Economic Integration and Business Cycle Synchronization in Asia

Economic Integration and Business Cycle Synchronization in Asia

Economic Integration and Business

Cycle Synchronization in Asia*

Chi Gong

Core Research Center of

Asia Center

房间 515, 建筑 220

Seoul National University

桑 56-1, Sillim-Dong,

Gwanak-Gu,

汉城 151-746, 韩国

gongchi81@snu.ac.kr

Soyoung Kim

经济系

Seoul National University

桑 56-1, Sillim-Dong,

Gwanak-Gu,

汉城 151-746, 韩国

soyoungkim@snu.ac.kr

抽象的

This paper examines the effects of internal (or regional) 与. exter-

纳尔 (inter-regional) integration and of trade vs. financial integration

on regional business cycle synchronization in Asia. 经验

results show the following: (1) similar and strong common exter-

nal linkages have significant positive effects on regional business

cycle synchronization; (2) after controlling for external linkages, 在-

ternal trade integration has a positive effect on regional business

cycle synchronization but internal financial integration has a nega-

tive effect; 和 (3) the measures of external linkages, 特别

the measure of external financial linkages, 更重要

than those of internal linkages in explaining regional business

cycle co-movements.

1. 介绍

After the 1997–98 Asian ªnancial crisis (亚足联), 内部-

tional linkages in both ªnance and trade have increased

rapidly in Asian countries. 在贸易方, reductions in

trade barriers and free trade agreements, 结合

the rise of production sharing networks in emerging Asian

国家, have deepened regional integration. 在 1990, 这

total exports and imports of ASEAN(西德:2)3 countries was

56 percent of their GDP (3.5 percent of world GDP). 这

value increased to 104 percent of their GDP (15.8 百分

* We thank Anwar Nasution, Bokyeong Park, Jiyoun An, Yukiko

Fukagawa, and seminar participants at Seoul National Univer-

sity Annual Conference of Western Economic Association,

A3 Conference on Monetary and Financial Cooperation in the

地区, and the Asian Economic Panel. Financial support from

the Institute for Research in Finance and Economics of the

Seoul National University is also gratefully acknowledged.

亚洲经济文件 12:1

© 2013 哥伦比亚大学和马萨诸塞州的地球研究所

技术研究院

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

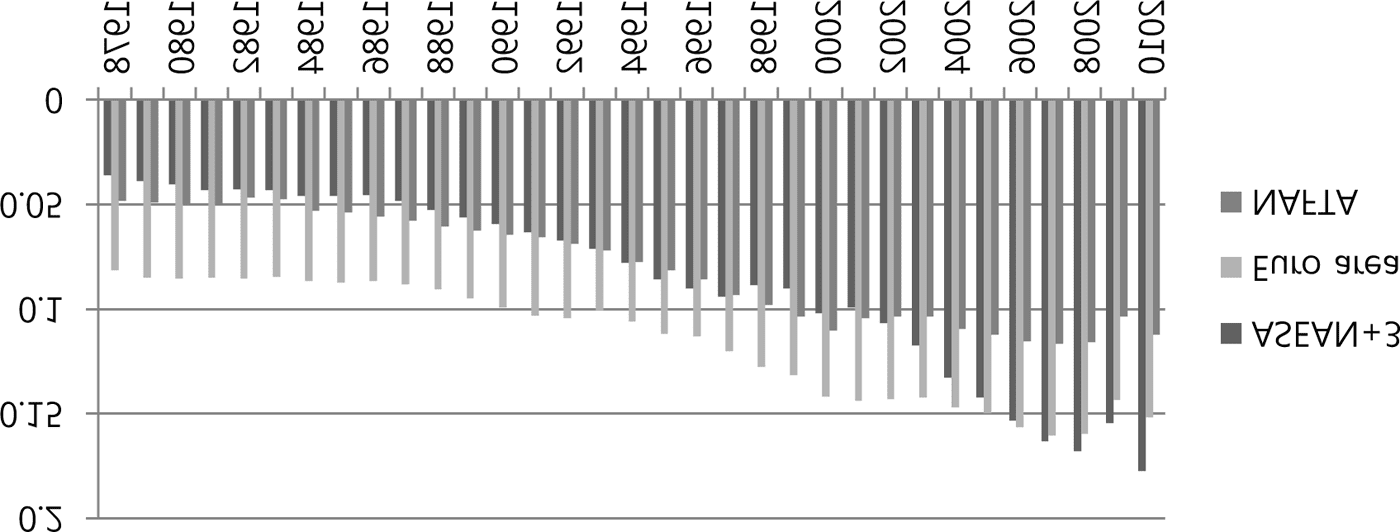

数字 1. Total trade of various regions (percent of world GDP)

来源: 世界银行, World Development Indicators & Global Development Finance.

笔记: 持续的 2000 美元$. of world GDP) 在 2010.1 数字 1 shows the total trade of ASEAN(西德:2)3 countries from 1987 到 2010 in comparison with that of countries in the North American Free Trade Agreement (NAFTA) and the Euro Area. Asia is currently a vital region for world trade, with the total trade of ASEAN(西德:2)3 becoming even larger than that of the Euro and NAFTA areas in recent years. On the ªnance side, capital account liberalization and various forms of regional ªnancial cooperation, such as the Chiang Mai Initiative Multilateralization (CMIM) and the Asian Bond Market Initiative (ABMI), have promoted the international inte- gration of Asian economies. 在 1990, the ratio of total assets and liabilities to GDP of ASEAN(西德:2)3 countries was 122.6 百分 (23.1 percent of world GDP). This value increased to 190.1 百分 (40.9 percent of world GDP) 在 2009. 在同一时期, the Euro and NAFTA areas recorded greater numbers at 347.05 百分 (74.73 percent of world GDP) 和 267.8 percent of their GDP (74.71 percent of world GDP), 分别. 尽管如此, the ªnancial globalization trend in Asian countries remains strong. Coinciding with the trends of rising trade and ªnancial integration has been an in- crease in business cycle co-movements across the Asian region. Past studies have documented the substantial changes in the business cycle co-movements of Asian countries after the AFC. 尤其, some studies (例如, Moneta and Ruffer 2009; 1 This paper considers nine economies in ASEAN(西德:2)3: 日本, 中国, 大韩民国, and the six economies (马来西亚, 菲律宾, 印度尼西亚, 泰国, 香港, and Singa- 毛孔) of ASEAN. 77 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / E D U A S E P A R T I C E – 压力 / 的f / / / / / 1 2 1 7 6 1 6 8 8 3 5 4 a s e p _ a _ 0 0 1 8 8 压力 . 来宾来访 0 9 九月 2 0 2 3 Economic Integration and Business Cycle Synchronization in Asia Imbs 2011; Kim and Lee 2012) found that business cycles of Asian countries have be- come more synchronized after the AFC and that these changes in business cycle properties are likely to be related to their economic integration process. The business cycle co-movements of Asian countries have various important impli- cations for the region. Some researchers and policymakers argue that the creation of an Asian monetary union or a common Asian currency unit is crucial for future de- velopment of the region.2 In this regard, business cycle synchronization or business cycle asymmetry of countries in the region is an important criterion to judge the costs and feasibility of Asian monetary integration.3 By investigating the effects of economic integration on regional business cycle co-movements, we may infer the possible effects of current trends of rapid economic integration on regional business cycle co-movements and the potential costs of Asian monetary integration. Even without explicit monetary integration of Asian countries, the magnitude of business cycle synchronization in the region has important implications for macro- economic policy coordination; 尤其, a high degree of business cycle synchro- nization within the region, common policy responses and/or policy cooperation within the region are needed to stabilize economic ºuctuations in the region. This paper investigates how economic integration affects the business cycle synchro- nization of Asian countries. 尤其, we distinguish two types of integration, 即, (1) trade integration vs. ªnancial integration, 和 (2) internal integration (regional integration or integration within Asia) 与. external integration (国际米兰- regional integration or integration of Asian countries with the rest of the world). This paper examines how different types of integration (trade vs. ªnancial and inter- nal vs. external) affect the regional business cycle synchronization of Asian countries. Distinguishing internal economic integration (within Asia) from external economic linkage (with the rest of the world) is important in explaining business cycle syn- chronization within Asia because both internal and external economic linkages can affect regional business cycle synchronization but in a different manner. The size of the effects of internal trade (or ªnancial) integration on regional business cycle may differ from the size of external trade (or ªnancial) linkages. 在这种情况下, the effects of internal and external integration should be estimated separately. 此外, 在- ternal and external integration may affect regional business cycle co-movement in opposite directions. 例如, a similar pattern of ªnancial linkages of Asian 2 例如, see Mundell (2003), Kuroda (2004), and Ogawa and Shimizu (2011). 3 Refer to Mundell (1961). 78 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / E D U A S E P A R T I C E – 压力 / 的f / / / / / 1 2 1 7 6 1 6 8 8 3 5 4 a s e p _ a _ 0 0 1 8 8 压力 . 来宾来访 0 9 九月 2 0 2 3 Economic Integration and Business Cycle Synchronization in Asia countries and the rest of the world may increase business cycle synchronization of Asian countries. A strong ªnancial integration among Asian countries, 然而, may decrease the business cycle synchronization of Asian countries. 此外, by separately estimating the effects, we can infer which one is more important in ex- plaining business cycle synchronization of Asian countries. 此外, the effects of recent regional integration efforts on business cycle synchronization can be better understood. 例如, we can clearly picture how trade integration within the region, such as free trade agreements (FTAs) among some ASEAN(西德:2)3 countries and Asian ªnancial cooperation such as CMIM and ABMI, has contributed to Asian business cycle synchronization. Based on our empirical results, we also draw some implications on these issues. To estimate the effects of internal and external integra- tion separately, we apply the method developed by Gong and Kim (2012). Although several studies have investigated the effects of economic integration on business cycle synchronization in Asia, these studies have not separated the effects of internal and external integration. Most studies (Rana 2007) concentrated on the effects of internal trade integration on regional business cycle synchronization. A few studies, such as those of Shin and Sohn (2006) and Imbs (2011), did examine the effects of both trade and ªnancial integration. These studies either concentrated only on internal integration or did not distinguish between internal vs. external integration, 然而. 纸的其余部分如下组织. 部分 2 shows the trends in internal vs. external integration and ªnancial vs. trade integration as well as the business cycle synchronization of Asian countries. 部分 3 explains the empirical methodol- 奥吉. 部分 4 discusses the empirical results. 部分 5 concludes with a summary of results. 2. Trends in economic integration and business cycle synchronization In this section, we brieºy examine trends in internal vs. external integration and trade vs. ªnancial integration, as well as in internal vs. external business cycle co- movements of Asian countries. 2.1 Economic integration Table 1 presents changes in the intra-regional and inter-regional trade relations of Asian countries between 1990 和 2009. The table shows that intra-regional trade among nine Asian economies (“ASEAN(西德:2)3”) increased steadily to 46.1 percent of to- tal trade in 2005 从 37.8 百分比在 1990. This value declined to 44.6 百分 (higher than the share of NAFTA economies but lower than the EU economies) 在 79 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / E D U A S E P A R T I C E – 压力 / 的f / / / / / 1 2 1 7 6 1 6 8 8 3 5 4 a s e p _ a _ 0 0 1 8 8 压力 . 来宾来访 0 9 九月 2 0 2 3 Economic Integration and Business Cycle Synchronization in Asia 2009, 然而, because of the global ªnancial crisis. If measured by percentage of GDP, intra-East Asian trade reached 25.6 百分比在 2005 和 21.7 百分比在 2009 从 11.1 百分比在 1990, higher than the EU economies and substantially higher than the NAFTA economies. The share of intra-regional trade is also substantial among 13 Asia-Paciªc economies (“ASEAN(西德:2)7”), peaking at 49.4 百分比在 2005 从 41.4 百分比在 1990, and declining only slightly to 49.2 百分比在 2009.4 As a percentage of GDP, intra-regional trade also increased through to 2005 but declined to 22.7 百分比在 2009. This increasing trend in intra-regional trade is observed not only in the entire Asian region, but also in individual Asian countries. 在 2009, the average of intra-regional trade between individual members of ASEAN(西德:2)3 and the whole ASEAN(西德:2)3 已经完了 60 percent of the GDP. This average is approximately 50 percent of GDP for ASEAN(西德:2)7 economies in 2009, reºecting a tight trade linkage among Asian countries. For external or inter-regional trade relations, the share of the G6 economies (G7 countries excluding Japan) in the trade of ASEAN(西德:2)3 has been declining but re- mained substantial at 21.0 百分比在 2009. The share of the G6 economies in the trade of ASEAN(西德:2)7 has also been declining, 到达 20.8 百分比在 2009. This does not necessarily imply that the trade linkages of Asian countries with G6 economies were weaker in the 2000s than in the 1990s, 然而. As a percentage of GDP, the trade of ASEAN(西德:2)3 with G6 was 10.5 百分比在 1990 and remained at 10.2 百分比在 2009. 相似地, the trade of ASEAN(西德:2)7 with G6 was 10.0 百分比在 1990 并重新- mained at 9.6 百分比在 2009. Considering the rapid economic growth of Asian countries, these numbers imply that the actual trade amount with G6 economies in- 有折痕的. As documented by previous studies (ADB 2007; Brooks and Hua 2008; 金, 李, 和公园 2011), a substantial part of intra-regional trade is driven by the trade of intermediate goods among Asian economies, with ªnal production destined for export outside the region. 在此背景下, intra-regional trade dynamics remain sensitive to changes in the external demand of industrialized economies or in the ex- ternal economic linkages with major industrial countries. 桌子 2 provides quantitative measures of ªnancial integration and cross-border holdings of portfolio assets and liabilities, including equity and long- and short- term debt securities. For ASEAN(西德:2)3, total portfolio assets increased from US$ 0.95 trillion in 1997 到US $ 4.86 trillion in 2010, whereas total portfolio liabilities increased from US$ 0.57 trillion in 1997 到US $ 3.07 trillion in 2010. 4 在本文中, 东盟(西德:2)7 includes the nine ASEAN(西德:2)3 经济体, 印度, 巴基斯坦, 新西兰, 和澳大利亚. 80 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / E D U A S E P A R T I C E – 压力 / 的f / / / / / 1 2 1 7 6 1 6 8 8 3 5 4 a s e p _ a _ 0 0 1 8 8 压力 . 来宾来访 0 9 九月 2 0 2 3 Economic Integration and Business Cycle Synchronization in Asia Table 1. Trade relations of selected economies in Asia A. As percent of Total Trade ASEAN(西德:2)3 东盟(西德:2)7 G6 1990 1995 2000 2005 2009 1990 1995 2000 2005 2009 1990 1995 2000 2005 2009 53 香港 56 中国 54 印度尼西亚 24 日本 35 韩国 54 马来西亚 38 菲律宾 44 新加坡 46 泰国 41 Australia India 18 新西兰 27 27 Pakistan ASEAN(西德:2)3 38 东盟(西德:2)7 37 55 54 50 34 41 54 44 51 47 45 23 31 30 45 44 56 48 51 34 40 54 45 50 46 45 22 30 23 44 43 64 40 58 40 45 55 55 52 50 49 26 31 24 46 45 67 35 57 43 44 57 58 52 49 55 27 34 25 45 44 56 58 58 29 38 59 41 49 49 47 21 48 30 42 41 57 57 55 39 45 58 47 55 50 52 25 54 32 49 48 59 50 57 38 43 58 47 54 50 50 24 53 27 48 47 67 44 65 44 49 59 57 58 55 56 29 55 27 50 49 70 40 66 48 49 64 61 58 55 62 30 58 29 50 49 27 25 24 44 39 28 39 30 30 34 35 32 36 36 36 24 27 26 38 32 28 36 27 25 29 34 28 33 31 31 23 29 22 37 30 26 32 25 26 28 30 29 30 30 30 17 28 16 28 22 24 22 20 19 23 25 26 27 24 24 14 26 14 22 17 17 19 17 16 19 19 21 22 21 21 乙. As percent of GDP ASEAN(西德:2)3 东盟(西德:2)7 G6 1990 1995 2000 2005 2009 1990 1995 2000 2005 2009 1990 1995 2000 2005 2009 Hong Kong China Indonesia Japan Korea Malaysia Philippines Singapore Thailand Australia India New Zealand Pakistan ASEAN(西德:2)3 东盟(西德:2)7 103 18 20 4 17 73 121 30 5 10 2 7 17 11 10 112 25 19 5 19 94 132 37 6 13 4 8 25 14 14 110 22 30 6 25 110 134 50 6 15 4 6 46 17 16 177 27 34 10 29 107 158 64 6 15 7 9 55 26 23 177 16 24 10 36 91 130 53 5 18 9 8 34 22 20 107 19 21 5 19 79 133 31 5 12 3 8 18 12 12 117 26 21 6 21 101 140 39 6 15 5 8 27 15 15 115 23 33 7 27 118 145 54 6 17 5 7 48 19 18 184 29 37 11 32 117 176 70 6 18 8 10 57 28 25 187 18 28 11 40 101 147 60 6 20 10 9 36 24 23 51 8 9 7 19 38 82 19 6 8 5 10 17 11 10 49 12 10 6 15 49 68 20 6 9 6 9 20 10 10 46 13 13 7 18 54 66 28 7 10 6 8 33 12 11 47 19 9 7 14 46 60 25 7 7 7 10 22 14 13 37 12 6 5 14 28 43 17 5 6 7 7 11 10 10 来源: Direction of Trade Statistics, 国际货币基金组织. 笔记: Total trade is the average of export and import. GDP uses the current price data. We can also observe a substantial increase in intra-regional portfolio investments. The total recorded level of cross-border portfolio asset and liability holdings among ASEAN(西德:2)3 economies was merely US$ 85.52 和US $ 44.98 十亿, 分别, 在 1997. These values increased to US$ 579.03 和US $ 541.75 十亿, 分别, 在 2010. The proportion of ASEAN(西德:2)3’s assets invested in ASEAN(西德:2)3 构成 9.0 percent of the total holdings of ASEAN(西德:2)3 在 1997, but decreased to 5.7 百分比在 2001, which could be partly attributed to the AFC; the value increased to 11.9 每- 分在 2010. 相比之下, the proportion of their assets invested in G6 declined from 62.0 百分比在 1997 到 46.6 百分比在 2010. For liabilities, we can see an even sharper increase in the proportion of intra-regional portfolio investments. 专业人士- portion of intra-regional portfolio investment in liabilities increased from 7.9 百分 81 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / 直接的 . 米特 . / E D U A S E P A R T I C E – 压力 / 的f / / / / / 1 2 1 7 6 1 6 8 8 3 5 4 a s e p _ a _ 0 0 1 8 8 压力 . 来宾来访 0 9 九月 2 0 2 3 Economic Integration and Business Cycle Synchronization in Asia Table 2. Total portfolio investment in Asia A. (US$ billion)

Year Economy

1997 中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

As percent

总计

东盟(西德:2)7

As percent

总计

2001 中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

As percent

总计

东盟(西德:2)7

As percent

总计

2010 中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

As percent

总计

东盟(西德:2)7

As percent

总计

Assets in

东盟(西德:2)3 东盟(西德:2)7 G6

Liabilities from

TOTAL ASEAN(西德:2)3 东盟(西德:2)7 G6

全部的

3.0

37.5

0.2

29.1

4.4

0.9

0.0

10.4

0.1

5.5

0.7

0.0

1.6

85.5

9.0%

93.3

9.4%

6.9

30.3

0.2

21.1

1.7

0.8

0.1

31.3

0.3

8.1

0.8

0.0

0.1

92.5

3.0

46.9

0.2

63.2

4.6

1.1

0.0

11.4

0.1

6.1

1.7

0.0

1.6

130.5

13.8%

139.9

14.1%

6.9

48.8

0.2

42.9

1.8

0.8

0.1

42.4

0.3

9.0

2.5

0.0

0.1

144.2

5.7%

8.9%

. . .

. . .

0.1

573.6

2.8

0.5

0.0

9.4

0.1

29.5

4.1

. . .

. . .

1.1

906.7

13.5

1.8

. . .

22.8

0.3

41.5

6.5

. . .

. . .

586.5

62.0% 100.0%

. . .

. . .

946.1

5.3

10.2

2.3

1.2

8.5

10.4

1.5

2.7

2.9

30.6

2.9

0.0

2.1

45.0

7.9%

620.0

994.1

62.4% 100.0% 11.2%

80.6

. . .

82.9

0.4

832.2

4.5

0.7

1.9

46.2

0.4

59.6

8.1

. . .

205.6

0.7

1,289.8

8.0

2.3

2.1

105.2

0.8

79.4

12.4

. . .

. . .

1,614.6

11.7

11.6

1.2

20.0

14.2

12.3

4.2

5.7

4.8

45.7

5.3

0.0

0.8

85.6

. . .

. . .

969.1

60.0% 100.0% 10.2%

5.3

11.1

2.4

5.7

8.7

10.5

1.6

2.9

2.9

31.6

3.4

0.0

2.1

51.2

9.0%

88.4

12.3%

11.7

13.9

1.2

25.3

14.6

12.4

4.2

6.5

4.8

47.3

6.2

0.0

0.8

94.5

11.3%

101.5

5.9%

155.7

9.1%

1,036.8

1,706.4

137.3

60.8% 100.0% 13.2%

148.8

14.3%

37.3

258.8

1.2

79.8

25.8

17.5

1.1

144.4

13.3

44.5

1.6

0.0

0.2

579.0

37.4

305.2

1.3

230.1

31.4

18.5

1.1

194.2

15.0

54.0

19.2

0.0

0.3

834.2

. . .

216.0

1.4

1,839.8

51.3

10.1

2.6

140.5

3.6

298.2

15.7

0.0

0.7

2,265.3

. . .

928.9

6.5

3,345.8

116.7

35.9

5.9

398.8

23.0

468.0

47.8

0.2

1.6

4,861.4

253.7

43.0

25.4

55.3

78.3

28.7

9.2

37.1

11.1

198.7

7.1

0.1

49.3

541.8

256.3

50.4

26.3

77.5

82.7

29.7

12.3

40.5

12.4

216.4

13.3

0.1

52.6

588.1

8.7

56.4

6.5

305.0

22.1

13.3

9.5

16.8

7.9

73.3

12.8

1.8

11.5

446.2

78.8%

545.7

76.1%

6.0

59.5

3.0

346.6

52.1

7.5

5.6

38.1

5.4

88.7

7.8

0.2

10.5

523.8

62.4%

631.1

60.5%

154.1

192.1

46.1

812.4

230.9

46.9

21.5

89.0

33.0

483.5

24.4

1.5

130.8

1,625.9

11.9%

17.2%

46.6% 100.0% 17.6%

19.2%

53.0%

625.4

11.6%

907.8

16.9%

2,579. 9

5,379.0

796.9

48.0% 100.0% 18.0%

870.4

19.7%

2,266.1

51.2%

14.8

74.1

9.8

365.0

32.7

25.1

11.7

21.5

11.5

116.3

17.7

1.9

14.8

566.2

100.0%

716.8

100.0%

20.3

96.7

5.6

542.3

76.8

22.6

12.8

50.7

12.0

170.0

18.3

0.5

15.4

839.6

100.0%

1,043.8

100.0%

498.2

320.8

101.9

1,348.2

407.8

105.8

46.5

172.2

68.8

931.5

44.7

4.6

376.5

3,070.1

100.0%

4,427.4

100.0%

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

来源: Coordinated Portfolio Investment Survey (CPIS), 国际货币基金组织.

China’s asset data are calculated by the counter data (the liabilities data) from IMF; Hong Kong’s 1997, India’s 1997 和 2001, 和

Pakistan’s 1997 和 2001 are also calculated by the counter data from IMF.

笔记: (. . .) (西德:3) no data available.

82

亚洲经济文件

Economic Integration and Business Cycle Synchronization in Asia

桌子 2. (持续)

乙. (As percent GDP)

Year Economy

Assets in

东盟(西德:2)3 东盟(西德:2)7 G6

Liabilities from

TOTAL ASEAN(西德:2)3 东盟(西德:2)7 G6

全部的

1997

2001

2010

中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

东盟(西德:2)7

中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

东盟(西德:2)7

中国

香港

印度尼西亚

日本

韩国

马来西亚

菲律宾

新加坡

泰国

澳大利亚

新西兰

巴基斯坦

印度

东盟(西德:2)3

东盟(西德:2)7

0.1

23.2

0.0

1.0

0.7

0.5

0.0

9.2

0.0

1.2

1.0

0.0

0.1

1.8

1.8

0.2

16.7

0.0

0.6

0.2

0.4

0.1

23.2

0.1

1.5

1.1

0.0

0.0

1.6

1.6

0.4

79.1

0.1

1.8

1.8

4.2

0.3

49.3

2.3

5.0

1.4

0.0

0.0

6.6

4.4

0.1

29.1

0.0

2.1

0.7

0.6

0.0

10.2

0.0

1.4

2.6

0.0

0.1

2.7

2.6

0.2

27.0

0.0

1.3

0.2

0.4

0.1

31.4

0.1

1.6

3.1

0.0

0.0

2.5

2.5

0.4

93.3

0.1

5.3

2.1

4.4

0.3

66.3

2.6

6.1

16.2

0.0

0.0

9.5

6.3

. . .

. . .

0.0

18.8

0.4

0.3

. . .

8.3

0.0

6.6

6.1

. . .

. . .

12.2

11.6

. . .

45.8

0.1

25.3

0.6

0.3

1.0

34.2

0.1

10.8

10.2

. . .

. . .

17.0

16.4

. . .

66.0

0.1

42.6

3.5

2.4

0.7

48.0

0.6

33.7

13.3

0.0

0.0

25.7

18.0

. . .

. . .

0.2

29.8

2.1

0.9

. . .

20.3

0.1

9.3

9.7

. . .

. . .

19.6

18.6

. . .

113.5

0.1

39.2

1.0

1.0

1.1

78.0

0.3

14.3

15.6

. . .

. . .

28.3

26.9

. . .

283.9

0.6

77.4

8.0

8.6

1.6

136.2

3.9

53.0

40.3

0.0

0.0

55.1

37.5

0.2

6.3

0.5

0.0

1.3

5.5

0.9

2.4

1.0

6.9

4.4

0.0

0.2

0.6

0.9

0.4

6.4

0.2

0.6

1.7

5.6

2.1

4.2

1.5

8.2

6.7

0.0

0.1

1.0

1.2

2.5

13.2

2.5

1.3

5.3

6.9

2.5

12.7

1.9

22.5

6.0

0.0

1.2

2.9

3.3

0.2

6.9

0.5

0.2

1.3

5.5

0.9

2.6

1.0

7.1

5.1

0.0

0.2

0.7

0.9

0.4

7.7

0.2

0.8

1.8

5.6

2.1

4.8

1.5

8.5

7.7

0.0

0.1

1.0

1.3

2.5

15.4

2.6

1.8

5.6

7.1

3.4

13.8

2.1

24.5

11.3

0.0

1.3

3.1

3.6

0.4

34.9

1.3

10.0

3.4

7.0

5.7

15.0

2.6

16.5

19.2

0.9

0.9

6.0

5.8

0.2

32.8

0.6

10.5

6.3

3.4

2.9

28.3

1.7

16.0

9.8

0.1

0.6

5.8

5.4

1.5

58.7

4.5

18.8

15.8

11.3

5.8

30.4

5.6

54.7

20.6

0.3

3.2

8.6

9.3

0.7

45.9

1.9

12.0

5.0

13.2

7.0

19.2

3.8

26.2

26.6

0.9

1.2

7.6

7.6

0.6

53.4

1.0

16.5

9.3

10.3

6.5

37.6

3.7

30.7

23.0

0.2

0.9

9.3

9.0

4.9

98.0

9.9

31.2

27.8

25.4

12.6

58.8

11.7

105.4

37.8

1.0

9.3

16.2

18.1

来源: Coordinated Portfolio Investment Survey (CPIS), 国际货币基金组织.

China’s asset data are calculated by the counter data (the liabilities data) from IMF; Hong Kong’s 1997, India’s 1997 和 2001, 和

Pakistan’s 1997 和 2001 are also calculated by the counter data from IMF.

笔记: (. . .) (西德:3) no data available.

在 1997 到 17.6 百分比在 2010. As in the case of trade relations, these results do

not imply that the ªnancial linkage with the G6 has decreased in recent years. 作为

如表所示 2, the actual size of cross-border assets between Asian countries and

the United States increased substantially, in line with ongoing ªnancial globalization

世界各地.

83

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

2.2 Business cycle co-movements

As in many previous studies, we use the contemporaneous bilateral correlation

coefªcient of (the log of) cyclical real GDP of two countries to describe their busi-

ness cycle co-movements. To obtain the trend of real GDP, an HP ªlter5 is applied.

To obtain the cyclical real GDP, the trend real GDP is subtracted from the real GDP.

Annual data are used for 1990–2009.6

桌子 3 presents the correlation coefªcients of cyclical real GDP for pairs of 13 亚洲-

Paciªc countries as well as the correlation coefªcients of cyclical real GDP for

13 Asia-Paciªc countries and G-6 countries. The business cycle co-movements of

Asian countries are higher in the 2000s than in the 1990s, and the bilateral correla-

tion among Asian countries increased in most cases. As depicted by the average

数字 (Avg.), business cycle co-movements increased in six out of nine countries

in ASEAN(西德:2)3 and in ten out of 13 countries in ASEAN(西德:2)7. 此外, 业务

cycle synchronization of Asian countries with the United States and G6 also in-

有折痕的. 平均而言, the correlation of ASEAN(西德:2)3 with the United States increased

from –0.03 to 0.50, and the correlation with G6 increased from –0.23 to 0.69. 更多的-

超过, the correlation of ASEAN(西德:2)7 with the United States increased from –0.02 to

0.49, and the correlation with G6 increased from –0.01 to 0.65.

The increase in the business cycle co-movements of Asian countries may be related

to a higher degree of trade and ªnancial integration within Asian economies as doc-

umented in the previous section. This increase may also be related to a higher busi-

ness cycle co-movement of Asian countries with advanced countries (桌子 3), 如何-

曾经. This phenomenon in turn could be related to more similar and stronger

economic linkages between Asian countries and advanced countries, possibly with

stronger shocks in advanced countries. In the next section, we formally examine the

effects of internal vs. external integration and trade vs. ªnancial integration on busi-

ness cycle co-movements of Asian countries.

3. Empirical method

3.1 Empirical model

Previous studies have used the following type of regression to analyze the effects of

trade and ªnancial integration on business cycle synchronization (IE。, Imbs 2004,

2006, 2011; Dées and Zorell 2011).

5 The Hodrick–Prescott (1980) ªlter is a mathematical tool used in macroeconomics, 尤其

in real business cycle theory to extract the cyclical component of a time series from the

原始数据.

6 Real GDP is measured in local units for all cases except for G6 aggregate, where real GDP in

purchasing power parity is used.

84

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

桌子 3. Correlation of output in Asia

A. 1990–1999

PAK INA US G6

HK CHN INO JPN KOR MAL PHI SIN THA AU NZ

(西德:6)1.00 (西德:6)0.27 (西德:6)0.92 (西德:6)0.67 (西德:6)0.72 (西德:6)0.87 (西德:6)0.08 (西德:6)0.71 (西德:6)0.91 (西德:6)0.61 (西德:6)0.20 (西德:6)0.14 (西德:6)0.60 (西德:6)0.70 (西德:6)0.73

香

CHN (西德:6)0.27 (西德:6)1.00 (西德:6)0.09 (西德:6)0.31 (西德:6)0.02 (西德:6)0.05 (西德:6)0.78 (西德:6)0.44 (西德:6)0.20 (西德:6)0.90 (西德:6)0.81 (西德:6)0.24 (西德:6)0.82 (西德:6)0.78 (西德:6)0.66

INO (西德:6)0.92 (西德:6)0.09 (西德:6)1.00 (西德:6)0.81 (西德:6)0.83 (西德:6)0.98 (西德:6)0.21 (西德:6)0.81 (西德:6)0.93 (西德:6)0.47 (西德:6)0.39 (西德:6)0.28 (西德:6)0.35 (西德:6)0.61 (西德:6)0.60

JPN (西德:6)0.67 (西德:6)0.31 (西德:6)0.81 (西德:6)1.00 (西德:6)0.67 (西德:6)0.78 (西德:6)0.25 (西德:6)0.47 (西德:6)0.63 (西德:6)0.52 (西德:6)0.04 (西德:6)0.46 (西德:6)0.30 (西德:6)0.59 (西德:6)0.44

KOR (西德:6)0.72 (西德:6)0.02 (西德:6)0.83 (西德:6)0.67 (西德:6)1.00 (西德:6)0.89 (西德:6)0.37 (西德:6)0.77 (西德:6)0.80 (西德:6)0.26 (西德:6)0.52 (西德:6)0.30 (西德:6)0.04 (西德:6)0.35 (西德:6)0.24

MAL (西德:6)0.87 (西德:6)0.05 (西德:6)0.98 (西德:6)0.78 (西德:6)0.89 (西德:6)1.00 (西德:6)0.36 (西德:6)0.87 (西德:6)0.89 (西德:6)0.32 (西德:6)0.52 (西德:6)0.27 (西德:6)0.18 (西德:6)0.46 (西德:6)0.44

PHI (西德:6)0.08 (西德:6)0.78 (西德:6)0.21 (西德:6)0.25 (西德:6)0.37 (西德:6)0.36 (西德:6)1.00 (西德:6)0.57 (西德:6)0.03 (西德:6)0.68 (西德:6)0.75 (西德:6)0.01 (西德:6)0.78 (西德:6)0.56 (西德:6)0.61

SIN (西德:6)0.71 (西德:6)0.44 (西德:6)0.81 (西德:6)0.47 (西德:6)0.77 (西德:6)0.87 (西德:6)0.57 (西德:6)1.00 (西德:6)0.70 (西德:6)0.08 (西德:6)0.80 (西德:6)0.10 (西德:6)0.08 (西德:6)0.10 (西德:6)0.15

THA (西德:6)0.91 (西德:6)0.20 (西德:6)0.93 (西德:6)0.63 (西德:6)0.80 (西德:6)0.89 (西德:6)0.03 (西德:6)0.70 (西德:6)1.00 (西德:6)0.57 (西德:6)0.35 (西德:6)0.30 (西德:6)0.45 (西德:6)0.71 (西德:6)0.71

Avg1 (西德:6)0.56 (西德:6)0.05 (西德:6)0.68 (西德:6)0.50 (西德:6)0.63 (西德:6)0.71 (西德:6)0.30 (西德:6)0.67 (西德:6)0.58 (西德:6)0.12 (西德:6)0.49 (西德:6)0.16 (西德:6)0.03 (西德:6)0.24 (西德:6)0.23

(西德:6)0.61 (西德:6)0.90 (西德:6)0.47 (西德:6)0.52 (西德:6)0.26 (西德:6)0.32 (西德:6)0.68 (西德:6)0.08 (西德:6)0.57 (西德:6)1.00 (西德:6)0.56 (西德:6)0.29 (西德:6)0.91 (西德:6)0.96 (西德:6)0.88

AU

(西德:6)0.20 (西德:6)0.81 (西德:6)0.39 (西德:6)0.04 (西德:6)0.52 (西德:6)0.52 (西德:6)0.75 (西德:6)0.80 (西德:6)0.35 (西德:6)0.56 (西德:6)1.00 (西德:6)0.13 (西德:6)0.59 (西德:6)0.36 (西德:6)0.29

NZ

PAK (西德:6)0.14 (西德:6)0.24 (西德:6)0.28 (西德:6)0.46 (西德:6)0.30 (西德:6)0.27 (西德:6)0.01 (西德:6)0.10 (西德:6)0.30 (西德:6)0.29 (西德:6)0.13 (西德:6)1.00 (西德:6)0.00 (西德:6)0.25 (西德:6)0.16

什么时候 (西德:6)0.60 (西德:6)0.82 (西德:6)0.35 (西德:6)0.30 (西德:6)0.04 (西德:6)0.18 (西德:6)0.78 (西德:6)0.08 (西德:6)0.45 (西德:6)0.91 (西德:6)0.59 (西德:6)0.00 (西德:6)1.00 (西德:6)0.86 (西德:6)0.88

Avg2 (西德:6)0.30 (西德:6)0.23 (西德:6)0.44 (西德:6)0.30 (西德:6)0.47 (西德:6)0.50 (西德:6)0.39 (西德:6)0.52 (西德:6)0.36 (西德:6)0.01 (西德:6)0.45 (西德:6)0.08 (西德:6)0.11 (西德:6)0.02 (西德:6)0.01

乙. 2000–2009

HK CHN INO JPN KOR MAL PHI

1.00 (西德:6)0.51 (西德:6)0.49 (西德:6)0.75 (西德:6)0.52

香

CHN 0.51 (西德:6)1.00 (西德:6)0.98 (西德:6)0.12 (西德:6)0.11

INO 0.49 (西德:6)0.98 (西德:6)1.00 (西德:6)0.15 (西德:6)0.14

JPN 0.75 (西德:6)0.12 (西德:6)0.15 (西德:6)1.00 (西德:6)0.79

KOR 0.52 (西德:6)0.11 (西德:6)0.14 (西德:6)0.79 (西德:6)1.00

MAL 0.91 (西德:6)0.47 (西德:6)0.47 (西德:6)0.73 (西德:6)0.56

0.93 (西德:6)0.70 (西德:6)0.69 (西德:6)0.57 (西德:6)0.37

PHI

SIN 0.97 (西德:6)0.61 (西德:6)0.57 (西德:6)0.66 (西德:6)0.50

THA 0.71 (西德:6)0.11 (西德:6)0.13 (西德:6)0.94 (西德:6)0.69

0.72 (西德:6)0.37 (西德:6)0.35 (西德:6)0.52 (西德:6)0.40

Avg1

0.65 (西德:6)0.22 (西德:6)0.23 (西德:6)0.71 (西德:6)0.71

AU

0.20 (西德:6)0.68 (西德:6)0.70 (西德:6)0.75 (西德:6)0.59

NZ

PAK 0.95 (西德:6)0.70 (西德:6)0.68 (西德:6)0.52 (西德:6)0.28

什么时候 0.64 (西德:6)0.98 (西德:6)0.96 (西德:6)0.01 (西德:6)0.04

0.69 (西德:6)0.35 (西德:6)0.33 (西德:6)0.51 (西德:6)0.39

Avg2

(西德:6)0.93 0.97

(西德:6)0.70 0.61

(西德:6)0.69 0.57

(西德:6)0.57 0.66

(西德:6)0.37 0.50

(西德:6)0.93 0.92

(西德:6)1.00 0.95

(西德:6)0.95 1.00

(西德:6)0.59 0.67

(西德:6)0.72 0.73

(西德:6)0.72 0.68

(西德:6)0.01 0.12

(西德:6)0.93 0.95

(西德:6)0.78 0.72

(西德:6)0.68 0.69

SIN THA AU NZ

(西德:6)0.71 0.65

(西德:6)0.11 0.22

(西德:6)0.13 0.23

(西德:6)0.94 0.71

(西德:6)0.69 0.71

(西德:6)0.80 0.81

(西德:6)0.59 0.72

(西德:6)0.67 0.68

(西德:6)1.00 0.74

(西德:6)0.52 0.61

(西德:6)0.74 1.00

(西德:6)0.77 0.45

(西德:6)0.51 0.53

(西德:6)0.02 0.27

(西德:6)0.52 0.56

G6

PAK INA US

(西德:6)0.20 (西德:6)0.95 (西德:6)0.64 (西德:6)0.68 0.91

(西德:6)0.68 (西德:6)0.70 (西德:6)0.98 (西德:6)0.24 0.18

(西德:6)0.70 (西德:6)0.68 (西德:6)0.96 (西德:6)0.28 0.14

(西德:6)0.75 (西德:6)0.52 (西德:6)0.01 (西德:6)0.98 0.94

(西德:6)0.59 (西德:6)0.28 (西德:6)0.04 (西德:6)0.74 0.74

(西德:6)0.27 (西德:6)0.84 (西德:6)0.57 (西德:6)0.66 0.83

(西德:6)0.01 (西德:6)0.93 (西德:6)0.78 (西德:6)0.46 0.75

(西德:6)0.12 (西德:6)0.95 (西德:6)0.72 (西德:6)0.59 0.83

(西德:6)0.77 (西德:6)0.51 (西德:6)0.02 (西德:6)0.94 0.85

(西德:6)0.15 (西德:6)0.71 (西德:6)0.52 (西德:6)0.50 0.69

(西德:6)0.45 (西德:6)0.53 (西德:6)0.27 (西德:6)0.61 0.69

(西德:6)1.00 (西德:6)0.04 (西德:6)0.58 (西德:6)0.83 0.50

(西德:6)0.04 (西德:6)1.00 (西德:6)0.81 (西德:6)0.45 0.74

(西德:6)0.58 (西德:6)0.81 (西德:6)1.00 (西德:6)0.10 0.32

(西德:6)0.10 (西德:6)0.64 (西德:6)0.43 (西德:6)0.49 0.65

0.91

0.47

0.47

0.73

0.56

1.00

0.93

0.92

0.80

0.72

0.81

0.27

0.84

0.57

0.69

来源: 彭博, 选择, 国际财务统计 (国际货币基金组织), and national sources.

笔记: The ªgures present the bilateral BCS as described in the paper. Average is the simple average of correlations among the nine East

亚洲经济体 (excluding own economy). 澳大利亚 (AU); 中华人民共和国 (CHN); 香港, 中国 (香); 印度 (什么时候);

印度尼西亚 (INO); 日本 (JPN); the Republic of Korea (KOR); 马来西亚 (MAL); 新西兰 (NZ); 巴基斯坦 (PAK); 菲律宾

(PHI); 新加坡 (SIN); 泰国 (THA).

(西德:4)

IJ

(西德:3) (西德:5)

0

(西德:2) (西德:5)

1Tij

(西德:2)

2Fij

(西德:2) e

IJ,

(1)

在哪里 (西德:4)

ij is the correlation between the cyclical components of real GDP of countries

i and j, Tij is the intensity of bilateral goods trade between countries i and j, and Fij is

the intensity of bilateral asset trade between countries i and j. (西德:5)

impacts of trade and ªnancial integration on business cycle synchronization.

2 show the

1 和 (西德:5)

In addition to economic integration among Asian countries, economic linkages be-

tween Asian countries and the rest of the world can contribute to business cycle co-

movements of Asian countries. 例如, structural shocks in the United States

can affect both Korea and Thailand in a similar manner, as Korea and Thailand have

similar and strong common economic linkages with the United States. To consider

85

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

such effects based on economic relations with countries outside the region, two vari-

ables are added to equation (1) 如下:

(西德:4)

IJ

(西德:3) (西德:5)

0

(西德:2) (西德:5)

1Tij

(西德:2)

(西德:2)

2Fij

3EXTij

(西德:2)

4EXFij

(西德:2) e

IJ,

(2)

where EXT and EXF are the variables that show the external trade and ªnancial

linkages, 分别, that generate business cycle synchronization between coun-

tries i and j. The measures show how strong and similar the external linkages of

countries i and j are to that of countries outside the region.

We also consider the following system of equations in which interactions among

various types of economic integration are allowed.

(西德:4)

IJ

(西德:3) (西德:5)

0

(西德:2) (西德:5)

1Tij

(西德:2)

(西德:2)

2Fij

3EXTij

(西德:2)

4EXFij

(西德:2) e

1 ,

IJ

(3)

Tij

(西德:3) (西德:7)

0

(西德:2)

1Fij

(西德:2) (西德:7)

2I T

IJ

(西德:2) (西德:7)

3EXTij

(西德:2) (西德:7)

4EXFij

(西德:2) e

2 ,

IJ

Fij

(西德:6) (西德:8)

0

(西德:2) (西德:8)

1Tij

(西德:2) (西德:8)

2I F

IJ

(西德:2) (西德:8)

3EXTij

(西德:2) (西德:8)

4EXFij

(西德:2) e

3 ,

IJ

ij and I F

ij are instruments that affect bilateral trade and ªnance intensities be-

where I T

tween country i and j, 分别. 在这个系统中, interactions among internal

ªnancial and trade integration are allowed. Internal trade integration can have both

direct ((西德:5)

2) effect by affecting internal ªnancial integration. Simi-

很大程度上, internal ªnancial integration can have both direct ((西德:5)

by affecting internal trade integration. 此外, two measures of external link-

ages are allowed to affect the measures of internal integration.

2) and indirect ((西德:7)

1) and indirect ((西德:8)

1) 影响

(西德:5)

(西德:5)

1

1

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

方程式 (1), (2), 和 (3) are estimated by ordinary least squares. Equation system

(4) (下一节) is estimated by three-stage least squares. More detailed explana-

tions on the empirical model are found in Gong and Kim (2012).

3.2 Measurement and data

To measure the degree of trade integration, the following measure of trade intensity

between countries i and j (Ti,j) is constructed.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Ti,j

(西德:3) 1

2时间

∑

(

X

我

,

t

+

)

瓦

M Y

J t

J t

t

我

,

,

,

*

Y Y

i t

,

J t

,

,

(4)

where Xi,j,t is the amount of country i’s export to country j at time t; 米,j,t is the

W is the world GDP at time t;

amount of country i’s import from country j at time t; 是

and Yi,t is country i’s GDP at time t. This measure is traces to Deardorff’s (1998) 这-

86

亚洲经济文件

Economic Integration and Business Cycle Synchronization in Asia

oretical work based on the gravity model, and has been used in several studies in-

cluding Imbs (2006). The measure depends on trade barriers and not on country

尺寸. This property is particularly useful in our case because Asian countries in our

sample are quite diversiªed in terms of their sizes but we would like to use the

measure that properly captures the extent of trade integration, independent of the

country size.7 Deardorff (1998) shows that the measure equals one if preferences are

homothetic and if trade barriers are nonexistent.

To properly capture the size of ªnancial integration, independent of the country

尺寸, a similar measure between countries i and j is constructed for ªnancial inte-

gration.8 The measure for ªnancial integration between countries i and j (fi,j) 是

给出的:

fi,j

(西德:3) 1

2时间

∑

(

我

我

,

t

+

我

J t

J t

我

,

,

,

*

Y Y

i t

,

J t

,

瓦

是

)

t

,

(5)

where Ii,j,t is the amount of portfolio investment from country i to country j at time t.

To measure the degree of ªnancial integration, past studies often used portfolio in-

vestment data. 在我们的情况下, we also used the bilateral portfolio investment data.9

The measure of external trade linkages that affects business cycle synchronization

between countries i and j (EXTij) is constructed as follows:

EXTij

(西德:9) S k = 1

6 wk{MAXT (西德:6) |Ti,k

(西德:6) Tj,k|}最小{Ti,k, Tj,k},

(6)

(西德:6) Tj,k|} 在方程式中 (6) shows the similarity in trade integration of countries i

where wk is the relative weight of G6 countries based on real GDP, and MAXT

is the largest value among Ti,j and Ti,k for all i, j, and k. The ªrst term {MAXT (西德:6)

|Ti,k

and k with that of countries j and k. |Ti,k

trade integration of countries i and k and that of j and k. By subtracting from the

largest possible value of T in the sample, the ªrst term {MAXT (西德:6) |Ti,k

shows the similarity. The second term (最小{Ti,k, Tj,k}) 在方程式中 (6) shows the com-

mon part of the trade integration of countries i and k and that of countries j and k.

The second term shows the strength of the common part of the trade integration of

countries i and k and that of countries j and k.

(西德:6) Tj,k| measures the difference between the

(西德:6) Tj,k|}

7 Other things being equal, a larger country is likely to trade more.

8 Previous studies suggested that the gravity model can also explain international transac-

tions in ªnancial assets (IE。, Portes and Rey 2001).

9 The asset data of China are calculated by the counter party’s (liability) data throughout the

sample period. The same method is used for the asset data of the following countries: 洪

孔 (1997), 印度 (1997, 2001, 2002, 2003), and Pakistan (1997, 2001).

87

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

The rationale behind this measure is that if two countries in a region (例如, Korea and

Thailand in Asia) have similar and strong common external trade integration with

countries outside the region (例如, G6), the business cycle co-movement between Ko-

rea and Thailand is likely to be high. The ªrst term naturally shows the similarity of

Korea and Thailand’s external trade linkages. The second term shows the strength

of the common external trade linkages of Korea and Thailand. Trade intensities of

Korea and Thailand with the G6 (Tik and Tjk) show the strength of the external trade

linkages of Korea and Thailand. The business cycle correlation of Korea and Thai-

land is likely to be generated only to the extent that they have the common part,

然而. 所以, the minimum of external trade intensities of two countries

使用.

The measure of external ªnancial linkages that affects business cycle synchroniza-

tion between countries i and j (EXTij) is constructed in a similar manner.

EXFij

(西德:9) S k = 1

6 wk{MAXF (西德:6) |fi,k

(西德:6) Fj,k|}最小{fi,k, Fj,k},

(7)

(西德:6) Fj,k|} shows the difference between the ªnancial integration of

where MAXF is the largest value between Fi,j and Fi,k for all i, j, and k. The ªrst term

{MAXF (西德:6) |fi,k

countries i and k and that of j and k. The second term (最小{fi,k, Fj,k}) shows the

strength of the common part of the ªnancial integration of countries i and k and that

of j and k.

Note that these measures for external linkages are different by nature from the mea-

sures for internal integration. The measures for internal integration simply show

how intensive trade and ªnancial integration are between countries i and j, 然而

the measures for external linkages show how strong and similar the external inte-

gration of country i and countries outside the region is to that of country j and coun-

tries outside the region (see Gong and Kim 2012 欲了解详情).

Following previous empirical studies, we include the geographic distance of the

capital cities of two countries, whether a border exists between two countries, 和

whether a common ofªcial language is used in both countries as instruments for the

trade equation. These three instruments are usually argued as clearly exogenous

with high predictive power when analyzing the determinants of bilateral trade. 为了

the ªnance equation, two instruments are used: the sum of two countries’ per capita

real GDP and the difference between the per capita real GDP of the two countries.

The combined income level may affect the degree of ªnancial integration because

ªnancial markets and technologies are better developed in high-income countries,

and ªnancial integration between high-income countries may be easier. On the con-

88

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

特里, a large difference in the level of income may make ªnancial integration

more difªcult.

We consider the following group of countries. 第一的, we consider nine countries in

东盟(西德:2)3, as policy cooperation such as CMIM and ABMI has been discussed

among this group of countries. 第二, we consider “ASEAN(西德:2)7” by adding four

国家 (印度, 巴基斯坦, 新西兰, 和澳大利亚) to ASEAN(西德:2)3 because pol-

icy debates often include these four countries as potential candidates for extended

policy cooperation in the Asia-Paciªc area.

For the measure of business cycle correlation, we calculate the correlation of cyclical

real GDP from 2001 到 2009 (annual data) as reported in Table 3. For all other mea-

确定, the annual average values from 2001 到 2009 被使用. Correlations among

various measures are reported in Table 4.10 The table shows that the business cycle

synchronization measure ((西德:4)) is more correlated with external linkage measures than

with internal integration measures. This correlation may imply that external link-

ages are more important in explaining the business cycle synchronization of Asian

countries compared with internal integration. A formal analysis of this possibility is

performed in the next section.

4. 结果

4.1 Basic results

桌子 5 shows the estimation results based on the single equation method. 什么时候

only the measure for internal trade integration (and a constant term) is included as

the regressor, the coefªcient is positive for the ASEAN(西德:2)3 和东盟(西德:2)7 样品,

although it is signiªcant at only the 10 percent level for ASEAN(西德:2)7. 相似地, 什么时候

only the measure for internal ªnancial integration is included as the regressor, 这

coefªcient is positive and signiªcant at the 5 百分比和 10 percent level for

东盟(西德:2)7 和东盟(西德:2)3, 分别. When both internal trade and ªnancial in-

tegration measures are included, 然而, no coefªcients are signiªcantly esti-

交配, probably because of the high correlation between two measures as reported

表中 4.

When the measures for external ªnancial and trade linkages (EXF and EXT) 是

额外, the coefªcients on the measures for internal trade integration and two exter-

nal linkages are positively estimated, whereas the coefªcient on the measure for

10 (西德:4)

1, EXT1, and EXF1 are alternative measures to check the robustness of the results. 部分 4

explains those measures.

89

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

桌子 4. Correlation among various measures

A. 东盟(西德:2)3

(西德:4)

(西德:4)

1

时间

F

EXT

EXT1

EXF

EXF1

(西德:2)

1

0.948

0.261

0.297

0.382

0.382

0.439

0.444

乙. 东盟(西德:2)7

(西德:4)

(西德:4)

1

时间

F

EXT

EXT1

EXF

EXF1

(西德:2)

1

0.903

0.208

0.232

0.281

0.282

0.333

0.334

(西德:2)1

1

0.231

0.276

0.374

0.374

0.424

0.430

(西德:2)1

1

0.164

0.202

0.243

0.244

0.279

0.281

时间

F

EXT

EXT1

EXF

EXF1

1

0.904

0.675

0.676

0.284

0.290

1

0.811

0.812

0.600

0.605

1

1.000

0.591

0.594

1

0.590

0.594

1

1.000

1

时间

F

EXT

EXT1

EXF

EXF1

1

0.864

0.712

0.712

0.249

0.253

1

0.757

0.758

0.606

0.612

1

1.000

0.437

0.439

1

0.437

0.439

1

1.000

1

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

桌子 5. Single equation estimation

A. 东盟(西德:2)3

(西德:2)

时间

F

EXT

EXF

R2

乙. 东盟(西德:2)7

磷

时间

F

EXT

EXF

R2

OLS

(0.005

(1.58)

OLS

(0.019

(1.82)*

OLS

((西德:6)0.001

((西德:6)0.11)

((西德:6)0.021

(西德:6)(0.87)

(0.041

(0.062

((西德:6)0.034

OLS

(0.006

(1.86)*

OLS

(0.020

(2.08)**

OLS

(0.001

(0.14)

(0.0177

(0.92)

(0.031

(0.041

(0.029

OLS

((西德:6)0.027

(西德:6)(2.56)**

(西德:6)0.109

((西德:6)2.61)**

((西德:6)0.015

(西德:6)(1.45)

((西德:6)0.090

(西德:6)(3.20)***

((西德:6)0.277

OLS

( 0.018

(西德:6)(2.09)**

((西德:6)0.069

((西德:6)2.24)**

((西德:6)0.011

(西德:6)(1.18)

((西德:6)0.067

(西德:6)(3.16)***

((西德:6)0.146

笔记: *Statistically signiªcant at the 10 百分比. **Statistically signiªcant at the 5 百分比. ***Statistically signiªcant at the

1 百分比.

90

亚洲经济文件

Economic Integration and Business Cycle Synchronization in Asia

internal ªnancial integration is negatively estimated. The estimated coefªcients on

the measures for internal trade and ªnancial integration are signiªcant at the 5 每-

cent level, whereas the estimated coefªcients on the measure for external ªnancial

integration are signiªcant at the 1 百分比. 桌子 5 shows the substantial in-

crease in the adjusted R2 when both measures of external linkages are added to

the regression.

桌子 6 reports the estimation results for the equation system (3). The estimation re-

sults for the main equation (the ªrst equation of equation [3]) are similar to those of

the single equation estimation. The sign of the effects of each variable in the GDP

correlation equation is the same; the internal trade integration and external trade

and ªnancial integration have positive effects on business cycle co-movements, 但

internal ªnancial integration has a negative effect. The estimated coefªcients are

signiªcant in most cases.

The results show that the measures of external trade and ªnancial linkages posi-

tively affect regional business cycle co-movements. This ªnding implies that similar

and strong common external linkages of two countries increase the business cycle

co-movements between them. This is not surprising. 例如, suppose the trade

linkages between Korea and the United States and that between Thailand and the

United States are strong and similar. Suppose further that the U.S. economy is hit by

recession. 然后, both Korea and Thailand will have difªculties exporting to the

美国. 因此, both countries are likely to experience a fall in income and a

worsening trade balance against the United States, which leads to business cycle

synchronization of the two countries. 相似地, suppose the ªnancial linkage be-

tween Korea and the United States and that between Thailand and the United States

are strong and similar. Suppose further that the U.S. economy goes into recession,

which decreases the price of U.S. ªnancial assets. 然后, the net investment income

and capital gain on ªnancial assets in the United States owned by Korea and Thai-

land are likely to fall. Such a case may lead to a fall in income of the latter two coun-

tries and therefore have a positive effect on the business cycle co-movement of

the two.

The results also indicate that internal trade integration has a positive effect on

business cycle co-movements. Many studies,11 following Frankel and Rose (1998),

likewise observed the positive effect of trade integration on business cycle

co-movements. 弗兰克和罗斯 (1998) interpreted that a possible negative effect

of trade-induced specialization can be weaker than the direct positive effect of trade

11 例如, Canova and Dellas (1993) found that productivity shocks in the production of

traded intermediate goods generate positive output co-movement across countries.

91

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

桌子 6. Equation system estimation

GDP correlations ((西德:2)) 方程

东盟(西德:2)3

东盟(西德:2)7

时间

F

EXT

EXF

R2

贸易 (时间) 方程

F

EXT

EXF

R2

Finance (F) 方程

时间

EXT

EXF

R2

((西德:6)0.070

(西德:6)(2.84)***

((西德:6)0.303

((西德:6)2.82)***

((西德:6)0.038

(西德:6)(2.20)**

((西德:6)0.186

(西德:6)(3.28)***

((西德:6)0.202

(西德:6)(3.941

(西德:6)(7.02)***

((西德:6)0.285

((西德:6)1.16)

((西德:6)1.950

((西德:6)5.32)***

(西德:6)(0.915

(西德:6)(0.217

(西德:6)(7.18)***

(西德:6)(0.122

(西德:6)(2.09)**

(西德:6)(0.473

(西德:6)(4.34)***

(西德:6)(0.948

0.033

(1.60)

(西德:6)0.155

((西德:6)2.07)**

0.023

(1.71)*

0.112

(2.63)***

0.045

((西德:6)3.794

(西德:6)(5.47)***

((西德:6)0.059

((西德:6)0.22)

((西德:6)2.026

((西德:6)5.42)***

((西德:6)0.848

(西德:6)(0.243

(西德:6)(5.95)***

(西德:6)(0.044

(西德:6)(0.49)

(西德:6)(0.517

(西德:6)(6.24)***

(西德:6)(0.908

笔记: *Statistically signiªcant at the 10 百分比. **Statistically signiªcant at the 5 百分比. ***Statistically signiªcant at the

1 百分比.

integration on business cycle co-movements; Imbs (2004) conªrmed such a conjec-

真实. We may attach a similar interpretation to our empirical results.

有趣的是, internal ªnancial integration is found to have a negative effect on the

regional business cycle correlation. Past empirical studies (例如, Imbs [2004, 2006]

and Kose, Prasad, and Terrones [2003] for the countries around the world; Shin and

索恩 [2006] for Asian countries) mostly found that the effect is either positive or

insigniªcant. The result of the current study is particularly interesting because the

effect is positive when the measures for external linkages are not included in the es-

timation as in the past studies. External linkages are found to have a signiªcant ef-

fect on internal business cycle synchronization. By omitting the measures for exter-

nal linkages, the effect of internal integration on internal business cycle

synchronization can be improperly estimated.12

12 Gong and Kim (2012) applied a similar method to various regions of developing countries

and found that the effect is negative after controlling external linkages. 另一方面

92

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

理论上, the effects of ªnancial integration on business cycle correlation are

模糊的. 一方面, some theories imply a negative effect. As suggested

by Backus, Kehoe, and Kydland (1992) and Baxter and Crucini (1995), a country-

speciªc positive productivity shock in the home country induces capital ºows from

the foreign country in a two-country model, by increasing the marginal productivity

of capital gap between the home and the foreign countries, thereby generating a

negative correlation between the two countries’ outputs. Obstfeld (1994) suggested

that ªnancial integration can promote investments on risky projects, leading coun-

tries to specialize based on comparative advantages. This effect may lead to a nega-

tive output correlation. 另一方面, other theories, such as that by Calvo and

Mendoza (2000) suggest a positive effect: Financial globalization may promote

contagion and increase business cycle co-movement by weakening incentives for

gathering costly information in the presence of short-selling constraints and by

strengthening incentives for imitating arbitrary market portfolio if below-market

performance is costly for portfolio managers. The former theory, which suggests a

negative effect, is consistent with our results.

Our results also show that internal trade and ªnancial integration affect each other

positively; the estimated coefªcients on the measure of internal trade integration in

the ªnance equation and the measure of internal ªnancial integration in the trade

equation are both positive and signiªcant. This result may imply that policy efforts

to promote regional trade (or ªnancial) integration lead not only to regional trade

(or ªnancial) integration but also to regional ªnancial (or trade) 一体化. This re-

sult also suggests that regional ªnancial integration has a negative direct effect on

business cycle co-movement, but it also has a positive indirect effect by affecting re-

gional trade integration positively. After considering this indirect positive effect, 这

overall negative effect of internal ªnancial integration on regional business cycle co-

movements may not be all that great.

4.2 Extended analysis

Most coefªcients are estimated signiªcantly in the previous regressions. 因此, infer-

ring which of the variables is the most important in explaining business cycle co-

movements is difªcult. To infer the relative importance of the variables, the method

suggested by Kruskal (1987) is applied in calculating the proportion of variance of

the business cycle correlation explained by each variable.13

手, the result is broadly aligned with that of Kalemli-Ozcan, Papaioannou, and Peydró

(2009). The latter suggested that past studies suffer from omitted variable bias (例如, not con-

trolling the aggregate effect) and that the effect of ªnancial integration on business cycle co-

movements is negative after controlling such a bias.

13 This method can be referred to as the averaging relative importance over all orderings of the

independent variables. 第一的, we calculate the proportion of variance of the dependent vari-

93

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

桌子 7. Partial and relative importance index

A. 东盟(西德:2)3

多变的

时间

F

EXT

EXF

乙. 东盟(西德:2)7

多变的

时间

F

EXT

EXF

Partial corr.

(西德:6)0.42

(西德:6)0.42

(西德:6)0.25

(西德:6)0.50

Partial corr.

(西德:6)0.24

(西德:6)0.25

(西德:6)0.14

(西德:6)0.35

Semipartial corr.

(西德:6)0.37

(西德:6)0.38

(西德:6)0.21

(西德:6)0.46

Semipartial corr.

(西德:6)0.22

(西德:6)0.24

(西德:6)0.12

(西德:6)0.33

Relative importance index

0.06

0.06

0.02

0.09

Relative importance index

0.02

0.03

0.01

0.05

笔记: Partial correlation measures the degree of association between two random variables, with the effect of a set of controlling random

variables removed. The semipartial correlation statistic is similar to the partial correlation statistic. Both measure variance correlations

after certain factors are controlled, but to calculate the semipartial correlation, the third variable is held constant for either x or y,

whereas for partial correlations, the third variable is held constant for both.

桌子 7 shows that the most important variable is external ªnance linkages, 紧随其后

by internal ªnancial integration, suggesting that ªnancial linkages may be more rel-

evant than trade integration in explaining the business cycle synchronization of

亚洲国家. 此外, the sum of the proportion for the two external linkages

is larger than the sum of the proportion for two internal linkages, 这是cons-

tent with the popular notion that Asian economies are signiªcantly affected by the

economic conditions of advanced countries.

We also perform various exercises to check the robustness of the results. 第一的, 我们

use the correlation of real GDP growth rate ((西德:4)

real GDP as the measure of business cycle correlation. 第二, the following alterna-

tive measures for external linkages are used:

1) instead of the correlation of cyclical

EXT1ij

EXF1ij

6

(西德:9) w

∑ kmin{Ti,k, Tj,k}

k = 1

6

(西德:9) w

∑ kmin{fi,k, Fj,k}

k = 1

In these measures, the size of the common external linkage is only considered by

dropping the term that shows the similarity of the external linkage. 第三, alterna-

tive measures for trade and ªnancial integration are considered.

able linearly accounted by the ªrst independent variable. 然后, we calculate the proportion

of the remaining variance of the dependent variable linearly accounted by the second inde-

pendent variable, 等等. 然后, we calculate the average proportion of all possible order-

英格斯. For the details, see Kruskal (1987).

94

亚洲经济文件

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

Economic Integration and Business Cycle Synchronization in Asia

T1i,j

(

(西德:3) 1

时间

∑

t

X

我

,

是

J t

,

i t

,

F1i,j

(

(西德:3) 1

时间

∑

t

我

我

,

是

J t

,

i t

,

+

+

+

+

中号

)

j i t

, ,

是

J t

,

我

j i t

, ,

)

是

J t

,

In contrast to the original measures, these measures also depend on country size.

第四, the business cycle co-movement structure might have caused economic inte-

gration. 在这方面, business cycle correlation measures are constructed for the

sample period of 2002–09, but integration measures are constructed based only on

2001 数据. 第五, we consider an alternative structure of the equation system in

which the external ªnancial (or trade) integration does not affect the internal trade

(or ªnancial) 一体化. 结果, which are generally the same, are reported in

桌子 8.

我

D

哦

w

n

哦

A

d

e

d

F

r

哦

米

H

t

t

p

:

/

/

d

我

r

e

C

t

.

米

我

t

.

/

e

d

你

A

s

e

p

A

r

t

我

C

e

–

p

d

/

我

F

/

/

/

/

/

1

2

1

7

6

1

6

8

8

3

5

4

A

s

e

p

_

A

_

0

0

1

8

8

p

d

.

F

乙

y

G

你

e

s

t

t

哦

n

0

9

S

e

p

e

米

乙

e

r

2

0

2

3

5. 结论

This paper examines the effects of economic integration on the regional business