Ashirul Amin

The Challenge of Combining

Credit and Savings

Innovations Case Discussion:

Jipange KuSave

Every once in a while, an initiative comes along that manages to elegantly combine

the essence of existing programs with something new whose utility is more than

the sum of its parts. Jipange KuSave (JKS) seems to be such an initiative. JKS offers:

• Both a credit and a savings product under the same rubric

• Immediate connectivity to the M-PESA system

• Significant flexibility in catering to the idiosyncratic needs of its clients

JKS “lends to save.” To appreciate this seemingly contradictory notion, we must

first appreciate the quite different but complementary properties of credit and sav-

ing. As Collins et al. have amply illustrated, the poor often have to make do with

an income that is small, irregular, and uncertain.1 This makes saving up hard to

do.2 The poor can and do save regularly, but this activity tends to be focused on

meeting regular expenses that do not coincide with cash inflow, rather than on

building savings for the long term or for emergencies. Inoltre, even if building

long-term savings is the intention, the overwhelming urgency of immediate needs

often disrupts the discipline needed to accumulate a significant sum.

Credit addresses that problem by providing funds up front and when needed,

and imposing a greater degree of the discipline required to pay small amounts fre-

quently over a set period of time. In a way, the client is “saving down,” repaying a

loan that is essentially an advance against future savings.3 However, there is an

underlying concern that credit often traps the poor into a repayment cycle in

which they are constantly repaying loans taken to deal with unforeseen expenses,

and never really saving in the true sense of the word.

How is it possible to combine the features of the two? At its core, JKS emulates

Rutherford’s pioneering work with SafeSave’s P9 program in Bangladesh. JKS

holds in escrow a significant portion of the loan that is taken out, often between a

third and half of the notional amount, and earmarks that as “savings” for the

client. The client then first pays up the loan amount that was actually disbursed,

and then pays up to replace the amount held in escrow with actual savings. In

doing so, JKS, like P9, transfers the loan repayment to build up the client’s savings.

Ashirul Amin is a PhD candidate and doctoral fellow at the Hitachi Center for

Technology and International Affairs at The Fletcher School, Tufts University.

© 2012 Ashirul Amin

innovazioni / volume 6, number 4

43

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023

Ashirul Amin

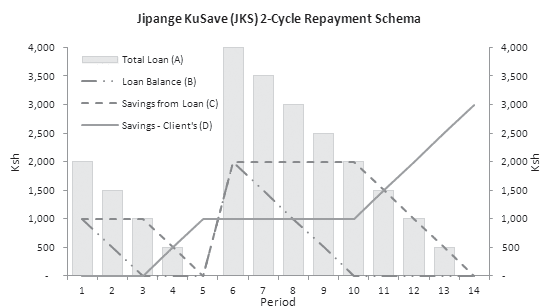

Figura 1. The Interplay of Credit and Savings Facilitated by Jipange KuSave

By starting with a small amount and “bootstrapping” up, the client can eventually

build a sizeable savings (Guarda la figura 1).

Figura 1 allows us to appreciate the fungible nature of the cash flows that result

in accumulated savings. Assuming that a client takes out a Ksh 2,000 loan (UN) E

“saves” 50 percent of it in period 1, he has a savings in escrow amount (C) of Ksh

1,000, but the amount he has actually saved through his own cash flow (D) È 0. If

he pays Ksh 500 in both period 2 and period 3 toward the outstanding loan bal-

ance (B), by period 4 he’s substituting the amount “saved” from the loan (C) con

his own savings (D). By period 5, he will have savings of Ksh 1,000.

The cycle repeats itself from period 6 if the client borrows another Ksh 4,000,

of which 2,000 is “saved” (C). C starts being replaced with actual savings, D, In

period 11, once outstanding balance (B) is zero again, and climbs to Ksh 3,000 by

period 14. Note that this is the combination of the Ksh 1,000 from the first cycle,

together with the Ksh 2,000 from the second cycle that was initially held in escrow

as savings.

By the final cycle, the client has had access to Ksh 3,000 of readily available

funds and accumulated savings of Ksh 3,000.

JKS adds two delectable features to this. The first is the automatic access to the

M-PESA platform and all its benefits, from intermediating existing bank balances

to paying bills to transferring funds to others. Even for an industry that has been

innovative in solving the “last-mile” problem around the world, inclusion in an

electronic ecosystem that functions in near real time is groundbreaking. This com-

mitment to remaining at the forefront of innovation is also reflected in JKS’s real-

time CRM system, which allows staff to monitor the program’s performance met-

44

innovazioni / Inclusive Finance

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023

Liquidity and Savings in the Age of M-PESA

rics on a day-by-day basis—something very valuable for a program that by design

embraces significant volatility.

The second key feature of JKS is its flexibility. Both draw-down and repayment

options are dictated by the loan recipient. Clients can take out a lump sum only

when they need it and repay it at their convenience. JKS has automated the process,

so once a loan is repaid, a new loan can be issued within an hour, pending confir-

mazione. Clients do not even have to show up at meetings or stand in lines, as all

the advantages offered by JKS are accessible via the humble cell phone.

The savings side of the program is less flexible. While JKS is not a compulsory

savings product, withdrawing before the savings goal is reached incurs a penalty.

Clients seem to respond positively to this incentive because it helps them build up

significant savings. Incidentally, clients note that JKS is but one of the savings

instruments they use, some of the others being Equity Bank accounts and M-PESA

itself. This reiterates JKS’s positioning as a niche product that clients use to access

short-term credit and invest in long-term savings.

JKS seems to be a mobile-based program that provides a huge amount of flex-

ibility on variable loan amounts that are available on very short notice, while

simultaneously enabling clients to build up significant savings in a relatively short

period of time. Is there anything that should give us pause?

Well, for one, the pricing of the product from the client’s point of view calls for

some reflection. The program is zero interest for the client, but it certainly is not

zero cost—and understandably so. JKS is designed as a fee-based product, Dove

the client is charged upon use, per use. Così, there is an account activation fee, an

origination fee of 2 percent to 5 percent for each cycle, and an early savings with-

drawal fee of 5 per cento. These charges can be translated into a representative annu-

al percentage rate (APR) or an effective interest rate (EIR), which in turn allows

apples-to-apples comparisons between loan products. Tuttavia, as the case points

fuori, this does not always make sense.

Specifically, this does not make sense if the draw downs are sporadic, because

APR/EIR inherently assumes that the loan tranches are rolled over and the effec-

tive interest charges occur back to back, which in turn justifies compounding over

relevant periods. If a client borrows Ksh 2,000, repays it in two weeks, does not

draw down the next Ksh 4,000 within another month but repays again within two

weeks, the simple APR/EIR calculations cannot be used and more sophisticated

techniques come into play. D'altra parte, as the case candidly points out, if

the client goes through cycles sequentially, the APR can become staggering, E

increasingly so as repayment cycles get shorter. So which is the more appropriate

scenario for JKS?

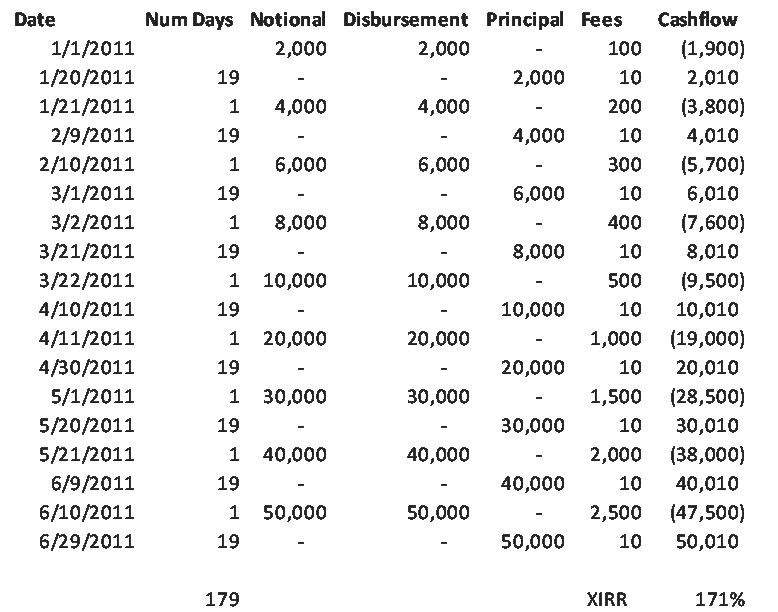

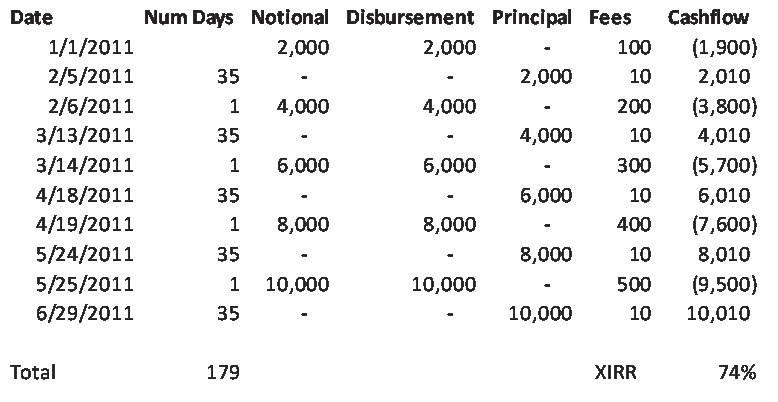

The suggested plans seem to be six months long and involve consecutive draw

downs. The smallest plan has a monthly savings goal of Ksh 2,500, which leads to

accumulated savings of Ksh 15,000. The largest plan has a goal of Ksh 100,000,

with a monthly savings target of Ksh 16,700. From JKS’s point of view, the interest

rates charged are 74 percent for the Ksh 15,000 plan and 171 percent for the Ksh

100,000 plan, as outlined in Tables 1 E 2.4 Note that we use the XIRR function in

innovazioni / volume 6, number 4

45

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023

Ashirul Amin

Tavolo 1. Illustrative Ksh 15,000 Savings Plan

Tavolo 2. Illustrative Ksh 100,000 Savings Plan

46

innovazioni / Inclusive Finance

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023

Liquidity and Savings in the Age of M-PESA

Excel to compute this rate, which allows us to incorporate cash flows made on

dates that are not on a regular schedule.

This is not the end of the story of equivalent interest rates, Tuttavia, because

the payment plan looks significantly different from the client’s point of view. IL

client only receives half the loan that is earmarked, and receives the other half as a

cumulative lump sum at the end of the savings period. In other words, we cannot

treat the balance held in escrow the same way we treat the credit balance. This “sav-

ings” amount is not only not being put to productive use by the client, it also is not

earning interest, as most savings accounts do. Inoltre, banks in Kenya gener-

ally offer savings accounts that cost nothing to maintain (though there sometimes

are withdrawal fees), so one could even argue that the entire 5 percent cost of the

notional amount should be borne by the amount that is actually drawn down and

not be spread over both the drawn-down and saved portions.

Accommodating each of these notions potentially engorges the equivalent-

interest-rate figure spectacularly and is a good candidate for detailed study.

Tuttavia, we should keep in mind that not all clients will engage in scheduled

rollovers as envisioned by the savings plans. Per esempio, using the numbers from

the Stage I pilot, we see that the 10 percent of borrowers who repaid their loan

within three weeks and moved on to subsequent cycles were exposed to significant

levels of APR-equivalent costs. D'altra parte, only 25 percent had paid a third

of their outstanding loan after two months, so three-quarters of its clients were

stretching out payments significantly, thus reducing the effective interest rate they

were exposed to. Those who diligently paid up early essentially subsidized the lag-

gards and delinquents.

The million dollar question (literally) is whether JKS will grow into a mature

financial services product that satisfies a niche demand that other products do not,

or remain a showcase of technological innovation that never made it past the pilot

phase.

The challenges for JKS are not trivial by any measure. Acquiring or otherwise

securing access to the appropriate licenses and satisfying regulatory requirements

will be crucial to JKS continuing operations. The regional offering to 10,000

potential clients will also demonstrate whether large-scale demand for the product

exists, and whether 300,000 clients is a realistic target. Banks can be expected to be

wary of the underlying risk because of the open-ended nature of the loans, E

thus to apply different treatment to the savings and credit components. Note that

the credit component is similar to a line of credit, but without the heavy due dili-

gence or underlying collateral that usually accompanies such arrangements. JKS’s

chances of finding a suitor will increase significantly if it can establish the feasibil-

ity of the product over a period of time, based on analyses of how a critical mass

of clients performs after the regional rollout. Until then, banks may prefer to act as

a conduit, rather than carrying the accounts on their books.

The M-PESA charge associated with making each payment, around Ksh 10,

does make the cost of making frequent repayments in small amounts somewhat

expensive, which could act as an impediment to more widespread adoption of the

innovazioni / volume 6, number 4

47

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023

Ashirul Amin

Prodotto. Per esempio, a client will conceivably prefer to save up to Ksh 1,000 Sopra

the course of ten days, instead of sending over about Ksh 100 every day or as it

becomes available. Negotiating reduced rates for making a certain number of pay-

ments per month would certainly make it easier for clients to save, and thus

increase clients’ propensity to pay down outstanding balances.

But perhaps the biggest challenge is to make sure that JKS is offering a prod-

uct that is financially sustainable. There is no doubt that there is an incipient

demand for the underlying product, even if the exact scale of the demand is still

unclear. The product is simple, flexible, and accessible. Figura 3 of the case suggests

a fairly low overhead structure, which implies that if JKS can retain clients, its life-

time economic value will be quite attractive. Given the iterative nature of product

development, the product itself can be expected to be client relevant, which would

contribute to client retention.5

The most significant determinant of financial sustainability will probably be

how JKS handles delinquencies. For a product that encourages clients to repay

when they can and does not impose penalties for not repaying a loan, it is conceiv-

able that repayments will slip more than a standard credit product, even with

incentives such as access to a larger sum at the next cycle and accrued savings.

Figura 3 in the case suggests a recognized loan loss level of about 10 per cento. Three

things must be kept in mind when evaluating this figure:

• Given the generous terms of the product, loan losses may not be recognized for

a while.

• Clients do not default immediately. Many repay the first couple of tranches and

then default.

• As JKS goes from 1,000 clients to 10,000 and more, its books will grow expo-

nentially within a short period of time. This new funding will dilute underly-

ing defaults from older vintages.

The net effect of this will be that JKS will not be exposed to the full delinquen-

cy level at a steady rate for years. Ma, when it does catch up, it has the potential to

severely disrupt the liquidity position of the financial company housing the prod-

uct. The good news is that JKS seems to have the monitoring and surveillance tools

in place that can track the performance of vintages on a regular basis, and has

already shown the organizational acumen to adapt deftly to changing portfolio

characteristics.

1. Daryl Collins et al., Portfolios of the Poor: How the World’s Poor Live on $2 a Day (Princeton, NJ:

Princeton University Press, 2009).

2. Stuart Rutherford, “Saving Up Is Hard to Do,” CGAP, microfinance blog. Available at

http://microfinance.cgap.org/2011/05/16/saving-up-is-hard-to-do/.

3. Collins et al., Portfolios of the Poor.

4. Assumptions: each cycle is of equal length, client rolls over to subsequent cycles the day after

repayment, there is a 5 percent origination charge, and a Ksh 10 M-PESA fee per repayment.

Account activation fee is ignored.

5. As opposed to the “build it and they will come” approach for a product perceived to be superior,

or the reliance on superior marketing to promote an otherwise unremarkable product.

48

innovazioni / Inclusive Finance

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/4/43/704814/inov_a_00099.pdf by guest on 08 settembre 2023