗拉多州, each

summer, and Dasra Social-Impact attracts India’s top social innovators to

Mumbai each year. Incubators can be city based, such as Idea Village in New

Orleans, or global, such as the Global Social Benefit Incubator in Santa Clara,

加利福尼亚州. Accelerators are remarkably effective, but all face the similar issue

of funding the staff and programming that provide support to enterprises.

通常, they are either nonprofits that must raise grant dollars to cover

成本, or for-profits that are still exploring revenue streams.

INNOVATIONS TO BRIDGE THE GAP

To build their companies, both Jen and Rajesh turned to accelerators. Jen

applied to the Idea Village, an incubator in New Orleans that has been support-

ing high-impact companies since 2001. Founded by Tim Williamson and Allen

钟, successful entrepreneurs in their own right, the Idea Village had been

working to build an entrepreneurial ecosystem in New Orleans, providing sup-

港口, 网络, and publicity to partner entrepreneurs. After Hurricane

Katrina, New Orleans received an influx of support and resources for entrepre-

neurial efforts to rebuild the city, and Idea Village was an effective gatekeeper

of those investments. Jen applied to the Idea Village Entrepreneur Challenge

class of 2009-2010.

Rajesh applied to Dasra Social-Impact in the fall of 2009, looking for a net-

work to help build his company. 几乎 10 years ago, Deval Sanghavi and

Neera Nundy cofounded Dasra to support social entrepreneurs in India. 在

Dasra’s early years, the organization was nonprofit oriented, but as impact

investing began to grow in India, Dasra developed the capacity to work with

for-profit entrepreneurs as well. Dasra partnered with Social-Impact

国际的, an enterprise support organization founded by the KL Felicitas

基础, to launch Dasra Social-Impact, with an eye toward attracting the

best social enterprises—nonprofit and for-profit—from across the country.

The heart of programs such as Idea Village and Dasra is the peer cohort, A

group of for-profit social entrepreneurs at similar stages who meet regularly.

Both Jen and Rajesh were grouped with high-impact start-up entrepreneurs

who were facing similar challenges. They held regular meetings to review busi-

ness models, discuss strategy, and work through similar problems. 他们俩

138

创新 / Impact Investing

从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023

Seed-Stage Investment and Support

entrepreneurs knew they could count on receiving support or mentoring or on

becoming part of a network through these accelerators, but they were expect-

ing the source to be famous entrepreneurs or resident experts. When they start-

ed their programs, 然而, they found that the bulk of their learning and feed-

back came from their closest confidants, toughest critics, and most proactive

supporters—their peers. Yet they still needed investors. While most accelerators

did not have investment capital to put to work, Jen and Rajesh were excited to

find that a partner investor had committed a substantial seed investment to the

cohort. In the most unusual twist, allocation of the investment was to be deter-

mined not by the investor or a professional committee but by the cohort mem-

bers themselves. Along with their peers, Jen and Rajesh assessed one another at

the end of the incubation period, and the precommitted seed investment went

to whomever the peers judged most investment ready.

“WHAT IF MICROFINANCE AND ANGEL INVESTING HAD A BABY?”

Peer allocation of investment is at the heart of the organization I run, Village

首都. 在 2009, we created Village Capital as an initiative of the seed fund First

Light in order to address many of the gaps in the seed-stage ecosystem outlined

多于. We thought of the concept of the “village bank” in microfinance, 在哪里

microentrepreneurs, receiving $100 loans through self-help groups, lower the cost of putting capital to work by performing many of the tasks that loan offi- cers would in a bank—coaching one another, demanding accountability, 麦- ing loan decisions, and monitoring repayment. We also asked ourselves, why wouldn’t this work for start-up companies? We had seen the power of peer groups in other concepts—professional networks such as YPO Forum, univer- sity student organizations, the Rotary Club, and political organizations, and we thought that community could certainly power enterprise growth in this sec- 托尔. But we needed partners. We surveyed potential partners worldwide and found four groups with whom to pilot the concept: in addition to Idea Village and Dasra Social-Impact, we piloted the Village Capital model with the Bay Area Hub Ventures and the Unreasonable Institute in Boulder. We found incu- bators with a strong cohort of entrepreneurs and a program that included a sig- nificant amount of peer-to-peer interaction, which we felt would create the strong bonds we were looking for. We announced that precommitted invest- ment would be decided by the peers themselves, which led Nathaniel Whittemore of Change.org to say of the program, “It’s as if microfinance and angel investing had a baby.” In Jen’s case, Village Capital helped her build a sales and marketing strate- gy for her company. The entrepreneurs met weekly in New Orleans for 12 weeks; Jen pitched to her fellow entrepreneurs repeatedly, which prepared her innovations / 体积 6, 数字 3 139 从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Ross Baird not only for investor pitches but also for sales cycles. Being able to communi- cate Drop the Chalk’s impact and value to people not familiar with education reform significantly improved her ability to be an advocate for her software. 在......的最后 12 weeks, the Idea Village peer group voted on one another’s propos- 作为. Jen learned that she and fellow entrepreneur John Burns—whose company, Jack and Jake’s, is building a local agriculture supply chain in New Orleans— received $100,000 each. With that money, Jen was able to hire enough techni-

cal and programming support to pilot Drop the Chalk in New Orleans. Jen said

that even if she hadn’t received the investment, the peer support and feedback

from the program were enough to have made the experience worth it for her.

尽管如此, the money sure was helpful in building Drop the Chalk!

Rajesh’s experience with Village Capital helped him build some structure

around the development of SABRAS. While he had some early success with his

顾客, his peer reviewers tore up his business model and financial plan for

the salt production and processing, and for the solar pump. Thanks in large

part to his peer group, Rajesh was able to develop a coherent business plan, 一个

easy-to-understand slide presentation, and solid financials for the first time. 在

the end of the program, Rajesh’s peers selected him for a $75,000 investment.1 Rajesh gained structure, 稳定, and much-needed investment to pilot the solar pumps and launch SABRAS. LESSONS FROM VILLAGE CAPITAL What did we learn from the Village Capital experience, and how can it influ- ence the impact investing sector in the seed stage? Follow the 80-20 规则. Seed-stage work is expensive. Because of the low dol- lar amount that is invested in the seed stage (relative to later-stage invest- 评论), investors face tight margins on investment. 相似地, enterprise sup- port organizations such as incubators can face high overhead costs because staff members provide hands-on support. With Village Capital, we found that the peers provided much of the support that an executive-in-residence or an investment analyst might provide for a similar organization. 这 80-20 rule— be 80 percent as effective at 20 percent the cost—applies with the tight margins and limited resources in seed-stage investing. When peers can help one anoth- er with marketing, business models, publicity events, 和更多, the model is more scalable than the alternative. People-powered capital changes investors, support organizations, and investees. Democratizing the flow of capital has significantly accelerated the seed-stage investing space. Investors often have a transformational experience as they move from “moneybags” to “mentor”—one Village Capital investor said that he was tired of being asked for money all the time. The Village Capital model of allowing entrepreneurs to make the investment decisions gave him 140 创新 / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Seed-Stage Investment and Support the ability to build relationships with the entrepreneurs as more than only a funder. On the investee side, having the power to allocate capital is also trans- formative. Incubator partners in the pilots reported that entrepreneurs’ atten- dance in peer group sessions was higher than in previous years, the peer review was more intense—and in some cases more critical!—than it had been in the past because real money was in play, and in the end, a more serious, more com- prehensive, and much closer cohort emerged. One year after the completion of the pilots, 90 percent of the entrepreneurs in peer cohorts continued to meet in person or virtually. Democratizing capital helps support organizations as well. The Unreasonable Institute has addressed the financial sustainability problem incu- bators face by making participants raise funds to cover the program tuition. The Idea Village has kept a revolving loan fund available to the cohort: entre- preneurs can take out loans, and the money from repaid loans is then available to other Idea Village entrepreneurs. 在 18 月, the fund has had a 100 每- cent repayment rate. Layered capital is necessary. Village Capital would not be possible without (A) grant-funded incubator partners who are able to manage peer groups and provide the infrastructure for peer support; 和 (乙) precommitted investment dollars from First Light or another partner investor. With the relative youth of impact investing, grant dollars for building ecosystems and investment dollars for building companies can work hand-in-hand to build up the sector. Because of the challenges and risks of seed-stage investing and the youth of the market, neither nonprofit or for-profit dollars alone can build a market. Foundations and governments are getting the picture regarding the catalyt- ic role they can play in the seed stage of investing. First Light and the Shell Foundation have launched a year-long pilot that will invest in three to four companies in India, with the ultimate goal of creating a sustainable roadmap for seed funding in that country. The New Orleans Startup Fund is a 501(C)3 that uses state government funds and nonprofit donations to make risk-toler- ant, seed-stage equity investments in start-ups expected to have a positive impact on the New Orleans area. In short, a lot of market-making needs to happen at the seed level, and private dollars alone cannot do it. Investors: “Get to yes.” On the investor side, there’s always a reason to say no. There are almost no “slam-dunk” seed investing opportunities worldwide, as every enterprise has a million risks. Instead of saying no to everything, investors need to find a way to “get to yes”—put conditions on an enterprise (例如, “hire a COO and then I’ll invest”); make a commitment based on a matching investment; spend some time building a financial model. Investors need to do more “company-building” and less “company-selecting.” Most of the time and energy dedicated to seed investing goes to sourcing and due diligence; cutting the cost of putting capital to work can increase bandwidth (那是, the innovations / 体积 6, 数字 3 141 从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023 Ross Baird resources needed to complete a task or project) in company-building. We’ve found a way to do this in Village Capital. Investors precommit their money to companies and invest in the one the peers choose. The Village Capital portfo- lio has been strong, and it is comparable to those of the average enterprises receiving investment from impact funds or angel networks. The difference is that organizing peer cohorts takes less time and money than managing a dili- gence process and it also empowers the entrepreneurs. By precommitting resources, investors force themselves to “get to yes” immediately, and then to build the companies that the process produces. Entrepreneurs: view investors as partners, not checkbooks. On the entre- preneur side, enterprises need to understand that impact investing is risky and seed-stage impact investing is even riskier. If the company does financially well, for-profit investors want to participate in the profits created. Entrepreneurs often ask for “softer” terms of investment, thinking that impact investors are not as commercially rigorous as a typical Silicon Valley angel. This is a danger- ous assumption. Investors will be turned off by entrepreneurs who treat them as softer than average, and if current investors do not share in the upside of a company’s success, the sector will have a harder time attracting commercial capital. Entrepreneurs need to view investors as true partners, rather than cap- ital providers, if they are to achieve maximum impact. In our experience at Village Capital, the bulk of the friction between precommitted investment and the entrepreneur cohort has been over the term sheets. 出奇, the more experienced entrepreneurs, who likely know how difficult it is to raise money and find a good investor partner, have pushed back less on terms than the first- time entrepreneurs. It’s not about the money—but the money helps. One entrepreneur said to me, “I have no shortage of free advice.” As impact investing grows, so do the number of organizations providing support to enterprises, but there are already dozens of organizations worldwide that do this well. If a government, 基础, or investor partner wants to make an impact on social enterprises, putting money directly into companies—or supporting entities that do—is probably where the need is greatest. NEXT STEPS FOR SABRAS, DROP THE CHALK, AND VILLAGE CAPITAL Jen and Rajesh wrapped up their respective programs in spring 2010, each receiving seed investment allocated by their peers. In the past year, both of their organizations have grown tremendously. Rajesh has built up SABRAS’s pro- cessing and sales capacity to the point where the company is cash-flow positive. He has piloted the solar-powered pump technology with two farmers and is developing an operational plan to scale to 50 farmers in the next year. The farmers piloting the pump have increased their take-home pay 150 百分. Rajesh is currently raising $1.5 million to scale the company and has strong

142

创新 / Impact Investing

从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023

Seed-Stage Investment and Support

buy-in from potential investment partners.

Drop the Chalk piloted in 2010-2011 在 15 schools in New Orleans. Based

on its initial success, Drop the Chalk raised $750,000, with buy-in from local funds (New Orleans Startup Fund), well-respected impact investment players (Calvert Foundation), and technology angels. Drop the Chalk is now poised for success next year: it has 87 percent customer retention and already has con- tracts with schools in nine cities across the country. And we at Village Capital are finding strong program feedback beyond the pilot. We have launched eight programs worldwide, 和 98 percent positive feedback from entrepreneurs and more than 100 enterprises supported. The average participant raises $75,000 in seed funding in the six months following

the end of their peer cohort meetings. Village Capital has incorporated into a

separate nonprofit so we can build the infrastructure of seed-stage investing,

and we are partnering with for-profit investors beyond First Light to launch

additional programs. We partnered with First Light and the Hub Ventures fund

for our most recent program in the Bay Area, and for our upcoming Village

Capital program in London, we will be partnering with Merism Capital.

Most players in the social capital markets assume the good companies are

out there—you just have to try really hard to find them. 事实上, 99 百分

of the promising companies need risk-tolerant money and heavy support.

幸运的是, innovation across the sector is building the seed-stage ecosystem,

which will provide returns well beyond financing for the social capital markets.

Portions of this article have been adapted from “Village Capital: Using Peer

Support to Accelerate Impact Investing,” winner of the NextBillion 2011 案件

Writing Competition and available at GlobaLens.com.

1. The peers also selected Vijaya Pastala, whose enterprise, Under the Mango Tree, teaches farmers

how to use beekeeping to increase crop yields and sells the honey for a profit.

创新 / 体积 6, 数字 3

143

从http下载的://direct.mit.edu/itgg/article-pdf/6/3/133/704719/inov_a_00089.pdf by guest on 08 九月 2023