跨学科历史杂志, xliii:4 (春天, 2013), 511–537.

PUBLIC DEBT IN THE PAPAL STATES

Donatella Strangio

Public Debt in the Papal States, Sixteenth to

Eighteenth Century Analysis of the Roman ªnancial sys-

tem highlights how Roman public debt in the pre-industrial pe-

里约德, unlike that in most other European settings at the time, 曾是

used for productive purposes. 例如, Smith pointed out

how England’s public debt helped to pay for the country’s costly

wars, and Braudel described the continuous use of debt ªnance to

bolster imperial Spain during the reigns of Philip II and Charles V,

whereas papal Rome used ªnancial tools primarily to maintain the

public food supply. This article also corrects certain important

details about the Roman ªnancial system in the literature, 这样的

as when the central government’s stable system of debt was

established.1

public debt in europe and the papal states The Papal States

occupied the central regions of the Italian peninsula. They were

divided into several provinces: Rome and its district, the provin-

cial Campagna, Marittima and Lazio, Umbria, Sabina, the Duchy

of Spoleto, Patrimonio, Marca, the Legation of Bologna e Ro-

magna, the legation of Ferrara, Comacchio, the State of Urbino,

Montefeltro, the State of Benevento, 阿维尼翁, and the Venaissin

农村. The collective state was economically fragmented.

Each province had its own currency and its own system of weights

and measures that hindered domestic trade. 罗马, the capital and

the seat of the papal government, was the most populous prov-

ince.

The organization of public debt in Europe varied from nation

to nation, each according to its own circumstances. 然而, 全部

of these states shared a common need for credit to compensate for

Donatella Strangio is Associate Professor, Faculty of Economics, Department of Methods and

Models for the Economy, the Territory, and the Finance (memotef), Sapienza University of

罗马. She is the author of The Reasons for Undevelopment: The Case of Decolonisation in Somali-

土地 (纽约, 2012); “Italian Colonies and Enterprises in Eritrea (XIX–XX Centuries),”

Journal of European Economic History, XXXIX (2010), 597–619.

© 2013 by the Massachusetts Institute of Technology and The Journal of Interdisciplinary

历史, Inc.

1 亚当·斯密, The Wealth of Nations (伦敦, 1904; orig. 酒吧. 1776), 三、, Book V,

Chap. 3, 221; Fernand Braudel, Civiltà e imperi del Mediterraneo nell’età di Filippo II (Turin,

1986), 二, 731–735.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

512 | DONATELLA STRA NGIO

the growing shortfall between tax revenues and public expendi-

真实. Debt ranged from a “ºoating” form, which generally in-

volved short-term, high-interest loans, to a “consolidated” form

bearing a lower interest rate and long-term or indeªnite maturity.2

Throughout the centuries, debt policy in Europe was the re-

sponsibility of government authorities, who typically resorted to

public debt without any speciªc restrictions. In Italy, the best-

known ªnancial markets were those of Rome and Genoa. 谢谢

to its autonomy, Genoa had substantial foreign investments. 这

system for the organization and management of the Papal States’

debt was, from the very beginning, a “technically perfect institu-

的, with a very speciªc purpose, that was to be replicated

throughout the centuries with minor changes being made only to

details.” As noted by Braudel citing Delumeau, the monti cameral

(public pontiªcal debt) system found immediate success: “Since it

tapped an international clientele, it is fairly natural that the public

debt of Genoa began to grow at a slower rate when Rome’s pub-

lic debt became increasingly sizable.”3

Until the end of the seventeenth century, public debt grew

incessantly in Italy. Italian states tended to borrow heavily, 但

never more than the resources available to them allowed. Except

for a few temporary suspensions and occasional changes in interest

费率, public debt was kept under greater control in Italy than in

other European countries, largely because no one would have in-

vested in the ªnances of a small state without watertight guaran-

tees. Seen within the context of the Italian states, public debt in

2 Anthony Molho, Florentine Public Finance in the Early Renaissance, 1400–1433 (剑桥,

大量的。, 1971); Giuseppe Felloni, Gli investimenti ªnanziari genovesi in Europa tra il Seicento e la

Restaurazione (米兰, 1971), 104–105; Enrico Stumpo, Finanza e Stato moderno nel Piemonte del

Seicento (罗马, 1985); Robert Bonney (编辑。), Economic Systems and State Finance (纽约

1995); idem (编辑。), The Rise of the Fiscal State in Europe, C. 1200–1815 (纽约, 1999); Luciano

Pezzolo, “Elogio della rendita: Sul debito pubblico degli Stati italiani nel Cinque e Seicento,”

Rivista di storia eco nomica, XII (1995), 283–233; idem, “Government Debts and Trust: 法语

Kings and Roman Popes as Borrowers, 1520–1660,” ibid., XV (1999), 233–261; idem and

Stumpo, “L’imposizione diretta in talia dal Medioevo alla ªne dell’ancien régime,“ 在

Simonetta Cavaciocchi (编辑。), La ªscalità nell’economia europea secc. XIII–XVIII (Florence, 2008),

75–98; Strangio, “Debito pubblico e sistema ªscale a Roma e nello Stato pontiªcio tra ’600 e

’700,” in ibid., 499–508; Fausto Piola Caselli, “Public Debt in the Papal State: Financial Mar-

ket and Government Strategies in the Long Run (Seventeenth–Nineteenth Centuries),“ 在

idem (编辑。), Government Debts and Financial Markets in Europe (伦敦, 2008), 105–119. 也可以看看

Carlo M. Cipolla, Storia economica dell’Europa pre-industriale (Bologna, 1990), 63.

3 Mario Monaco, “Il primo debito pubblico pontiªcio: il Monte della Fede (1526),” Studi

罗马尼人, VIII (1960), 553–569, 562; Braudel, Civiltà e imperi, 二, 783.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 513

the Papal States was a model of efªciency in its ªnancial manage-

ment and its administrative techniques. In spite of the predomi-

nantly conservative nature of the Roman Curia in economic and

other matters, the Apostolic Camera, the main governing body,

quickly and successfully implemented a debt policy that was in

step with the development of Papal public ªnances by introducing

innovative measures.4

Although Papal public debt was similar to that of other states

on the Italian peninsula and in Europe, the manner of government

in the Papal States, verging on absolute, and the nature of its elec-

torate, 然而, could not help but inºuence the governing of its

ªnances. The absence of a dynasty in Rome meant that whoever

ran the state could act only as a pro-tempore governor. 虽然

continuity was possible in matters of religion, political and eco-

nomic measures varied and, 有时, were even contradictory.

尽管如此, a common denominator of careful administration is

evident in the public-debt policy of all of the popes The differ-

ences in their policies did not derive primarily from the “two-

faced” papal sovereignty, as Reinhardt deªned it, which saw the

pope, 一方面, as the ruler of a medium-sized Italian state,

和, 在另一, as the source of livelihood for the Roman pop-

ulace. As Kaplan pointed out, a state’s condition depended on its

地点, the variety and organization of its culture, and the class

alliances that its creators were able to forge. 最后, 这

way in which rulers, particularly Rome’s, dealt with the problem

of public debt depended on the general policy of state-building

that they adopted.5

The Roman market was a paragon of effective public-debt

management because of the conªdence that the Apostolic Camera

was able to inspire, thanks to its low risk and its high returns rela-

tive to those of other ªnancial instruments (尽管, truth be told,

the area presented few signiªcant investment alternatives). 更多的-

4 Piola Caselli, Il Buon Governo: Storia della ªnanza pubblica nell’Europa preindustriale (Turin,

1997), 239.

5 Paolo Prodi, Il sovrano ponteªce: Un corpo e due anime: la monarchia papale nella prima età

moderna (罗马, 1982); Mario Caravale, Lo stato pontiªcio da Martino V a Gregorio XIII, in idem

and Alberto Caracciolo (编辑。), Lo Stato pontiªcio da Martino V a Pio IX (Turin, 1978), 3–371;

Volker Reinhardt, “Prezzo del pane e ªnanza pontiªcia dal 1563 al 1762,” Dimensioni e

problemi della ricerca storica, 二 (1990), 109–134; Steven Laurence Kaplan, Bread, Politics and Polit-

ical Economy in the Reign of Louis XV (The Hague, 1976); idem, Le complot de famine: histoire

d’une rumeur au XVIIIe siècle (巴黎, 1982).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

514 | DONATELLA STRA NGIO

超过, a highly effective and well-deªned administration reassured

investors.6

The commitment of the Papal States to make good on its

promise to pay principal and interest to bondholders, in the pres-

ence of a budget surplus, represented an additional expenditure to

be met in subsequent ªscal years. These costs were magniªed

when interest paid on current and past bond issues were met by is-

suing new debt. Although this approach seemed less painful, 它

could turn into a vicious circle. 因此, public debt became a bur-

den on savings that extended well into the future, seriously con-

straining opportunities for economic development. The Papal

States underwent a signiªcant rising trend in taxes, ªrst to raise

funds to pay interest and repay debt and second to meet war debts,

which diverted savings from productive uses. Thus did the tax sys-

tem become a necessary complement of the system of national

loans.7

The monti system had, to some extent, a redistributive effect

on the income of the population. 实际上, the increasing expendi-

ture on interest placed a growing tax burden on all taxpayers.

Those who did not buy bonds were hit by new taxes, while bond-

holders continued to collect interest on bonds or purchased addi-

tional bonds, even though they too were required to pay higher

税收. 换句话说, the taxes introduced to pay a greater

amount of interest on bonds, as a result of new issues, 翻译的

into an income shift in favor of the bondholders, the States’ credi-

tors.8

For the nearly three centuries during which the monti system

6 Peter Partner, The Papal State under Martin V: The Administration and Government of the

Temporal Power in the Early Fifteenth Century (罗马, 1958), 131–136.

7 Among classical economists, Thomas Robert Malthus, whose views in this area are similar

to those of John Maynard Keynes, has a different opinion on the effects of public debt. 这

importance that he places on aggregate demand leads him to pay special attention to the posi-

tive effects that the recipients of interest can generate, thus boosting production. 然而,

Malthus was also aware of the problems that might arise from a sizable public debt. See Mal-

因此, Principles of Political Economy (剑桥, 1820); Keynes, “The Colwyn Report on Na-

tional Debt and Taxation,” Economic Journal, XXXVII (1927), 198–212; idem, General Theory

of Employment, Interest and Money (伦敦, 1936). The rising trend especially involved indi-

rect taxes, reºecting a common attitude in most European countries; it was easier to keep an

eye on consumption, customs, and monopolies than to toil at measuring houses, 土地, 和

租金. See Caselli, Il buon governo, 281.

8 Malthus believed that public debt might be a useful distribution tool in some respects.

John Stuart Mill also noted that the transfer of capital from the private to the public sector re-

sults in a loss for creditors. 然而, he added that a public loan might be warranted by the

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 515

was operational, and especially in the seventeenth century, 这

Holy See made extensive investments in building and urban im-

provement. Although the renovation work certainly accelerated

the machinery of indebtedness, since most, if not all, of it was

ªnanced through public debt, it also triggered a demand for labor.

全面的, public debt cannot be viewed in a totally negative light.

The evidence suggests that the construction of St. Peter’s Basilica,

which was ªnanced through ad hoc bond issues, was important

not only for religious and artistic purposes but also for economic

and political ones. 此外, the total number of construction

projects undertaken throughout the Papal States was smaller than

those undertaken in the city of Rome, since funding for them in

Rome was subject to government approval, unlike in the States’

communities and provinces where it was obligatory. This situation

led to an increase in the pressure on provinces for taxes to service

the public debt. 此外, much of the expenditure incurred for

the city had no practical or economic rationale but was simply to

enhance personal prestige or to indulge papal nepotism. 然而,

the economic conditions of the Papal States were such that not

even these incentives could revive it; the economic strategies dur-

ing this epoch did not accommodate public countercyclical ac-

tions or activities designed to correct structural imbalances.9

Few areas had advanced manufacturing capability, 除了

Bologna and its environs and a few other areas scattered through-

out the States that specialized in particular products. 许多

historians and economists who study the seventeenth and eight-

eenth centuries maintain that the bonds diverted capital from

manufacturing and the primary sector. The uncertainties pertain-

ing to the primary sector prompted investors to prefer less risky in-

struments that generated a steady income. Landowners, even new

那些, managed their property with traditional agricultural tech-

好的. Because they were not open to innovation, their estates

were underdeveloped and relatively unproductive, creating a fur-

ther incentive for investors to neglect agriculture and concentrate

on ªnancial assets.10

unproductive use of capital in the private sector. See Mill, Principles of Political Economy (朗-

大学教师, 1915).

9 Caselli, Public Finances and the Arts in Rome: The Fabbrica of St. Peter’s in the 17th Century, 在

Michel North (编辑。), Economic History and the Arts (维也纳, 1996), 53–66.

10 Loans became primarily a means to achieve a steady rate of return on wealth, a rational

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

516 | DONATELLA STRA NGIO

Another important consideration was the capital that foreign

investors siphoned from the state during the sixteenth, 七-

第十, and eighteenth centuries. Capital outºows due to interest

paid on public debt was a common problem in most European na-

民族国家. Even Smith regarded the notion that “it is the right

hand which pays the left in the payment of interest on public

debt” as untrue, because it assumed that public debt was essentially

funded by a nation’s own inhabitants. History has proved this

theory to be incorrect, as shown most famously by the English

debt, a substantial portion of which was held by the Dutch in the

form of public bonds.11

the monti system Public debt in the Roman State was funded

in two ways at this time, ªrst and foremost by borrowing through

the monti system and then through ufªci vacabili, or the sale of

public ofªces and titles by the Curia. Whoever bought an ofªce

exercised its functions until his death, garnering all of its payments

and beneªts. But the monti system, which was introduced later,

eventually overshadowed the importance of the revenues gener-

ated by the sale of ofªces, the practice of which continued, 甚至

marginally, 直到 1898 when it was ªnally banned by Leo XIII.12

The word monte, from the Latin mons meaning “mountain,”

signiªed a stack or a pile—a monte of cash lent to a body for a spe-

ciªc purpose. The different types of monte took their names from

the group whose assets were given as collateral for the loan.

因此, the Monti Camerali originated with the Reverenda Camera

Apostolica (Reverend Apostolic Camera); the Monti Comunitativi or

economic and social investment; debt, which was increasingly a tool of rational investment

for a growing number of people in both the towns and countryside, was still, for many of the

rural poor, the source of their exploitation. See Thomas Brennan, “Peasants and Debt in

Eighteenth-Century Champagne,” Journal of Interdisciplinary History, XXXVII (2006), 175–

200, 176, 200; Gérard Béaur, Le marché foncier (巴黎, 1984); Philip Hoffman, Gilles Postel-

Vinay, Jean-Laurent Rosenthal, “Economie et politique: les marches du credit à Paris, 1750–

1840,” Annales, 49 (1994), 65–98; idem, “Redistribution and Long-Term Private Debt,” Jour-

nal of Economic History, LV (1995), 256–284; Postel-Vinay, La terre et l’argent (巴黎, 1998).

11

12 Research has still not been able to pin down the date of origin for the practice of selling

public ofªces and titles in the Papal States. 然而, it was certainly a common occurrence

by the beginning of the ªfteenth century. See Caselli, “Aspetti del debito pubblico nello Stato

Pontiªcio: Gli ufªci vacabili,” Annali della Facoltà di Scienze Politiche dell’Università degli Studi di

Perugia, XI (1970–72), 101–170; Stefano Levati, “La venalità delle cariche nello Stato

Pontiªcio tra XVI e XVII secolo,” Ricerche Storiche, XXVI (1996), 525–543.

史密斯, 国富论, 三、, Book V, Chap. 3, 238.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 517

Comunitari (Community Debt) derived from town councils; 和

the Monti Baronali were created for the beneªt of noble families.

These latter instruments were much favored by investors until the

second half of the sixteenth century, when their prices began to

fall (作为, 的确, did the returns for investors) due to the difªculties

experienced by these families in fulªlling their ªnancial obliga-

tions.13

The various monti had different characteristics, though their

basic organizational features, which ranged from interest rates to

monetary units, were the same. The Bologna and Ferrara monti

borrowed considerable funds; these two cities ranked second and

third among the Papal States for the extent and management

structure of their public debt. The monti system also included

funds borrowed by the city of Rome. Other types of monti were

those named after their intended purpose, the name of the pope

who authorized them, or their terms of maturity. Distinctions be-

tween them were made on the basis of the redeemability of the

loan, or lack thereof. Sometimes this clause was not even spec-

iªed, leaving debt administrators considerable freedom in deter-

mining the repayment schedule.

Bonds issued under these monti were called luoghi di monte

(literally, mountain places), to indicate a fraction of the bond or

nominal shares, either vacabili (vacatable) or non vacabili (nonvacat-

有能力的). Vacatable bonds were restricted to the life of the investors,

who could not leave them to their heirs. When their holders died,

the Apostolic Camera repossessed their vacatable bonds and resold

them in the market for a net gain equivalent to the market price.

In the case of freely negotiable vacatable bonds, which could be

sold to anybody, the last buyer had to relinquish ownership upon

the death of the ªrst investor. The nonvacatable bonds were

bequeathable to heirs. All of these conditions affected the nominal

interest rates paid, which were higher in the case of vacatable

bonds due to their higher risk.

Current research appears to indicate that the ªrst pope to set

13 Giovan Battista De Luca, Tractatus de ofªciis venalibus vacabilibus romanæ curiæ auctore Joanne

Baptista De Luca S.R.E Cardinali cui accedit alter tractatus eiusdem Auctoris de locis montium non

vacabilium Urbis (罗马, 1682); Felloni, Gli investimenti ªnanziari, 180–200; Mauro Carboni,

Il debito della città: Mercato del credito ªsco e società a Bologna fra Cinque e Seicento (Bologna, 1995);

idem, “Public Debt, Guarantees and Local Elites in the Papal States (XVI–XVIII Centuries),”

Journal of European Economic History, 我, (2009), 149–174.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

518 | DONATELLA STRA NGIO

up a monti system was the Florentine-born Clement VII, who was

elected in 1523. He used it for the ªrst time in 1526 to support

Charles V in his war against Suleiman II, emperor of the Turks,

raising debt on behalf of the dominions of the Holy See by placing

2,000 bonds in the market. Paul IV followed his example in sup-

port of Francesco I of France against the “heretic” Huguenots by

borrowing funds through the Monte Pio, First Monte Soccorso, 秒-

ond Soccorso, and Monte Avignone for a total of 10,000 bonds worth

in total 1,000,000 scudi. These monti were added to the Monte

Recuperato or Ristorato after the reform of Alexander VII.14

在 1571, Pius V issued additional bonds in the Monte della Fede

and Monte Novennale and established new monti, such as Leggi

(Laws) and Religione (宗教), to raise 2 million scudi. He also

enacted new ªnancial measures after forming an alliance with

Filippo II of Spain and the “Veneto nation” against Selim II, 这

Ottoman emperor who was eventually defeated at the battle of

Lepanto. Sixtus V also helped to defend the “Catholic cause” by

providing support for Philip II of Spain against England and for

Mary Stuart, the Catholic cousin of Elizabeth I. 为了这些目的, 他

established the Monte S. Bonaventura to issue 3,000 bonds and raise

300,000 scudi.15

之后, other bonds were issued for various military expedi-

tions or fortiªcations and for work on the ports of Ancona and

Civitavecchia (and its arsenal). There is evidence of a vacatable

Monte Difesa (defense bond) 在 1663, extinguished in 1664, 还有

as a nonvacatable defense bond in 1663, extinguished in 1685, 和

defense bonds issued by Clement XI in 1708 to pay for the extra

expenses incurred during the War of Succession. In all, Marchetti

calculated that approximately 19,632,143 scudi were spent on the

Catholic cause between 1542 和 1716, thanks to the public

debt.16

Clement VI’s monte of 1526, 然而, does not appear to

represent a watershed, since the practice of raising funds from pri-

14 摩纳哥, “Il primo debito pubblico,” 562, writes that Clement VII was encouraged to

adopt this instrument by the government of Florence, his native city, where he had served for

a long time. Camerale I, Pontiªcal chirographs, 乙. 164, Chirograph by Alexander VII dated

六月 10, 1656, Archivio di Stato di Roma (hereinafter asr).

15 Gaetano Moroni, Dizionario di erudizione storico ecclesiastica da SS. Pietro ai nostri giorni

(威尼斯, 1846), XL,150.

16 Giovanni Marchetti, Calcolo ragionato del denaro straniero che viene a Roma, e che se ne va per

cause ecclesiastiche (罗马, 1800).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 519

vate sources was already widespread at both central and local levels

and in different forms. 的确, the existence of monti generated

by the sale of debt instruments to investors certainly pre-dates that

年. Documents relating to public debt incurred to ªnance the

restructuring of port strongholds place the 1526 event into a more

exact historical perspective. Particularly meaningful is the text of a

bull by Niccolò V, dated July 29, 1454, whereby he conªrmed a

resolution taken by the embattled port city of Ancona to raise

money to strengthen its mercantile facilities and military fortiªca-

tions against pirate raids and the Turkish threat in the eastern

Mediterranean, especially after the fall of Constantinople in 1453.

This last event, 尤其, had disrupted or introduced sig-

niªcant risks into trade with the East, one of the main sources of

livelihood for the city of Ancona. With the pope’s approval, 这

city council created a public monte (“unum montem publicum magne

quantitatis pecunie”), assigning its governance (“gubernationem”) 到

city ofªcers vested with the power to offer the bonds to private in-

vestors at the best possible price and to pay an interest rate of

5 percent per annum on the nominal value of the bonds sold.

Ancona’s situation marks one of the ªrst times that the term

monte was used in a ªnancial document of the Papal States to indi-

cate the public raising of private funds. 然而, the document refers to

an even older, unspeciªed monte, without offering any direct in-

formation about it. Proof that Ancona had, 实际上, inaugurated a

public-debt transaction is given by further explanations offered by

the pope about the transaction. 特别是, he noted that al-

though the city would receive a lower return (“lucrum”) than that

generated by mercantile ventures, the buyers of the securities

would improve the city’s welfare and make it possible to provide

for various underprivileged members of the community. Obvi-

乌斯, the Pope forgot to add that, in the event of a fall in mercan-

tile proªts, public debt would represent a safe haven for the

富裕.

The application of the general regulations governing the pa-

pal public debt issued to fund public works, as managed by local

当局, did not present special difªculties. Not even in matters

of taxation were local authorities totally autonomous; 他们是

subject to policies and controls that the central authorities installed

as soon as a debt was issued. Local ofªcials interested in raising

funds had two options: They could either join a monte established

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

520 | DONATELLA STRA NGIO

by the Apostolic Camera, with the resulting assignment of a pre-

established share of the proceeds of the bond sale, which would

eventually be serviced for them, or they could request permission

to set up their own monte, which they would manage from be-

ginning to end under the general supervision of the central au-

thorities. 最终, these transactions involved the use of certain

taxes to pay principal, as required, and interest. This lien on tax

revenues had to be approved by the central treasury, 因为它

might involve tax revenues intended for the Apostolic Camera,

但, in any case, it also had to be approved by local authorities.

Debt issued in this way could be repaid with old taxes, but new

ones could also be introduced.

management of the public pontifical debt The administra-

tive and management structure of public debt was streamlined and

consolidated over the years to achieve the level of efªciency nec-

essary to inspire conªdence. Bonds were the safest investments for

investors. Public-debt administrators projected a reassuring man-

agement style, such as that of the Apostolic Camera, 的作用

which was to raise the funds necessary to meet growing public ex-

penditures.17

The increasing success of the monti system is reºected in the

rising trend of the total nominal value of the bonds issued, 作为

shown by the nonvacatable bonds issued for three centuries, 和

throughout the eighteenth century, by the Apostolic Camera’s

debt monti—the Monti S. Pietro I to IX, S. Paolo Religioni, Restaur-

ato II, Restaurato III, Abbondanza, Nuovo Comunità, and Monte Di-

fesa. These data were taken from records kept at the State Archives

of Rome in the series comprised of “ªelds” (Broliardi) and “li-

censes” (Patenti). The ªelds recorded the consent of those who

had subscribed to the bond; the licenses represented the actual

bonds that legitimized their ownership and therefore the availabil-

ity of the credit.

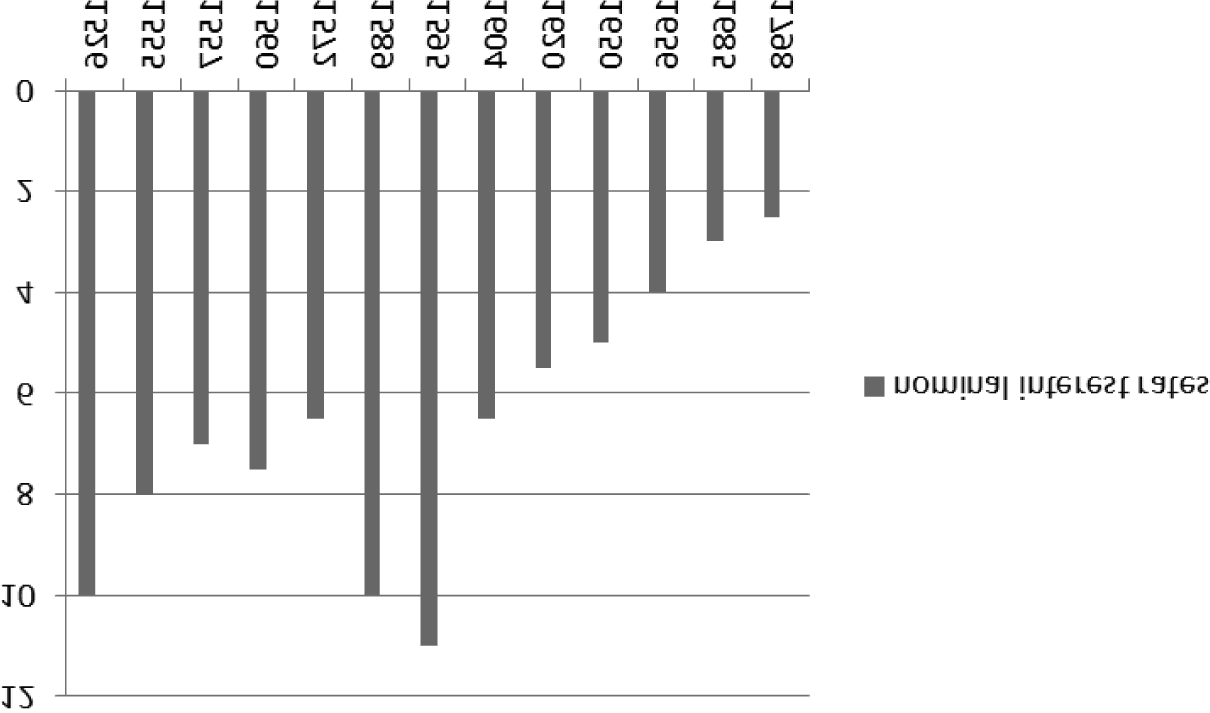

Unlike the interest rates on the total amount of bonds, aver-

age nominal interest rates on the nonvacatable bonds issued by the

monti camerali evince a falling trend (see Figures 1a and 1b), partly

because of the government’s intention to cut the deªcit radically.

The lower interest rates and the repayment of bonds managed to

17 Camerale II, Conti di entrata e di uscita della Camera, bb. 8–15, asr.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 521

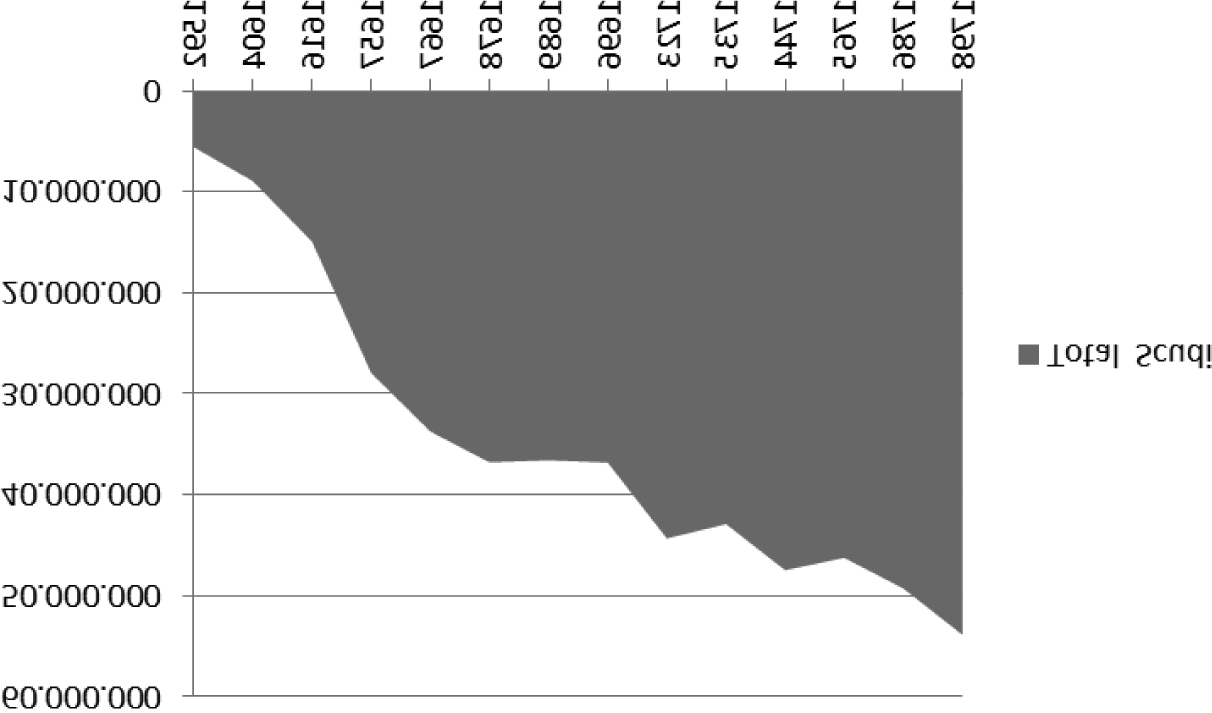

如图. 1a Trend of Capital Underwritten in the Papal States

source Archivio di Stato di Roma: Luoghi di monte bb. 1139–1146, 1159–1181, 1185–

1187, 1192–1213, 1218–1230, 1233–1239, 1243–1265, 1269–1291, 1295–1317, 1321–1343,

1347–1369, 1373–1378, 1379–1388, 1390–1395, 1399–1402, 1399–1421, 1425–1430, 1444–

1447, 1470–1473, 1496–1499.

reduce the Apostolic Camera’s level of indebtedness to some ex-

帐篷. 实际上, interest rates were falling throughout Italy, 也

国外. Interest-rate changes in France during the eighteenth cen-

tury seemed to follow a pattern similar to those in Britain, 尽管

absolute values differed. 最初, interest rates were high in both

国家, but declined signiªcantly during the ªrst two or three

decades of the eighteenth century, remaining relatively low for a

while before rising steeply in both countries. During the eight-

eenth century, Britain managed to cut the interest rate that it paid

on consolidated debt from 8 percent or higher to about 3 百分

by mid-century, though it was unable to keep it so low. 长的-

term Dutch interest rates, 然而, remained much lower than

这 5 percent prevailing in France.18

The nominal interest rates on nonvacatable bonds (哪个

were ªxed in the indenture of the bond issue and depended on

market interest rates) decreased from an initial 10 百分比到 7 每-

cent in the 1560s, until they reached around 6 percent by the end

of the century, 4 之间的百分比 1656 和 1683, 和 3 百分

18

Sidney Homer and Richard Sylla, A History of Interest Rates (伦敦, 1991), 232, 240.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

522 | DONATELLA STRA NGIO

如图. 1b Trend of Nominal Interest Rates in the Papal States

source Archivio di Stato di Roma: Luoghi di monte bb. 1139–1146, 1159–1181, 1185–

1187, 1192–1213, 1218–1230, 1233–1239, 1243–1265, 1269–1291, 1295–1317, 1321–1343,

1347–1369, 1373–1378, 1379–1388, 1390–1395, 1399–1402, 1399–1421, 1425–1430, 1444–

1447, 1470–1473, 1496–1499.

从 1685 to the end of the eighteenth century (see Figure 1b).

Pope Alexander VII’s administration tried to tackle the debt, ªrst

by converting several vacatable bonds into nonvacatable bonds,

thus lowering their nominal interest rates. The montisti (bondhold-

呃) were given the option of investing in newly issued bonds

(every bond held would be exchanged for one and a half newly is-

sued bonds) or of receiving repayment of the bonds held at par.19

The measures undertaken to curb interest expense, which ac-

counted for more than 50 percent of the Apostolic Camera’s reve-

nue, continued through the repayment of old 4 percent nonvacat-

able bonds and the issue of new bonds at a lower interest rate.

Bondholders were given the option of being repaid at par (100

scudi per bond) or transferring their ownership to new bonds bear-

ing a 3 percent interest rate—the going interest rate for all bonds

自从 1683, when Innocent XI had implemented a far-reaching

but only partially successful public-debt consolidation and conver-

sion policy. The effort to reduce debt accompanied other cuts on

Stumpo, Il capitale ªnanziario a Roma fra Cinque e Seicento: Contributo alla storia della ªscalità

19

pontiªcia in età moderna (1570–1660) (米兰, 1985), 258.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 523

ofªces for sale, 职员, and other expenses. Although they had a par

value of 100 scudi, bonds were freely negotiable and had an im-

portant secondary market; they could be easily sold above par at

127 和 130 scudi romani (obviously the issuer repaid only the

nominal value of the bond).20

The pope headed the administration of the monti, authoriz-

ing the creation of new bond issues with a papal chirograph, 和

the Apostolic Camera was responsible for coordinating the various

administrative structures for ªnancial and cash management and

控制 (through the general depositary). Every monte had its ad-

ministrative ofªce in Rome; four departments carried out the rel-

evant functions—a secretariat; a bookkeeping unit for the speciªc

monte, which was merged into the general accounting depart-

ment in 1732; and a depositary department.21

The secretariat, with its own supervisor, was the administra-

tive center; the bookkeeping unit assigned to a monte kept the re-

cords of the issue. One of its main tasks was to draw up a complete

and updated alphabetical list of investors for the depositary, 印迪-

cating the bonds attributable to each investor. The general book-

keeping department was responsible for recording all of the state’s

expenses on the basis of the data provided by the units assigned to

the individual monti. In January 1732, Clement XII decided on

他自己 (“Motu Proprio”) to merge the individual bookkeeping

units into the general bookkeeping department, which underwent

a series of reforms that changed its organizational and administra-

tive structure. One of these reforms was passed by Pope Prospero

Lambertini, Benedict XIV,

这

Apostolicae Sedis Aerarius (Apostolic tax department), to implement

stricter centralized accounting controls, which were common

thoughout Europe by then. The main tasks of the depositary in-

through the establishment of

20 Felloni, Gl investimenti ªnanziari, 163–164; Camerale II, Luoghi di monte, 乙. 3, asr. 这

sources report the prices on the secondary market value of the other luoghi di monte (期间

the same period). The bonds of the Monte S. Pietro (I–IX) could easily be sold above par at 132

scudi romani or 127 和 119 scudi romani at the end of the eighteenth century; Monte

Ristorato and Monte delle Comunità could be sold at 108 和 111; Monte S. Paolo delle Religioni

could be sold at 105, 例如. The fees for the broker (who was a ªnancial intermediary)

must be added. The scudo was the silver coin of the Papal States; its value in grams silver was

26.398 (Camerale II, Zecca b. 3, asr).

21 Caselli, “La disciplina amministrativa ed il trattamento ªscale dei luoghi di monte della

Camera Apostolica tra il XVI e il XVII secolo,” in Manuel J. Peláez (编辑。), Historia Economica y

de las Istitutiones Financieras en Europa: Trabajos en Homenaje a Ferran Valls I Taberner (巴塞罗那,

1989), 3525–3549, 3533.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

524 | DONATELLA STRA NGIO

volved the payment of interest on pre-established dates and the re-

payment of the bonds drawn, thus basically acting as cashier.22

the negotiability of the luoghi di monte Tradability, 或者

ability to transfer securities from one investor to another, 做作的

the price of bonds, which varied in accordance with supply and

demand conditions in the secondary market. Supply and demand

in the bond market were also subject to the nature of the bonds

and their associated rights. Expenditure for such urgent circum-

stances as war, famine, and public works was increasingly ªnanced

through public borrowing.23

Often ªnanciers, especially foreign ones, purchased entire

bond issues, particularly in the sixteenth and seventeenth centu-

里斯. Marcantonio Ubaldini and his Florentine merchant col-

联赛, 例如, bought the entire Monte Sisto issue of vacat-

able bonds, and in the eighteenth century, both Monte di Pietà

and Banco di S. Spirito placed bonds. Although the creation of the

monti system was initially considered an effective, but exceptional,

way of raising funds quickly, 从长远来看, the monti came to

represent ordinary revenue that a pope could generate at will. 在-

契据, debt issuance was substantial in the sixteenth and seven-

teenth centuries. It fell slightly during the ªrst half of the eight-

eenth century, only to rise again by the end of the second half.

Pius VI repeatedly resorted to public borrowing to implement the

reforms that he designed to stimulate the economy. The increase

in debt came to a temporary halt only with the birth of the Jacobin

Republic in 1798.24

The monte was highly successful in the Papal States, 尽管

its associated costs. Competing directly with other types of invest-

蒙特, it marked a departure from the previous system of extract-

ing forced contributions from taxpayers and engaging in relation-

ships with bankers. It was a way of tapping directly into capital

22 Camerale II, Luoghi di monte, 乙. 2; Camerale II, Computisteria Generale, 乙. 1, asr.

23 Franciso P. Zech, Rigor moderatus doctrinae pontiªciae circa usuras a SS D. 氮. Benedictus XIV.

per epistolam encyclicam episcopis Italiae traditus. Dissertatio III. inauguralis sancti Rigoris specimina

exhibens moderationis pontiªciae (Ingolstadt, 1751), 150–225.

24 These two public banks were required to purchase entire issues, or fractions thereof

(Camerale II, Luoghi di monte, 乙. 11; Camerale II, Dataria, 乙. 3, asr). Caselli, “La diffusione

dei luoghi di monte della Camera Apostolica alla ªne del XVI secolo: Capitali investiti e

rendimenti,” in Giovanni Zalin (编辑。), Credito e sviluppo economico in Italia dal medio evo all’età

contemporanea (Verona 1988), 191–216.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 525

市场, in which lending transactions occurred mostly between

private parties. 此外, these bond issues were intended to

raise funds for welfare services and for public works, thus achiev-

ing the political objective of setting up a social security system in

the city.

The governmental authorities placed a strong emphasis on the

guarantees provided by the bonds to inspire the conªdence of in-

vestors. No effort was spared to ensure bondholders their interest

as it became due, as well as the repayment of principal. 自从

regular payment of interest on bonds issued was considered neces-

sary and sufªcient for the Apostolic Camera to project an image of

safety and stability, the funds earmarked to pay interest, such as tax

revenue or funds from property, were identiªed as “certain reve-

nue.” Regular interest payments were necessary not only to in-

spire conªdence but also to enable the government to have a con-

siderable number of investors ready to subscribe to public bonds at

any time.

The Dutch case is similar to the Roman one. The Bank of

Amsterdam attracted foreign lenders, stabilized currency transac-

系统蒸发散, and provided safe deposit facilities for local merchants. Great

conªdence was placed in the honesty of the ªnancial arm of the

government in the Netherlands until the end of the eighteenth

century when a shroud of secrecy surrounding public ªnances

generated suspicions of malfeasance. Investors’ conªdence in the

Roman monti was also strengthened by detailed regulations for

administrative procedures.25

Besides the ªnancial returns, bondholders received a number

of other beneªts, especially from a well-developed secondary mar-

ket. 实际上, the ease with which bonds could be traded gave bond-

holders the certainty that, in case of need, they could easily con-

vert them into cash. The Apostolic Camera itself encouraged

bondholders to re-invest repaid principal in other bonds and not

to collect it, setting an example by purchasing securities under its

own name through the general treasurer.26

Anybody could purchase and own securities—from church-

In the Papal States, as already noted, payment took place through a contractor and the

25

treasury system. In case of need, 然而, two Roman banks, the Banco di Santo Spirito and

the Banco del Monte di Pietà, were used. The role of these two institutions would become in-

creasingly important during the eighteenth century. See Homer and Sylla, 历史, 201, 236.

26 Luoghi di monte bb. 2460–2463; A.S.V., t. 203, ff. 49–52, asr.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

526 | DONATELLA STRA NGIO

men and religious orders to minors, 女性, invalids, and foreign-

呃. 此外, bondholders were exempt from the seizure and

conªscation of their bonds for any crimes that they committed,

except for lese-majesty and heresy. The state’s growing demand

for credit was met by the willingness of individuals and groups to

lend their funds. A large proportion of individual savers came from

members of the middle class, who invested modest amounts to

purchase bonds or spezzature (fractions of bonds). Because there

were many small investors, the nominal interest paid was com-

mensurate with the fractions of bonds purchased.27

the use of the monti system to augment the food supply

The papal government used the monte system for different pur-

姿势, including such important functions as the distribution of

food through the department of the Annona, which maintained

the grain supply, and the implementation of agricultural policy.

In the Papal States, but especially in Rome, “the central role

of charitable works in the governance of the city somehow high-

lighted the differences in organization between Rome and other

contemporary capitals and distanced the city even further from the

policies and measures that elsewhere marked the ªrst reforms in-

spired by the Enlightenment.” This charitable work was not just a

matter of providing good governance; it also created social har-

mony through the public organization of social assistance, 在下面

the watchful eye of the political authorities. Rome had to set an

example of Catholic and Roman charity. 的确, the eighteenth

century witnessed the progressive “institutionalization” of hospi-

tals, alms houses, and orphanages—“this being a slow process of

took place under Benedict XIV,

rational reorganization that

thanks to the activities of the Apostolic Visitors.” Historiography

has highlighted the increasingly strong links between the charita-

27 Women could invest autonomously. 然而, their investments were due mainly to

bequeathed dowries, inheritance, or donations (在这种情况下, the sum necessary to purchase

bonds was provided by the family of the bride). The bride held title to the bonds, but the hus-

band had full use of the interest. 因此, these situations were exceptional, and the intention to

purchase was limited, or even nil, thus giving further evidence that the status of women was

akin to that of incapacitated persons and, 像这样, requiring special protection. See Fabritii

Evangelista, Opus de locis montium cameralium non vacabilium (罗马, 1767), 88. 有

many nonresident foreigners. The majority of them were either from Genoa or Florence, liv-

ing in the Papal States for commercial and ªnancial reasons. See Felloni, Gli investimenti

ªnanziari, 200; Piola Caselli, La diffusione dei luoghi di monte, 212–213.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 527

ble and social-assistance policies of the central and local authori-

领带, which aimed to satisfy the needs of those members of the

population who were unable to support themselves through their

own work or “with the help of their family network, 这是

also required by law.”28

Demographic growth in Rome, especially from the mid-

ªfteenth century onward, was due mainly to immigration, 或者

更确切地说, the migration of rural masses to the cities. 如何-

曾经, in contrast to the events taking place in England, for in-

姿态, one of the reasons for the exodus of farm laborers from the

Roman countryside to the city was their extreme poverty. 一次

in Rome, these people did not encounter any process of “forced

recruitment” for labor; many of them resorted to begging for food

as the city’s economic structure could not absorb them. A docu-

ment dated 1693 shows that the authorities were aware that intro-

ducing regulations for founding charities would be pointless with-

out a serious commitment to provide relief for the poor.29

Religious charity was not an end in itself, but in due course,

the links between the central authorities and the popes’ direct in-

tervention through the institutions and subsidies of “Roman char-

ity” became increasingly stronger. The work of both types of

charity could be seen through the States’ Opere Pie (Charitable

Works), confraternities, the popes’ alms (which were recorded in

the accounts of the Apostolic Camera), public largesse—such as

the bread handouts that took place twice a week—and the system

of public debt—such as the New Monte Abbondanza.

Managing food supplies was a priority throughout Europe for

a good part of the early modern era. The exact nature of the prob-

lem in each country depended on its location, the diversity of its

文化, the class alliances of those in power, and the general strat-

egy of local governance. Several factors contributed to the vulner-

28 Maura Piccialuti, La carità come metodo di governo: Istituzioni caritative a Roma dal pontiªcato

di Innocenzo XII a quello di Benedetto XIV (Turin, 1994), 19, 247; Angela Groppi, “Birbanti e

poveri benestanti: attitudini e pratiche assistenziali nei confronti della vecchiaia nella Roma

pontiªcia (secc. XVI–XVIII),” in Vera Zamagni (编辑。), Povertà e innovazioni istituzionali in

Italia: Dal Medioevo ad oggi (Bologna, 2000), 259–277, 260.

l’évolution

29 Claudio Schiavoni

démographique à Rome: 1598–1824,” Annales de démographie historique, XIX (1992), 91–109,

98–99; Maurice Dobb, Problemi di storia del capitalismo (罗马, 1991; orig. 酒吧. 1946), 243–

247. Istituzioni e regole degli Ospizi generali per li poveri da fondarsi nello Stato Ecclesiastico di ordine

della Santità di Nostro Signore Papa Innocenzo XII (罗马, 1693), asr.

and Eugenio Sonnino, “Aspects généraux de

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

528 | DONATELLA STRA NGIO

ability of food supplies—the low productivity of agricultural labor,

climatic uncertainties, difªculties in the transportation system, 和

a lack of resources. 作为结果, countries set up political

and administrative schemes to alleviate the problem, the ration

system being one of them. The primary task of these schemes was

to bring food from places of production to places of consumption.

Other functions ranged from price controls to the control of ºour

and bread quality, and from the organization of stocks to the sale

of stocks to retailers.

In the agricultural sector, 例如, a review of the An-

nona’s accounts reveals its extensive credit activities, in wheat and

especially money. It had pre-emptive rights on the wheat of its

borrowers. In areas with highly intensive wheat cultivation, 当地的

authorities established near-exclusive relations with major produc-

呃, arranging their ªnancing while leaving small producers in the

clutches of local usurers. Because farmers who obtained seeding

loans from the prefect of the Annona and the provincial commis-

sioners sold only part of their wheat, retaining the rest of it for

speculative purposes, a law was introduced to forbid these farmers

from selling their stockpiles before they repaid their debt with the

Annona or received authorization from the prefect or the com-

missioner to sell in order to repay it. Farmers often borrowed di-

rectly from traders, who were thus able to secure their wheat pur-

chases before harvest. The net effect of hoarding was to deplete

the market and drive prices up. In Rome, as well as in the Papal

状态, authorities attempted to solve the problems of fraud by

farmers and wasteful loan dispersion through borrowing.

Loans channeled through the public monte system to farmers

or communities that needed them to expand or simply engage in

their usual agricultural activities were issued through the system of

public bonds, funded by speciªc papal chirographs. Local city

councils

sent a single representative from their membership,

armed with a letter from the local governor, to the Sacra Congrega-

zione del Buon Governo (Holy Congregation of Good Government,

which mediated between communities and the Apostolic Camera)

in Rome to sanction their proposals. This agent remained in

罗马, taking care of his community’s business and checking on

the sale, and any draw on, its bonds. When the Congregation of

Good Government approved an application, notifying a commu-

nity of its admission to the Monte Nuovo Abbondanza, it cancelled

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

PUBLIC DEBT IN THE PAPAL STAT ES | 529

all previous loans and other facilities. The immeditate beneªt to a

community would be a lower rate of interest, compared to the

typical 5 到 7 percent charged by individual lenders.30

The Monte Nuovo Abbondanza delle Comunità, created ex-

pressly for communities, was issued on September 3, 1735, with an

indeªnite amount of bonds to be underwritten to meet the ªnanc-

ing requirements of as many communities as possible. It and subse-

quent monti had all of the negotiability and unrestricted rights ac-

cruing to nonvacatable bonds. The nominal price of each bond

曾是 100 scudi, tax-free; investors paid only for the despatch of the

securities.

The use of public borrowing to ªnance food supplies in the

communities of the Papal States was not new, though the speciªc

purpose of raising funds for the purchase of wheat was. Two other

issues of this loan occurred in September 1763 and September

1779, when famine hit the Papal States, 但, unlike the earlier is-

起诉, not all of the debt was repaid (见表 1). This loan saw a

further extension with the Papal Chirograph of August 1766. 这

involvement of the state in this monte guaranteed potential lend-

ers the fulªllment of the terms and the communities their grain

supplies in mutual equity. Through the organ of the Sacred Con-

gregation of Good Government, the communities collected funds

and paid for their admission to the monte, including both the

nominal price of the securities and the interest to the secretariat of

the Chamber. The capital needed to extinguish the bonds was col-

lected in the Depositary of the Apostolic Camera. To guarantee

the regular payment of interest and to help the communities that

had to amortize the debt, new taxes were levied with a papal

Motu Proprio in August 1764. 此外, in the case of an ex-

tinction of a monte or part of it, an obliged community had to pay

the secretariat of the Chamber only the price of the nominal value

of the issue, thus protecting itself from possible speculation.31

The data obtained from the general registers of the montisti

show that in 1736 (这些年 1735 到 1736, when the loan was ªrst

S. Congregazione del buon governo, serie XII, 乙. 1694, asr.

30

31 Camerale II, Luoghi di monte, 乙. 6. Cfr. Evangelista Opus de locis montium, 帽. 二, p. 9;

Camerale II, Luoghi di monte, 乙. 6; Camerale I, Registro dei chirograª, reg. 177, cc. 39–42;

Bandi, bb. 472–478; Camerale II, Luoghi di monte, 乙. 6; S. Congregazione del Buon

Governo, serie XII, 乙. 1706; Camerale II, Luoghi di monte, 乙. 6; Camerale I, Registro dei

chirograª, reg. 177, cc. 39–42, asr.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

530 | DONATELLA STRA NGIO

issued, coincided with a famine), the number of loans increased to

1,499, but the following two years saw a signiªcant decrease

(1,118 在 1737 和 453 在 1738). This trend continued gradually

直到 1756, when there were only seven loans (直到 1760) 和

then ªve until 1763 (见表 1).

As Table 1 indicates, the number of loans, net of repayments,

steadily increased from 2,084 在 1764 到 12,530 在 1768 (从 1764

到 1766 wheat was in short supply), followed by a slow, steady de-

cline until 1779 (8,848) due to higher reimbursements

比

underwritings. Despite an increase in 1780 (9,188), the year of the

third issue, the number continued to fall until 1783 (7,946). 从

this year onward, the number of loans remained constant at 7,946

直到 1814, as a result of lost drawings.

桌子 2 shows the overall situation of the Chamber public

debt with the amount of nominal capital for loans, net of repay-

评论, in correspondence with the years of issue and the emission

of the Monte Nuovo Abbondanza securities. So far as the latter is

担心的, callable debt consolidation answered the need to meet

a temporary cash deªciency among the communities that were

supposed to purchase wheat.32

The percentage of the total debt that the Monte Nuovo Ab-

bondanza comprised during its three issues varied from 0.1 到

0.4 之间的百分比 1735 和 1737, 从 1 到 3 之间的百分比

1765 到 1768, 和来自 1.9 到 1.6 之间的百分比 1780 和 1783

(见表 3). These percentages are the lowest for the value of a

single monte in relation to total debt, except for those of the

Monte San Paolo delle Religioni for the years 1765 到 1768 和

1780 到 1783 (see Tables 2 和 3). The loans with which the

Monte Nuovo Abbondanza are compared, 然而, had won the

conªdence of investors, based on a global rating that had been

formed over many years.

During the same period of time (那是, the three issues of

loans), 然而, the data on the number of bonds issued reverse

these positions. The results of issues, 实际上, show that the Monte

Nuovo Abbondanza recorded the highest number of bonds issued

和, 最后, a considerable amount of nominal capital for

这些年 1735 (surpassed only by the Monte S. Pietro II), 1763,

1779, 和 1736 (exceeded only by the Monte S. Pietro III), 1765

32

S. Congregazione del Buon Governo, serie XI, 乙. 1707, 法西斯. 1704, asr.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

桌子 1 The Amount of Luoghi di Monte in the Monte Nuovo Abbondanza

(1735–1814)

年

luoghi

di monte

年

luoghi

di monte

1735

1736

1737

1738

1739

1740

1741

1742

1743

1744

1745

1746

1747

1748

1749

1750

1751

1752

1753

1754

1755

1756

1757

1758

1759

1760

1761

1762

1763

1764

1765

1766

1767

1768

1769

1770

269

1,499

1,118

453

398

342

251

189

186

161

137

119

112

106

102

96

90

90

82

78

75

7

7

7

7

7

5

5

5

2,084

5,028

7,942

12,312

12,530

12,530

12,374

1771

1772

1773

1774

1775

1776

1777

1778

1779

1780

1781

1782

1783

1784

1785

1786

1787

1788

1789

1790

1791

1792

1793

1794

1795

1796

1797

1798

1799

1800

1801

1802

1803

1804

1805

1806

11,806

11,384

11,168

10,928

10,701

10,323

9,710

9,156

8,848

9,168

8,648

8,039

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

年

1807

1808

1809

1810

1811

1812

1813

1814

luoghi

di monte

7,946

7,946

7,946

7,946

7,946

7,946

7,946

7,946

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

e

d

你

/

j

我

/

n

H

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

4

3

4

5

1

1

1

6

9

9

8

8

1

/

j

我

n

H

_

A

_

0

0

4

6

0

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

7

S

e

p

e

米

乙

e

r

2

0

2

3

source Archivio di Stato di Roma: Luoghi di monte bb.10–25; 1141–1146; 1150–1158.

桌子 2 The Amount of Pontiªcal Public Debt during the Eighteenth

世纪

年

monti

1735

1736

1737

1738

S, Pietro I

S, Pietro II

S, Pietro III

S, Pietro IV

S, Pietro V

S, Pietro VI

S, Pietro VII

S, Pietro VIII

S, Pietro IX

Restaurato II

Restaurato III

S, 磷, Religioni

氮, Comunità

氮, A, Comunità

3,894,764

4,363,602

3,457,461

3,100,099

3,662,363

4,614,506

4,387,351

3,279,956

3,838,013

3,432,055

1,916,872

779,860

1,281,573

26,950

3,894,764

4,492,912

3,457,461

3,100,099

3,662,326

4,614,506

4,467,492

3,279,956

3,868,965

3,432,055

1,916,872

759,337

1,395,473

149,975

3,894,764

4,518,920

3,457,461

3,100,099

3,662,330

4,616,159

4,547,353

3,279,956

3,868,965

3,432,055

1,916,873

743,075

1,636,002

111,885

3,944,570

4,601,455

3,457,461

3,100,099

3,662,332

4,647,656

4,587,356

3,279,956

3,868,965

3,432,055

1,916,872

743,218

1,766,184