Saurabh Lall, Lily Bowles, y ross baird

Bridging the “Pioneer Gap”

The Role of Accelerators in Launching

High-Impact Enterprises

Despite our current age of unprecedented global wealth, billions of people world-

wide still live in poverty. Over the past decade, sin embargo, gobiernos, the non-

profit sector, and the business world have explored the ability of small and grow-

ing businesses (SGBs) to reduce poverty, particularly in emerging markets. El

promise of finding market-based solutions to social problems has generated a good

deal of excitement about impact investing—an investment strategy that seeks

social/environmental returns in addition to financial returns. According to a 2013

study by J. PAG. Morgan and the Global Impact Investing Network (GIIN), a total of

$17 billion is expected to be deployed into socially beneficial sectors in 2012-2013.1 Sin embargo, this capital is not yet reaching many of the innovative small and growing businesses that can help to alleviate poverty through the jobs they create and the products and services they provide. While social enterprises continue to emerge— Village Capital alone has seen over 5,000 applications from impact-focused entre- preneurs worldwide over the last three years—many innovative companies in their early stages have had difficulty getting off the ground. They are still not able to access and take advantage this new flow of capital, or the other types of support and resources they need to succeed. A 2012 report from Monitor-Deloitte and the Acumen Fund highlights this paradox: The Pioneer Gap: While there are thousands of early-stage innovators seeking to launch companies that can drive social change worldwide, very few are able to build the teams, find the customer base, or raise the investment necessary to scale.2 The so-called pioneer gap specifically refers to the burden shouldered by enterprises that are pioneering new business models for social change. Monitor and Acumen identify four stages that these firms typically go through, from the Saurabh Lall is Research Director of the Aspen Network of Development Entrepreneurs. Lily Bowles is Global Operations Manager of Village Capital. Ross Baird is Executive Director of Village Capital. This article was completed with the support of Halloran Philanthropies and Potencia Ventures. © 2013 Saurabh Lall, Lily Bowles, and Ross Baird innovations / volumen 8, number 3/4 105 Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023 Saurabh Lall, Lily Bowles, and Ross Baird blueprint stage to validation, preparation, y, finalmente, escala. The pioneer gap occurs in the early stages of an enterprise’s growth, when it is not yet considered investable by many impact investors. The pioneer gap hypothesis is supported by additional research on the social impact sector. In an industry survey conducted by Village Capital in 2012, de más de 300 self-described impact investment funds, fewer than 10 invested, at less than $250,000 per company.3 Additionally, a Monitor study of African impact

investors found that only 6 de 84 invested in companies still in the early stages.4

According to a 2013 GIIN/J. PAG. Morgan report, impact investors cite a “lack of

appropriate capital across the spectrum” and a “lack of investable enterprises” as

the top two barriers to deploying more impact investment, which suggests that the

bottleneck of (a) not enough quality companies in the early stage and (b) no

enough effective support to produce later stage investable companies is thwarting

the growth of this sector.5

THE ROLE OF ACCELERATORS

Over the past several years, actors in the impact investing sector have developed a

growing recognition that early stage support—specifically in the form of business

incubators and accelerators—is a key intervention for addressing the pioneer gap.

Business incubators and accelerators support early stage entrepreneurs by provid-

ing them with (a) business development support (p.ej., consulting, tecnología

asistencia); (b) infrastructure support (p.ej., access to office space, shared back-

office services); (C) network support (p.ej., access to potential customers, investors,

mentors); y (d) financial support (in the form of grants/investments). This study

surveys 52 impact-focused accelerators worldwide in order to understand their

características, operaciones, and performance more fully.6

This research is particularly timely, as the number of accelerators has grown

significantly over the past five years—in fact, 73 percent of accelerators surveyed

are fewer than five years old. While the role accelerators play in entrepreneurship

has been studied to some extent (we review the existing literature in the next sec-

ción), existing studies are largely limited to those focused on technology compa-

nies in developed markets—that is, Estados Unidos. and Europe. There is little research on

accelerator activity in emerging markets and almost none on the role of accelera-

tors focused on impact investment. With over 40 impact-focused accelerators

founded in the last half-decade, we need an accurate assessment of what accelera-

tors are doing and where so that we can eventually understand how well accelera-

tors are doing in addressing market-based solutions to poverty.7

The Aspen Network of Development Entrepreneurs (ANDE) and Village

Capital believe there is a pressing need for a more holistic, evidence-based

approach to leveraging the potential of incubators and accelerators and to under-

standing what makes them successful. This report, which builds on an earlier piece

of research conducted by Village Capital, represents the first data-driven analysis

of the social enterprise accelerator landscape.8 Through a comprehensive survey of

106

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

accelerator pipelines, services, redes, and outcomes, we expect our findings to

be relevant to accelerators, impact investors, philanthropists, empresarios, y

the broader field of SGB development.

BACKGROUND

Incubators and Accelerators in Traditional Business Sectors

The study of incubators and accelerators that are focused on having a social impact

is in its infancy. Sin embargo, the research on business incubators and accelerators in

developed markets provides solid guidance for this study. The critical work of

investigadores, most prominently VanderStraeten, McMullen, and Sherman, stresses

that any accelerator has a relatively high financial cost for funders when compared

to traditional venture capital as a percentage of funds deployed, and a high time

cost for participants. Thus they emphasize the importance of evaluating an accel-

erator’s performance up front while recognizing that measuring such performance

is often challenging.9

Lalkaka and Bishop state that the performance of a business incubator should

be measured by “the survival and growth of the businesses it incubates.”10 However,

there is little consensus among researchers on the best way to measure enterprise

growth. Various studies suggest using growth in sales, employees, cash flow, y

assets as measures of success.11 Based on a review of the literature on performance

measures for incubators by Vanderstraeten and Matthyssens, we found the follow-

ing two measures of incubator performance the most relevant for our study: el

percentage of graduate enterprises companies that have received a major invest-

mento, or are operating profitably (success rate), and the percentage of graduate

enterprises that are surviving (which includes firms that may not yet be prof-

itable).12

There is some consensus on the key factors that lead to accelerator success:

(cid:2)(cid:1)Organizational resources. Some research suggests that resource dependence, o

the funding structure for accelerators, can have an impact on their performance.

Chandra and Fealey suggest that overreliance on philanthropic support can have

a negative impact on accelerator performance.13

(cid:2)(cid:1) Selection. A number of studies confirm that enterprise selection has a critical

relationship with accelerator performance, and that a rigorous selection process

enables incubators and accelerators to evaluate key enterprise characteristics.

Screening best practices includes evaluating managerial, product, and financial

características, as well as market dynamics.14

(cid:2)(cid:1)Quality of (and access to) services. The same researchers suggest that access to

professional management services, as well as other supporting resources

(administrative support, accounting, marketing, legal support), is considered

important, yet the quality of services and the period of engagement have a

stronger relationship with the success of an accelerator.15

innovaciones / volumen 8, number 3/4

107

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

(cid:2)(cid:1)Networks. Haapasalo and Ekholm argue that the most important factor for incu-

bator success is organized networking, and the most critical service a strong net-

work of experts, potential investors, and business contacts.16

Sin embargo, evidence to date on accelerator performance in traditional business

sectors is mixed. Both Ferguson and Olofsson, and Löfsten and Lindelöf suggest

that startup companies with accelerator intervention have a higher survival rate

and rate of sales growth than similar startup companies without exposure to an

accelerator.17

Sin embargo, the data is inconclusive. Amezcua studied a nationally representative

sample of U.S. firms and found that incubated firms demonstrate short-term

employment and sales growth but in fact fail 10 percent sooner than their non-

incubated counterparts, which suggests that the protective environment of an

incubator may actually inhibit firms from developing resilient routines and com-

petencies.18 In this same vein, in his study of business incubators in Europe, de

Oliveira found that there is often a mismatch between the services that incubators

offer and the needs of participating enterprises.19

Underscoring all these findings is the relative paucity of significant research

conducted on accelerator inputs and enterprise outcomes, which demonstrates the

need for a study on the impact investing/social entrepreneurship landscape.

Incubators and Accelerators in the Impact Investing Sector

According to our findings, the number of accelerators serving impact enterprises

has grown rapidly over the last five years (encima 70 percent of the accelerators sur-

veyed were founded in 2008 or later). Despite this strong growth, there is only lim-

ited research and data-driven analysis of accelerators’ role in the impact invest-

ment ecosystem. This report aims to generate a greater understanding of accelera-

tors in that sector and is part of a broader strategy to analyze, evaluate, benchmark,

and strengthen accelerators. It is not intended to be a comprehensive evaluation of

impact accelerators but an initial assessment of the landscape of these organiza-

ciones

We have divided this report into six sections:

(cid:2)(cid:1)The landscape of accelerators. We present an overview of the data collected from

52 incubators and accelerators between November 2012 and February 2013,

focusing on key descriptors such as organizational structure, finances, geograph-

ic scope, and human capital. This overview presents the landscape of a growing

group of accelerators that are seeking to have an impact beyond financial

returns.

(cid:2)(cid:1)Enterprise pipeline and selection. We discuss key impact areas, the stage of the

enterprises they support, and their recruitment and selection processes.

(cid:2)(cid:1)Services and benefits. We examine the various services that accelerators provide

to their enterprises, the duration of their programs, and the frequency of the

mentoring sessions. We also study the post-program support accelerators pro-

vide.

108

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

(cid:2)(cid:1)Accelerator networks. We review the various kinds of formal partnerships accel-

erators typically seek, with impact investors, commercial investors, foundations,

gobiernos, and universities. We also present findings from our survey of

investors about their connections with accelerators.

(cid:2)(cid:1)Metrics and evaluation. We discuss accelerators’ efforts to collect financial and

social performance data from their enterprises and identify gaps in current prac-

tices.

(cid:2)(cid:1)Measuring accelerator performance: First steps. Drawing from the literature on

traditional incubators and accelerators, we examine which factors are associated

with improved accelerator performance in terms of organizational age, estructura,

selección, services, and networks. We do not suggest any potential causality but

expect our findings to guide more rigorous future evaluations of the perform-

ance of social enterprise accelerators.

Based on our findings, we highlight common conclusions and trends that we

hope can help funders, investors, and enterprises leverage accelerators most effec-

tively to drive their enterprises’ impact and growth. We conclude by providing a

series of recommendations for these various groups.

DATA AND METHODOLOGY

Village Capital launched the first phase of this project in spring 2012, gathering

initial data from accelerators in the impact investment sector, and it joined with

ANDE that summer to integrate the initial findings into a broader research strate-

gy on accelerators. En octubre 2012, Village Capital and ANDE shared the findings

from an initial survey of 25 accelerators at the conference of the Society of

Consumer Affairs Professionals in Business, or SOCAP, and other conferences in

a report titled, “Bridging the Gap: The Role of Accelerators in Impact Investing.”

Based on feedback from various stakeholders, including impact investors,

accelerators, foundations, and academics, Village Capital and ANDE revised the

survey in October 2012, sending it in mid-November to approximately 50 addi-

tional accelerators identified through our networks. El 25 original respondents

also received a supplemental survey to enable a comparison of data points from the

first research report. In January 2013, we identified 122 additional incubators and

accelerators through F6S, a website that serves as a bulletin board for upcoming

incubator and accelerator programs for startups. We asked all accelerators sur-

veyed up front for their “impact objectives beyond financial returns,” and allowed

accelerators to state that they “have no impact objective beyond financial returns”

in order to enable a comparison of impact-focused accelerators to non-impact-

focused programs.

Initial feedback from the first report also focused on investors; given that 98

percent of the accelerators surveyed listed “access to investors” as a primary bene-

fit of the program, industry feedback suggested that an appropriate study of the

accelerator landscape should also focus on investors’ engagement with accelera-

innovaciones / volumen 8, number 3/4

109

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

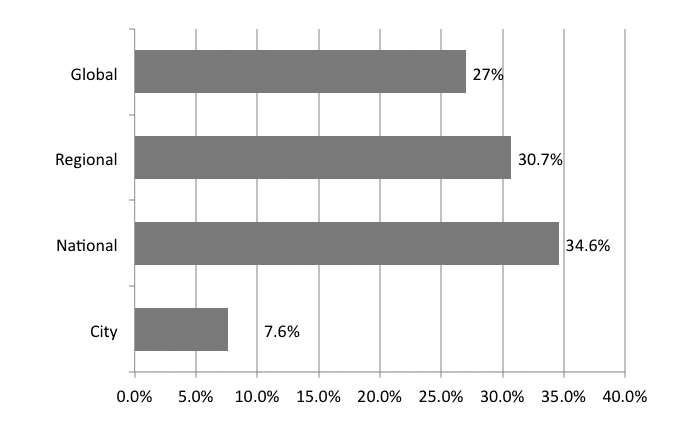

Cifra 1. Geographic scope (norte = 52)

tores. We surveyed 60 impact investors on different variables relative to their rela-

tionship with accelerators.

After significant follow-up via email and phone from December 2012 a

Febrero 2013, we closed the surveys in mid-February with a final response rate of

33 por ciento (65 out of 197 accelerators). We also received a 60 tasa de respuesta porcentual

for the investor survey (36 out of 60 investors surveyed).

We dropped seven incomplete responses due to insufficient data, leaving us

con 58 complete responses. Sin embargo, only six accelerator respondents identified

themselves as having “no impact objectives beyond financial returns,” which was

not a sufficient sample to make a reasonable comparison between impact-focused

and non-impact-focused accelerators. Por lo tanto, we dropped these six observa-

tions and focused on the 52 social impact-focused accelerators in this study.

In presenting our findings, we provide descriptive statistics on key accelerator

characteristics and performance, and also conduct some preliminary analysis of

the factors that may contribute to better performance. We used t-tests to compare

accelerators’ performance in different categories related to organizational structure

and funding, selección, services, and networks. Given the relatively small sample

size and the fact that all the data are self-reported, we are cautious about making

strong inferences at this stage.

Sin embargo, we suggest that these findings will be helpful in pointing the way for

further, more rigorous analysis of incubator and accelerator performance. Somos

currently developing a more extensive analysis on this topic by building a longitu-

dinal dataset of social enterprises—both accelerator and non-accelerator gradu-

110

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

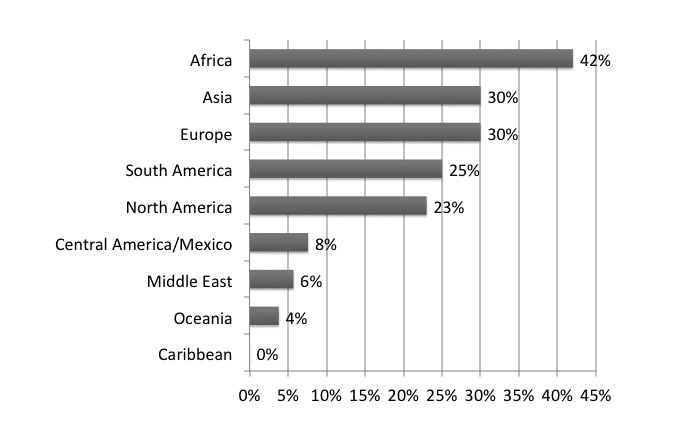

Cifra 2. Geographic focus (norte = 52)

ates—to find relationships between accelerator interventions and enterprise per-

rendimiento, as well as an evaluative framework to assess accelerator performance.

THE LANDSCAPE OF IMPACT-FOCUSED ACCELERATORS

Geographic Scope

Del 52 accelerators surveyed, 27 percent are open to enterprises across the globe

(p.ej., the Unreasonable Institute and the Global Social Benefit Incubator); 31 por-

cent are open to ventures from specific regions (p.ej., GrowthAfrica is open to ven-

tures from East Africa, Agora Partnerships is open to ventures across Central

America and Mexico); 35 percent operate nationally (p.ej., Artemisia is open to

ventures in Brazil, New Ventures-Mexico operates pan-Mexico), y 8 por ciento

operate in specific cities (p.ej., the SEHub focuses on Singapore-based ventures)

(Cifra 1). The majority of accelerator operations in this study are focused on

África (Cifra 2).

Organizational Structure

As a baseline analysis of accelerators, we first analyzed the founding of organiza-

ciones, as well as their structure and funding sources. As mentioned before, acceler-

ators are relatively new, although though the oldest in our sample was founded in

1996. Perhaps counter-intuitively, impact-focused accelerators seem more focused

on developing revenue streams beyond philanthropic support than traditional

innovaciones / volumen 8, number 3/4

111

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Human Capital

With the growing awareness of accelerators’ valuable role in impact investment,

these organizations are attracting significant human capital and resources to

their operations. De término medio, accelerators employ about 11 staff members (eight

full-time and three part-time employees).* Older accelerators (those founded

antes 2008) are considerably larger, with an average of 27 employees, than

younger accelerators, with about six employees, suggesting that accelerators have

the potential to scale. As newer accelerators become more established and

strengthen their operations, we expect them to need more human capital.

* We excluded a large accelerator with 280 employees for this estimate. If included, accelerators

in the sample would have an average of 17 employees.

business accelerators. Curiosamente, while research on incubators and accelerators

in traditional business sectors suggests that the majority are structured as nonprof-

es, 38 percent of the accelerators in our sample are set up as for-profits, 44 por ciento

as nonprofits, y 17 percent as hybrids.20

Funding Sources

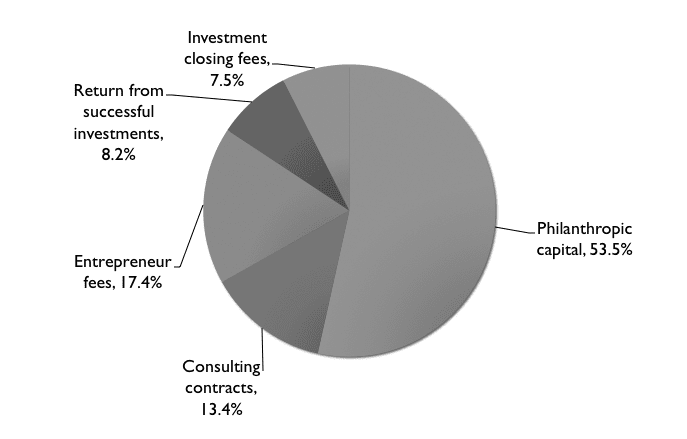

Accelerators appear to have sufficient resources to operate but they are by no

means self-sustaining. De hecho, 57 percent of the respondents stated their financial

condition was “operating smoothly,” while 16 percent reported operating with a

surplus. Only about a quarter of the respondents said they were “strapped for

cash.”21 Accelerators’ current sources of revenue include, in order, filantrópico

capital, program fees, consulting contracts, program fees, and investment closing

fees (Cifra 3).

(cid:2)(cid:1) Filantropía. Even though almost two-thirds of the accelerators we surveyed

report being structured as for-profits or hybrids, 74 percent of all accelerators

rely on philanthropic support for their operations and 54 percent of the total

capital currently used by accelerators is from philanthropic sources. This finding

suggests that, while many accelerators expect to develop revenue streams in the

future, the majority are also likely to rely on grants to support some portion of

their operations for the foreseeable future.

(cid:2)(cid:1)Entrepreneur fees. About one-third of the accelerators surveyed charge partici-

pants fees, while an additional 17 percent plan to have fees in the future.

Accelerators charge from $120 a $5,000, averaging $1,300 per enterprise, excluding three that charge $10,000 or more.

(cid:2)(cid:1)Consulting contracts. The second-highest source of accelerator budgets is rev-

enue from consulting contracts. Accelerators have the unique position of having

high exposure to a large volume of enterprises and are able to monetize their

expertise in two ways: (a) research on knowledge and insights gained from

enterprise exposure, y (b) direct business development assistance provided to

entrepreneur graduates.

112

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 3. Accelerator budgets by funding source (norte = 50)

(cid:2)(cid:1)Returns from investment. Returns from investment represents a small percent-

age of revenue (8.2 por ciento), although nearly half the accelerators surveyed

reported taking some equity in the enterprises that go through their programs.

This is unsurprising, given that the sample of accelerators is relatively young, y

that liquidity events from impact investments are rare and can take several years

to materialize.

(cid:2)(cid:1) “Success fees” from investment. Ninety-eight percent of accelerators promote

access to investors as a valuable service, and many monetize it by charging “suc-

cess fees” for investments that are brokered. While this remains the lowest line

item of all accelerator budgets, cerca de 7.5 percent of all accelerator budgets are

funded by success fees.

ENTERPRISE PIPELINE AND SELECTION

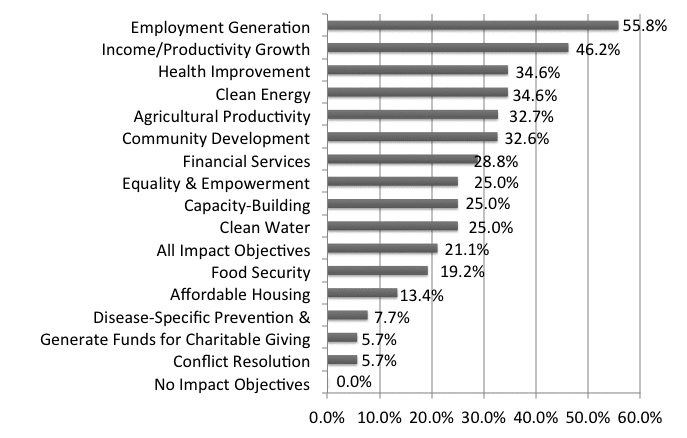

Sector and Impact Objectives

Twenty percent of accelerators focus on entrepreneurs from one particular sector,

40 percent work with entrepreneurs from several specific sectors, y 40 por ciento

are not sector specific. As certain sectors continue to grow, we expect to see more

specialization.

We focused our study specifically on incubators and accelerators that claim to

have at least one impact objective beyond financial returns. Based on our sample,

the types of impact objectives can be put into two broad categories: employment,

and products and services for the underserved. The majority of accelerators sur-

innovaciones / volumen 8, number 3/4

113

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Cifra 4. Impact objectives (norte = 52)

veyed (Cifra 4) focus on employment generation (56 por ciento) and income and

productivity growth (46 por ciento), and they aim to stimulate socioeconomic devel-

opment by supporting SGBs. Sin embargo, a significant proportion also focus on sup-

porting enterprises working in health care (35 por ciento), clean energy (35 por ciento),

and agriculture (33 por ciento). This finding is consistent with previous data suggest-

ing that these three sectors are the largest and fastest growing in impact investing.22

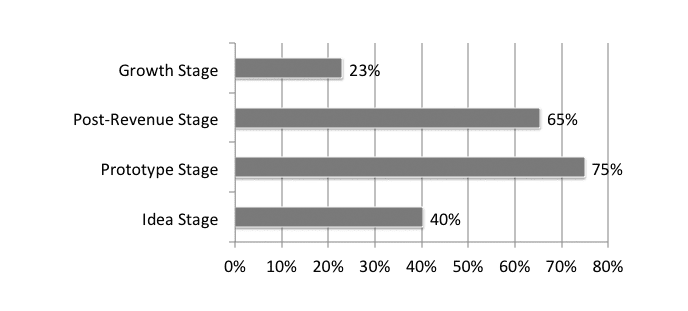

Enterprise Stage of Development

The accelerators surveyed work with enterprises in a range of developmental

stages, ranging from the idea stage to the growth stage (Cifra 5). To focus on spe-

cific areas where accelerators have intervened in ventures, we clearly defined four

areas of enterprise development and identified the percentage of accelerators that

reported working with ventures in each stage (some accelerators reported involve-

ment in multiple stages):

(cid:2)(cid:1)Idea stage (40 percent of accelerators). The proverbial “idea on paper”; ventures

at this stage do not yet have a working prototype, good/service/product, or cus-

Tomeros.

(cid:2)(cid:1)Prototype stage (75 percent of accelerators). The most common stage for accel-

erator involvement, “prototype stage” is where accelerators have a working “min-

imum viable model” of their good or service but do not yet have revenue.

(cid:2)(cid:1) Post-revenue stage (65 percent of accelerators). Ventures have customers and

typically functioning revenue models; sin embargo, their business model is not yet at

escala, they are not yet cash-flow positive, and they typically have not raised sig-

114

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 5. Enterprise stage of development (norte = 52)

nificant financing outside “friends and family.”

(cid:2)(cid:1)Growth stage (23 percent of accelerators). Ventures are operating business mod-

els at scale; they typically are cash/flow positive and/or have raised significant

outside venture financing.

Of particular note is a less clear distinction between incubators and accelera-

tors in the social enterprise space than in traditional business sectors, where these

roles are more clearly defined. Social enterprise accelerators tend to work across a

fairly wide spectrum of enterprise development stages, perhaps reflecting the rela-

tively limited pipeline of firms.

Enterprise Recruitment and Selection

Accelerators devote significant resources to the recruitment and selection process;

el 52 we surveyed have worked with a total of 20,216 empresarios. Mientras 7 por-

cent of accelerators spend less than a month on recruitment activities, 33 por ciento

spend between three months and one year, but most common are the 60 por ciento

that spend between one and three months recruiting each new cohort.

Accelerators recruit entrepreneurs through a host of different channels. El

most common sources cited include:

1. Referrals from entrepreneurs affiliated with the accelerator

2. Impact investors (individuals and investment funds)

3. Commercial investors (individuals and investment funds that do not self-iden-

tify as impact investors)

4. Entrepreneurial associations (fellowships, scholarships) in the social impact

espacio

5. Entrepreneurial associations that do not identify with social entrepreneurship or

impact investing

6. Universities

7. Industry associations focused on specific sectors

innovaciones / volumen 8, number 3/4

115

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

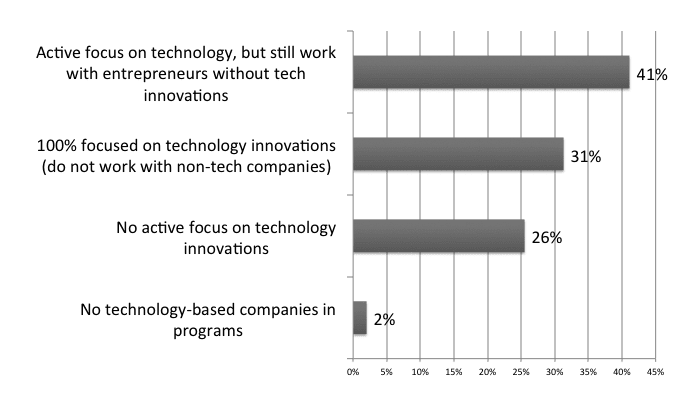

Tecnología- and Invention-based Enterprises

While accelerators are not necessarily focused on technology/invention, nosotros

studied the degree to which accelerators were actively focused on invention-

based enterprises, which we define as enterprises that have a core technology

that was invented/created by the founding team, who owns or seeks to own core

intellectual property on the invention.

Twenty-five percent of accelerators surveyed focus exclusively on working

with enterprises that have technology and/or an invention at the center of their

enterprises, while another 41 percent have an active focus on technology but still

work with non-technology or invention-focused entrepreneurs. Solo 31 por ciento

have no active focus on tech innovations, and only one accelerator had no tech-

nology-based companies in its program (Cifra 6).

8. Sector-specific conferences (p.ej., agricultura, education)

9. Social entrepreneurship or impact investing conferences

10. Requests from outside program marketing efforts and social media

11. Direct, cold-call recruitment (p.ej., finding and contacting entrepreneurs on the

web, Facebook, LinkedIn)

Not all sources are equally helpful. Accelerators ranked the following sources,

en orden, as most helpful:

1. Referrals from entrepreneurs affiliated with the accelerator (considered “help-

ful” by over 50 percent of the organizations surveyed)

2. Requests from outside program marketing efforts (30 por ciento)

3. Referrals from entrepreneurial associations (19 por ciento)

4. Referrals from upstream impact investors (15 por ciento)

Curiosamente, social entrepreneurship and impact investing conferences were

listed as the least helpful. This finding is somewhat surprising, considering the

prevalence of conferences in the sector that promote themselves as a way to con-

nect with entrepreneurs. Sin embargo, it may be that social enterprise conferences typ-

ically feature more successful and mature enterprises, making them a less useful

source of early stage companies that might apply to participate in accelerators.

Based on our sample, accelerators in the impact investment sector appear to be

less competitive in terms of selection—average acceptance rate, almost 21 por-

cent—than accelerators in the traditional business sector—average acceptance

tasa, acerca de 5 percent.23 The reasons for the lack of selectivity are unclear, but it is

possible that there is simply a much smaller pipeline of socially oriented enterpris-

es or that, due to the high percentage of accelerators earning revenue from entre-

preneur fees, investment returns, and success fees, accelerator managers may

admit these enterprises more readily in order to bring in more revenue.

Philanthropic support may also be linked to the number of entrepreneurs being

apoyado, which would also encourage accelerators to accept a greater percentage

of applicants. But selectivity does matter: below we compare key performance

116

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 6. Focus on technology and invention (norte = 50)

characteristics of accelerators that accept 10 percent or fewer of their applicants

with those of less selective accelerators.

SERVICES AND BENEFITS

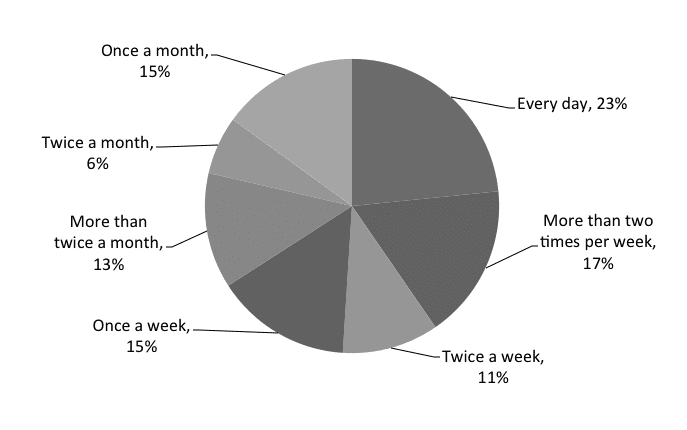

Program Duration and Frequency

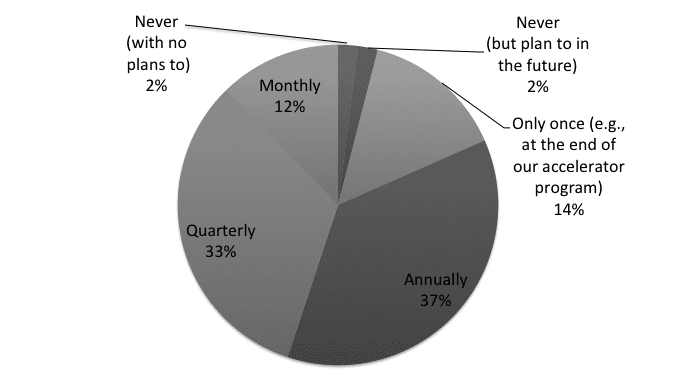

The average duration of the accelerator programs surveyed is six months.24 The fre-

quency of meetings during this period varies widely, ranging from every day (26

por ciento) to once a month (14 por ciento), with many different meeting frequencies in

entre (Cifra 7, following page).

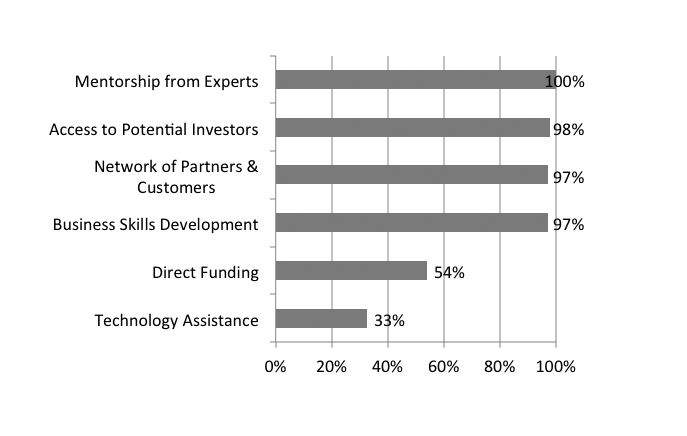

Program Services and Benefits

Eighty-three percent of accelerators describe their support approach as “high-

touch.” In this case, accelerators focused on social impact appear to be similar to

the majority of incubators and accelerators in traditional business sectors that pro-

vide “high-touch,” highly tailored services to a small group of enterprises.

Almost all programs surveyed provide the following benefits: mentorship from

experts (100 por ciento), access to potential investors (98 por ciento), a network of part-

ners and customers (97 por ciento), and business skills development (97 por ciento).

The majority of programs provide direct funding (54 por ciento), while a minority

provide technology training and assistance (33 por ciento) (Cifra 8, following page).

Other self-identified benefits of accelerators include media exposure, brand

recognition, access to a co-working space, referrals to vetted talent and human

capital, exposure to relevant and timely R&D, and membership in an extensive

innovaciones / volumen 8, number 3/4

117

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Cifra 7. Frequency of program sessions (norte = 47)

Cifra 8. Accelerator services and benefits (norte = 52)

118

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

alumni network consisting of other like-minded entrepreneurs, service providers,

and investors.

Sin embargo, the existing literature reinforces the fact that when a service is pro-

vided it is not necessarily of high quality. We expect to dive deeper into this issue

through the next phase of our research strategy by collecting enterprise-level data

from ventures that have participated in accelerators, and comparable enterprises

that have not received accelerator support.

Post-Program Support

The majority of accelerators (66 por ciento) offer post-program support to all of their

graduates at no cost; 28 percent provide free post-program services on a case-to-

case basis; 4 percent provide these services for a fee on a case-to-case basis; y 2

percent do not provide post-program support at all, due to a lack of bandwidth or

resources.

Of the accelerators that do provide post-program services to their entrepre-

neurs, 21 percent offer them for between one and six months after an entrepreneur

graduates from their program, y 9 percent offer support for between six and

eight months. The majority (70 por ciento) offer services longer than nine months,

possibly as long as the entrepreneurs’ ventures exist. The types of post-program

services offered include public relations opportunities, connections with investors,

board participation, HR/recruitment support, regional meet-ups, alumni network-

En g, and online communities listing funding and promotion opportunities.

ACCELERATOR NETWORKS

Types of Formal Partnerships

Many accelerators have formal partnerships with other organizations, which we

define as

(cid:2)(cid:1)“pipeline/deal flow partners,” which recommend enterprises for the accelerator

program and attend events/pitchfests, but do not commit financial support to

either the accelerator or the entrepreneurs;

(cid:2)(cid:1)“enterprise support partners,” which pre-commit capital to enterprises but do not

fund the accelerator program’s operations;

(cid:2)(cid:1)“organization support partners,” which fund accelerators’ organizational/opera-

tional expenses but do not fund the underlying enterprises; y

(cid:2)(cid:1)“enterprise and organization support partners,” which commit capital to both the

accelerator’s operations and the underlying enterprises.

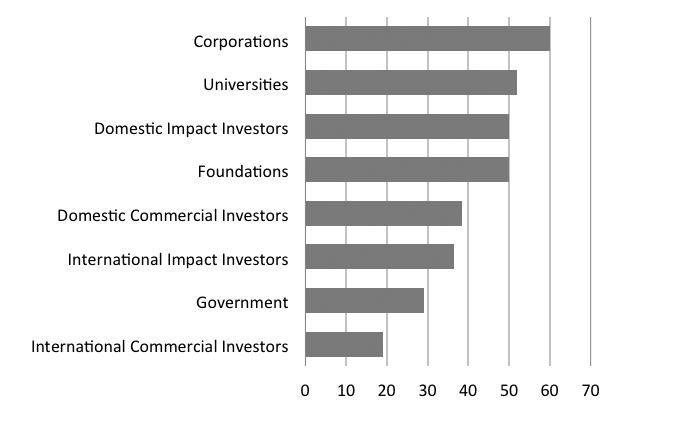

Accelerators have partnerships with five main groups: corporations, universi-

corbatas, investors, foundations, and governments (Cifra 9, following page).

Partnerships with Impact Investors

To corroborate our data from the accelerator survey and to understand accelera-

tors’ connections with impact investors more fully, we also collected data from 38

innovaciones / volumen 8, number 3/4

119

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Cifra 9. Types of organizations with which accelerators have formal

partnerships

Cifra 10. Impact investors that have a formal partnership with an accelerator

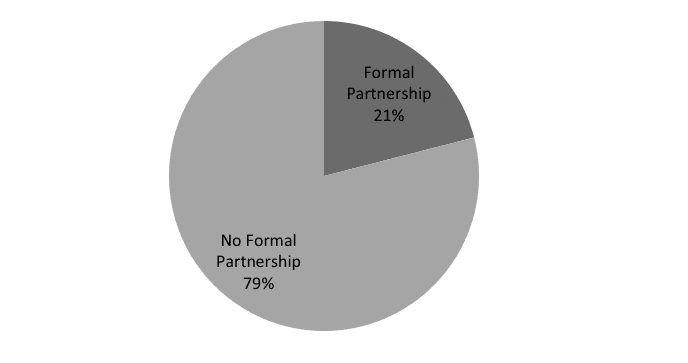

impact investment funds. Solo 21 percent of the investors we surveyed had estab-

lished formal partnerships with accelerators (Cifra 10, following page). The fol-

lowing are the most common reasons for not partnering with an accelerator:

(cid:2)(cid:1)Mandate fit. Forty-three percent of investors surveyed view accelerators as valu-

able “feeders” for their pipeline but do not consider it within their mandate to

fund them directly.

120

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 11. Impact investors with informal partnerships with accelerators ‘

(cid:2)(cid:1)Not additionally useful. Twenty-three percent of investors state that they were

able to meet their current investment goals without relying on accelerators.

(cid:2)(cid:1) Interested, but no current partnerships. Sixteen percent of the investors state

that they are interested in pursuing formal relationships with accelerators but

have not yet done so.

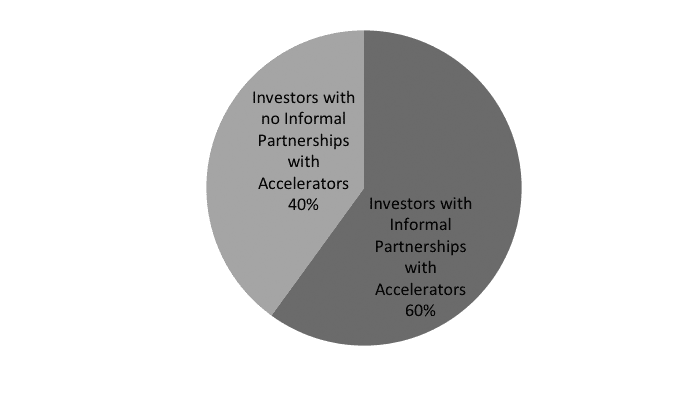

Despite the lack of formal partnerships and funding from impact investors, 60

percent of the investors in our sample did report having informal partnerships

with accelerators (Cifra 11). In our survey, we defined an informal partnership as

one in which an investor regularly communicates with accelerator staff, attends

events, or stays otherwise informed, with a primary goal of obtaining deal flow, pero

does not fund the accelerator directly.

The range of accelerator/investor engagement is wide across the board. Alguno

accelerators are in sync with impact investors: 32 percent of investors report that

hasta 20 percent of their portfolio was sourced from accelerators. Sin embargo, a plu-

rality of impact investors does not rely on accelerators for “deal flow”; 47 por ciento

report that none of their current portfolio was sourced from accelerators.

Our findings underscore the critical need for philanthropic support for accel-

erators in the near term and also raise important questions about aligning the serv-

ices that accelerators provide with the needs of impact investors. Many impact

investors do not look to accelerators for deal flow, and the majority do not con-

tribute to accelerators’ budgets in any formal and consistent way. We suggest that

accelerators need to calculate the specific value that they add for investors in terms

of lower searching and due diligence costs more accurately, and to design their

pipeline and curriculum in collaboration with experienced investors. ANDE is

innovaciones / volumen 8, number 3/4

121

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Co-Working Spaces

Many accelerators’ work is made financially viable by their operating out of free

or affordable co-working spaces. De hecho, 61 percent of accelerators surveyed

maintain a formal partnership with a university, organización, or co-working

espacio (p.ej., the Hub) to lower the cost of their operations.

pursuing additional research on developing a framework to analyze the value cre-

ated by accelerators (described in Conclusions and Next Steps).

METRICS AND EVALUATION

Based on our analysis, metrics and evaluation are key target areas for improvement

among impact-focused accelerators. Desafortunadamente, a significant proportion of

organizations that we surveyed do not track financial or social performance data

on an ongoing basis, making it difficult to assess performance and establish bench-

marks for the sector.

Financial and Social Performance Data Collection

We asked accelerators to report on the status of their graduate enterprises. Mientras

the majority of accelerators (96 por ciento) collect financial data from their enterpris-

es, 23 percent do not track the status of their graduate enterprises at all, cual

makes it difficult to evaluate their performance. We noticed the following gaps in

accelerator data analysis:

(cid:2)(cid:1)Lack of any data collection. Of the accelerators we surveyed, 4 percent do not

collect any financial performance data from their enterprises, mientras 28 por ciento

do not collect any social or environmental performance data (Figures 12, 13).

We find this discrepancy surprising, given the impact-oriented focus of these

accelerators. Potential interventions to improve the impact-oriented data collec-

tion with accelerators could be to support the introduction of standardized

reporting frameworks also used by those who invest and provide capital in the

sector, such as IRIS and GIIRS.

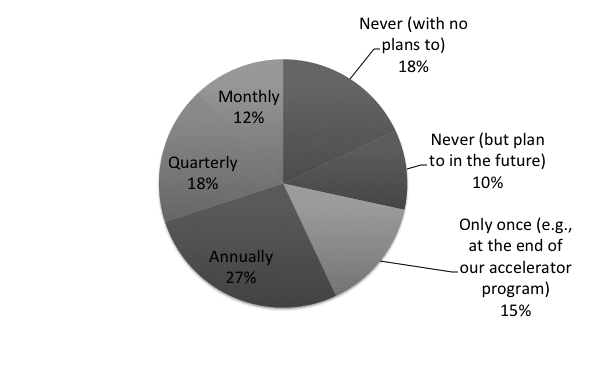

(cid:2)(cid:1)Data tracking venture performance over time. Además, 14 por ciento de la

respondents only collect financial data at a single point in time (p.ej., at the begin-

ning or end of their program), y 15 percent only collect social and environ-

datos mentales (n=48) at a single point (Cifra 14, abajo). This makes it difficult to

assess whether there is any change in the social or financial performance of the

enterprises that go through these programs.

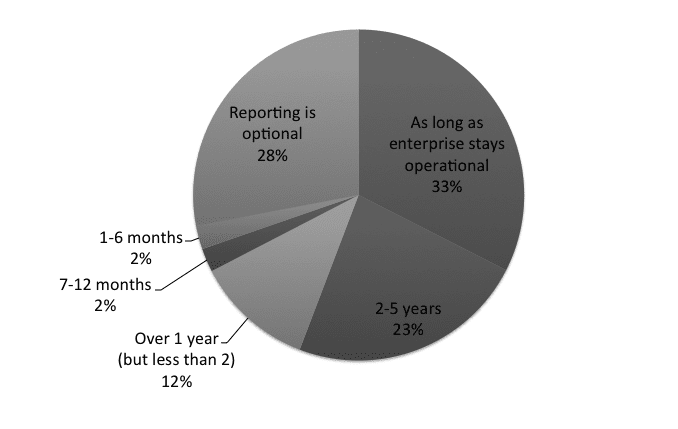

(cid:2)(cid:1)Accelerator-driven data collection mandates. Finalmente, 28 percent of respondents

consider reporting by their program participants to be “optional.”25 The majori-

ty of the accelerators that do require reporting expect enterprises to provide data

for at least one year after the end of their programs, and about one-third require

reporting as long as the enterprise is in operation.

122

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 12. Frequency of financial performance data collection (norte = 49)

Cifra 13. Frequency of social and environmental performance data collection

(norte = 48)

(cid:2)(cid:1) Data-collection methodologies. The primary method of collecting data also

varies widely, con 64 percent of accelerators collecting data through in-person

interviews or site visits, 52 percent via phone, y 50 percent via email or online

mechanisms. The variety of methods used in data collection also affects how

reliable and unbiased the data are.

innovaciones / volumen 8, number 3/4

123

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Cifra 14. Data reporting period (norte = 48)

Accelerator Graduate Performance

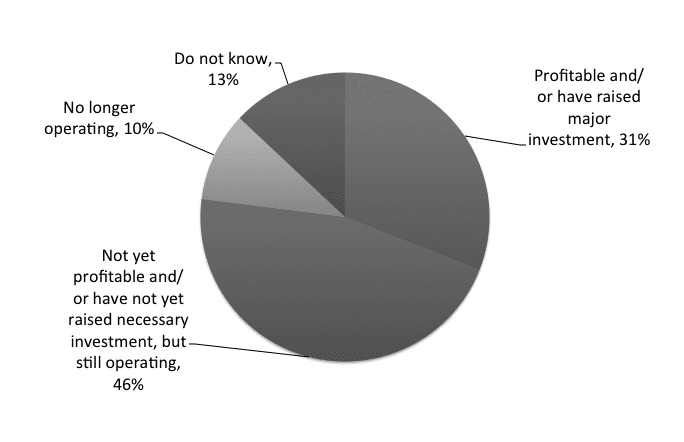

Acerca de 77 percent of the accelerators in our sample track the status of their gradu-

ate enterprises, though their data-collection methodologies are varied and incom-

plete. We analyzed the performance of ventures that graduated from the accelera-

tors that do collect data (n=40): 31 percent are reported to be profitable and/or

have received major investment, otro 46 percent are still in operation but are

not yet profitable and/or have not yet received major investment, and about 10 por-

cent are no longer operating. There is no data available on 13 percent of the enter-

tomado, even for the accelerators that do track their enterprises (Cifra 15).

MEASURING ACCELERATOR PERFORMANCE: FIRST STEPS

Based on research on incubators and accelerators in developed markets, we ana-

lyzed four key factors among the sample size of this study that typically affect

accelerator success: organizational funding sources, selectivity, services, and net-

obras. We also analyzed the variable “accelerator years in operation” to compare

older accelerators (those that have been in operation over five years) to younger

accelerators. We used the following two self-reported variables as measures of

accelerator success, consistent with the literature on incubators and accelerators.26

(cid:2)(cid:1)Enterprise success rate. Percentage of graduate enterprises operating at a prof-

itable level, and/or having raised major investment ($500,000 or more) (cid:2)(cid:1)Enterprise survival rate. Percentage of graduate enterprises that are operating at a profitable level, and/or have raised major investment ($500,000 or more), o

124

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Cifra 15. Status of graduate enterprises (norte = 40)

are still operating, but are not yet profitable and/or have not yet raised necessary

investment (es decir., inclusive of previous category)

We conducted independent sample t-tests to compare average performance

measures across different categories for these factors.27

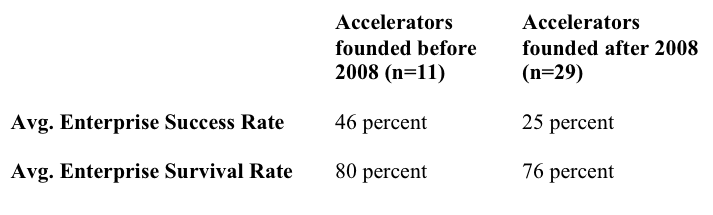

Accelerator Years in Operation

While many accelerator characteristics can influence their performance, Residencia en

the literature, we hypothesized that older, more established accelerators would per-

form better on average, given their experience and track record.28 In our sample,

we find that older accelerators do perform better in terms of their enterprise suc-

cess rates, with an average of 46 percent as compared to only 25 percent for

younger accelerators, a difference that is statistically significant at the 5 por ciento

nivel. Sin embargo, we do not observe any differences in terms of survival rates, con

older accelerators achieving an 80 percent survival rate, compared to a 76 por ciento

survival rate for younger programs (Mesa 1). A more thorough study could inves-

tigate whether the discrepancy in results is due to graduates of older accelerators

having more time to develop successful business models, thus we are proposing to

conduct an enterprise-level study as a follow-up to this initial study in order to

investigate this hypothesis more thoroughly.

innovaciones / volumen 8, number 3/4

125

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Mesa 1. Comparing accelerators by age

Mesa 2. Comparing organizational funding sources

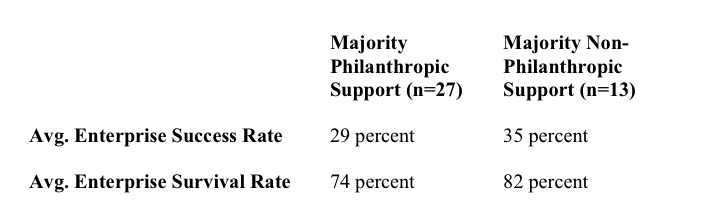

Organizational Funding Sources

In our sample, we found that about two-thirds of respondents relied primarily on

grants for their operations, defined as over 50 percent of annual revenue. Sin embargo,

we did not find any significant differences in this study in the enterprise success

rate or the enterprise survival rate (Mesa 2). Accelerators reliant on grants had an

average enterprise success rate of 29 percent and a survival rate of 74 por ciento, mientras

those that were not grant reliant had a success rate of 35 percent and a success rate

de 82 por ciento.

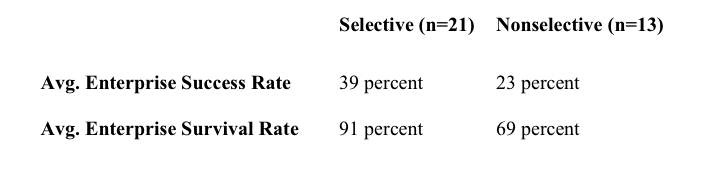

Selectivity

We found that, consistent with general theory on incubators, selectivity is a key

characteristic of successful incubators/accelerators in the social enterprise sector.

In traditional incubator literature, a 5 percent acceptance rate is considered a char-

acteristic of a good program. Incubators in the social enterprise space are still rel-

atively new, so we defined accelerators that accept 10 percent or fewer of their

applicants as “selective” and the rest as “non-selective.”

We were only able to gather data points from 34 accelerators for this part of the

análisis, so it is difficult to draw definitive inferences at this stage. Sin embargo, en

conducting t-tests across selective and nonselective accelerators, we found that

selective accelerators do appear to perform better, with an average enterprise suc-

126

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

Mesa 3. Comparing selective and nonselective accelerators

cess rate of 39 percent and an average enterprise survival rate of 91 por ciento. En

comparación, nonselective accelerators have an average enterprise success rate of 24

percent and a survival rate of 69 por ciento. The differences are weakly significant, en

el 10 percent level (Mesa 3). Sin embargo, we believe more research is needed to

understand why social enterprise incubators in general are not as selective, y el

extent to which selectivity factors into accelerator performance. We hope to exam-

ine this issue in more detail by encouraging more accelerators to collect data from

their graduate enterprises and by developing a longitudinal dataset of enterprises,

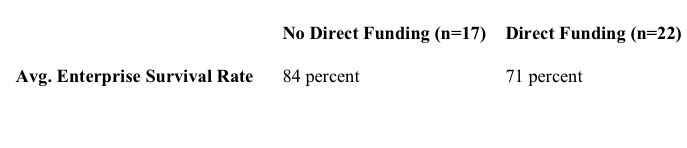

Services

We received data from 52 accelerators globally. We found that the majority of

accelerators provide the same core services: business skills training, mentoring, a

network of partners/customers, and access to potential investors. The only differ-

entiation was whether or not an accelerator provided direct funding to its enter-

prises as part of its program.

Thirty-nine accelerators responded to the question on providing direct fund-

En g. Asombrosamente, we found that accelerators that do not provide direct funding

appear to have higher enterprise survival rates, although the results were not sta-

tistically significant. De término medio, accelerators that did not provide any direct fund-

ing had enterprise survival rates of 84 por ciento, compared to 71 percent among

those that did (Mesa 4, next page).

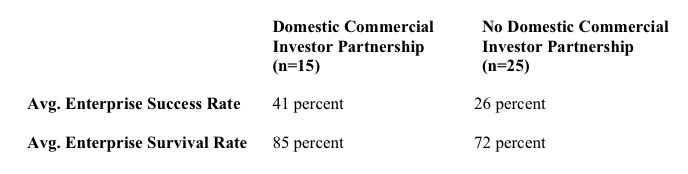

NETWORKS AND PARTNERSHIPS

As discussed previously, accelerators partner with a wide range of organizations,

including investors (both commercial and impact focused), foundations, universi-

corbatas, corporations, and governments. We found no apparent differences between

accelerators that partnered with the following types of organizations and those that

no lo hizo:

(cid:2)(cid:1)International impact investors

(cid:2)(cid:1)Domestic impact investors

(cid:2)(cid:1)International commercial investors

(cid:2)(cid:1)Foundations

(cid:2)(cid:1)Universities

innovaciones / volumen 8, number 3/4

127

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Mesa 4. Comparing accelerators that provide direct funding to those that do not

Mesa 5. Comparing accelerators that have partnerships with domestic

commercial investors to those that do not (norte = 40)

(cid:2)(cid:1)Governments

When we compared accelerators that had formal partnerships with “domestic

commercial investors,” such as the local banks, angel investors, and venture capital

funds in their networks, we found differences in the average enterprise success and

enterprise survival rates. In this sample of 40 accelerators, those that had formal

partnerships with these investors had an average 41 percent success rate and 85

percent survival rate. En comparación, accelerators that did not have formal partner-

ships with these types of investors had an average enterprise success rate of 26 por-

cent and an enterprise survival rate of 72 por ciento. The differences in the enterprise

success rate were also weakly significant, en el 10 nivel porcentual (Mesa 5).

It is interesting to note that formal partnerships with impact investors were not

statistically related to enterprise success rates for these acceleration programs, sug-

gesting a potential disconnect between accelerators and investors with similar

impact objectives.

CONCLUSIONS AND NEXT STEPS

The number of incubators and accelerators providing tailored support to social

enterprises continues to grow. In many countries, these incubators and accelera-

tors are the first entry point for social enterprises into a broader ecosystem and

impact investing community that can help them grow at a key stage of develop-

mento, creating the opportunity for organizations to play a critical role in bridging

the pioneer gap.

128

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

This study identified several key variables that are related to the success and

failure of accelerators, as well as several key gaps that may be holding back accel-

erator success. We have outlined key findings below and provided recommenda-

tions that reflect these findings.

Partnership with in-country commercial investors matter.

For many impact accelerator graduates, the next step in financing may not be

impact investors—a 2012 Emory-Village Capital study found that fewer than 10

impact investors invested less than $250,000 per enterprise—but traditional com-

mercial investors such as banks, angel networks, and strategically aligned corpora-

tions that find a particular interest in the impact objective of the accelerator. El

form of partnership that generated the greatest difference between enterprise suc-

cess rates was the domestic commercial investor; local investors that were able to

finance ventures but did not necessarily self-identify as impact investors.

Two relevant examples are Nigeria’s Wennovation Hub, which has partnered

with Google Africa in a move to enable all ventures to use Google products to

build their businesses, and Nairobi’s m:Lab, which has partnered with Nokia and

Samsung to help mobile-based entrepreneurs who are developing products to

address needs of the poor. In our own experience, Village Capital is launching a

program with the Pearson Affordable Learning Fund in India to source, accelerate,

and invest in education interventions that support the base of the pyramid.

Selectivity matters.

It stands to reason that the accelerators selecting the best ventures are likely to have

the best results. Various studies on traditional business accelerators suggests that

programs with a lower acceptance rate and more rigorous selection process had a

higher degree of success among their graduate ventures.29 Knowing that most start-

ups fail, accelerators cast a wide net when recruiting ventures. Our research, cual

is consistent with the broader literature on the topic shows that impact accelerators

with a lower percentage acceptance rate have a higher proportion of successful

graduates. This finding provides two actionable steps for accelerators: (1) encima-

resource recruiting so that accelerators are not required, for business model rea-

hijos, to accept substandard ventures; (2) focus on the quality rather than the quan-

tity of entrepreneurs served and develop a rigorous selection process.

Further research could explore the cumulative impact of more selective accel-

erators, as some accelerator programs operate a high-volume, light-touch model

that they believe may lead to less selective cohorts and a higher failure rate, pero

ultimately have a greater impact per dollar invested due to a high volume of grad-

uate ventures.

innovaciones / volumen 8, number 3/4

129

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

Philanthropy is currently necessary for accelerators to survive but is not

statistically related to enterprise success.

Three out of four accelerators rely on philanthropy to survive, y 54 percent of all

accelerator budgets are funded through grants. This finding suggests the following:

(1) impact accelerator business models are not yet proven to the point where they

can develop sustainable revenue streams, and accelerators currently require grants

to fill the gaps they are seeking to address; y (2) most accelerators are providing

resource leverage on philanthropy by complementing grants with sources of

earned revenue. We believe that philanthropy will play a critical role in supporting

impact-focused accelerators in the immediate future. Sin embargo, donors can also

encourage accelerators to explore new revenue streams that will allow them to

become less reliant on grants without compromising their social mission.

Most impact investors are looking to accelerators for investment opportunities

but are not finding them.

Mientras 60 percent of impact investors say they have an informal sourcing partner-

ship with accelerators, 47 percent say they have sourced “zero” portfolio companies

directly from an accelerator. This disconnect reflects a more fundamental chal-

lenge that accelerators face, balancing the business development needs of social

entrepreneurs on the one hand while trying to meet the specific criteria of impact

investors on the other. Investors cite “lack of fit with our investment criteria” as a

primary reason they do not invest in accelerator graduates, suggesting that accel-

erators could do a better job of engaging proactively with investors in the selection

process to develop cohorts that are more ready for follow-on investment.

Accelerators might face a “free rider” problem.

Al mismo tiempo, while the majority of impact investors look to accelerators as a

sourcing mechanism, solo 20 percent help accelerators fund their operations. El

primary reason for this lack of involvement is “mandate fit”—investors do not view

it as their role to support accelerators. In the long run, as cash-strapped accelera-

tor programs try to fund their operations, they may see a “free-rider” problem that

causes a misalignment between accelerators and investors. Accelerators, investors,

and donors need to find a funding model that covers the cost of quality business

acceleration for entrepreneurs, maintains the impact focus, and also generates a

reasonable value proposition for all parties.

We have little systematic data on how accelerators are performing, and many

accelerators are not even collecting data.

These findings are from a sample of 52 accelerators worldwide; sin embargo, nosotros necesitamos

much more data on the effectiveness of incubators and accelerators to assess the

quality of services provided, as well as the importance of selection and networks.

While small for conducting statistical analysis, our sample of accelerators is rela-

tively large, given the current stage and size of the impact investing sector. Nosotros

130

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

believe that expanding this dataset will allow a more refined, multivariate analysis

of key accelerator success factors.

To assess accelerator performance more fully, we need more and better longi-

tudinal data on the enterprises that receive support, and on those that apply but do

not receive support. Village Capital and ANDE, in collaboration with several key

partners, are currently working with Emory University’s Social Enterprise @

Goizueta to develop a longitudinal database of enterprise performance. This proj-

ect will address the following:

(cid:2)(cid:1)How do entrepreneurs that participate in accelerator programs perform differ-

ently than others?

(cid:2)(cid:1)Are there differences in measurable impact between general/global accelerator

programs and those that focus on specific sectors or regions?

(cid:2)(cid:1)What specific program design choices (related to participant selection, services

provided, and network development) are associated with more positive acceler-

ator impacts?

Over the longer term, this database will allow additional longitudinal analysis

of how various interventions can affect social enterprises at different stages of their

desarrollo.

The majority of accelerators that did not collect data cited a lack of

time/resources for data collection. Most accelerators are startups themselves, y

we recommend that philanthropists or investors who support accelerators also

provide support for data collection/assessment.

Finalmente, ANDE is collaborating with I-Dev International to develop a common

framework to quantify the value created by incubators and accelerators for

investors and enterprises. I-Dev is evaluating and benchmarking six-eight impact

incubators and accelerators, identified through the ANDE-Village Capital survey,

and using this framework to compare the performance of “accelerated” versus “un-

accelerated” SGBs that have received investment. Through this analysis, we hope

to quantify the monetary value created for both SGBs and investors by comparing

the costs associated with deal sourcing, due diligence, investment cycle, advisory

services, and probability of exits.

We believe this broad, multipronged initiative will provide significant value for

the enterprises, incubators, and funders that support accelerator services. Nuestro

work will provide answers to critical questions and thus allow entrepreneurial

firms to make more educated decisions about whether to join an incubator and, si

entonces, which one. It will inform accelerator managers about best practices and provide

mechanisms to improve their performance. Finalmente, foundations, investors, y

development institutions will be able to assess the impact of their investments and

identify strategies to scale or replicate successful incubator models.

innovaciones / volumen 8, number 3/4

131

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

RECOMMENDATIONS

Based on this research, we recommend several actions for various players in this

ecosystem: incubators and accelerators, impact investors, foundations, and aca-

demics.

For Incubators and Accelerators

(cid:2)(cid:1)Invest in platforms and systems to encourage and enable quality data collection

from the enterprises you support,

(cid:2)(cid:1)Collect data from all enterprises that apply to your programs, even those that are

not accepted or do not receive services, to assess performance against a control

group more comprehensively. Simple data-collection processes can be built into

your application form.

(cid:2)(cid:1)Collect data from participating enterprises for at least five years post-graduation

to track progress and growth over the medium to long term. The impact of accel-

erator support can take several years to materialize.

(cid:2)(cid:1)Partner with academic institutions and industry associations to develop stronger

data-collection systems.

(cid:2)(cid:1) Strengthen your processes for searching and sourcing ventures for your pro-

gramos. Being in a position to select the top ventures without compromising qual-

ity matters.

(cid:2)(cid:1)Develop more rigorous, multistage selection processes, drawing from best prac-

tices in other sectors. Engage other ecosystem members, such as investors, foun-

dations, and technical experts, in the selection process so that you are building a

cohort that aligns with the needs of upstream financers.

(cid:2)(cid:1)Build networks with the local financial sector, particularly domestic commercial

investors, which may be able to directly support a plurality or majority of your

graduates more readily than impact investors.

(cid:2)(cid:1)Build networks with corporate supply chains, both domestic and international.

Enterprises need not only investment but access to markets.

(cid:2)(cid:1)Explore other revenue streams such as investment closing fees and direct invest-

mento.

For Impact Investors

(cid:2)(cid:1)Leverage the networks and reach of incubators and accelerators, and collaborate

with them to strengthen your pipeline and explore potential areas for improved

alignment in their activities.

(cid:2)(cid:1) Build formal partnerships with accelerators that are closely aligned with your

investment strategy and that have strong performance records.

(cid:2)(cid:1) Invest in accelerators with either time or money. Accelerators will be more

inclined to deliver you the deal flow you’re asking for as a customer if you help

them do the work they are trying to do.

132

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

For Foundations

(cid:2)(cid:1) Support the development and continuation of best practices among successful

accelerators and incubators by contributing to their operations, development of

performance management systems, and dissemination of their results.

(cid:2)(cid:1)Emphasize quality of services over quantity of entrepreneurs served when sup-

porting incubator and accelerator grantees.

(cid:2)(cid:1)Build stronger networks between investors and incubators to enhance ecosystem

eficiencia.

(cid:2)(cid:1)Provide support for accelerators to track enterprise performance.

For Academics

(cid:2)(cid:1)Focus on developing methodologies to assess incubator and accelerator perform-

ance more effectively.

(cid:2)(cid:1)Conduct empirical research on key success factors for incubators and accelera-

tores, including an analysis of the quality of services, the relevance of the selection

proceso, and the effects of strong partnerships and network.

APPENDICES

Organization Names (in alphabetical order)

1. Agora Partnerships*

2. Angels Initiatives

3. Artemisia*

4. Betaspring

5. Global Accelerator Network

6. Bethnal Green Ventures

7. BiD Network*

8. Capital Innovators

9. Dasra*

10. Eleven Accelerator Venture Fund

11. Endeavor*

12. Endeavor Global*

13. FATE Foundation*

14. Fledge

15. Global Catalyst Initiative*

16. Global Social Benefit Incubator*

17. Groundwork Labs

18. GrowLab

19. GrowthAfrica/The GrowthHub*

20. Hired By Society

21. HUB Vienna Incubation

22. iAccelerator, Centre for Innovation Incubation and Entrepreneurship, IIM-

Ahmedabad

23. ImpactAmplifier

innovaciones / volumen 8, number 3/4

133

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

24. Incubate

25. Intellecap (Intellectual Capital Advisory Services Pvt. Limitado.)*

26. Invest2Innovate*

27. Investment Ready Program

28. iStarter

29. LGT Venture Philanthropy Foundation*

30. metro:lab East Africa

31. Mara Foundation

32. Mozilla WebFWD

33. National Collegiate Inventors and Innovators Alliance

34. NESsT*

35. New Ventures India*

36. NewME Accelerator

37. Nxtp Labs

38. Panzanzee

39. Sinapis Group

40. StarCube

41. Startupbusiness

42. good.bee

43. Startup Farm

44. StartupYard

45. SURF Incubator

46. Tree Labs

47. UnLtd India

48. Unreasonable Institute

49. Village Capital*

50. Wennovation Hub

51. Villgro*

52. Z80 Labs Technology Incubator

* ANDE Members

Organization Names (in alphabetical order)

1. Accion Venture Lab*

2. Adobe Capital

3. Anavo

4. Angel Ventures Mexico

5. Annona Sustainable Investments BV

6. Bamboo Finance*

7. Creas

8. EcoEnterprises Fund*

9. eVA Fund

10. Ferd Social Entrepreneurs

11. Good Capital

12. Gray Ghost Ventures*

134

innovaciones / Accelerating Entrepreneurship

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Bridging the “Pioneer Gap”

13. GroFin *

14. Injaro Agricultural Capital Holdings

15. Insitor Management

16. Inversor Fund *

17. Invested Development

18. Jacana Partners *

19. LGT Venture Philanthropy*

20. Lundin Foundation*

21. ManoCap

22. Oasis500 (Oasis Ventures 1)

23. Oikocredit USA

24. Peery Foundation

25. PhiTrust Partenaires

26. Pomona Impact

27. Renewal2 Investment Fund

28. RSF Social Finance

29. Small Enterprise Assistance Fund (SEAF) *

30. SITAWI-Finance for Good

31. Social Venture Fund

32. TBL Mirror Fund

33. Unitus Impact *

34. Unitus Seed Fund

35. Vox Capital *

36. Voxtra *

37. Willow Impact Investors*

* ANDE Members

1. Y. Saltuk, A. Bouri, A. Mudaliar, and M. Pease, Perspectives on Progress: The Impact Investor

Survey. Nueva York, Nueva York, EE.UU: j. PAG. Morgan and Global Impact Investing Network, 2013.

2. h. Koh, A. Karamchandani, y r. katz, From Blueprint to Scale: The Case for Philanthropy in

Impact Investing. Nueva York, Nueva York, EE.UU: The Monitor Institute and Acumen Fund, 2012.

3. R. Baird, h. Hedinger, and C. Seekins, Bridging the Gap: The Role of Accelerators in Impact

Invertir. Atlanta, Georgia, EE.UU: Village Capital, 2012.

4. METRO. Kubzansky, A. Cooper, and V. Barbary, Promise and Progress, Market Based Solutions to Poverty

in Africa. Cambridge, MAMÁ, EE.UU: Monitor Group, 2011.

5. Y. Saltuk, A. Bouri, A. Mudaliar, and M. Pease, Perspectives on Progress: The Impact Investor

Survey. Nueva York, Nueva York, EE.UU: j. PAG. Morgan and Global Impact Investing Network, 2013.

6. In traditional business sectors, incubators and accelerators generally focus on different stages of

enterprise development. Incubators typically serve earlier stage enterprises (pre-customers and

pre-revenue), while accelerators support enterprises with existing customers and revenue.

Sin embargo, we have found that these differences are less distinct for the impact investing sector. Para

the purposes of this paper, we will use the term “accelerator” to describe an organization that pro-

vides some subset of the support outlined in the previous paragraph.

7. Over the past 30 años, several terms have been used to describe market-based solutions to social

problemas: “social entrepreneurship,” popularized by Bill Drayton, the founder of Ashoka; “impact

investing,” pioneered by the Rockefeller Foundation and GIIN; “bottom of the pyramid” business-

innovaciones / volumen 8, number 3/4

135

Descargado de http://direct.mit.edu/itgg/article-pdf/8/3-4/105/705086/inov_a_00191.pdf by guest on 07 Septiembre 2023

Saurabh Lall, Lily Bowles, y ross baird

es, coined by Prahalad and Hart; and several others (p.ej., “triple-bottom-line investing,” “inclusive

business”). Given that accelerators typically aim to serve both enterprises and investors, for this

report we use the terms “impact investing” and “social enterprise” to encompass all business activ-

ity that seeks to use markets to address social problems, as well as investment strategies that proac-

tively seek social/environmental returns in addition to financial returns.

8. R. Baird, h. Hedinger, and C. Seekins, Bridging the Gap: The Role of Accelerators in Impact

Invertir. Atlanta, Georgia, EE.UU: Village Capital, 2012.

9. j. Vanderstraeten and P. Matthyssens, “Measuring the Performance of Business Incubators: A

Critical Analysis of Effectiveness Approaches and Performance Measurement Systems,” paper

published in ICSB conference proceedings, páginas. 978-0). Cincinnati: ICSB, Junio 2010; h. sherman

and D. S. Chappell, “Methodological Challenges

in Evaluating Business Incubator

Outcomes.” Economic Development Quarterly 12, No. 4 (1998): 313-321; mi. McMullan, j. j.

Chrisman, and K. Vesper, “Some Problems in Using Subjective Measures of Effectiveness to

Evaluate Entrepreneurial Assistance Programs.” Entrepreneurship Theory and Practice 26, No. 1

(2001): 37-54.

10. R. Lalkaka and J. obispo, Business Incubators in Economic Development: An Initial Assessment in

Industrializing Countries. Nueva York, Nueva York, EE.UU: United Nations Development Programme,

1996.

11. Hacket, S. METRO. & D.M. Dilts (2008). “Inside the Black Box of Business Incubation: Study B – Scale

Evaluación, Model Refinement, and Incubation Outcomes,” The Journal of Technology Transfer,

33, 439-471.

Schwartz, METRO. & METRO. Gothner (2009). “A Multidimensional Evaluation of the Effectiveness of Business

Incubators: an Application of the PROMETHEE Outranking Method,” Environment and

Planning C: Government and Policy, 27, 1072-1087.

12. Vanderstraeten and Matthyssens “Measuring the Performance of Business Incubators,” op cit.

13. A. Chandra and T. Fealey, “Business Incubation in the United States, China and Brazil: A

Comparison of Role of Government, Incubator Funding and Financial Services.” International

Journal of Entrepreneurship 13, No. 13 (2009): 67-86.

14. F. A. Khalid, D. Gilbert, A. Huq, and U. t. METRO. Melaka, “Investigating the Underlying Components

in Business Incubation Process in Malaysian ICT Incubators.” Configurations 1, No. 1 (2012); k.

Aerts, PAG. Matthyssens, and K. Vandenbempt, “Critical Role and Screening Practices of European

Business Incubators.” Technovation 27, No. 5 (2007): 254-267; j. R. Lumpkin and R. D. Irlanda,

“Screening Practices of New Business Incubators: The Evaluation of Critical Success

Factors.” American Journal of Small Business 12, No. 4 (1988): 59-81.

15. Khalid et al., “Investigating the Underlying Components”; Aerts et al., “Critical Role and

Screening Practices”; Lumpkin and Ireland, “Screening Practices of New Business Incubators.”

16. h. Haapasalo and T. Ekholm, “A Profile of European Incubators: A Framework for

Commercialising Innovations.” International Journal of Entrepreneurship and Innovation

Management 4, No. 2 (2004): 248-270.

17. R. Ferguson and C. Olofsson, “Science Parks and the Development of NTBFS: Location, Survival

and Growth.” The Journal of Technology Transfer 29, No. 1 (2004): 5-17; h. Löfsten and P.

Lindelöf, “Science Parks and the Growth of New Technology-Based Firms: Academic-Industry

Enlaces, Innovation and Markets.” Research Policy 31, No. 6 (2002): 859-876.

18. A. S. Amezcua, Boon or Boondoggle? Business Incubation as Entrepreneurship Policy. Whitman

School of Management, Syracuse University, 2010.

19. t. F. R. A. de Oliveira Are They Helping? An Examination of Business Incubators’ Impact on

Tenant Firms. Twente, Países Bajos. University of Twente, 2011.

20. Vanderstraeten and Matthyssens, “Measuring the Performance of Business Incubators,” op cit.

21. We received 37 responses for this question (71 percent of the sample).

22. Aspen Network of Development Entrepreneurs, 2012. ANDE 2012 Impact Report. Washington,

corriente continua, EE.UU. The Aspen Institute.

23. Aerts et al., “Critical Role and Screening Practices,” op cit.

24. We excluded two outliers that have 60- and 84-month engagement periods. If we include those

136