Matu Mugo

Regulation of Banking and

Payment Agents in Kenya

Fletcher School Leadership Program in Financial Inclusion:

Kenya Policy Memo

Kenya has made significant strides in recent years in extending financial services to

its populace. This has been accomplished on the back of the rapid expansion of

banks across the country, particularly in rural areas, and the transformational

introduction of mobile money transfer services in 2007. 然而, the battle for

financial inclusion remains far from won, and Kenyan policymakers and regulators

continue to develop and implement innovative models to expand financial inclu-

锡安. 为此, the agent banking model was rolled out in 2010 to enable banks

to contract with third-party agents, just as telecommunications companies have

been doing since 2007.

This policy memo explores the tensions between the payment agent model run

by telecommunications companies and the banking agent model. It starts by out-

lining the supply and demand sides of Kenya’s financial sector. The barriers to

financial inclusion, including income, literacy levels, product characteristics, 和

geographical distance, are articulated. This memo analyzes the geographic distance

barrier in special detail. The areas of tension cited by banks include differing

requirements for payment and banking agents with respect to business track

记录, liability, and exclusivity. This memo recommends a review of the require-

ments for both types of agents to allow for proportional regulation, based on risk

and types of services provided.

PROBLEM STATEMENT

Kenya’s current development blueprint, Vision 2030, seeks to graduate the country

from a low- to medium-income country by 2030 (Government of the Republic of

肯尼亚, 2007). The vision is underpinned by massively upscaling access to formal

Matu Mugo leads teams at the Central Bank of Kenya that are responsible for the

review and development of policies to promote safe, affordable, and inclusive finan-

cial services. He has held various positions in the Bank Supervision Department over

最后 11 年. Before joining the Central Bank of Kenya, 先生. Mugo worked as an

auditor for KPMG, an international audit and consultancy firm.

This policy memo was originally written for the Fletcher School Leadership Program

in Financial Inclusion, where Mugo was a Fellow in 2011.

© 2012 Matu Mugo

创新 / 体积 6, 数字 4

125

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Matu Mugo

financial services from current levels of 23 百分比以上 60 percent of the bank-

有能力的 (adult) population.1

The barriers to financial inclusion identified in national financial access sur-

veys carried out in 2006 和 2009 include costs of financial services (minimum

balances and fees), low financial literacy, documentation requirements, distance to

financial services locations, and income constraints. Long distances to financial

services locations increase the transaction cost to consumers in terms of transport

cost and time spent traveling. It is therefore critical that this constraint be

addressed in order to expand access to formal financial services.

The rollout of an extensive network of mobile phone payment agents in Kenya

自从 2007 有, in large part, targeted this challenge. 在 2010, with an eye to deep-

ening these initiatives, the Central Bank of Kenya (CBK) issued guidelines to

enable banks to offer a broad range of banking services through agents. 这

framework differs from that for payment agents, which is currently guided by

requirements set by telecommunications companies. The Central Bank has also

recently issued draft regulations covering payment agents (Central Bank of Kenya,

行进 2011). Banks have therefore submitted a request to the Central Bank to

review the agent banking guidelines in light of the requirements that differ from

those of payment agents. An urgent review of this problem by CBK is required to

maintain the momentum of the growth of financial inclusion through both pay-

ment and banking agents, and to ensure that achieving the Vision 2030 targets is

kept on track.

Overview of Kenya’s financial sector

背景

Financial access landscape (supply)

Kenya’s financial sector comprises both the formal and informal financial sectors.

The formal sector is one of the largest and best developed in sub-Saharan Africa.

It is comprised of a number of different financial institutions and independent

监管者, each charged with the supervision of their particular subsectors. 作为

十二月 31, 2010, the banking sector included 43 commercial banks, one mort-

gage finance company, two representative offices of foreign banks, 126 licensed

Forex Bureaus, five Deposit-Taking Microfinance Institutions, and one Credit

Reference Bureau, all supervised by the Central Bank of Kenya (CBK, 六月 2011).

The National Payment System, which is part of the financial system, is also over-

seen by the Central Bank. Other players include the capital markets, insurance,

pension schemes, and savings and credit cooperatives.

Financial access landscape (要求)

Kenya’s financial access landscape has shown marked improvement over the past

few years, as revealed by two national financial access surveys conducted in 2006

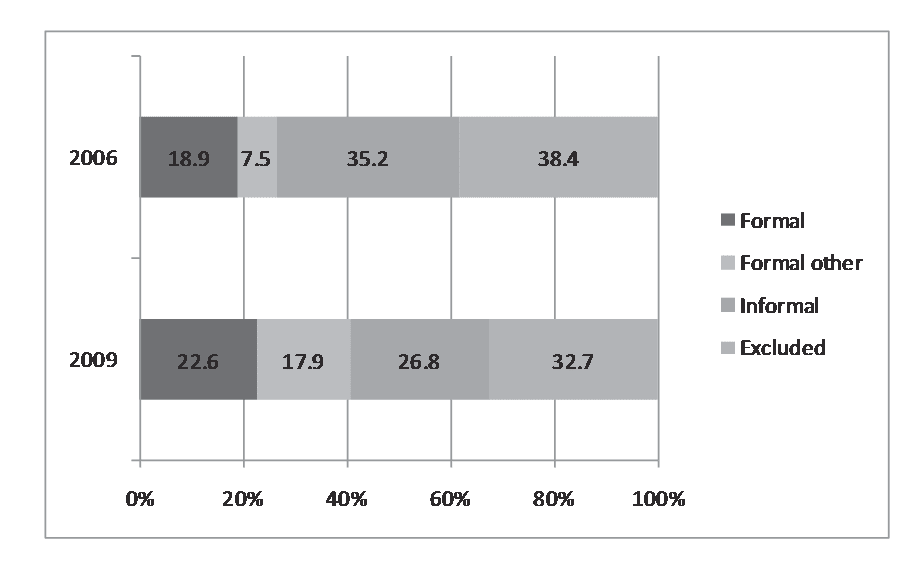

和 2009 (FinAccess, 2006, 2009). As indicated in Figure 1, access to formal finan-

cial services increased from 18.9 percent of the bankable population in 2006 到

126

创新 / Inclusive Finance

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Regulation of Banking and Payment Agents in Kenya

数字 1. Financial Access Strand in 2006 和 2009

来源: FinAccess (2009)

22.6 百分比在 2009.2 The number excluded from any formal or informal financial

service decreased from 38.4 百分比在 2006 到 32.7 百分比在 2009.

Barriers to financial inclusion

The key challenges and barriers to financial inclusion as revealed in the 2006 和

2009 surveys (FinAccess, 2006, 2009) and various related studies are as follows:

Low income continues to be the main barrier to expanding access, 和 61.8

percent of the unbanked citing income-related barriers as the key reason for exclu-

锡安.

Non-income-related access barriers—such as documentation and qualifica-

系统蒸发散, product characteristics, literacy levels, gender and cultural values, and geo-

graphical distance—together constitute the second most important reason for

being unbanked.

While all of the above listed barriers are important, this memo will focus pri-

marily on the geographical distance barrier.

Initiatives to address distance/financial services outlets constraints

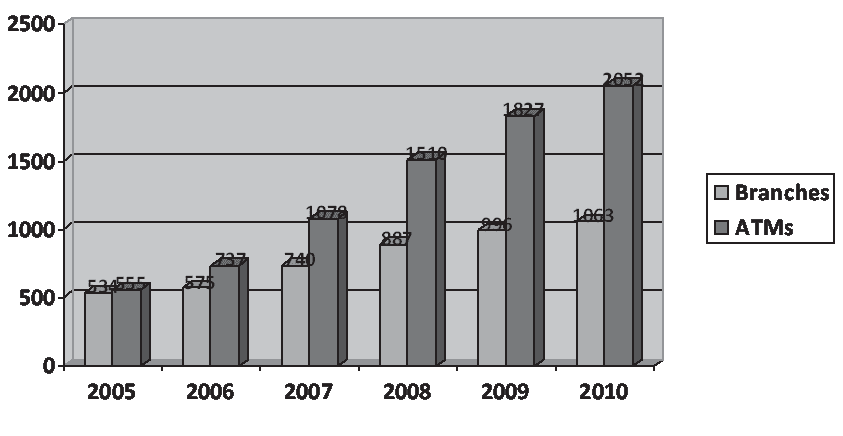

Growth in bank branches and ATMs

To reduce the distance to financial services, commercial banks have massively

expanded their branch and ATM networks in the last five years, as indicated in

数字 2.

创新 / 体积 6, 数字 4

127

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Matu Mugo

数字 2. Kenyan Banking Sector: Branches and ATMs, 2005 到 2010

来源: Central Bank of Kenya

The number of bank branches expanded from 534 在 2005 到 1,063 at the end

的 2010, A 99 percent increase. The ATM network increased from 555 在 2005 到

2,052 在 2010, A 270 percent increase.

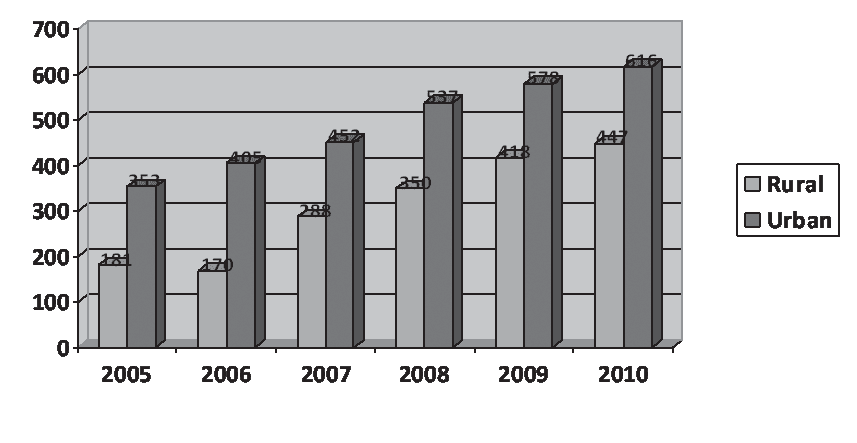

Bank branches have also expanded significantly in rural areas, as depicted in

数字 3. The number of rural branches has expanded by 150 百分, 从 181 在

2005 到 447 at the end of 2010. Urban branches, 另一方面, have expand-

ed by 75 百分, 从 353 在 2005 到 616 at the end of 2010.

Mobile/payment and banking agents

One of the most significant initiatives in addressing access to financial services in

Kenya has been the development of mobile money transfer services. Safaricom,

Kenya’s leading mobile operator, launched the M-PESA money transfer service in

2007. M-PESA has experienced viral growth in its first four years, gaining over 15

million subscribers and more than 20,000 agents.3 The introduction of mobile

financial services has helped to more than double the use of non-bank financial

机构, 从 7.5 percent of the bankable population in 2006 到 17.9 百分

在 2009 (FinAccess, 2009). The attraction of mobile financial services such as M-

PESA is their extensive reach all over Kenya, including in villages and slums (克莱因,

2011).

The amendment of Kenya’s Banking Act through the Finance Act of 2009 每-

mitted banks to use third parties (agent banking) to provide certain banking serv-

ices on their behalf. The Central Bank subsequently issued guidelines on agent

银行业, in May 2010 (CBK, 可能 2010). The guidelines require banks to seek

CBK’s approval for the agent network, as well as approval for specific agents, 和

to clearly specify the services to be provided by the agents. It is the institutions’

responsibility to vet the suitability of the agents in keeping with the guidelines. 作为

128

创新 / Inclusive Finance

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Regulation of Banking and Payment Agents in Kenya

数字 3. Kenyan Banking Sector: Branches Distribution, 2005 到 2010

来源: Central Bank of Kenya

of December 2010, CBK had granted approval to five institutions to engage agents.

Of these, two institutions had appointed a total of 8,809 specific agents, 包括

telecom-related agents and individual specific agents, spread across the country

(CBK, 六月 2011).

Representations by banks on a regulatory framework for banking agents

Following the rollout of agent banking in May 2010, banks have made proposals to

the Central Bank on possible areas of revision of the Agent Banking Guidelines.

This is based on their experience on the ground, as well as on the various frame-

works for payment agents contracted by mobile phone operators. The contracting

of payment agents is currently guided by the requirements of individual telecom-

munication companies. 然而, the Central Bank has recently issued a request

for comment on draft regulations on e-money and retail payment systems (CBK,

行进 2011), which are intended to apply to payment agents.

总之, the banking sector argues that three issues warrant special exam-

信息:

• Payment agents are generally required to have at least a six-month track record

in an existing business before being contracted. 反过来, the Agent Banking

Guidelines mandate an 18-month track record for banking agents.

• The Agent Banking Guidelines explicitly place liability for the agents’ actions

on the bank. The liability of telecommunications companies with respect to

liability for payment agents is not explicit.

• Banking Agents cannot be exclusive and can serve more than one bank. 为了

payment agents, this is not explicit, and there are payment agents that exclu-

sively serve one telecommunications company.

创新 / 体积 6, 数字 4

129

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Matu Mugo

The banking sector argues that the Agent Banking Guidelines should be

amended to allow for a tiered approach in order to create:

• Payment agents whose requirements would be less rigorous and be similar to

those of telecommunications agents that offer only cash-in and cash-out serv-

冰

• Banking agents whose requirements would remain as per existing agent bank-

ing guidelines but would be able to offer a broader range of services beyond

付款, including origination of deposit and loan accounts.

Policy considerations

ANALYSIS

Vision 2030 financial sector targets

Under Kenya’s current develelopment blueprint, Vision 2030, a more efficient and

competitive financial sector is expected to drive savings and investments for sus-

tainable and broad-based economic growth. The central policy objectives of the

long-term strategy for the financial sector include improved access and deepening

of financial services and products for a much larger proportion of Kenya’s popu-

lace (Government of the Republic of Kenya, 2007). The goals for the financial sec-

tor are to raise savings and investment rates from 14 百分比到 25-30 的百分比

GDP by 2030, and to increase bank deposits from 44 百分比到 80 percent of GDP

经过 2012 (Government of the Republic of Kenya, 2008).

Scaling-up of agent networks

The ambitious targets under Vision 2030 require massive expansion of access to

financial services for Kenyans. Identified constraints to accessing financial servic-

英语, particularly distance to financial services points, will need to be addressed. 这

proliferation of mobile money services in Kenya and the demonstrable success in

enhancing access to financial services provides key lessons. The success, 特别的-

ly of the pioneering M-PESA service, has been partly attributable to its wide net-

work of agents (Dittus and Klein, 2011; 克莱因, 2011; Mas and Radcliffe, 2011).

The effect of a large network of participants, particularly for M-PESA, 有骗局-

tributed to its success. A similar network effect will be critical for banking agents

to get to scale and to have a significant impact on access to second-generation

financial services for savings mobilization and credit. The current mobile money

services offered by mobile operators are largely focused on first-generation pay-

ment services, although linkages with commercial banks are increasing.

Proportionate/risk-based regulation

The Kenyan financial landscape presents a unique ecosystem of both banking and

payment agents (Tarazi and Breloff, 2011). The proposals by banks in the earlier

part of this memo are to some extent illustrative of the tensions between the two

型号, particularly given the head start afforded the telecommunications compa-

130

创新 / Inclusive Finance

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Regulation of Banking and Payment Agents in Kenya

nies with payment agents. This begs the question of whether the regulatory regime

for both types of agents should be the same.

To determine the appropriate regulatory framework, financial services that

enhance financial inclusion need to be unbundled. The key components could

include exchange of different forms of money (virtual money for cash), storage of

money for safekeeping (without payment of interest), transfer of money from one

person/entity to another, and investment of money (intermediation) (Dittus and

克莱因, 2011).

The model will then require varying degrees of regulation based on risk, 哪个

is lowest with the exchange of different forms of money and highest with interme-

diation. This suggests differing intensity of regulation with “light touch” regulation

at the basic exchange of forms of money to intensive prudent regulation at the

intermediation end. 因此, it is useful to unbundle the banking and payment

agents in Kenya along these lines and recommend proportionate regulation.

Policy choices

Retain status quo

One choice is to maintain the status quo. Doing so would not entail any changes

in the existing regulatory framework for banking and payment agents. 相当, 它

would mean taking a “wait and see” approach, allowing market forces to deal with

the unlevel playing field for banking and payment agents. Although this approach

represents the easiest course of action, it runs the risk of slowing Kenya’s rapid

progress toward financial inclusion. 更重要的是, it could deter the achieve-

ment of the ambitious financial sector targets set out under Vision 2030, 特别的-

ly if banking agents do not scale-up rapidly to benefit from network effects.

Amend regulatory framework for payment and banking agents

Amending the regulatory framework for both payment and banking agents is

another option. This would require more work but would ensure that Kenya’s

financial inclusion momentum is not only maintained but possibly accelerated.

Extensive networks of banking and payment agents would be complementary,

with payment agents offering first-generation financial services and the banking

agents providing second-generation financial services.

RECOMMENDATION

The Central Bank of Kenya should review and amend the regulatory framework

for banking and payment agents by unbundling the services offered. A tiered

approach should be adopted in the Agent Banking Guidelines to incorporate pay-

ment agents (“cash merchants”), as well as full-fledged banking agents. The regu-

latory regime for “cash merchants” under both regimes (Agent Banking and Draft

E-Money Guidelines) should be reviewed to ensure proportionate regulation. 这

regime for payment agents should be less rigorous than that of banking agents, 作为

创新 / 体积 6, 数字 4

131

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023

Matu Mugo

they would only provide basic payment services. The key areas to be considered in

both guidelines for review should be:

• Harmonization of track record and documentation requirements for both

banking and payment agents

• Clarity on the liability of institutions contracting payment and banking agents

• Exclusivity of agents

参考

Central Bank of Kenya, “Agent Banking Guidelines,“ 可能 2010.

Central Bank of Kenya, “Draft E-Money and Retail Payment Systems Guidelines,” March 2011.

Central Bank of Kenya, “Bank Supervision Annual Report 2010,” June 2011.

Dittus, 彼得, and Klein, 迈克尔. (2011, 可能). On Harnessing the Potential of Financial Inclusion, BIS

working papers No. 347.

FinAccess National Survey, “Central Bank of Kenya and Financial Sector Deepening Trust,” 2006.

FinAccess National Survey, “Central Bank of Kenya and Financial Sector Deepening Trust,” 2009.

Government of the Republic of Kenya, “Kenya Vision 2030, A Globally Competitive and Prosperous

Kenya”, 2007.

Government of the Republic of Kenya, “First Medium Term Plan (2008-2012), Kenya Vision 2030,”

2008.

克莱因, 迈克尔. (2011). Mobile Money in 2006 和 2016, private sector development blog. 可用的

在http://blogs.worldbank.org/psd. 四月检索 16, 2011.

但, Ignacio, and Radcliffe, Dan, Scaling Mobile Money, Bill & Melinda Gates Foundation, 四月

2011.

Tarazi, 迈克尔, and Breloff, 保罗. (行进 2011). Regulating Banking Agents, CGAP focus note 68.

华盛顿, 直流: CGAP.

1. “Bankable population” refers to adults over age 18.

2. Formal financial services refer to use of a commercial bank, postal bank, or insurance product.

The “formal other” designation refers to use of services from non-bank financial institutions such

as savings and Ccedit cooperatives, microfinance institutions, and mobile financial services. 这

informal strand uses informal financial services such as accumulating savings and credit associa-

的, rotating saving and credit association, and groups/individuals. The excluded do not use any

formal/formal other or informal financial services.

3. Central Bank of Kenya statistics.

132

创新 / Inclusive Finance

从http下载的://direct.mit.edu/itgg/article-pdf/6/4/125/704832/inov_a_00107.pdf by guest on 08 九月 2023