Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Understanding the Sources of Friction

in U.S.–China Trade Relations: El

Exchange Rate Debate Diverts

Attention from Optimum Adjustment*

Wing Thye Woo

Brookings Institution

Washington DC

Universidad de California, davis

Central University of Finance

and Economics, Beijing

Brookings Institution

1775 Massachusetts Avenue,

NW

Washington, corriente continua 20036

EE.UU

wwoo@brookings.edu

Abstracto

China has been accused of exchange rate manipulation that has

caused large U.S. trade deficits, which have reduced U.S. welfare

by increasing unemployment and reducing wages. De hecho, el

strong claims by some observers that the trade imbalances are

deeply deleterious to China’s welfare almost make it a moral im-

perative for the United States to use tariffs to force an renminbi

(RMB) appreciation for China’s own good.

The truth, sin embargo, is that:

(cid:129) The claim that a 40 percent appreciation of the renminbi (RMB)

against the US$ would reduce the U.S. global trade deficit repre- sents the triumph of hope over experience. When the average Yen–US$ exchange rate fell from 239 en 1985 a 128 en 1988,

Estados Unidos. global current account deficit only fell from 2.1 por ciento

a 1.7 percent of GDP because the United States replaced Jap-

anese imports with imports from other countries. For similar

razones, a large RMB appreciation would not reduce the United

States trade deficits significantly.

(cid:129) The claim that China’s swelling balance of payments surplus had

caused the People’s Bank of China (PBC) to lose some control of

credit growth is wrong. Chinese banks face credit quotas, y

credit growth could not have stayed high in 2003–07 without

continual upward adjustments of the credit quotas by the PBC.

The reason is not technical inability to control money growth

but the political reality of factional politics.

(cid:129) The alleged negative effects on U.S. labor from the trade imbal-

ances are greatly exaggerated. The average unemployment rate

in 1999–2006 was 5 percent compared to 6 por ciento en

1991–98; and the total compensation (including benefits) para

blue-collar workers rose in the 1991–2006 period. Besides ac-

celerated globalization, accelerated technological innovation

* I am grateful to the Asian Economic Panel for insightful com-

ments on an earlier draft; and to Gary Burtless for invaluable

help compiling labor market data.

Asian Economic Papers 7:3

© 2008 The Earth Institute at Columbia University and the Massachusetts

Institute of Technology

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

was another important trend in this period. The latter produced large productivity gains that

enabled labor income to rise despite the greater competition from imports. These two

trends caused more frequent job turnovers, which increased worker anxiety, and hence de-

mand for protection.

China’s current account surplus exists because its dysfunctional financial system cannot inter-

mediate the growing savings into investments. The private savings rate is high because China

does not have the variety of financial institutions that would 1) pool risks by providing medical

insurance, pension insurance, and unemployment insurance; y 2) transform savings into edu-

cation loans, housing loans, and other types of investment loans. The backward financial system

in China has made the private savings rate in China 7.0 a 12.2 percentage points higher than

in the United States.

The optimal solution to the present trade tensions is a policy package that emphasizes multilat-

eral actions. It is bad economics and bad politics to focus on only one party (China alone must

cambiar), on only one instrument (RMB appreciation alone), or on only one policy objective

(current account balance).

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

1. The acrimony over China’s exchange rate policy and the drift toward

protectionism

China’s current account (California) balance has been in chronic surplus since 1994. Alabama-

though the CA surplus did rise rapidly from 1.4 percent of GDP in 1994 a 3.8 por-

cent in 1997 y 3.9 por ciento en 1998, it also quickly fell to 2.7 por ciento en 1999 y

stayed below that value in 2000–03. Cifra 1 muestra 2004 to be a turning point in

China’s CA behavior. The CA surplus accelerated from 2.2 percent of GDP in 2003 a

3.5 percent of GDP in 2004, and then surged to unprecedented values: 7.2 por ciento en

2005, 8.7 por ciento en 2006, y 9.5 por ciento en 2007. One disharmonious result from

this large sustained rise in China’s CA surplus is that increasingly harsh words are

being said about China’s trading practices and exchange rate policy.

At a U.S. congressional hearing in March 2007, Morris Goldstein (2007) opined that

the RMB was overvalued by 40 percent against the US$ and accused China of ex- change rate manipulation, a charge echoed by Fred Bergsten (2007). On 14 Junio 2007, four U.S. Senators introduced legislation “to punish China if it did not change its policy of intervening in currency markets to keep the exchange value of the cur- rency, the Yuan, low.”1 Barack Obama, the Democratic presidential nominee, has de- clared that he supports the bill.2 1 “4 in Senate Seek Penalty for China,"El New York Times, 14 Junio 2007. 2 “Clinton and Obama back China crackdown,” Financial Times, 5 Julio 2007. 62 Asian Economic Papers Understanding the Sources of Friction in U.S.–China Trade Relations l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 7 0 0 2 – 8 7 9 1 , t n u o c c a t n e r r u c , n o i t a º n i , h t w o r G — a n i h C . 1 e r u g i F 63 Asian Economic Papers Understanding the Sources of Friction in U.S.–China Trade Relations The introduction of the U.S. Senate bill was followed by demands from the Interna- tional Monetary Fund (IMF) and the European Union (EU) that China change its policy regime on external economic engagement. On 19 Junio 2007, the IMF, with strong endorsement from the U.S. Treasury, adopted a new country surveillance framework that sets out a catchall obligation on countries not to adopt policies that undermine the stability of the international system, and lists a set of objective criteria that will be used to indicate whether a country is complying with its commitments. Warning lights will include large-scale currency intervention, the accumulation of reserves and “fundamental exchange rate misalignment”—a term that mirrors language in a bill before the U.S. Congress that would impose penalties on nations that fail to correct such misalignments. . . . Rodrigo Rato, managing director of the IMF, dicho: “This decision is good news for the IMF reform pro- gramme and good news for the cause of multilateralism . . . [because this new framework]” gives clear guidance to our members on how they should run their exchange rate policies, on what is acceptable to the international community and what is not.3 According to the Evening Standard of the United Kingdom (“Mandelson: China Trade ‘Out of Control’," 17 Octubre 2007): European Trade Commissioner Peter Mandelson has warned that China is taking business with Europe for granted. Writing to EU President Jose Manuel Barroso, he said: “The Chinese juggernaut is, hasta cierto punto, out of control.” China is the EU’s largest source of manufactured goods but trade the other way is negligible. Mandelson called the relationship “deeply unequal” and said China was being “procedurally obstructive”. Under the headline of “EU Hoping to Hit Back at Chinese on Trade,” the Interna- tional Herald Tribune reported on 18 Octubre 2007: [Peter Mandelson, the European trade commissioner, admitted] that dialogue and cooperation with Beijing have failed to secure concessions for Europe, [and he called for the EU to] align policy more closely with Washington and be more ready to take cases against China to the World Trade Organization. The comments came before EU heads of government were to meet on Thurs- day in Lisbon to discuss calls from Nicolas Sarkozy, the French president, and Angela Merkel, the German chancellor, for a more aggressive stance toward emerging Asian economies over trade. 3 “IMF set to scrutinize exchange rate policies,” Financial Times, 19 Junio 2007. 64 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Understanding the Sources of Friction in U.S.–China Trade Relations These recent developments in the United States and the EU should be seen as warn- ings that China, Europa, and the United States could be marching toward a trade war. The threat of a serious disruption in trade between China and the developed countries should be taken seriously. The turn against free trade is especially notable in the United States. The Pew Research Center (2007) reported in the 2007 report of the Pew Global Attitudes Survey that the proportion of U.S. residents who have a pos- itive view of trade was only 59 por ciento, the lowest satisfaction level in the sample of 47 countries. This was also a dramatic drop from the 78 percent reported in the 2003 informe (Pew Research Center 2003). Even more worrying for the future of the multi- lateral free trade system as constituted by the WTO is that this rise in discontent with trade is not limited to the United States, it is a global phenomenon. Mesa 1 displays the proportion of population in 38 countries who regarded trade in a positive light in 2003 y 2007. Twenty-seven countries reported a drop in support for free trade, two countries were unchanged in their view, and nine countries in- creased their support. If we take an absolute change of 5 percentage points or less to be indicative of an unchanged level of support for trade, entonces 13 countries turned signiªcantly against free trade, y 4 countries turned signiªcantly in favor of free trade. The most alarming sign of threat to the WTO system is that ªve of the G-7 countries are viewing trade in a signiªcantly more negative light than before; the decline in support was 24.4 percent in the United States, 13.9 percent in Italy, 11.4 percent in France, 10.5 percent in Britain, y 6.6 percent in Germany. None of the four countries (Bangladesh, Argentina, India, and Jordan) that became more ar- dent supporters of trade is a major trading power at present. Why have the largest stakeholders in the world economic system, especially the United States, become more disenchanted with the present WTO system? Our hy- pothesis is that many analysts have drawn the wrong conclusions on China’s ex- change rate policy and on economic globalization because they have not been sufªciently cognizant of the other major driver of the world economy, which is the accelerated pace of technological innovation. The two mutually interacting interna- tional trends of deep economic globalization and dynamic technological innovation have brought huge increases in prosperity to some segments in each national econ- omy but they have also caused painful structural adjustments in some other seg- ments of each national economy. Because of the latter, the world multilateral free trade system embodied by the WTO system is under threat. The proposed disruption in trade with China will unfortunately not solve the major complaints of the U.S.–EU coalition against China because it does not address the true causes that generated the trade tensions between these countries. En particular, the much-touted solution of an immediate downpayment of a 25 percent revalua- 65 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Understanding the Sources of Friction in U.S.–China Trade Relations Table 1. The rise in discontent with trade, 2003–07 Proportion of population with a positive view of trade (%) 2003 2007 78 87 95 79 88 82 95 87 95 67 86 88 91 84 86 90 86 98 79 83 83 93 96 73 78 88 89 72 82 90 88 90 77 78 84 60 69 52 59 71 81 68 78 73 85 78 86 61 79 82 85 80 82 86 83 95 77 81 81 91 94 72 77 87 88 72 82 91 89 93 80 82 90 68 89 72 Country United States Indonesia Uganda Italy France Turkey Nigeria Britain Mali Egypt Venezuela Russia Germany Czech Rep. Canada South Korea Slovakia Senegal Mexico Peru Lebanon Ukraine Ivory Coast Brazil Poland South Africa Bulgaria Japan Tanzania China Ghana Kenya Bolivia Pakistan Bangladesh Argentina India Jordan Increase in level (puntos de porcentaje) (cid:2)19 (cid:2)16 (cid:2)14 (cid:2)11 (cid:2)10 (cid:2)9 (cid:2)10 (cid:2)9 (cid:2)9 (cid:2)6 (cid:2)7 (cid:2)6 (cid:2)6 (cid:2)4 (cid:2)4 (cid:2)4 (cid:2)3 (cid:2)3 (cid:2)2 (cid:2)2 (cid:2)2 (cid:2)2 (cid:2)2 (cid:2)1 (cid:2)1 (cid:2)1 (cid:2)1 (cid:2) 0 (cid:2) 0 (cid:2) 1 (cid:2) 1 (cid:2) 3 (cid:2) 3 (cid:2) 4 (cid:2) 6 (cid:2) 8 (cid:2)20 (cid:2)20 Proportionate increase in level (por ciento) (cid:2)24.4 (cid:2)18.4 (cid:2)14.7 (cid:2)13.9 (cid:2)11.4 (cid:2)11.0 (cid:2)10.5 (cid:2)10.3 (cid:2)9.5 (cid:2)9.0 (cid:2)8.1 (cid:2)6.8 (cid:2)6.6 (cid:2)4.8 (cid:2)4.7 (cid:2)4.4 (cid:2)3.5 (cid:2)3.1 (cid:2)2.5 (cid:2)2.4 (cid:2)2.4 (cid:2)2.2 (cid:2)2.1 (cid:2)1.4 (cid:2)1.3 (cid:2)1.1 (cid:2)1.1 (cid:2) 0.0 (cid:2) 0.0 (cid:2) 1.1 (cid:2) 1.1 (cid:2) 3.3 (cid:2) 3.9 (cid:2) 5.1 (cid:2) 7.1 (cid:2)13.3 (cid:2)29.0 (cid:2)38.5 Fuente: Pew Research Center (2003, 2007). tion of the Chinese currency (Renminbi, RMB) against the U.S. dollar does not de- serve the central place it has occupied in the discussions of what is to be done about the large and growing trade imbalances with China. The optimum solution is a poli- cy package that uses a wider set of policy instruments (including RMB apprecia- ción); is multilateral in adjustment (Estados Unidos. and the EU also need to make policy changes); and is focused on a wider set of objectives and not just external balance alone. Cifra 1 shows that the earlier period of 1978–96 was typiªed by large boom–bust cycles in output growth and inºation, and that the post-2004 period has come to look increasingly like the earlier period, especially with the acceleration of inºation at the end of 2007. We will suggest in the last part of this paper that the appropriate 66 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Understanding the Sources of Friction in U.S.–China Trade Relations way to stabilize the Chinese economy in May 2008 is to rely more on exchange rate appreciation than on interest rate increases. 2. The triumph of hope over experience: Exchange rate appreciation as panacea In 2002, Haruhiko Kuroda and Masahiro Kawai (2002) accused China of exporting deºation because China had pegged the RMB to the US$ and was experiencing

deºation in the 1998–2002 period.4 They recommended that the RMB be appreciated

in order to end China’s negative impact on its neighbors. En 2003, Morris Goldstein

and Nicholas Lardy (2003) noted China’s persistent CA surplus and made the ªrst

of their many proposals for a substantial appreciation of the RMB. Goldstein and

Lardy called for an immediate 15 a 25 percent appreciation of the RMB against the

US$. On 21 Julio 2005, China allowed the RMB to appreciate 2.1 percent discretely and an- nounced that it was moving to a more ºexible exchange rate regime. This incremen- tal process of appreciation against the US$ has continued as the upward march of

China’s CA surplus has remained unabated. The end-of-year RMB–US$ exchange rate stood at 8.28 en 2004, 8.07 en 2005, 7.81 en 2006, y 7.30 en 2007. The pace of RMB appreciation has picked up substantially in 2008 to reach 6.98 RMB per US$ on

18 Puede 2008: an appreciation of 15.7 por ciento desde 21 Julio 2005.5

In our opinion, there is little doubt that a large appreciation of the RMB against the

dollar (decir 40 percent as suggested in Goldstein 2007) could eliminate the bilateral

U.S.–China trade deªcit, and perhaps even China’s global trade surplus as well, pero

this move would only hurt China and not “save” the world. The economic reason-

ing involved is straightforward. Ceteris paribus, in the aftermath of the 40 por ciento

RMB appreciation, foreign companies producing in China for the G-7 markets

would move their operations to other Asian economies (p.ej., Vietnam and India)

and export from there, and G-7 importers would start importing the same goods

from other Asian countries instead. In the absence of a collective appreciation of all

Asian currencies, the RMB appreciation would only reconªgure the geographical

distribution of the global imbalances and not eliminate them.

4 See Figure 1 for the course of Chinese inºation in the 1978–2007 period. En octubre 1997, en

response to the Asian ªnancial crisis, China pegged the RMB at 8.28 per US$. China main- tained this RMB–US$ exchange rate until 21 Julio 2005.

5 It would be politically naive not to notice that this faster rate of appreciation came only after

the conclusion of the 17th Congress of the Chinese Communist Party (CCP) in November

2007, which enabled the CCP leader, Hu Jintao, to consolidate his political power.

67

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Mesa 2. Impact of appreciation of Yen against US$ on current account balance of Japan and the United States (1985–88) Exchange rate (Yen/ US$)

Global current account balance (% de

PIB)

end of

período

251.10

200.50

159.10

123.50

125.85

143.45

período

promedio

Japón

(a)

237.52

238.54

168.52

144.64

128.15

137.96

3.76

4.24

3.52

2.74

(b)

3.74

4.24

3.43

2.66

1984

1985

1986

1987

1988

1989

United States

(a)

(b)

Bilateral Japan–U.S.

trade balance

(% of Japanese GDP)

(d)

(C)

(cid:2)2.10

(cid:2)2.58

(cid:2)2.69

(cid:2)1.70

(cid:2)2.95

(cid:2)3.30

(cid:2)3.39

(cid:2)2.38

2.97

2.60

2.16

1.61

3.64

2.90

2.43

1.86

Fuente: IMF, International Financial Statistics and Direction of Trade Statistics.

Nota: The Global Current Account Balance is constructed two ways:

Measure (a) is constructed as: 100*(series 90c.c (cid:2) series: 98c.c (cid:2) series 98.nc)/series 99b.c).

Measure (b) is constructed as: (100*series 78ald * series rf)/(series 99b.c).

The bilateral trade balance in (C) is calculated as export (cid:2) import (cif), using Japanese data.

The bilateral trade balance in (d) is calculated as expot (cid:2) import, using U.S. datos.

This economic reasoning is supported by the Yen-bashing experience of the 1980s,

when a number of prominent economists pushed for a large Yen appreciation

against the US$ to reduce the trade imbalances in both countries. El 1981 Reagan tax cuts had caused the U.S. global CA deªcit to soar, and the resulting concern about U.S. unemployment prompted the U.S. Treasury to pressure the other major economies to appreciate their currencies to reduce the U.S. trade account deªcit. On 22 Septiembre 1985, Francia, Japón, the United Kingdom, the United States, and West Germany (G-5) signed the Plaza Accord to engineer a collective appreciation against the US$. The outcome was a spectacular appreciation of the Yen against the US$ in 1985–88. The end-of-year Yen–US$ exchange rate fell from 251 en 1984 a 201 en 1985,

and then to 159 en 1986 (ver tabla 2).

This fast, large appreciation of the G-5 currencies against the US$ was, sin embargo, quickly considered to be excessive and destabilizing to global ªnancial markets. The upshot was that the G-5 and Canada signed the Louvre Accord on 22 Febrero 1987 to halt the slide of the dollar. The Yen, nevertheless, continued to appreciate against the US$ to reach 123 Yen/US$ at the end of 1987; and it was only in the last part of 1988 that the Yen reversed direction and started depreciating again the US$ to reach

126 Yen/US$ at the end of 1988 y 143 Yen/US$ at the end of 1989 (ver tabla 2).

The outcome of this gyration of the Yen was that the average Yen–US$ exchange rate was 239 en 1985, 169 en 1986, 145 en 1987, 128 en 1988, y 138 en 1989. When the average Yen–US$ exchange rate fell during the 1985–88 period, Japan’s

global CA surplus declined from 3.76 percent of GDP to 2.74 por ciento, a drop of

68

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

1.02 puntos de porcentaje (ver tabla 2). Estados Unidos. global CA deªcit, por otro lado,

showed little change, going from 2.1 percentage of GDP to 1.7 por ciento, a drop of

0.4 percentage points.6 In short, the sizable appreciation of the Yen against the US$ had substantial impact on the Japanese global trade imbalance but almost no impact on the U.S. global trade imbalance. The huge appreciation of the Yen–US$ exchange rate did cause a sizable decrease in

the bilateral U.S.–Japan trade imbalance. The bilateral Japan–U.S. trade surplus de-

clined from 2.97 percent of Japan’s GDP in 1985 a 1.61 por ciento en 1988, a reduction

de 1.36 percentage points.7 The drop in the bilateral Japan–U.S. trade surplus was

even greater than Japan’s global trade surplus, revealing that the Plaza Accord

caused Japan to start running a larger bilateral trade surplus against some other

countries.

The mechanism that caused Japan’s bilateral trade surplus with non-U.S. countries

to increase under the Plaza Accord was the same mechanism responsible for the

small improvement in the U.S. global CA deªcit. With the gigantic appreciation of

the Yen against the US$, Japanese companies started investing in production facili- ties in Southeast Asia and other developing countries, and started exporting to the United States from there. Japan’s bilateral trade surplus with non-U.S. countries in- creased because of increased Japanese export of capital equipment to Japanese- afªliated companies in these countries. A NOSOTROS. global CA surplus hardly changed be- cause while the United States imported less from Japan, it imported more other countries. En breve, the present expectation of many analysts that an enormous RMB apprecia- tion would reduce the U.S. global CA deªcit represents the triumph of hope over ex- experiencia. The recent calls for a new Plaza Accord8 to reduce the U.S. trade account deªcit are thus similarly wrong-headed unless this new accord would include the entire world (and this unprecedented feat in global cooperation is simply not realis- tic). 6 These estimates are those of column (a) en mesa 2. When the global CA balances of these two countries are calculated another way, the respective declines are 1.08 y 0.57 puntos de porcentaje (see column (b) en mesa 2). 7 This statement is based on column (C), which used trade data from Japan’s page in the Direc- tion of Trade Statistics. When the trade data from the U.S. page were used, the bilateral imbal- ance fell from 3.64 percent of Japan’s GDP in 1985 a 1.86 por ciento en 1988: a drop of 1.78 por- centage points. 8 Por ejemplo, see Cline (2005). 69 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China 3. What is the correct level for the exchange rate? The Economist magazine constructs a PPP9 exchange rate based on the prices of Big Mac sandwiches sold in different countries. En 2006, it cost RMB 10.4 to buy a Big Mac in China and US$ 3.15 in the United States, and so the PPP exchange rate was

RMB 3.3 per US$ in 2006 compared to the actual (nominal) exchange rate of ex- change rate of RMB 8 per US$. So is it meaningful to say that the Chinese exchange

rate was under-valued by almost 60 por ciento en 2006? The answer is no because the

prices of the sandwiches included non-tradable inputs, and the prices of non-

tradables were lower in China than in the United States. En general, the prices of

non-tradables are lower in developing countries than in the developed countries be-

cause labor costs are lower in the former. With economic development, the prices of

non-tradables in the developing country will rise to bring the price ratio of non-

tradables to tradables closer to the price ratio in the developed country.

To see that the gap between the usual PPP exchange rate and the actual exchange

rate reºects the development gap between the two countries, we ªrst make the fol-

lowing deªnitions:

(a) Deªne the consumer price index in China and United States

(cid:4) a PC

CPI of China, CPIC (cid:3) (1 (cid:2) a) PC

CPI of United States, CPIU (cid:3) (1 (cid:2) a) PU

t

norte,

(cid:4) a PU

t

norte,

where CPI (cid:3) consumer price index,

C (cid:3) Porcelana,

Ud. (cid:3) United States,

(cid:3) price of tradable good in country i,

Pi

(cid:3) price of non-tradable good in country i,

Pi

a (cid:3) weight of non-tradable goods in price index.

norte

t

(b) Deªning the PPP exchange rate

ePPP (cid:3) CPIC / CPIU.

We next state the equilibrium conditions.

9 PPP (cid:3) purchasing power parity.

70

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

(1) Goods arbitrage:

PC

t

(cid:3) eactual PU

t,

where eactual (cid:3) actual (nominal) exchange rate expressed as number of RMB per US$. (2) Relationship between prices of tradables and non-tradables within each country: for developing China, for developed United States, PC N PU N (cid:3) d PC T, (cid:3) f PU T. (3) The difference between developed and developing country is that relative price of non-tradables is higher in the former: F (cid:5) d (cid:5) 0. We can now derive the following relationship between the PPP exchange rate and the actual exchange rate: ePPP (cid:3) CPIC / CPIU, ePPP (cid:3) [(1(cid:2)a(cid:4)anuncio)/(1(cid:2)a(cid:4)af)] eactual, ePPP (cid:6) eactual. This exercise above shows that it is conceptually difªcult to determine the “correct- ness” of a country’s exchange rate based on PPP exchange rates. The actual ex- change rate of a developing country would always be “undervalued” in relation to the PPP exchange rate, and it would be unsustainable for the developing country to set its exchange rate equal to the PPP exchange rate. There is only one meaningful deªnition of the “correct exchange rate” and it is the “market-clearing exchange rate,” which is the exchange rate that is generated by the foreign exchange markets in the absence of interventions by any central bank. The fact that the PBC has been accumulating foreign reserves every period means that the RMB is under-valued according to this “market-clearing” deªnition. Sin embargo, what would happen if China were to go further in its marketization of foreign ex- change transactions by removing its capital controls? Diversiªcation of asset port- folios by private Chinese agents would surely result in a great outºow of funds, possibly causing the RMB to depreciate instead. In such a case, the present exchange 71 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Understanding the Sources of Friction in U.S.–China Trade Relations rate of RMB 6.9 per US$ would be “over-valued” compared to the “complete free

market exchange rate.” Of course, no one knows whether the “complete free market

exchange rate” would be higher or lower than RMB 6.9 per US$. Primero, suppose the value of the “complete free market exchange rate” is RMB 6.0 per US$, and the “market-clearing exchange rate with controls on capital outºows” is

RMB 4.5 per US$, y, segundo, assume that the government stops intervention immediately and then removes capital controls a few years later after it has strengthened the supervision, management, and technical capability of the domestic ªnancial institutions. One plausible result of this particular two-step market liberal- ización (which we call Option A) would be RMB appreciation to RMB 4.5 per US$

upon cessation of foreign market intervention followed by RMB depreciation to

RMB 6.0 per US$ upon removal of the capital controls. Option A produced an over- shooting of the RMB. Suppose China adopts another form of two-step liberalization (Option B), incremen- tal appreciation of the RMB and then removal of the capital controls after a few years. Option B is better than Option A because the exchange rate overshooting in Option A creates an unnecessary to-and-fro movement in resources. As mentioned, the removal of capital controls could very well cause the RMB to depreciate past RMB 6.9 per US$, decir, to RMB 7.5 per US$, meaning that Option A would result in very severe exchange rate overshooting compared to Option B. In effect, the Chinese government has been implementing a form of Option B since July 2005. In our opinion, sin embargo, the Chinese government has chosen a speed of exchange rate adjustment that is too slow, causing the RMB to depreciate signiªcant- ly against the euro. We recommend that the Chinese government increase the speed of the RMB appreciation—but not in the form of an immediate discrete 10–15 per- cent appreciation as advocated by Goldstein (2007). The instinctive calls by some economists for the use of the exchange rate mechanism to solve China’s external imbalance is only partially correct. Given China’s capital controls, a freely ºoating currency regime could mean a value for the RMB that would be greatly over-appreciated compared to what its value would be under free capital ºows; an outcome that could reduce economic growth signiªcantly.10 Freeing capital ºows is not, sin embargo, an option at this time. Given the weakness of the bal- 10 In Robert Mundell’s opinion: “China’s growth rate could fall by half and foreign direct in- vestment (FDI) could slow to a crawl if the country were to abandon its long-standing sup- port of pegging the currency.” Quoted in “Abandoning Peg Will Slash Growth 50 pc in China,” South China Morning Post, 15 Septiembre 2003. 72 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 7 3 6 1 1 6 8 2 4 9 5 a s e p 2 0 0 8 7 3 6 1 pd . . . . . f por invitado 0 8 septiembre 2 0 2 3 Understanding the Sources of Friction in U.S.–China Trade Relations ance sheets of China’s state-owned banks, the considerable embezzlement of state assets that has occurred, and the experience with the Asian ªnancial crisis, we ad- vise against allowing the free movement of capital in the short term. The correct way to think about exchange rate management is to analyze the issue within the context of overall macroeconomic management and not just about its im- pact on the balance of payment. There are usually combinations of macroeconomic policies that would produce results superior to the one generated by appreciating the RMB alone. The general point is that because the balance of payments is only one of the main outcomes of concern11 and because the exchange rate is only one of the ways12 to affect the balance of payments, it is seldom optimal to concentrate ex- clusively on one policy target (which does not dominate the other policy targets in importance) and then to employ only one particular policy tool (which is chosen id- iosyncratically) to achieve that one policy target. En breve, the much-touted solution of an immediate down payment of a 25 percent revaluation of the RMB against the US$ does not deserve the central place it has occupied in the discussions of what is

to be done about the large trade imbalances with China.

4. Understanding the rise in worker anxiety in the United States

Allegations that the bilateral U.S.–China trade deªcit represents the export of unem-

ployment from China to the United States are common. A recent study by Robert

Scott (2007) of the Economic Policy Institute used an input–output model to arrive

at the claim that the bilateral trade deªcit of US$ 49.5 billion in 1997 caused the loss of 597,300 jobs that year and the 2006 bilateral trade deªcit of US$ 235.4 billion

caused the loss of 2,763,400 jobs, and that every state had suffered a net loss in job

from the rise in the bilateral trade deªcit between 1997 y 2006. The alleged job

loss in 2006 from the bilateral trade deªcit implied that the unemployment rate that

same year was 1.21 percentage points higher than if the bilateral trade balance were

zero.13

With these alleged job losses, another alleged outcome from U.S.–China trade that is

common is that the bilateral deªcit has forced down U.S. wages.14 As it is well docu-

11 The inºation rate and the unemployment rate would be among the other key concerns.

12 Other ways include taxes, subsidies, and interest rates.

13 Estados Unidos. civilian labor force in 2006 era 151.4 millón; Table B-35 in Executive Ofªce, Coun-

cil of Advisors (2007).

14 Estrictamente hablando, import competition could lower U.S. wages permanently without increas-

ing the unemployment rate permanently. The structural adjustment required to accommo-

date the increased imports would cause a temporary increase in the unemployment rate.

73

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Mesa 3. The distribution of the global labor force (millions)

The non-SIC countries

The SIC countries

Global

Total

2,315

2,672

1990

2000

Non-SIC

Total

Developed

Economies

Developing

Economies

1,083

1,289

403

438

680

851

SIC

Total

1,232

1,383

Porcelana

India

687

764

332

405

Soviet

bloc

213

214

Fuente: Hombre libre (2004).

Nota: SIC countries (cid:3) former Soviet bloc, India and China. Our ªgure for “total” in 2000 is different from that in Freeman because his

“total” does not equal the sum of the components.

mented that worker anxiety15 in the United States has increased steadily in the last

two decades just as U.S.–China trade has increased steadily, it is tempting indeed to

blame the rise in worker anxiety in the United States on the rise of China as a major

trading nation.

De hecho, the integration of China into the international division of labor was only

part of the broader process of economic globalization that accelerated in the last dec-

ade of the 20th century. The labor force of the former Soviet Union and India joined

the international division of labor on a mass scale at about the same time that China

did.16 Table 3 shows that the number of workers already engaged in the interna-

tional division of labor was 1.08 billion in 1990, and the combined labor force of the

former Soviet bloc, India, and China (SIC) era 1.23 billion. The division of labor in

1990 was certainly an unnatural one because half of the world’s workforce had been

voluntarily kept out of it by the SIC’s autarkic policies. A decade after the start of

the internationalization, the number of workers involved in the international eco-

nomic system had increased to 2.672 billion in 2000 (con 1.363 billion workers from

SIC). The straightforward implication of the Heckscher–Ohlin model is that this

15 See Otoo (1997) and Valletta (2007).

16 The economic isolation of the Soviet bloc started crumbling when the new non-communist

Solidarity government of Poland began the marketization and internationalization of the

Polish economy on 1 Enero 1990. The economic transition and political disintegration of

the Soviet bloc became irreversible when Yeltsin replaced Gorbachev as the unambiguous

leader of Russia in August 1991 and implemented market-oriented reforms in January 1992.

For the Chinese elite, the events in the Soviet Union conªrmed that there did not exist a

third way in the capitalism vs. socialism debate. In early 1992, Deng Xiaoping led a success-

ful campaign to put China ªrmly on the path of convergence to a private market economy.

En 1991, India faced a balance of payments crisis, and it responded by going well beyond the

administration of the standard corrective macroeconomic medicine of ªscal-monetary tight-

ening and exchange rate devaluation into comprehensive adjustments of microeconomic in-

centives. India’s trade regime was deregulated signiªcantly, the restrictions on foreign in-

vestment were relaxed, reform of the banking sector and the capital markets was initiated,

and divestment of public enterprises and tax reform were announced.

74

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

doubling of the world labor, achieved by bringing in cheaper labor from SIC, would

lower the relative price of labor-intensive goods and hence reduce the income of la-

bor in the industrialized country.17 The fact that U.S. capital could now move abroad

to set up production facilities in the SIC economies to service the U.S. market and

foreign markets meant another channel (besides the cross-border movement of

goods) for globalization to depress the U.S. labor income.18

There is no denying that the Heckscher–Ohlin model provides a coherent mecha-

nism for globalization to lower U.S. labor income, and to cause U.S. unemployment

to rise during the process. The fact that the U.S. global trade deªcit widened steadily

de 1.5 percent of GDP in 1991 a 2.5 por ciento en 1996, 4.4 por ciento en 2001, y 6.7

por ciento en 2006 could only have worsened the drop in labor income and the rise in

the unemployment rate because U.S. exports are less labor-intensive than U.S. im-

ports.

The inconvenient truth, sin embargo, is that these two expectations based on the

Heckscher–Ohlin model have turned out to be wrong. The alleged rise in U.S. y-

employment is not seen when we use the 1998–2006 period chosen by Robert Scott

(2007) as the reference point. The average unemployment rate of 4.9 percent in the

1998–2006 period was actually lower than the average unemployment rates in the

immediate previous periods of 1980–88 and 1989–97, which were 7.5 percent and

6.0 por ciento, respectivamente. En realidad, Estados Unidos. economy has been a highly successful

job-creation machine in the 1997–2006 period.

Many analysts have pointed out that the inºation-adjusted weekly earnings (wages

and salaries) of non-supervisory employees in 1980 are higher than in every year in

the 1982–2006 period.19 So is the backlash against globalization in the G-7 countries

the result of the immiseration of their low-skilled workers? The answer is no, ser-

cause earnings is only one of the two components of compensation received by

workers, the other component is employer-paid beneªts (p.ej., pension contributions,

health insurance). The neglect of beneªts gives the wrong picture on income re-

ceived by labor because the growth of beneªts has been especially rapid in the last

decade due to the soaring costs of health insurance. When we measure labor income

as the sum of earnings (wages and salaries) and beneªts, then we ªnd that labor in-

17 More accurately, the wage of the formerly isolated SIC worker would rise while the wage

for the worker in the industrialized country would fall.

18 Por eso, the imposition of a high U.S. tariff would not only drastically curb imports from SIC

but also radically reduce this type of FDI ºow from the United States to SIC.

19 Por ejemplo, ver figura 1 in Polaski (2007).

75

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

come in 1980 is lower than in every year in the 1982–2006 period, refuting the con-

clusion drawn from looking only at the earnings component of labor income.

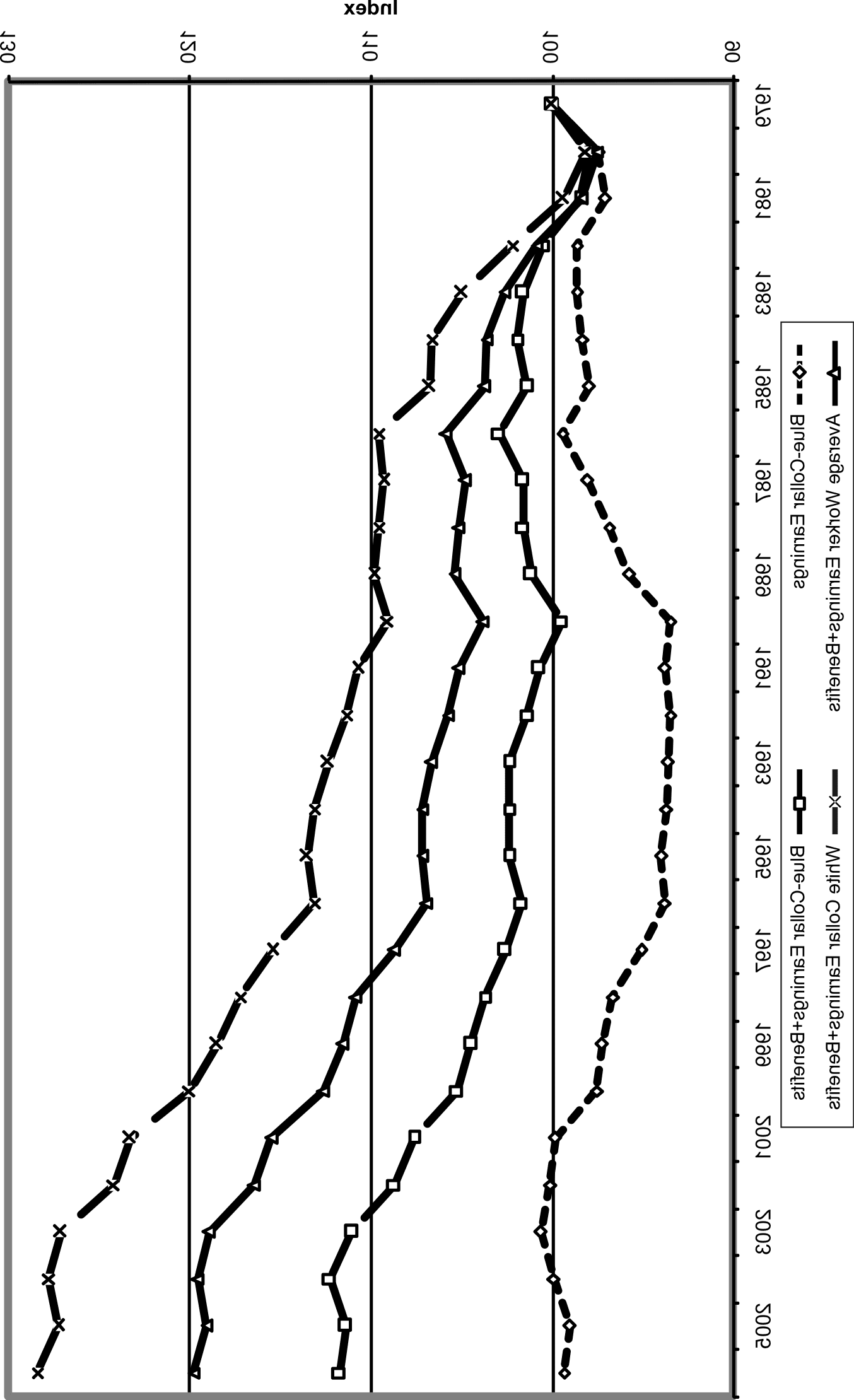

Cifra 2 reports the evolution of four data series over 1979–2006, each indexed at

100 in December 1979:20

• Series (a) is the inºation-adjusted earnings received by a blue-collar worker in De-

cember of each year.

• Series (b) is the inºation-adjusted compensation (es decir., earnings plus beneªts) re-

ceived by a blue-collar worker in December of each year.

• Series (C) is the inºation-adjusted compensation received by an average worker in

December of each year.

• Series (d) is the inºation-adjusted compensation received by a white-collar (ex-

cluding sales occupations) worker in December of each year.

Serie (a) shows that the earnings of the blue-collar worker in 2006 eran 1 por ciento

lower than in 1979. Serie (b) shows that the compensation (earnings plus beneªts)

of the blue-collar worker in 2006 era 12 percent higher than in 1979. De hecho, azul-

collar compensation had been higher than in 1979 desde 1991. Además, azul-

collar compensation started growing faster beginning in 1997, just as the U.S. global

trade deªcit began to grow faster. Serie (d) shows that the compensation of the

white-collar worker in 2006 era 28 percent higher than in 1979. This much higher

income growth of the white-collar worker caused the compensation of the average

worker, series (C), en 2006 ser 20 percent higher than in 1979. The important

message from Figure 2 is that the income growth of the United States in the 1990–

2006 period of accelerated globalization was shared by both low-skilled workers

and high-skilled workers, albeit the latter received a larger share of the income

growth.

The possible key to reconciling the theoretical predictions of the Heckscher–Ohlin

model with the actual outcomes is to recognize that economic globalization was not

the only signiªcant economic process in the last two decades. The other signiªcant

economic process was accelerated technological innovation, especially in the ad-

vanced economies, notably the United States. The reason why the U.S. real labor in-

come has not fallen despite economic globalization is that there has been remark-

ably high U.S. productivity growth since the late 1980s, perhaps enabled in large

20 Each data series is produced by combing the relevant SIC-based series of the 1979–2005 pe-

riod with the relevant NAICS-based datum for 2006. SIC (cid:3) Standard Industrial Classiªca-

ción; and NAICS (cid:3) North America Industrial Classiªcation System. Data are from Bureau

of Labor Statistics (2007a, 2007b).

76

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

)

0

0

1

9

7

9

1

(

s

r

mi

k

r

oh

w

.

.

S

Ud.

y

b

d

mi

v

i

mi

C

mi

r

norte

oh

i

t

a

s

norte

mi

pag

metro

oh

C

.

2

mi

r

tu

gramo

i

F

77

Asian Economic Papers

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

part by the ICT21 revolution. It is instructive here to note that Alan Greenspan has

attributed his (generally hailed) superior ability in making the “correct” policy to his

early recognition that the U.S. entered into a period of rapid technological innova-

tion in the late 1980s.

We note that while this high productivity growth was able to offset the downward

pressures on the real labor income from economic globalization, it was also likely to

have joined economic globalization in diminishing the labor share of GDP.22 Recent

technological innovations have more than substituted capital for labor (p.ej., fewer

secretaries are needed because answering machines can now convert messages into

voice ªles that can be emailed to traveling professionals). They have also trans-

formed many of what have been traditionally non-tradable services into tradable

services, allowing jobs to be outsourced to foreign service providers. Por ejemplo,

the ICT revolution has allowed offshore call centers to handle questions from

A NOSOTROS. customers, offshore accountants to process U.S.-based transactions, and off-

shore medical technicians to read the X-rays of U.S. patients.23

What is fueling the resentment toward imports from China when the average

A NOSOTROS. worker is experiencing neither more unemployment nor lower compensation?

The explanation is that the U.S. worker is feeling more insecure in the 2000s than in

the 1980s because of the faster turnover in employment. Globalization and techno-

logical innovation have required the worker to change jobs more often and she ªnds

that there are considerable costs associated with the job change because of the inade-

quacies of U.S. social safety nets.

The more frequent change in jobs is documented in Table 4 by the declining trend in

the length of the median job tenure for older male workers. The median job tenure

for males has changed as shown:

21 ICT (cid:3) information and communications technology.

22 Besides capital-bias technological innovation and economic globalization, there have been

two other developments in the U.S. economy that have likely contributed to the decline in

labor share of GDP. The ªrst is changes in the institutional nature of the U.S. labor market;

union membership has declined and there has been an upward shift in the compensation

norms for high-level executives. (This shift in compensation norms could reºect a combina-

tion of a shift in social attitudinal norms, and more collusion between managers and their

boards. Akerlof (2007) is a recent discussion on “norms” and their economic consequences.)

The second of these other developments is increased immigration into the United States (ser-

delantero 2001); see Borjas (1994) and Ottaviano and Peri (2005).

23 There is a large empirical literature on the relative impact of technological changes and

globalization on the U.S. wage rate, notable contributions include Sachs and Shatz (1994)

and Feenstra and Hanson (1996, 1998).

78

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Mesa 4. Median years of tenure with current employer for employed wage and salary male

workers by ages, elected years, 1983–2004

Age and sex

16 years and over

16 a 17 años

18 a 19 años

20 a 24 años

25 years and over

25 a 34 años

35 a 44 años

45 a 54 años

55 a 64 años

65 years and over

Enero

1983

Enero

1987

Enero

1991

Febrero

1996

Febrero

1998

Febrero

2000

Enero

2002

Enero

2004

Enero

2006

4.1

0.7

0.8

1.5

5.9

3.2

7.3

12.8

15.3

8.3

4.0

0.6

0.7

1.3

5.7

3.1

7.0

11.8

14.5

8.3

4.1

0.7

0.8

1.4

5.4

3.1

6.5

11.2

13.4

7.0

4.0

0.6

0.7

1.2

5.3

3.0

6.1

10.1

10.5

8.3

3.8

0.6

0.7

1.2

4.9

2.8

5.5

9.4

11.2

7.1

3.8

0.6

0.7

1.2

4.9

2.7

5.3

9.5

10.2

9.0

3.9

0.8

0.8

1.4

4.9

2.8

5.0

9.1

10.2

8.1

4.1

0.7

0.8

1.3

5.1

3.0

5.2

9.6

9.8

8.2

4.1

0.7

0.7

1.4

5.0

2.9

5.1

8.1

9.5

8.3

Fuente: This is Figure 10 in Burtless (2005) updated with 2006 and expanded with addition of (25–34) age group.

• 35 a 44 age group, decreased from 7.0 years in 1987 a 5.1 years in 2006;

• 45 a 54 age group, decreased from 11.8 years in 1987 a 8.1 years in 2006; y

• 55 a 64 age group, decreased from 14.5 years in 1987 a 9.5 years in 2006.

In terms of social safety nets, Gary Burtless (2005) reports that within the G-7 in

2004, only the United Kingdom has a less generous unemployment beneªts scheme

than the United States. Mesa 5 shows that an unemployed person in the United

States received initial unemployment beneªts that equaled 53 percent of previous

income compared to 78 percent in Germany, 76 percent in Canada and France,

61 percent in Japan, 60 percent in Italy, y 46 percent in the UK. Mesa 5 also docu-

ments that the duration of unemployment beneªts was 6 months in the United

States compared to 12 months in Germany, 9 months in Canada, 30 months in

Francia, 10 months in Japan, y 6 months in Italy and the UK.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

The dilemma is that the fast rate of technological innovation has been good for labor

income but bad for job stability because technological improvements in the produc-

tion process usually mean occupational obsolescence. The unfortunate fact is that

the temporary unemployment associated with job changes are especially painful in

the United States compared with most of the advanced countries because of the less

generous social safety nets and because health coverage is usually supplied by the

employer.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

En breve, the popular outcry in the United States and the EU against China’s trade

surpluses is misplaced. Even if China’s trade balance were zero, the pains of struc-

tural adjustment and income redistribution caused by technological innovations, en-

stitutional changes, globalization, and immigration would still be there. The fact

that the blue-collar worker did receive a higher level of compensation suggests that

79

Asian Economic Papers

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

Mesa 5. Unemployment beneªts in 20 OECD countries in 2004

Percent of net earnings initially replaced by

after-tax value of unemployment beneªts

Duration of unemployment beneªts

(meses)

Suecia

Finland

Suiza

Alemania

Países Bajos

Portugal

Canada

Dinamarca

Francia

España

Austria

Norway

New Zealand

Australia

Bélgica

Japón

Italia

Irlanda

EE.UU

Reino Unido

83

82

82

78

78

77

76

76

76

75

73

73

67

66

61

61

60

55

53

46

14

23

24

12

18

24

9

41

30

24

9

36

a

a

b

10

6

15

6

6

Fuente: Burtless (2005).

Notas: a. Australia and New Zealand offer only means-tested beneªts. If the eligibility test continues to be met, unemployment beneªts

can last indeªnitely.

b. Belgium essentially provides unemployment beneªts of indeªnite duration.

the additional pain from the incremental structural adjustment caused by the wid-

ening trade deªcit is minor by comparison. It is our hypothesis that the enhanced

worker anxiety in the developed countries has been created not by a lower real

wage and a higher unemployment rate but by job insecurity resulting from (1) occu-

pational obsolescence because of rapid technological innovation, y (2) import

competition from economic globalization. The job insecurity in the United States is

exacerbated by inadequate social safety nets and by the inappropriate design of the

funding of medical insurance.

5. Understanding the evolution of China’s current account balance

Desde 1986, except for the four years (1990, 1991, 1997, y 1998) associated with an

economic downturn in China, the bilateral surplus with the United States has ex-

ceeded China’s global trade surplus, meaning that China is running massive deªcits

in its trade with some of its other trade partners. The changing conªguration of

China’s bilateral trade balances since 1986 reºects mainly the steady expansion of

production networks into China. In this new geographical division of the produc-

tion of components and of the production stages in manufacturing, China usually

makes the cheaper components and assembles the ªnal products by combining the

80

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

domestically produced components with imported components. The fast transfer of

manufacturing and assembly operations from Japan, Taiwán, and South Korea to

China translates directly into high growth in the China–U.S. bilateral trade surplus

because this transfer reduces the bilateral Japan–U.S. trade surplus, the bilateral

Taiwan–U.S. trade surplus, and the bilateral South Korean–U.S. trade surplus, corre-

spondingly. En breve, the China–U.S. trade deªcit could be reduced by transferring

the assembly operations of Korean, Taiwanese, Japanese, and European production

networks to Vietnam, but the Vietnam–U.S. trade deªcit would then increase, leav-

ing the global U.S. trade balance unchanged.

Al mismo tiempo, sin embargo, China’s chronic and growing global trade surplus does

reveal a deep-seated serious problem in China’s economy: its dysfunctional

ªnancial system. This problem is revealed by the aggregate-level accounting iden-

tity that the global CA balance is determined by the ªscal position of the govern-

mento, and the savings-investment decisions of the state-controlled enterprise (SCE)

sector and the private sector.24 Speciªcally:

California (cid:3) (t (cid:2) GRAMO) (cid:4) (SSCE

(cid:2) ISCE) (cid:4) (Sprivate

(cid:2) Iprivate),

where CA (cid:3) current account in the balance of payments.

California (cid:3) (X (cid:2) METRO) (cid:4) R,

X (cid:3) export of goods and non-factor services,

METRO (cid:3) import of goods and non-factor services,

R (cid:3) net factor earnings from abroad (es decir., export of factor services),

t (cid:3) state revenue,

GRAMO (cid:3) state expenditure (including state investment),

SSCE

ISCE

Sprivate

Iprivate

(cid:3) saving of the private sector,

(cid:3) investment of the private sector.

(cid:3) saving of the SCEs,

(cid:3) investment of the SCEs,

For the last decade, the Chinese ªscal position (t (cid:2) GRAMO) has been a small deªcit, y

so it is not the cause for the swelling CA surpluses in the 2000s. The CA surplus ex-

ists because the sum of savings by SCEs and the private sector exceeds the sum of

their investment expenditures; and it has expanded steadily because the non-

24 The SCE category covers companies that are classiªed as SOEs (state-owned enterprises);

and joint-ventures and joint-stock companies, which are controlled by third parties (p.ej., le-

gal persons) who are answerable to the state. For an analysis of how the principal–agent

problem in SOEs has shaped China’s macroeconomic performance, see Woo (2006).

81

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

government savings rate has been rising faster than the growth of non-government

investment.25

Why has China’s ªnancial system failed to translate the savings into investments?

Such an outcome was not always the case. Before 1994, the voracious absorption of

bank loans by SCEs to invest recklessly kept the CA usually negative and the cre-

ation of nonperforming loans (NPLs) alto. When the government implemented

stricter controls on the state-owned banks (SOBs) de 1994 onward (p.ej., eliminando

top bank ofªcials whenever their bank lent more than its credit quota or allowed the

NPL ratio to increase too rapidly), the SOBs slowed down the growth of loans to

SCEs. This cutback created an excess of savings because the SOB-dominated ªnan-

cial sector did not then re-channel the released savings (which were also increasing)

to ªnance the investment of the private sector.

This failure in ªnancial intermediation by the SOBs is quite understandable. Primero,

the legal status of private enterprises was, hasta hace poco, lower than that of the state

enterprises; y, segundo, there was no reliable way to assess the balance sheets of

the private enterprises, which were naturally eager to escape taxation. The upshot

was that the residual excess savings leaked abroad in the form of the CA surplus. En-

adequate ªnancial intermediation has made developing China a capital exporting

country!

This perverse CA outcome is not new. Before the mid 1980s, Taiwan experienced

this same problem when all Taiwanese banks were state-owned and were operated

under a civil service regulation that required each loan ofªcer to repay any bad loan

that she approved. The result was a massive failure in ªnancial intermediation that

caused Taiwan’s CA surplus to be 21 percent of GDP in 1986. The reason why China

has not been producing the gargantuan CA surpluses seen in Taiwan in the mid

1980s is the still large amount of SCE investments.

Why is the savings rate of the non-government sector rising? The combined savings

of the SCE and private sectors rose from 20 por ciento en 1978 a 30 por ciento en 1987,

and has remained above 45 por ciento desde 2004. In discussions on the rise of the sav-

ings rate, a common view is that the rise reºects the uncertainty about the future

that many SOE workers feel in the face of widespread privatization of loss-making

SOEs. We ªnd this explanation incomplete because it seems that there has also been

25 See Wiemer (2008) for a recent quantiªcation of the increase in the savings rate of the differ-

ent groups.

82

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

7

3

6

1

1

6

8

2

4

9

5

a

s

mi

pag

2

0

0

8

7

3

6

1

pag

d

.

.

.

.

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Comprender las fuentes de fricción en las relaciones comerciales entre Estados Unidos y China

a rise in the rural saving rate even though rural residents have little to fear about the

loss of jobs in the state-enterprise sector because none of them are employed there.26

We see two general changes that have caused both urban and rural saving rates to

rise signiªcantly in China. The ªrst change relates to increased worries about the fu-

ture by the Chinese. The steady decline in state subsidies to medical care, housing,

loss-making enterprises, and education, and mismanagement of pension funds by

the state have led people to save more to insure against future bad luck (p.ej., sick-

ness, job loss), buy their own lodging, build up nest eggs for retirement, and invest

in their children.

The second change is the secular improvement in the ofªcial Chinese attitude to-

ward market capitalism. Given the high rate of return to capital, this increasingly

business-friendly attitude in the Communist Party of China has no doubt encour-

aged both rural and urban residents to save for investment, eso es, greater optimism

about the future has spawned investment-motivated saving.

In our explanations for the existence of the CA surpluses and the growth of the sur-

plus, there is a common element in both: China’s ªnancial system. The point is that

savings behavior is not independent of the sophistication of the ªnancial system. Un

advanced ªnancial system will have a variety of ªnancial institutions that would en-

able pooling of risks by providing medical insurance, pension insurance, and unem-

ployment insurance; and transform savings into education loans, housing loans, y

other types of investment loans to the private sector. Ceteris paribus, the more so-

phisticated a ªnancial system, the lower the savings rate.

Liu and Woo (1994) and Woo and Liu (1995) tested the proposition that ªnancial

market sophistication inºuences the private savings rate by adding a ªnancial so-

phistication (FS) variable to the well-known private savings rate equation of

Modigliani (1966, 1970) to arrive at the following econometric speciªcation:

PSR (cid:3) F(PROD, AGER, DEPR, RETS, R, FS),

dónde

PSR (cid:3) private savings rate,

PROD (cid:3) productivity growth,

AGER (cid:3) ratio of aged population to working population,

DEPR (cid:3) ratio of young population to working population,

26 The Economist Intelligence Unit (2004, páginas. 23) reported that “farmers’ propensity to save

seems to have increased.”

83

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro