TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

Wiji Arulampalam and Andrea Papini*

Abstract—Analysis of the relationship between taxes and self-employment

should account for the interplay between responses in self-employment and

wage employment. To this end, we estimate a two-state multispell duration

model which accounts for both observed and unobserved heterogeneity

using a large longitudinal administrative data set for Norway for 1993 à

2011. Our findings confirm theoretical predictions and are robust to var-

ious changes to definitions and sample selections. A policy experiment

simulating a flatter tax schedule in the year 2000 is found to encourage

self-employment, delivering a net increase of predicted inflow into self-

employment from 2.8% à 5.3%.

je.

Introduction

MODELS of choices facing wage earners typically ne-

glect the fact that taxpayers may exit or enter self-

employment because of differences in tax schedules. Since

the interplay between the occupational choices is typically

not considered in models of labor supply, these models are

silent on how tax differences across occupational choice af-

fect decisions.1,2 However, in contrast, models of choice

of the self-employed are dominated by perspectives where

decisions are based on implicit or explicit comparisons to

the wage sectors. One obvious reason for this asymmetry

is the relative sizes of the sectors. Par exemple, the self-

employment rate (as a percentage of total employment) dans

Norway is 7%, whereas the European Union average is ap-

proximately 15% (OECD, 2018).

The relationship to the wage sector is not the only fac-

tor that complicates the assessment of the effects of taxation

on self-employment. From a theoretical perspective, the tax

effects are ambiguous. D'une part, an increase in the

tax rate may diminish the self-employment rate as it reduces

expected returns. On the other hand, high taxes may encour-

age self-employment if loss offsetting is allowed because the

government provides an implicit insurance by sharing the

Received for publication June 13, 2018. Revision accepted for publication

Février 17, 2021. Editor: Brigitte C. Madrian.

∗Arulampalam: Department of Economics, University of Warwick, IZA,

Oxford CBT, and OFS Oslo; Papini: European Commission and Joint

Research Centre.

This paper is part of the research of Oslo Fiscal Studies supported by the

Research Council of Norway. We are grateful to Statistics Norway (SSB)

for providing us with access to the confidential administrative data used in

the paper. The paper has benefited from comments from many individuals.

We are very grateful to Thor O. Thoresen for his detailed comments on mul-

tiple drafts of the paper. The paper has benefited from comments received

from Frank Fossen, ˚Asa Hansson, Ben Lockwood, Jean-François Wen, le

participants at the Workshop on Self-Employment/Entrepreneurship and

Public Policy held at the University of Oslo, Septembre 2016, and the par-

ticipants at the Skatteforum held in Hadeland, Juin 2017, the referees, et

the editor of this journal. The views expressed are purely those of the au-

thors and may not in any circumstances be regarded as stating an official

position of the European Commission.

A supplemental appendix is available online at https://est ce que je.org/10.1162/

rest_a_01046.

1See Blundell and MaCurdy (1999), and Keane (2011) for reviews of the

literature on labor supply.

2“Occupational choice” here means a choice between wage employment

and self-employment.

risk associated with self-employment (Domar & Musgrave,

1944).3

A large majority of empirical studies on the effect of taxes

on the level of self-employment activity focuses on the United

États. These studies examine the extensive margin in occu-

pational choice models (see Bruce, 2000, 2002; Gentry &

Hubbard, 2000, 2004; Schuetze, 2000; Schuetze & Bruce,

2004; Cullen & Gordon, 2007; and Moore, 2004).4 Études

for other countries include Hansson (2012) for Sweden; Fos-

sen (2007, 2009) and Fossen and Steiner (2009) for Germany,

and Wen and Gordon (2014) for Canada. Results from these

studies are mixed. Results for the United States, Par exemple,

do not provide an unambiguous answer about the relationship

between tax progressivity and self-employment. Cependant, dans

other countries, tax progressivity is generally found to dis-

courage self-employment.5

The representation of the tax schedule is important in any

analysis of tax effects on self-employment. Some studies in-

clude measures of marginal and/or average taxes in a quasi-

experimental or reduced-form analysis to investigate the ef-

fect of nonlinearities in taxes on entrepreneurship.6 In other

études, authors have used measures of expected net-income

differences and/or tax progressivity to capture the tax ef-

fects. Par exemple, Gentry and Hubbard (2000, 2004) utiliser

the spread in the marginal (or average) tax rates faced by a

self-employed individual at various levels of “success,” where

success is defined as the observed distribution of the three-

year real wage growth for entrants into self-employment.

In two recent studies (Fossen, 2009; Wen & Gordon, 2014),

authors derive the tax variables within a structural framework

3The role of loss offsetting is less clear in the presence of a progressive

tax schedule. If the tax rate is an increasing function of taxable income, le

savings made because of the loss offset are usually lower in magnitude than

the taxes paid on profits (Gentry & Hubbard, 2000).

4See Hansson (2012), Gale and Brown (2013), and Clingingsmith and

Shane (2016) for surveys on taxation and self-employment.

5A positive correlation between taxes and self-employment may also

partly be attributed to the higher tax evasion or avoidance possibilities in

self-employment relative to wage employment (voir, par exemple, Schuetze

& Bruce, 2004). Our data do not allow us to address this issue. Recent

tax evasion estimates for Norway show that around 14% of the business

income is not reported (Nygård et al., 2019). This estimate is lower than

typical estimates for the United States but close to what is found among the

self-employed in Finland (Johansson, 2005) and Denmark (Kleven et al.,

2011). Slemrod (2007) estimates that around 57% of U.S. nonfarm business

income was not reported. The time and individual unobservable effects in-

cluded in our model will partially mitigate this problem if the differential

evasion possibilities are relatively constant over the time period under con-

sideration. Another issue is the possibility of a tax-induced organizational

shift. See Papini (2018) for a recent analysis of this issue. We treat a self-

employed individual who decides to incorporate and, thus, decides to earn

wages from the company, as a wage earner. We also include region fixed

effects to partly control for this issue, as this organizational shift was more

common in some regions and time periods (Papini, 2018).

6Par exemple, Bruce (2002), and Gurley-Calvez and Bruce (2008) utiliser

expected marginal tax rates, ou, alternativement, average tax rates to capture

nonlinearities in the tax schedule. These authors do not include any measure

of riskiness of income received.

The Review of Economics and Statistics, Mars 2023, 105(2): 376–391

© 2021 The President and Fellows of Harvard College and the Massachusetts Institute of Technology. Published under a Creative Commons Attribution 4.0

International (CC PAR 4.0) Licence.

https://doi.org/10.1162/rest_a_01046

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

377

where the decision making is based on the difference in ex-

pected utilities. Yet the two papers differ in many aspects

and draw different conclusions. The use of different utility

functions and assumptions regarding the pretax income dis-

tribution of the individual result in different variables that

capture the effects of nonlinearities in the tax schedule. Ils

also use different statistical models (logit versus probit).

Fossen (2009) models the transitions between wage

and self-employment using data from the German Socio-

Economic Panel (GSOEP) over the period 2002 à 2006 et

a logit model in which agents are assumed to trade-off risks

and returns. He uses a constant relative risk-aversion utility

and assumes normally distributed pretax income. The two

relevant model-generated variables are (je) the difference in

net-of-tax incomes in the two occupations and (ii) la variété-

ances of the individual’s posttax income distributions in the

transition equation.

In contrast, Wen and Gordon (2014) use a pooled cross-

sectional sample from the Canadian Survey of Labour and

Income Dynamics over the years 1999 à 2005 to estimate

the probability of self-employment in a probit model.7 They

assume risk neutrality and a log-normal distribution for the

pretax income. The relevant “tax variables” are (je) the differ-

ence in log net-of-tax incomes in the occupations (netincdiff)

et (ii) a variable that they call convexity. The variable con-

vexity has an intuitive interpretation as the “increase in tax-

liability taken on by the self-employed due to the volatility

of their business income, expressed as a proportion of their

disposable income.”

Both studies use selectivity-corrected income equations

to predict individual pretax incomes and then use a tax-

transfer microsimulation model to generate the relevant ex-

pected value and variance of after-tax incomes in wage em-

ployment and self-employment. The estimated models are

subsequently used to simulate the effects of hypothetical tax

policy scenarios that reduced progressivity. Fossen finds the

“flatter-tax” reforms considered discourage individuals from

choosing self-employment;8 Wen and Gordon find a “small”

positive effect on the probability of finding someone in self-

employment.9

Here we use the two variables netincdiff and convexity used

by Wen and Gordon (2014). Although some of the tax effects

in both studies are captured via net-income differences, le

additional variable convexity in Wen and Gordon (2014) est

an individual-specific measure that intuitively captures the

interaction between the progressivity of the tax schedule and

7Ainsi, the focus is on being in self-employment at the time of interview

and not on entering self-employment.

8The interpretation given in Fossen (2009) is that a flatter tax schedule

increases expected returns in self-employment, but at the same time it also

increases the risk because the variance of the net income distribution also

increases. The second effect is found to dominate the first one, and hence,

a flatter tax schedule discourages self-employment.

9The “flatter-tax” reform considered is found to increase the probability

of finding someone in self-employment by 0.04 percentage points from the

base model prediction of 5.76%.

the volatility of self-employment income relative to wage

revenu.

Our work complements the existing empirical literature

in various ways. D'abord, our definitions of wage employment

and self-employment are based on reported incomes from tax

records and not on survey responses. We use data drawn from

various Norwegian population registers over the period 1993

à 2011. The data include rich sociodemographic informa-

tion together with highly accurate income measures from the

annual tax returns. Deuxième, we model the evolution of em-

ployment spells using a two-state multispell duration model

that controls for observed and unobserved heterogeneity cor-

related across spells and accounts for left and right censoring

in the observed spells. This contrasts with several previous

contributions, which mainly focus on self-employment en-

tries or exits using survey data with self-reported employment

status and short panels of individuals.

We generally find significant effects of both netincdiff and

convexity on the probability of exit from both types of em-

ployment spells, conforming to theoretical predictions as dis-

cussed in section VA. The increase in convexity is found to

increase the probability of exiting self-employment and to

decrease the probability of entry into self-employment; que

est, convexity has a discouraging effect on self-employment,

ceteris paribus. On the other hand, an opposite effect is found

for netincdiff: negative (positive) in the self-employment

in our base

(wage-employment) equation. En plus,

model, we find a larger effect of convexity relative to that of

netincdiff, implying that small increases in convexity will

require large increases in netincdiff to discourage the self-

employed from quitting and to encourage wage earners to

enter self-employment.

Given the way the tax variables are constructed, a change

in the progressivity of the tax schedule will have an impact

on the convexity and on the netincdiff by changing the ex-

pected net income difference in self-employment and wage

employment. From this, the total effect on the rate of self-

employment of a decrease in the progressivity of the tax

schedule is hard to predict. Ainsi, to better understand the net

effect, we simulate a tax experiment that replaces the personal

income tax structure in the year 2000 with a less progressive,

revenue-neutral tax schedule, as explained in section VB. Le

overall estimated effect of this policy change is positive on

the share of self-employment. The average exit rate from self-

employment is estimated to go down by 0.018 (s.e. 0.184)

percentage points, and the estimated exit rate from wage-

employment is estimated to increase by 0.119 (s.e. 0.010)

percentage points. This change results in a net increase of

predicted inflow into self-employment changing from about

2.8% à 5.3%.

The rest of the paper is organized as follows. Section II de-

scribes the taxation of self-employment income and wages

during our sample period. Section III sets out our economet-

ric model. In section IV we provide details of the data and

the sample selected for our analyses. We also present the pro-

cedure used for estimating the tax variables. The estimation

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

378

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 1.—MARGINAL TAX RATE FOR WAGE AND SELF-EMPLOYMENT INCOMES, YEAR 2005

(je) Solid line: Marginal tax rate for a wage earner in tax class 1 (see online appendix A.2 for the definition of tax class 1) with only wage income. Employer’s social security contributions are excluded. (ii) Dashed line:

Marginal tax rate for a self-employed individual in tax class 1 with only self-employed income and no capital invested in the firm.

results are discussed in section V along with the results from

our policy simulation and some sensitivity checks. Enfin,

section VI concludes the paper.

II. Taxation in Norway

Tax reforms undertaken in 1992 introduced a dual-income

tax system in Norway. Under this regime, all types of capital

income are taxed at a flat rate, but a progressive schedule

applies to labor and pension income. Individuals pay income

tax on two different tax bases: (je) ordinary income and (ii)

personal income.

Income from wages, self-employment, capital, transfers,

and pensions are first grouped as ordinary income. After de-

ductions, individuals pay tax at a flat rate (28% during most

of the sample period) on ordinary income.10 The other tax

base—personal income—includes wage income, transfers,

and pension income and self-employment income due to ac-

tive efforts, but not capital income. Individuals pay a sur-

tax and social security contributions levied on the personal

revenu.

As an example, consider a wage earner whose only source

of income is from wages in the year 2005. The solid line

in figure 1 represents the marginal tax rates that apply to the

wage income. No taxes and contributions are paid for income

below the tax-free threshold. This threshold was NOK 29,600

10The deductions include a standard personal allowance, a deduction for

expenses including interest payments, and a basic allowance, which is a

percentage (up to a maximum) of labor or pension income.

dans 2005.11 Above the threshold, a social security contribution

de 25% (of the personal income above NOK 29,600) is due, en haut

to the amount where the total amount is the same as one would

get using the standard rate of 7.8% on all personal income.

Thereafter the rate is 7.8%. The flat tax on ordinary income

(28% dans 2005) is paid on the part of income that exceeds

the sum of the personal allowance and the basic allowance.

The basic allowance is 31% of wage income with a lower

limit of NOK 31,800 and an upper limit of NOK 57,400. Le

personal allowance is a standard deduction from ordinary

revenu, set at NOK 34,200 dans 2005. The last two steps in

figure 1 represent the two surtaxes that raise the marginal tax

rates by 12 percentage points and 15.5 percentage points. Le

maximum marginal tax rate of 51.3% is reached after the two

surtaxes become effective.

Taxation is more complicated for the self-employed be-

cause income represents the reward to the labor of the indi-

vidual as well as the returns to the capital invested in the firm.

Given the lower tax rate on capital income, the decision about

how to declare the income was not left to the discretion of the

self-employed; rules were established to split the profits into

labor and capital income.12 The dashed line in figure 1 rep-

resents the marginal tax rates that apply to self-employment

income in the case where no capital is invested in the firm.

11The exchange rate in 2005 était 1 USD ≡ 6.45 NOK; 1 EUR ≡ 8.01

NOK.

12Capital income is calculated by multiplying the capital invested in the

firm with a rate of return annually established by the government. The labor

income is then estimated by subtracting the imputed capital income from

the reported self-employment income net of expenses.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

379

FIGURE 2.—MARGINAL TAX RATE FOR WAGE INCOME, YEARS 1995, 2005, AND 2010

(je) Marginal tax rate for a wage earner in tax class 1 with only wage income in years 1995, 2005, et 2010. Employer’s social security contributions are excluded. Thresholds are adjusted to account for income growth

during the period (base year is 2005). Marginal tax rate is reported only for income larger than 200,000 NOK. (ii) To improve readability, the case for self-employment income is not reported, because it would imply

only a proportional vertical shift of each of the three curves presented; see figure 1.

The main differences to the wage income case are the lack of

basic allowance and the higher social security contribution

(10.7% dans 2005).

Tax progressivity is achieved through the tax-free al-

lowances applied to ordinary income and the surtaxes on

personal income. Cependant, during the years under consid-

eration, the progressivity changed several times because of

changes to the tax rates, the number of surtaxes, and their

thresholds. Dans l'ensemble, tax progressivity decreased during the

period. Figures 2 et 3 show the marginal tax rates and aver-

age tax rates in different years for an individual whose only

source of income was wage income.13 Marginal tax rates in

the year 2010 were overall lower than in the year 1995, et,

for most part, they were also lower than in the year 2005. Sim-

ilarly, the average tax rates in 1995 were in general higher

than the rates in 2005 et 2010 (figure 3).

III. Econometric Model

Drawing heavily on the framework of Ham et al. (2016),

we model employment transitions using a two-state multi-

spell discrete duration model accounting for unobserved in-

dividual heterogeneity.14 The two employment states are self-

13Note that the thresholds account for wage growth.

14Following the early pioneering work by Lancaster (1979), and Nick-

ell (1979), the literature on modeling durations using survival analysis has

developed very fast. Lancaster (1990) and Van den Berg (2001) provide a

comprehensive discussion of theoretical issues as well as empirical exam-

ples that helped to develop this literature. See Carrasco and García-Pérez

employment and wage employment. The duration variable is

measured in terms of the Norwegian financial year, which is

the calendar year (January–December). Approximately 70%

of individuals in our sample have a first spell that is left cen-

sored. Without dropping these individuals from the analysis

sample, we include them and specify a different model of exit

rates for them (Ham et al., 2016). We check for sensitivity of

our estimates to excluding the left-censored spells, which is

equivalent to using an inflow sample.

With regard to the unobserved heterogeneity, we follow

the literature and assume this to be distributed independently

across individuals and of the covariates included but fixed

over the same type of spell, but correlated across the two

employment states and the type of spell (fresh versus left-

censored). A discrete distribution is assumed for the unob-

served heterogeneity.

As we closely follow the setup in Ham et al. (2016), we pro-

vide only the form of the hazard function used and refer read-

ers to their paper for further details. For notational simplicity,

we do not distinguish between duration time and calendar

temps, although the estimated model does. The duration time

random variable is denoted as ϒ. Let j = {s f , w f , sc, wc}

where the first letter denotes a self-employment (s) or a wage-

employment (w) spell, and the second letter denotes a fresh

( F ) or a left-censored spell (c). The probability that individ-

ual i would leave the spell in spell type j at the end of duration

(2015) for another recent application of a two-state multispell duration

model with discretely distributed unobserved heterogeneity.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

380

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 3.—AVERAGE TAX RATE FOR WAGE INCOME, YEARS 1995, 2005, AND 2010

(je) Average tax rate for a wage earner in tax class 1 with only wage income in years 1995, 2005, et 2010. Employer’s social security contribution are excluded. Thresholds are adjusted to account for income growth

during the period (base year is 2005). (ii) To improve readability, the case for self-employment income is not reported, because it would imply only a proportional vertical shift of each of the three curves presented;

see figure 1.

time t, conditional on not having left in t − 1, is a discrete

time hazard λ(t ) given by

ωs f = ωe f = ωsc = ωec = 0 as a normalization, and esti-

mate the associated probability, p.

λi, j (t|xi, j, ωi, j )

= Pr(ϒi, j = t|ϒi, j > t − 1, taxationi, j (t ), xi, j (t ), ωi, j )

= F

(cid:2)

h j (t ) + xi, j (t )(cid:4)β j + un(cid:4)

j taxationi, j (t ) + ωi, j

(cid:3)

,

(1)

where h j is the duration dependence function, xi, j (t ) con-

tains time-fixed and time-varying observed individual char-

acteristics, taxation contains the tax variable(s), and ωi, j is

the unobserved heterogeneity. F is specified as the comple-

mentary log-log distribution function.15 To achieve conver-

gence with stable parameter estimates, we restrict the du-

ration dependence function to a log linear form and model

the unobserved heterogeneity to be discrete with two points

of support.16 We keep the hazard-specific intercepts, ensemble

15The distribution function is given by F (z) = 1 − exp[− exp(z)]. Some

other popular distributions used are the standard normal and the logistic

cdfs, which are symmetric distributions. The distribution we employ is not

a symmetric distribution. A discrete time hazard model derived from an

underlying continuous time proportional hazard model can be written in

this form. See Narendranathan and Stewart (1993) for an application.

16Theoretical results exist for lack of nonparametric identification in haz-

ard models when one or more of the following are present: duration depen-

dence, time-varying variables, time-varying effects, and unobserved hetero-

geneity. Par exemple, Baker and Melino (2000), using simulations, look at

the behavior of the nonparametric maximum likelihood estimator for a dis-

crete duration model with unobserved heterogeneity and unknown duration

effect, and find the estimator to be biased when both are nonparametrically

specified. Sans surprise, empirical researchers have also found the model

IV. Données, Sample, and Variable Definitions

UN. Data and Sample Selection

The present study benefits from rich longitudinal Norwe-

gian administrative data for the period 1993 à 2011. Le

main data source is the Income and Wealth Statistics for Per-

sons and Families (Statistics Norway, 2005). The data are

drawn from the annual tax returns and the education registers

(years of education and fields of studies). The data also con-

tain individual and family sociodemographic characteristics.

Our focus is on wage earners and the self-employed who have

strong labor market attachment, and so we restrict our anal-

ysis to Norwegian citizens aged 25 à 61 and exclude those

who have reported any income from agricultural, forestry, ou

fishing activities.17

We use an income-based definition to identify periods or

spells of self-employment and wage employment. In our

main analysis, we classify an individual observation as “self-

employed” if the major source of income is self-employment

estimations to be unstable when most of the time effects are modeled in an

unrestricted manner and have thus imposed some functional form restric-

tions to identify the parameters. See Ham and Rea (1987) for a discussion

of these issues in the context of an empirical application.

17Since immigrants are a group of “selected” individuals, we exclude

eux.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

381

FIGURE 4.—ANNUAL SHARE OF SELF-EMPLOYMENT OBSERVATION

Annual self-employment observation as a share of total self-employment plus wage employment observations. Categorisation into self-employment and wage employment is described in section III.

revenu, c'est à dire., if the reported self-employment income (net of

expenses) is larger in absolute value than the wage income

and is also larger than government transfers (qui comprennent

disability insurance, unemployment benefits, and other types

of pensions).18 En plus, we restrict our sample to those

who have been classified as either being in wage employ-

ment or self-employment during the observation period 1993

à 2011.19

The majority of individuals never experience any self-

employment spells. Par exemple, the average rate of self-

employment over the sample period is around 5% (see figure

4). To reduce the computational burden of working with more

que 2 million individuals, we use a 50% random sample to

generate our tax variables. From this sample, we next ran-

domly select 2% of individuals who have never been catego-

rized as self-employed and 20% from the other group, lequel

includes individuals with periods of self-employment spells

only and individuals with a mix of types of employment. Ce

gives us a sample of 476,275 individual-year unweighted ob-

servations. All analyses presented use sample weights to ac-

count for this endogenous sample selection, following Solon,

Haider, and Wooldridge (2015).

18We also exclude individuals who do not report any wage income or

business income that is larger than the “Basic amount” during the obser-

vation period for at least three years. The “Basic amount” is the base for

calculating many of the Norwegian social insurance scheme’s payments and

était 78,024 NOK in 2011 (the approximate exchange rate in that year was:

1 USD ≡ 5.67 NOK; 1 EUR ≡ 7.79 NOK).

19Around 18% of the individuals in the sample experienced at least one

“third-state” spell (periods of time that cannot be defined either as wage

employment or as self-employment) and are omitted from the analysis.

B. Defining and Estimating the Tax Variables

Our analysis is based on the theoretical exposition of an ex-

pected utility maximization approach discussed by Wen and

Gordon (2014), who in turn base their model on the one de-

veloped by Rees and Shah (1986). Assuming risk neutrality,

a convex tax schedule, and log-normally distributed pretax

revenu, they show how the probability of self-employment

can be written as a function of the tax schedule using two

representations of the effects of taxation.20 These are (1) net-

incdiff, which is the difference in log of expected net incomes

in self-employment and wage employment, et (2) convexity,

which is a measure of how the expected tax liability changes

due to the volatility of their self-employment income relative

to the net income in wage employment (see online appendix

A.1 for further details).

The construction of the two tax variables requires net-

income distributions for each individual. We use a tax simula-

tor to generate these (see online appendix A.2). The simulator

considers the yearly rules for taxing self-employment income

net of expenses, wages, and other sources of income. Other

sources of income are taken to be exogenous; these are added

to the predicted self-employment or wage income. The sim-

ulator also accounts for the main deductions and allowances,

as well as for the system for taxation of the labor and capital

parts of net self-employment income; see section II.

20Wen and Gordon (2014) represent the convex tax function specifying

the after-tax income x j as (y j )1−τy0

τ, where the tax parameters τ and y0

are such that 0 < τ < 1, and y0 > 0 represents the income at which the tax

liability is zero. (1 − τ) is the elasticity of posttax income with respect to

pretax income (also see Musgrave & Thin [1948] and Benabou [2000]).

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

382

THE REVIEW OF ECONOMICS AND STATISTICS

TABLE 1.—SUMMARY STATISTICS: MEAN (STD DEVIATION)

Individual-specific variables

Females

Lower secondary school and less

Upper secondary school

University

Time-varying variables

Age at the start of the spell

Years 1993–1998

Years 1999–2002

Years 2003–2007

Years 2008–2011

Eastern Norway

Southern Norway

Western Norway

Central Norway

Northern Norway

Local unemployment rate

convexity

netincdiff

Proportion of exits

All

0.47 (0.50)

0.39 (0.49)

0.30 (0.46)

0.32 (0.47)

35.06 (9.24)

0.30 (0.49)

0.22 (0.41)

0.27 (0.44)

0.21 (0.41)

0.50 (0.50)

0.05 (0.22)

0.26 (0.44)

0.09 (0.28)

0.10 (0.30)

2.73 (0.83)

0.007 (0.008)

−0.448 (0.19)

WE Sample

0.48 (0.50)

0.35 (0.49)

0.31 (0.46)

0.34 (0.47)

34.84 (9.20)

0.30 (0.46)

0.22 (0.41)

0.27 (0.44)

0.21 (0.41)

0.49 (0.50)

0.05 (0.22)

0.26 (0.44)

0.09 (0.29)

0.10 (0.30)

2.73 (0.83)

0.007 (0.008)

−0.429 (0.17)

0.006

SE Sample

0.27 (0.44)

0.53 (0.50)

0.27 (0.45)

0.20 (0.40)

39.80 (8.80)

0.34 (0.47)

0.21 (0.41)

0.27 (0.44)

0.18 (0.39)

0.55 (0.50)

0.06 (0.24)

0.24 (0.42)

0.07 (0.26)

0.08 (0.27)

2.78 (0.83)

0.012 (0.008)

−0.825 (0.25)

0.106

(je) Years covered in the analysis are 1993–2011. (ii) Definitions of wage employment and self-employment and the sample selection criteria used are provided in section IV. (iii) All averages and proportions are

based on the weighted sample (see section IV for further details). (iv) The number of unweighted observations is 476,275, of which 362,217 are classified as wage employment and 114,058 as self-employment. (v)

The number of unweighted individuals is 34,746.

Our construction of the two tax variables closely follows

Wen and Gordon (2014). Assuming pretax income to be log-

normally distributed, y j ∼ LN (μ j, σ j ), where j = s for self-

employment, and j = e for wage employment, we have

à 0, so that convexity is associated with uncertainties in self-

employment income only.

The convexity variable for each individual in each time

period is calculated as

y j

≡ E (y j ) = exp

(cid:4)

(cid:5)

.

μ j + 1

2

σ2

j

(2)

convexity = E [T (ys)] − T ( ¯ys)

¯ys − T ( ¯ys)

.

(4)

The first tax variable, netincdiff, that enters the occupational

choice probability is given by

C.

Summary Statistics

netincdiff = [(1 − τs) ln(ys)]/[(1 − τe) ln(ye)]

(cid:6) ln [netincomes/netincomee] ,

(3)

where τ is a tax parameter from the tax function (see footnote

21). For each individual, we first estimate the selectivity-

corrected expected pretax income (y j ) for each occupation

in each period.21 We then use the tax simulator to gener-

ate the individual specific net incomes in both occupations:

netincomes and netincomee.

Suivant, we define the second individual specific tax variable

representation: convexity. This variable is defined as the dif-

ference between the expected tax liability E [T (ys)] et le

tax liability at the expected income T ( ¯ys), relative to the ex-

pected net income ¯xs = ( ¯ys − T ( ¯ys)).22 Wage employment is

generally less riskier than self-employment. Ainsi, suivre-

ing Wen and Gordon (2014), we derive our convexity variable

by setting the coefficient of variation for wage income equal

21Online appendix A.3 contains the full set of estimates from the equations

that we used to generate the income variables.

22As shown in Wen and Gordon (2014), the tax liability function T (y j )

in the theoretical model is given by y j (1 −

). This term is strictly

convex and hence the use of the term convexity; see Wen and Gordon (2014,

p. 472).

(cid:2)

y0/y j

(cid:3)τ

Summary statistics for the main estimation sample are pro-

vided in table 1. En moyenne, in the weighted sample, le

proportion of individuals exiting out of a period of work and

into a period of self-employment is less than 1%, whereas the

average share of exits out of a period of self-employment is

11%. We next turn to our tax variables.

The overall distributions of the two tax variables are pro-

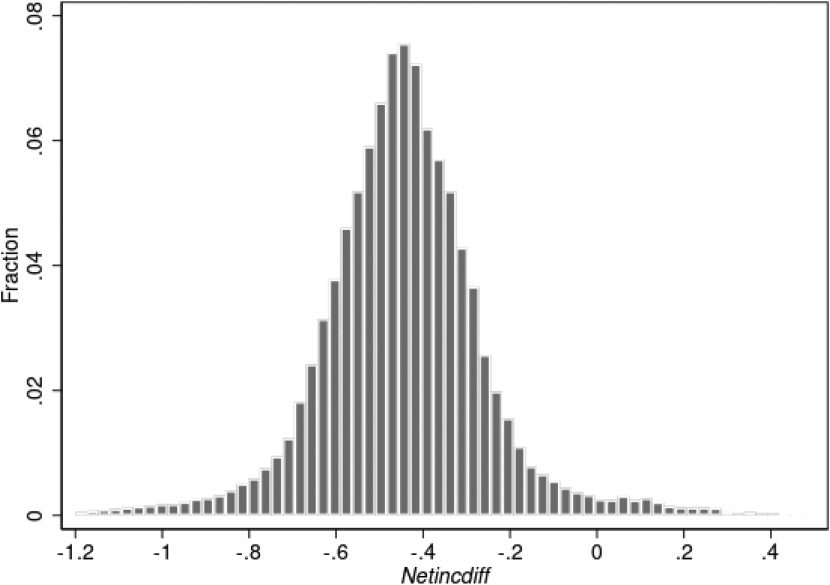

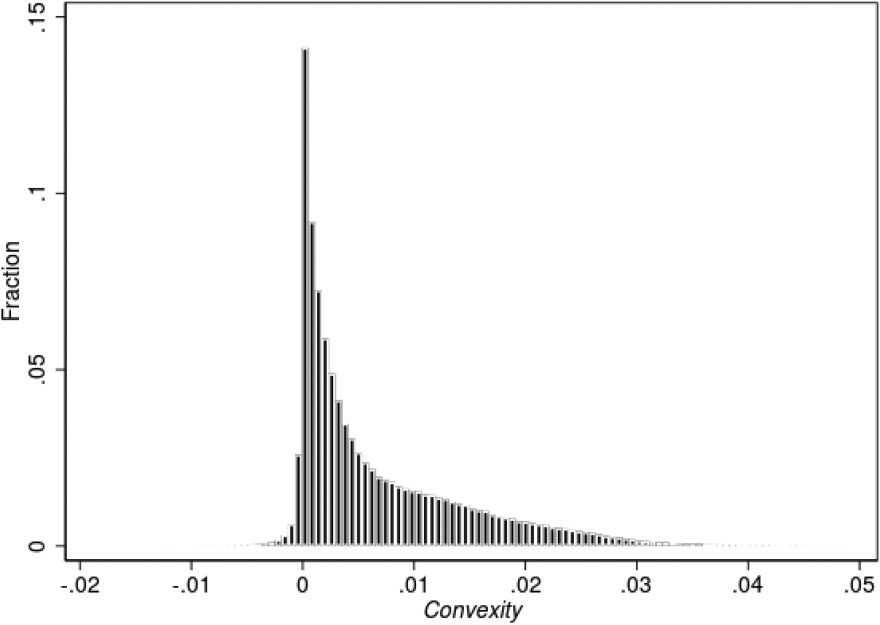

vided in figures 5 et 6. netincdiff is predominantly negative,

indicating that, for the majority of observations in the sample,

the predicted net wage income is higher than the predicted

net self-employment income.23 convexity is as expected, es-

timated to be mostly positive.24 The average value of pre-

dicted netincdiff of −0.448 implies that the net income in

self-employment is about 64% of net income in wage em-

ployment. The average estimated value of convexity is 0.007

23The paradox of self-employment being characterized by higher uncer-

tainty and lower earnings than wage employment is a common finding in

previous studies (voir, Par exemple, Hamilton [2000] and Hurst & Pugsley

[2011], or Berglann et al. [2011] for the case of Norway). There are several

possible explanations for this puzzle. Among them, (je) the relevance of un-

observed nonpecuniary benefits; (ii) unobserved underreporting of income

by the self-employed; et (iii) overestimation by the self-employed of their

probability of success.

24Negative convexity values are possible if the tax function is not convex.

Estimated convexity is 0 for about 1.5% of the observations and negative

for about 5.5% of the observations.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

383

FIGURE 5.—DENSITY OF netincdiff

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

netincdiff distribution across all years and observations. netincdiff is defined in equation (3).

FIGURE 6.—DENSITY OF convexity

convexity distribution across all years and observations. convexity defined in equation (4).

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

384

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 7.—BOX-AND-WHISKER PLOT FOR netincdiff

(je) netincdiff = ln[net income in SE/net income in WE]. See section IVB for further details. (ii) The box shows the median and the interquartile range (IQR). The end of the whiskers gives 1.5 times IQR.

(s.d.= 0.008), which is lower than the convexity value of

0.011 (s.d. 0.16) reported by Wen and Gordon (2014) pour

Canada.

Box-and-whisker plots in figures 7 et 8 show how these

estimated tax variables change over time. The median net-

incdiff remains stable over time without experiencing a clear

trend, and the spread decreases over time. A slightly declin-

ing trend is observed for convexity, which complies with the

reduced progressivity of the taxation during the sample pe-

riod (section II). The temporary up-tick in the median and

spread of convexity in 2000 is consistent with the fact that

two surtaxes were introduced in that year, making the overall

tax schedule more progressive.25,26

In addition to the two tax variables, the models also in-

clude time-varying and time-invariant control variables. Le

time-invariant variables are sex, age at the start of the spell, dans-

dicator variables for highest education level achieved, and re-

gional dummies to account for local labor market conditions.

Calendar time dummies control for macroeffects. The data

are an unbalanced panel; see descriptive information in table

1. Self-employed individuals are on average older and less

educated than individuals who are paid wages, and a lower

proportion of females is found among the self-employed.

Self-employment is also highly concentrated in the more

densely populated areas of eastern Norway (the Oslo region)

and western Norway (the Bergen region).

25Another possible explanation for this is the increased uncertainty due

to the recession in the early 2000s.

26We carried out an analysis of covariance to assess the contribution of

various factors to the variation of the two tax variables. We included all

the variables (sex, marital status, éducation, region, enfants, family head,

year dummies, two selection correction terms, and estimated variances)

that were used in the predictions of these two tax variables along with the

“other” tax variable (convexity or netincdiff). The model R-squared values

étaient 29% et 49% respectively in the netincdiff and convexity equations.

The top four largest contributors explained 46% of the model sum of squares

(SS) in the netincdiff equation. These were education, selection into SE, et

the regional and year dummies. With regard to the convexity variable, le

top four largest contributors were the year effects, éducation, and estimated

heteroskedastic functions, which together explained 38% of the model SS.

The convexity (netincdiff) variable in the netincdiff (convexity) equation ex-

plained less than 4% (2%) of the model variations. The largest contributions

to the model SS came from the year effects.

V. Results

UN. Main Results

Before discussing the parametric model estimation results,

we provide a plot of the empirical hazard in figure 9.27 Le

raw data self-employment (SE) hazard consistently lies above

the wage-employment (WE) hazard, implying that the condi-

tional exit rate from SE is higher relative to an exit from WE.

The WE hazard is quite low and stable over the spell dura-

tion. The probability of exiting from SE into WE is around

27This is the number of individuals exiting during the year divided by the

number of individuals in that state at the beginning of the year.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

385

FIGURE 8.—BOX-AND-WHISKER PLOT FOR convexity

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

(je) See equation (4) for the definition of convexity. (ii) The box shows the median and the interquartile range (IQR). The end of the whiskers gives 1.5 times IQR.

FIGURE 9.—NONPARAMETRIC HAZARD ESTIMATES

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

The figure presents the nonparametric hazard estimates for wage employment and self-employment spells. These are the OLS estimated coefficients on the duration time dummies in a linear regression of the duration

variable. The duration variable takes the value of 0 if that particular year refers to an ongoing spell and 1 when it is associated with an exit.

386

THE REVIEW OF ECONOMICS AND STATISTICS

TABLE 2.—HAZARD MODEL ESTIMATES, MAIN SAMPLE

Fresh Spells

Left-Censored Spells

netincdiff

convexity × 100

Male

Age at the start of the spell

High school

University

ln(duration)

Constant

Support points

Probability masses

p1 (constants + support points)

p2 (constants only)

N observations (unweighted)

N individuals (unweighted)

Maximized log likelihood value

SE

[1]

−0.429

(0.053)

0.049

(0.015)

−0.024

(0.027)

−0.012

(0.001)

−0.006

(0.029)

0.220

(0.028)

−0.520

(0.016)

−1.135

(0.092)

−0.531

(0.049)

0.805

(0.019)

0.195

(0.019)

476,275

34,746

−105,687.67

WE

[2]

1.685

(0.082)

−0.246

(0.021)

0.602

(0.030)

0.030

(0.002)

0.115

(0.035)

0.131

(0.037)

−0.490

(0.018)

−3.11

(0.103)

−3.042

(0.200)

SE

[3]

−0.725

(0.109)

−0.017

(0.030)

0.191

(0.058)

−0.034

(0.002)

−0.131

(0.048)

0.051

(0.051)

−0.016

(0.037)

−0.892

(0.192)

−1.337

(0.072)

WE

[4]

1.753

(0.087)

−0.163

(0.023)

0.776

(0.037)

−0.046

(0.002)

−0.008

(0.038)

0.100

(0.038)

−0.234

(0.032)

−1.930

(0.118)

−1.839

(0.094)

(je) MLE standard errors in parentheses. (ii) The models are estimated using a random sample of individuals as detailed in section IV. (iii) Omitted education category is no-education/high-school drop-out. (iv) Le

model additionally includes region and time indicators; see table 1. Complete sets of results are available in the online appendix A.4.

0.23 in the first year of the spell compared to 0.02 from WE

into SE.

Our base model estimates are presented in table 2.28 All

four hazard functions are estimated simultaneously. Except

for the left-censored SE hazard, the other three hazards show

negative duration dependence, ceteris paribus. Insignificant

duration dependence estimated for the left-censored SE spells

is consistent with the observation that the probability of ex-

iting is almost zero for high duration spells, and the sample

of left-censored spells has a higher probability of containing

large-duration spells.

We focus our discussions on the interpretation of the es-

timated effects of the tax variables. The theory predicts a

positive (negative) effect of the netincdiff variable on the

probability of exit from WE (SE). Par exemple, the higher

the proportionate increase in the net-income differential with

respect to the net income from WE, the higher the exit rate

from WE (Wen & Gordon, 2014; Taylor, 1996; Fossen, 2009).

On the other hand, the theoretical prediction of the effect of

convexity is negative on exit rate from WE since higher “con-

vexity” would be expected to discourage SE. The estimated

effects of the two tax variables conform to these theoretical

prédictions.

These estimated coefficients are also found to be higher

in absolute value for WE exit probabilities (columns 2 et

4). These results suggest that, compared to exits from SE, le

probability of an exit from WE is more sensitive to changes in

both expected net-income differences and tax progressivity.

This is consistent with the fact that the SE tend to continue

their business activities even if they experience lower earn-

ings growth (Hamilton, 2000).

These estimates also indicate that a one percentage point

increase in convexity requires an increase of approximately

nine to fourteen percentage points in netincdiff to keep these

hazards unchanged. Note that increases in convexity in this

calculation are assumed to take place via changes to the

volatility of SE income (online appendix A.1 equation [A.4])

because we assume no uncertainty in WE income in the cal-

culation of this variable. De la même manière, the increase in netincdiff

is assumed to work either via a reduction in the pretax income

in WE or via an increase in the expected pretax SE income

(not altering the variance of the SE income distribution). À

further explore these effects accounting for the relationship

between the two tax variables, we simulated a policy experi-

ment. The results are presented below.

28The bootstrapped standard errors to account for the tax variables be-

ing “generated regressors” did not change the significance of our variables

compared to the usual maximum likelihood standard errors for our base

model reported in table 2. Ainsi, we report only the usual MLE standard

errors in this table and subsequent tables.

B. Results from a Policy Experiment

So far we have looked at the effects of partial changes in the

tax variables netincdiff and convexity. Motivated by the anal-

ysis in Wen and Gordon (2014), to gain further understanding

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

387

FIGURE 10.—MARGINAL TAX RATE FOR WAGE INCOME, YEAR 2000, AND HYPOTHETICAL UNIQUE SURTAX ON PERSONAL INCOME

(je) Bold line: Marginal tax rate for a wage earner in tax class 1 (see online appendix A.2) with only wage income in year 2000. Employer’s social security contributions are excluded. (ii) Dashed line: année 2000 tax

experiment. The two surtaxes are replaced by a single surtax of 11% for gross incomes exceeding 200,000 NOK. (iii) To improve readability, the case for self-employment income is not reported, because it would only

imply a proportional vertical shift of each marginal tax curve presented; see figure 1.

of how these related changes may be achieved through tax-

ation, we consider a hypothetical reform in the year 2000.

We chose this year because the Norwegian government in-

troduced two changes in the taxation of gross income from

wage and self-employment in that year. The threshold for the

1999 surtax rate of 13.5% was increased from 269,100 NOK

à 277,800 NOK. More importantly, an additional surtax was

introduced for income exceeding 762,700 NOK (dashed line

in figure 10). These changes increased the overall progres-

sivity of the Norwegian income tax system.29

Our policy experiment is to replace two of the surtaxes

applied to personal income with one surtax, to create a flat-

ter tax schedule (solid line in figure 10). The surtax value

de 11% on gross income above 200,000 NOK is chosen to

ensure revenue neutrality, given a “no behavioral reaction”

assumption. Other features of the taxation are held constant.

New values of netincdiff and convexity were generated un-

der the hypothetical scenario using our tax simulator and the

transition rates predicted from the estimated models.

The average values of the netincdiff and convexity variables

in our weighted sample are −0.374 and 0.0071 under the

new policy regime, compared to the original figures for the

année 2000 of −0.382 and 0.0087, respectivement. As expected,

the less progressive tax schedule leads to a decrease of 0.16

percentage points in convexity. The hypothetical policy also

29According to exchange rates for 2000: 1 EUR ≡ 8.11 Norwegian kroner

(NOK), et 1 USD ≡ 8.81 NOK.

leads to a small increase in the mean netincdiff, so that average

ratio of net income in SE to net income in WE changes from

68.2% à 68.8%.

The predicted transition probabilities and the correspond-

ing standard errors, under the old and the new tax regimes,

are reported in table 3.30 In the benchmark year 2000, le

model predicts that around 9.33% of self-employed individ-

uals will transit out of SE to WE (case A).31 Cependant, le

reform reduces this figure to 9.32% (case B). Under the new

regime, the predicted transitions from WE to SE are higher

à 0.68% compared to 0.56% in the base model. Since a very

large proportion of individuals are in WE compared to SE,

even with this small increase in the exit rates out of WE can

generate a substantial net inflow into SE. The change in the

exit rates induced by the policy reform is not significant for

the self-employed.

To further explore how the model predicts responses to

separate changes in the two tax variables, we look at these

effects separately. In case C we hold the convexity variable

fixed at a value that is the same as in the base case scenario

and let the netincdiff variable change. Inversement, in case D

we see a change in the convexity variable only. Tableau 3 shows

that the partial effect of a change in netincdiff is an increase

in transitions out of both SE and WE. This result is consistent

30All predictions including the differences in predicted exit rate, et le

associated standard errors, use all four hazards. These are calculated using

STATA’s margins command.

31The observed exit rates in 2000 étaient 9.813% et 0.595%.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

388

THE REVIEW OF ECONOMICS AND STATISTICS

Case

UN

B

C

D

TABLE 3.—AVERAGE PREDICTED EXIT PROBABILITIES (%) UNDER THE TAX REFORM SCENARIO

Tax Scenario

from SE, %

from WE, %

Probability of Exit

Base model: année 2000, two surtaxes

(s.e.)

Reform scenario: année 2000, one surtax

(s.e.)

Change A − B

(s.e.)

Sample size in year 2000

convexity: unchanged from baseline netincdiff: reform

(s.e.)

netincdiff: unchanged from baseline convexity: reform

(s.e.)

9.334

(0.227)

9.316

(0.289)

0.018

(0.184)

6,043

9.622

(0.234)

9.034

(0.276)

0.562

(0.011)

0.682

(0.016)

−0.119

(0.010)

130,019

0.571

(0.011)

0.673

(0.015)

(je) Actual exit rates in 2000 étaient 9.813% et 0.595%. (ii) Predicted exits are based on the estimated model from table 2. (iii) The percentage exits are calculated with respect to the stocks in each of the occupational

catégories. (iv) Case A refers to the actual situation as it was in year 2000 with two surtaxes; Calculated convexity and netincdiff in this scenario were used in the estimation of the main model. (v) Case B refers to a

hypothetical reform scenario that replaces two surtaxes with just one surtax. New values of convexity and netincdiff are recalculated given the new tax rules. (vi) Case C considers values of convexity from the baseline

scenario and values of netincdiff from the reform scenario. (vii) Case D considers values of netincdiff from the baseline scenario and values of convexity from the reform scenario. (viii) The above predictions and

the associated standard errors were calculated using the delta method in STATA’s command margins. Average exit rates as well as the differenced average exit rates were all calculated using all four hazards. (ix) All

calculations are based on the weighted sample.

with the fact that mean netincdiff experiences a decrease in the

reform scenario for the self-employed, whereas it increases

for wage earners. A possible explanation for this effect is that

the reduced progressivity of the tax system would encourage

a larger share of wage earners who expect to be successful

in self-employment to transit into SE. On the other hand,

because a majority of self-employed individuals have been

predicted to have a higher posttax income in regular employ-

ment, a flatter tax scenario would increase the proportion of

them leaving SE for WE. In contrast, the decrease in convex-

ville, common to both WE and SE observations, reduces the

transitions from SE and increases the exit from WE. In sum-

mary, the hypothetical tax scenario is found to encourage the

net inflow into SE. Translating these estimates to numbers,

we find that such a policy would have resulted in an increase

depuis 2.76% à 5.34% in the net inflow into SE.32

Enfin, we briefly compare our results to the findings of

Wen and Gordon (2014), given that the same variables are

used to capture the effects of taxes and uncertainty. Wen and

Gordon (2014) also simulated the effect of a flatter tax sched-

ule in the year 2000 using Canadian data. Their policy reform

implied decreases in the average values of (je) netincdiff and

convexity from −22.5% to −23.3% (a decrease of 4%) et

(ii) depuis 1.2% à 0.8% (a reduction of 33%). The policy re-

form we considered increased the average values of netincdiff

by around 2%, and reduced the average values of convexity

par 18%. From the simulated policy reform, Wen and Gordon

(2014) estimate an increase in the number of self-employed

individuals of 0.78% (5.76% à 5.80%), which is substan-

tially below our estimate of 2.6% (our experiment implies an

increase of the self-employment share in 2001 depuis 4.56%

à 4.68%). One should however note that Wen and Gordon

(2014) do not model transitions.

32The predicted probability of exit from SE in the reform scenario is not

statistically significantly different from the base model, and so we use the

base model predicted probability. With the reform scenario prediction, le

predicted net inflow would rise to 5.36%.

C.

Sensitivity Checks

In this subsection we present results of some of our inves-

tigations into key assumptions of our empirical approach. Nous

consider the following: (je) redefinition of a self-employment

spell; (ii) estimation based only on the inflow sample;

(iii) trimming the netincdiff with respect to extreme values;

(iv) controlling for local unemployment rates; (v) y compris

a dummy variable for individuals receiving some unemploy-

ment insurance during the year; et (vi) allowing for the

share of capital in SE income to be nonzero. Tableau 4 reports

the results of these investigations. The estimated effects of

the tax variables are qualitatively unchanged. The full set of

results is available in the online appendix A.3.

Our first investigation examines the influence of the defini-

tion of an SE spell. In our base model we included individuals

in the sample if they had at least three years of labor market

attachment, c'est, if the net SE income or WE is larger in ab-

solute value than the basic amount for at least three years over

the years the individual is observed in data. We now redefine

the sample requiring only one year of labor market attach-

ment. The results using this new definition are presented in

panel B of table 4. Individuals with less attachment to the la-

bor market would be expected to be more sensitive to changes

in the tax variables, and this is what we find when we include

these individuals in the estimation sample. The results are

qualitatively similar to the results from our base case (panel

UN). Cependant, the coefficient for convexity in the SE fresh

spells hazard decreased substantially. Individuals with less

attachment to the labor market with low predicted SE income

might be expected to be less sensitive to the progressivity of

the tax system.

The base model was estimated using both the left-censored

and fresh spells. We reestimate our model using only the in-

flow sample. This reduces the total number of unweighted

observations to 229,036. The definition of an SE spell is the

same as the one used in our base model. The results are pre-

sented in panel C of table 4. The results are broadly similar

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TAX PROGRESSIVITY AND SELF-EMPLOYMENT DYNAMICS

389

TABLE 4.—SENSITIVITY CHECKS: HAZARD MODEL ESTIMATES

Fresh Spells

Left-Censored Spells

Variables

UN. Base case

netincdiff

convexity × 100

B. Changes to sample definition

netincdiff

convexity × 100

C. Excluding left-censored spells

netincdiff

convexity × 100

D. Using trimmed netincdiff

netincdiff

convexity × 100

E. Including regional unemployment rate 1996–2011

netincdiff

convexity × 100

F. Including regional dummies 1996–2011

netincdiff

convexity × 100

G. Including unemployment benefits dummy

netincdiff

convexity × 100

H. Using 3.7% capital income invested in SE

netincdiff

convexity × 100

SE

[1]

−0.429

(0.053)

0.049

(0.015)

−0.493

(0.016)

0.011

(0.005)

−0.405

(0.053)

0.055

(0.015)

−0.333

(0.068)

0.065

(0.017)

−0.531

(0.057)

0.045

(0.018)

−0.519

(0.057)

0.036

(0.018)

−0.415

(0.053)

0.049

(0.015)

−0.434

(0.052)

0.058

(0.016)

WE

[2]

1.685

(0.082)

−0.246

(0.021)

1.734

(0.026)

−0.277

(0.007)

1.920

(0.083)

−0.292

(0.022)

2.281

(0.108)

−0.222

(0.025)

1.709

(0.096)

−0.292

(0.026)

1.762

(0.095)

−0.314

(0.026)

1.698

(0.082)

−0.252

(0.022)

1.712

(0.083)

−0.264

(0.024)

SE

[3]

−0.725

(0.109)

−0.017

(0.030)

−0.615

(0.034)

0.016

(0.009)

−0.871

(0.138)

−0.061

(0.032)

−0.718

(0.110)

0.047

(0.029)

−0.754

(0.110)

0.038

(0.030)

−0.694

(0.109)

−0.014

(0.030)

−0.719

(0.108)

−0.008

(0.031)

WE

[4]

1.753

(0.087)

−0.163

(0.023)

1.768

(0.028)

−0.187

(0.007)

2.998

(0.134)

−0.237

(0.026)

1.568

(0.083)

−0.115

(0.025)

1.607

(0.081)

−0.140

(0.024)

1.763

(0.087)

−0.165

(0.023)

1.761

(0.086)

−0.166

(0.025)

(je) Standard errors in parentheses. (ii) See section VC for further details. (iii) Panels E and F report results with no unobserved heterogeneity (see footnote 35). (iv) Also see notes to table 2. (v) A full set of results

are available in the online appendix A.3.

to our base model results. As expected, dropping those spells

for which we have no information about the length of time

they had spent in a particular state prior to the sample start

slightly increases the estimates.

The third investigation involves omitting observations with

extreme predicted values for the variable netincdiff. Comme indiqué

in figure 5, the distribution of netincdiff exhibits some lumpi-

ness in the tails. To assess the effect of extreme values of

netincdiff, we drop those individuals who have at least one

occupation-specific netincdiff above the top 1% or below the

1% cut-off values.33 Since individuals with very high or low

netincdiff would be expected to be less sensitive than the oth-

33To preserve a continuous series of observations, all observations be-

longing to an individual are dropped if we find at least one neticdiff that

is either less than the first percentile or above the 99th percentile value for

that individual resulting in a loss of more than 2% of the sample. We lose

à propos 9% of the observations, resulting in 432,409 observations in our un-

ers, we would expect the estimated effects of netincdiff to be

higher in absolute values. This is what we see with the results

reported in panel D. In the base model (panel A), we found

the WE exits to be more sensitive than the SE exits, and now

we see that the effect of netincdiff goes up for the WE exits

without much change for in SE exits.

The next investigation examines the influence of local labor

market conditions. In the main specification we use regional

dummies to partially control for labor market conditions. Per-

haps a better control for local labor market conditions would

be the use of local unemployment rates. Unfortunately such

information is available only from 1996, so we report two

sets of results. In panel E we substitute the regional dummies

with regional unemployment rates. In panel F we reestimate

weighted sample. The definition of a SE spell is the same as the one used

in our base model.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

e

d

toi

/

r

e

s

t

/

je

un

r

t

je

c

e

–

p

d

F

/

/

/

/

1

0

5

2

3

7

6

2

0

7

3

2

9

9

/

r

e

s

t

_

un

_

0

1

0

4

6

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

390

THE REVIEW OF ECONOMICS AND STATISTICS

our base model using the restricted sample of 1996 à 2011.

The results are very similar to each other and qualitatively

similar to the baseline results.34

As described in section IV, in our base model we drop

individuals who received more in social security benefits than

their self-employment income or wages in any year. Cependant,

it can be the case that individuals are unemployed for a short

period and the unemployment insurance is small enough so

that the individual is still defined as a self-employed or a wage

earner. Individuals with an interruption to their work might