Finbarr Livesey

The Need for a New Understanding of

Manufacturing and Industrial Policy

in Leading Economies

Ongoing debates about economic growth in the United States and the United

Kingdom following the 2008 financial crisis have given a new primacy to manu-

facturing within the two countries’ respective economies. President Obama’s 2012

State of the Union address focused on manufacturing as the bedrock of future

growth. The contrast to the financial sector was writ large when he said, “We will

not go back to an economy weakened by outsourcing, bad debt, and phony finan-

cial profits” and called for “an economy built on American manufacturing.”1 In a

similar vein, the UK coalition government has focused on the theme of rebalanc-

ing the economy, which is characterized as increasing the role of manufacturing.

David Cameron’s first economic speech after becoming prime minister set the

trend, when he stated, “Our economy has become more and more unbalanced,

with our fortunes hitched to a few industries in one corner of the country, while

we let other sectors like manufacturing slide.”2

It is as yet unclear whether these reactions to the crisis caused by the near col-

lapse of the global financial system represent a well-formed approach to achieving

long-term growth. The rules of the global economic game continue to change, E

the current narratives on the economy, manufacturing, and growth are sadly out of

date. Trapped within a framework that has become less and less representative of

the economy, laden with ideological baggage, and lacking new thinking on how

manufacturing has evolved in terms of production technologies, company organi-

zation, and impact on the economy, it should not be a surprise that our current

responses to the call for rebalancing and growth might be off the mark.

This article investigates attempts by the UK and the U.S. to focus on and pro-

vide support for manufacturing in the wake of the financial crisis. We focus on

these two countries due to the significant attention being paid there to this debate,

and because their actions highlight the general weaknesses in how policymakers

are considering the future evolution of manufacturing.

Finbarr Livesey is Acting Director of the MPhil in Technology Policy and Fellow,

Institute for Manufacturing at the University of Cambridge.

© 2012 Finbarr Livesey

innovazioni / volume 7, number 3

193

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

Finbarr Livesey

FALLING OUT OF LOVE

WITH MANUFACTURING AND INDUSTRIAL POLICY

Nel 40 years since 1970, one trend has stood out for the developed economies of

the G7: manufacturing as a share of national economies has fallen dramatically.3

Across the G7, the greatest decline has been in the UK, where manufacturing has

fallen by 20 percentage points as a share of gross domestic product (GDP), con-

tracting in this sense to one-third of its original size. The United States has seen a

similar contraction of manufacturing during this time, from 24 percent to 12 per-

cent of GDP. Some observers believe that these statistics actually underplay the

depth of the decline in manufacturing in the developed economies. According to

this argument, the loss of manufacturing jobs is not due to rising productivity but

is “a function of slow growth in output . . . caused by a steep increase in the man-

ufactured goods trade deficit.”4

These changes, loosely termed “deindustrialization,” were seen by many to be

almost a natural part of the evolution of leading economies from agriculture

through industry and on to services. Daniel Bell’s influential 1973 book, IL

Coming of the Post-Industrial Society, in many ways created a context in which this

interpretation flourished. This book capped a long-running narrative of progress

in which the leading economies move from the land to industry, then from indus-

try on to services, all the while retaining the high-value elements of research,

progetto, and service delivery.

A strong ideological position appeared in parallel to this characterization of

the economy on the role of government in the economy. This was a reaction in par-

ticular to the strong state intervention that had taken place in many countries,

loosely under the banner of industrial policy. A dominant ideology emerged that

supported government creating an environment for innovation or establishing

enabling conditions, but it did not support sectoral or targeted interventions. For

many at the time, “industrial policy . . . turned out to be an idea with a brief

career.”5

By the turn of the 21st century, it appeared that an “end of policy” had been

reached in Anglo-American policymaking, with almost no dissent on the role gov-

ernment was to play and with manufacturing thought to be a declining and almost

irrelevant force. From this point on, government was to provide funding for

research and then encourage the private sector to take products to market, with no

particular concern for the sectoral composition of the economy. This position was,

and in some cases still is, supported by the concept of a hyper-connected flat world

dependent on knowledge rather than labor. Until the advent of the financial crisis,

this conception of how countries and the global economy worked was not called

into question. Tuttavia, when the crisis hit and attention turned to manufacturing,

a key problem emerged: there was no compelling description of how developed

countries could achieve growth and prosperity based on manufacturing as a key

element of their recovery.

194

innovazioni / Making in America

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

The Need for a New Understanding of Manufacturing and Industrial Policy

THE RETURN OF MANUFACTURING

Given how deeply embedded the narrative on deindustrialization, the knowledge

economy, and the postindustrial society were in the UK and U.S. policy and eco-

nomic thinking, the fact that this narrative has been called into question is an indi-

cation of the depth of the financial crisis. Both the UK and the U.S. turned to man-

ufacturing as a potential route to growth, which in many ways was a reaction

against financial services. What is less clear is whether manufacturing can provide

the desired growth and whether the actions of both governments are as strong as

their rhetoric, as many of the policies are a repackaging of existing or planned pro-

grams.

Britain’s coalition government’s Plan for Growth, which focuses on advanced

manufacturing without defining what is included in the term, has four major ini-

tiatives:6

• Provide funding for Catapult Centres (originally called Technology and

Innovation Centres), with the first being in high-value manufacturing, Quale

would focus on precompetitive development work

• Form nine Centres for Innovative Manufacturing to carry out research on

strategic areas of importance for manufacturing

• Accelerate the relaunch of the Manufacturing Advisory Service to provide

expert advice to manufacturing companies on productivity and innovation

improvements

• Offer an international prize in engineering worth one million pounds (now

termed the Queen Elizabeth Prize for Engineering)

Much of this effort is a continuation of policies that were already in place, con

the exception of the Catapult Centres. The Catapult Centres, loosely modeled on

the German Fraunhofer Institutes, were developed following the Hauser Review,7

which was commissioned by the previous government.8 The high-value manufac-

turing Catapult is the first of what will be 10 such centers, and it claims to include

“all forms of manufacture using metals and composites, in addition to process

manufacturing technologies and bio-processing,” with the aim of drawing on

“excellent university research to accelerate the commercialization of new and

emerging manufacturing technologies.”9

At the core of the government’s approach is rebalancing the economy, although

the specifics of what rebalancing means are as yet undefined. The share of the

economy in manufacturing versus that of financial services, the location of activi-

ty in the south versus the north of the UK, and the levels of public and private debt

are all mentioned, but no clear definition is given for a balanced economy, nor is it

explained how each of the tradeoffs should be resolved.

The policy response in the U.S. has some similar patterns but it appears to take

a more holistic view of manufacturers. There are three main elements in the

administration’s response:10

• Support advanced manufacturing through the Advanced Manufacturing

Initiative, specifically the Advanced Manufacturing Partnership11

innovazioni / volume 7, number 3

195

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

Finbarr Livesey

• Promote a campaign to have companies manufacture in America via the

Manufacturing Extension Partnership

• Provide tools and incentives for companies to reshore (return to the U.S.)

some of their manufacturing activities (the Reshoring Initiative)

A National Network for Manufacturing Innovation was recently announced,

which is similar to the Catapult Centre under development in the UK. This net-

work of centers is intended to “integrate capabilities and facilities required to

reduce the cost and risk of commercializing new technologies and to address rele-

vant manufacturing challenges on a production-level scale.”12 However, these cen-

ters have yet to be established; there is a call for input (open until the end of

ottobre 2012) on how the network should be structured, and a request for propos-

als for a pilot center focused on additive manufacturing was recently closed.13

Finalmente, the Obama administration has proposed removing tax breaks for compa-

nies that move their production overseas and giving a tax break to companies that

bring their production back to the U.S., although this has yet to be taken up by

Congress.

Fundamental to the U.S. response is a focus on advanced manufacturing, COME

highlighted in the report by the President’s Council of Advisors on Science and

Tecnologia (PCAST) entitled “Ensuring American Leadership in Advanced

Manufacturing.”14 The report explicitly rejects industrial policy in favor of innova-

tion policy and focuses on manufacturing that is based on new technologies. IL

emphasis on advanced manufacturing is also written into legislation; the America

Competes Act calls for a strategic plan to guide federal investment in supporting

advanced manufacturing research and development.15 Earlier this year, IL

National Science and Technology Council’s Interagency Working Group on

Advanced Manufacturing released “A National Strategic Plan for Advanced

Manufacturing” in response to the act,16 which builds on the PCAST report, and a

new interagency National Program Office has been founded at the National

Institute of Standards and Technology to bring together the federal agencies that

have manufacturing-related missions with fellows from academia and industry.17

Both UK and U.S. policies created after the financial crisis recognize the need

for a new approach to growth and acknowledge that manufacturing has been neg-

lected, although it has a role to play in both economies. Tuttavia, these changes

mask how much of the old narrative has survived the crash, such as government

setting enabling conditions and the West being the dominant location for research

and innovation.

BADLY BUILT FOUNDATIONS

The fall and rise of manufacturing’s importance to policymakers in the U.S. E

the UK is being played out against a significant weakness: the frameworks used to

describe the economy, in particular the large-scale structure of the economy, are

out of date.

196

innovazioni / Making in America

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

The Need for a New Understanding of Manufacturing and Industrial Policy

Analysis of the economy at the national or global level is mediated by the

frameworks available to describe the elements of the economy and how they are

changing over time. This may appear obvious to many, but when the structure of

companies and the nature of manufacturing is changing so rapidly, it causes a

problem. Not only are the categories used to discuss the economy out of date,

which creates tensions that do not actually exist, old divisions also are kept alive

well beyond their “use by” date.

The roots of the current narrative on the economy and the intrinsic separation

of manufacturing and services go back to 1937, when the Interdepartmental

Committee on Industrial Classification was formed in Washington, D.C.18 This

committee was formed to provide a standard set of definitions so that data collect-

ed by different agencies could be compared and combined. In taking on the task,

the committee immediately separated the economy into manufacturing industries

and nonmanufacturing industries. This fracture has lived on in the U.S. classifica-

tion codes and is also reflected in the approach taken in the UK, with clear water

between the manufacturing elements of the economy and those based on services.

Even if the description of the economy as having distinct categories of those

who make and those who serve was once accurate, it is fundamentally misleading

when discussing modern companies and industrial organization. A rising trend of

“servicization”—where manufacturers offer services based around the product and

extend their offering—has made explicit how companies regarded as manufactur-

ers have a significant portion of their activity and revenue based in providing serv-

ices.19 It appears that over half of U.S. manufacturing companies with 100 or more

employees are servitized; in other words, the majority of U.S. manufacturers offer

services of some kind. The level of servitization globally is approximately 30 per-

cent, with significant variation and growth; Per esempio, China moved from 1 per-

cent to 19 percent servitization between 2007 E 2011. Inoltre, companies

carry out a broad array of activities, which include production but in many cases

span research, progetto, service provision, and end-of-life management.

Unfortunately, the definition—and, more importantly, the study—of industries

has in many ways passed out of fashion just as we need such studies to be carried

fuori. “In both economics and management, the focus of analysis has moved in the

last half century from industry to ‘inside the firm’ . . . Industrial economics gave

way to business economics and organization economics, based on game theoretic

frameworks, principal-agent theory, contracting and incentive theories.”20 This is

also reflected in how governments have addressed issues of growth and support for

industry. Because of this, much of our analysis, the responses generated, and the

narrative developed around manufacturing in the economy may be off the mark.

Our tools for analyzing the economy simply are not up to the job.

Trajectories of Scale and Scope

Besides having an overarching framework that is, at best, out of date to describe

and interpret the economy, the policy responses in the U.S. and the UK appear to

innovazioni / volume 7, number 3

197

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

Finbarr Livesey

have unwittingly adopted a key part of the old narrative—that our future in man-

ufacturing lies only with sophisticated products and processes that are linked to

new science and technology. This ignores contextual changes that are occurring in

the global economy, and in many cases inadvertently implies both complex prod-

ucts and processes. Tuttavia, where production is located and what it is producing

are intimately linked to both the global economic context and the types of produc-

tion processes available.

It is important to realize that, over time, various industries have evolved the

scale of production at which they operate—which can be thought of as either the

efficient plant size for a given industry or the typical batch size in production—and

the degree to which their products are produced in a global value chain or close to

the customer and their point of use, which in some sense is a distance measure.

While not suggesting that there is a single pattern or trajectory, many industries

begin with relatively low volume and limited geographic spread, and over time

move into higher volume with a larger global footprint for their production and

value chain.

The historic pattern is different for every industry, as each starts its lifecycle at

different points in time and faces different constraints, such as whether there is a

need for significant labor input or if there is access to specific raw materials and

leading science and technology inputs. There has been a general trend over the

past 50 years toward global value chains, and the scale of production has increased.

Per esempio, in the early 1970s, 91 percent of automobile production was concen-

trated in the U.S., Japan, and Europe. Today there is major investment in automo-

tive production in emerging markets, and the share of production in the top three

regions has fallen to 54 percent.21 The publishing industry, which began with

Guttenberg producing books one at a time, now has global distribution via online

retailers such as Amazon. Inoltre, the possibilities of digital printing on demand

have started to bring the consumption and the production of each book together.

Many studies of globalization and internationalization provide a dominant

view of the development path of industries and, potentially, countries. In this view,

companies and industries develop and mature in the West, then send their produc-

tion activities overseas, where they can lower input costs and open new markets.

Tuttavia, the interaction of production technology, global trends, and government

action is complex, and it will determine at what volume and how far from the user

companies will decide to produce for any given industry.

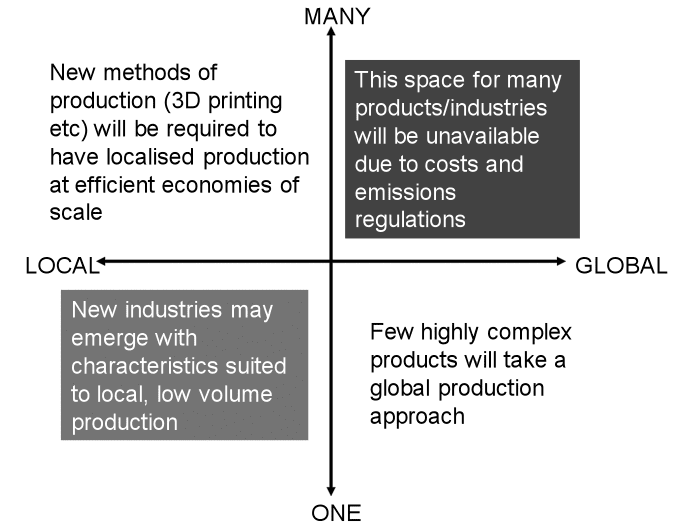

There is a potential inflection point where global value chains are no longer

viable, due to rising costs such as oil, transportation, and labor, and the greater reg-

ulation of transport emissions. Current discussions on re-shoring, bringing activ-

ities back within the company’s home country, and near-shoring, having activities

in a country usually bordering the home country, are expressions of this, but they

do not yet take into account a potential doubling of the price of oil in the next 10

years (admittedly, future oil prices are notoriously hard to predict) or more strin-

gent regulation of emissions in transportation.22 At the same time, new manufac-

turing technologies will possibly allow for smaller scale production and fewer pro-

198

innovazioni / Making in America

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

The Need for a New Understanding of Manufacturing and Industrial Policy

Figura 1. Long-term options for manufacturing organization

duction steps, such as 3D printing, the use of biomaterials, or advances in nanofab-

rication.

Bringing these together suggests that the long-term pressures will result in

fewer truly global value chains and potentially significant amounts of low-volume

manufacturing close to the consumer (see figure 1).

Current UK and U.S. approaches to supporting manufacturing do not appear

to have this kind of vision for the long-term trajectory of industry, and in that

sense they appear to be reverting to the narrative of the past 40 years, in which the

leading economies target advanced manufacturing based on advances in science

and technology that lead to new products. NOI. policies do appear to focus on

process innovations for manufacturing, but there is no clear discussion of scale or

of how the interaction of location and scale of production may lead to a new indus-

trial organization.

An “Industrial Commons” Fit for Purpose

The current policies being promoted in both the UK and the U.S. are essentially a

reaction to the financial crisis. Primarily responsive, they are to a great extent a

repackaging of programs that were either in place or in planning before the crisis

hit. Both governments appear to lack a long-term vision for manufacturing, E

innovazioni / volume 7, number 3

199

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

Finbarr Livesey

thus risk supporting an out-of-date narrative on what companies need and what

companies will do as the global context rapidly changes.

This is important for two key reasons: (1) the organization of industries based

on more localized production is radically different from what we have today,

implying significant changes in the patterns of global trade; E (2) a new under-

standing is needed for how the industrial commons—“the collective R&D, engi-

neering, and manufacturing capabilities that sustain innovation”23—should be

structured.

As multinational enterprises emerged and trade expanded during the last

quarter of the 20th century, there was a significant rise in the trade of intermediate

or unfinished goods.24 This implied a fragmentation of production, with different

stages of the production process for more products taking place in different coun-

tries. Tuttavia, as industries adapt to conditions that favor smaller scale produc-

tion with shorter supply chains and fewer production steps, it is likely that those

activities will be contained within smaller geographic boundaries.

This is much more than simply re-shoring or near-shoring; it reflects a radical-

ly different global economy, potentially with significantly lower overall trade.

Inoltre, if many industries move to lower-scale, localized production structures,

trade will be replaced by ownership. This is a very important point of discussion

for open economies like that of the UK, as it raises the following question: if the

productive assets within the country are foreign owned, how will UK companies

access production? Inoltre, if foreign countries restrict the ownership of pro-

duction assets, access to emerging markets may be highly constrained.

These changes would imply a need for a new “industrial commons” and a rad-

ically different approach to industrial policy in the West. How production might

be organized at this scale is an open question. Per esempio, companies might have

many small, widely distributed production facilities, or many companies might

share a large, flexible facility that they use on an as-needs basis. Again, these dif-

ferent modes of industrial organization imply different things for the industrial

commons, and for the type of support needed from government. There is a danger

that current policies are not well suited to such a context and will not provide the

foundation for either the UK or the U.S. to move toward this new industrial struc-

ture at the national or international level.

CHALLENGES AND OPPORTUNITIES

In addition to challenging the models of growth in developed economies, these

changes may offer significant opportunities to emerging economies. In terms of

development, building an industrial commons based around more localized,

smaller-scale production would allow countries to link directly to leading-edge

production, with potentially lower levels of investment required for each produc-

tion facility. Multilateral funders may also need to update their narrative on man-

ufacturing in the ways the U.S. and the UK governments have yet to do, which may

be a key task for future industrial development in emerging economies.

200

innovazioni / Making in America

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

The Need for a New Understanding of Manufacturing and Industrial Policy

In all cases, a number of challenges and open questions remain, which are

being discussed to a greater or lesser extent in the U.S. and the UK. One is whether

this version of the industrial future will create significant job growth, even with a

significant increase in manufacturing activity.25 Given the likely level of automa-

zione, the use of digital technologies to prototype, and the potential reduction of

waste (cioè., products are made on demand rather than to inventory), how such an

industrial future will play out in terms of employment is unclear. This is a difficult

political message; if manufacturing provides headline GDP growth but does not

create jobs in the sector, it may be viewed as a failure. Whether this is offset by

increased employment in related and dependent sectors will be key to manufactur-

ing being viewed in a positive light and as a strong catalyst for long-term growth.

A second point is that, in a more localized manufacturing environment with

significantly reduced need for trade, ownership of productive assets matters more.

This may challenge openness to foreign direct investment (FDI) in countries that

want to favor nationally based companies, and it may make protectionism against

FDI easier to engage in. Tuttavia, countries like the UK, which operate a very open

economy and depend on the forces of globalization to work in their favor, may

have a problem if little of the manufacturing base is owned by British companies.

Allo stesso tempo, the government, depending on how rules on the repatriation of

profits and corporate taxes are structured, may have an issue with the level of

income that goes from industry to the exchequer.

Finalmente, each industry will have a different trajectory over time, and adapting

to those changes over time will be a constant challenge for national policymakers.

The capacity for developing strategy within government relative to manufacturing

has eroded significantly over the past 30 years, and investments in foresight, hori-

zon scanning, and economic modeling are therefore needed to provide the kind of

input that the changes in the manufacturing landscape imply.

Changing the narrative on the likely development of manufacturing across

existing and new industries will not be a simple process. This article has focused

on the UK and the U.S. and their responses to the financial crisis, based on their

renewed focus on manufacturing. Their policies are examples of how many gov-

ernments are using an out-of-date narrative when developing policies to support

manufacturing and lack a vision for the long-term future of the sector. These weak-

nesses may hamper future growth that is based on manufacturing, and in some

cases could lead countries to a point where they cannot access manufacturing, due

to a lack of the appropriate commons. This article has described a simple frame-

work for discussing how manufacturing industries may evolve, and it is our hope

that this will serve as a jumping-off point for a larger discussion in both developed

and developing economies, to the benefit of the global economy.

1. Full text of the 2012 State of the Union address is available at http://www.whitehouse.gov/the-

press-office/2012/01/24/remarks-president-state-union-address.

innovazioni / volume 7, number 3

201

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023

Finbarr Livesey

2. See http://www.number10.gov.uk/news/transforming-the-british-economy-coalition-strategy-

for-economic-growth/ for a full transcript of the speech.

3. All figures for manufacturing refer to ISIC D and are taken from the United Nations National

Accounts Main Aggregates database, which is available at

http://unstats.un.org/unsd/snaama/introduction.asp.

4. R. Atkinson, l. Stewart, S. Andes, and S. Ezell, Worse Than the Great Depression: What Experts

Are Missing about American Manufacturing Decline. Washington, DC: The Information

Technology and Innovation Foundation (ITIF), 2012.

5. R. Norton. “Industrial Policy and American Renewal,” Journal of Economic Literature 24, NO. 1

(1986): 1-40.

6. HM Treasury, The Plan for Growth. London: HM Treasury, 2011.

7. H. Hauser, The Current and Future Role of Technology and Innovation Centres in the UK.

London: Department of Business, Innovation and Skills, 2010.

8. The formal action to commission the Hauser review is contained in Going for Growth. London:

Department of Business, Innovation and Skills, 2010. Available at

http://dera.ioe.ac.uk/465/1/GoingforGrowth.pdf.

9. For more detail, see https://catapult.innovateuk.org/en_GB/high-value-manufacturing.

10. Much of the detail on the U.S. position on support for manufacturing is collected at

http://www.manufacturing.gov.

11. For full details of the partnership, see http://www.manufacturing.gov/amp/amp.html.

12. Federal Register 77 FR 26509, May 4, 2012.

13. Full details of the request for proposals for the Additive Manufacturing Innovation Institute

are available at http://www.manufacturing.gov/amp/news-050912.html.

14. PCAST, “Report to the President on Ensuring American Leadership in Advanced

Manufacturing,” Executive Office of the President, 2011. Available at

http://www.whitehouse.gov/sites/default/files/microsites/ostp/pcast-advanced-manufacturing-

june2011.pdf.

15. HR 5116.

16. NSTC, “A National Strategic Plan for Advanced Manufacturing,” Executive Office of the

President, 2012. Available at

http://www.whitehouse.gov/sites/default/files/microsites/ostp/iam_advancedmanufacturing_st

rategicplan_2012.pdf.

17. More detail on the NPO can be found at http://www.manufacturing.gov/amp/ampnpo.html.

18. This section is based on E. Pearce, “History of the Standard Industrial Classification,” U.S.

Bureau of the Budget, Office of Statistical Standards, 1957.

19. See A. Neely, “Exploring the Financial Consequences of the Servitization of Manufacturing,"

Operations Management Research 2, NO. 1 (2009): 103-118; UN. Neely, O. Benedittini, and I.

Visnjic, “The Servitization of Manufacturing: Further Evidence,” presentation at EurOMA

Conferenza, Cambridge, England, Luglio 2011.

20. M. Sako, “Do Industries Matter?” Labour Economics 15 (2008): 674-687.

21. M. Holweg, P. Davies, and D. Podpolny, “The Competitive Status of the UK Automotive

Industry,” commissioned report for the New Automotive Innovation and Growth Team, 2009.

22. Vedere, Per esempio, J. Benes et al. “The Future of Oil: Geology versus Technology,” IMF working

paper WP/12/109, 2012.

23. G. Pisano and W. Shih, “Restoring American Competitiveness,” Harvard Business Review (Luglio-

agosto 2009).

24. R. Feenstra, “Integration of Trade and Disintegration of Production in the Global Economy,"

The Journal of Economic Perspectives 12:4 (1998): 31-50; D. Marin and T. Verdier,

“Globalisation and the New Enterprise,” Journal of the European Economic Association 1, NO.

2/3 (2003): 337-344.

25. See E. Brynjolfsson and A. McAfee, Race against the Machine: How the Digital Revolution Is

Accelerating Innovation, Driving Productivity, and Irreversibly Transforming Employment and

the Economy. Boston: Digital Frontier Press, 2011.

202

innovazioni / Making in America

Scaricato da http://direct.mit.edu/itgg/article-pdf/7/3/193/704947/inov_a_00146.pdf by guest on 08 settembre 2023