Michael Chu

Commercial Returns at the

Base of the Pyramid

More than three decades after its birth as a quixotic initiative in Latin America and

Asia to bring financial products to the poor, modern microfinance is entering the

mainstream consciousness. While its profile had been rising steadily in develop-

mental circles for half that time, a breakthrough with the public at large came with

the United Nations declaration of 2005 as the International Year of Microcredit.

This was topped last December, when the 2006 Nobel Prize for Peace was awarded

to the most visible exponents of the industry, Professor Muhammad Yunus and the

Grameen Bank. The Norwegian Nobel Committee based its decision on “their

efforts to create economic and social development from below” given that “Lasting

peace cannot be achieved unless large population groups find ways in which to

break out of poverty.” In addition, “Development from below also serves to

advance democracy and human rights.”1

As the world is introduced to microfinance as a response to global poverty,

public and private decision-makers run the risk of having their analysis of the

industry overwhelmed by the field’s stirring capability to generate social value.

Throughout the development of microfinance, the accounts of low-income men

and women in developing nations whose lives are changed by a few hundred dol-

lars of loans or savings have always tended to crowd out the income statements and

balance sheets of the institutions delivering those products and services. This is

further reinforced by the Nobel Peace Prize honoree himself, who in his acceptance

speech identified “two sources of motivation, which are mutually exclusive, Ma

equally compelling—a) maximization of profit and b) doing good to people and

the world.”2

Michael Chu is Senior Lecturer at the Harvard Business School and a Senior Partner

and Founding Partner of Pegasus Capital, a firm dedicated to deploying equity in

Latin America. Pegasus Capital’s current portfolio includes investments in consumer

retail, consumer finance, real estate and technology. Before Pegasus, as President &

CEO of ACCION International, a nonprofit corporation dedicated to microfinance,

Chu worked to develop financial services for the working poor as a new segment of

banking capable of outstanding returns. He participated in the founding of several

microcredit financial institutions and regulated banks throughout Latin America,

including Banco Solidario, one of the premier microlending institutions in the world,

which under his chairmanship has been the most profitable bank in Bolivia.

© 2007 Michael Chu

innovazioni / winter & spring 2007

115

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Michael Chu

Given these circumstances, it may be timely to subject microfinance to a series

of fundamental questions:

Is microfinance a legitimate commercial market? As an activity centered on the

base of the socioeconomic pyramid, can it sustain levels of profitability that are

comparable to those obtained at the top?

If microfinance is a commercial activity, are the poor a distinctly separate seg-

ment, or are they part of a continuous market in which relatively minor adjust-

ments to existing business models are sufficient to serve them effectively?

How has the business model of commercial microfinance evolved? Are models

at the base of the pyramid essentially stable after a “killer” concept opens the mar-

ket or is constant change the more likely pattern?

Are the key success factors of commercial microfinance generalizable across

geographical boundaries and cultures or are they location-specific?

Is commercial microfinance a contributor or a detractor in the fight against

global poverty?

MICROFINANCE AS A LEGITIMATE COMMERCIAL MARKET

Since its earliest days, the study of microfinance has been burdened by a particu-

lar complication: it is an activity centered on the poor. Di conseguenza, it is difficult for

analysts not to enter the field with preconceptions about poverty, imbuing micro-

finance with their own fears and hopes, and notions of success. In the 1970s, Quando

modern microfinance got its start, it was severely and harshly criticized by the

development community in Latin America because it advocated not only charging

interest on loans to the poor but setting them at levels calculated to cover all costs

plus inflation. The prevailing view then was that the poor needed and deserved

subsidies. Thirty plus years later, the pendulum is swinging to the other end, Dove

business at the base of the pyramid is beginning to be fashionable in vanguard cir-

cles, a sign of both smart management and advanced social responsibility. Questo

underscores the need for rigor at both ends in the analysis of microfinance (E

any other commercial approach targeting the poor). The creation of social value

should certainly not be taken at face value. Infatti, the existence of comprehensive,

longitudinal data bases at some leading microfinance institutions (MFIs) and new

thinking on social enterprise combine to pave the way for additional contributions

to the small body of impact studies that incorporate both rigor and practicality.

Nel frattempo, this article will focus on the other end of the spectrum, examining

whether or not the delivery of financial goods and services to the poor at a price

can be considered bona fide business.

At its most basic, for an activity to be part of business, it must be able to gen-

erate a revenue stream sufficient to cover all the related expenses and yield a sur-

plus. No matter how traditional or unconventional, whether practiced for millen-

nia or just a gleam in the eye of an innovator, an activity that exhibits these char-

acteristics (or seeks to have them in the future) is in the realm of business. In addi-

zione, to this static definition must be added the element of time: profitability needs

116

innovazioni / winter & spring 2007

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Commercial Returns at the Base of the Pyramid

to be sustained, to ensure that the attributes of business are not the result of a tem-

porary accident. A third element is the level of profitability: over time, the activity

must generate financial returns at least equal to the average of those with similar

risk profiles, in order to attract and retain the capital necessary to sustain it. Failing

Quello, even when revenues may exceed costs, economic rationality will dictate that

the surplus produced will migrate elsewhere, eventually causing the activity to

become unsustainable. At times, conscious decisions are made to continue with an

activity regardless of its inadequate economic performance. Accepting unprof-

itability or subprofitability as a steady state condition removes the activity from

business to other areas of human endeavor, such as social enterprise, corporate

social responsibility, philanthropy, politics or personal hobby. This is true regard-

less of the type of organization undertaking the activity. A stand-alone unprof-

itable or subprofitable line of activity that exists permanently within a large multi-

national corporation is not a business in itself.3 On the other hand, an activity

within a nonprofit charitable organization that permanently generates market lev-

els of profitability is part of the business sector, whether it likes it or not.

Although many organizations currently deploy one or another microfinance

Prodotto, whether microfinance can meet the standard of sustainable, market-level

profitability is a question to pose to a relatively small group of institutions that for

all intents and purposes define the market. As has been noted,

A rough rule of thumb in the field places the total number of entities in

the world providing some form of microfinance in the range of 7,000 A

12,000. It is probable that virtually all the significant share of any relevant

measure—size of assets, number of loans, annual growth, earnings,

financial returns—is concentrated in no more than fifty MFIs [microfi-

nance institutions]. Questo, Ancora, is typical of the development of an

industry. While there may be many entrants, the direction of the new

field is set by the handful of leaders. Accordingly, in looking at the future

of microfinance, the relevant starting point is the industry as it has been

defined by this core of leading MFIs.4

These leaders, with few exceptions, operate under general charters and statu-

tory frameworks established by the national banking or financial authorities of

their respective countries. This is irrespective of their origins. Some evolved from

NGOs that pioneered the practice, and in time changed their role from direct oper-

ators to shareholders once the financial institutions were created; others are finan-

cial institutions newly formed to enter the field. Still others are specialized sub-

sidiaries or divisions of traditional commercial banks diversifying into a new seg-

ment, and one is the reincarnation of a state-owned failing agricultural bank. Tutto

have grown rapidly, both in terms of number of clients and volume of assets, E

represent the dominant microfinance presences in their markets. This group is also

the source of the best practices in the industry in terms of market penetration,

innovation, cost efficiency, profitability and solvency.

In Latin America, a comprehensive study of microfinance estimated that out of

innovazioni / winter & spring 2007

117

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Michael Chu

Tavolo 1. Financial Returns of Microfinance and Conventional Banking in Latin

America

Sources: Marulanda, Beatriz and Otero, María. “The Profile of Microfinance in Latin America in 10

Years: Vision & Characteristics.” Boston: ACCIÓN International, April 2005; Worldscope.

RU: Regulated “Upgrading”

RD: Regulated “Downscaling”

NGO: Non Governmental Organization

Tavolo 2

Sources: Marulanda, Beatriz and Otero, María. “The Profile of Microfinance in Latin America in 10

Years: Vision & Characteristics.” Boston: ACCIÓN International, April 2005; Worldscope.

3.3 million active clients in the region in December 2004, 2.4 million or 73.3%

were accounted for by regulated banks and microfinance institutions. This concen-

tration is even higher in terms of loan portfolio. Out of an estimated $3.35 billion in loan balances outstanding at year-end 2004, the regulated entities accounted for $2.97 billion or 89%.5 The activities of these institutions and their leading NGO

colleagues take place in low-income urban neighborhoods, and some rural areas,

across the region. The loans are disbursed to merchants in open-air markets, metal

fabricators producing pots and pans from their backyards, bakers with ovens off

118

innovazioni / winter & spring 2007

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Commercial Returns at the Base of the Pyramid

Tavolo 3. Microfinance & other Finance Institutions: Bolivia

Fonte: ASOFIN

unpaved streets, weavers in adobe huts and women selling their wares by the side

of the road. Do these financing activities meet the standards of commercial busi-

ness?

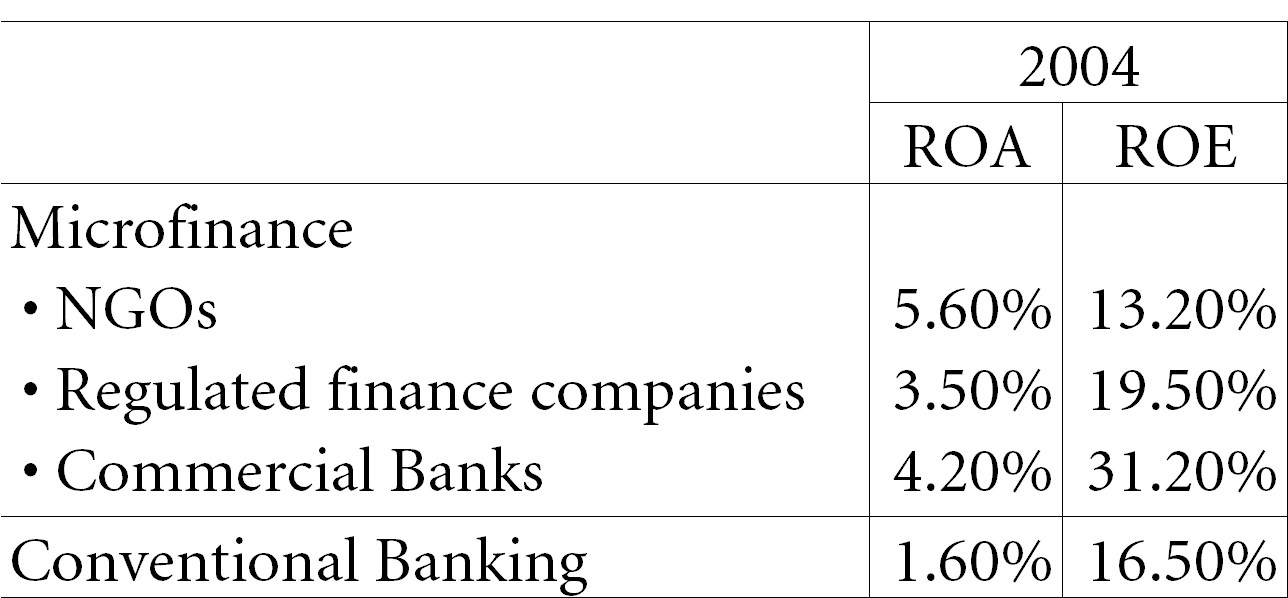

The same study reported that in 2004 non-bank regulated single-purpose

institutions in microfinance earned a return on assets (ROA) Di 3.5%, with a

return on equity (ROE) Di 19.5%. Commercial banks engaged in microfinance

earned a ROA of 4.2%, with a ROE of 31.2%. Surveyed NGOs, representing the

largest and most efficient in the region, actually showed a higher ROA of 5.6%, Ma

with less capability to assume leverage, the resulting imputed ROE6 was lower at

13.2%.7 In comparison, conventional commercial banking in Latin America in

2004 yielded an average ROA of 1.6% and a ROE of 16.5%8 (Vedi la tabella 1).

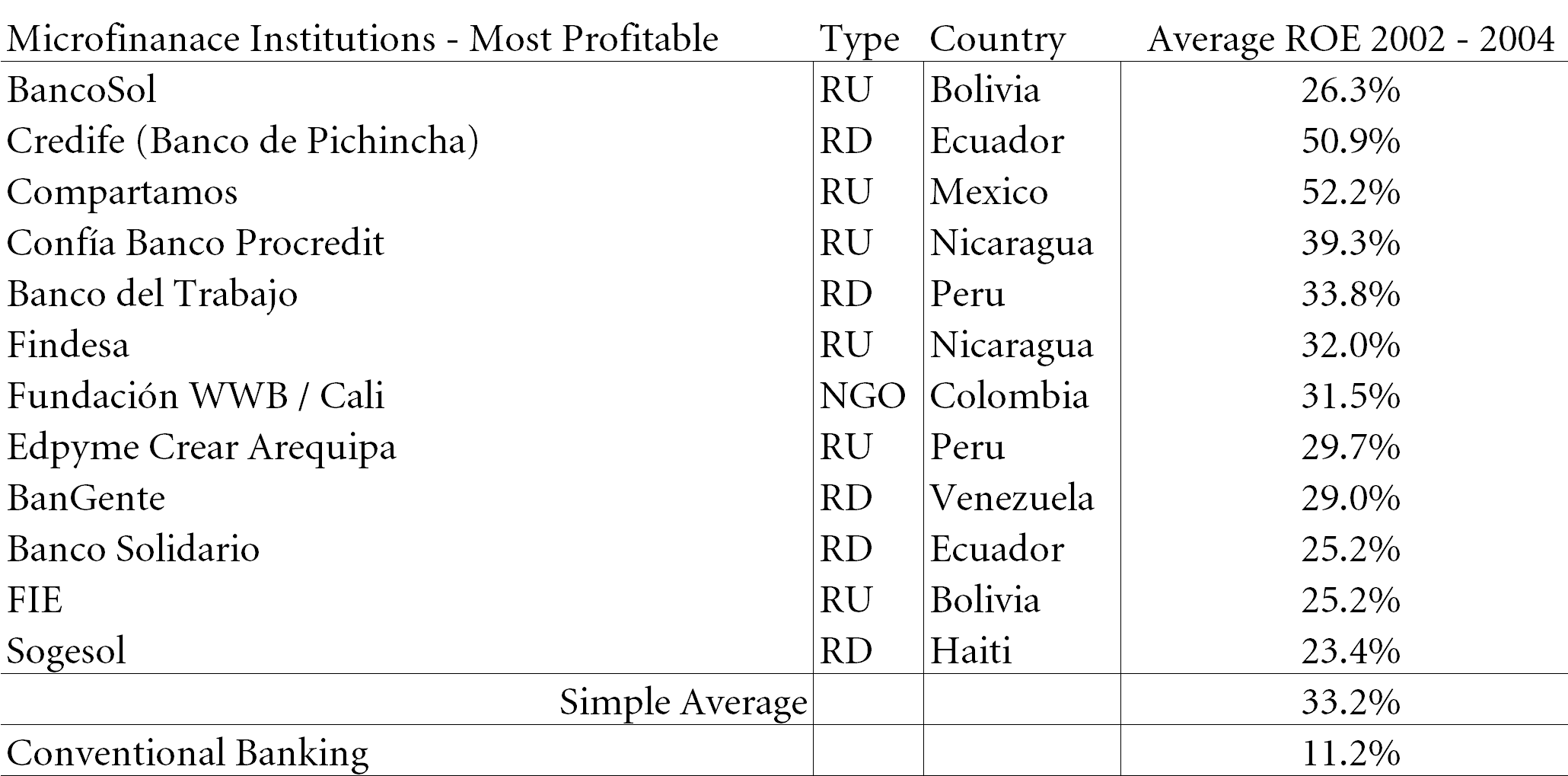

The top performers in Latin American microfinance performed substantially

better. Taking a three-year mean (2002-2004) to smooth out the results of 2004 COME

an above-average year of economic recovery for the region, Tavolo 2 shows that for

the top 12 performers, the average ROE was 33.2%9, ranging from a high of 52.2%

to a low of 23.4%.10 By contrast, the universe of commercial banks in Latin

America during this period had an average ROE of 11.2%.11 In a comprehensive

overview of microfinance in The Economist, the journal made the same point in a

table showing that, even considering a limited universe of only the microfinance

institutions rated by specialist MicroRate, In 2004 there were 17 entities with ROEs

that “outshone” Citigroup.12

Just as important, the profitability of these Latin American microfinance lead-

ers has survived the test of time. Banco Solidario S.A. of Bolivia, or BancoSol as it

is known around the world, is the first commercial bank in Latin America char-

innovazioni / winter & spring 2007

119

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Michael Chu

Tavolo 4. Microfinance & other Finance Institutions: Bolivia

Fonte: ASOFIN

tered under the regular banking laws of its country solely dedicated to the base of

the socio-economic pyramid; it has operated in the black ever since it was found-

ed in 1992. While it has had its ups and downs, particularly at the onset of the

intense competitive pressure that characterizes the Bolivian microfinance market,

BancoSol ranked among the most profitable and solvent institutions in the

Bolivian financial system, both in the late 1990s and in recent years. As of

settembre 30, 2006, BancoSol had 71,211 active clients and a loan portfolio of

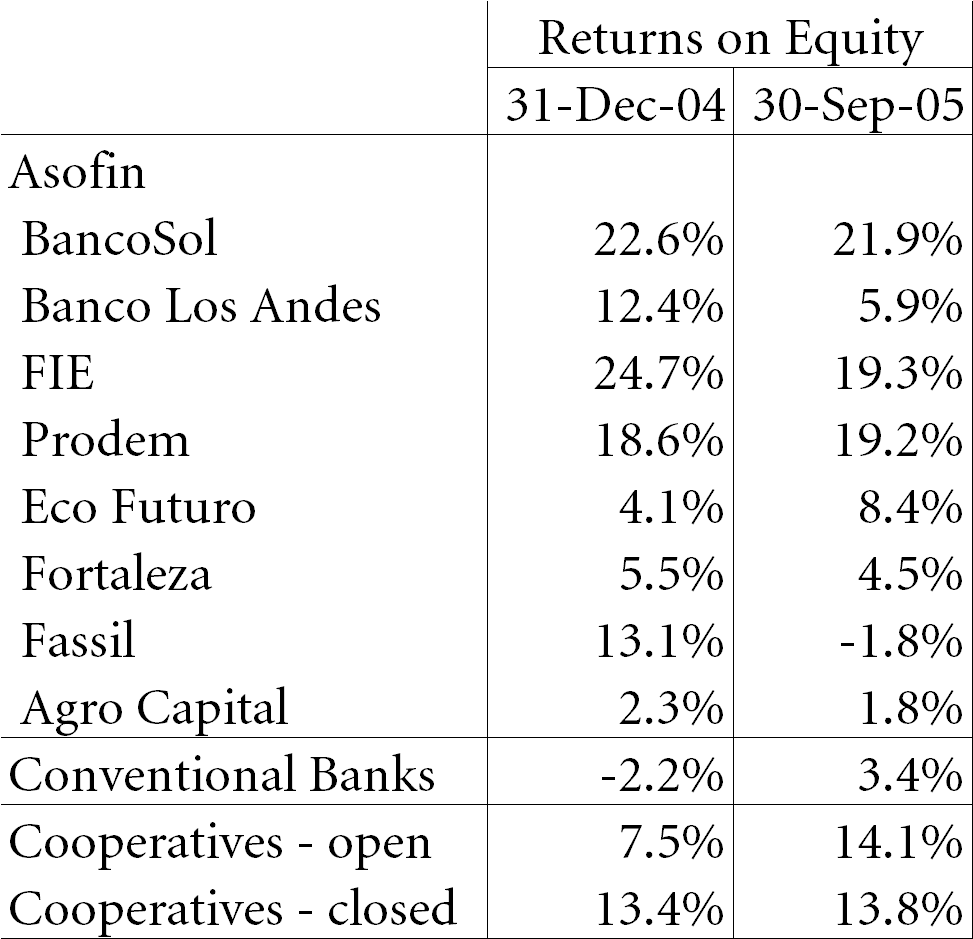

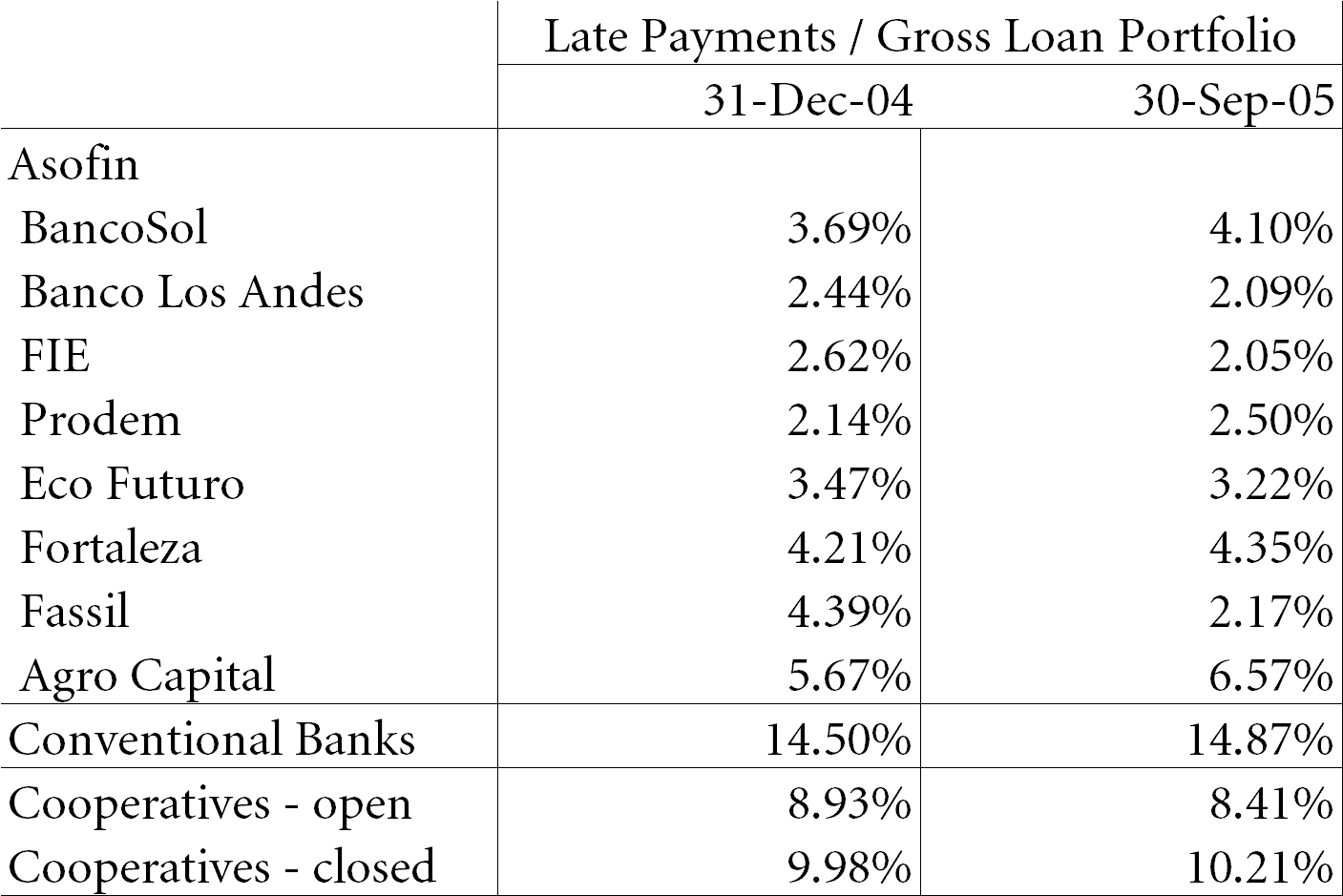

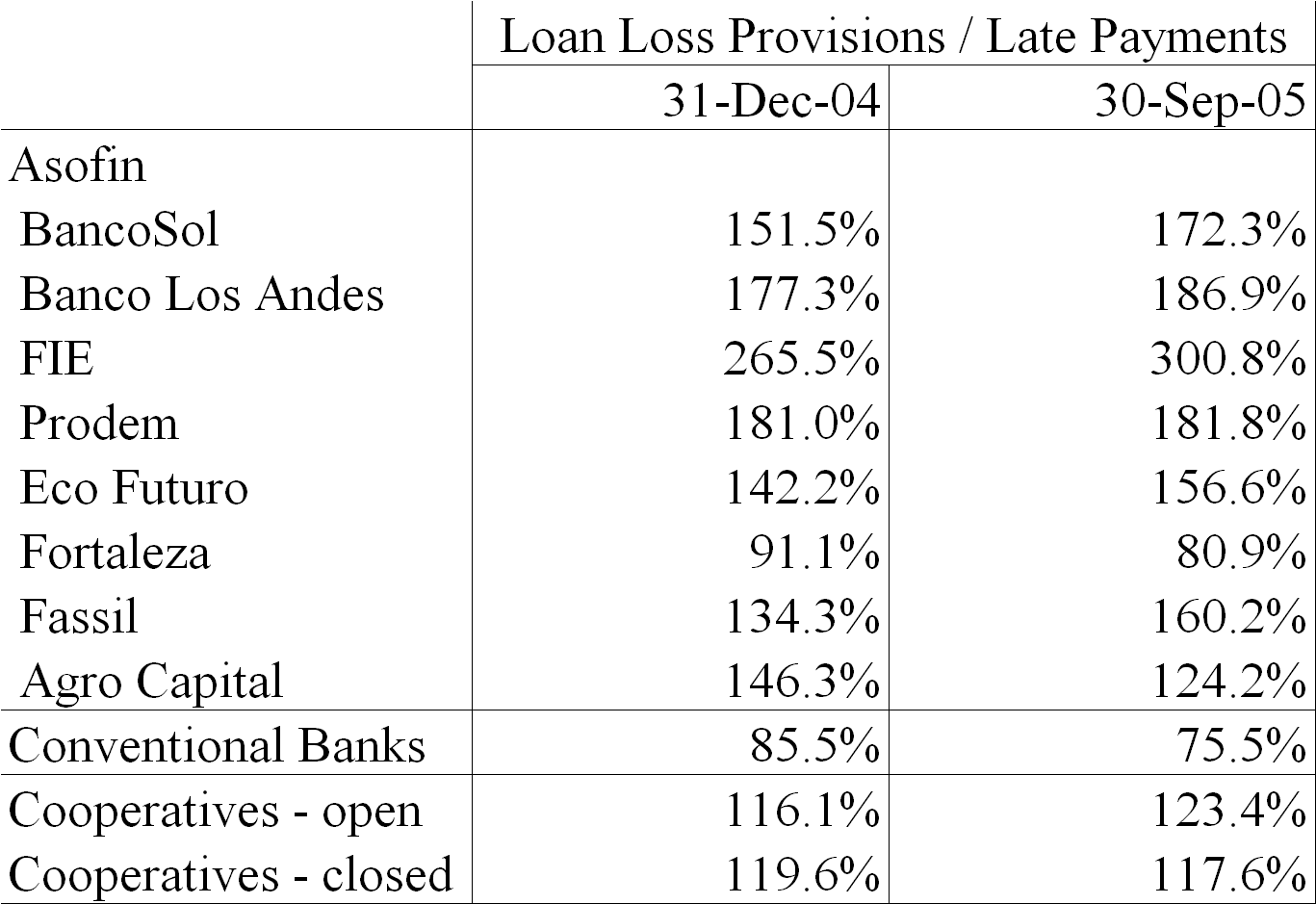

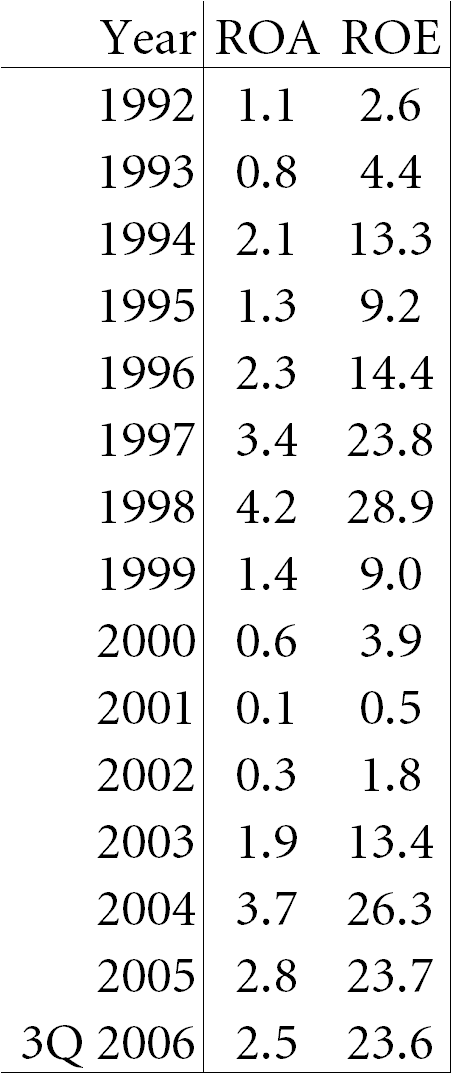

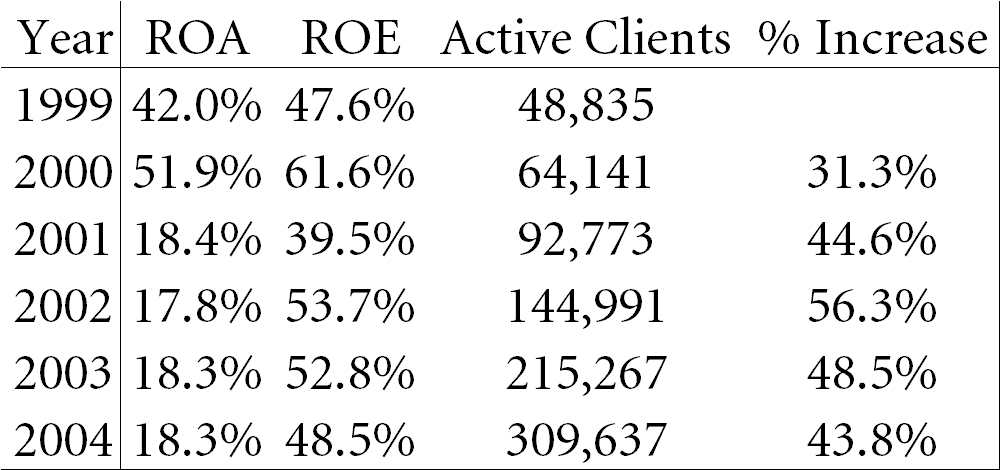

$151.7 million, and was running at a ROE rate of 23.6%.13 While BancoSol’s performance may be the most widely known, it is not an iso- lated case in Bolivia. The data compiled by ASOFIN, the industry association for regulated microfinance institutions that includes the leading industry players14 accounting for 84% of the microcredit loan portfolio of Bolivia,15 indicates that: In 2004, an extremely difficult year for Bolivia in general,16 all the ASOFIN members were profitable, with five institutions earning double-digit ROE, led by BancoSol (22.6%) and FFP (Fondo Financiero Privado) FIE (24.7%). In the same period, the conventional Bolivian banking system17 reported a loss, resulting in a negative ROE of 2.2% (Vedi la tabella 3). For the first nine months of 2005, the conventional banking system returned to profitability, with an ROE of 3.4%. While one ASOFIN member was operating in the red, three continued to earn double-digit ROEs, with the leader, BancoSol, generating an ROE 6.4 times that of conventional banking (Vedi la tabella 3). This difference in profitability was not at the expense of asset quality. The ASOFIN members, both for 2004 and the first nine months of 2005, had late pay- ment to gross loan portfolio ratios in the low single digits (from 2.05% A 6.57%), while the same ratio for conventional banking was above 14% (Vedi la tabella 4). Often, 120 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid Table 5. Microfinance & other Finance Institutions: Bolivia Source: ASOFIN the comparison between microfinance and regular banking is made difficult by potentially wide differences in the way similar financial terms are applied,18 but in this case all institutions, ASOFIN members and conventional banks alike, are reporting to the Bolivian Superintendent of Banks using uniform definitions, under a system where misreporting carries legal penalties. In arriving at the profitability and asset quality indicators above, the income statements of the ASOFIN members already reflect higher provisions for late pay- ments than those made by the conventional banks. Seven of the eight ASOFIN institutions have provided for significantly above 100% of their late payments (with one member, FFP FIE, providing for 3 times as much) compared to 85.5% for the traditional banks at year end 2004, E 75.5% at the end of September 30, 2005 (Vedi la tabella 5). By demonstrating that it can consistently generate returns supe- rior to banking at the top of the pyramid, microfinance in Latin America has grad- ually gained acceptance as a legitimate component of the business sector. Reflecting this, microfinance institutions have begun to participate directly in the in Mexico and bond markets. Two examples are Financiera Compartamos19 Mibanco in Peru.20 Financiera Compartamos, con 565,991 active clients and a loan portfolio of $219.1 million as of September 30, 2006,21 is the largest microfinance institution in

Latin America. It is among the top-earning microfinance entities in the world, con

an ROE in September 2006 Di 59.1%,22 while its client base continues to be pre-

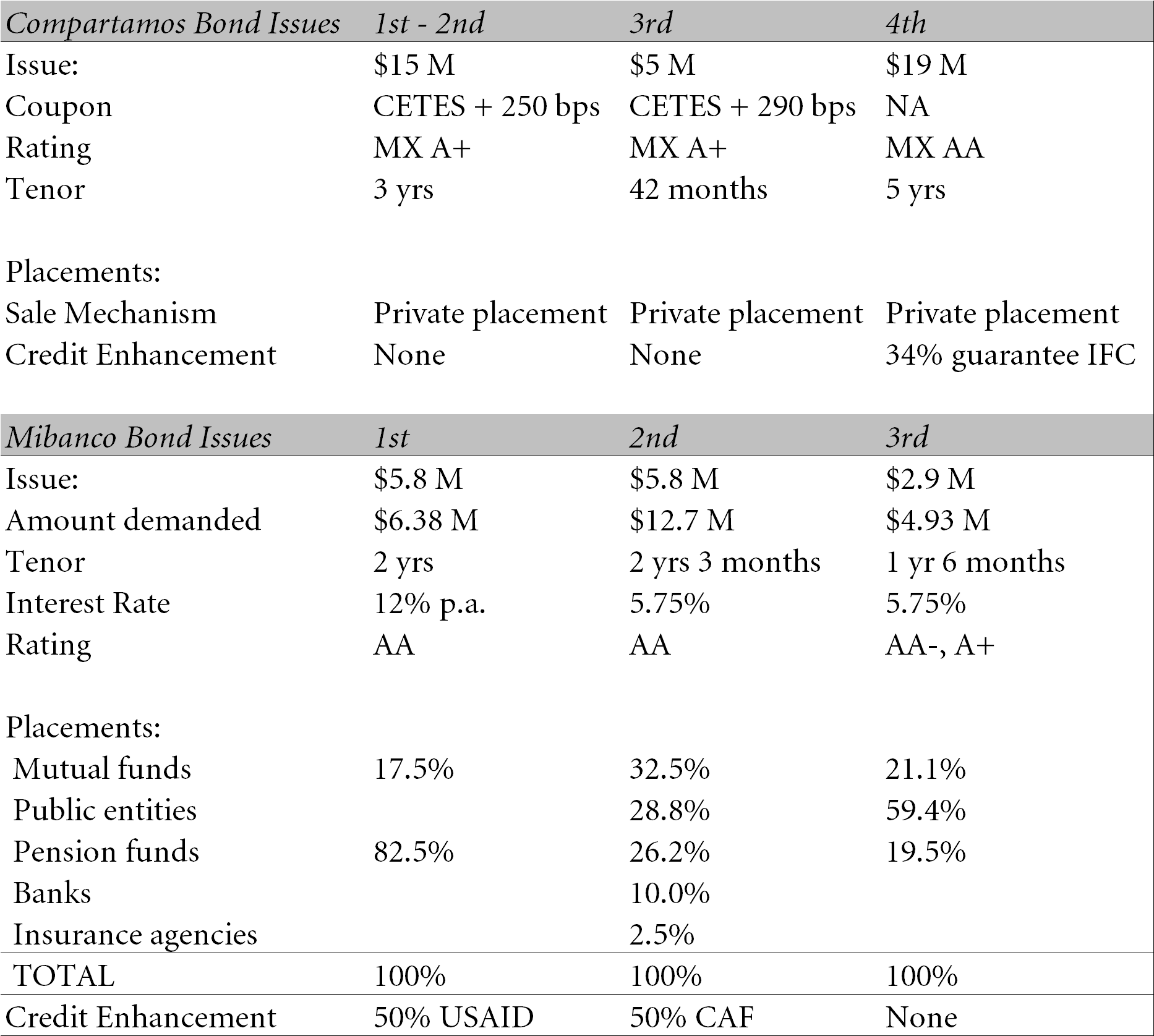

dominantly rural and its average outstanding loan is $387.23 In July 2002, Compartamos made a private placement of $15.0 million in local currency 3-year

bonds through Banamex-Citibank, at the Mexican treasury rate + 250 basis points.

Later that year, it followed with a supplemental placement of $5 million, under the innovations / winter & spring 2007 121 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu Table 6. Results of the Compartamos and Mibanco bond issues Source: Lopez, Cesar, “Microfinance approaches the bond market—the cases of Mibanco and Compartamos” in Small Enterprise Development, Vol 16, No. 1, Marzo 2005, pag. 50-56 same terms. In 2003, Compartamos entered into the market again to place $5.0

million, extending the term to 3.5 years, at a slightly higher price of the Mexican

treasury rate + 290 basis points. In 2004, Compartamos launched a $50 million bond program, with a first tranch (or portion) Di $19 million, pushing the matu-

rity to five years.

Mibanco, a commercial bank established in 1998 from the pioneering micro-

credit work of its predecessor NGO, had 207,992 active clients and a loan portfo-

lio of $281.5 million in September 30, 2006, running at a ROE rate of 33.3%.24 In the period 2002-2004, it had an average ROE of 23%, a profitability “well above the average for the Peruvian banking sector during the same period.”25 In December 2002, it issued $5.8 million in local currency 2-year corporate bonds into the

Peruvian capital markets via Dutch auction, at a fixed interest rate of 12.0%. In

settembre 2003, Mibanco issued another $5.8 million of bonds, extending the maturity to 2 years and 3 months, but at a significantly lower rate of 5.75%. A month later, it followed it with a $2.9 million issue of 18-month bonds at the same

122

innovazioni / winter & spring 2007

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Commercial Returns at the Base of the Pyramid

pricing. Tavolo 6 summarizes the bond market activity of Compartamos and

Mibanco.

From this experience, the following observations can be made:

The bond markets welcomed microfinance. In all seven instances, IL

Compartamos26 and Mibanco issues were oversubscribed. As the market got to

know the issuer, the oversubscription was significant, reaching 219% E 170% In

the last two issues of Mibanco.

The bond markets in Mexico and Peru have come to accept microfinance insti-

tutions on a stand-alone basis. Compartamos made its first three issues without

any credit enhancement at all, going to a partial 34% guarantee only when it

expanded its program to $50 million, extended the maturity of its bonds to 5 years and wanted to make sure it accessed the institutional market. Mibanco issued its first and second bonds with a 50% guarantee, but went with no credit enhance- ment in its last round, with only a marginal drop in rating and no meaningful decline in buyer interest. Buyers of microfinance bonds reflect the normal universe of the bond capital market: pension funds, mutual funds, public entities, insurance companies, e banche. The purchasers of Compartamos and Mibanco bonds did not show a par- ticular predisposition towards social issues but appear to have made their decision on purely economic grounds. The marketing efforts were conventional and includ- ed such standby as roadshows and the usual prospectuses and private placement memoranda. Traditional rating agencies, both international27 and local, are already serving microfinance. This extends a practice that began in the late 1990s, when these rat- ing services started to qualify the leading regulated microfinance institutions as part of their coverage of the banking sector.28 The goals of the two microfinance issuers were similar to those of convention- al corporate issuers (lower borrowing costs, diversify funding sources, extend maturities in the capital structure) and they amply met these objectives. For instance, Mibanco lowered its total funding costs on average by 50 basis points; Compartamos accessed debt at 450 basis points lower than the available commer- cial bank lines of credit.29 The successful experiences of Compartamos and Mibanco followed in the path of BancoSol, which issued $5 million in dollar-denominated 2-year bonds at 13%,

credit-enhanced by a 50% guarantee provided by USAID, in March 1996.

If profitability is the minimum requirement for admission into the world of

bona fide business and access to bond markets is one of its privileges, full member-

ship in the club may mean acceptance as an asset class suitable for equity invest-

ment. Various microfinance banks are, in a formal sense, public; their shares are

registered in the stock exchange of their country. An example of this is BancoSol.

But the exchanges they are listed on are so illiquid that the shares trade “by

appointment only” and in practice they remain private corporations. One notable

exception is Bank Rakyat of Indonesia, where microfinance is a major compo-

nent—and some would say the most important source of its profits. Its initial pub-

innovazioni / winter & spring 2007

123

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Michael Chu

lic offering in 2003 gave it a truly public listing.

Ancora, virtually all microfinance equity transactions, whether at founding or

later on, have been privately negotiated deals. Up to now, the major investors have

been NGOs, multilateral development organizations and governments, with some

participation by sophisticated socially-responsible private investors. These protag-

onists have acted alone and through specialized equity investment funds, whose

numbers have been growing in recent years. The first of these was formed in 1995

through an initiative headed by ACCION International, Calmeadow of Canada,

FUNDES of Switzerland and SIDI of France. This effort

raised $23 million to create Profund, a Latin American investment pool intended to demonstrate that investing in microfinance could be com- mercially viable. It was designed to run for ten years, and true to its mis- sion it sold off its last investment [in the] summer [Di 2005]. By liquidat- ing its portfolio and turning it into real cash, it became a yardstick for the investment performance of a microfinance institution.30 By November 2005, Profund had either fully realized or sold but not yet collected on the sale of all its assets.31 On that basis, its management estimated that the annu- alized internal rate of return over the ten years of the fund would be 6.61%.32 As The Economist put it, At first sight, its returns look unexciting … But on closer examination, this was a remarkable performance. All of Profund’s capital was con- tributed in dollars and then invested in local currency. In every country it operated in, its dollar returns were reduced by local currency depreci- ations, reflecting the economic chaos in much of Latin America during the decade.33 In fact, to gauge the performance of microfinance equity investing compared to conventional asset categories, a more appropriate measure is not absolute returns, but the position of Profund relative to the other equity funds deployed during the same time in the emerging markets. Applying this criterion, the IFC,34 a Profund investor, has made these calculations: • Against a widely-accepted industry benchmark of emerging markets venture capital and equity funds raised in 1995, Profund’s IRR of 6.61% placed it squarely in the top quartile. In this universe of 14 funds, the pooled mean return to investors was a loss of 0.37% and the median was a loss of 0.60%. • The lower quartile returned a negative 8.27%. • Only two other funds provided a higher return to their investors, and the top performer returned 12.16%. Profund’s accomplishment is all the more remarkable when we consider the small size of the fund, $23 million. Because of this, management costs represented a larg-

er than normal proportion of the funds under management. Profund’s IRR before

operating and financial expenses was 9.03%.35

Superior returns generated by serving the financial needs of the poor can also

124

innovazioni / winter & spring 2007

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Commercial Returns at the Base of the Pyramid

be found outside of Latin America. Perhaps the most successful microfinance insti-

tution in the world is also one of those the least known by the general public: Bank

Rakyat of Indonesia (BRI). A wholly state-owned bank until its partial privatiza-

tion in 2003, it is also the oldest bank in Indonesia, tracing its origins to 1895. In

the early 1970s, BRI developed an extensive national infrastructure reaching deep

into rural areas to deploy agrarian credit as part of Indonesia’s drive for rice self-

sufficiency. This became the framework for what today is its formidable microfi-

nance operation.36 As of June 30, 2003, BRI’s assets totaled $11.1 billion, of which $5.7 billion represented government bonds, cash and securities, E $5.3 billion was the gross loan portfolio.37 Of that, $1.6 billion was in what the bank calls its

microloan portfolio (representing 3 million loans with an average balance of

$532).38 On the other side of the balance sheet, BRI funds itself with $9.0 billion in

deposits, of which $3.0 billion is captured by its rural and urban microfinance operations in 29 million accounts.39 This base of business provided outstanding returns: for the years 2001, 2002 and the first six months of 2003, BRI had ROAs of 1.5%, 1.9% E 2.7%, yielding ROEs of 24.0%, 28.2% E 38.3%, respectively.40 With this level of financial return and the size of its operations, BRI has been able to spearhead microfinance in many ways. Mention has already been made of BRI as the first institution identified with microfinance to be publicly listed. In September 2003, it also went into the global capital markets to issue $150 million

of Subordinated Notes due in 2013.41 As in Mexico and Peru, both BRI equity and

debt issues were oversubscribed.

Financially successful microfinance institutions are also to be found in Africa

and Eastern Europe. One of them is Uganda Microfinance Limited (UMU), a local

NGO founded in August 1997 which began to break even in 2001. The following

year it reported a ROA of 4.3% and a ROE of 12.7%. In 2003, it had increased that

to a reported ROA of 12.36% and ROE of 48.4%. While returns for 2004 were not

publicly available, the level of profitability continued to be superior.42 At year-end

2003 UMU had 28,099 active borrowers and 47,529 active savers.43 In July 2005,

UMU obtained a license from the Central Bank as a Microfinance Deposit Taking

Institution and became a regulated institution. Another African example is K-Rep

Bank Limited, the first microfinance bank in Kenya, licensed in 1999. Its return on

capital employed was 7.69% In 2001, 9.89% In 2002, 11.55% In 2003 E 9.93% In

2004.44 In Eastern Europe and elsewhere, the experience of the Pro Credit banks,

the network in 14 countries connected to Internationale Projekt Consult GmbH

(IPC), has also been profitable. A recent review of the group found that “Overall,

the return on equity of the banks in the network, measured in book value terms

and weighted by the banks’ equity, is above 10 per cent.”45

Looking to capitalize on the potential of these new entities to create economic

returns based on serving the poor, several equity investment funds focused on

microfinance have followed Profund’s trail. The second one was ACCION’s

Gateway Fund, an experience that led to the creation in 2003 of ACCION

Investments in Microfinance SPC, targeted at both Latin America and Africa, E

innovazioni / winter & spring 2007

125

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Michael Chu

Tavolo 7. Average Interest Rates for Microfinance Loans in Latin America

Institutions rated by Microrate as of December 31, 2004.

Sources: ASOFIN, MicroRate

currently in the process of extending its reach globally. Another leading microfi-

nance investment fund is ProCredit-Holding AG (formerly Internationale Micro

Investitionen AG), seeking to extend the ProCredit bank network worldwide.

Others are regionally focused, such as AfriCap in Africa. Recentemente, three microfi-

nance funds have started operations in India, with eight more likely to come in the

next two years, including veteran ACCION.46

The expansion of microfinance to Africa and Eastern Europe reflects the

126

innovazioni / winter & spring 2007

Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023

Commercial Returns at the Base of the Pyramid

impact of the intellectual capital accumulated in three decades of development in

Latin America and Asia. Shaped into a body of expertise and transmitted by the

industry’s management consultants such as ACCION International, IPC,

ShoreBank and others, in just a few years it has allowed African and Eastern

European microfinance operators to achieve levels of commercial profitability that

took decades for Latin Americans and Asians to reach.47 This is particularly mean-

ingful because the field will continue, for the foreseeable future, to be mostly pop-

ulated by an overwhelming number of microfinance operations that are econom-

ically unsustainable and for whom providing financial products to the poor is not

a business enterprise but an extension of social services. Periodic shakeouts, IL

usual evolutionary mechanism through which new industries advance, are hard to

come by when donor funds, with the best of intentions, continue to play primitive

roles. Accordingly, the assurance that, regardless of geography, leaders of microfi-

nance can and will continue to meet the most stringent definitions of business is

the final guarantee that serving the financial needs of low-income people is a legit-

imate commercial market.

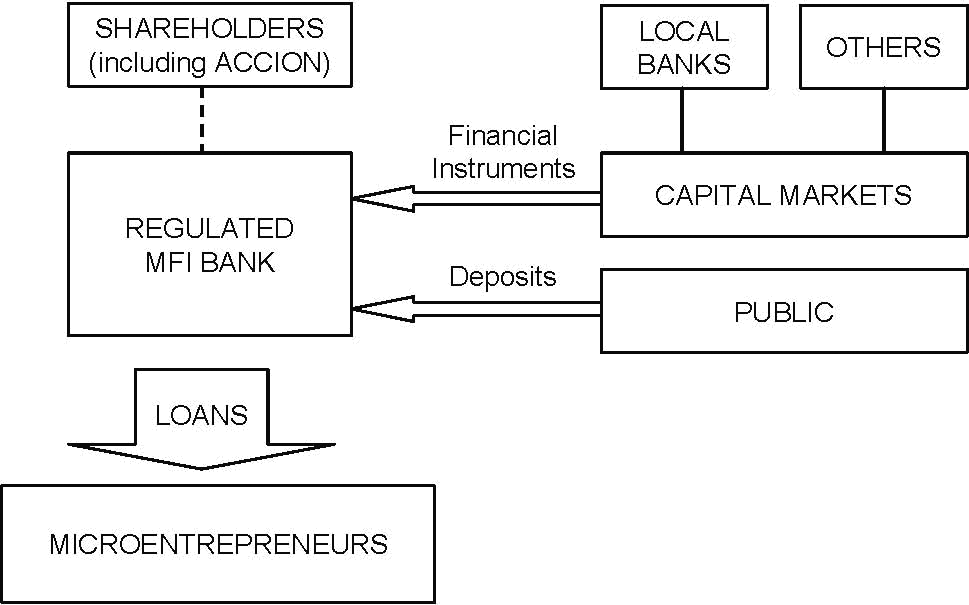

MICROFINANCE AS A SEPARATE COMMERCIAL SEGMENT

The single most important factor behind the commercial returns obtained by

microfinance has been the ability to charge prices that more than cover the

extraordinarily high costs per unit because the average size of the transaction

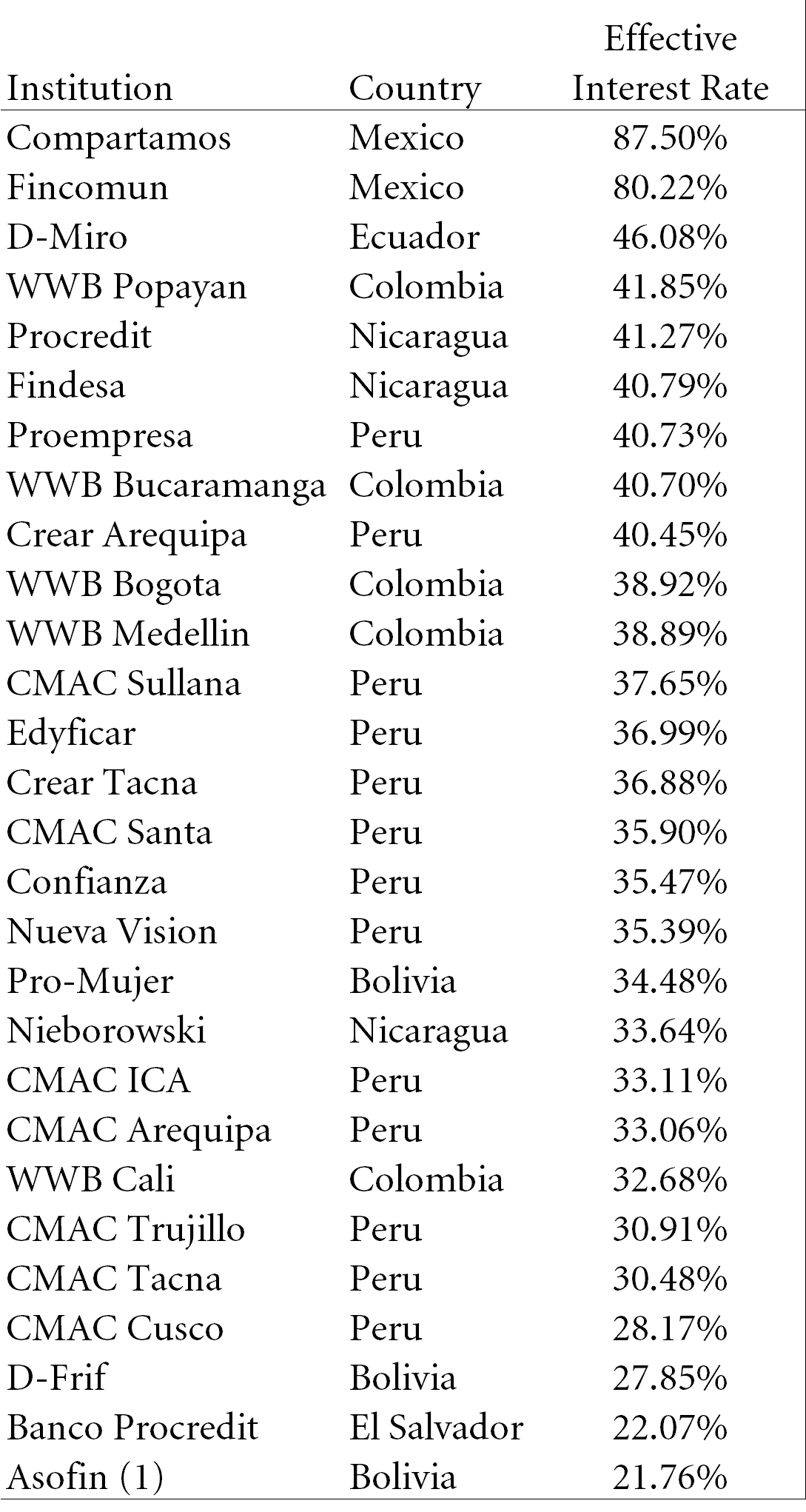

(whether credit, savings, insurance or any other product) is so small. Tavolo 7,

showing the effective annual interest rates of a handful of Latin American micro-

finance institutions rated by specialist MicroRate, drives home this point: the price

of credit for the poor in the region ranges from just over 20% to just under 90%.

Given the enormous disparity between these rates and those prevalent at the top

of the pyramid, two relevant questions are why this difference can exist and how

long it can be sustained. E, given how exorbitantly high these rates seem to be

from the perspective of the affluent, how is it that the poor can pay them?

Part of the answer lies in what I have already described. Financial services for

the poor is a retail business characterized by the smallest packaging size in the

whole market. Inoltre, although lenders continue to hone ever more efficient

methodologies, it is largely a high-contact business, requiring a level of interaction

between the MFI staff and their clients which makes it similar not to commercial

lending but to personal private banking. Both elements make the cost to serve a

microfinance product extremely high in comparison to loans placed with the more

affluent. It is not coincidental that Compartamos, the institution charging the

highest rate in Table 7, also has one of the lowest average loan sizes of any micro-

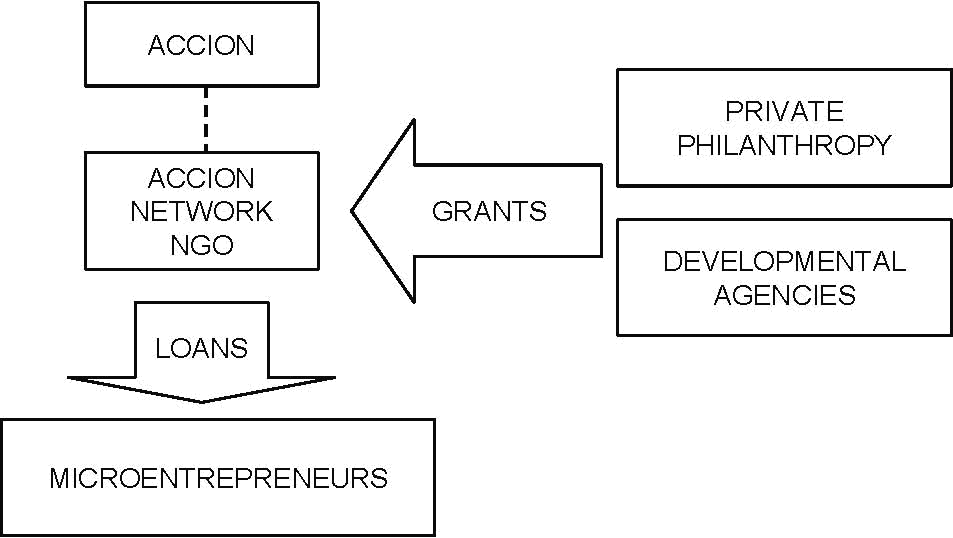

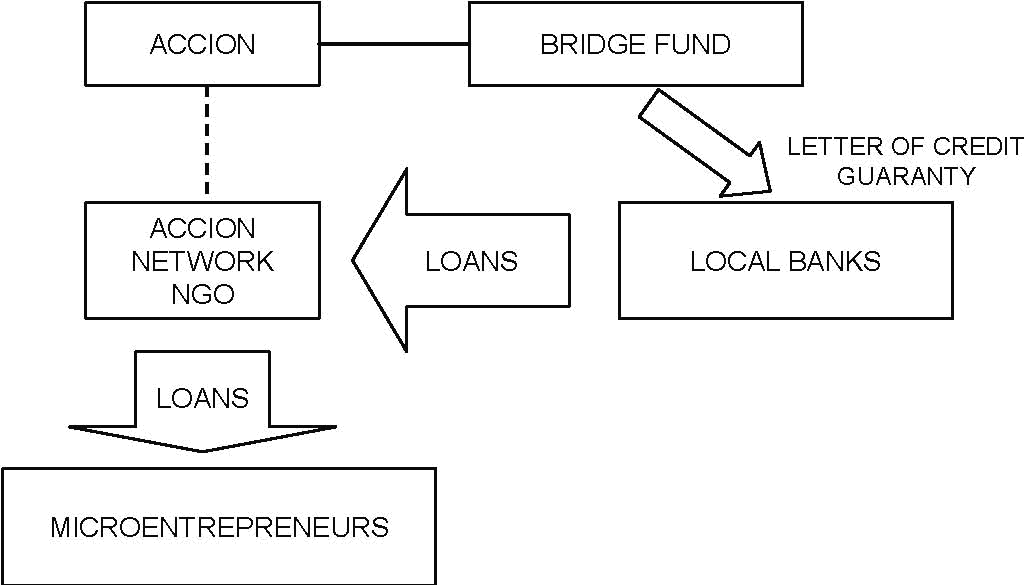

finance institution ($387 as of September 200648). The higher cost of serving the base of the pyramid has been easy for tradition- al banking to intuit and has often been the first consideration for commercial bankers when asked to approach low-income segments. Inoltre, they believed that the much higher credit risk would drive up costs further and, to top it off, the innovations / winter & spring 2007 127 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu underlying asset pool was too small to make the effort worthwhile. Other serious challenges, such as the need for different personnel profiles, compensation plans and skill sets, are usually less clear at the outset. All these obstacles have some base in reality, and helped explain why microfinance did not evolve naturally from the established financial system. Yet, with the benefit of hindsight, we see the key insight that banking strategists missed — and thus missed seeing as potential cus- tomers the low-income populations they co-existed with for hundreds of years — was that the pricing paid by the people at the base of the socio-economic pyramid bears little relation to that paid by the inhabitants at the top. So long as the ques- tion was posed as how to meet the higher costs of serving the base with the prices paid at the top, banking for the poor remained a dilemma without a solution. Because it could not be solved, the poor had no other recourse than to pay the prices set by those among them with surplus funds: the local moneylender and the very last link of the distribution chain. The rates charged on the streets for money in this “informal” financial system have been widely documented. Since the rates far surpass any prevailing inflation or devaluation, they share a commonality across the Third World that transcends geography. The range within a given city, town or neighborhood is extremely wide as there is no accepted standard format, and loans can have daily, weekly or monthly repayments calculated on a wide variety of bases, making the calculation of effective annual rates a challenge for even the most quantitative MBA.49 From the Andes to Zambia, interest rates for the poor can range from 5% a week to 30% a month, with cases of 100% a month and more also recorded. This translates into rates per annum of 1,100% A 2,200%, and higher. But on the streets, empirical observation of the poor indicates that the bottleneck is not the search for new clients but the capital base of the moneylenders. Despite the dramatic growth of the leading microfinance institutions, the market still belongs to the informal moneylenders. How can the poor afford to pay such prices? The poor have three fundamental reasons why it makes sense to pay the going rates on the street. Primo, street loans are extremely short in duration, thus limiting the compounding effect of the high interest rates. An effective annual interest rate in excess of 1,000% may translate to a $1.50 charge for $100 lent for two days, an amount payable by a woman who has invested the $100 in shirts sold for $110 over the same two days. Secondo, financial costs are only one component of the total costs incurred by the borrower. This seminal insight helped lay the foundation for commercial microfinance in Latin America, as it permitted microfinance pioneer ACCION International to understand why the interest rate on loans was often not the most important consideration for the clients it was seeking to serve. In 1989, ACCION laid this lesson out in a publication aptly entitled “What Microenterprise Credit Programs Can Learn from the Moneylenders.”50 In it, in addition to direct financial costs, it defined two others: transaction costs, the indirect costs (such as financial and legal documentation) that lenders impose as a result of their delivery systems but which add no value to the borrower; and accessibility costs, the business oppor- 128 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid tunities lost because of the inefficiencies in the credit delivery system (e.g. missing delivery of a shipment of shirts or losing a machine sold to others). The author then compared two alternative funding sources from the perspective of a borrow- er: a local moneylender with a $200 loan for 60 days at 10% a month and a credit

union charging 2% a month but requiring compensating balances, and four trips

back and forth to its offices to process, receive and then service the loan. Factoring

in some paperwork delays in line with current practice, the author demonstrated

that for the borrower, the cost of the moneylender is $40 (the direct financial costs and no transaction or accessibility costs, as disbursement is immediate and repay- ment is collected at the borrower’s location) versus $96 for the credit union, Di

which just $10 is the direct financial cost.51 Only when ACCION understood this could it realize that transaction and accessibility costs directly affected the toler- ance for high interest rates at the base of the pyramid, and that it was completely rational for its clients to trade off one against the other. High interest rates were sustainable if efficiency and reliability were guaranteed. While simple once understood, this insight was a great breakthrough because it was absolutely contrary to the mindset of the professionals engaged in microfi- nance, who invariably came from the top of the pyramid. There, the financial sys- tem on one hand and the clients on the other have been working literally for cen- turies to minimize and absorb transaction and accessibility costs. These have either been driven down to minimal levels (e.g. the density of branches and ATMs in high-income districts) or fully absorbed and standardized as the costs of doing business (e.g. lawyers, credit agreements, perfection of security). Hence, they are mostly taken for granted, with the result that attention is drawn to the one remain- ing dimension: interest rates. This explains why the level of interest rates has always been more controversial at international development conferences than at the base of the pyramid. The third factor that allows low-income people to absorb high interest rates is the high marginal productivity of capital where capital is so scarce. When an elec- tric saw is introduced to a carpenter making furniture with a hammer, nails and a handsaw in his one-room dwelling, his productivity increases not by 20 O 30%, but by various orders of magnitude. D'altra parte, when one more electric saw is introduced in a furniture factory running various production lines fully equipped with electric saws, the increase in productivity may be barely noticeable. This was another insight that ACCION acquired in the field: The smaller the microbusiness, the greater the return to assets … A … study conducted among 320 of the smallest businesses in 40 poor neighborhoods that participate in [an] ACCION affiliated program … demonstrated their capacity to generate returns. For businesses with an average US $833 in total

assets, the gross return on assets was 700 percent annually… A similar study of

small commerce in La Paz, Bolivia … revealed gross rates of return of over 100

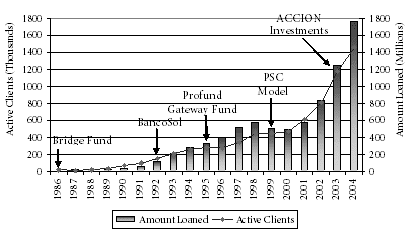

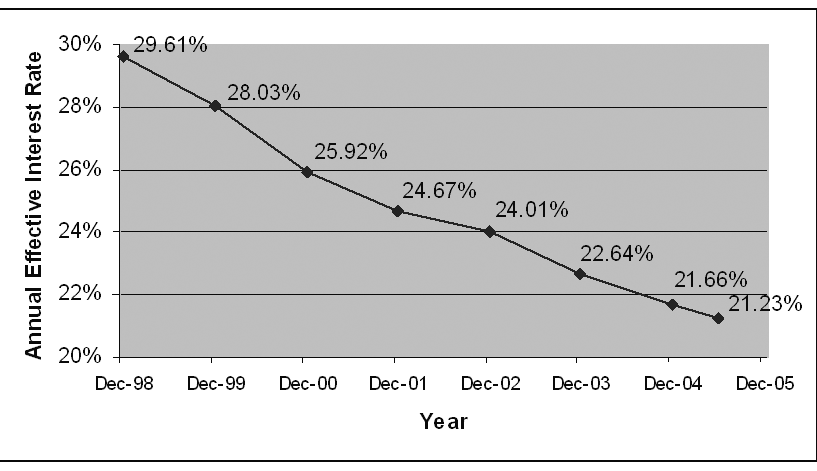

percent a year for businesses with an average of $545 in assets. Rates of return for the very smallest approached 3,000 percent annually.52 Revisiting the basic conceptual breakthroughs that made commercial microfi- innovazioni / winter & spring 2007 129 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu nance possible highlights the deep differences that separate the top from the bot- tom of the pyramid. A lesson from that experience is that commercial success in serving the poor must start with a fundamental understanding of the day-to-day realities of low-income lives. Most, if not all, protagonists who come from outside that world are likely to carry deeply ingrained assumptions into the base of the pyramid without realizing their inappropriateness when dealing with the poor. Accordingly, theory-down approaches have a dismal record in the history of microfinance; successes have always flowed street-up. In that process, initiatives driven by commercial considerations seem to have an advantage. Unlike philan- thropy, which can measure itself on quality alone, given the small unit value of the products for the poor, commercial initiatives cannot succeed without engaging siz- able numbers of the target population. That success, in turn, cannot be maintained long-term without responding effectively to the key needs of the people at the base of the pyramid, whether these needs have been understood from the start or had to be discovered in the crucible of the marketplace. THE EVOLUTION OF COMMERCIAL MICROFINANCE In an overview of the microfinance industry, The Economist noted the current strong interest in microfinance and then reflected that “What is now generating so much hope and excitement is less the discovery of some entirely new way to deliv- er financial services to the poor than the effect of the rapid innovation that has taken place in the past three decades.”53 Indeed, for practitioners in the field, dynamic change has been a constant and that characteristic may be a key difference between microfinance and other initiatives aimed at alleviating global poverty. The distance traveled by microfinance can be gauged by looking at its history in Latin America, where arguably the greatest transformation has taken place—from its birth as a tentative experiment by fledgling NGOs to the current involvement of established local and international commercial banks. How quickly this evolution has occurred is demonstrated by one fact: all these changes have taken place in less than the span of a person’s career. Many of today’s key protagonists actively driv- ing the entry of conventional banking into microfinance were involved with NGOs and civil society organizations when they were launching their first microlending operations—and these people still have plenty of productive years left. Why has innovation been so prevalent in microfinance? What does it have to teach us about commercial models serving the poor? Modern microfinance began in the early 1970s in both Latin America and Asia. In 1973 In 1971, Opportunity International started lending in Colombia;54 ACCION International issued its first microcredit loan in Recife, a poor area of Brazil. In 1970, an entrepreneur established Bank Dagang Bali in Indonesia to lend to and capture savings from people who had no access to the financial system; In 1976 Yunus began experimenting in Bangladesh. None of these early pioneers knew each other nor did they realize the scope of what they were unleashing. In Latin America, the evolution of commercial microfinance is reflected in the 130 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid Figure 1. Seeking Economic Viability (1973-1985) history of ACCION, founded as a nonprofit in 1961. During its first 12 years, ACCION mobilized young men and women from the U.S. and Europe to work among the low-income populations of Latin America. Soon after its initial micro- credit experience in Brazil, ACCION focused entirely on microfinance as the means to fulfill its mission of combating global poverty. ACCION’s key contribu- tions to the creation of commercial microfinance can be summarized in four inno- vations: Seeking Economic Viability (1973-1985): Given the radical departure from con- vention that at the time characterized providing financial services to the poor, microfinance began as the exclusive province of NGOs. While ACCION itself was a nonprofit, from inception it believed in a model that could be financially self-suf- ficient, covering all expenses and generating a surplus from the income of the loan portfolio. As previously noted, this ran counter to the accepted views in develop- ment circles. ACCION proceeded to co-found various local NGOs with business leaders as champions. These, together with the few existing NGOs that bought into the ACCION concept, became the ACCION Network. A decade of intense experi- mentation followed. By the mid 1980s, the leading NGOs had managed to crack the problem and cross breakeven. During this period, the funding for the operat- ing costs and the loan portfolio came from philanthropy and bilateral and multi- lateral development agencies (Guarda la figura 1). Connecting with the Banking System (1985-1990): Once ACCION attained breakeven, scale ceased to be a challenge and became an ally. As the institutions began to meet the market demand, the bottleneck changed from enough donor sources to cover operating deficits to accessing pools of capital large enough to fuel the growth of operations. While economically-viable NGOs could now potential- innovazioni / winter & spring 2007 131 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu Figure 2. Connecting with the Banking System (1985-1990) Figura 3. Becoming Regulated Microfinance Institutions (1992 SU) ly borrow on a corporate basis, the challenge became to link them with the local banking systems. To do this, In 1986 ACCION established the Bridge Fund, a guar- antee fund made up of assets solicited from foundations and socially responsible investors which it used as collateral for a program of letters of credit (L/C) from first-tier global banks. It then used these L/Cs to guarantee credit lines extended by local banks to ACCION-affiliated microcredit NGOs. The guarantee was never for the full risk. Typically, it might start at 90%. This provided local banks with an extremely attractive economic proposition: receiving 100% of the interest, while 132 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid Figure 4. Creating the Private Service Company Model (1992 SU) incurring only 10% of the risk. As the Bridge Fund enabled the connection to the local banking system, the loan portfolios grew dramatically. As the banks got to know the microfinance NGOs, their stellar performance allowed for a higher and higher leverage on the L/Cs, until these disappeared altogether (Guarda la figura 2). Becoming Regulated Microfinance Institutions (1992 SU): Effective as the Bridge Fund was in relieving the funding bottleneck for the successful microfinance NGOs, the sustained growth quickly exhausted the ability of the local banking sys- tem to serve the NGOs as corporate clients. This situation was the result of two fac- tori. While the NGOs were excellent clients, they had no hard collateral, as their main asset remained IOUs from the base of the pyramid. Without hard assets and operating under prevailing regulations, the local banks had to limit what they could lend to a single customer on an unsecured basis. Inoltre, the banks had to provision the loan (regardless of performance), making the cost prohibitive. ACCION concluded that the only way the successful NGOs could continue grow- ing past that obstacle was to bypass the intermediary step and become banks (or regulated financial companies) themselves. The first of these “transformations” was BancoSol in 1992. The funding model gained in efficiency and power (Guarda la figura 3). Creating the Private Service Company Model (1999 SU): While the conversion of successful microfinance NGOs into regulated financial institutions was highly suc- cessful in opening another stage of high growth, the costs of such a process were also high in terms of time and financial and human resources. Simultaneously, conventional commercial banks had become aware of the financial attractiveness of serving clients at the base of the pyramid. As they began to explore how to do this, many concluded that they lacked the proper expertise. This led ACCION to innovations / winter & spring 2007 133 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu design a model in which it established joint ventures with commercial banks. The joint venture takes on all contact with the microfinance market, from marketing the product through making the credit decision to collecting the payments. To do this, the joint venture recruits, trains and manages its own staff. But when it issues a loan, the loan is carried not on the balance sheet of the joint venture but on the books of the bank. This is a highly efficient model as it redefines two key levers: finanziamenti, which now benefits from the volume and the cost of a much larger com- mercial bank; and back-office operations, eliminating the need to establish a new stand-alone processing center for microfinance (see Figure 4). The first of these joint ventures was established in 1999 with Banco Pichincha, the largest Ecuadorian bank, under the name of Credife. It has since been followed by SogeSol (2000), a joint venture with Sogebank, the largest bank in Haiti, and by RealMicrocredito (2003), a joint venture with Banco Real, the ABN-AMRO bank in Brazil. Through this model, ACCION has helped conventional banks move into microfinance. Allo stesso tempo, the efficiency of the model is resulting in levels of return significantly superior55 to those of the average regulated microfinance insti- tutions in the ACCION Network, which include many of the most profitable enti- ties in the industry.56 Consistently producing radical innovations within one organization over three decades requires a constant questioning from the inside of the very models that have brought the institution success and acclaim. While no doubt this is attribut- able to more than one factor, it is notable that a principal driver of all the innova- tions at ACCION has been the urgent search for ways to break the bottlenecks to growth and efficiency. Another example of innovation driven by the same motiva- tions is the current greenfields model developed by IPC of ProCredit banks creat- ed from scratch, wholly-owned or controlled by one single entity, extending economies of scale and knowledge over national borders. Since growth and effi- ciency are natural outgrowths of a commercial concept but not necessarily of oth- ers, a question arises: would such innovations have occurred under a different view of microfinance? The model may help explain why, over the last three decades, the introduction of new concepts—after the original innovations responsible for founding organizations—have come overwhelmingly from those institutions most committed to commercial microfinance. This link between innovation and com- mercial approaches can perhaps be extended to the entire field of business at the base of the pyramid. A second observation derived from the evolution of microfinance is that low- income markets are currently so underserved that no killer concept that manages to open the field, even to great success, is likely to last for long without challenge. In the history of the ACCION Network recounted above, the NGOs responsible for the methodologies that resulted in breakeven, fundamental as that step was, have all ceased to be at the head of the industry. Some have remained in the field as bou- tique players, well-run operations that no longer seek to grow exponentially; oth- ers have contributed their operations to a new organizational form with stronger financial and operating capabilities and turned to new social or developmental 134 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid activities. The same evolution can be seen in all the products, delivery systems and infra- structure that at one time or another had been deemed to be the cutting edge. A consequence of tapping into the majority of the population is that the market in number of clients is so much larger that rapid growth can be sustained for far longer periods than previously conceived. Such continued waves of growth will constantly render obsolete all concepts and systems. Infatti, despite its explosive growth in the last decade, microfinance continues to be a high-margin, low-vol- ume (in relation to total market) business. Yet its end-state will be as a low-margin high-volume business, with the concept of market size recalibrated to take into account not a portion but the whole of humankind.57 THE KEY FACTORS OF SUCCESS That commercial microfinance can succeed in every major region of the Third World, under the most varied cultures, ethnicities and religions, and within a spec- trum of political circumstances, suggests the existence of a set of factors so funda- mental that it cuts across all these dimensions. While it is not within the parame- ters of this article to address this issue in detail, I suggest that five characteristics, based on my experience as a practitioner, are present in successful microfinance institutions:58 Pricing is set by market forces alone. In these cases, pricing reflects all costs relat- ed to microfinance and, at least for the most efficient operator in the market, a return commensurate to the risks of the business. Experience indicates that when interest rates for microfinance loans are capped, credit is forced inexorably towards larger initial loan sizes. This happens because institutions cannot afford to wait for interest income to achieve breakeven solely on the growth of the average balance of the loan portfolio because their clients’ enterprises are succeeding. This is sig- nificant, as initial loan size is an indicator of the socio-economic outreach of a microfinance program: the lower it is, the poorer the population reached.59 One way to get around the drift towards higher initial loans is through subsidy, in effect capping the interest rate for the borrower but not for the lender. Tuttavia, history shows that when the end-borrower’s rates are below market, sometimes even lower than the prevailing inflation rate, so much value is embedded in the mere fact of receiving the loan that it is difficult to protect disbursement from political inter- ference or fraud. Contrary to popular belief, the effective result of both interest rate caps and subsidies is the perverse transfer of capital away from the base and towards the top of the pyramid. Client selection is at the sole discretion of the microfinance institution and the cri- teria used are entirely economic. This does not mean that the lender shies away from risk but that it only disburses funds when it has in place procedures and systems that can manage that risk appropriately. It also means that loans are disbursed only to borrowers who can repay. This helps to confine microfinance loans to those who can benefit from contracting debt—men and women who have an income stream innovations / winter & spring 2007 135 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu that will support repayment, especially if that income stream will increase as a result of the loan. It is no favor for the poor to end up saddled with debt obliga- tions which they cannot repay, the unintended but disastrous consequences of poorly executed microfinance. Risk is borne entirely by the microfinance institution. There are no mechanisms to insulate the lender from the full consequences of its decisions. There are no grants to cover operating deficits or to make up negative net worth. Guarantees such as those backing the bonds issued by BancoSol, Mibanco and Compartamos do not violate this provision so long as the credit enhancement is provided on a commercial, arms-length basis. Shareholders, even those with deep pockets, respond only to the extent that it makes sense commercially. Microfinance is the sole business focus. The attention and energy of the entire organization is devoted to microfinance and is not diluted by other activities that require different success factors and skill sets. A corollary is that the careers of the people involved rise or fall with the microfinance operations. In the case of con- ventional banks, this must be made to apply to the unit within the bank that deploys microfinance, especially difficult as the microfinance segment is so differ- ent from the rest of the institution. It is precisely the ability to do this that consti- tutes one of the main attractions for conventional banks of ACCION’s “private service company” model. Long-term survival of the business unit is critically affected by the returns of microfinance. This is true regardless of successful activity in other areas, such as fulfilling social goals or contributing positively to corporate objectives such as image and brand name. These five factors alone do not guarantee the success of a microfinance insti- tution. Infatti, all the usual requirements of a successful business also need to be in place: strong management and sound business model; robust control, account- ing and information systems; well-aligned promotion and compensation policies; great products and good customer service, and so on. But the absence of even one of the five considerations identified above weakens the chances of the microfi- nance project succeeding. This may explain why microfinance has not yet taken off in China despite a multitude of pilot projects and why it is beginning to do so in India today. In any other commercial enterprise, the five factors would be so basic as to make their enumeration clearly redundant. Yet because it is a business serv- ing the poor, this perspective of microfinance has caused controversy in the past and may still continue to do so for some time. COMMERCIAL RETURNS AND GLOBAL POVERTY Succeeding as a business ultimately brings microfinance back to the question posed by Professor Yunus in Oslo: are profits and creating social value mutually exclusive? After all, every cent of the net incomes and the ROAs and ROEs in microfinance is earned off the sweat of hard-working low-income men and women. While interest rates may not be the only factor that matters to the poor 136 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid when they borrow, they remain a major element of cost and it is difficult to ignore the fact that some of the institutions earning the highest financial returns are also those charging the highest rates. At the top of the socioeconomic pyramid, relying on the market to determine pricing may make perfect sense, but should this be extended to the base? Even if market forces will eventually bring the price down, in poor communities the elapsed time is measured not in pleasures deferred but in hardships suffered and life chances lost. To answer this, it is relevant to examine why the bulk of humanitarian respons- es to poverty alleviate its effects while failing to significantly reduce it. As Sisyphus found, the task becomes eternal, with the final goal always out of reach. Di conseguenza, the greatest victories against poverty come not from the concerted efforts aimed against it but as byproducts of high macroeconomic growth sustained for long periods, as in post-war Europe, the last 25 years in China and, more recently, in India. To actually win against poverty requires interventions that can simultaneous- ly deliver four attributes. The first is the ability to reach large numbers. The need for scale is determined by the enormity of the problem. As Jim Wolfenson said dur- ing his tenure as President of the World Bank, “across the world, 1.3 billion people live on less than one dollar a day; 3 billion live on under two dollars a day; 1.3 bil- lion have no access to clean water; 3 billion have no access to sanitation; 2 billion have no access to electricity.”60 In this context, no matter how effective an initiative is by itself in changing poverty, it will matter little if it fails to reach sufficient num- bers to make a difference in the aggregate. To reach hundreds, thousands, or hun- dreds of thousands, key as that may be to those involved, remains only a small skir- mish in the total war. The second attribute is the ability to sustain an intervention across genera- zioni. Poverty is so entrenched and complex that no solution can be expected to succeed in the span of just one lifetime. The third attribute is efficacy: constantly testing, improving, pruning, and culling interventions to weed out the less effec- tive and replace them with better models. The fourth is efficiency, as the enormity of the problem makes any amount of resources that can be marshaled seem puny in comparison. A key reason why poverty is intractable is that none of the major protagonists whose traditional role is to fight it are structurally suited to deliver these four attributes. When NGOs and philanthropy (public or private) are at their best, their collaboration gives birth to powerful ideas that may change the world. Philanthropic resources then help those ideas take their first steps. Developmental agents, such as bilateral aid agencies, the multilateral regional development banks and the World Bank itself, also when they are at their best, recognize these high- impact ideas and become the resource platform that can turn them into pilot pro- grams. But neither philanthropy nor development agencies are structurally designed to guarantee either scale or sustainability. Aware of these limitations, they have traditionally sought to partner with the state. Governments, despite shifting political priorities and budgetary constraints, can sometimes deliver massive reach innovations / winter & spring 2007 137 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu Figure 5. Impact of Commercial Microfinance Source: ACCION International and permanence. Tuttavia, experience indicates that the public sector, for diverse reasons, faces enormous challenges in delivering efficacy and efficiency. Through the ages, one actor has proven consistently able to attain the attrib- utes of scale, permanence, efficacy and efficiency: business. Unfortunately for the fight against poverty, it has also been the protagonist that traditionally has stood by the sideline. Business delivers these four attributes not through a particular company or firm; business enterprises, even giant ones, come and go. It does so because the natural outcome of a profitable venture is the creation of an industry that, year in and year out, stands ready to respond to the needs of its market. The innovative breakthrough of microfinance as a response to poverty lies in having harnessed that unique power of business to propel activities that can change the lives of the men and women in the low-income sectors of the world’s population. The impact of this power is clearly illustrated in the history of the ACCION Network.61 Figure 5 shows its evolution since 1986 in terms of annual loan dis- bursements and the number of active clients at year-end. On this chart, the estab- lishment of the Bridge Fund (1986) marks the point where the Network, then comprised of NGOs, connected to the local banking sector. BancoSol, established in 1992, was the first regulated commercial bank focused solely on microfinance. Profund and Gateway (1995) identifies the creation of equity investment funds in microfinance. The private service company (PSC) model bringing in convention- al banks as partners was introduced in 1999. ACCION Investments, the successor to the Gateway Fund, was capitalized in 2003. Accordingly, the chart tracks the effect of linking microfinance to the capital markets, first indirectly as a corporate client of banks (1986-1992) and subsequently, as an integral part of the financial system, with ever-wider access to capital markets. While Figure 5 omits the prior 138 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid Figure 6. Average Microfinance Interest Rate, Bolivia, 1998-2005 Fonte: ASOFIN 13 years of microfinance activity (1973-1986), a key stage that led to achieving commercial breakeven, the volume attained by the Network in loans and active clients would have barely registered on the chart. Connecting to the local banks in 1986 allowed the network to increase active clients from 18,000 to almost 100,000 and to lend $100 million, but the real jump comes after connecting directly to the

capital markets, enabling the ACCION Network in 2006 to reach 2.4 million active

clients and disburse $3.3 billion in loans. In opening the doors of the capital markets to the economic activities of low- income men and women, profits have been a must, and outstanding profits have been critical. Precisely because microfinance works with the poor, it has had to push hard to gain legitimacy in the world of business. Emerging from a sector that is so closely associated with social work and philanthropy, it has had to overcome strong prejudices, regarding both the poor and those who work with them. This has been further clouded by the large number of entities in microfinance, which vary enormously in their performance and whose information is often not trans- parent. Inoltre, the field harbors two ultimately contradictory conceptions of microfinance: at one end, some see it as a “human right” and at the other some see it as a component of the financial system. Di conseguenza, until the late 1990s, business by and large ignored microfinance. Where it was known in emerging markets, it was viewed with great skepticism. To pierce through, microfinance had to perform like business, only more so. It not only had to generate market rates of return—it had to beat them. The opening of the bond markets and the entry of convention- al commercial banking would not have been possible without that. But has this outreach come at too high a price for the poor, despite the repeat customers and the growing number of clients? The answer to that lies in the real- innovazioni / winter & spring 2007 139 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu Figure 7. BancoSol: From monopoly/monoproduct to multiproduct Source: BancoSol ization that, from a social perspective, the real success of microfinance in Latin America is not financial institutions dedicated to the poor that earn rates of return matching or surpassing traditional banks. It is that these profit leaders were able to attract the entrants to create an entire industry dedicated to the base of the pyra- mid. Once the moneylenders were displaced, this competition has driven the con- tinuous improvement of the terms under which financial services reach the poor. When BancoSol opened its doors in 1992, it charged an effective interest rate of 35%.62 The rate was such a bargain compared to the moneylender that the bank enjoyed a virtual monopoly. Caja Los Andes was formed in 1995 as an FFP.63 At that time, market penetration was still low and both institutions could grow without having to compete for clients. The competitive scene in Bolivia changed radically with the crisis of 1999-2000. While the wave of overindebtedness exacted a social cost, the end result of the intense competition was to provide several new benefits to the poor. Ever since the crisis, the Bolivian microfinance industry has remained intense- ly competitive. This has had a fundamental impact on pricing. Figura 6 shows that effective interest rates64 in Bolivia have dropped constantly, with apparently no end in sight. Since 1998, the price paid by the poor for credit has gone from just under 30% A 21.2%, the lowest in Latin America. Together with lower prices, the variety of credit products available to the poor has also blossomed in Bolivia. When it first started, BancoSol offered one single product, solidarity loans: people with no col- 140 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid lateral and no ascertainable credit history could borrow from the bank if they got together in a self-selected group of 3 A 5 people who would cross-guarantee each other. This was a highly effective mechanism to bring new borrowers into the bank while preserving asset quality, but the high trans- action costs of forming groups made it vul- nerable to individual loans, which the com- petition was quick to introduce. Figura 7, tracing the evolution of loan products at BancoSol from 1997 A 2001, shows it went from effectively being a monoproduct bank to offering nine different credit options by the end of the competitive crisis. As Rhyne states, “Unquestionably, most microfinance clients benefit from the advent of competi- zione. More people have access to financial services, they can choose their supplier, and they can demand favorable terms. … it is important to reiterate the effects of com- mercialization on service quality, methodol- ogy, and new product development and to emphasize that these emerged inde- pendent of the crisis.”65 Since then, the Bolivian competitive experience has played out in several other countries, with the resulting drop in prices and the increase in product variety. In Mexico, where pricing remains high relative to the rest of the region, serious competition is emerging for the first time and this will accelerate the downward evolution of pricing and the introduction of changes to lending products and methodologies. The beneficiaries of this process will be Mexico’s poor. Tavolo 8. Financial returns of BancoSol since inception. Sources: BancoSol, ACCION International Competition is precisely what reconciles profitability and the creation of social value. In the early years of BancoSol, when the only other source of credit for the poor was the moneylender, the competitive price umbrella was set so high that the bank had little incentive to become more efficient or to adapt to different client needs. While price was held constant, profitability improved as market penetration produced growth that leveraged the economies of scale of the bank’s infrastruc- ture. Eventually, In 1998 this model produced an ROE just under 30%. This was significant, as it solidified the image of BancoSol in the business community and strengthened its links to the capital markets. Nel frattempo, the creation of social value was limited to the gains in the outreach of the bank: new clients and larger loans for existing clients. But superior returns brought in competition. With the onset of intense com- petition, the Bolivian market went through a deep crisis in 1999-2000 and the bank’s profitability was decimated. In an intensely competitive market, arguably innovations / winter & spring 2007 141 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Michael Chu Table 9. Financiera Compartamos: Financial Returns & Active Clients, 1999-2004 Fonte: MIX Market Table 10. Financiera Compartamos: Dividend Payments Source: ACCION International what BancoSol was losing in profitability was what the poor were gaining, via bet- ter pricing, more products and improved service. Competitive pressures have remained intense in Bolivia and BancoSol achieved its recent return to attractive levels of profitability in a declining price environment. Now, profitability improve- ments are the result of management skills applied diligently to obtain efficiencies in the cost structure more quickly than prices drop. Di conseguenza, achieving a ROE of 26.3% In 2004 (E 23.6% in the first nine months of 2006) was consistent with the creation of social value (Vedi la tabella 8). At the base of the pyramid, in an environment where competition is weak or nonexistent, the link between profitability and social value may range from benign (where the issue may maximizing the potential of creating social value), to harm- ful (where financial return is exacted while creating little or no social return.) An example of the latter may be an open air market strategically located at the inter- section of two important roads, but where all the financing is provided by one moneylender in complicity with the local police chief, who will not allow anyone else to compete. It follows that a key variable to examine at the intersection of busi- ness and poverty is the barriers to competition—their origins and the ease with which they can be overcome. When barriers to entry are not artificial, and competition is not yet significant, whether profitability and social returns are complementary or antagonistic may 142 innovazioni / winter & spring 2007 Scaricato da http://direct.mit.edu/itgg/article-pdf/2/1-2/115/704145/itgg.2007.2.1-2.115.pdf by guest on 08 settembre 2023 Commercial Returns at the Base of the Pyramid depend on the use given to earnings. In the last six years, Compartamos in Mexico has been earning an average annual ROE of 50.6%66 but it has used this to fuel an extraordinary growth, going from 48,835 active clients in 1999 A 309,637 In 2004, an average annual increase of 44.9%, making it the largest microfinance bank in Latin America (see Table 9). By its active clients had September 2006, grown to 565,991.67 Compartamos made dividend payments of $2.50 million in