MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION:

EVIDENCE FROM A VAT INCREASE IN JAPAN

David Cashin and Takashi Unayama*

Abstract—We estimate the intertemporal elasticity of substitution in con-

assunzione (IES) using a preannounced increase in Japan’s consumption tax

rate. Because this tax is highly comprehensive, the rate increase was

announced prior to its implementation, and because other factors that affect

the real interest rate were constant, the tax rate increase presents an ideal nat-

ural experiment to estimate the IES. A Japanese monthly household survey

is exploited to accurately categorize nondurables, and our empirical specifi-

cation addresses intratemporal substitution bias. We find that the IES is 0.21

and not significantly different from 0, but it is significantly less than 1.

IO.

introduzione

I N this paper, we estimate the intertemporal elasticity of

substitution in consumption (IES) using an increase in the

Japanese consumption tax rate as a natural experiment. IL

consumption tax, which is a value-added tax (VAT),

increased from 3% A 5% in April 1997. Unlike VAT in many

other countries, Japan has a single flat rate with a relatively

small number of exemptions. As expected, the tax burden

was borne fully by consumers in the form of higher prices.

Because nominal interest rates and the inflation rate were

constant around the implementation of the tax rate increase, Esso

can be treated as an exogenous change in the real interest rate,

which provides an ideal situation to estimate the IES.

Previous research on this topic (Hall, 1988; Attanasio &

Weber, 1993, 1995; Ogaki & Reinhart, 1998) has relied on an

instrumental variables approach to address the critical econo-

metric problem that the real interest rate is endogenous in the

standard log-linearized Euler equation for consumption.

Tuttavia, as Yogo (2004) notes, asset returns are notoriously

difficult to predict, and as a result, the available instruments

are weak. Weak instruments can lead to biased estimators

and finite sample distributions of test statistics that depart

greatly from their limiting distributions. This paper avoids

the problem of weak instruments by exploiting the natural

experiment presented by the consumption tax rate increase.

In addition to the novel research design, our data set

plays an important role in estimating the IES. We use the

Japanese Family Income and Expenditure Survey (JFIES),

Received for publication November 1, 2012. Revision accepted for pub-

lication January 5, 2015. Editor: Mark W. Watson,

* Cashin: Federal Reserve Board of Governors; Unayama: Hitotsubashi

University and RIETI.

We thank Joel Slemrod, James Hines, Chris House, Mel Stephens, Caro-

line Weber, anonymous referees, and seminar participants at the 2012

NBER Japan Project Meeting, Japan’s Ministry of Finance, IL 2011 Inter-

national Institute of Public Finance Congress, the University of Michigan,

and the University of Otago for helpful comments and suggestions. In addi-

zione, we thank Megumi Araki for her helpful assistance. We are also grate-

ful to the National Science Foundation, the Japan Society for the Promotion

of Science, and RIETI for funding part of this study. The views expressed

here are strictly our own and do not necessarily represent the position of

the Federal Reserve Board or the Federal Reserve System.

A supplemental appendix is available online at http://www.mitpress

journals.org/doi/suppl/10.1162/REST_a_00531.

a monthly household-level panel data set. Given our use of

microdata, our results are free from the aggregation bias

discussed in Attanasio and Weber (1993, 1995). Its high-

frequency (monthly) panel structure allows us to adopt the

conventional Euler equation approach and observe con-

sumption expenditure immediately before and after imple-

mentation of the tax rate increase.

Inoltre, because the JFIES is highly disaggregated by

item type, we can define nondurables appropriately. The defi-

nition in previous studies has included goods and services

that exhibit some degree of storability or durability. For

esempio, as Mankiw (1985) points out, footwear and clothing

are usually considered to be nondurables, but they should be

classified as durables. Attanasio and Weber (1993, 1995), IL

first to address this issue, exclude durables and semidurables

but pay little attention to storability. Storable goods can be

stockpiled during low-price periods for consumption in high-

price periods. Failing to account for this behavior could bias

the estimate of the IES upward. To avoid these biases, we

separate nonstorable nondurable goods and services (per esempio.,

eating out) from storable nondurable (per esempio., laundry detergent)

and durable (per esempio., automobiles) goods and services.

With multiple goods, we explicitly consider intratemporal

substitution between nondurables, storables, and durables by

constructing a model of consumer choice. As Ogaki and Rein-

hart (1998) demonstrate, failing to account for intratemporal

substitution can induce a biased estimate of the IES when pre-

ferences over nondurables and durables are nonseparable. In

general, the service flow from durables becomes higher prior

to a tax rate increase because the user cost of durables falls.

With nonseparable preferences, households substitute between

nondurables and durables. If we do not control for this, the esti-

mate of the IES will be biased, where the sign of the bias

depends on the structure of intratemporal preferences. IL

empirical specification derived below, consistent with our

modello, is robust to the possibility of intratemporal substitution.

Exploiting these advantages, our point estimate of the IES

È 0.21, which is significantly less than 1 but not significantly

different from 0. While the baseline regression uses the sam-

ple period between April 1992 and March 2002, the choice of

sample period has little impact on our results. Inoltre, IL

results are robust to sample selection criteria. Point estimates

from those robustness checks range between 0.17 E 0.36,

comparable to those in previous studies using macrodata such

as Hall (1988), Ogaki and Reinhart (1998), and Yogo (2004),

but less than those using microdata such as Attanasio and

Weber (1993, 1995), Vissing-Jorgensen (2002), and Gruber

(2013). We employ additional tests to check whether liquidity

constraints or data quality is responsible for the small IES but

find no evidence to support these assertions.

The Review of Economics and Statistics, May 2016, 98(2): 285–297

(cid:2) 2016 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 3.0

Unported (CC BY 3.0) licenza.

doi:10.1162/REST_a_00531

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

286

THE REVIEW OF ECONOMICS AND STATISTICS

Our analysis also highlights the importance of allowing

nonseparable preferences over durables and nondurables

and suggests the two composite goods are strong comple-

menti. When we restrict preferences over durables and non-

durables to be separable, we obtain a point estimate of the

IES of 0.91, which is significantly larger than our baseline

estimate of 0.21 and similar to the estimates of Attanasio

and Weber (1993, 1995) and Vissing-Jorgensen (2002),

who also use microdata but restrict preferences to be separ-

able over durables and nondurables. Combining our empiri-

cal results with the Euler equation derived from the baseline

modello, we can go beyond our finding that preferences over

durables and nondurables are nonseparable and place an

upper bound on the elasticity of substitution between dur-

ables and nondurables. Specifically, our results imply that

the elasticity of substitution between durables and nondur-

ables is less than our IES estimate of 0.21. Così, durables

and nondurables are strong complements.

To the extent that our finding of a small IES is applicable

in other contexts, it suggests that policies that aim to dam-

pen volatility in household consumption expenditure

through changes in the real interest rate will not be effec-

tive. For the same reason, the deadweight loss from a prean-

nounced increase in a VAT and the taxation of interest

income is likely to be small.

The remainder of the paper is organized as follows. Sez-

tion II provides background on Japan’s April 1997 con-

sumption tax rate increase and evidence for our assertion

that the tax rate increase presents an ideal natural experi-

ment to estimate the IES. Section III introduces a represen-

tative agent model of household consumption to make pre-

dictions about household consumption in the months

following announcement of a Consumption Tax rate

increase. We then present an empirical specification consis-

tent with the model and discuss identification of the IES.

The data used in estimation and our results are presented in

section IV. Section V summarizes and discusses our results.

II. The Consumption Tax Rate Increase: An Ideal

Natural Experiment to Estimate the IES

Japanese government made it clear that it expected the bur-

den of the Consumption Tax would be borne fully by consu-

mers.2 Accordingly, changes in consumer prices should be

proportional to changes in the Consumption Tax rate. In

other words, given a nominal interest rate, an increase in the

Consumption Tax rate lowers the real interest rate through a

proportional price increase across goods and services.

The Consumption Tax was introduced in 1989 at a rate

Di 3%, and it was increased to 5% in April 1997. IL 1997

increase was originally proposed as a part of the Murayama

tax reform, which passed through the Japanese Diet in late

1994.3 Because the primary purpose of the reform was to

continue the shift from direct to indirect taxation, the con-

sumption tax rate increase was coupled with immediate cuts

in income tax rates. In that sense, the tax increase was com-

pensated.

Although the Murayama reform package set a target date

of April 1997 for the Consumption Tax rate increase, it was

unclear whether the increase would actually be implemen-

ted then. This is because the reform legislation also stated

that the increase would be imposed only if the economy

had sufficiently recovered from a prolonged recession

(1991–1993) and subsequent years of feeble growth. Hav-

ing judged the economy to have sufficiently recovered, IL

ruling Liberal Democratic Party (LDP) decided to raise the

tax rate as scheduled. The bill to raise the Consumption Tax

rate passed through the upper house on June 25, 1996, E

the tax rate increase was scheduled to become effective on

April 1, 1997.

Even after this passage, it was not clear that the Con-

sumption Tax rate increase would be implemented in April,

as it was the central issue in October 1996 elections to the

lower house of the Diet, with the LDP promising to imple-

ment the tax rate increase as planned while the opposition

promised to shelve it. The LDP narrowly won the election,

and on December 26, 1996, the government submitted the

fiscal year 1997 budget, finally deciding to increase the

Consumption Tax rate to 5% on April 1, 1997.

B. The Consumption Tax Rate Increase as a

Natural Experiment

UN. Japan’s Consumption Tax and the April 1997

Rate Increase

Japan’s Consumption Tax is a value-added tax (VAT).

Unlike VAT in many other countries, the consumption tax

has a single flat rate with a relatively small number of

exemptions.1 In addition, as documented by Ishi (2001), IL

To estimate the IES, variation in the real interest rate, IL

price of current consumption relative to future consump-

zione, is necessary. Because the real interest rate is defined

as the nominal

interest rate minus the inflation rate, UN

change in the inflation rate will induce the necessary varia-

zione. Di conseguenza, the April 1997 Consumption Tax rate

1 Exemptions include transfer or lease of land, transfer of securities,

transfer of means of payment, interest on loans and insurance premiums,

transfer of postal and revenue stamps, fees for government services, inter-

national postal money orders, foreign exchange, medical care under the

medical insurance law, social welfare services specified by the social wel-

fare services law, midwifery service, burial and crematory service, trans-

fer or lease of goods for physically handicapped persons, tuition, entrance

fees, facilities fees, examination fees of schools designated by the Articles

of the School Education Law, transfer of school textbooks, and the lease

of housing units.

2 When the consumption tax was introduced in 1989, the government

took several steps to ensure this outcome. Primo, the Special Council on

the Transition was formed to promote enforcement of the tax across agen-

cies. Secondo, the government carried out an extensive advertising cam-

paign to allay the public’s fear of price hikes and restrain overcharging by

traders. A telephone service was also set up so consumers could report

complaints about prices. Finalmente,

the Economic Planning Agency

increased the budget for the price monitoring system. The situation was

nearly identical in 1997.

3 For the political process, see Ishi (2001) and Takahashi (1999).

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION

287

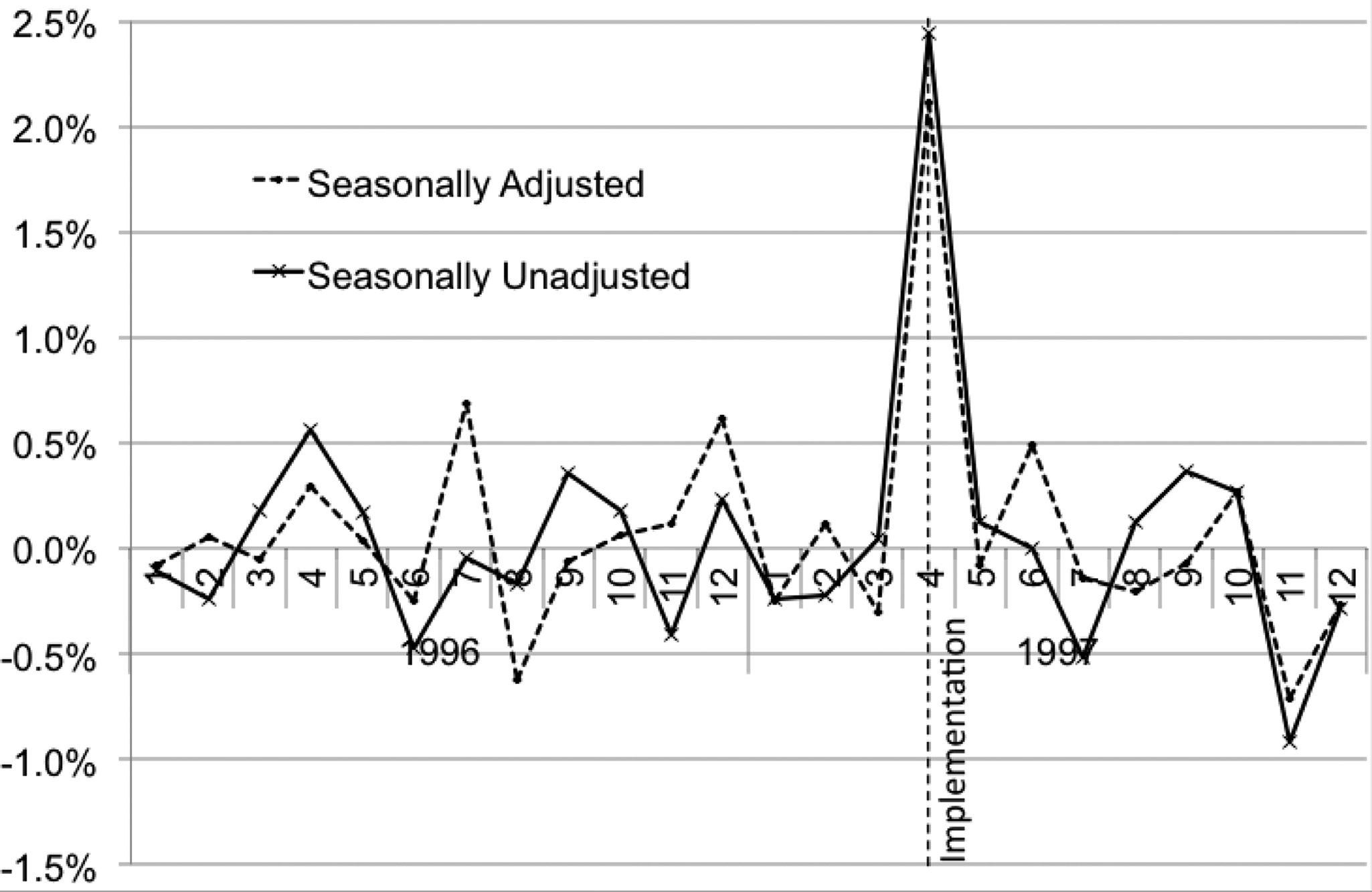

FIGURE 1.—PERCENTAGE CHANGE IN NONSTORABLE, NONDURABLE PRICES

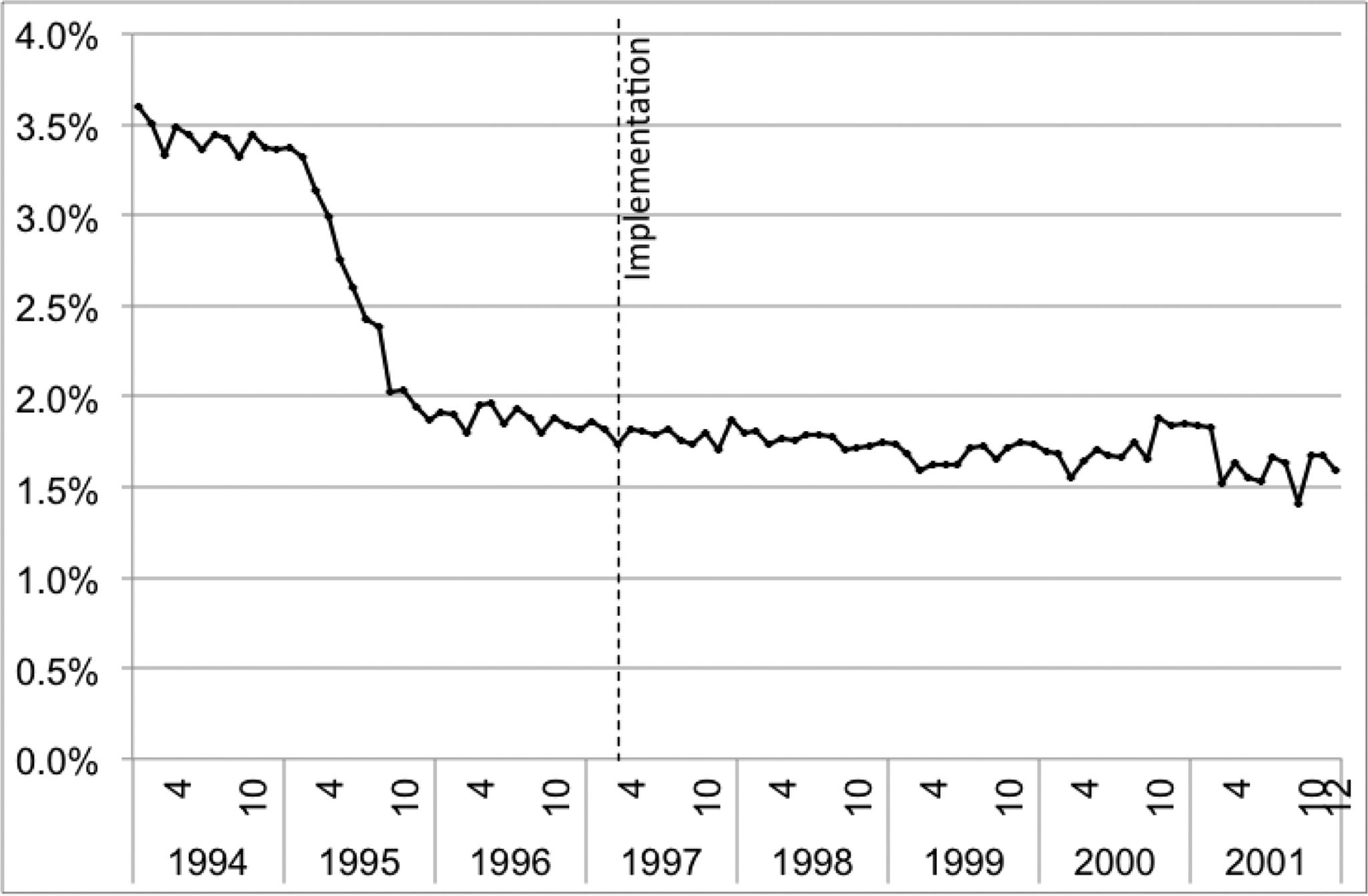

FIGURE 2.—AVERAGE INTEREST RATES ON SHORT-TERM LOANS AND DISCOUNTS

The figure presents the month-to-month percentage change in unadjusted and seasonally adjusted non-

storable, nondurable prices. To remove seasonality, we regress the monthly percentage price change in

nonstorable, nondurable goods and services on month dummies. The residuals are added to the constant

term from the regression to obtain a seasonally adjusted monthly percentage price change. The dashed

vertical line in the figure is April 1997, the month the consumption tax rate increase was implemented.

The figure presents the average contracted interest rate on short-term loans and discounts. These are

the average interest rates applied to a contract of less than one year between commercial banks and len-

ders. The data come from the Bank of Japan.

increase, which represented an exogenous increase in the

future price level during a period in which nominal interest

rates were stable, presents an ideal natural experiment to

estimate the IES, which we discuss below.

Primo, the tax rate increase can be regarded as an exogen-

ous change in consumer prices. Not only is it the case that

the tax system is exogenous to individual households, but it

is also true that the impact of the tax rate increase is inde-

pendent of consumer behavior. This is because the VAT by

and large applies to expenditures regardless of the charac-

teristics of the consumer, the point of purchase, or the type

of goods purchased. Figura 1 shows the month-to-month

percentage change in the consumer price index for nonstor-

able, nondurable goods and services, the component of con-

sumption expenditure that we use to estimate the IES.

While inflation was negligible in most months prior to and

following implementation of the tax rate increase, the price

level increased by 2.39% between March and April 1997,

consistent with full forward shifting of the Consumption

Tax onto consumers at the time of implementation.4 The

figure also suggests that there was not a significant seasonal

component to price changes around the time of the tax rate

increase. Consequently, the optimal response to the Con-

sumption Tax rate increase is unlikely to be confounded by

seasonality in prices. Di conseguenza, we can focus on a one-

time price change and rule out the influence of an additional

factor (cioè., variation in pretax prices due to transitory or

seasonal components) that affects the real interest rate.

We can also rule out the influence of the nominal interest

rate on the real interest rate. Figura 2 presents the average

contracted interest rates on short-term loans and discounts,

which are the average interest rates applied to a contract of

less than one year between a commercial bank and lender.

The average interest rate fell precipitously throughout 1995

4 Carroll et al. (2010) find that full forward shifting at the time of a con-

sumption tax rate increase is the norm across most countries.

but remained relatively constant thereafter. This suggests

that households would not change their nominal interest

rate expectations in the months surrounding implementation

of the Consumption Tax rate increase. In other words,

households should not have expected any changes in nom-

inal interest rates by the central bank that would offset or

augment the intertemporal substitution incentives.

These facts imply that

the tax rate increase can be

regarded as an exogenous change in the real interest rate,

which allows for consistent estimation of the intertemporal

substitution response using ordinary least squares (OLS).

Previous studies of intertemporal substitution have relied

on an instrumental variables approach to address the well-

documented endogeneity between the real interest rate and

consumption growth. The standard approach has been to

instrument for the contemporaneous real interest rate with

lagged interest rates. Tuttavia, there are several potential

issues with the instruments that have been employed. Primo,

as Yogo (2004) notes, it is notoriously difficult to predict

the real interest rate, and therefore some of the previous stu-

dies in this literature (especially those using aggregate data)

suffer from the weak instrument problem. Weak instru-

ments lead to estimates of the IES biased in the direction of

OLS, which itself is likely to suffer from a downward bias.5

Even if the weak instrument problem is overcome, there

still exists the potential for correlation between the lagged

5 Two-stage least squares (2SLS) estimators using weak instruments are

biased in the direction of OLS for the following reason. Suppose the

structural equation is given by yi ¼ bxi þ gi and the first-stage equation

by xi ¼ pzi þ ni. If p is truly 0 due to weak instruments, then any varia-

tion in the predicted value of xi, ^xi will come from ni. It follows that the

variation in ^xi is no different from the variation in xi, and the OLS and IV

estimates are estimating the same quantity on average. For more informa-

zione, see Pischke (2010).

Using OLS, Gruber (2013) obtains an estimate of the IES of (cid:2)0.55,

which is significantly less than his estimates when instrumenting for the

after-tax real interest rate. Vissing-Jorgensen (2002) finds that estimates

of the IES converge toward 0 as the number of instruments is increased.

This is because the weak instrument problem is increasing in the degree

of overidentification.

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

288

THE REVIEW OF ECONOMICS AND STATISTICS

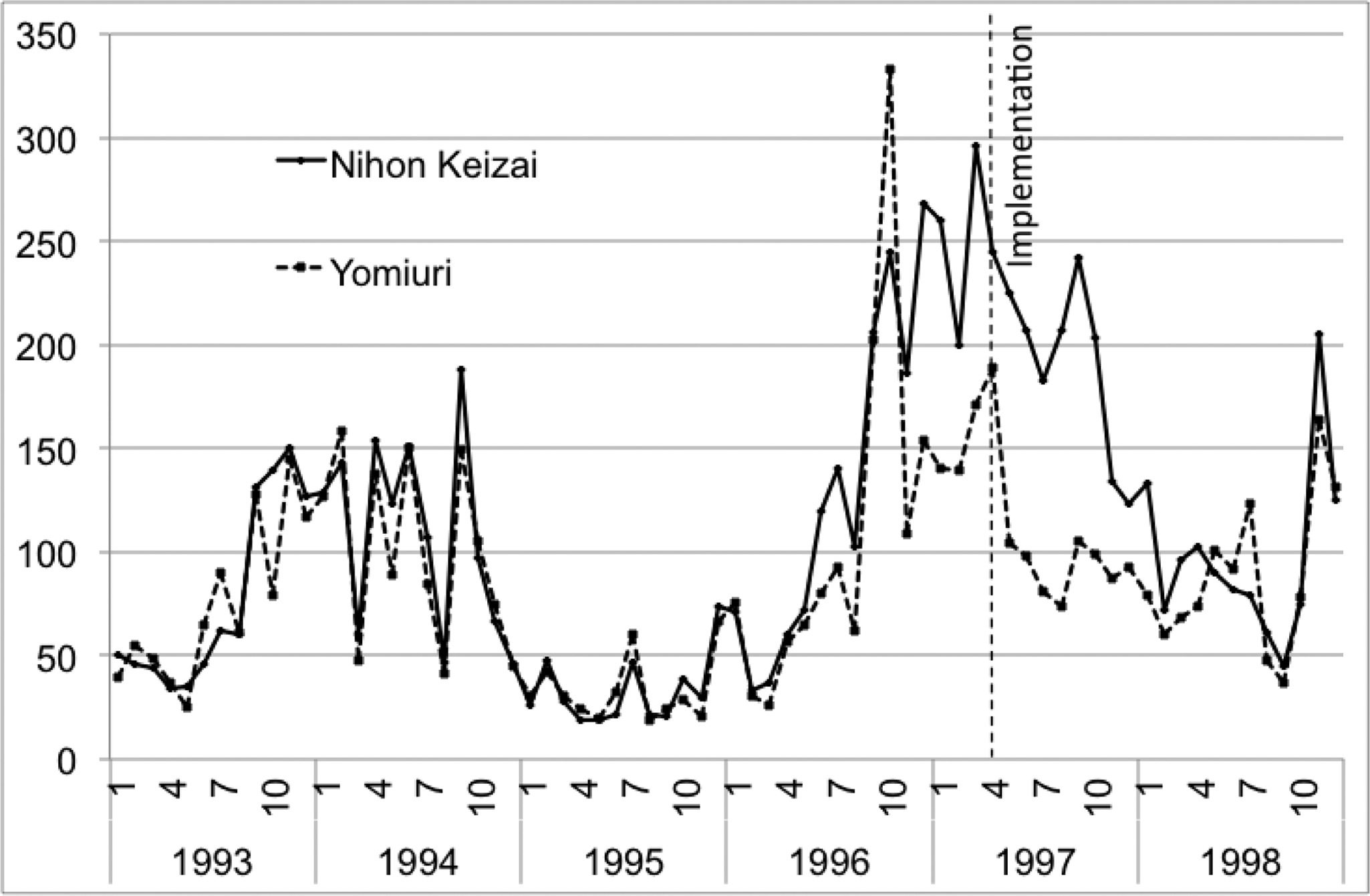

FIGURE 3.—NUMBER OF ARTICLES MENTIONING THE CONSUMPTION TAX

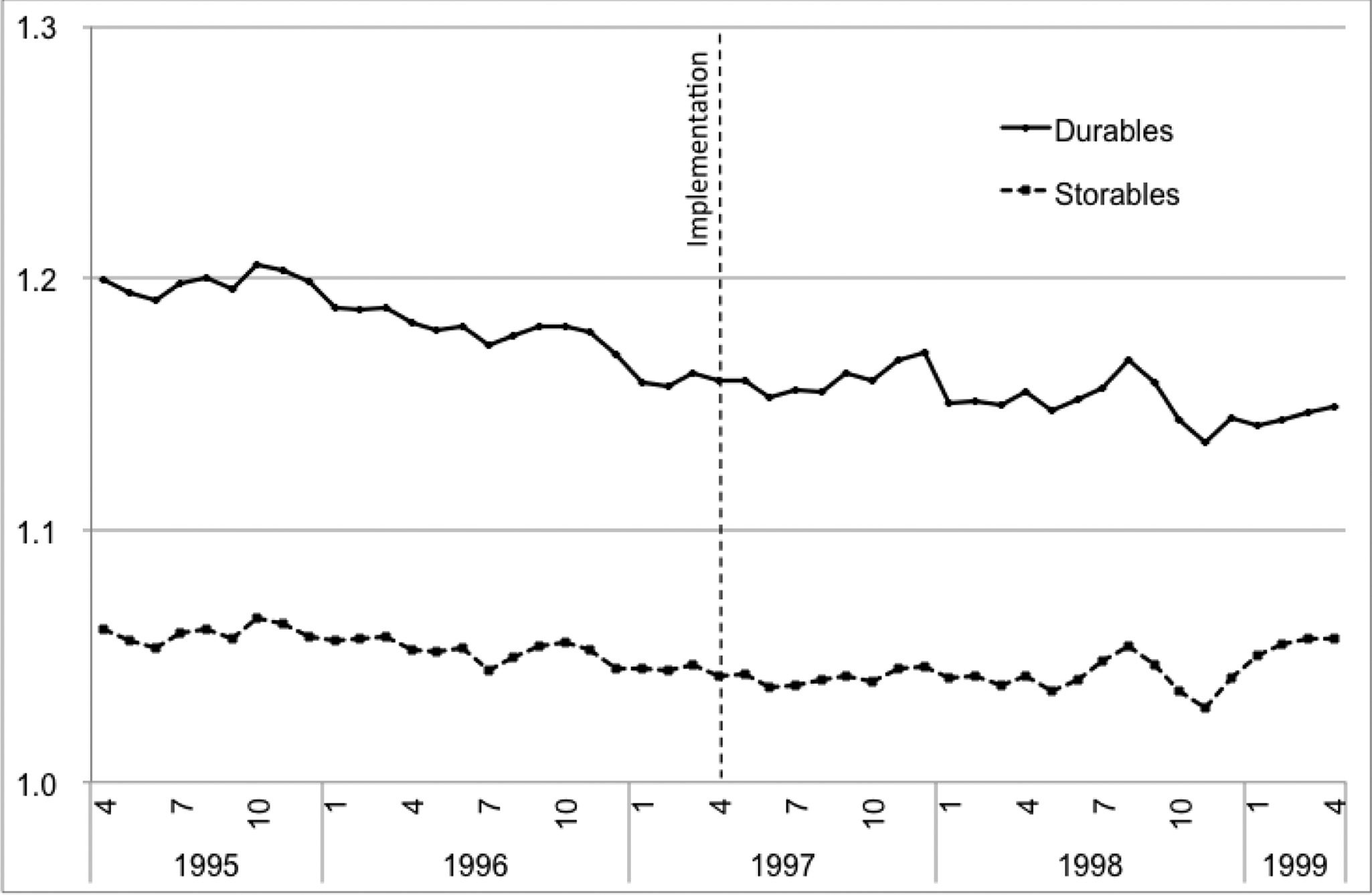

FIGURE 4.—PRICE RATIOS RELATIVE TO NONSTORABLE NONDURABLES

Fonte: Authors’ calculations. Circulation numbers for the Nihon Keizai Shimbun and Yomiuri Shim-

bun are from Japan’s Audit Bureau of Circulations.

interest rates and consumption growth, which is discussed

by Gruber

(2013). Inoltre, Attanasio and Weber

(1993, 1995) show that studies using lagged instruments

and aggregate nondurable expenditure data suffer from a

downward bias in estimates of the IES known as aggrega-

tion bias.6 This study avoids these issues by using an exo-

genous institutional price change.

While exogenous variation in the real interest rate is a

necessary condition for estimating the IES, it must also be

the case that households are aware of the change. While we

cannot provide direct evidence on household awareness of

the consumption tax rate increase, we can provide indirect

evidence by examining news coverage prior to implementa-

zione. Figura 3 reports the number of articles that mention the

phrase consumption tax in the Nihon Keizai Shimbun,

Japan’s leading business newspaper, with a circulation of

Sopra 3 million (In 2010), and the Yomiuri Shimbun, a leading

nonbusiness newspaper, with a circulation of over 10 million

(In 2010).7 There was a steady upward trend that began just

prior to enactment of the June 1996 legislation. Coverage

peaked in the Yomiuri Shimbun in October 1996, Quale

coincided with elections to the lower house of the Diet.

Overall coverage in both papers was consistently high in the

months following the election but prior to the tax change,

with nearly 300 articles in the Nihon Keizai Shimbun

mentioning the consumption tax in March 1997. Questo

suggests that households were aware of the tax rate increase

and might therefore engage in intertemporal substitution

behavior.

The news coverage also suggests that households may

have been aware of the effects of the Murayama reform

package as a whole. Figura 3 shows that coverage initially

6 Attanasio and Weber (2010) sum up aggregation bias as follows:

‘‘The aggregate consumption growth rate is computed by taking logs of

the mean of individual consumption, whereas [the log-linearized Euler

equation] implies that means of the logs should be taken instead. . . . IL

difference between these two terms is highly serially correlated, così

invalidating lagged consumption growth as an instrument.’’

7 Circulation numbers come from Japan’s Audit Bureau of Circulations.

The figure presents the ratio of seasonally adjusted durable and storable nondurable prices to nonstor-

able nondurable prices. To remove seasonality, we regress the consumer price indices for durable, stor-

able nondurable, and nonstorable nondurable goods and services on month dummies. The residuals are

added to the constant in the regression to obtain seasonally adjusted price indices. To calculate the ratios,

we divide the seasonally adjusted durable and storable nondurable price by the seasonally adjusted non-

storable nondurable price in each month. The dashed vertical line in the figure is April 1997, the month

of implementation.

peaked in September 1994, which coincided with the pas-

sage of the Murayama reform. Accordingly, households

may have known the package was intended to be revenue

neutral over the long run. This in turn implies that the

income effect associated with the tax rate increase would be

piccolo, and thus, we need not pay much attention to separate

identification of the intertemporal substitution and income

effects.8

Finalmente, the relative pretax price of goods and services

did not change around the time of the consumption tax rate

increase. Figura 4 shows the price of durables and storable

nondurables relative to nonstorable nondurables around the

time of the consumption tax rate increase. As the figure

demonstrates, there was little change in the relative price of

these goods. This fact allows us to make the simplifying

assumption of constant relative pretax prices in the model

presented in section III. Di conseguenza, we need only concern

ourselves with the possibility of intratemporal substitution

between durables and nonstorable nondurables resulting

from the reduction in the user cost of durables just prior to

the Consumption Tax rate increase, which we discuss

further in Section IIIA.

To summarize, we argue that the April 1997 consump-

tion tax rate increase presents an ideal natural experiment

to estimate the IES for the following reasons: the tax rate

increase can be regarded as an exogenous change in the

real interest rate, the real interest rate was relatively stable

prior to and following implementation, the tax rate increase

was predictable and consumer awareness was high, E

relative pretax prices were constant among taxable goods

and services.

8 That said, our empirical specification does attempt to identify the

combined income and intertemporal substitution effects in the months

immediately following announcement of

the consumption tax rate

increase.

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION

289

III. A Consumption Tax Rate Increase and the

Intertemporal Elasticity of Substitution

UN. The Model

In this section, we construct a model to demonstrate the

impact of a Consumption Tax rate increase on both house-

hold consumption and expenditure. A household consumes

three types of taxable goods and services: nonstorable non-

durables (N), storable nondurables (S), and durables (D).9

Household i maximizes its lifetime utility function, U, IL

discounted sum of the instantaneous utility, tu. Suppose the

utility function at time s is

Us ¼

X1

t¼s

bt(cid:2)S

(cid:2)

R

R (cid:2) 1

(cid:3)

H

ut

io

R(cid:2)1

;

R (cid:2) 1

where b is the subjective discount factor, s is the IES, E

ut is the instantaneous utility. Unlike previous studies, we

use a deterministic setting because we focus on short-run

dynamics around the time of the consumption tax rate

increase.

Following Ogaki and Reinhart (1998), the intratemporal

utility function is assumed to take the CES form for N, S,

and D,

ut ¼ u CN

T ; CS

T ; Dt

(cid:4)

H

(cid:5) ¼ CN

T

2(cid:2)1

2 þ aCS

T

2(cid:2)1

2 þ bDt

io 2

2(cid:2)1

2(cid:2)1

2

;

t and CS

where CN

t are consumption of N and S, rispettivamente;

Dt is the stock of D held at the end of period t; [ is the intra-

temporal elasticity of substitution; and a and b are some

positive numbers that determine the weights attached to S

and D.10 It is worth noting that the utility function becomes

additively separable in N, S, and D if s ¼ [.

The CES specification assumes that preferences are

homothetic. Pakos (2011) finds instead that preferences are

nonhomothetic. Specifically, durables are luxuries and non-

durables are necessities. If this is the case, ignoring nonho-

motheticity can lead to an estimate of the IES that is biased

in su (see also Okubo, 2008). Nevertheless, we believe it

is reasonable to maintain the simplifying assumption of

homotheticity, since income effects should not be present

on implementation of the Consumption Tax rate increase.11

9 In online appendix A, we construct a model that allows nonseparable

preferences over taxable and tax-exempt goods and services and derive

testable implications regarding additive separability. The null hypothesis

of additive separability is not rejected by the data. Based on this result,

we ignore tax-exempt goods and services throughout our analysis.

10 Because we are focusing on short-run dynamics, our model ignores

the labor/leisure choice, effectively assuming that labor supply is fixed

during the period of interest. This is made more plausible by the fact that

we restrict our sample to households who do not change jobs during their

time in the sample. Crossley, Basso, and Wakefield (2009), who investigate

a VAT rate change in the United Kingdom, also ignored the labor supply

decision.

11 Income effects associated with the Consumption Tax rate increase

should appear on announcement of the tax rate increase, whereas identifi-

cation of the IES relies on changes in expenditure on implementation of

the Consumption Tax rate increase.

In maximizing its lifetime utility, the household faces

three constraints: the intertemporal budget constraint and

laws of motion for the stock of S and D. The intertemporal

budget constraint is given by

ÞAt(cid:2)1 þ Yt (cid:2) pN

At ¼ 1 þ it

ð

(cid:6)

(cid:4)

t XD

t þ u XD

(cid:2) pD

T

T (cid:2) pS

t XS

t CN

T

(cid:7) (cid:2) h Stð Þ for t ¼ s (cid:3) (cid:3) (cid:3) 1;

(cid:5)

where At is financial wealth held at the end of period t; it is

T , pS

the nominal interest rate in period t; Yt is income; pN

T ,

t are the prices of N, S, and D, rispettivamente; XS

and pD

t and

XD

t are gross expenditures on S and D, rispettivamente; and St

is the stock of S held at the end of period t. The functions y

and u represent costs associated with the storage of S and

purchase of D, which we discuss below. Finalmente, we take

As(cid:2)1, Ds(cid:2)1, and Ss(cid:2)1 as given.

As we discussed in the previous section, it was expected

that the Consumption Tax rate increase would be fully

passed onto consumers in the form of higher prices at the

time of implementation (hereafter, period T). Inoltre,

nominal interest rates and the pretax price level were stable

around implementation. Di conseguenza, we can safely make the

following two simplifications to the intertemporal budget

constraint:

8

>>><

>>>:

1:

t ¼ pN; pS

pN

t ¼ pS; pD

t ¼ pD

pN

t ¼ 1 þ s

ð

ÞpN; pS

before and at period T (cid:2) 1

t ¼ 1 þ s

ð

in and after period T:

ÞpS; pD

t ¼ 1 þ s

ð

ÞpD

2: it ¼ i 8 T;

where t is the inflation rate due to the tax rate increase. In

our case, t ¼ 0.0239 because the CPI for N increased by

2.39% from March to April 1997.

The function y accounts for the cost of holding a stock of

storables, S.12 This consists of costs from stock shortages as

well as storage costs. Per esempio, if a household runs out

of storable nondurable goods such as toothpaste, there is a

time cost associated with making a trip to the store to pur-

chase an additional

tube. Alternatively, stockpiling S

requires the use of storage space that could be used for

other purposes. These scenarios suggest that there exists a

bliss point for the stock of S, S(cid:4), which means that

h0ðSi;tÞ (cid:5) 0 if Si;T (cid:5) S(cid:4) and h0ðSi;tÞ > 0 if Si;t > S(cid:4).

u accounts for costs associated with the purchase of D.

The purchase of a durable good is an infrequent event, E

more effort is required than for a nondurable purchase. Questo

may include collecting catalogs, identifying key specs, E

shopping around to get a better price. Assuming that the

12 Previous studies have shown empirically that demand is affected by

the storability of a good (Hendel & Nevo, 2004, 2006). In particular,

households weigh the benefits of purchasing storable goods at a lower

price against the cost of holding additional inventory.

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

290

THE REVIEW OF ECONOMICS AND STATISTICS

opportunity cost of a household’s time spent shopping is

increasing, convex, and proportional to the amount spent on

durable goods, it follows that ui is increasing and convex in

its argument, questo è, u0 > 0 and u00 > 0.

Finalmente, the evolution of the stocks of S and D is given by

St ¼ 1 (cid:2) ds

ð

ÞSt(cid:2)1 (cid:2) CS

t þ XS

T

for t ¼ s (cid:3) (cid:3) (cid:3) 1

E

(cid:4)

Dt ¼ 1 (cid:2) dD

(cid:5)Dt(cid:2)1 þ XD

T

for t ¼ s (cid:3) (cid:3) (cid:3) 1;

where dS and dD are the depreciation rates of S and D,

respectively.13

B. Optimal Consumption Path and the Intertemporal

Elasticity of Substitution

Solving the household’s optimization problem, we obtain

the following first-order conditions:

@Ut=@CN

T

@Ut(cid:2)1=@CN

T(cid:2)1

¼

¼

(cid:9)(cid:2)1

R

(cid:8)

(cid:8)

(cid:9) R(cid:2)2

Ft

Ft(cid:2)1

1

B 1 þ i

(cid:8)

rð2(cid:2)1Þ CN

T

CN

T(cid:2)1

(cid:9) pN

(cid:9)

(cid:8)

T

;

pN

Þ

T(cid:2)1

ð

(cid:8)

t ¼ CN

CS

T

(cid:8) (cid:9)

(cid:8) (cid:9) pS

pN

1

UN

(cid:9)(cid:2)2

;

t þ h0 Stð Þ ¼

pS

1 (cid:2) dS

1 þ i

;

Dt ¼ CN

T

(cid:8) (cid:9)

pD

H

pN

(cid:9)

(cid:8)

1

B

1 (cid:2) dD

1 þ i

(cid:8)

(cid:2)

Dove

(cid:2)

1 þ u0

(cid:3)

(cid:5)

(cid:4)

XD

T

1 þ Ctþ1s

ð

(cid:2)

Þ 1 þ u0

(cid:4)

XD

tþ1

(cid:3)(cid:10)(cid:9)(cid:2)2

(cid:5)

;

(4)

Ft ¼ 1 þ a

2

(cid:8) (cid:9)2(cid:2)1

CS

T

CN

T

þ b

2

(cid:8) (cid:9)2(cid:2)1

Dt

CN

T

E

Ct ¼

(cid:11)

1 if t ¼ T

0 if t 6¼ T:

Equazione (1) gives the standard Euler equation, Quale

can be rewritten as

13 In the case that dS and dD are equal to 1, S and D effectively become

nondurables.

CN

T

CN

T(cid:2)1

¼ b 1 þ i

ð

½

(cid:6)R 1 þ Cts

Þ

ð

(cid:8)

Þ(cid:2)r Ft

Ft(cid:2)1

(cid:9)R(cid:2)2

2(cid:2)1

:

Then, taking the logarithm of both sides and using the gen-

Þ ffi x for small x, the consump-

eral approximation ln 1 þ x

tion changes can be denoted as

ð

DlnCN

t ¼ j þ

R(cid:2) 2

2 (cid:2)1

DlnFt (cid:2) rCts

(5)

T (cid:2) lnCN

t ¼ lnCN

where DlnCN

T(cid:2)1 and DlnFt ¼ lnFt (cid:2) lnFt(cid:2)1:

This shows that once we assume that preferences over N,

S, and D are additively separable (cioè., s ¼ [), the IES, S,

can be estimated simply by dividing the change in log con-

sumption growth of N at the time of implementation by the

size of the tax rate increase, T. Tuttavia, as Ogaki and Rein-

hart (1998) point out, if preferences over N, S, and D are in

fact nonseparable (cioè., s = [), this simple approach could

yield a biased estimator. To address this issue, we add

regressors to allow for nonseparable preferences in the

empirical specification described below.

(1)

(2)

(3)

C. Empirical Specification

To estimate the IES, we use an empirical specification

that is consistent with the model and is able to separately

identify the IES from intratemporal substitution effects.

According to the model presented above, the intratemporal

substitution effects, or changes in ln Ft, will appear symme-

trically in the months prior to and following implementa-

zione. D'altra parte, the intertemporal substitution effect

is present only at the time of implementation. This is key to

identifying the IES.

With this in mind, the following specification can iden-

tify the IES,

DlnCN

sì;m ¼ controls þ

X

aN

sì;mDDy;m þc1997;AprD1997;Apr;

sì;mð

Þ2I

where DDy;m is the first difference of month dummies for

the period I and D1997,Apr is a dummy for April 1997.

Our main coefficient of interest is c1997;Apr, which corre-

sponds to (cid:2)rs. Since t is known to be 0.0239, as discussed

above, the IES, S, can be identified as (cid:2)c1997;Apr=s. IL

sì;m’s correspond to r(cid:2)2

aN

2(cid:2)1 DlnFy;M, which capture the intra-

temporal substitution effects. Unless preferences are addi-

tively separable (cioè., s ¼ [), at a minimum, aN

1997;Mar

should be nonzero and statistically significant, since the

user cost of durables fell in this month. In more general

cases where durable adjustment costs are present (cioè.,

u 6¼ 0), aN

sì;m may be nonzero in other months surrounding

implementation as well, since changes in Ft will be nonzero

in months other than March 1997 (cioè., the set I may contain

months in addition to March 1997).

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION

291

TABLE 1.—BOUNDING [ USING ESTIMATES OF aN

1997;Mar AND s

^r

< 1 > 1

^aN

1997;Mar

> 0

< 0

1 > r >2

1 >2> r or 2> 1 > r

r >2> 1 or r > 1 >2

2> r > 1

While our empirical specification can exactly identify the

IES, the intratemporal elasticity of substitution, [, is not

directly identified. Tuttavia, based on our model, bounds

on the value of [ can be given. By the definition of Ft, we

know that Ft is an increasing function of Dt=CN

if [ > 1,

T

and vice versa. Inoltre, D1997;Mar=CN

1997;Mar should be

greater than D1997;Feb=CN

1997;Feb due to the lower user cost of

durables in March. Così, it follows that D ln F1997;Mar > 0 if

[ > 1 and D ln F1997;Mar < 0 if [ < 1. On the other hand, it

is mathematically obvious that the term r(cid:2)2

2(cid:2)1 > 0 if s > [ >

1 or s < [ < 1 while r(cid:2)2

2(cid:2)1 < 0 if [ < s < 1 or [ > 1 > s.

Accordingly, once we estimate s and aN

1997;Mar; we can

place a bound on [, as shown in table 1. To demonstrate,

suppose we find that ^r < 1 and ^aN

1997;Mar > 0 (the actual

case we will find below); then we can conclude that [ < s

< 1. Since aN

2(cid:2)1 DlnF1997;Mar, it is

positive when r(cid:2)2

2(cid:2)1 < 0

and DInF1997;Mar < 0: Consequently, we know that either

r >2> 1 O 2< r < 1 should be satisfied. However, the

former condition, r >2> 1, cannot be satisfied with an

estimate of s less than 1; Perciò, the theoretical upper

bound of [ should be the estimated s, ^r.

2(cid:2)1 > 0 and DInF1997;Mar > 0, or r(cid:2)2

1997;Mar corresponds to r(cid:2)2

In addition to the dummies of interest, we add controls

for factors affecting consumption that were excluded from

the theoretical model, such as seasonality, demographics,

and unobservables. The actual regression equation is

DlnCN

io;sì;m ¼ c þ DZmdm þ DXi;sì;m/þ

þ c1996;OctD1996;Oct þ c1996;NovD1996;Nov

þ c1996;DecDDec þ c1997;AprD1997;Apr

i DDy;m þ mN

aN

þ

io;sì;M;

X

(6)

sì;mð

Þ2I

where DZm is the first difference of a vector of month dum-

mies. Consequently, dm represents the seasonal effects.

DXi;sì;m is a vector of (potentially) time-varying household-

specific characteristics, which includes the number of

household members;

the number of working household

members; the number of household members under age 18;

the number of household members above age 65; and inter-

view dummies, which control for ‘‘survey fatigue,’’ the ten-

dency of households to report lower expenditure in later

interviews. It is worth noting that household-specific fixed

effects (or non-time-varying characteristics) are already

controlled for by taking the first difference.

The dummies for October, novembre, and December

1996 (D1996;Oct, D1996;Nov, and D1996;Dec, rispettivamente) are

included to determine whether there was any effect on con-

sumption associated with announcement of the tax rate

increase. The effect is the sum of the income effect and the

intertemporal substitution effect. As we discussed in section

II,

the announcement of the tax rate increase occurred

sometime between October and December 1996; così, it is

preferable to include not a single month but all three month

dummies. The signs of the coefficients associated with each

dummy are, Tuttavia, ambiguous. The income effect should

be negative because the rate increase represents a negative

income shock, while the intertemporal substitution effect

should be positive, reflecting households’ incentive to

increase their consumption during the periods between

announcement and implementation, when the price level

was relatively low. Di conseguenza, the sign of the coefficients

depends on which effect dominated the other.14

Finalmente, mN

io;sì;m is an error term that accounts for unobserva-

bles affecting household consumption of N. Standard errors

are robust to serial correlation within households over time.

IV. Empirical Evidence

UN. Data

We use data from the Japanese Family Income and Expen-

diture Survey (JFIES) to estimate the IES.15 The JFIES is a

rotating panel survey in which households are interviewed

for six consecutive months and approximately 8,000 house-

holds are interviewed each month.16

Our estimates make use of JFIES data from the period

between April 1992 and March 2002, a symmetric five-year

window around the April 1997 rate increase. We choose to

exclude the bubble years before April 1992 because house-

hold expenditures prior to 1992 grew at a much faster pace

than they did after the bursting of the economic bubble in

1991; they remained more or less flat after that. Our sample

period ends in March 2002, which coincided with the

beginning of another boom.

We limit the sample to households that complete all six

interviews, but nearly all households can be used as the

response rate of the JFIES is quite high. Although data for

agricultural households are available in the JFIES after

14 There is also a literature that suggests that the income effect asso-

ciated with a tax change is absent until the tax change is implemented.

Vedere, Per esempio, Watanabe, Watanabe, and Watanabe (2001) and Mer-

tens and Ravn (2012). If this were the case, our estimate of the IES would

be biased upward, as the decline in expenditure from March to April

would capture not only intertemporal substitution but also the negative

income effect.

15 See Stephens and Unayama (2011, 2012) for more information

regarding the JFIES design and content.

16 Until 2002, single-person and agricultural households were excluded

from the JFIES. As of the 2009 JFIES, single-person households com-

posed 11.8% of the population and were responsible for 18.1% of expen-

ditures, while agricultural households accounted for 2% of the population

E 2.1% of expenditures.

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

292

THE REVIEW OF ECONOMICS AND STATISTICS

Variable

Age of head

Number of household members

Number of household members under age 15

Number of household members aged 65 or over

Number of working members

Yearly income

Total expenditure

Excluding tax-exempted items

Nonstorable nondurables (N)

Storable nondurables (S)

Durables (D)

Number of observations

Number of households

TABLE 2.—SUMMARY STATISTICS

Mean

51.5

3.38

0.68

0.47

1.52

7,113

317

221

120

52

47

SD

13.7

1.24

0.98

0.75

0.95

4,652

266

195

78

32

138

Yearly household income and monthly household expenditures are listed in thousands of yen, con 2005 serving as the base year.

Minimum

Maximum

17

2

0

0

0

0

20

15

7

0.58

0

646,900

129,380

99

11

7

4

7

97,043

14,346

9,255

5,523

3,790

7,678

1999, we drop them to maintain consistency over the sam-

ple period. Also, we use male-headed households and those

whose head does not change his job because March is the

end of the fiscal year in Japan, when we observe many job

changes that may cause systematic changes in consumption

around the time of the consumption tax rate increase. IL

sample restrictions leave us with 646,900 observations from

129,380 households. Tavolo 2 presents summary statistics

for our sample.

The JFIES expenditure data are highly disaggregated by

item type, which allows us to accurately categorize goods

and services. It is critical for our purpose to distinguish not

only between taxable and tax-exempt goods and services

but also between N, S, and D. To construct expenditure on

N, we first exclude expenditures on goods and services that

were not subject to the consumption tax. As shown in table

2, expenditure on taxed items was 70% of total expenditure,

while most

tax-exempt expenditure consists of rent for

housing and education (per esempio., tuition for school), which we

would not expect to respond to a tax rate increase in the

short run.

In the next step, we divide goods and services that were

subject to the tax into three subcategories: D, S, and N. Noi

define N as goods and services that are neither storable nor

durable; questo è, they depreciate relatively quickly over time

when not in use, and when in use, they are fully consumed.

Di conseguenza, this category contains goods and services for

which the timing of consumption and expenditure roughly

coincides. Per esempio, fresh fruit, if not eaten, will spoil,

and it

is fully consumed with use. This category also

includes services such as taxi service, which is consumed at

the point of purchase.

We define S as those goods and services that depreciate

slowly over time if not used and fully if used. It follows that

these goods can be stockpiled for future consumption; con-

sequently, consumption and expenditure do not necessarily

coincide. Per esempio, laundry detergent can be stored for

long periods of time with little to no effect on its ability to

clean clothing, but once it is put into use, whatever amount

was used has been fully consumed. This category also

includes rail service, due to the fact that many Japanese

households purchase passes that are good for train travel for

several months. Così, one might expect that a household

would purchase a pass good for several months during a

low-price period and use the pass during a relatively high-

price period.

We define D as goods and services that depreciate rela-

tively slowly over time if not used and do not depreciate

fully with use. Consequently, consumption and expenditure

do not coincide for durables. This category includes tradi-

tional durables such as refrigerators and automobiles, COME

well as goods such as clothing that are classified as semi-

durables in the JFIES. Inoltre, we include a select

group of services such as home repair and tailoring, from

which consumers derive benefits long after the service is

provided.17

We then deflate monthly expenditures on N, S, and D

using tax-inclusive consumer price indices specific to our

categories.18 We are left with real monthly expenditures for

Japanese households from April 1992 through March 2002.

Tavolo 2 shows that more than half of taxable expenditure is

on N, while expenditures on S and D are similar. While it is

known that D may be underreported in the JFIES, this is not

the case for our dependent variable, N (see Unayama,

2011). Consequently, we are relatively unconcerned with

selection issues for nondurable goods and services.

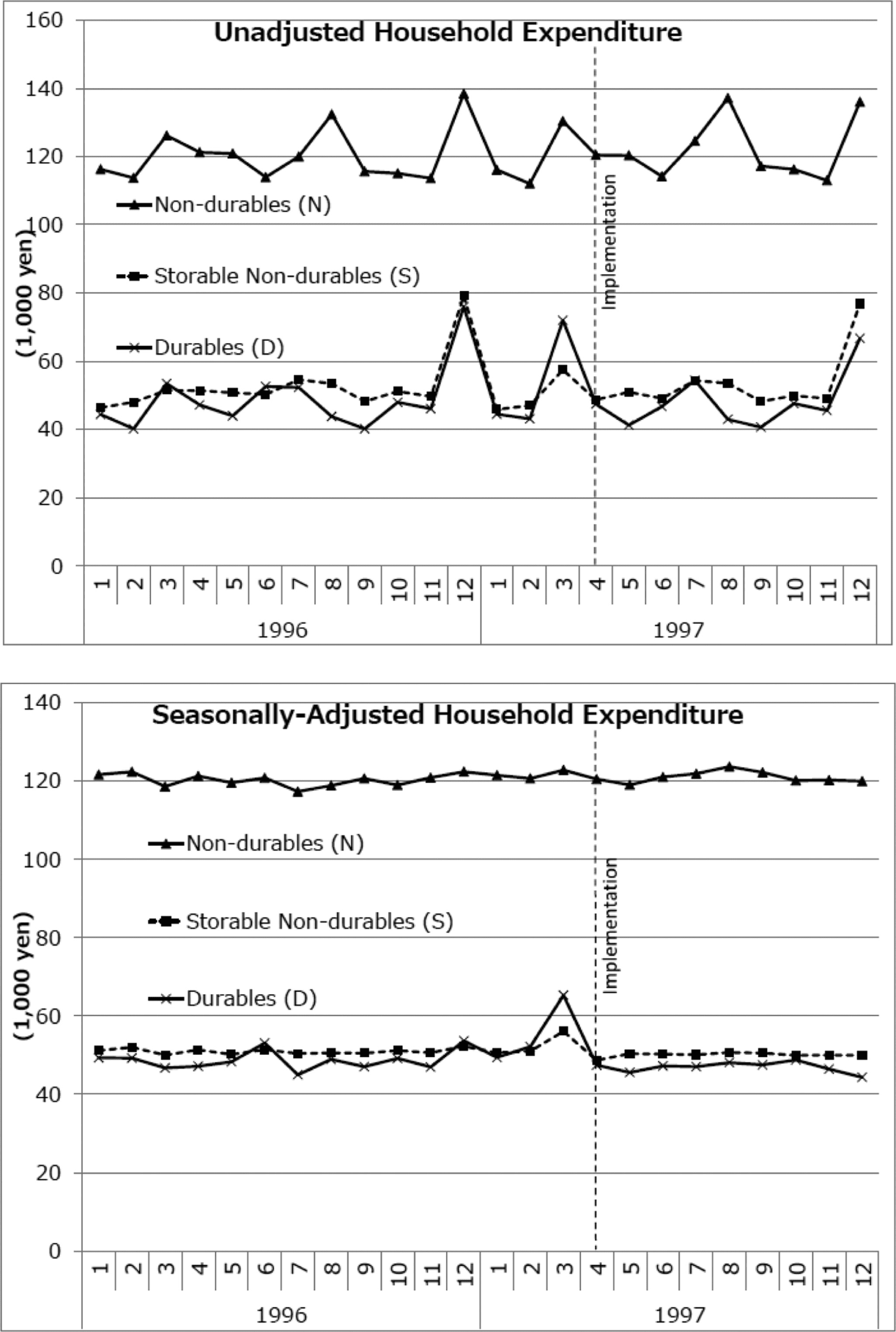

Figura 5 displays plots of unadjusted and seasonally

adjusted real monthly household expenditure on N, S, E

D in 1996 E 1997. Note that once expenditures on N are

seasonally adjusted, as is the case in our empirical specifi-

cation presented in section IIIC, there appears to be rela-

tively little variation in N before and after implementation

of the Consumption Tax increase, while expenditures on S

and D exhibit a large spike in March 1997, followed by

somewhat lower expenditure after the tax increase.

17 See table 2 in the online appendix for our complete categorization of

N, S, and D.

18 In particular, we construct Laspeyres price indices for each of our

four categories using item-specific price indices and expenditure shares in

1990 for each of these items as the weights.

l

D

o

w

N

o

UN

D

e

D

F

R

o

M

H

T

T

P

:

/

/

D

io

R

e

C

T

.

M

io

T

.

e

D

tu

/

R

e

S

T

/

l

UN

R

T

io

C

e

–

P

D

F

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

R

e

S

T

_

UN

_

0

0

5

3

1

P

D

.

F

B

sì

G

tu

e

S

T

T

o

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION

293

FIGURE 5.—JFIES AVERAGE MONTHLY HOUSEHOLD EXPENDITURE, 1996–1997

The figure displays plots of unadjusted and seasonally adjusted real monthly household expenditures

(in thousands of yen) on nonstorable nondurable (N), storable nondurable (S), and durable goods and ser-

vices in 1996 E 1997. The bottom figure, which displays seasonally adjusted household expenditures,

plots the residuals plus the constant term from a regression of real monthly household expenditure on

month dummies, where April serves as the base month. The dashed vertical line represents implementa-

tion of the consumption tax increase in April 1997.

B. Empirical Results

Tavolo 3 presents our estimates for the entire sample based

on the specification given in equation (6). Regression (1)

includes only a dummy for April 1997. In effect, it ignores

announcement and intratemporal substitution effects. Noi

find that expenditure on N fell significantly between March

and April 1997. IL 2.16% decline in expenditure implies

that the intertemporal elasticity of substitution is 0.91. IL

estimate of the IES remains unchanged in regression (2),

which allows for announcement effects, but still these esti-

mates ignore intratemporal substitution.

Regression (3), our baseline specification, adds a first-

differenced March 1997 dummy intended to capture any

intratemporal substitution that resulted from the fall in the

user cost of durables in that month. Inclusion of this

dummy reduces the coefficient associated with the April

1997 dummy from (cid:2)2.16 A (cid:2)0.51. The implied IES is

0.21, which is significantly less than 1 but not significantly

different from 0. The coefficient associated with the first-

differenced March 1997 dummy, aN

1997;Mar, is positive and

significantly different from 0.

Given our interpretation of aN

sì;m in section IIIC and IES

(S) estimate of 0.21, it follows that preferences over dur-

ables and nondurables are nonseparable and that the two

composite goods are strong complements (cioè., [ < s ¼

0.21). Intuitively, this result is derived from the fact that the

fall in the user cost of durables in March 1997 was accom-

panied by an increase in both durable and nondurable

expenditures, while nondurable expenditures

in other

months prior to and following the tax rate increase exhib-

ited little variation. The result is consistent with the findings

of Pakos (2011) and Cashin (2016), but conflicts with the

results of Ogaki and Reinhart (1998), who find an elasticity

of substitution between durables and nondurables that

exceeds 1.19

To develop a better sense of the strength of our comple-

mentarity result, we also examine the contemporaneous cor-

relation between the first difference of the logarithm of

monthly durable and nonstorable nondurable expenditures

over our entire sample period. Figure 4 shows that the price

of durables (relative to nondurables) fell throughout our

sample period. Given this fact, a positive contemporaneous

correlation would be consistent with complementarities.

Indeed, we find a positive and highly significant contem-

poraneous correlation (0.10) between durable and nondur-

able expenditures, which further strengthens our finding

that durables and nondurables are strong complements.20

To consider the possibility that the intratemporal substi-

tution effects persisted beyond March and April 1997 as a

result of durable adjustment costs, regression (4) of table 3

includes additional first-differenced month dummies. In this

case, the estimate of the IES is slightly larger than in the

baseline estimate (0.30), while we cannot reject the null that

all first-differenced month dummies are 0.

Table 4 presents regression estimates intended to test the

robustness of our results. Because seasonal effects may

change over time, a longer sample period could yield an

incorrect estimate of the IES. While we use the symmetric

five-year window from 1992 through 2002 in the baseline,

regression (1) uses a four-year window (1993–2001) and

19 Pakos (2011) demonstrates that Ogaki and Reinhart’s result may be

biased due to the assumption of homothetic preferences. Given homo-

thetic preferences where durables are luxuries and nondurables are neces-

sities, growth in the durable consumption share over time that has accom-

panied a fall in durable prices is incorrectly attributed to the substitution

effect rather than the income effect.

20 Another story, which is consistent with our result, but unrelated to

complementarities between durables and nondurables, is that nondurables

serve as an input to the durable purchase technology (e.g., consuming

gasoline and eating out when purchasing a new television from an elec-

tronics store). Identification of the IES is robust to either story. The differ-

ence is the interpretation of the first-differenced March 1997 dummy.

Under the complementarity story, the dummy captures complementarities

between the service flow from the durable stock and nondurable con-

sumption, while under the other story, it captures the additional nondur-

able purchases that must be made in order to facilitate the increase in dur-

able purchases.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

r

e

s

t

_

a

_

0

0

5

3

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

294

THE REVIEW OF ECONOMICS AND STATISTICS

TABLE 3.—ESTIMATES OF THE INTERTEMPORAL ELASTICITY OF SUBSTITUTION (IES)

DEPENDENT VARIABLE: NONSTORABLE NONDURABLES (DlnCN

i;y;m (cid:8) 100)

(1)

(2)

(3)

(4)

Coefficient

SE

Coefficient

SE

Coefficient

SE

Coefficient

SE

First difference of month dummies

DDFeb,1997

DDMar,1997

DDApr,1997

DDMay,1997

DDJun,1997

p-value for F-test for all DD ¼ 0

Month dummies

DOct,1996 (a)

DNov,1996 (b)

DDec,1996 (c)

DApr,1997 (d)

F-test: (a) þ (b) þ (c) ¼ 0

( p-value)

Implied IES (¼|(d)| divided by 2.39)

[95% CI]

Sample period

Sample restrictions

Observations

1.66**

0.82

NA

NA

0.042**

(cid:2)2.16***

0.78

NA

0.91

[0.27, 1.55]

(cid:2)0.93

1.21

(cid:2)0.05

(cid:2)2.16***

0.78

0.76

0.79

0.78

(cid:2)0.93

1.21

(cid:2)0.05

(cid:2)0.51

0.78

0.76

0.79

0.84

0.23

(0.80)

0.91

[0.27, 1.55]

0.23

(0.80)

0.21

[(cid:2)0.48, 0.90]

0.23

(0.65)

0.30

[(cid:2)0.65, 1.24]

1992–2002

Yes

646,900

(cid:2)1.10

0.56

(cid:2)0.89

(cid:2)1.54*

0.06

0.139

(cid:2)0.93

1.21

(cid:2)0.05

(cid:2)0.71

0.78

0.91

0.94

0.90

0.78

0.78

0.76

0.79

1.15

This table presents estimates from a regression based on equation (6). The dependent variable is the first difference of the logarithm of monthly household expenditures on nonstorable nondurable goods and ser-

vices. Standard errors are robust to serial correlation within households over time. All columns report OLS regressions, which include, in addition to variables in the table, the first difference of month dummies, age

of household head, and the first difference of the following variables: indicators for each interview, the number of household members, working members, members under age 18, and members over the age of 65.

Significant at *10%, **5%, ***1%.

TABLE 4.—ROBUSTNESS TESTS: DIFFERENT SAMPLES

Dependent Variable: Non-storable Non-durables (DlnCN

i;y;m (cid:3) 100)

(1)

Coefficient

1.75**

(cid:2)1.03

1.60**

0.03

(cid:2)0.41

SE

0.83

0.79

0.78

0.80

0.86

0.59

(.407)

0.17

[(cid:2)0.53, 0.87]

1993–2001

Yes

526,612

(2)

Coefficient

1.54*

(cid:2)0.38

1.33*

0.13

(cid:2)0.71

SE

0.85

0.81

0.79

0.82

0.88

1.08

(0.266)

0.30

[(cid:2)0.43, 1.03]

1994–2000

Yes

394,673

(3)

Coefficient

1.79**

(cid:2)0.94

1.60**

0.10

(cid:2)0.86

SE

0.74

0.73

0.71

0.72

0.78

0.42

(.650)

0.36

[(cid:2)0.27, 0.99]

1992–2002

No

764,895

First difference of month dummies

DDMarch,1997

Month dummies

DOct,1996 (a)

DNov,1996 (b)

DDec,1996 (c)

DApr,1997 (d)

F-test: (a) þ (b) þ (c) ¼ 0

( p-value)

Implied IES (¼|(d)| divided by 2.39)

[95% CI]

Sample period

Sample restriction

Observations

This table presents estimates from a regression based on equation (6). The dependent variable is the first difference of the logarithm of monthly household expenditures on nonstorable nondurable goods and ser-

vices. Standard errors are robust to serial correlation within households over time. All columns report OLS regressions, which include, in addition to variables in the table, the first difference of month dummies, age

of household head, and the first difference of the following variables: indicators for each interview and the number of household members, working members, members under age 18, and members over the age of 65.

Significant at *10%, **5%, ***1%.

regression (2) a three-year window (1994–2000). The

resulting IES estimates (0.17 and 0.30, respectively) are

similar to the baseline estimate. Regression (3) removes all

sample selection criteria (e.g., male-headed household, par-

ticipated in all six interviews). The implied IES is the lar-

gest of all our regressions (0.36), but still small and signifi-

cantly less than 1.

Our results are comparable to the results in previous stu-

dies that use macrodata. Hall (1988) summarizes his results

by saying that ‘‘the value may even be zero and is probably

not above .2’’ (p. 350). Ogaki and Reinhart (1998) conclude

that the point estimates fall in a ‘‘range of 0.32 to 0.45’’

when allowing for nonseparable preference (p. 1095);

moreover, Yogo (2004) reports the 95% confidence inter-

vals [(cid:2)0.56, 0.45] using Japanese data between 1970 and

1998 (Yogo, 2004, table 3).

In contrast, studies based on survey data have found lar-

ger estimates of the IES. Attanasio & Weber (2010) sum-

marize their results (Attanasio & Weber, 1993, 1995) as fol-

lows: lower estimates of the IES based on macrodata can be

explained by aggregation bias; once this bias is taken into

account, the IES estimate increases to approximately 0.8

(Attanasio & Weber 2010). Similarly, Vissing-Jorgensen

(2002) obtain point estimates of the IES in the range of 0.8

to 1.0 when accounting for limited asset market participa-

tion. Gruber (2013) obtains an even larger IES estimate of 2

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

9

8

2

2

8

5

1

9

7

4

6

2

5

/

r

e

s

t

_

a

_

0

0

5

3

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

MEASURING INTERTEMPORAL SUBSTITUTION IN CONSUMPTION

295

TABLE 5.—HETEROGENEITY ACROSS HOUSEHOLD TYPES

Dependent Variable: Nonstorable Nondurables (DlnCN

i;y;m (cid:8) 100)

(1)

(2)

(3)

(4)

Coefficient

SE

Coefficient

SE

Coefficient

SE

Coefficient

SE

First difference of month dummies

DDMar,1997

Month dummies

DOct,1996 (a)

DNov,1996 (b)

DDec,1996 (c)

DApr,1997 (d)

1.19

(cid:2)0.82

0.99

(cid:2)0.13

(cid:2)0.57

0.89

0.85

0.81

0.86

0.93

3.95**

(cid:2)1.37

2.28

(cid:2)0.27

(cid:2)0.36

2.00

2.00

2.22

2.05

1.94

1.48

(cid:2)1.88

1.18

0.39

(cid:2)0.36

1.11

1.10

1.06

1.10

1.17

1.70

0.25

1.28

(cid:2)0.74

(cid:2)0.80

1.21

1.09

1.10

1.13

1.22

F-test: (a) þ (b) þ (c) ¼ 0

( p-value)

Implied IES (¼|(d)| divided by 2.39)

[95% CI]

Sample period

Sample group

Observations

0.04

(0.97)

0.24

[(cid:2)0.53, 1.01]

1992–2002

Working

539,073

0.36

(0.62)

0.15

[(cid:2)1.45, 1.75]

1992–2002

No job

107,827

0.23

(0.81)

0.15

[(cid:2)0.81, 1.11]

1992–2002

Higher income

311,837

0.23

(0.55)

0.34

[(cid:2)0.67, 1.34]

1992–2002

Lower income

335,063

This table presents estimates from a regression based on equation (6). The dependent variable is the first difference of the logarithm of monthly household expenditures on nonstorable, nondurable goods and ser-

vices. Standard errors are robust to serial correlation within households over time. All columns report OLS regressions, which include, in addition to variables in the table, the first difference of month dummies, age

of household head, and the first difference of the following variables: indicators for each interview; the number of household members, working members, members under age 18, and members over the age of 65.

Significant at *10%, **5%, ***1%.

when using cross-sectional variation in capital income tax

rates as a source of identifying variation.

We believe that our estimates are preferable to previous

estimates because we use microdata, a natural experiment

approach, an appropriate categorization of nondurables, and

a specification that is robust to nonseparable preferences

between durables and nondurables. The use of microdata

implies that our result

is free from aggregation bias.

Exploiting a natural experiment allows us to avoid the pro-

blem of weak instruments and the potential for correlation

between lagged instruments and contemporaneous con-

sumption growth.21 Restricting the analysis to nonstorable

nondurable goods and services mitigates the concern that

we are capturing an expenditure elasticity rather than the

intended consumption elasticity. Finally, as evidenced by

the results from regressions (2) and (3) in table 3, allowing

for nonseparable preferences has a significant impact on our

estimate of the IES.

It is possible that our small estimate of the IES is attribu-

table to liquidity constraints. Because liquidity-constrained

consumers are less able to smooth consumption across peri-

ods, the estimated IES could be smaller if many households

faced a binding constraint around the time of the consump-

tion tax rate increase. To test for this possibility, we sepa-

rate the sample into groups that are more likely to be liquid-

ity constrained and groups that are relatively less likely to

be constrained. First, we separate working and nonworking

households. While the nonworking group includes unem-

ployed households, most are retired.22 Because retired

households can expect little to no income growth, they are

21 As in this paper, Engelhardt and Kumar (2009) use microdata and an

approach that exploits a natural experiment to find the IES is 0.74. Unlike

other papers (including this one), however, the IES is not derived from

the Euler equation, and as a result, it is difficult to compare to our esti-

mates.

22 More than 90% of nonworking households are aged 60 or older.

much less likely to be liquidity constrained. As regressions

(1) and (2) in table 5 show, the difference in the estimated

IES between working and nonworking is small. A more

conventional method to test for liquidity constraints is to

divide households into higher- and lower-income groups.

The results in regressions (3) and (4) indicate that the IES is

slightly larger for lower-income households. Overall, the

results in table 5 suggest that liquidity constraints are not

responsible for our small IES estimate.

Data quality is another possible explanation why con-

sumption of N was insensitive to the tax rate increase. If

households incorrectly report

their expenditures every

month, the real changes would be attenuated by measure-

ment error, causing our estimate of the IES to be biased

toward 0. To evaluate this, we regress the first difference of

the logarithms of S and (1 þ D) on the same set of vari-

ables.23 Expenditures on S and D should change around

implementation much more than expenditure on N. This is

because S and D are subject not only to intertemporal sub-

stitution in consumption, but also arbitrage effects. Regres-

sions (2) and (3) in table 6, which employ the same specifi-

cation used for N, given in equation (6), show that

expenditures on S and D in March 1997 increased signifi-

cantly. While it is difficult to interpret these coefficients,

the results demonstrate that changes in expenditure are

accurately reported, suggesting that data quality issues do

not preclude us from finding a response to the Consumption

Tax rate increase.

Finally, we consider the announcement effects. Specifi-

cally, we are interested in their sum. We find that the sum is

slightly positive, but does not differ significantly from 0 in

23 A small percentage of households report 0 monthly expenditure on

durables, and as a result, we must take the logarithm of 1 þ D. Results do

not significantly change if we omit households with 0 durable expendi-

tures from the analysis.

l

D

o

w

n

o

a

d

e

d

f

r

o