From Import Substitution to Integration into

Global Production Networks: The Case

of the Indian Automobile Industry

Prema-chandra Athukorala and C. Veeramani∗

This paper examines the growth trajectory and the current state of the Indian

automobile industry, paying attention to factors that underpinned its transition

from import substitution to integration into global production networks.

Market-conforming policies implemented by the government of India over the

过去的 2 几十年, which marked a clear departure from protectionist policies

in the past, have been instrumental in transforming the Indian automobile

industry in line with ongoing structural changes in the world automobile

行业. India has emerged as a significant producer of compact cars within

global automobile production networks. Compact cars exported from India have

become competitive in the international market because of the economies of

scale of producing for a large domestic market and product adaptation to suit

domestic market conditions. 有趣的是, there are no significant differences

in prices of compact cars sold in domestic and foreign markets. 这表明

that the hypothesis of “import protection as export promotion” does not hold

for Indian automobile exports.

关键词: automobile industry, foreign direct investment, global production

网络, 印度

JEL codes: F13, F14, L92, L98

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

我. 介绍

The global landscape of the automobile industry has been in a process

of notable transformation over the past 3 几十年. Until about the late 1980s,

automobile production remained heavily concentrated in the United States, 日本,

and Western Europe (known as the “triad”). While the leading automakers

headquartered in the triad had assembly plants in many developing countries,

most of these plants served domestic markets under heavy tariff protection. 自从

then the industry has become increasingly globalized, driven by a combination

∗Prema-chandra Athukorala (corresponding author): Professor of Economics, Australian National University. 电子邮件:

prema-chandra.athukorala@anu.edu.au; C. Veeramani: Associate Professor, Indira Gandhi Institute of Development

研究. 电子邮件: veeramani@igidr.ac.in. The authors would like to thank the managing editor and the journal

referees for helpful comments and suggestions. ADB recognizes “China” as the People’s Republic of China and

“Russia” as the Russian Federation. The usual ADB disclaimer applies.

Asian Development Review, 卷. 36, 不. 2, PP. 72–99

https://doi.org/10.1162/adev_a_00132

© 2019 Asian Development Bank and

Asian Development Bank Institute.

在知识共享下发布

归因 3.0 国际的 (抄送 3.0) 执照.

From Import Substitution to Integration into Global Production Networks 73

of technological advances in the industry, changes in global demand patterns,

and widespread trade and investment reforms in the developing world (夏皮罗

1994, Humphrey and Memedovic 2003, Klier and Rubenstein 2008, Bailey et al.

2010, Kierzkowski 2011, Amighini and Gorgoni 2014, Traub-Merz 2017).1 上

supply side, production standards have become increasingly universal, accompanied

by a palpable shift in production process from generic to modular technology.

最后, parts and components production has grown rapidly to cater to

multiple assemblers. 在需求方面, growth prospects for vehicle sales

are increasingly promising in emerging market economies, whereas the principal

automobile markets in the triad have been rapidly approaching a point of saturation

in recent years. These structural changes in the global automobile industry have

led automakers to set up new assembly bases in countries with large domestic

markets to serve regional markets. With this regional focus, carmakers tend to

consolidate their assembly facilities within a region and decide which models to

produce at which locations (国家), at what prices and quality standards, 并为

which markets (either regional or global). The process of trade and investment

liberalization across the world has facilitated this global spread, creating cost-

efficient plants aimed at global markets.

This massive transformation in the structure, 执行, and performance

of the world automobile industry has opened opportunities for countries in

the periphery to join the global automobile production network. 然而, 一个

important unresolved question is whether the government in these countries should

follow the conventional “carrot and stick” (活动家) approach to promote export

orientation of indigenous industries with significant domestic value added or a

“market-conforming” approach in which multinational enterprises (MNEs) 玩

the leading role in integrating domestic industry into global production networks

(GPN).

The purpose of this paper is to contribute to this policy debate by examining

the emergence of India as a significant production hub within global automobile

网络. The Indian automobile industry is an ideal case study of this subject given

the government’s long history of protecting domestic industry and the significant

structural changes following liberalization reforms that were initiated in the early

1990s and gathered momentum from about 2000. For over a half a century from

the late 1940s, the Indian automobile industry remained a canonical example of a

high-cost industry that evolved and survived under heavy trade protection. 然而,

过去 2 几十年, the industry has shown promising signs of gaining

significant capabilities and global competitiveness through integration into GPNs.

Most of the world’s leading automakers now have well-established production bases

in India. According to data reported by the International Organization of Motor

1在 2000, 74% of total world car production (in terms of number of cars) took place within the triad. 这

declined to 39% 经过 2017 (OICA 2017).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

74 Asian Development Review

Vehicle Manufacturers (OICA), India’s ranking among automobile producing

countries increased from 16th to 6th between 1999 和 2017, and its share in global

passenger car production (in terms of number of cars) increased from 1.3% 到 5%

(OICA 2017).

A study of the automobile industry is also relevant for the policy debate

in India given its contrasting growth experience compared to other major

manufacturing industries in the country. India’s economic growth has been primarily

driven by the service sector while manufacturing growth has been sluggish.

Manufacturing accounts for only about 17% of India’s gross domestic product

(GDP) compared to about 30% for the People’s Republic of China (PRC).

Engagement in GPNs has been the prime mover of manufacturing export expansion

in the PRC and other high-performing East Asian economies. 然而, 这

manufacturing sector in India remains generally cutoff from GPNs (Athukorala

2019, Joshi 2017, Krueger 2010). The automobile industry is an exception—over

the past 2 decades it has recorded impressive growth and export expansion through

global production sharing.

To preview the paper’s key findings, the analysis suggests that market-

conforming policies over the past 2 几十年, which marked a notable departure from

protectionist policies of the past, have played a key role in transforming the Indian

automobile industry. Learning and capacity development through foreign market

participation and entry of parts and components producers to set up production

bases in India has been the key factor behind the country’s emergence as a

production base within automobile GPNs. 有趣的是, there are no significant

differences between prices of cars sold in domestic and foreign markets. 这

suggests that the competitiveness of Indian cars sold in foreign markets is not

rooted in the prevailing tariffs on completely built-up units (CBUs) in India. 相当,

this competitiveness seems rooted in the economies of scale of producing for a

large domestic market and product adaptation to suit domestic market conditions

under a natural protection arising from the bulky nature of the product (unlike most

electronics and electrical products). An important question in the present context

of economic globalization, 所以, is whether trade protection has outlived its

purpose.

The rest of the paper is organized as follows. Sections II and III set the

background by providing a survey of the evolution of the Indian policy regime

relating to the automobile industry and by describing the entry of the main players

in the industry. Section IV examines the growth and composition of automobile

生产, with emphasis on the experience following the policy transition from

import substitution to global integration since the early 2000s. Section V analyzes

the extent of India’s engagement in automobile GPNs in terms of the MNEs’

involvement in domestic industry, export expansion, and international sourcing of

成分. Section VI provides a comparative perspective on automobile and

electronics industries with a view to highlighting the importance of differences in

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 75

the underlying policy regimes and product characteristics as possible explanations

for India’s contrasting performance in these industries. Section VII supplements

the analytical narrative in the previous sections with an econometric analysis of

the determinants of automobile exports from India using the gravity modeling

方法. The final section summarizes the main findings and policy implications.

二. Policy Context

The automobile industry has figured prominently in India’s industrialization

strategy since its independence in 1947 (Bhagwati and Desai 1970). The ensuing 6

decades can be divided into four subperiods in terms of the policy regime affecting

the automobile industry.

The period from late 1940s to mid-1970s was characterized by progressive

规定, 保护, and indigenization. 在 1948, automobiles and tractors were

included in the list of industries subject to “central regulation and control,” which

involved banning imports of CBUs and increasing tariffs on component imports

(Arthagnani 1967, 1424). 从 1953, only companies with plans to manufacture

components and CBUs were permitted to operate, and the existing assemblers

of imported completely knocked down (CKD) units were required to terminate

operations within 3 年. The Industrial Policy Resolution of 1956 permitted

private sector initiative and enterprise in the automobile industry subject

到

state control through industrial licensing. This was in sharp contrast to industry

policy in other capital-intensive industries (such as iron and steel, machinery, 和

electronics), of which the prime responsibilities for capability development rested

with state-owned enterprises (SOEs). Further regulations introduced in the first half

of the 1970s required all production expansion plans to have government approval

subject to local content requirements while capping foreign ownership of Indian

automobile companies at 40% (Kathuria 1987).

The period from the early 1980s to 1990 saw some easing of restrictions,

with emphasis on technological upgrading through foreign collaboration and a

relatively liberal import policy for capital goods and components (D’Costa 1995,

2009). The government loosened its tight grip on industrial licensing in favor of

increased competition and greater participation of foreign capital. Automakers were

permitted to adjust their product mix and produce a range of related products

instead of only one type of product as decreed by industrial licensing. 在 1982,

the Indian government for the first time became an investor in a car project when it

created Maruti Udyog Limited as a joint venture (80% government owned) 和

Suzuki Motors of Japan. Restrictions on capacity expansion of all automobile

assemblers were lifted. 然而, local content and technology transfer requirements

and reservation of the production of some automobile components for small and

medium-sized enterprises (中小企业) continued to remain in force.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

76 Asian Development Review

桌子 1. Tariff Rate on Automobile Imports in India (%)

Commercial

Vehicles

(HS 8702/04)

Cars and Utility Vehicles (HS 8703)

General Used Vehicles New CBU

CKD

Parts and

成分

(HS 8708)

150

65

50

50

40

40

40

35

1990

1992

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008–2011a

2011–2012

2012–2013

2013–2016a

53

60

50

50

40

40

40

35

35

30

25

20

15

12.5

10

10

10

10

10

QR

QR

QR

QR

QR

QR

QR

QR

105

105

105

105

100

100

100

100

100

100

125

QR

QR

QR

QR

QR

QR

QR

QR

60

60

60

60

60

60

60

60

60

60/75d

60/100d

35

30

25

20

15

12.5

10

10

10b/30c

10b/30c

10b/30c

40

65

n.a.

52

40

n.a.

40

38.5

35

30

25

30

15

12.5

12.5

10

8.57

10

10

CBU = completely built-up, CKD = completely knocked down, HS = Harmonized System, n.a. = not available.

QR = quantitative restrictions

Notes: Data for HS code 8708 are on a calendar-year basis. Other data are based on the Indian fiscal year: 1 April in

the reporting (给定) year to 31 March in the following year.

aNo change in tariffs during these subperiods.

bContains engine, gearbox, and transmission mechanism not in preassembled condition.

cContains engine, gearbox, or transmission mechanism in preassembled form.

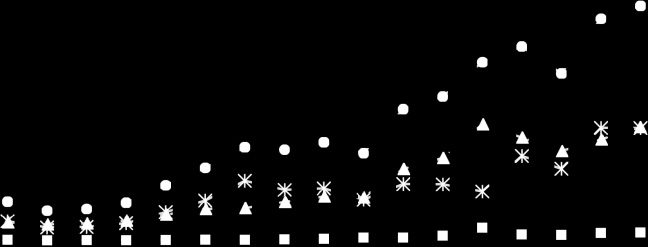

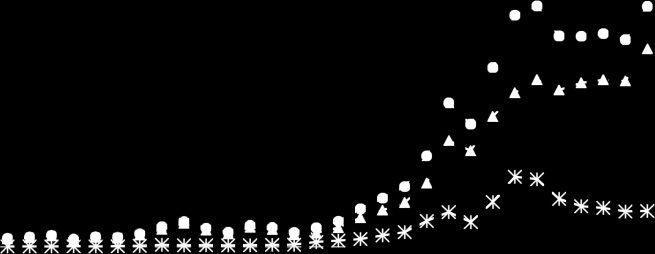

dFor vehicles valued above $40,000. 来源: Data for 1990,1992, and HS 8708 (all years) are from UNCTAD-TRAINS database (calendar-year based), and other data are from the Society of Indian Automobile Manufacturers (SIAM 2016). As part of the liberalization reforms initiated in 1991, several reforms were introduced incrementally. 第一的, licensing requirements were abolished for commercial vehicles and automobile component production in 1991 and for passenger vehicles in 1993. 第二, automatic approval for foreign holding of up to 51% of equity was announced in 1991 in several sectors including automobiles. 第三, importation of capital goods and automobile components were placed in 1997 under open general license. 第四, the import tariff rates for CKD units and parts and components were brought down from 65% 在 1992 到 35% during 2000–2001 (桌子 1). The liberalization reforms during the 1990s, 然而, were halfhearted. Import of cars and utility vehicles continued to remain under import licensing (quantitative restrictions) (桌子 1). An indigenization requirement was reintroduced in 1995 making it compulsory for all new joint ventures to indigenize ownership up to 70%–75% over a period of 5–7 years. Effective December 1997, l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 From Import Substitution to Integration into Global Production Networks 77 joint ventures involved in passenger vehicle production were required to sign a memorandum of understanding stipulating, 除其他事项外, to stop importing CKD or semi-knocked down kits for “mere assembly”, increase the share of domestically procured components to at least 50% of the components used within 3 years and 70% 之内 5 年, and balance export earnings with the value of imported components during the 3-year memorandum of understanding period (Pursell 2001). The early 2000s witnessed major policy initiatives aimed at integrating the Indian automobile industry into GPNs. 在 2001, as part of the membership commitments under the World Trade Organization, all quantitative import restrictions on used vehicles and CBUs were removed while tariffs were imposed (桌子 1), and the local content requirement for automobile production was abolished. Full foreign ownership was permitted for firms both in automobile and components production, enabling several MNEs to enter the industry by setting up wholly owned subsidiaries. Import tariffs on commercial vehicles, CKD, and components were progressively reduced, 从 35% during 2001–2002 to about 10% by the end of the decade. Since 2011–2012, CKD in preassembled form attracted a higher duty of 30% while those not in preassembled form attracted a lower tariff of 10%. Excise duties on cars were also progressively reduced from 40% during the 1990s to 32% 在 2002 和 25% 在 2004. The excise duty on smaller cars was reduced further to 17% 在 2006. During the period 2008–2017, excise duties for small cars varied in the range of 9%–13.5% and bigger cars in the range of 21%–28%. 三、. Entry of Main Players Table 2 summarizes information on the timing and mode of entry of MNEs in the Indian automobile industry. The wholly owned subsidiaries of General Motors and Ford Motor Company started the assembly of CKD trucks and cars in India in the late 1920s. Both companies left India in 1954 following the imposition of stringent import restrictions and local content requirements. During the first half of the 1940s, Hindustan Motors and Premier Automobiles set up production plants under license agreements with Morris Motors and Chrysler, 分别. Ashok Motors (later renamed Ashok-Leyland) started manufacturing Austin cars and Leyland commercial vehicles in 1948. Tata Engineering and Locomotive Company started manufacturing commercial vehicles in 1954 in collaboration with Daimler-Benz. Mahindra & Mahindra, another important player in the commercial vehicles segment, started production of jeeps in 1955. Bajaj Tempo began producing light commercial vehicles in 1958 under license from Vidal and Sohn Tempo-Werk of Germany (Arthagnani 1967). Until the mid-1980s, there were only two key firms in the passenger car segment (Hindustan Motors and Premier Automobiles), while all other firms l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 78 Asian Development Review Table 2. Profile of Main Players in the Indian Automobile Industry Company Mode of Entry Ford Motor Co. of Canada General Motors Hindustan Motors Premier Automobiles Ashok Motors/Ashok Leyland 100% subsidiary 100% subsidiary License agreement with Morris Motors License agreement with Chrysler License agreement with Austin Motor TELCO/Tata Motors Mahindra & Mahindra Bajaj Tempo/Force Motors Standard Motor Products Suzuki Mercedes-Benz PAL Peugeot Daewoo Motors Honda Siel Ford General Motors Hyundai Toyota Kirloskar Fiat Skoda (Volkswagen) Renault Nissan BMW Isuzu Motors Company and Leyland JV with Daimler-Benz License agreement with Willys Jeep License agreement with Vidal and Sohn Tempo-Werk of Germany License agreement with Standard-Triumph JV with Maruti JV with TELCO JV with Premier Automobiles JV with DCM JV with Shriram JV with Mahindra & Mahindra JV with Hindustan Motors 100% subsidiary JV with Kirloskar JV with Tata Motors 100% subsidiary JV with Mahindra 100% subsidiary 100% subsidiary 100% subsidiary JV = joint venture, TELCO = Tata Engineering and Locomotive Company. 笔记: Data are based on calendar years. 来源: Assembled from various internet sources. Year of Entry 1926, left in 1954 1928, left in 1954 1942 1944 1948 1954 1955 1958 1949, left in 2006 1983 1995 1995 1995 1995 1996 1996 1996 1997 1997 2001 2005 2005 2007 2012 manufactured commercial vehicles. The arrival in 1983 of Suzuki Motors as the Indian government’s joint venture partner in Maruti Udyog Limited (later renamed Maruti Suzuki) was an important landmark in the history of the Indian automobile industry (Hamaguchi 1985).2 当时, the government was concerned about its oil import bill, and Suzuki, a world leader specializing in small fuel-efficient cars, was an ideal joint venture partner (D’Costa 2004). Following the entry of Suzuki, other major Japanese automobile manufacturers (Toyota, Mitsubishi, Nissan, and Mazda) arrived, perceptibly changing the stature of the Indian automobile industry. included Mercedes-Benz with Tata Engineering and Locomotive Company (1994), General Motors with Hindustan Motors (1994), Peugeot with Pal Automotives (1994), established ventures 1990s other joint The the in 2As already noted, the government initially owned 80% of the joint venture’s equity, but this share was reduced over the years. Maruti Suzuki became fully foreign owned when the Indian government sold the remaining 18% of its shares in 2007. The company continued to remain the largest small and compact car producer in India. 在 2016, Maruti Suzuki accounted for 51% of the annual global vehicle production of Suzuki Motors Corporation (1.5 million out of 2.9 million units) (OICA 2017). l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 From Import Substitution to Integration into Global Production Networks 79 Daewoo with Toyota (1995), Honda Motors with Siel Ltd. (1995), Ford with Mahindra & Mahindra (1996), Fiat with Tata Motors (1997), and Toyota with Kirloskar Group (1997). Hyundai and Volvo entered the Indian market by setting up fully owned subsidiaries in 1996 和 1997, 分别. Following the abolition of ownership restrictions in 2000, the dominant mode of entry changed from license agreements and joint ventures to wholly owned subsidiaries. Hyundai was the first automobile MNE to establish a 100% subsidiary in the country. Volkswagen, Nissan, BMW, and Isuzu Motors followed suit. Companies that first entered as joint ventures, such as Honda, Ford, Fiat, and Renault severed links with their local partners and established 100% subsidiaries (Foy 2012). Following the entry of Japanese carmakers in the 1980s, several Tier 1 automobile parts suppliers (such as Denso, Aisin Seiki, and Toyota Boshoku) set up operations in India. 然而, operations of foreign-owned automobile parts producers faced constraints until early 2000s because of local content requirements for automobile assembly and the SME reservation policy. Following the removal of these restrictions in 2001, many more global automobile parts producers arrived (such as Robert Bosch, Delphi, Magna, Eaton, Visteon, and Hyundai Mobil). As we will discuss below, the Tier 1 automobile parts market play a pivotal role in the expansion of the Indian automobile industry as intermediaries between the local automobile parts makers and automobile producers. Automobile parts suppliers account for almost two-thirds of the value of the average car. 所以, the competitive advantage of a carmaker depends crucially on its ability to maintain a harmonious relationship with its parts suppliers (Klier and Rubenstein 2008, Dyer 2000). 实际上, Japanese carmakers consider a long-standing constructive relationship with their parts suppliers as “legitimate semi-insiders” a key factor of their success (Sako 2004). IV. Growth and Composition of Production Figure 1 shows the trends in passenger and commercial vehicle production during the period 1950–2017. Total production remained at fewer than 100,000 units until the mid-1980s. The production of passenger vehicles gradually increased during the second half of the 1980s, picked up pace during the 1990s, and then grew much faster since the early 2000s. Production of passenger vehicles crossed the 1 million mark in 2004 while that of commercial vehicles remained below 1 million throughout the ensuing years. The share of passenger vehicles in the total number of vehicles produced stood at 82% 在 2017, 从 56% 在 1985. Real gross output (value added) in the automobile industry, which includes final assembly, manufacture of bodies (coach work), and parts and components production, grew at an average annual rate of 18.5% during 2000–2015, compared to about 6% during the previous 2 几十年 (数字 2). l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 80 Asian Development Review Figure 1. Vehicle Production in India Source: Constructed using data from the Society of Indian Automobile Manufacturers (SIAM 2016). 数字 2. Real Output (value added) of the Automobile Industry l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 来源: Nominal value-added data are from the Annual Survey of Industries (ASI), Central Statistical Organization (公民社会组织); and nominal values are deflated using the gross domestic product deflator for transport equipment obtained from the National Accounts Statistics, 公民社会组织. During 1999–2016, compact cars accounted for over 80% of passenger vehicles, followed by midsize cars (engine size of 4,001 millimeters [毫米] 到 4,500 毫米) 和 18%, and large cars (engine size of over 4,500 毫米) accounting for the balance. Maruti Suzuki (with a market share of 51%) and Hyundai (27%) From Import Substitution to Integration into Global Production Networks 81 桌子 3. Passenger Car Production in India: Shares of Automakers (%) and Total Number of Vehicles Produced Compact (最多 4,000 毫米) Midsize (4,001–4,500 mm) 大的 (>4,500 mm) 2009 2014 2009 2014 Maruti Suzuki Hyundai Tata Motors Nissan Honda Volkswagen Ford Toyota Kirloskar General Motors Fiat Renault Mahindra & Mahindra BMW Hindustan Motors Mercedes-Benz Skoda Total Number 50.8 33.6 9.4 0.0 0.6 0.0 0.5 0.0 3.7 0.9 0.0 0.0 0.0 0.0 0.0 0.4 100 1,614,539 51.3 27.5 5.6 4.9 3.7 1.8 1.8 1.8 1.1 0.3 0.1 0.1 0.0 0.0 0.0 0.0 100 2,021,676 37.5 17.6 9.9 0.0 17.3 0.0 10.6 0.0 1.4 0.0 0.0 2.3 0.0 3.4 0.0 0.0 100 265,993 16.4 14.7 0.7 12.0 20.8 18.4 2.5 9.0 1.8 0.0 0.2 0.5 0.0 0.0 0.0 3.1 100 372,876 2009 0.0 0.8 0.0 0.0 18.3 0.6 0.0 18.8 9.5 21.6 0.0 0.0 5.3 0.0 6.5 18.5 100 52,088 mm = millimeters. Notes: Data are based on the Indian fiscal year: 1 April in the reporting (给定) year to 31 March in the following year. 来源: Compiled from the Society of Indian Automobile Manufacturers (SIAM 2016). dominate the compact car segment (桌子 3).3 相比之下, the market structure for midsize cars is less concentrated, with the following carmakers accounting for more or less similar market shares: Honda (21%), Volkswagen (18%), Maruti Suzuki (16%), Hyundai (15%), and Nissan (12%). In commercial vehicles, Tata Motors accounts for the largest share in light commercial vehicles (43%) and medium and heavy commercial vehicles (54%), with the next largest players being Mahindra & Mahindra (39.8%) and Ashok Leyland (29.2%), 分别. Notwithstanding the entry of foreign parts suppliers, domestic firms still account for the bulk (关于 80% during 1997–2017) of locally procured automobile parts and components.4 As expected, within the components industry, 最多 (if not all) firms with foreign partners are Tier 1 suppliers who work closely with automobile producers. Most of the fully Indian firms are operating at the Tier 3The term “compact cars” is used here to refer to cars with ignition engine capacity of less than 1,500 cubic centimeters (cc). In automobile production statistics, this category of cars is recorded under two subcategories: 袖珍的 <1,000cc (ignition engine capacity of less than 1,000cc) and compact >1,000cc (ignition engine capacity between 1,000cc and 1,500cc). 4Estimated using data from the Center for Monitoring the Indian Economic Prowess database. Foreign firms are defined as those with a foreign equity share of 25% 或者更多. l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 82 Asian Development Review 2 and Tier 3 级别 (Dash and Chanda 2017, Saripalle 2016). Undoubtedly, the domestic content requirements and SMEs reservation policy imposed during the import substitution era have played a role in the continued dominance of local firms in the automobile components segment. 然而, it is important to note that the “direct” output shares of Tier 1 firms (20%) grossly understate their role in globally integrating the Indian automobile industry. As already noted, these firms play a vital role in linking Tier 2 and Tier 3 suppliers with automakers. Some automobile MNEs have begun to use India as an export platform within their GPNs. 例如, Toyota Kirloskar Auto Parts, a joint venture between Toyota and a local manufacturer, is exporting gearboxes from India to assembly plants in various countries, including Argentina, 南非, and Thailand. Toyota Indonesia, which specializes in multipurpose vehicles, has integrated its production system with its operations in India, importing engine components from Indonesia and exporting gearboxes and automobile parts. Suzuki India has developed a two-way sourcing network encompassing its plants in India, 印度尼西亚, and the PRC. Hyundai has its largest overseas production base in India, with industrial clusters in Bengaluru, Chennai, 德里, and Mumbai. Hyundai Motors India is playing an important role in expanding the parent company’s presence in neighboring Southeast Asian countries. It exports a compact car designed in India (Santro) as semi-knocked down and CBUs to Pakistan, Bangladesh, Nepal, and Sri Lanka. 有趣的是, Santro was launched in the Republic of Korea under the name Visto, with body panels, 引擎, and transmission components entirely imported from India. This is the first-known case in the history of the Indian passenger car industry of reverse technology transfer: a car designed by an MNE in India subsequently becoming part of the parent company’s domestic production base (公园 2004). V. Export Performance India’s exports of CBUs increased from about $225 百万 2001 到 $8.8 十亿 2017, while exports of parts and accessories increased from $408 百万

到 $5.5 billion between these 2 年 (数字 3). The pattern is quite different on the import side with parts and accessories growing significantly faster than assembled vehicles during the same period (数字 4). 在 2017, the import value of assembled vehicles stood below $1 billion compared to about $5.4 billion of imports of parts and accessories. While assembled motor vehicles constitute the bulk of India’s automobile exports (parts and components plus final assembly, 这是 62% 在 2017), parts and accessories account for the lion’s share of total automobile imports (82% 在 2017). This pattern is consistent with the emergence of India as an assembly center of automobiles. l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 From Import Substitution to Integration into Global Production Networks 83 数字 3. Automobile Exports, 1988–2017 l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . 笔记: Data based on International Standard Industrial Classification (ISIC). ISIC codes are in parentheses. 来源: Constructed with United Nations Comtrade data accessed using the World Bank’s World Integrated Trade Solution. 数字 4. Automobile Imports, 1988–2017 / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 笔记: Data based on International Standard Industrial Classification (ISIC). ISIC codes are in parentheses. 来源: Constructed with United Nations Comtrade data accessed using the World Bank’s World Integrated Trade Solution. The export–output ratio (the share of exports in total domestic production) for passenger vehicles is significantly higher (in the range of 15% 到 20%) than for commercial vehicles (in the range of 8% 到 13%) (桌子 4). Within the passenger 84 Asian Development Review Table 4. Number of Vehicles Exported as a Share of the Number of Vehicles Produced (%) 2009 2010 2011 2012 2013 2014 2015 2016 2017 Passenger vehicles Passenger cars Utility vehicles Commercial vehicles 18.9 22.9 1.0 7.9 15.2 18.2 1.1 10.1 16.2 19.8 1.2 9.9 17.2 22.4 1.2 9.6 19.3 23.7 5.9 11.0 19.3 22.4 10.0 12.3 18.8 n.a. n.a. 13.1 20.0 n.a. n.a. 13.4 18.6 n.a. n.a. 10.8 n.a. = not available. Notes: Data are based on the Indian fiscal year: 1 April in the reporting (给定) year to 31 March in the following year. 来源: Compiled from the Society of Indian Automobile Manufacturers (SIAM 2016). vehicles segment, export orientation for passenger cars is significantly higher (in the range of 18%–24%) than for utility vehicles. Passenger vehicles dominate the composition of automobile exports. The share of passenger vehicles in total vehicle exports increased from 31% 在 1988 到 84.5% 在 2017. A striking feature of passenger vehicle exports is their heavy concentration in compact cars. Cars belonging to this size category accounted for over 80% of passenger vehicle exports from India, compared to a global average of a mere 15% during 2000–2015. In Thailand, the largest car exporter in the region, compact cars accounted for only 38% of total passenger vehicle exports during this period. 之间 2000 和 2015, India’s share in world exports of compact cars increased from 0.7% 到 5.6%, whereas India accounted for only about 1.4% of world passenger vehicle exports in 2015.5 Data on the geographic profile of compact car exports covering the top 25 destinations are given in Table 5. Markets in middle-income countries account for 45% of exports while high-income countries account for 37%. Among the middle-income group, the top individual country destinations include South Africa (16.4%), 阿尔及利亚 (7.6%), Eswatini (5.2%), 和墨西哥 (3.8%). Among high-income countries, the top destinations include the United Kingdom (英国) (10.3%), 西班牙 (4.5%), the United Arab Emirates (3.9%), 澳大利亚 (3.9%), 荷兰人 (3.6%), 意大利 (2.7%), 和德国 (2.1%). In contrast to popular perception, the markets for Indian cars are not restricted only to developing countries. The high concentration of exports in South Africa and the UK is underpinned by the investment of Indian automobile companies in these countries. 例如, Tata Motors acquired Jaguar Land Rover in the UK. Tata Motors and Mahindra & Mahindra have begun to penetrate markets in African countries from their bases in South Africa. Tata has invested over $700 million to set up

a production base in South Africa. Mahindra & Mahindra exports automobiles to

博茨瓦纳, Eswatini, 纳米比亚, 赞比亚, and Zimbabwe using South Africa as the

center of its operations in the region (Nyabiage 2013).

5Figures reported in this section, unless otherwise stated, are calculated from the United Nations Comtrade

数据库 (using export data at the 6-digit level of the Harmonized System).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 85

桌子 5. Top 25 Destinations for India’s Exports of Compact Cars, 2011–2014

国家

$ Million Number Share in Value (%) (A) High-income countries United Kingdom Spain United Arab Emirates Australia Netherlands Italy Germany Israel Saudi Arabia Chile Bahrain Ireland Total (乙) Middle-income countries South Africa Algeria Eswatini Mexico Indonesia Lebanon Colombia Libya Tokelau Angola Peru Turkey Panama Republic Total (C) Low-income countries 115.4 50.8 43.7 43.7 40.8 30.8 23.7 17.1 15.6 15.1 11.3 8.9 416.9 184.3 85.6 58 43.1 21.7 18.8 18.2 15.8 14.9 14.6 13 11.8 8.7 508.5 198 14,890 6,322 4,444 4,578 4,933 4,293 3,374 2,153 1,709 2,462 1,168 896 51,222 24,196 13,609 2,252 7,194 3,251 2,438 3,829 2,643 1,652 1,747 2,178 1,263 1,180 67,432 26,386 10.3 4.5 3.9 3.9 3.6 2.7 2.1 1.5 1.4 1.3 1 0.8 37.0 16.4 7.6 5.2 3.8 1.9 1.7 1.6 1.4 1.3 1.3 1.2 1.1 0.8 45.3 17.6 来源: Compiled from data provided by the Directorate General of Commercial Intelligence and Statistics, Ministry of Commerce, Government of India. Having shown that India has been successful in carving out a niche in compact cars in both high- and middle-income countries, a pertinent question is how do Indian compact cars compare with those of competitors in terms of price? To address this question, we compare India’s export unit values with those of the US for compact cars (桌子 6).6 The US is used here as the comparator country because of the availability of comparable data, and the comparison is appropriate given that India has a significant market presence in developed countries where it faces direct competition from carmakers in advanced countries, including the US. 6Unit values have well-known limitations as price proxies (particularly for manufactured goods), including spuriously capturing price changes associated with quality and brand changes as true price changes (Lipsey, Molineri, and Kravis 1991). Mindful of these limitations, we have used unit values here and in the next paragraph solely for making an overall comparison of price levels, rather than for analyzing intertemporal variations in prices. l 从http下载 : / / 直接的 . 米特 . / e d u a d e v / 文章 – p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 压力 . 来宾来访 0 9 九月 2 0 2 3 86 Asian Development Review Table 6. Unit Value of Compact Car Exports from India and the United States, 2003–2013 ($)

Compact <1,000cc Cars Compact >1,000cc Cars

年

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

印度

3,872

4,437

4,284

3,877

3,779

3,888

6,475

5,200

5,740

5,494

5,743

我们

4,697

4,946

5,390

5,500

5,580

5,952

6,324

7,454

7,402

7,873

7,986

印度

5,697

4,622

5,601

9,828

5,753

6,135

6,869

6,946

6,849

7,395

7,347

我们

8,776

8,618

9,100

13,012

15,061

15,274

15,326

15,164

15,318

15,763

15,232

cc = cubic centimeters, US = United States.

笔记: Data are based on the calendar year.

来源: Unit values for India are estimated using data (at the 8-digit level

of the Harmonized System) from the Directorate General of Commercial

Intelligence and Statistics, Ministry of Commerce, Government of India.

Unit values for the US for the same product description are obtained from

the US Census Bureau.

We find that Indian unit values are significantly lower than for the US. 因此, 价格

competitiveness seems to be an important factor behind India’s export success in

this segment of the global automobile market.

It is also pertinent to compare unit-value realization from domestic sales

with unit-value realization from exports. This comparison will help us understand

the importance of tariff protection as a determinant of India’s attractiveness as a

production base for automakers, 那是, whether tariff protection helps exporting

firms maintain international competitiveness by relying on excessive profits earned

domestically at tariff-ridden prices (Krugman 1984).

For this price comparison we computed the unit value of domestic sales

of two major automobile producers in India—Hyundai and Maruti Suzuki—and

export unit values of total compact car exports from India (桌子 7). To facilitate the

比较, it is important to note that Hyundai mostly exports cars in the compact

>1,000 cubic centimeters (cc) segment while Maruti Suzuki exports both types of

compact cars (那是, cars with ignition engine capacity of less than 1,000cc and

between 1,000cc and 1,500cc). It is evident that the export unit value of exports

is not significantly different from the domestic unit value for Hyundai, 和

domestic unit value for Maruti Suzuki is approximately the weighted averages of

export unit values for the two types of cars. Allowing for spikes, which possibly

reflect limitations of unit values as a proxy for price (脚注 7), 它出现

overall that domestic prices are approximately equal to export prices, implying that

tariff protection is virtually redundant as a determinant of India’s attractiveness as

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 87

桌子 7. Unit Value of Domestic Sales and Exports of Compact

Passenger Cars

Unit Value Realization

from Domestic Sales ($) Unit Value Realization from Export Sales ($)

Hyundai

Maruti

Suzuki

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

n.a.

n.a.

n.a.

n.a.

n.a.

7,089

7,102

7,079

6,779

6,796

7,676

6,434

7,505

4,910

5,348

5,540

5,424

6,367

5,271

6,414

6,612

6,671

6,922

6,188

6,081

6,095

Compact

Compact

<1,000cc Cars >1,000cc Cars

3,933

4,535

4,118

3,713

3,960

4,549

6,547

5,103

5,818

5,410

5,825

6,238

5,783

4,816

6,275

7,905

5,926

6,755

6,876

7,001

7,096

7,248

7,391

7,557

7,754

7,486

cc = cubic centimeters, n.a. = not available.

Notes: Data are based on the Indian fiscal year: 1 April in the reporting (给定)

year to 31 March in the following year.

来源: Unit values of domestic sales are computed using firm-level data

from the Center for Monitoring the Indian Economy database. Unit values of

exports are computed using export data (8-digit Indian Trade Classification) 从

the Directorate General of Commercial Intelligence and Statistics, Ministry of

Commerce, Government of India.

a production base of compact cars. Ex-showroom prices gathered from various

newspaper clippings also indicate a similar pattern. 例如, 平均数

ex-showroom price for Maruti Alto, the major brand exported in the compact car

segment, was about $5,710 在 2012. 相似地, the ex-showroom price for Hyundai, the most exported brand in the 1,000cc–1,500cc car segment, was about $7,320 在

2013. 总共, the cost competitiveness of Indian cars sold in foreign markets does

not seem to be rooted in tariff protection.

六、. Comparison with Electronics and Electrical Goods

Electronics and electrical goods account for the bulk of manufacturing

exports from the PRC and other East Asian economies, which have integrated

well into GPNs. The PRC has emerged as the global hub of electronics assembly

在世界上 (Athukorala 2014). 然而, these products account for only a tiny

share of India’s exports (Athukorala 2019). An important question in this context,

所以, is what are the specific conditions which have made it possible for India’s

automobile industry to successfully integrate into GPNs but not the electronics

行业? We argue that the divergent outcomes are related to both differences in

the policy regime and industry characteristics.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

88 Asian Development Review

Under planning for industrialization in India during the first 3 几十年

of independence, electronics and electrical machinery remained reserved for

the public sector and the private SME sector. Until

the late 1980s, foreign

collaboration was not permitted in these sectors other than in 100% export-oriented

ventures (Subramanian and Joseph 1988). 相比之下, government policy was more

accommodative of a private sector role and MNE participation in the automobile

行业, even during the heydays of import substitution (section II). This long

history of opening up for the private sector and allowing MNE participation

presumably set the stage for global integration of the automobile industry following

the liberalization of reforms initiated in the early 1990s and which gathered

momentum from about the start of the new millennium.

Turning to industry characteristics, both electronics and automobiles have

production processes conducive to global production sharing: 离散的 (separable)

stages of production with different scales, 技能, and technological needs and that

can be located in different sites. 然而, unlike electronics, automobiles are bulky

and have a low value-to-weight ratio and hence transport cost is a key determinant of

market price. There is also a need to design the product to suit the tastes and budget

of the consumer. 所以, there is a natural tendency for car assembly plants to

locate in countries with large domestic markets (Lall, Albaladejo, and Zhang 2004).

Once automakers choose to set up assembly plants in a given country, 部分

and component producers follow them because of two reasons. 第一的, 也许

更重要, most automobile parts are also bulky and characterized by low

value-to-weight ratios, which make it too costly to use air transport to ensure the

timely delivery required by the final assembler’s just-in-time production schedule.7

第二, there is an asymmetrical market power relationship between component

makers and automakers within the global automobile industry—products of many

automobile parts manufacturers are used in vehicles made by a handful of

carmakers. Electronics parts such as integrated circuits and semiconductors, 经过

对比, are used in many industries. 因此, there is an incentive for automobile

parts makers to set up factories next to the assemblers to secure their position in the

市场 (Klier and Rubenstein 2008, Dyer 2000).

Once a complete production base (involving both final assembly and

component assembly and/or production) is established in a given (大的) 国家,

exporting to third countries becomes a viable option for automakers. Scale

economies gained from domestic expansion makes exporting both parts and

components and assembled vehicles profitable as part of their global profit

maximization strategy. Adapting products to suit domestic demand conditions and

lower transportation costs compared to exporting from the home base also become

important drivers of exporting to regional markets from the new production base.

7相比之下, air shipping is the mode of transport for over two-thirds of electronics exports from Malaysia,

the Philippines, 新加坡, and Thailand to the US (Hummels 2009).

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 89

In electronics, the value-to-weight ratio of the final products and most

components is generally much higher than in the automobile industry. 所以,

the industry has the flexibility to locate various slices and/or tasks of the production

process in different sites based on relative cost advantages, provided the reduction

in production cost more than offsets the “service link” cost (Lall, Albaladejo,

and Zhang 2004; Jones and Kierzkowski 2004). The term service link refers to

arrangements for connecting and coordinating activities in each country with what

is done in other countries within the production network. Service link costs are

determined by the overall investment climate of a given country encompassing

foreign trade and investment regimes and the quality of trade-related infrastructure

and logistics. India’s average manufacturing wage is much lower than in the PRC

and other major East Asian countries (Athukorala 2019). As labor costs are rising

sharply in the PRC, India has an opportunity to make inroads into GPNs. 这

experience in the PRC clearly demonstrates that the availability of a large labor

pool is an advantage, particularly for final goods assembly within GPNs, 哪个

require production in factories that employ a large number of workers. 然而,

notwithstanding significant trade and investment policy reforms over the past 2

几十年, India has not been able to meet the service link standards required for

electronics to fit into GPNs.8

VII. Determinants of Exports: Gravity Model Analysis

在这个部分, we undertake an econometric analysis of the determinants of

automobile exports. The analysis uses the standard gravity modeling framework,

which has now become the workhorse for modeling bilateral trade flows (Head and

Mayer 2014). The export equation is estimated separately for compact <1,000cc

cars, which accounted for the largest share of total automobile exports during the

1990s, and compact >1,000cc cars, which started to gain a bigger share of the

export mix from the early 2000s.

A.

The Model

After augmenting the basic gravity model by adding several explanatory

变量, which have been found to improve its explanatory power in previous

学习 (Head and Mayer 2014, van Bergeijk and Brakman 2010), the empirical

model is specified as

EX Pjt = f (L(GDP) jt

, L(PRD) jt

, L(POP) jt

, L(MPC)它

DP2000, DH I jt, DU MI jt, DLMI jt, DF T Ait, DEU jt, DNAF T A jt,

DSACU jt, T RENDt, δt, ε jt )

, L(RER) jt

, L(TAR)它

,

8详情, see Athukorala (2019) and the studies cited therein.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

90 Asian Development Review

j is India’s trade partner, t is year, and L denotes the

where i stands for India,

natural logarithm. The notation δt represents partner fixed effects, which captures

time-invariant, partner-specific variables such as distance from India, 商业

语言, and a common border, and precludes the need to explicitly control for

这些因素. ε jt is a stochastic error term, assumed to have a normal distribution.

The variables are defined below, with the postulated signs of the coefficient for

explanatory variables given in parentheses.

EXP Bilateral exports, $ 百万. GDP Gross domestic product of trade partner, $ 百万 (+)

POP Midyear population (+)

PRD Automobile production (gross output), $ 百万 (+) RER Bilateral real exchange rate index (2010 = 100) (+) TAR Nominal applied import tariff rate (%) (− or +) MPC Import of vehicle parts and components, $ 百万 (+)

D2000 A dummy variable to capture policy shifts from 2000, 1 for the years

后 2000 和 0 否则 (+)

DHI A dummy variable that takes a value of 1 if a partner country belongs

to the group of high-income countries and 0 否则 (+)

DUMI A dummy variable that takes a value of 1 if a partner country belongs

to the group of upper-middle-income countries and 0 否则 (+)

DLMI A dummy variable that takes a value of 1 if a partner country belongs

to the group of lower-middle-income countries and 0 否则 (+)

DFTA A binary dummy that takes a value of 1 if both India and its trade

partner belong to the same free trade agreements (+)

DEU A binary dummy variable that takes a value of 1 if a partner country is

a member of the European Union or 0 否则 (+ or −)

DNAFTA A binary dummy variable that takes a value of 1 if a partner country is a

member of the North American Free Trade Agreement and 0 否则

(+ or −)

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 91

DSACU A binary dummy variable which takes a value of 1 if a partner country

is a member of the Southern African Customs Union or 0 否则 (+

or −)

TREND A linear time trend to capture secular changes in exports over time (+

or −)

Among the explanatory variables, GDP and POP of partner countries capture

external demand for Indian automobile exports, and PRD captures Indian supply

capability. Bilateral real exchange rate (RER), measured as the domestic currency

price of the trading partner’s currency adjusted for relative prices between the two

国家, is included to capture the relative profitability of exporting compared to

selling in the domestic market.

The variable TAR represents India’s nominal import tariff rate for CBU

imports. According to the Lerner symmetry theorem, import tariffs act as an export

tax by reducing the relative profitability of exporting compared to selling in the

domestic market (Lerner 1936). 然而, the theory of import protection as export

promotion postulates that producing for a protected domestic market helps achieve

scale economies that, 反过来, enhance export competitiveness (Krugman 1984).

所以, the sign of the regression coefficients can be positive or negative.

MPC is a proxy for the positive effect on export performance of procuring

parts and components within automobile GPNs. D2000 is included to capture the

impact of an acceleration of reforms in the early 2000s aimed at integrating the

Indian automobile industry into GPNs compared to the early years (首先 9) 的

改革 (see section II). DFTA represents the impact of tariff concessions offered

under various trade agreements, while DEU, DNAFTA, and DSACU aim to capture

the impact of major trade blocs in which India is not a member.9 The three income

group variables (DHI, DUMI, and DLMI) are specified based on the World Bank

country classification and using the low-income country group as the base dummy.

These three variables are included to test whether the stage of development of

destination countries has a distinctive effect on export demand in addition to their

GDP levels. 最后, TREND captures secular changes in exports over time.

As a robustness check, we estimate the above export equation by including

four time-invariant variables, which are commonly used in gravity models in place

of country-pair fixed effects (δ j). The variables are DST, the geographical distance

between New Delhi and capital city of partner countries; BDR, a common border

dummy (1 if India and the partner share a common land border and 0 否则);

CLK, a colonial economic link dummy (1 for India–UK bilateral exports and 0

9It is possible to include these variables along with partner fixed effects, as they are defined with respect to

the year and the partner. The time subscripts in these variables refer to the years during which the trade blocs have

been in operation.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

92 Asian Development Review

for other country); and CML, a common language dummy (1 if India and the

partner use a common business language and 0 否则). The expected sign of

the regression coefficient is negative for DST and is positive for the other three

变量.

乙.

Data and the Estimation Method

The dataset covers 196 trading partner countries during the period

1988–2015. Export data are from the United Nations Comtrade database. 数据

on value of output for motor vehicles are from the Annual Survey of Industry

conducted by the Central Statistical Office of India. Data on GDP, POP, 和

the variables used for computing RER (bilateral exchange rate and GDP deflator

for India and partner countries) are from the World Bank’s World Development

指标. Data on TAR and the information used for constructing DFTA, DEU,

DNFT, and DSACU are from the World Bank’s World Integrated Trade Solution

and Global Preferential Trade Agreement databases. Following recent trade flow

analyses using the gravity model, we use nominal US dollar values for EXP, GDP,

MPC to avoid estimation biases associated with deflating (Head and Mayer 2014).

Within the gravity modeling framework, TREND serves as a deflator of the nominal

US dollar series used.

The estimation method used is the Poisson pseudo maximum likelihood

(PPML) estimator

(Santos Silva and Tenreyro 2006, 2010). PPML is a

multiplicative estimator that has the advantage of retaining 0 export values. 它也是

yields consistent coefficient estimates in the presence of heteroscedasticity. 这

PPML requires that the dependent variable enters in level (nonlog) 形式, 但是

coefficient estimates of the independent variables, used in log form, can still be

interpreted as elasticities.

C.

结果

桌子 8 presents estimates of the export equation with country-pair fixed

effects. Alternative estimates with the standard time-invariant variable in place of

country-pair fixed effects are reported in the Appendix for comparison.

Looking first at the equation for compact <1,000cc cars, the coefficient of the trade partner’s GDP is statistically significant, with the coefficient indicating that a 1% increase in the partner country’s GDP on average is associated with an increase in India’s exports by 0.11%, other things being equal. The coefficient for population has the perverse (negative) sign and is significant only at the 10% level. Taken together, the results for GDP and POP seem to suggest that the stage of development as measured by per capita income, rather than the absolute market size measured by GDP or population, is more relevant for explaining changes in India’s l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a d e v / a r t i c e - p d l f / / / / / 3 6 2 7 2 1 6 4 4 2 1 8 a d e v _ a _ 0 0 1 3 2 p d . f b y g u e s t t o n 0 9 S e p e m b e r 2 0 2 3 From Import Substitution to Integration into Global Production Networks 93 Table 8. Determinants of India’s Bilateral Exports (EXP): Gravity Model Estimation Results Compact <1,000cc Cars Compact >1,000cc Cars

log GDP

log POP

log PRD

log RER

log TAR

log MPC

D2000

DHI

DUMI

DLMI

DFTA

DEU

DNFT

DSACU

TREND

Partner fixed effects

观察结果

R-squared

0.105***

(0.027)

−0.069*

(0.036)

0.934***

(0.235)

−0.042

(0.065)

−0.886***

(0.268)

0.396**

(0.227)

1.141***

(0.427)

1.234**

(0.625)

1.035***

(0.327)

1.309***

(0.428)

0.513

(0.397)

−1.376***

(0.291)

0.769

(1.237)

3.150***

(0.157)

−0.067

(0.042)

是的

4,393

0.776

−0.002

(0.033)

−0.011

(0.042)

−0.043

(0.289)

0.173***

(0.068)

0.108

(0.229)

1.417***

(0.327)

3.010***

(0.648)

0.418

(0.761)

0.589

(0.473)

0.200

(0.594)

0.969**

(0.484)

2.920***

(0.571)

3.057**

(1.277)

4.336***

(0.256)

−0.014

(0.048)

是的

4,411

0.775

cc = cubic centimeters.

Notes: Robust standard errors clustered by trading partner are in parentheses. ***, **,

和 * indicate statistical significance of the regression coefficients at 1%, 5%, 和 10%,

分别. See footnote 3 for the definition of the two types of compact cars.

来源: Authors’ estimates.

export patterns over time.10 This finding is also consistent with the coefficient

estimates of the three dummy variables classifying destination countries by income

团体 (DHI, DUMI, and DLMI with low-income countries as the base dummy).

The coefficients of these three variables, which are highly statistically significant,

show that the geographic profile of compact car exports has a bias toward high- 和

middle-income partner countries relative to low-income partners.

10Note that change in per capita GDP is equal to change in GDP minus change in POP.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

94 Asian Development Review

The coefficient of PRD is positive and highly significant, suggesting that a

1% increase in domestic production is associated with a 0.93% increase in exports.

The result for the import tariff variable (TAR) suggests that a 1% reduction in

India’s import tariff rate is associated with an 0.89% increase in exports. 相似地,

there is evidence that a 1% increase in imports of parts and components (MPC) 是

associated with a 0.4% increase in exports. According to the coefficient of D2000,

export earnings during the period after 2000 are on average 1.14% higher compared

to the previous years covered in the analysis. 全面的, the results for these four

variables confirm the importance of supply-side reforms in the emergence of India

as a dynamic player within global compact car markets.

有趣的是, the coefficient of RER is not statistically different from zero,

suggesting that relative profitability of exporting compared to selling domestically

is not a significant determinant of the export decisions of Indian automobile firms.

This is understandable because exporting decisions of firms operating within GPNs

depend on the parent firm’s locational decision at the global level, 而不是

on the relative profitability of selling in the domestic market of a given country.

As discussed, Indian subsidiaries of compact automobile producers (尤其,

Suzuki and Hyundai) have gained a competitive edge within the global automobile

网络.

Turning to the equation for compact >1,000cc cars, the coefficients of the

three main gravity variables—GDP, POP, and PRD—are not statistically different

from zero. The coefficient of TAR is also not statistically significant. 这些

results are understandable because India has emerged as an important player in

this segment only in recent years and production is still predominantly for the

middle-income domestic market. The results for MPC and D2000 are consistent

with those for compact cars. Providing easy access to intermediate inputs and

broadening of reforms to facilitate carmakers to integrate within global production

seem equally important for the export expansion of both types of compact cars.

Unlike in the case of compact <1,000cc cars, the bilateral real exchange

rate (RER) coefficient is statistically significant for compact >1,000cc cars and

has the expected sign. The coefficient suggests that a 1% depreciation of the RER

is associated with a 0.17% increase in exports. This somewhat intriguing contrast

presumably suggests some export spillover from predominantly domestic-oriented

production in response to changes in relative profitability of exporting compared to

selling in the domestic market. This finding is also consistent with a comparison

of results for DFTA between the two equations. The coefficient for this variable is

statistically significant with a positive sign only for compact >1,000cc cars. 这

highly significant and positive coefficient of DSACU in both equations is consistent

with our observation (section V) that India-based carmakers expand exports to

countries in the Southern African Customs Union using South Africa as the entry

观点.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

d

e

v

/

A

r

t

我

C

e

–

p

d

我

F

/

/

/

/

/

3

6

2

7

2

1

6

4

4

2

1

8

A

d

e

v

_

A

_

0

0

1

3

2

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

From Import Substitution to Integration into Global Production Networks 95

The inferences made so far in this section are generally consistent with

includes a time-invariant gravity

an estimation of the export equations that

variable instead of country-pair fixed effects (compare Table 8 with the Appendix).

然而, the overall fit of the two alternative export equations is much lower

(measured by R-squared) compared to their fixed effects counterparts. The upshot

is that export patterns are significantly influenced by unobservable destination

country-specific effects over and above the four observable time-invariant variables

we have included in the equations. This justifies our choice of the fixed effect

estimates as the preferred econometric evidence.

In alternative estimates, colonial dummy (CLK) is highly significant with

the expected positive sign in both equations. This result indicates the importance

of colonial links in explaining the growing importance of the UK as the largest

destination among developed countries for automobile exports from India (部分

V). 有趣的是, geographic distance (夏令时), which has been commonly found

as a key determinant of trade patterns in applications of the gravity model to

aggregate trade flows, is not a significant determinant of automobile exports from

印度. It could be that consideration of “natural” trade cost associated with distance

to market is overwhelmed by other specific considerations relating to MNE’s

production sharing within GPNs.

VIII. Concluding Remarks

From about the early 2000s, the Indian automobile industry has undergone

a remarkable transformation from domestic market-oriented production that

prevailed for over a half century to global integration. During the past 2 几十年,

most major automobile MNEs have set up wholly owned subsidiaries in India to

produce for the growing domestic market as well as to use India as a production

base for global markets of compact cars. Several global Tier 1 parts and component

suppliers have also established production facilities in India. 因此, 国家

has emerged as a major assembly center for compact cars. Our analysis shows that

Indian compact cars are highly price competitive in the international market.

Our analysis also suggests that simply granting trade protection in

the absence of enabling conditions for foreign technology transfer is not an

effective strategy to build a globally competitive automobile industry. 学习

and capacity development

through foreign market participation and entry of

parts and components producers to set up production bases has been the key

factor behind India’s emergence as a production base within automobile GPNs.

Market-conforming policies in the automobile sector over the past 2 几十年, 哪个

constituted a notable departure from the protectionist policies in the past, 有

played a key role in transforming the Indian automobile industry.

Both car manufacturing and component production in India are dominated

by foreign firms, with local firms mostly involved as suppliers of parts and

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t