Ann-Kristin Achleitner, Andreas Heinecke,

Abigail Noble, Mirjam Schöning, E

Wolfgang Spiess-Knafl

Unlocking the Mystery

An Introduction to Social Investment

The field of social entrepreneurship has changed significantly over the past decade.

Traditional sources of funding, such as charitable donations, foundation grants,

and government subsidies, are not keeping pace with the innovations social entre-

preneurs are creating to address the world’s most intractable problems. As social

enterprises have gained scale and credibility, new funding sources have emerged

that aim to provide both financial and social returns to the investor.

Social investment or impact investment, as this form of financing is often

called, provides an important complement to grants and government subsidies.

Social investors typically invest in organizations that have a strong mission of

social change and generate an income but are not yet considered commercially

attractive.

Paradoxically, while successful social entrepreneurs with proven track records

face a chronic lack of capital, social investors say the opportunities to invest are

limited. Tuttavia, it is more than a simple market inefficiency that must be solved.

When social investors and social enterprises do not transact, it is often because the

skills and expertise needed to achieve a particular objective are not understood.

The best of intentions on both sides cannot prevent such deals from failing.

Ann-Kristin Achleitner holds the KfW Endowed Chair in Entrepreneurial Finance

and is Scientific Director of the Center for Entrepreneurial and Financial Studies at

the Technische Universität München in Munich, Germany.

Andreas Heinecke is Founder and CEO of Dialogue Social Enterprise and a professor

at the Danone Chair for Social Business at the European Business School in Oestrich-

Winkel, Germany.

Abigail Noble is head of Latin America and Africa at the Schwab Foundation for

Social Entrepreneurship in Geneva, Svizzera.

Mirjam Schöning is head and Senior Director of the Schwab Foundation for Social

Entrepreneurship, Geneva, Svizzera.

Wolfgang Spiess-Knafl is a research assistant at the KfW Endowed Chair in

Entrepreneurial Finance at the Technische Universität München, Munich, Germany.

© 2011 The Schwab Foundation for Social Entrepreneurship

innovazioni / volume 6, number 3

145

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Achleitner, Heinecke, Noble, Schöning, and Spiess-Knafl

The authors of this article believe that this is a multifaceted problem and that

improved information and understanding can play a key role in resolving it. Primo,

a better understanding of the social investment space is needed on both ends.

Secondo, rigorous and mutually agreed to metrics that facilitate social investment

transactions are imperative.

This article intends to unlock the mystery of social investment for social entre-

preneurs. It is written from the perspective of social entrepreneurs who have gone

through the process of bringing an investor on board and wished they had been

aware of several key issues up front. Our aim is to help shorten the time and effort

entrepreneurs expend in the initial stages of the investment dialogue, to evaluate

the expectations once they have found the right investors, and to have more

informed negotiations with them.

WHO SHOULD CONSIDER SOCIAL INVESTMENT?

Social investment is neither a silver bullet to close the funding gap in the social

entrepreneurship space nor a suitable solution for every social enterprise at every

stage of growth. The social enterprises that are best served by social investment are

those that have clear and realistic plans for how they will address their short- E

medium-term needs and are open to inviting outsiders into their decision-making

processes—and, in some cases, to ceding decision-making rights on their strategy

and operations to outsiders.

Given that investors demand a high level of accountability and quantifiable

risultati, social investment should not be used to plug holes in a budget, nor is it well

suited to enterprises operating in a saturated social market with limited future

growth.

WHAT DOES THE SOCIAL INVESTMENT PROCESS ENTAIL?

The social entrepreneurs we spoke with found it helpful to break down the process

into several concrete decisions they must make in order to determine what form of

social investment is best for their social enterprise, and with which social investors

they should continue the conversation. The following pages explore each of the

following steps:

1. Finding the financing instrument most appropriate for your enterprise

2. Finding the right social investor

3. Approaching the social investor

4. Passing the initial screening and participating in the due diligence process

5. Negotiating the financing terms

6. Working with the investor, including performance measurement

7. Exiting the investment

146

innovazioni / Impact Investing

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Unlocking the Mystery

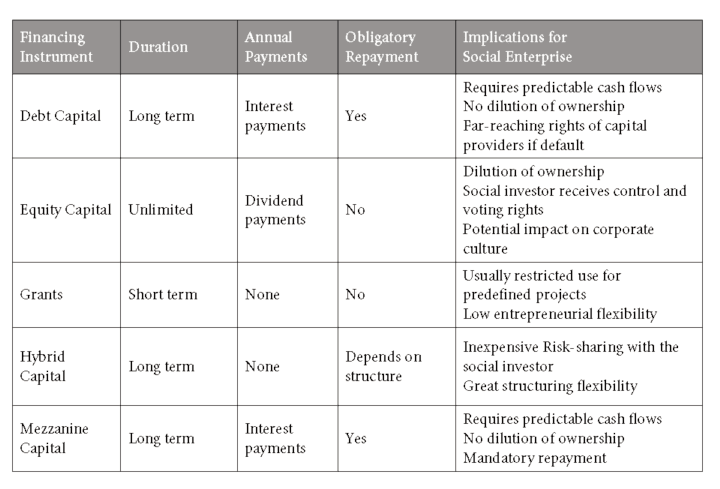

Tavolo 1. Comparison of Financing Instruments

FINDING THE FINANCING INSTRUMENT

MOST APPROPRIATE FOR YOUR ENTERPRISE

When determining the right financing instrument, social entrepreneurs should

first ask themselves questions that will help them determine whether debt or equi-

ty is more suitable for their purposes. Per esempio:

• Can we set aside capital to repay any debts incurred within 5-7 years?

• Can we take on capital that requires making regular interest or dividend pay-

menti (Per esempio, 5 percent interest) throughout the course of the financing?

Below are brief descriptions of common financial instruments.1

Debt capital can be used for long-term investments or project financing that

promises stable and predictable cash flows over the coming years. Stable and pre-

dictable cash flows are necessary, as the debt capital providers receive an annual

interest payment. Debt capital is provided on a temporary basis and generally must

be repaid within 5-7 years.

Equity capital gives the investor a share of the future profits generated by the

social enterprise in exchange for an infusion of capital. This tends to be the financ-

ing instrument with the highest risk for the investor, who only gets paid when the

enterprise is earning money. Besides a share of the profits, the social investor has

certain control and voting rights that depend on the legal form of the enterprise.

Grants, often thought of as “free” capital, are usually provided by foundations

or individuals for certain projects; they often exclude overhead or development

costs. Grants can have a high opportunity cost, especially when they are short

innovazioni / volume 6, number 3

147

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Achleitner, Heinecke, Noble, Schöning, and Spiess-Knafl

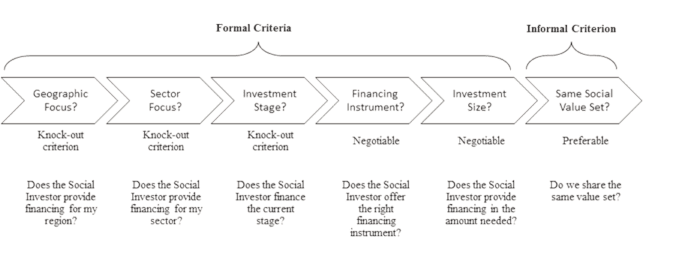

Figura 1. Investment Fit

term, paid out in small amounts, and require significant time to secure and main-

tain.

Hybrid capital contains elements of grants, equity capital, and debt capital.

Like a grant, there are no interest costs, and in certain agreements the financing

instrument is converted into a grant. Financing instruments in this category

include recoverable grants, forgivable loans, convertible grants, or revenue-sharing

agreements.

Mezzanine capital combines elements of debt and equity capital and repre-

sents a convenient financing alternative if pure equity or debt capital is not appli-

cable. The interest payment can be linked to the company’s profits, and the total

amount is repaid after a certain time. The flexible structure makes mezzanine cap-

ital an attractive option for both social entrepreneurs and social investors.

KNOWING WHETHER AN INVESTOR IS RIGHT FOR YOU

The social finance sector emerged with the goal of reducing transaction costs and

helping to allocate capital more efficiently in the social enterprise space. Below we

describe several of the types of investors available to a social enterprise.

Value banks, which take deposits from savers and give loans to individuals and

enterprises, offer loans and have more experience in the financing of social enter-

prises than traditional commercial banks. Some of the leading banks involved in

the social finance arena form the Global Alliance for Banking on Values.

Social stock exchanges, which create efficient public trading platforms for

both equity and debt capital in a social enterprise, can be an attractive financing

option for social enterprises with a proven business model, a good track record,

and significant financing needs. In Singapore (Impact Investment Exchange Asia),

London (Social Stock Exchange), and Mauritius (NeXii), social stock exchanges

are currently working on building a fully functional stock exchange under strict

regulatory requirements.2

148

innovazioni / Impact Investing

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Unlocking the Mystery

Social investment funds, which collect funds from individuals or foundations

and invest in a given sector, such as microfinance or the solar industry, act as inter-

mediaries by bundling funds from investors that they subsequently invest in cer-

tain asset classes. This approach reduces the transaction costs and the risk through

diversification effects.

Venture philanthropy funds, which bring together medium-term venture

financing with a screened portfolio of social investees, offer social enterprises non-

financial support such as management consulting or access to networks in order to

create a multiplied social return on investment. The funding can be structured

according to the needs and requirements of the social enterprise and in some cases

even includes grant funding. In some cases, venture philanthropy funds (some-

times called high-engagement philanthropy or social venture capital) do not focus

on the financial return on the investment.

Once the social entrepreneur has decided which types of investors might be

right for the enterprise, they can begin to explore which prospective investors

would be the best partner for their enterprise in the near future. In so doing, IL

social entrepreneur should consider not only formal criteria related to the

investor’s profile (for example, sector, geography, or instrument type), but also

informal criteria related to their values and personality. The questions in Figure 1

are designed to help the social entrepreneur determine whether a particular social

investor is the right fit.

Many social investors concentrate their funding in a particular geographic

region or sector, thereby deepening their expertise and allowing them to transfer

knowledge among various social enterprises. The geographic and sector focus tend

to be important criteria for how the investor chooses to invest.

Investors focus on specific investment stages—seed, early stage/start-up, E

later stage/mature. This can make it difficult to negotiate when the social enter-

prise is at a different stage than the social investor is usually interested in.

Financing terms often offer room for negotiation. As social investors consider

financial return as well as social returns, they can be flexible in structuring the

financing instrument to meet the requirements of the social enterprise. Investors

often have a set amount they can invest; if the enterprise requires more capital than

the investor alone can offer, investors may syndicate the investment, resulting in

the simultaneous investment of two or more investors. This lowers the risk for the

investor, as another investor has been vetted and is committed to the success of the

investee.

Conflicts can arise between the investor and the enterprise around the social

mission, profit distribution, and future development of the enterprise. These con-

flicts can dramatically change the vision, mission, and strategy of a social enter-

prise. Perciò, before giving an investor a key decision-making role, the social

entrepreneur should be certain the investor is the right partner over the next few

years. When first meeting with the social investor, the social entrepreneur can

gauge whether the investor shares the organization’s vision and mission and the

entrepreneur’s values.

innovazioni / volume 6, number 3

149

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Achleitner, Heinecke, Noble, Schöning, and Spiess-Knafl

APPROACHING THE SOCIAL INVESTOR

Investors cast a wide net in the early stages of the selection process in order to iden-

tify investment prospects from as large and competitive a pool as possible. Sociale

enterprises can get on the radar screen of prospective investors by various means,

including attending relevant conferences and networking events, and occasionally

by making a “cold call.”3

Social investment advisors, who assist social enterprises in setting up an appro-

priate financing structure and finding the right investors, can also act as financial

advisors and play an intermediary role between enterprises and investors.

At this stage, the social entrepreneur should have a polished “elevator pitch”

that explains their vision or concept, business model, and the reason they need

finanziamenti (Per esempio, to scale the business model, launch new activities, or pro-

vide working capital).

SCREENING AND DUE DILIGENCE PROCESS:

HOW YOU WILL BE JUDGED

Social investors analyze several hundred social enterprises per year, but only a few

make it to the final round. Investors assess nearly 50 different selection criteria

when evaluating these enterprises, which include the overarching themes listed

below:

• Concept

• Market

• Financials

• Social impact

• Social entrepreneur4

Concept, the single most important selection criterion, allows investors to

understand whether the offering will change the relevant sector through its strate-

gy or innovation. Investors assess how the social enterprise works with the target

group and whether it has the support of the relevant stakeholders. For the due dili-

gence, social entrepreneurs can prepare to answer specific questions on whether

the enterprise has a clear strategy to solve the social problem (the theory of

change) and how it differs from existing concepts.

Market, which allows investors to evaluate the potential of an enterprise,

explores the competitive environment and the characteristics of the target group.

Social entrepreneurs should be prepared to answer questions about the total num-

ber of people affected by the social problem and how the social enterprise is posi-

tioned to reach them.

Financials, which are relevant for debt capital investments, evaluate the busi-

ness model and capital requirements in the context of how and how much income

will be generated. The social enterprise should have 3- to 5-year projections in

terms of revenue, costs, and budget based on realistic assumptions and past data.

Social impact refers to both the scalability and reach of the business model.

Scalability depends on the business model characteristics, such as the necessary

150

innovazioni / Impact Investing

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Unlocking the Mystery

know-how for providing a service and how certain stakeholders can block the scal-

ing of the social enterprise. Reach is the percentage of the market covered by the

concept. The social entrepreneur should be prepared to speak in depth about the

external and internal factors that will facilitate (or might limit) the enterprise and

increase its scale and impact.

Social entrepreneur refers to the leader of an organization. Many investors say

that they invest first in the entrepreneur and second in the enterprise. Once an

investor has faith in an entrepreneur, they will invest in whatever that person

churns out. There are five different aspects of the social entrepreneur that investors

consider: strategic skills, professional skills, creativity, attitude, and development

potential. Most important to the assessment of the social entrepreneur are their

commitment to the concept, creativity in achieving the social impact or reaching

the market, and their previous track record.

NEGOTIATING THE FINANCING TERMS

The financing terms differ between debt capital (loan) and equity capital (owner-

ship stake). In some cases, the social investor provides the financing in separate

tranches after the completion of certain stages (Per esempio, $250,000 at the start and $250,000 after setting up a second location).

Equity capital: Primo, the social entrepreneur has to negotiate the valuation of

the social enterprise and whether the financial return should be realized through

an increase in its value or through regular dividend payments. Secondo, the entre-

preneur and investor should agree on a financial and dividend policy during the

holding period. Third, while the investor should be able to influence decisions in

the company, the social entrepreneur should maintain the rights to flexible and

entrepreneurial decision-making authority for the social enterprise. Fourth, social

entrepreneurs and social investors should discuss the options for the investor’s

future exit strategy.

Debt capital: Primo, the social enterprise and investor should discuss the inter-

est rate and the repayment schedule. Then the two parties should discuss the inter-

est payments and the principal repayment schedule in the event of distress to

secure the necessary financial flexibility. Grace periods can be an attractive option

for social enterprises. Third, the parties should discuss the worst-case scenario. In

the event of default or bankruptcy, the loan provider’s right to be repaid might take

precedence over the social entrepreneur’s rights. For this reason, the social entre-

preneur should avoid taking on personal liabilities for the social enterprise or

negotiating extensive debt-to-equity swaps in case of default. A debt-to-equity

swap gives the loan provider a certain share of the equity capital (ownership) if the

social enterprise defaults on its debt. If the social entrepreneur takes on personal

liabilities and the social enterprise defaults or goes bankrupt, the social entrepre-

neur can lose his personal assets.

innovazioni / volume 6, number 3

151

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Achleitner, Heinecke, Noble, Schöning, and Spiess-Knafl

WORKING WITH INVESTORS

After working out the structure of the investment, the social entrepreneur and the

investor should discuss how to formalize their ongoing relationship. The most

common way is to create an advisory board.

An advisory board involves the social investor in the operations and gives them

voting and control rights (for example, one social enterprise sends a monthly

overview of the financial situation to the members of the advisory board, Quale

convenes four times annually). The members of the advisory board usually include

representatives of the social enterprise and of the shareholders, as well as inde-

pendent experts who can contribute expertise from the social or the business sec-

tor.

The advisory board can strengthen the quality of entrepreneurial decisions

and management accountability by asking tough questions about current practices

and suggesting new policies, procedures, or approaches. Social investors tend to

have extensive knowledge about corporate governance, reporting, controlling, E

corporate finance, but only limited knowledge of the core activities of the compa-

ny, such as delivering the social services to the target group. The social entrepre-

neur should adjust their expectations and use the existing skill sets and network of

the social investor.

PERFORMANCE MEASUREMENT

Performance measurement enables the social investor to control and monitor the

work of the social entrepreneur. Performance measurements include both finan-

cial and social indicators. While there is not yet a globally accepted and applicable

performance or impact measurement method, a few have become more widely

used.

The Roberts Enterprise Development Fund has developed a quantitative

method called social return on investment (SROI), which aims to express the value

of an enterprise’s activities in monetary terms. Qualitative methods include a bal-

anced scorecard for social organizations.6 The choice of performance measure-

ment method should be discussed with the capital providers in advance.

Performance measurement methods require similar information to financial

analyses that assesses the valuation or the credit rating of a company. Those meth-

ods require solid and comparable information. The traditional capital markets

standards, such as the International Financial Reporting Standards (IFRS) or the

United States Generally Accepted Accounting Principles (US-GAAP), guarantee

that companies are reporting on a comparable basis. Regional standards have been

developed to address the special characteristics of social enterprises. Two popular

standards include the Social Reporting Standard (SRS) developed in Germany, E

the Impact Reporting and Investment Standards (IRIS) developed in the United

States.

152

innovazioni / Impact Investing

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Unlocking the Mystery

From the social entrepreneur’s perspective, reporting requires initial addition-

al effort and costs, yet it generates long-term benefits. It allows the social entrepre-

neur to track results, improve processes, and have better documentation of the

social enterprise’s successes.

EXIT CONSIDERATION

The exit routes for equity capital, debt capital, and grant funding are quite differ-

ent.

There are several exit strategies for equity capital. Shares can be sold to a third-

party investor, the social entrepreneur can buy back shares from the investor, IL

parties can issue an initial public offering on a social stock exchange, or they can

liquidate the ownership. The buy-back arrangement implies that the social entre-

preneur has sufficient funds to buy back the shares held by the social investor.

In the case of debt capital, social entrepreneurs can either repay or refinance

the loan. In the case of refinancing, the same or another social investor must be

willing to provide debt capital for another period. If the social enterprise defaults

on the loan (Per esempio, failure to repay or a long-term delay on scheduled pay-

menti), there are three scenarios:

• Social investor institutes bankruptcy proceedings to recover part of the loan

(liquidation)

• Social investor extends the period of the repayment schedule (financial flexibil-

ità)

• Social investor accepts equity in exchange for the loan (debt-for-equity swap)

Grant funding also presents several exit options. A social investor can fund a

significant part of the total budget or take over part of the overhead costs for a

given period of time. After this period, the social enterprise will have reached

financial self-sustainability or will need to secure follow-up financing.

FURTHER DEVELOPING THE FINANCING ENVIRONMENT

FOR SOCIAL ENTREPRENEURS

To bring the field of social investment to greater maturity and relevance, we must

address several issues. Primo, we must create a deeper understanding among the

broader community of social enterprises and investors of the respective require-

ments for both parties. Secondo, the sector must agree on rigorous, transferable,

and consistent metrics that can facilitate smoother social investment transactions

and deal flow. Third, we must create a common and open platform through which

social investors and investees can sort through the range of opportunities quickly

and accurately.

The challenge of the coming years is to bring to maturity the financing

mechanics fueling the momentum of social innovation. Several actors have begun

the hard work on each of the three actions proposed above. What we need is more

conversation and collaboration and a commitment to building this sector into a

innovazioni / volume 6, number 3

153

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023

Achleitner, Heinecke, Noble, Schöning, and Spiess-Knafl

viable and important avenue for advancing investment in enterprises that have a

social and financial impact.

This article is based on the Social Investment Manual that has been conceived

by the social entrepreneurs in the Social Investment Task Force initiated by the

Schwab Foundation for Social Entrepreneurship. A.-K. Achleitner, UN. Heinecke, UN.

Noble, M. Schöning, and W. Spiess-Knafl, Social Investment Manual, 2011.

Available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1884338. Noi

would like to thank the members of the Social Investment Task Force and our

interview partners.

1. For more information on these and other instruments, see Achleitner et al., Social Investment

Manual.

2. A key concern of social entrepreneurs is the ability to protect the social mission, as they cannot

control the ownership structure, which can lead to unsolicited takeover bids. The social enterprise

can protect its social missions through various measures, such as the control of a minority stake

by a foundation, setting up adequate articles of association, or the use of poison pills; see A.-K.

Achleitner and W. Spiess-Knafl, “Financing of Social Entrepreneurship,” in Understanding Social

Entrepreneurship and Social Business, C. Volkmann, K., Tokarski, and K. Ernst, eds. in press. Poison

pills discourage unsolicited takeovers and become effective when there is a change of control.

3. A long of list of investors active in this field can be found in Achleitner et al., Social Investment

Manual.

4. P. Heister, Finanzierung von Social Entrepreneurship durch Venture Philanthropy und Social Venture

Capital, Wiesbaden, 2010.

5. A list of 20 preparatory questions can be found in Achleitner et al., Social Investment Manual.

6. For an overview and case studies, see C. Clark, W. Rosenzweig, D. Lungo, and S. Olsen, Double

Bottom Line Project Report: Assessing Social Impact in Double Line Ventures, 2004. Available at

http://www.riseproject.org/DBL_Methods_Catalog.pdf; Rockefeller Foundation and Goldman

Sachs Foundation, Social Impact Assessment: A Discussion among Grantmakers, 2003. Available at

http://www.riseproject.org/Social%20Impact%20Assessment.pdf.

154

innovazioni / Impact Investing

Scaricato da http://direct.mit.edu/itgg/article-pdf/6/3/145/704716/inov_a_00090.pdf by guest on 07 settembre 2023