Desentrañando la aversión a la ambigüedad ∗

Ilke Aydogan†

Lo¨ıc Berger‡

Valentina Bosetti§

Abstracto

We report the results of two experiments designed to better understand the

mechanisms driving decision-making under ambiguity. Provocamos individuo preferir-

ences over different sources of uncertainty, entailing different degrees of complexity,

from subjects with different sophistication levels. Nosotros mostramos que (1) ambiguity

aversion is robust to sophistication, but the strong relationship previously reported

between attitudes toward ambiguity and compound risk is not. (2) Ellsberg am-

biguity attitude can be partly explained by attitudes toward complexity for less

∗We thank Mohammed Abdellaoui, Aur´elien Baillon, Laure Cabantous, Thomas Ep-

por, Helena Hauser, Chen Li, Massimo Marinacci, Sujoy Mukerji, Vincent Th´eroude,

Uyanga Turmunkh, and Peter Wakker for helpful comments and suggestions. Nosotros también

thank seminar and conference participants at D-TEA, FUR, MUSEES, Bocconi Uni-

versity, Ghent University, and LMU for insightful comments and discussions. Somos

grateful to Hans-Joachim Zwiesler for the opportunity to run the experiment at ICA

2018 and thank the organizing committee for their help with the experiment. Nosotros

also thank Diana Valerio for her help with the laboratory experiment. This project

has received funding from the European Union’s Horizon Europe research and innova-

tion programme under grant agreement (No 101056891 CAPABLE), the Agence Na-

tionale de la Recherche (ANR-17-CE03-0008-01 INDUCED and ANR-21-CE03-0018

ENDURA), the Region Hauts-de-France (2021.00865 CLAM), and the I-SITE UNLE

(project IBEBACC). Logistic support from the Bocconi Experimental Laboratory for

the Social Sciences (BELSS) and from the Anthropo-Lab (ETHICS EA 7446) is kindly

acknowledged.

†IESEG School of Management, Univ. Lille, CNRS, UMR 9221 – LEM – Lille ´Economie

Gestión, F-59000 Lille, Francia; and iRisk Research Center on Risk and Uncertainty

(i.aydogan@ieseg.fr).

‡Corresponding author. Univ. Lille, CNRS, IESEG School of Management, UMR

9221 – LEM – Lille ´Economie Management, F-59000 Lille, Francia; iRisk Research Cen-

ter on Risk and Uncertainty; RFF-CMCC European Institute on Economics and the

Environment (EIEE), and Centro Euro-Mediterraneo sui Cambiamenti Climatici, Italia

(loic.berger@cnrs.fr). Phone: +33 320 545 892.

§Department of Economics and IGIER, Bocconi University, and RFF-CMCC Euro-

pean Institute on Economics and the Environment (EIEE), Centro Euro-Mediterraneo

sui Cambiamenti Climatici, Italia (valentina.bosetti@unibocconi.it).

1

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 por el presidente y becarios de Harvard College y el Instituto de Tecnología de Massachusetts. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

sophisticated subjects only. En general, regardless of the subject’s sophistication level,

the main driver of Ellsberg ambiguity attitude is a specific treatment of unknown

probabilities.

Palabras clave: Ambiguity aversion, reduction of compound risk, model uncertainty, com-

plejidad

JEL Classification: C91-C93-D81

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

.

/

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

2

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

1

Introducción

For several decades, the standard way to make rational decisions under uncertainty has

been to follow Savage’s (1954) subjective expected utility (SEU) theory. En 1961, Ellsberg

proposed several experiments challenging canonical axioms of SEU. These experiments

have given rise to a vast literature studying the phenomenon of ambiguity aversion (es decir.,

the preference for known probabilities, or risk, over unknown probabilities, or ambiguity)

at both theoretical and empirical levels. Sin embargo, whether this deviation from SEU

constitutes an irrational response to uncertainty or not remains an open question (Gilboa

et al., 2009, 2010, 2012; Gilboa and Marinacci, 2013). As ambiguity is present and plays an

important role in most real-life decision problems,1 such a question is critical for normative

interpretations of ambiguity attitudes and for the use of ambiguity models in applications

with prescriptive purposes. Por eso, it has profound implications for policymaking (Berger

et al., 2021). Our goal, in this paper, is to clarify the extent to which ambiguity aversion

is tied to an arguable mistake, such as the failure to reduce compound lotteries, y

study its relationship with the decision-makers’ potential limitations or the complexity

of a situation.

We explore experimentally decision-making under uncertainty along three dimensions.

(1) The first dimension concerns the sources of uncertainty.2 We investigate attitudes

1Por ejemplo, in financial economics, Mukerji and Tallon (2001) show how ambiguity

aversion may lead to incompleteness of financial markets, while Easley and O’Hara (2009)

show how it can explain low participation in the stock market despite the potentially high

benefits. In the health domain, Berger et al. (2013) show that ambiguity aversion affects

treatment decisions. In climate change economics, Drouet et al. (2015) and Berger et al.

(2017) show how ambiguity aversion affects optimal emission policies.

2Sources of uncertainty are defined as “groups of events that are generated by the

same mechanism of uncertainty, which implies that they have similar characteristics”

(Abdellaoui et al., 2011, pag. 696).

3

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

toward different sources of risk (presented in simple or compound forms) and ambiguity

(presented in the form of model ambiguity `a la Marinacci (2015)3 or ambiguity `a la

Ellsberg (1961)). Under SEU, the distinction between these sources is irrelevant: todo

ambiguous sources are treated as risks through the assignment of subjective probabilities,

whereas compound risks are reduced to simple risks in accordance with the reduction

of compound lotteries axiom.

(2) The second dimension concerns the subjects’ level

of sophistication. We investigate the preferences of a unique pool of risk professionals

(working in insurance related jobs and possessing a high level of education in the fields of

matemáticas, Estadísticas, or actuarial science) and compare them to those of a convenience

sample of university students. Given their background and their training in dealing

with computationally complex problems requiring proficiency in probabilistic reasoning,

risk professionals can be considered as being more quantitatively “sophisticated” than

estudiantes. (3) Finalmente, the third dimension relates to the complexity of the problem. Por

proposing tasks with varying degrees of complexity within the same source, we are able

to isolate the role of complexity in decision-making under risk and ambiguity.

We elicit individual preferences using a two-color Ellsberg-type setting. The large

body of existing empirical literature using such a setting has so far highlighted two stylized

hechos:

SF1: Individuals are ambiguity averse.

SF2: There exists a strong relationship between attitudes towards ambiguity and com-

pound risk.

SF1 results from the many experiments that have formally tested Ellsberg’s (1961) idea,

typically using student subjects (L’Haridon et al., 2018; see also the reviews of Machina

3Model ambiguity arises when the decision-maker is not able to identify a single proba-

bility distribution (among a set of probability models) corresponding to the phenomenon

de interés (Hansen, 2014; Marinacci, 2015).

4

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

and Siniscalchi, 2014; Trautmann and van de Kuilen, 2015).4 It also typically generalizes

to alternative subject pools, including risk professionals (Cabantous, 2007; Cabantous

et al., 2011; Hogarth and Kunreuther, 1989). While ambiguity and compound risks have

distinct properties, SF2 has been put forward by Halevy (2007), who documented strong

similarities in attitudes towards Ellsberg ambiguity and compound risks among student

sujetos. Based on his findings, Halevy wrote “The results suggest that failure to reduce

compound (objetivo) lotteries is the underlying factor of the Ellsberg paradox.” (halevy,

2007, pag. 532). Such findings have been replicated on other student samples (p.ej., Masticar

et al., 2017; Dean and Ortoleva, 2019; Gillen et al., 2019), and on a representative sample

of the U.S. población (Chapman et al., 2018). Whether explicitly or implicitly, SF2

has been invoked to challenge the normative status of ambiguity aversion. Específicamente,

if non-reduction of compound (o, more generally, of complex) risks is considered as a

mistake (possibly related to computational difficulties), and if the subjects making this

“mistake” are mainly those who are ambiguity non-neutral, there would be little room

for using ambiguity models for normative purposes.

Although results in line with SF1 and SF2 have consistently emerged from the lit-

erature, their relationship with the subjects’ level of sophistication has received little

attention so far. Exceptions are the studies of Chew et al. (2018), who investigate the

role of subjects’ level of comprehension for SF1; and Abdellaoui et al. (2015), and Berger

and Bosetti (2020), who report somewhat weaker relationships between ambiguity and

compound risk attitudes among engineering students and climate policymakers respec-

activamente. Además, the role of complexity as a factor contributing to explain SF1 and SF2

remains largely understudied, with the exceptions of Armantier and Treich (2016), y

Kov´aˇr´ık et al. (2016). Our paper attempts to fill these gaps by examining two research

4We note that ambiguity seeking is also common for ambiguous events with low like-

medios de vida. This local ambiguity seeking attitude is shown to be due to an ambiguity-

generated likelihood insensitivity (Dimmock et al., 2015). Our study focuses on proba-

bilities around 50% and does not consider this other component of ambiguity attitudes.

5

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

preguntas:

RQ1: Are SF1 & SF2 robust to sophistication?

RQ2: What are the main drivers of ambiguity attitude?

To answer these questions, we specifically targeted a sample of risk professionals, OMS

possess a high level of sophistication in probabilistic reasoning. Hasta donde sabemos, we are

the first to study the preferences of such a unique pool of subjects in an incentivized ex-

periment with a simple, context-free, design allowing us to make direct comparisons with

other subject pools. Although focusing on such a unique sample necessarily sacrifices

representativeness, it enables us to answer our first research question and to bring novel

insights on the role of sophistication. Our second research question aims at disentangling

the driving mechanisms of the Ellsberg paradox. Different explanations have been pro-

posed in the literature: Following theories that equate ambiguity to compound risk (p.ej.,

Segal, 1987; SEO, 2009), the driving factor of the Ellsberg paradox is the failure to reduce

compound risks.5 Along similar lines, some recent studies have suggested that ambiguity

aversion can be related to an aversion towards complex risks (p.ej., Armantier and Treich,

2016; Kov´aˇr´ık et al., 2016). Alternativamente, according to a variety of theoretical models

with normative underpinnings (see Gilboa and Marinacci, 2013, para una revisión), Ellsberg-

type behaviors are primarily driven by a specific attitude towards unknown probabilities.

En lo que sigue, we analyze the effect of these factors to understand their respective roles

in explaining SF1 and SF2, and relate them to the subjects’ sophistication level.

2 experimentos

We report the results of two experiments. The data were collected in the context

of a broad research project investigating the layers of uncertainty (see Aydogan et al.,

5Segal (1987, pag. 179) wrote: “In other words, risk aversion and ambiguity aversion

are two sides of the same coin, and the rejection of the Ellsberg urn does not require a

new concept of ambiguity aversion, or a new concept of risk aversion.”

6

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

2023). Específicamente, Aydogan et al. (2023) proposed and experimentally tested the layer

hypothesis by comparing attitudes towards the layers of risk, model ambiguity, and model

misspecification. They reported behavioral differences across the three layers based on a

main experiment conducted with university students, which was supplemented by robust-

ness experiments conducted with different subject pools (including risk professionals). En

el estudio actual, we use a subset of the same data to address the distinct research ques-

tions RQ1 and RQ2.6 In particular, the current study focuses on the contrast between

two specific subject pools with distinct characteristics and documents new results on the

relationship between uncertainty, sophistication, and the level of complexity.

2.1 Samples

We consider two distinct samples. The main experiment in this study is an artefactual

field experiment run on a unique pool of risk professionals (actuaries). The control

experiment is a standard laboratory experiment with university students.

Actuaries at ICA We collected data from 84 risk professionals during the 31st Inter-

national Congress of Actuaries (ICA).7 The average age was around 40 y 44% del

subjects were female. The subjects were highly educated: 58 sujetos (69%) reported

a master’s degree as the highest level of education completed and 18 sujetos (21%) re-

ported a PhD degree. 46 subjects reported that their highest degree was obtained in a

field related to mathematics and statistics, mientras 17 subjects reported it related to actu-

6More specifically in the current study, we leave out the treatments involving model

misspecification and report on the standard Ellsberg treatment, which is different from

the Extended Ellsberg treatment reported in the main analysis of Aydogan et al. (2023).

7ICA is a conference organized by the International Actuarial Association every four

años. It gathers more than 2,500 actuaries, academics, and high-ranking representatives

from the international insurance and financial industry. The 31st congress was held from

Junio 4 a 8, 2018, in Berlin, Alemania.

7

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

.

/

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

arial sciences. The remaining subjects reported diplomas in physics (2), engineering (1),

finance (1), economics and management (3), or did not report anything (14). Finalmente, el

subjects had an average of 13 years of relevant work experience.

University students We collected data from 125 social science students at Bocconi

Universidad, Italia. At the time of the experiment, 80 de ellos (64%) were in a bachelor’s

program while 34 (27%) were in a master’s program, y el resto (9%) were in a PhD

programa. 42% of the subjects were female, and the average age was 20.5.

En lo que sigue, we characterize sophistication by the background of the subjects.

En ese sentido, actuaries are considered as more “sophisticated” than students. Such a

distinction is justified on the ground that actuaries are experts in decision-making under

uncertainty and experienced risk evaluators, who are used to make decisions in situations

of ambiguity in their professional roles. They also possess a high training in statistics,

probability and decision theory. debería, sin embargo, be clear that different dimensions may

arguably contribute to making the pool of actuaries different than that of students. En

particular, the two samples differ in the following dimensions: (1) Curriculum: 79% del

actuaries possess a training in STEM (ciencia, tecnología, engineering, y matemáticas),

while the students are in social science programs; (2) Level of education: 90% del

actuaries reported to hold at least a master’s degree, while this is the case for only 9%

of the students; (3) Experience: actuaries reported an average 13 years of relevant work

experiencia, whereas most students had no work experience at all. Además, the age

difference between the two groups could be seen as a confounder to what precedes. Nosotros

report the results of a within-sample heterogeneity analysis in the Online Appendix.

2.2 Diseño

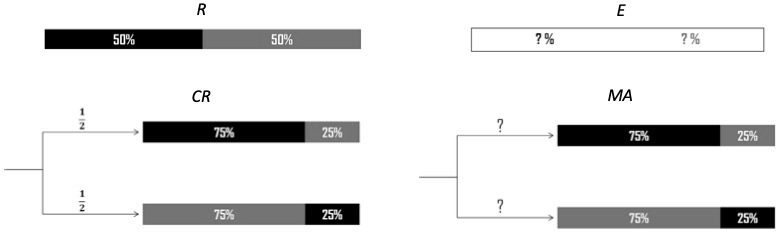

Sources of uncertainty We use a within subject design to study individual choices

under risk and ambiguity. The experiment entails betting on the color of a card drawn

from a deck in different situations. We consider the following four distinct sources of

uncertainty that are constructed in a two-color Ellsberg-type setting (Ver también Figura 1

8

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

(a)).

1. (R) Risk entails a deck that contains equal proportions of black and red cards.

2. (CR) Compound Risk entails, with equal probabilities, either a deck that contains

p% red and (1 − p)% black cards, or a deck that contains p% black and (1 − p)%

red cards.

3. (M A) Model Ambiguity entails, with unknown probabilities, either a deck that

contains p% red and (1 − p)% black cards, or a deck that contains p% black and

(1 − p)% red cards.

4. (mi) Ellsberg ambiguity entails a deck of 100 cards that contains an unknown pro-

portion of black and red cards.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

9

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

(a) Illustration of the four sources of uncertainty (here p = 25 in CR and M A)

(b)

(C)

Cifra 1: Sources of uncertainty and their characteristics

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

10

RiskAmbiguityRECRMANon compoundCompound1.a1.b1.cGlobal attitudes towards sourcesCR0MA0CR25MA25Less complexMore complex3223Attitudes CompoundriskModelambiguityReview of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

The sources R and CR are two sources of risk (known probabilities), mientras que el

sources M A and E are ambiguous (unknown probabilities). The sources CR and M A are

compounded as they explicitly entail two stages, with two potential deck compositions.

They differ from each other in the type of uncertainty they entail in the first stage.

Específicamente, the two possible deck compositions are unambiguously assigned an objective

50% probability under CR, whereas these probabilities are unknown in the case of M A.

On the basis of a symmetry argument, a 50% probability could be assigned to the two

possible deck compositions under M A, but these probabilities would then necessarily be

subjectively determined.8 E is the standard ambiguous source originally proposed by

Ellsberg (1961).

Complexity We consider a notion of complexity related to the number of stages of

uncertainty a situation features. Respectivamente, for each source CR and M A, we propose

two distinct cases that are characterized by different levels of complexity. In the first case,

we consider p = 0 so that the deck features a degenerate distribution: it contains either

100% black or 100% red cards. We denote the corresponding situations CR0 and M A0.9

This case is of minimal complexity: although the situation is presented in two stages, él

entails only one stage of uncertainty (as all the uncertainty stems from the first stage).

The second case considers p = 25, so that the deck contains either 25% rojo (y 75%

8In our experiment, symmetry in the prior distribution stems from the indifference

between betting on a red or black card. The symmetry condition can also be justified

on the grounds of a general symmetry of information argument: given the information

disponible, there is a priori no reason to believe that one composition deserves more weight

than another.

9In the literature, CR0 has also been used to study the hypothesis of time neutrality

(Segal, 1987, 1990; Dillenberger, 2010; Nielsen, 2020), es decir., the indifference between early

and late resolution of risk. It should be clear that the time dimension is not considered

in our experiment.

11

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

.

/

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

negro) cards or 25% negro (y 75% rojo) cards. We denote the corresponding situations

CR25 and M A25.10

Procedure Our experiments measure individual preferences over the situations R, CR0,

CR25, M A0, M A25, y e. For each of them, the subjects faced a bet on the color of a

card randomly drawn from a deck. For every bet, the winning color was determined by

the subjects themselves. We elicited the certainty equivalents (CEs) of the bets using a

choice-list design. We use the midpoint of an indifference interval implied by a switching

point as a proxy for the CE of a bet. In view of the stark income gap between risk pro-

fessionals and students (see Online Appendix), we adjusted the stakes offered to the two

groups by a factor of 10. Específicamente, bets yielded either e200 or e0 in the experiment

with actuaries and either e20 or e0 in the experiment with students. We used a standard

prior within-subject random incentive mechanism in the lab (es decir., all students were paid

based on one of their choices) but adopted a between-subject random incentive system in

the field (es decir., one-in-ten actuaries was paid) due to budgetary and logistical constraints.11

The details of the experimental procedures are provided in the Online Appendix.

10Note that our characterization of complexity can also be seen as referring to the

number of branches of a lottery. It is consistent with Chew et al. (2017, Ver nota al pie 20)

in the case of compound risk, and with the notion of complexity under simple risk, cual

is typically assessed by the number of different outcomes of the lottery (Sonsino et al.,

2002; Moffatt et al., 2015).

11Previous literature has reported no systematic difference between paying all subjects

or paying one-of-N (Beaud and Willinger 2015; Clot et al. 2018; Berlin et al. 2022). Nota

also that to further encourage risk professionals to reveal their preferences conditional on

being selected for payment, we carried out the between-subject randomization prior to the

experimento, thus enhancing the isolation assumption of Kahneman and Tversky (1979)

(see Johnson et al., 2021 for more discussion on the prior random incentive mechanisms).

Under the isolation assumption, the higher stakes offered to actuaries compensate for the

12

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

.

/

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

3 A relative premium measure

To examine attitudes toward the different sources of uncertainty, we introduce the

following premia measure relative to risk (R).

Definición 1. The relative premium ΠR,j is the difference between the CE of the bet on

R (CER) and the CE of the bet on j (CEj), expressed in % of the CE of the bet on the

most preferred situation:

ΠR,j ≡

CER − CEj

máximo {CER, CEj}

∀j ∈ {CR0, CR25, M A0, M A25, mi} .

(1)

Intuitivamente, two cases can be distinguished. If the individual is relatively more averse to

the uncertainty present in situation j, the preferred bet is the one on R, and the relative

premium represents the percentage of extra money that an individual would be ready to

sacrifice to avoid betting on j, relative to the value of the bet on R. Symmetrically, si

the preferred situation is j, the relative premium ΠR,j represents the extra money that

would be sacrificed to avoid betting on R, relative to the value of the bet on j. This index

possesses some desirable properties. Primero, ΠR,j is symmetric around zero across relatively

more or less averse preferences. Segundo, ΠR,j belongs to the interval [−1; 1], which also

makes it easy to interpret in terms of percentages. Por último, the normalization with respect

to the maximum CE allows more robust comparisons among subject pools by controlling

for differences in payoffs and subjects’ overall level of uncertainty attitudes.12

In the literature, ΠR,E has been commonly referred to as the Ellsberg-ambiguity pre-

mium (ver, p.ej., Berger, 2011; Maccheroni et al., 2013), and ΠR,CR as the compound risk

large income gap between risk professionals and students (see Online Appendix).

12In the Online Appendix, discutimos

some alternative measures

that have

been proposed in the literature, such as ΠR,j ≡ (CER − CEj)/CER or ΠR,j ≡

(CER − CEj)/(CER + CEj) (Sutter et al., 2013; Trautmann and van de Kuilen, 2015).

Our conclusions do not differ when using these alternative definitions.

13

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

premium (ver, p.ej., Abdellaoui et al., 2015).

En la misma vena, ΠR,M A represents the

model ambiguity premium. These premia are represented by the arrows 1.a-c in Figure

1(b). The relative premium can furthermore be used to measure the effects of complexity

and of a specific attitude toward unknown probabilities (in the first stage), as illustrated

by arrows 2 y 3 En figura 1(C). Específicamente, as the sources CR and M A both present

a relatively less and more complex case (es decir., one stage of uncertainty when p = 0 vs.

two stages of uncertainty when p = 25), the effect of complexity, within each source, poder

be examined by (ΠR,CR25 − ΠR,CR0) y (ΠR,M A25 − ΠR,M A0). These differences indicate

whether the compound risk or model ambiguity premia are larger in more complex cases

than in less complex ones. Similarmente, (ΠR,M A0 − ΠR,CR0) y (ΠR,M A25 − ΠR,CR25) gorra-

ture the effect of the distinct treatment of known and unknown probabilities in the first

stage within situations entailing the same degree of complexity.

4 Resultados

Our data consist of six choice lists per subject. Observations with multiple-switching,

reverse-switching, or no-switching patterns are not included in the analysis as they do

not provide clear measurements of the CEs.13 We do not detect any order effect on

tratos (see Online Appendix).

13The proportions of subjects affected by such inconsistencies in at least one of the

choice lists are 11.9% for actuaries (10 fuera de 84) y 10.4% for students (13 fuera de 125)

and do not differ across the two samples (two-sample Z-test of proportions, p=0.73).

Discarding four actuaries who show inconsistent patterns in all lists, suggesting a lack of

attention to the experiment, inconsistencies were present in 16 fuera de 480 liza (3.3%) para

actuaries and in 25 fuera de 750 liza (3.3%) for students. These proportions are notably

lower than what is typically observed in the literature (Yu et al., 2021).

14

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

d

oh

i

/

/

.

1

0

1

1

6

2

/

r

mi

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

mi

s

t

_

a

_

0

1

3

5

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 Internacional (CC POR 4.0) licencia.

4.1 General attitudes toward different sources of uncertainty

Mesa 1 presents the mean relative premia. We observe that both groups of subjects

are comparable in terms of ambiguity premia, exhibiting aversion toward the sources M A

y e (t-tests, pag<0.001).14 This suggests that ambiguity aversion (SF1) is robust to the

subjects’ level of sophistication. Regarding the source CR, the average relative premium

for CR25 is positive for students (p<0.001), indicating aversion toward compound risk,

but we cannot reject the null hypothesis that ΠR,CR25 = 0 for actuaries (t-test, p=0.03 but

p=0.17 after Bonferroni correction15). The difference between actuaries and students is

particularly marked for this premium (t-test, p<0.001). In contrast, the average relative

premium for the less complex case CR0 does not differ from zero for both groups (t-test,

p=0.59 for actuaries, and p=0.55 for students).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

14Testing multiple hypotheses

(e.g.,

testing H0

: ΠR,j = 0 for all j ∈

{CR0, CR25, M A0, M A25, E}) may require Bonferroni corrections. To allow for direct

comparisons with previous literature, we report the original p-values, together with Bon-

ferroni corrections when these affect the results.

15The minimum detectable difference from zero mean premium for 5% level of signifi-

cance (with Bonferroni correction) and a power of 90% is 0.043.

15

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Table 1: Average premia relative to risk

Actuaries

Students

ΠR,CR0

ΠR,CR25

-0.007 (0.0127)

0.023∗ (0.0108)

0.010 (0.0171)

0.136∗∗∗ (0.0216)

Two-sample tests

(p-value)

0.472

<0.001

ΠR,M A0

ΠR,M A25

ΠR,E

Notes: Standard errors in parentheses. The tests are based on two-sided t-tests.

0.121∗∗∗ (0.0324)

0.106∗∗∗ (0.0227)

0.190∗∗∗ (0.0316)

0.130∗∗∗ (0.0219)

0.181∗∗∗ (0.0227)

0.191∗∗∗ (0.0249)

0.814

0.027

0.982

∗∗∗

significant at 0.001, ∗∗ significant at 0.01, ∗ significant at 0.05. Significance stars are

based on p-values before Bonferroni correction. Values that are significant at 0.05 after

Bonferroni correction are bolded.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

/

.

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

16

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

4.2 The relationship between ambiguity and compound risk at-

titudes

Following the existing literature, we investigate the relationship between attitudes

towards ambiguity and compound risk within our two subject pools and test the robust-

ness of SF2 to sophistication. Table 2 reports the Pearson correlation coefficients between

compound risk premia and ambiguity premia.16 In line with SF2, we observe a significant

correlation between attitudes toward ambiguity and compound risk for students (except

between ΠR,CR0 and ΠR,E, p=0.475). However, such a relationship is absent in the case

of actuaries.17

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

16The same conclusions are obtained with Spearman rank correlations, which measure

monotonic –rather than linear– relationships between premia (see Online Appendix).

17We also analyzed correlations based on the method of obviously related instrumen-

tal variables (ORIV) developed by Gillen et al. (2019) to correct for measurement

errors. ORIV uses an instrumental variable approach to compute correlations when

there are multiple measurements of behavioral variables. We used ORIV in our data

by using multiple elicitations of preferences under compound risk and model ambigu-

ity (i.e., with p = 0 and p = 25). We observe that, although the correlations be-

tween compound risk and ambiguity using ORIV are consistently high for students:

corr(ΠR,CR, ΠR,M A)=0.988 and corr(ΠR,CR, ΠR,E)=0.916, they remain remarkably low for

actuaries: corr(ΠR,CR, ΠR,M A)=0.369 and corr(ΠR,CR, ΠR,E)=0.057.

17

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Table 2: Pearson correlations between compound risk and ambiguity pre-

mia

Actuaries

Students

ΠR,M A0 ΠR,M A25

ΠR,E

ΠR,M A0 ΠR,M A25

ΠR,E

0.169

0.135

-0.033

-0.078

ΠR,CR0

ΠR,CR25

Notes: ∗∗∗ significant at 0.001, ∗∗ significant at 0.01, ∗ significant at 0.05. Significance

stars are based on p-values before Bonferroni correction. Values that are significant at

0.05 after Bonferroni correction are bolded.

0.315∗∗∗ 0.344∗∗∗

0.407∗∗∗ 0.652∗∗∗ 0.475∗∗∗

ΠR,CR0

ΠR,CR25

0.067

0.107

0.109

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

/

.

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

18

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Next, we examine the links between ambiguity neutrality and reduction of compound

risk. We adopted a comprehensive definition of ambiguity neutrality according to which a

subject is considered as ambiguity neutral if ΠR,E = ΠR,M A0 = ΠR,M A25 = 0.18 Similarly,

a subject is said to be reducing compound risk if ΠR,CR0 = ΠR,CR25 = 0.

The proportion of ambiguity non-neutrality among subjects who do not reduce com-

pound risk is 95% (=20/21) for actuaries and 94% (=77/82) for students. These propor-

tions, which are in line with the literature, suggest that non-reduction of CR is sufficient

for ambiguity non-neutrality, irrespective of the subjects’ sophistication level. Turning to

necessity, we find that 80% (=77/96) of ambiguity non-neutral students are also not re-

ducing CR. However, this proportion is 57% (=20/35) for actuaries, which is significantly

less than for students (two-sample test of proportions, p=0.008). This result indicates

that, although compound risk non-reduction appears to be also necessary for ambiguity

non-neutrality when less sophisticated subjects are considered, this is not the case for

more sophisticated ones. Overall, this first set of results enables us to answer RQ1.

Result 1 (a) Ambiguity aversion is robust to the subjects’ sophistication level, but (b)

the strong relationship between attitudes toward ambiguity and compound risk is not.

4.3 Complexity and ambiguity

We now focus on compound sources to examine the effects of complexity and ambiguity

in different subject pools. For this, we run a regression analysis with random effects at

individual level, where the relative premia ΠR,j for j ∈ {CR0, CR25, M A0, M A25} are

regressed on a dummy for complexity (taking value 1 if j ∈ {CR25, M A25}), a dummy

for the presence of ambiguity (taking value 1 if j ∈ {M A0, M A25}), and their interaction.

The baseline is the behavior in a compound risk situation with minimal complexity. To

test the effect of sophistication, we run a regression by pooling data from the two samples

and using a dummy for actuaries.

18Our conclusions are robust to the use of alternative definitions of ambiguity neutrality

under M A and E separately (see Online Appendix).

19

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Table 3 reports the results. We observe positive coefficients for complexity and model

ambiguity, indicating that the relative premia are higher when the situation is more

complex or does not entail objective probabilities, in comparison to the less complex

situation with objective probabilities (i.e., CR0). Therefore, both students and actuaries

can be said to be averse to complexity and unknown probabilities in the first-stage.

However, the effect of complexity is significantly lower among actuaries than among

students, although there is no difference between the two groups regarding the effect of

unknown probabilities. We also observe a negative interaction between the variables,

suggesting that the effect of complexity is less pronounced in the presence of model

ambiguity. This interaction is significant for students but not for actuaries.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

20

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Table 3: Random Effects Regressions of Relative Premia

Complexity

Model ambiguity

Complexity × Model ambiguity

Constant

Actuaries

Students

0.031∗

(0.015)

0.128∗∗∗

(0.033)

-0.046

(0.031)

0.123∗∗∗

(0.023)

0.120∗∗∗

(0.023)

-0.075∗∗

(0.026)

-0.006

(0.013)

299

0.010

(0.017)

471

Effect of

sophistication

(pooled data)

-0.092∗∗∗

(0.027)

0.008

(0.040)

0.028

(0.040)

-0.016

(0.021)

770

Observations

Notes: Cluster-robust standard errors in parentheses.

∗∗∗ significant at 0.001, ∗∗

significant at 0.01, ∗ significant at 0.05. Similar results are obtained when controling

for age, gender, income, and education (see Online Appendix).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

21

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

4.4 Explaining Ellsberg ambiguity

Based on what precedes, we now investigate the roles of attitudes toward complex-

ity and unknown probabilities, together with the failure of the reduction principle in

explaining Ellsberg-ambiguity attitude. We use the following OLS regression:

E-AM Bi = β0 + β1COM P Xi + β2U N KN OW Ni + β3REDi + εi,

(2)

where Ellsberg ambiguity attitude (E-AM B) for subject i is computed by ΠR,E. At-

titudes toward complexity and unknown probabilities (COM P X and U N KN OW N ,

respectively) are both measured with respect to ΠR,CR0 to isolate their pure effects

and avoid interactions between them. Specifically, complexity attitude is captured by

(ΠR,CR25 − ΠR,CR0), which computes the difference between the compound risk premia

under different degrees of complexity.19 Attitude toward unknown probabilities is mea-

sured by (ΠR,M A0 − ΠR,CR0), which captures the difference in relative premia between

two compound situations presenting the same degree of complexity, but different type

of probabilities in their first stage.20 Finally, the measure of reduction (RED) is based

on ΠR,CR0: As CR0 is arguably the most easily reducible compound risk situation, its

non-reduction shows a clear failure of the reduction principle (rather than a failure to

deal with complexity). The dummy for (non-) reduction takes 1 if ΠR,CR0 (cid:54)= 0 and 0

otherwise.

Table 4 reports the results of the regressions. We find that attitude toward un-

known probabilities has a positive and significant impact for both actuaries and stu-

19Note that the alternative, which is to use (ΠR,M A25 − ΠR,M A0), could be confounded

by ambiguity attitudes because M A0 may also be seen as being more ambiguous than

M A25 due to a larger spread of first stage probabilities (see Jewitt and Mukerji, 2017;

Berger, 2022).

20The alternative, which is to use (ΠR,M A25 − ΠR,CR25) could be confounded by risk

attitudes because of the presence of risk in the second stage (see the discussion in Berger

and Bosetti, 2020).

22

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

/

.

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

dents. The magnitudes of the coefficients indicate that one percentage point increase in

(ΠR,M A0 − ΠR,CR0) leads to 0.74 percentage points increase in ΠR,E for actuaries, and to

0.43 percentage points increase for students. The difference in this coefficient between

the two groups is significant (p = 0.03), indicating a stronger effect of attitude toward

unknown probabilities for actuaries. In contrast, complexity attitude has a positive and

significant impact for students only. The difference in the magnitude of the coefficients

between the groups suggests that the effect of complexity is also more pronounced for

students (p=0.04). Finally, the positive coefficients of the reduction variable suggest that

failure of the reduction principle increases the ambiguity premium, although the coeffi-

cients are neither significant nor different in the two groups. Overall, this second set of

results enables us to answer RQ2.

Result 2:

(a) For both actuaries and students, the main driver of Ellsberg-ambiguity

attitude is a specific treatment of unknown probabilities. (b) A specific attitude toward

complexity is found to play a significant role in explaining Ellsberg-ambiguity attitude for

students only.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

/

.

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

23

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

Table 4: OLS Regressions of Ellsberg Ambiguity Premium

COM P X

U N KN OW N

RED

Constant

Actuaries

Students

-0.170

(0.167)

0.735∗∗∗

(0.091)

0.137

(0.074)

0.079∗∗

(0.026)

0.253∗

(0.116)

0.434∗∗∗

(0.106)

0.036

(0.048)

0.091∗∗∗

(0.024)

Difference between

groups (pooled

data)

-0.423∗

(0.203)

0.302∗

(0.140)

0.101

(0.088)

-0.012

(0.036)

Observations

Notes: Robust standard errors in parentheses, ∗∗∗ significant at 0.001, ∗∗ signif-

188

114

74

icant at 0.01, ∗ significant at 0.05. Simlar results are obtained when controling

for age, gender, income, and education.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

24

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

5 Concluding remarks

Decisions made by unusual subject pools, such as climate policymakers (Berger and

Bosetti, 2020), professional traders (Fox et al., 1996), professional chess players (Levitt

et al., 2011), or golf players (Pope and Schweitzer, 2011) have been the focus of stud-

ies trying to explain important behavioral phenomena. Following this line of research,

we focus on a unique pool of risk professionals to re-examine two stylized facts about

ambiguity attitudes, which have emerged in the literature. Because these professionals

routinely price risk and uncertainty at work, their occupational practice makes them of

special interest for studying decision-making under uncertainty.

Our results show that this selected group of subjects is as much affected by ambi-

guity as a standard pool of university students. However, attitudes towards ambiguity

and compound risk are less closely related for risk professionals than for students. In

particular, compound risk non-reduction is found sufficient but not necessary for am-

biguity non-neutrality for these more sophisticated subjects. We argue that attitudes

toward complexity may explain these findings. Indeed, if ambiguity is viewed as a com-

pound source of uncertainty, or presented as such (as in model ambiguity situations),

non-reduction of compound risk can be sufficient for ambiguity non-neutrality. On the

other hand, if complexity makes compound risk situations being perceived as ambiguous

by some subjects, those who are ambiguity non-neutral will also exhibit compound risk

non-reduction (and hence the necessity). Interestingly, this effect is significantly weaker

for more sophisticated subjects, who are less affected by the complexity of a situation.

Consistent with this interpretation, we observe that a non-negligible proportion of ambi-

guity non-neutral actuaries do actually reduce compound risk.

The paper closest to ours is Abdellaoui et al. (2015), who compared two student

samples differing in their training (engineering vs. non-engineering fields). While they

also report a somewhat weaker link between compound risk and ambiguity for more

quantitatively sophisticated students, the differences they find between their two student

samples are not as stark as those between students and actuaries. By studying a pool of

25

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

d

o

i

/

.

/

1

0

1

1

6

2

/

r

e

s

t

_

a

_

0

1

3

5

8

2

1

5

6

1

6

6

/

r

e

s

t

_

a

_

0

1

3

5

8

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Review of Economics and Statistics Just Accepted MS. https://doi.org/10.1162/rest_a_01358 © 2023 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0 International (CC BY 4.0) license.

risk professionals, whose contrast with students is more extreme, our study may be seen

as more revealing for the role of sophistication in decision-making. Yet we also note that

differences in sophistication might exist within the populations studied. An additional

analysis of our data indeed indicates some heterogeneity among students but not among

risk professionals (for the details, see Online Appendix). For example, undergraduate

students are found to be more affected by complexity than graduate ones, whereas work

experience (or age) is not found to play any role among actuaries.

We argue that our findings may have important implications for different ambiguity

models. Overall, by suggesting that ambiguity aversion is mainly driven by a genuine

preference for known probabilities over unknown ones, but not necessarily by an inabil-

ity/aversion to deal with the compoundness or complexity of a situation, the results

we report in this paper are more consistent with the predictions of ambiguity theories

with normative underpinnings. Thus, they leave room for using ambiguity models in

applications with prescriptive purposes.

l

D

o

w

n

o

a

d

e

d

f

r

o