Markets Matter: The Potential of

Intra-Regional Trade in ASEAN and Its

Implications for Asian Regionalism∗

Lurong Chen

The Economic Research Institute for ASEAN and East Asia (ERIA)

Sentral Senayan ll, 6th Floor

JL. Asia Afrika, 不. 8

Gelora Bung Karno, Senayan, Daerah Khusus Ibukota

Jakarta, 印度尼西亚

lurong.chen@eria.org

Philippe De Lombaerde

Neoma Business School

1, rue du Mar´echal Juin BP 215

76825 Mont-Saint-Aignan Cedex

法国

philippe.de-lombaerde@neoma-bs.fr

Ludo Cuyvers

Centre for ASEAN Studies

University of Antwerp, 比利时

and North-West University (Potchefstroom Campus), 南非

Prinsstaat 13

BE-2000, Antwerpen, 比利时

ludo.cuyvers@uantwerpen.be

抽象的

This paper attempts to shed new light on further deepening the economic integration process in

Southeast Asia using a quantitative assessment of the potential for further developing intra-regional

贸易. It is evident that ASEAN’s export space is expanding faster than the world average and that

there is still room for ASEAN countries to further develop the role of their intra-regional trade. 到

improve its export potential, ASEAN should liberalize trade not only intra-regionally but also globally.

It could be in ASEAN’s interest to accelerate the pace of regional integration under frameworks that

involve the participation of non-ASEAN countries, especially an ASEAN Framework for Regional

Comprehensive Economic Partnership.

1. 介绍

It is generally accepted that in Southeast Asia, the de facto regionalization process that

historically centered around Japan has dominated the de jure regional integration process

∗ The authors thank Fukunari Kimura, Wing Thye Woo, Maria Socorro Gochoco-Bautista, Toshihiro

Okubo, Sisira Jayasuriya, Inkyo Cheong, Ding Lu, and the participants of the 2016 Asian Eco-

nomic Panel for helpful comments. The authors thank Bonaventura Francesco Pacileo for excellent

research assistance.

Asian Economic Papers 16:2

C(西德:3) 2017 by the Earth Institute at Columbia University and the Massachusetts

Institute of Technology

土井:10.1162/ASEP_a_00510

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

in the context of ASEAN. The former process has been described as a bottom–up process

of gradual industrialization following a “flying geese” pattern, supported by the develop-

ment of a dense network of trade and investment linkages from the late 1950s to the mid

1980s, with primary (日本) and secondary tiers (韩国, Hong-Kong, 台湾, Sin-

gapore). The emergence of China has modified the structure of the system but not neces-

sarily its functional logic. The Chinese take-off was especially spectacular since the 1990s.

The Chinese economy has attracted large quantities of foreign direct investment (FDI) 和

has been connected to global and regional production networks.

After the 1997–98 Asian financial crisis, more policy coordination and cooperation in the

areas of international trade and finance took place in the wider region. Although the in-

stitutionalization of the “ASEAN-plus” process(英语) might still remain shallow (Baldwin

2004; 2006), regular meetings have been organized since then between ASEAN and Japan,

中国, and Korea (ASEAN+3). These meetings are organized on a yearly basis with two

parallel structures: ASEAN+1 and ASEAN+3, including annual meetings of ASEAN+3

ministers of foreign affairs, 贸易, investment and finance. This “ASEAN-plus” framework

has been further extended to ASEAN+6 by recruiting Australia, 新西兰, 和印度

to the group.

From a comparative perspective, the ASEAN case is thereby singled out as a counter-

model for the EU. It is associated with features such as: low levels of institutionalization,

实用主义, bottom–up or de facto regionalization, regional production platforms, 所以

在. The positive features of this “model” are often emphasized, although in recent years

there have also been calls for deepening the institutionalization of ASEAN.

This paper attempts to shed new light on further deepening the economic integration

process in Southeast Asia by using a quantitative assessment of the potential for further

developing intra-regional trade. The paper is organized as follows: 部分 2 reviews the

literature and the scores of some indicators that will be presented for a selection of re-

gional integration schemes. 部分 3 further analyzes the relative export potential for

ASEAN countries. 部分 4 provides some policy-oriented concluding remarks based on

our findings.

2. The “Asian way” of regional integration

Since the 1960s, Japan has played a crucial role in regional cooperative operations and

it led the process of industrialization in East and Southeast Asia. Other East Asian

economies started to follow Japan in sequence to upgrade their industries from rela-

tively low value-added activities to relatively high value-added activities. This “flying

geese” pattern of growth demonstrates how cross-sector shifts of comparative advantages

2

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

from relatively labor-intensive production to relatively capital-intensive or technology-

intensive production can lead to industrialization and economic growth.

Since the early 1990s, with the slowdown of the Japanese economy and the rise of China

和韩国, the “flying geese” formation gradually evolved to “Factory Asia”,

where “formerly national production processes have been unbundled and dispersed

to the lowest cost location in East Asia” (Baldwin 2006, 25). 因此, the process

of regional integration in East Asia has entered a stage in which two regional hubs

of economic activity co-exist: Japan serves as a hub of high technology, and China is

emerging as a hub of labor-intensive activities (Baldwin 2004; 陈 2008; Chen and

De Lombaerde 2011).

This pathway of regional economic growth leads to a number of characteristics of Asian

regionalism: 第一的, de facto regionalization outweighs formal (de jure) regionalism. Asian

regionalism is mainly market-driven and constructed around partnerships between the

私营部门, playing a crucial role in the process, and the state (Cuyvers 2014). 第二,

and somewhat uncritically, European and Asian regionalism are usually associated with

“closed” and “open” regionalism, 分别. 那是, whereas the EU has often been

associated with “Fortress Europe”, Asian regionalism (in particular that of ASEAN) 是

much more directed towards the economic partner countries outside ASEAN because of

the relative dependence of ASEAN member countries on the rest of the world for goods,

服务, 投资, and technology—that is, ASEAN is relatively open towards third

国家 (Kimura and Ando 2005; Ando and Kimura 2013). 第三, Asian regionalism

is characterized by the absence of a unique center of influence or a clear regional leader

(De Lombaerde 2014) and show a complex network of bilateral free trade agreements

(FTAs) instead—the so-called “spaghetti bowl” (Bhagawati 1995) or “Asian noodle bowl”

(Baldwin 2007).

The de facto regionalization of ASEAN economies can be measured by a set of indicators

(见表 1). The intra-regional trade share of ASEAN is currently around 25 百分.

The development model in the region has been export-oriented, and countries have been

competing for outsourced tasks from advanced economies (Cuyvers and Dumont 2005;

Kimura and Ando 2005; Wakasugi, Ito, and Tomiura 2008). The emergence of “Factory

Asia” has therefore also been encouraging competitive unilateral liberalization. 虽然

the share of intra-regional trade has been increasing continuously since 1995, the score of

intra-regoinal trade intensity did decline from 4.2 百分比在 2005 到 3.4 百分比在 2010.

This means that the growth of intra-regional trade that has taken place during this period

has been overcompensated for by the increase in size of the regional economy.

The openness of the ASEAN region, as measured by the ratio of extra-regional trade

on regional GDP, first increased from 76.6 百分比在 1995 到 89.6 百分比在 2005, 和

3

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 1. Selected ASEAN integration indicator scores (%)

1995 2000 2005 2010

21.1

Intra-regional trade sharea

3.1

Intra-regional trade intensitya

Openness of regional economiesb

76,6

Intra-regional shares of trade in parts and componentsc 25.8

15.0

Intra-regional FDI inflows as a share of total FDId

3.6

Average AV dutiese

22.7

3.7

85,5

24.5

5.8

3.0

24.9

4.3

89,6

25.0

11.9

1.7

24.7

3.7

78,7

24.2

17.9F

0.8

笔记:

A. 来源: ARIC online database.

乙. Openness of the regional economies is measured by the ratio between extra-regional trade

(extra-regional imports plus extra-regional exports) and regional GDP. 来源: Authors’

calculation based on data retrieved from UNCTAD database.

C. The definition of trade in parts and components is based on Ng and Yeats (2003). 来源:

Authors’ calculation based on data retrieved from UN COMTRADE database.

d. 来源: ADB database.

e. 来源: Authors’ calculation based on data retrieved from WTO tariffs database.

F. Data of year 2014. 来源: ASEANstats Database.

then decreased to 78.7 百分比在 2010. The first phase can be explained by the wave of

economic globalization and the region’s fast integration into the global economy, 和

the second phase seems to be consistent with the fact that regional economic integra-

tion has been a rising trend in Asia since 2000. In comparison with other regions, 如何-

曾经, the level of extra-regional economic openness is clearly higher for ASEAN. 作为

evidence of intensive intra-regional production sharing, about one-quarter of ASEAN’s

trade in parts and components occurred within the region. 虽然, in relative terms,

the intra-regional share for ASEAN did not change significantly over time, the overall size

of ASEAN’s trade in parts and components, both intra-regionally and extra-regionally,

did increase by over 160 percent during the period between 1995 和 2010.

Turning now to investment flows, the intra-regional share of total FDI inflows in ASEAN

is still much below EU levels (多于 50 百分).1 What is striking here is that the

1997–98 Asian financial crisis seems to have had a great (negative) impact on intra-

regional FDI flows. Generally speaking, it appears that de facto regional integration in

ASEAN has been largely driven by trade, much less by investment. 而且, the intra-

ASEAN flows of parts and components are likely to be driven proportionately more by

FDI from outside the region than by intra-ASEAN FDI.

最后, de jure regional integration is more difficult to quantify. Given that average ad

valorem tariff levels in ASEAN have now also fallen below 1 百分, an additional re-

duction seems to garner limited impact. A greater impact can be expected from nontariff

1 According to data published by EUROSTAT for EU28. ADB data show figures for intra-ASEAN

FDI inflows of around 15 percent of total FDI in the 1990s. Towards the end of the 1990s and at

the beginning of the 2000s these figures drop to levels below 10 百分, after which there is some

partial recovery in these flows.

4

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 2. ASEAN trade and investment, 2014

COUNTRY

Brunei Darussalam

Cambodia

印度尼西亚

Lao PDR

Malaysia

缅甸

菲律宾

新加坡

Thailand

越南

ASEAN

Trade in goods

GDP

(十亿 (billion USD)

USD)

Export

Import

Trade in services FDI inflow (billion USD)

其他

(billion USD)

首都

Export

Import Total

Equity

Reinvested

earning

17.1

16.8

888.5

12.0

338.1

64.3

284.8

307.9

404.8

186.2

2520.5

10.6

10.7

176.3

2.6

233.9

11.0

61.8

409.8

227.6

148.1

1292.4

3.6

19.0

178.2

2.7

208.9

16.2

67.8

366.2

228.0

145.7

1236.2

1.1

3.8

23.5

0.8

41.9

3.2

24.8

140.4

55.3

10.9

305.8

1.7

1.9

33.5

0.5

45.3

1.9

20.0

141.6

53.2

14.5

314.0

0.6

1.7

22.3

0.9

10.7

0.9

6.2

72.1

11.5

9.2

136.2

0.1

1.7

12.5

n.a.

6.7

n.a.

2.0

57.3

4.6

5.0

89.9

0.1

0.0

5.0

n.a.

1.5

n.a.

3.3

10.4

1.0

4.2

25.6

0.3

0.0

4.8

n.a.

2.5

n.a.

0.8

4.4

5.9

0.0

18.8

来源: ASEANstats database, ASEAN Secretariat, 可以在 http 上找到://aseanstats.asean.org/ (last visited on 15 二月 2016).

measure reductions, including technical barriers and barriers based on national legal re-

quirements that are generally more difficult to measure.

3. ASEAN’s export potential

桌子 2 shows the importance of foreign trade for individual ASEAN economies. 这

exports to GDP ratio ranges from about 23 percent in Indonesia and Myamar to nearly

180 percent in Singapore. Despite the fast growth of trade in services, trade in goods still

accounts for the largest proportion in their international trade and investment profiles. 在

2014, the ratio between trade in goods, trade in services, and FDI was 19:5:1. As a group,

ASEAN is a net exporter of goods but a net importer of services. The surplus generated

from trade in goods was big enough to cover the deficit from trade in services. 整体

trade surplus corresponded to around 2 percent of the region’s annual GDP.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

Generally speaking, a large share of ASEAN’s economic growth can be attributed to

exports. Eight of ASEAN’s top ten trading partners are Asian economies. Based on its

current trade pattern (见表 3), the Regional Comprehensive Economic Partnership

(RCEP) already covers a regional market that represents nearly 60 percent of ASEAN total

trade and contributes over 40 percent of inward FDI. The “big three”—Japan, 韩国, 和

China—together account for one-fourth of ASEAN’s exports, one-third of its imports, 和

one-fifth of its FDI inflow in 2014.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Despite the already high degree of economic interdependence, is there still space for

ASEAN to export more to the regional market? How important is RCEP for ASEAN from

the perspective of ASEAN’s export potential? To answer these questions, we adopt a

forward-looking position based on empirical data and simulate its evolution over time

as the basis for exploring the possible correlation between deepening regional integration

and the expansion of ASEAN’s exports.

5

Asian Economic Papers

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 3. ASEAN’s major trading partners (merchandise) 2014

Partner

Exporta

Importa

WORLD

ASEAN+6

ASEAN+3

Intra-ASEAN

中国

欧洲联盟

日本

美国

Republic of Korea

台湾

香港

澳大利亚

印度

来源:

1292.4

746.9

651.9

329.6

150.4

132.5

120.2

122.4

51.6

39.5

85.3

45.3

43.3

1236.2

737.1

683.3

278.6

216.1

115.8

108.8

90.1

79.8

68.8

14.1

25.0

24.4

全部的

贸易

2528.6

1484.0

1335.2

608.2

366.5

248.3

229.0

212.4

131.4

108.3

99.4

70.4

67.7

Trade

balance FDI flowa

Inward

FTA (year of entry

into force)乙,C

56.2

9.9

−31.4

51.1

−65.7

16.7

11.4

32.3

−28.2

−29.4

71.2

20.3

18.9

136.2

58

51.1

24.4

8.9

29.3

13.4三、

13.0

4.5

n.a.

n.a.

5.7

0.8

Noi

不

是的 (1992)

是的 (2007)二

不

是的 (2008)四号

不

是的 (2009)

不

不

是的 (2010)

是的 (2010)v

A. ASEANstats database, ASEAN Secretariat, 可以在 http 上找到://aseanstats.asean.org/ (last visited on 15

二月 2016).

乙. Asia Regional Integration Center (ARIC), available at https://aric.adb.org/ (last visited on 8 十月 2015).

C. WTO Regional Trade Agreements gateway, available at https://www.wto.org/english/tratop_e/region_e/region_e.htm

(last visited on 8 十月 2015).

笔记: Unit: billion USD.

我. ASEAN has signed FTAs with each of the six. RCEP negotiation under the ASEAN+6 framework is still

under negotiation. It is expected to be concluded by the end of 2016.

二. 十一月 2015, ASEAN and China signed an FTA upgrade protocol (ACFTA 2.0).

三、. The annual FDI inflow from Japan in ASEAN reached a historical high of 21.8 billion USD in year 2013,

but then decreased by one-third in 2014.

四号. Years of entry into force: 2008 for Singapore, 日本, 越南, Laos PDR, and Myanmar; 2009 for Brunei

Darussalam, Malaysia, Thailand, and Cambodia; 2010 for Philippines. The entry into force for Indonesia is

pending based on ARIC record.

v. Years of entry into force: 2010 for India, Malaysia, 新加坡, Thailand, Brunei Darussalam, 缅甸

and Vietnam, and Indonesia; 2011 for Lao PDR, 菲律宾, and Cambodia.

3.1 The model

Redding and Venables (2004) presents a method to derive a supplier access indicator

and a market access indicator by decomposing countries’ bilateral trade flows. A similar

approach was adopted by Head and Mayer (2004) and Mayer (2009). Our theoretical

framework for the analysis in this paper is based on the earlier work.

方程 (1) shows that the bilateral export from i (the exporting country) to j (the import-

ing country), denoted by Xij, can be expressed as a share (mi) of j’s total import Mj.

Xi j

= mi

· Mj

(1)

Three factors affect country i’s share in j’s import profile, mi: i’s general export compet-

itiveness, Ai; the degree of market competitiveness in country j, (西德:2)

j ; and the trade cost

between i and j, δ

j is essentially a set of mar-

ket opportunities that it offers to all its trade partners, and each partner’s market share

is fundamentally determined by the country’s effective competitiveness but has to face

我j . From the import country’s perspective, (西德:2)

6

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

i j when exporting to j. 所以, j’s overall market potential for foreign

a trade cost of δ

producers can be expressed by (西德:2)

h Ah

trade partners and h ∈ V. This allows us to rewrite equation (1) into equation (2):

h j , where V is defined as a set of country j’s

(西德:2)

· δ

=

j

Xi j

= mi

· Mj

= (Ai

· δ

我j

· (西德:2)−1

j ) · Mj

.

(2)

Country i’s total exports Xi can thus be expressed as the sum of bilateral trade flows with

its trade partners:

席

= Ai

·

(西德:3)

H

δ

i h

· Mh

· (西德:2)−1

H

.

(3)

By defining sh,m and sh,x as country h’s share in the world total imports and exports re-

spectively, country i’s share in the world total exports (si,X) becomes a product of i’s com-

petitiveness and a set of market opportunities that country i gains worldwide, 这是

the sum of all of its trade partners’ overall market potential (西德:2)

to access these markets δ

economy sh,米, as equation (4) shows.2

h weighted by the trade cost

i h and the relative importance of country j’s market in the global

si,X

= Ai

·

(西德:5)

δ

i h

· sh,米

· (西德:2)−1

H

,

(西德:4)

(西德:3)

H

where sh,米

= Mh

/中号, sh,X

= Xh

/ X, M = X, 我和 (西德:5)= h.

To simplify, we call the set of market opportunities that country i gains worldwide as

i’s overall export space ((西德:4)

to foreign suppliers as i’s overall import space ((西德:2)

ble to the supplier access indicator and the market access indicator in Redding and

Venables (2004).

我 ), and the set of market opportunities that country i offers

我 ). Respectively, these are compara-

(西德:3)

=

H

δ

i h

· sh,米

· (西德:2)−1

H

.

/Ai

(西德:4)

我

(西德:2)

我

= si,X

(西德:3)

=

δ

你好

· sh,X

· (西德:4)−1

H

.

(4)

(5)

(6)

H

Suppose that all firms are symmetric (firms in the same country produce the same quan-

tity qi and charge the same price pi) and the production structure is rigid in the short term

(there are no changes in the product variety), all changes in country i’s export competi-

tiveness are solely reflected in the price.

Ai

= Ni

· p1−σ

我

.

(7)

2 The term in parentheses is a set of market opportunities that country i owns worldwide.

7

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

Combining equations (5) 和 (7) into equation (8), we see that pi is positively related to

the country’s overall export potential (西德:4)

我 :

(西德:6)

=

pi

si,X

· (西德:4)

我

Ni

(西德:7) 1

1−σ

(西德:6)

=

· qi

pi

X · (西德:4)

我

(西德:7) 1

1−σ

= c · (西德:4) 1

σ

我

, where c is a constant.

(8)

另一方面, one can see that the set of alternatives for consumers in country j ((西德:2)

is inversely related to the price index of imported products in the market (Pj ),

j )

(西德:2)

j

=P

σ −1

j

.

(9)

直观地, we can expect a lower price to be associated with a higher degree of compe-

tition among foreign suppliers in the market. From equation (2), bilateral trade between

countries i and j can be expressed as

Xi j

= Ai

· δ

我j

· (Mj

· P 1−σ

j

).

(10)

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

This structure can be incorporated easily into a gravity equation where the countries’

bilateral trade is determined by three groups of factors: factors related to the exporting

country’s capacity to export f (·) = Ai , factors related to the importer’s capacity to import

· P 1−σ

G(·) = Mj

ij. The overall export space of country i

j

can thus be estimated by

, and the bilateral trade resistance δ

ˆ(西德:4)

我

=

(西德:3)

H

ˆδ

i h

· ˆgh

, h ∈ V.

(11)

3.2 Variables and data

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

This study aims to estimate market potential in a regional context and investigates its

correlation with the process of further regional integration. A technical challenge is to

choose variables that can properly capture the characteristics of the three groups of factors

上文提到的. Recent studies that use different augmented gravity models, 例如

Kimura and Lee (2006), Mayer (2009), and Corcos et al. (2012), have introduced and sug-

gested some candidate variables/indices to be used in addition to the standard variables

in the gravity equation. We opted for GDP, Internet access and usage, economic freedom,

WTO membership, paved roads, and the stock of inward FDI as variables to describe a

country’s economic characteristics. Trade resistance between countries is measured by ge-

ographic distance and weighted average bilateral tariff3 level as proxies of the geographic

and political friction, 分别, together with two complementary dummy variables

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

3 As mentioned before, nontariff measure reductions are likely to be the main source of liberaliza-

tion gains in the future. 到目前为止, 然而, we do not have reliable quantitative data on nontariff

措施. This evidently is a drawback of our model estimations presented in this paper.

8

Asian Economic Papers

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

to capture the additional trade-inducing effects of having common languages and contin-

gent territories. Appendix A provides the details of each variable and the corresponding

data sources.

In our analysis, we use a panel data set of global bilateral aggregate trade flows, covering

the period from 1995 到 2014, allowing us to take both the cross-sectional characteristics

and time-variant changes into account. By observing the changes of dependent variables

in these two dimensions we control for some omitted variables without the need for direct

measurement of these factors.

The assumption of whether these omitted variables are constant over time and/or

whether they are cross-sectional determine the choice of the regression model. In prin-

原则, the fixed effects model is applied to determine the existence of true differences

among the estimated mean of sector-specific errors; and the random effects model is

used for the analysis on variant components, since all effects are assumed to have a

zero mean. The tradeoff between the two models is related to efficiency and consistency

(陈 2008).

Instead of imposing extra assumptions on the model, Hausman’s test is conducted to as-

sess the econometric justification of using random effect estimations. The Hausman test

results reject the null hypothesis of non-systematic difference between fixed effect estima-

tors and random effect estimators (见表 4). Because of the inconsistency of random

effects estimators, we therefore will use the fixed effects model in our analysis.

3.3 结果

GDP has positive impacts on bilateral trade from both the supply and demand sides, 但

with different elasticities. Roughly speaking, a change of 1 percentage point in the im-

porter’s GDP will be equivalent to a change of 3 percentage points in the exporter’s GDP

regarding the direct impacts on bilateral trade. This is consistent with the knowledge that

the world economy is dominated by the buyer’s markets. A large market has a large con-

sumption capacity and therefore a large (潜在的) 要求.

Relatively speaking, countries with better Internet access tend to export more and import

较少的. This demonstrates that the increased usage of Internet in a country can effectively

increase the competitiveness of its products/services (例如, accessing the Internet

can improve workers’ skills and knowledge and consequently their productivity), 还有

as improving broader production lifecycle processes such as design, 营销, 反式-

portation, supply chain management, 等等.

The coefficient of the Index of Economic Freedom is generally positive. As economic free-

dom goes together with increasing economic openness towards the rest of world, 这是

9

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 4. Results of Hausman tests

Fixed effect Random effect Hausman’s

比较

estimators

estimators

r_lgdp

p_lgdp

r_internet

p_internet

r_free

p_free

r_wto

p_wto

r_lpaved

p_lpaved

r_linstock

p_linstock

Tariff

Ldist

Contig

Comlng

∗∗∗

0.786∗∗∗

(0.013)

0.370∗∗∗

(0.013)

0.015

(0.003)

−0.021∗∗∗

(0.003)

0.003∗∗∗

(0.001)

0.007∗∗∗

(0.001)

0.309∗∗∗

(0.021)

0.202∗∗∗

(0.019)

0.004∗∗∗

(0.000)

0.006

(0.000)

0.035∗∗∗

(0.007)

0.024∗∗

(0.006)

−0.358∗∗∗

(0.030)

−1.100∗∗∗

(0.007)

1.588∗∗∗

(0.041)

0.749∗∗∗

(0.020)

∗∗∗

∗∗∗

0.820∗∗∗

(0.009)

0.883∗∗∗

(0.009)

0.033

(0.003)

−0.039∗∗∗

(0.003)

0.007∗∗∗

(0.001)

0.011∗∗∗

(0.001)

0.211∗∗∗

(0.020)

0.113∗∗∗

(0.018)

0.007∗∗∗

(0.000)

0.009

(0.000)

−0.140∗∗

(0.007)

−0.028∗∗∗

(0.006)

−0.234∗∗∗

(0.030)

−1.266∗∗∗

(0.021)

1.387∗∗∗

(0.115)

1.075∗∗∗

(0.054)

∗∗∗

−0.033

(0.010)

−0.514

(0.009)

−0.018

(0.000)

0.018

(0.000)

−0.005

(0.000)

−0.004

(0.000)

0.099

(0.007)

0.089

(0.006)

−0.002

(0.000)

−0.002

(0.000)

0.175

(0.003)

0.051

(0.002)

−0.125

(0.002)

笔记: Stata output of the Hausman test:

b = consistent under Ho and Ha; obtained from xtreg

B = inconsistent under Ha, efficient under Ho; obtained from xtreg

Test: Ho: difference in coefficients not systematic

chi2(13) = (b-B)’[(V_b-V_B)ˆ(-1)](b-B)

= 9179.21

Prob>chi2 = 0.0000

∗∗∗

Statistically significant at the 1 percent level;

∗∗

statistically

significant at the 5 percent level;

∗

statistically significant at the

10 percent level.

intuitively clear that imports grow as the market becomes more open to foreign suppliers;

on the exporting side, the competition induced by economic openness tends to make the

domestic industry stronger and more competitive in the long run, supporting increasing

exports in the global market. This does not exclude the fact that in the short term the in-

flow of foreign competitors may crowd out some domestic producers from the industry

and cause exports to contract temporarily.

WTO membership, 反过来, is a strong factor in the promotion of exports and imports.

而且, bilateral trade flows between WTO member states are on average 70 百分

larger than those between non-WTO member countries. Under a multilateral framework

10

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

of trade liberalization, countries open their domestic markets in exchange for better access

to the global market.

The positive effects of infrastructure are also significant. For both importing and ex-

porting countries, building infrastructure can facilitate logistics and transportation and

therefore reduce trade costs. There is little difference between infrastructure’s impacts

on exports and on imports. It is estimated that an additional 1 percent increase in paved

roads may cause countries’ bilateral trade to increase by 0.4 到 0.6 百分.

The index of the FDI stock, although imperfect for measuring international trade-related

capital flows, does provide insights for the relationship between trade and FDI. Our es-

timations show that a country’s inward FDI stock and its foreign trade (both imports

and exports)4 are positively correlated, which probably is related to the association of

inward FDI with technology transfer and knowledge spillover, such that the host country

becomes more competitive and thus exports more. 或者, inward FDI in labor-

abundant countries is often related to export-oriented manufacturing and assembly oper-

ations. 另一方面, the increasing FDI inflows can also be interpreted as indicating

a country’s positive economic outlook and expanding market potential, which will en-

courage more imports.

The estimated coefficients of three variables measuring trade resistance (or facilitation)—

geographical distance, common language, and contingent territory—are in line with what

theory predicts. There is a negative correlation between the countries’ geographical dis-

tance and the size of bilateral trade flows. It is also evident that common language and

contingent territory are positive factors that stimulate bilateral trade.

最后, the most revealing result is the impact of tariff duties on bilateral trade—this is

negative and highly significant. 平均而言, bilateral trade will increase by about 3 每-

cent when the ad valorem import tariff rate imposed by the importing country decreases

经过 10 百分, starting from 100 百分. The marginal effect of import tariff reduction

增加, 然而, as the tariff rate approaches zero, such that the removal of the last

10 percent tariff duty (bringing it to zero) 将要, 一般来说, induce a 5 percent increase in

双边贸易.

3.4 Capturing the regional fixed effects

To illustrate the unique trade pattern of ASEAN and East Asia, and to capture its general

特征, we add three dummy variables to the basic model to distinguish between

4 The coefficient of the exporting country’s stock of inward FDI presents the lowest degree of statis-

tical significance in our fixed effect estimations of the basic model, 然而.

11

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 5. Decomposing the regional fixed effects

Basic model ASEAN

ASEAN

欧洲联盟

欧洲联盟

MERCOSUR MERCOSUR

−1.111∗∗∗

(0.007)

1.532∗∗∗

(0.040)

0.717∗∗∗

(0.020)

Ldist

Contig

Comlng

Import dummyi

Export dummyii

Intraregional dummyiii

−1.097∗∗∗

(0.007)

1.522∗∗∗

(0.040)

0.727∗∗∗

(0.020)

∗∗∗

2.272

(0.099)

−1.225∗∗∗

(0.007)

1.384∗∗∗

(0.040)

0.813∗∗∗

(0.019)

0.905∗∗∗

(0.024)

1.991∗∗∗

(0.024)

−0.614

(0.104)

∗∗∗

−1.003∗∗∗

(0.008)

1.544∗∗∗

(0.040)

0.792∗∗∗

(0.020)

∗∗∗

1.404

(0.033)

−1.008∗∗∗

(0.008)

1.732∗∗∗

(0.039)

0.931∗∗∗

(0.019)

0.111∗∗∗

(0.015)

1.539∗∗∗

(0.016)

∗∗

0.081

(0.038)

−1.111∗∗∗

(0.007)

1.484∗∗∗

(0.040)

0.712∗∗∗

(0.020)

∗∗∗

1.505

(0.173)

−1.136∗∗∗

(0.007)

1.440∗∗∗

(0.040)

0.699∗∗∗

(0.020)

−0.473∗∗∗

(0.031)

1.441∗∗∗

(0.032)

0.566

(0.177)

∗∗∗

∗∗∗

笔记:

Statistically significant at the 1 percent level;

∗∗

statistically significant at the 5 percent level;

∗

statistically significant at the 10

percent level.

我. value = 1 if the export country comes from region R, otherwise value = 0;

二. value = 1 if the import country comes from region R, otherwise value = 0;

三、. value = 1 if both trade partners come from the same region R, otherwise value = 0.

three subcategories of intra-regional trade bias (imports, exports, and net additional pref-

erence to trade with partners from the same region) (见表 5).

The estimation results for the EU and MERCOSUR (阿根廷, 巴西, Paraguay, Uruguay

and Venezuela), which are included for the sake of comparison, provide evidence that

ASEAN countries are in general more foreign trade–oriented; both on the export and the

import side, they trade much more than the world’s average. When taking the ASEAN

countries’ pro-export and pro-import characteristics into account, 然而, 额外的

preference for intra-regional trade is not visible. 相反, a negative intra-regional

bias is observed. 尽管如此, our estimation results show that when comparing trade be-

tween pairs of ASEAN countries with trade between pairs of countries otherwise under

the same conditions, the former more than doubles the latter. It is interesting to compare

these findings with the results for the EU and MERCOSUR. These country groupings also

export substantially more than the world average. The import bias is much smaller for

the EU (大约 10 百分), and even negative for MERCOSUR. In both cases the intra-

regional dummy is significant. As higher values for the dummy in the case of MERCO-

SUR is not due to deeper integration, it might be hypothesized that the specific situation

of MERCOSUR, characterized by the absence of important nearby trade partners in the

broader region and contrasting with the EU and ASEAN, may possibly have inflated the

dummy. Compared with ASEAN, the EU shows weaker export and import biases.

3.5 Market potential

Based on the derivation in Section 3.1, the value of region R’s export potential index is

simply (西德:4)

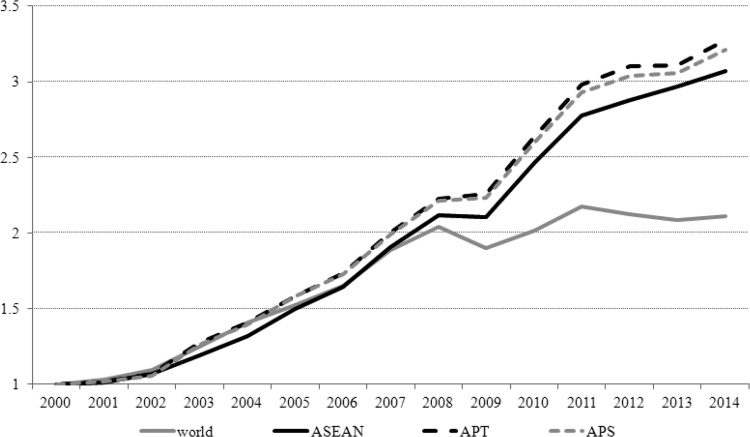

ASEAN+3, and ASEAN+6, 使用 2000 as the baseline year.

H. 数字 1 depicts the growth path of market potential in ASEAN,

h∈R

(西德:2)

=

(西德:4)

右

12

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

数字 1. Changes in market space, 2000–14

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

笔记: APT = ASEAN+3; APS = ASEAN+6.

全面的, ASEAN’s export space is expanding at an annual rate of growth that is higher

than the world’s average, particularly after 2009. The estimation shows that ASEAN’s

export space in 2014 is three times that of 2000, given the average annual growth rate

的 8.3 百分. 而且, this growth is continuous and smooth. 从 2000 到 2014, 这

only year the growth slowed down is between 2008 和 2009 when the export space of

most main trade countries contracted because of the global economic crisis. Looking at a

broader region, ASEAN+3 as a group has improved its market potential even faster than

that of ASEAN itself during that period.

在 2014, ASEAN accounted for nearly 4 percent of the world’s total export space, as com-

pared with only 2.5 百分比在 2000. This trend somehow indicates the increasing demand

for products made in ASEAN and reflects the region’s generally growing export capacity.

The progress of regional integration among ASEAN member states could be a positive

factor contributing to regional market capacity building.

桌子 6 presents the ratio of intra-regional and extra-regional export space for ASEAN as

well as that of within/outside ASEAN+3 and ASEAN+6 based on the respective export

特征 (the “ideal” ratio) and the ratio calculated using actual trade statistics (这

“actual” ratio). 用于比较, we list the 1995–99 and the 2010–14 average levels.

13

Asian Economic Papers

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 6. Export potential vs. actual exports, 1995–99 vs. 2010–14

Estimated export space Actual exports

1995–99

2010–14

1995–99

2010–14

ASEAN

Intra-regional

Extra-regional

Within ASEAN+3

Outside ASEAN+3

Within ASEAN+6

Outside ASEAN+6

欧洲联盟

Intra-regional

Extra-regional

MERCOSUR

Intra-regional

Extra-regional

41.8%

58.2%

63.6%

36.4%

72.1%

27.9%

87%

13%

72.9%

27.1%

42.7%

57.3%

73.5%

26.5%

79%

21%

82.5%

17.5%

61.6%

38.4%

19.5%

80.5%

43%

57%

55%

45%

61.9%

38.1%

23.9%

76.1%

22%

78%

58.9%

41.1%

67.9%

32.1%

62.9%

37.1%

12.4%

87.6%

笔记: We use the import data shown in the import country’s balance sheet to measure the

actual export flows instead of directly using the export data. 例如, we use country

B’s reported imports from country A to measure the actual export flow from A to B. 这

is because imports are normally calculated based on Cost, Insurance, and Freight, 这是

indeed closer to the price faced by the domestic consumers or producers.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

第一的, considering the ASEAN market, the estimated ideal ratio of intra- and extra-regional

export was approximately 2:3, whereas the actual ratio was about 1:4. The ratio shows no

significant change overtime. When looking at the expansion of ASEAN’s intra-regional

export space and the actual aggregated intra-regional trade flows in absolute measures,

然而, 经过 2014 both figures have increased by over four times compared with the

scale in 1995, which provides strong evidence of ASEAN’s progress in economic inte-

gration and its increasing export capacity. The gap between the ideal and actual ratio,

然而, hints that there is still a significant amount of space for ASEAN countries to

further strengthen the intra-regional market.

From a broader regional perspective, 然而, Southeast Asian countries have not only

made progress with integration within ASEAN but also within the extended region such

as the ASEAN+3 or ASEAN+6 frameworks. Based on the estimations, the overall mar-

ket space that ASEAN+6 could offer to ASEAN exports in 2014 (80.7 百分) was al-

ready quite close to the space that the integrated EU market could offer to its member

状态 (82.7 百分) for the same year. 事实上, around two-thirds of ASEAN’s exports

go to the ASEAN+6 market in 2014. The formation of RCEP, an arrangement among

ASEAN+6 member states, will further secure ASEAN’s export market, 因此

provide a supportive regional environment for the economic development of ASEAN

成员国.

3.6 Scenario analysis

Our model demonstrates that an exporting country can expand its export space by

either strengthening its export capacity and/or reducing trade resistance, 和

14

Asian Economic Papers

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 7. Impact of trade liberalization on ASEAN’s

export potential

2015

2016

2017

2018

2019

2020

Scenario 1

Scenario 2

Scenario 3

23.75% 23.88% 23.94% 23.92% 23.90% 23.85%

36.54% 36.76% 36.81% 36.85% 36.90% 36.97%

38.75% 39.05% 39.12% 39.20% 39.29% 39.39%

improvement of a region’s export potential could also be achieved by further facilitating

the intra-regional exchange of goods and services. To show ASEAN’s potential gains of

extra export space via further trade liberalization and facilitation (桌子 7) 下列

scenarios are simulated:

• Baseline: All countries keep their effective tariff rates of 2014 and other export-related

特征 (such as trade infrastructure and economic freedom) unchanged in the

following years.

• Scenario 1: Full tariff elimination within the ASEAN community from 2015.

• Scenario 2: ASEAN member states receive full duty-free access to the ASEAN+3 mar-

ket from 2015.

• Scenario 3: ASEAN member states receive full duty-free access to the ASEAN+6 mar-

ket from 2015.

The simulation results of Scenario 1 show that the full removal of import duties on intra-

regional trade within ASEAN will enhance intra-regional trade and expand the region’s

overall export space by almost one quarter. 那是, tariff elimination would potentially

have a significant postive effect on ASEAN’s trade.

In comparison, the potential duty-free access to a broader regional market may induce

额外的 12 到 16 percent increase in ASEAN’s export space in the next five years.

If ASEAN can obtain free access to the ASEAN+6 market under the RCEP, its overall

export space will increase by almost 40 percent over time. In Scenarios 2 或者 3, the share of

intra-regional trade space within ASEAN is lower than that in Scenario 1 where ASEAN

only eliminates tariffs among the ten member states, but it is not much different from the

baseline level. Relatively speaking, it seems less likely that trade liberalization under the

ASEAN+6 framework generates much trade diversion from within ASEAN to the six

neighboring markets compared with the current status quo.

From the global perspective, if ASEAN member states can obtain duty-free access to the

ASEAN+6 market, the overall world trade space will expand by 1.7 百分; if free trade

would only occur within the ASEAN community, we could still see an almost 1 百分

increase in the overall world trade space (桌子 8). This is quite significant when consider-

ing ASEAN’s relatively small share in world GDP.

15

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

桌子 8. Impact of trade liberalization on the overall

world export potential

2015

2016

2017

2018

2019

2020

Scenario 1

Scenario 2

Scenario 3

0.96% 0.99% 1.01% 1.02% 1.03% 1.05%

1.48% 1.53% 1.55% 1.57% 1.60% 1.63%

1.57% 1.62% 1.64% 1.67% 1.70% 1.73%

4. Concluding remarks

In the qualitative literature on regional economic integration, ASEAN is usually singled

out as a counter-model to the EU, characterized by relatively high degrees of de facto inte-

gration in combination with relatively low degrees of de jure integration. When contrast-

ing this image with a series of cross-regional indicators, it appears that it should probably

be more nuanced. The de facto relative importance of intra-regional trade, 投资,

and/or migration flows are close to the global average level. This seems to suggest that

regional economic integration in ASEAN is not necessarily deeper than in several other

地区, as measured by these outcome indicators. This also implies, 然而, that further

gains from deepened intra-regional interdependence can be expected. 然而, the relative

openness of the ASEAN region was confirmed, such that important additional benefits

will come from further reductions of trade barriers vis-`a-vis the rest of the world.

The augmented gravity model used to estimate ASEAN’s export space provided an over-

all satisfactory fit. Intra-regional trade biases were observed for the regions, with ASEAN

thereby finding itself in an intermediate position, because of its intra-regional trade bias

being somehow masked by its generally strong trade orientation. We found that ASEAN’s

average intra-regional trade levels are approximately twice as much as the corresponding

levels among other countries under the same conditions.

It has been observed that ASEAN’s export space is expanding faster than the world av-

erage and that further progress of regional integration among the ASEAN member states

can be an additional positive factor contributing to its regional export capacity. Our es-

timation shows that there is still space for ASEAN countries to further develop intra-

regional trade.

尽管如此, the process of regional integration will still need more driving force from

the market engine. Tariff elimination can still have significant impacts on improving

ASEAN’s export potential, even though the average tariff rate within the region is al-

ready close to zero. It is true that with trade liberalization, industries in developing coun-

tries will face strong competition from advanced economies, but this will at the same time

push these countries to improve their export capacity and benefit from more business op-

portunities that will come along with an expanding global export space. It is in ASEAN’s

16

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

interests to accelerate the pace of regional integration under frameworks that involve also

the participation of non-ASEAN countries, especially the RCEP.

Although RCEP is not a pure south–south free trade initiative; it does involve many de-

veloping and less-developed countries in the Asia-Pacific region. The initiative aims to

build a “modern, 综合的, high-quality, and mutually beneficial FTA” by consol-

idating the existing ASEAN+1 FTAs with the emphasis on strengthening ASEAN’s cen-

trality in regional economic integration, and committing to the compatibility of RCEP’s

rules with the trade principles of the WTO. 在这方面, RCEP seems to be a prag-

matic way to regionalize the sophisticated global production networks via the reduction

of trade barriers and setting of new rules that are consistent with WTO agreements, 这

facilitation of technology transfers and factor mobility, the rationalization and better ad-

ministration of rules of origin, and the improvement of trade governance.

The formation of a free trade area under the ASEAN+6 framework carries a large po-

tential for export growth and economic development, although the conclusion of RCEP

should be seen as a milestone, not an ultimate achievement, of ASEAN’s long-term mis-

sion to build a competitive region with equitable development and deep involvement

into global value chains. The more quickly the agreement is concluded and the higher the

quality it achieves, the more easily can Asia move forward to the next stage architecture

of regional integration.

参考

Ando, Mitsuyo, and Fukunari Kimura. 2013. Evolution of Machinery Production Networks: Linkage

of North America with East Asia. Asian Economic Papers 13(3):121–160.

Baldwin, 理查德. 2004. The Spoke Trap: Hub and Spoke Bilateralism in East Asia. KIEP Discussion

Paper No. 04–02. Seoul: Korea Institute for International Economic Policy.

Baldwin, 理查德. 2006. Multilaterizing Regionalism: Spaghetti Bowls as Building Blocks on the Path

to Global Free Trade. The World Economy 29(11):1451–1518.

Baldwin, 理查德. 2007. Managing the Noodle Bowl: The Fragility of East Asian Regionalism. CEPR

Discussion Paper No. 5561. 伦敦: The Centre for Economic Policy Research.

Bhagwati, Jagdish. 1995. 我们. Trade Policy: The Infatuaqtion with Free Trade Areas. In The Dangeri-

ous Drift to Preferential Trade Agreements, edited by Jagdish Bhagwati and Anne O. Krueger, PP. 1–18.

Washington DC: The AEI Press.

陈, Lurong. 2008. The Market Driven Trade Liberalization and East Asian Regional Integration.

HEI Working Papers No. 12/2008. 日内瓦: The Graduate Institute.

陈, Lurong, and Philippe De Lombaerde. 2011. Regional Production Sharing Networks and Hub-

ness in Latin America and East Asia: a Long-term Perspective. Integration & Trade 15(32):17–34.

Corcos, Gregory, Delphine Irac, Giordano Mion, and Thierry Verdier. 2012. The Determinants of

Intrafirm Trade. CEP Discussion Paper No. 1119. 布鲁塞尔: Centre for European Policy Studies.

17

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

Cuyvers, Ludo. 2014. Some Tough Facts about ASEAN’s Institutional Stalemate. Europe’s World

27:87–88.

Cuyvers, Ludo, and Michel Dumont. 2005. Tigers, Pussycats and Flying Geese: The Faunal

Characteristics of Economic Growth in South-East Asia. In Transnational Corporations and Economic

发展: From Internationalisation to Globalisation, edited by Ludo Cuyvers and Filip De Beule,

PP. 122–140. Hampshire, 英国: Palgrave MacMillan.

De Lombaerde, Philippe. 2014. Measuring and Modeling Regional Power and Leadership. 杂志

Policy Modeling 36(S1):1–5.

Head, 基思, and Thierry Mayer. 2004. Market Potential and the Location of Japanese Investment in

欧盟. Review of Economics and Statistics 864:959–972.

Kimura, Fukunari, and Mitsuyo Ando. 2005. Two-dimensional Fragmentation in East Asia: Concep-

tual Framework and Empirics. International Review of Economics and Finance 14(3):317–348.

Kimura, Fukunari, and Hyun-Hoon Lee. 2006. The Gravity Equation in International Trade in Ser-

恶习. Review of World Economics 142(1):92–121.

Mayer, Thierry. 2009. Market Potential and Development. CEPII Working Paper No. 09–24. 巴黎:

Centre d’ ´Etudes Prospectives et d’Informations Internationales.

的, Francis and Alexander Yeats. 2003. Major Trade Trends in East Asia: What Are Their Implica-

tions for Regional Cooperation And Growth. Policy Research Working Paper Series No. 3084, 这

World Bank.

Redding, 斯蒂芬, and Anthony Venables. 2004. Economic Geography and International Inequality.

Journal of International Economics 621:53–82.

Wakasugi, Ryuhei, Banri Ito, and Eiichi Tomiura. 2008. Offshoring and Trade in East Asia: A Statis-

tical Analysis. Asian Economic Papers 7(3):101–124.

附录A: Description and data sources of exogeneous variables

Variable

描述

Gross domestic

产品 (GDP)

Internet access and

用法 (INTER)

The sum of the gross value added of products and services produced

within a country in a year. For an exporting country, this is an

indicator of its total economic output, and therefore a mirror of its

production capacity. For an importing country, this is a measure

of its overall market capacity or consumption potential.

The percentage of the total population accessing the Internet. 这

Internet is an important channel for knowledge acquisition,

沟通, and productivity improvement. The popularity of

using the Internet is an important measure of a country’s advance

in information and communication technology (ICT); 这

development of ICT will have a positive effect on a country’s total

productivity frontier (TPF).

Data source

The World Bank World

发展

指标 (WDI)

数据库

The World Bank World

发展

指标 (WDI)

数据库

Economic freedom

This is a proxy of a country’s overall degree of trade liberalization.

The Heritage

(FREE)

WTO membership

(WTO)

直观地, countries with freer trade policies trade more, 然而

countries with more restrictive policies trade less.

A dummy variable, of which the value equals zero for years before

the country’s entry to WTO and equals one for years afterwards.

WTO membership provides a stable institutional framework for

trade relations.

Foundation Index of

Economic Freedom

The World Trade

组织 (WTO)

Paved roads (PAVED)

The share of paved roads is an indicator of the level of a country’s

The World Bank World

physical infrastructure. A proper level of infrastructure can

improve efficiency, save time, lower trade risks, 因此

facilitate international trade.

发展

指标 (WDI)

数据库

18

Asian Economic Papers

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

Markets Matter: The Potential of Intra-Regional Trade in ASEAN and Its Implications for Asian Regionalism

附录A: Continued.

Variable

描述

Data source

Inward foreign direct

investments stock

(FDI)

The size of a country’s FDI pool. The bilateral capital and trade flows

UNCTAD FDI database

are highly relevant. Inward FDI can be a proxy of a country’s

openness, market stability, technological progress, and economic

看法.

Distance (DIST)

The geographic distance in kilometers between the countries’ capitals.

CEPII database

This is a proxy of transportation costs and related costs of

international trade. As it is positively related with trade costs, 它

has a negative impact on trade flows.

Simple average

The direct measure of the bilateral tariff rate can be a proxy of de

TRAINS database

bilateral tariff level

(TARIFF)

Common language

(COMLNG)

facto policy friction of bilateral trade. Its accuracy for our purpose

may be affected by the existence of various nontariff barriers,

然而.

A dummy variable, of which the value equals one for countries that

CEPII database

share at least one same official language and equals to zero

否则.

Contingent territory

A dummy variable, of which the value equals one for countries that

CEPII database

(CONTIG)

share border and equals to zero otherwise.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

6

2

1

1

6

8

5

8

3

3

A

s

e

p

_

A

_

0

0

5

1

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

19

Asian Economic Papers