Sustaining Growth of the People’s Republic

of China

∗

JUSTIN YIFU LIN AND FAN ZHANG

This paper reviews economic growth theory in the framework of economic devel-

opment and explores the possibility of sustained growth in the People’s Republic

of China (RPC) in the long run. We argue that the PRC has the potential to sus-

tain relatively high growth rates. D'abord, since the technological gap with major

developed countries still exists, the PRC can continue to enjoy its “advantage of

backwardness” in the near future. Deuxième, large-scale infrastructure investment,

which began several decades ago, may possibly extend to the future and provide

the country a basis for further growth. Troisième, structural readjustment, which is

needed in many areas, should similarly be able to support the Chinese economy.

This paper argues that to sustain long-term growth in the PRC, a number of gen-

eral preconditions need to be fulfilled—these include well-functioning markets,

a minimum amount of investment, continued structural upgrading, and effective

government.

Mots clés: GDP growth rate, technological innovation, infrastructure invest-

ment, structural adjustment

Codes JEL: E6, O43, O47

je. Introduction

Economic development of the People’s Republic of China (RPC) over the past

30 years has been an intriguing phenomenon. The country provides an interesting

case for the study of economic growth, especially the sources of growth and expec-

tations about future performance. With the PRC’s declining growth rate during the

past 4 années, there have been heated debates recently on the potential growth rate

of the country in the medium and long run. Lin (2012un) argues that the Chinese

economy has the potential to grow by 8% annually for another 20 years beginning

dans 2008.

This paper attempts to provide answers to the question of whether or not the

PRC can indeed maintain a relatively high growth rate in the coming decades. Nous

first present a review of the history of growth performance over the past 35 années

including the recent slowdown, which had triggered concern about long-run growth

∗Justin Yifu Lin (corresponding author, justinlin@nsd.pku.edu.cn) and Fan Zhang (zhangfan@nsd.pku.edu) are both

professors at the National School of Development of Peking University. The authors thank ADB for organizing the

symposium, the referees for useful comments, and Qingqing Chen for her research assistance.

Revue du développement en Asie, vol. 32, Non. 1, pp. 31–48

C(cid:3) 2015 Banque asiatique de développement

et Institut de la Banque asiatique de développement

Publié sous Creative Commons

Attribution 3.0 IGO (CC PAR 3.0 IGO) Licence

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

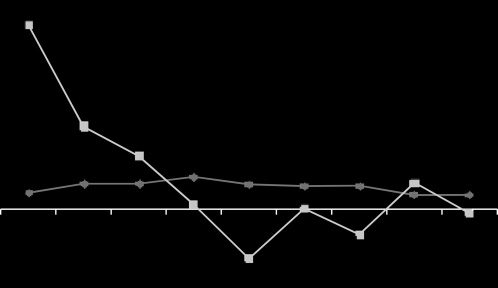

32 ASIAN DEVELOPMENT REVIEW

potential. We also provide a review of the various theories on sustaining growth in

the long run, which serve as the basis for subsequent analysis of the PRC’s growth

potential. Enfin, we discuss the preconditions for sustained growth.

II. Historical Review of the PRC’s Growth Performance

The PRC has been experiencing extraordinary growth in the past 3 and a half

decades, with annual gross domestic product (PIB) growth averaging 9.8% over

the 35-year period since 1978. No country has ever grown as fast or for as long

a time as the PRC during the past 35 années. Before the transition from a planned

economy to a market economy in the late 1970s, the country had been trapped in

poverty for centuries. Cependant, it is now an upper-middle-income economy, avec

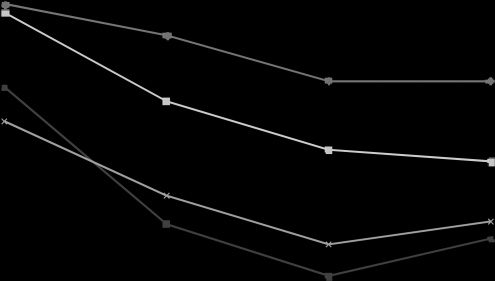

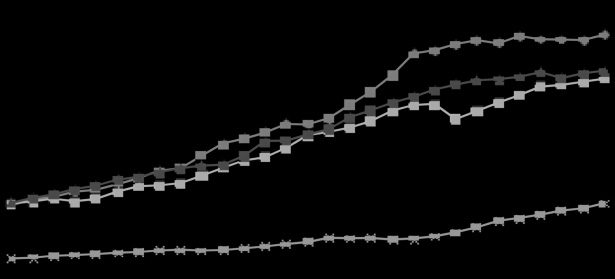

GDP per capita of over $6,000. Prior to the late 1970s, the PRC failed to achieve dynamic growth, as it applied a strategy that prioritized the development of heavy industries. From the 1950s to the 1970s, the Chinese government subsidized the firms in priority sec- tors through various price distortions and protections. Such a strategy was clearly inconsistent with the comparative advantage of the country during the period. Par conséquent, resources became misallocated, total factor productivity (TFP) remained low, and growth was driven mainly by input increases. Firms in the priority sectors became unviable in an open and competitive market. Despite annual GDP growth of 6.1% and the establishment of a complex system of advanced industries during 1952–1978, household consumption grew by only 2.3% annually during the period (Lin 2012a). The PRC has achieved rapid growth since the start of economic reform in the late 1970s, with the extraordinary performance partly due to the adoption of a gradual, dual-track transition strategy. On one hand, the government provided protection in the form of transitory subsidies to prioritized heavy industry sectors to maintain stability. On the other hand, it liberalized entry into sectors where the country had comparative advantage based on factor endowments. The PRC recently experienced a decline in economic growth, which had fallen from 10.4% dans 2010 à 7.7% dans 2013. This is the longest period of growth deceleration since the country’s transition to a market economy in 1979 and has naturally raised concern about the sustainability of growth. Cependant, the slowdown had not been due to overinvestment, financial repres- sion, the state-led growth model, or other internal structural problems frequently mentioned by observers predicting a crash in the Chinese economy.1 The recent slowdown of the Chinese economy in fact was mainly caused by external and 1These include Paul Krugman in his columns (par exemple., Hitting China’s Wall, New York Times, 18 Juillet 2013) and Nouriel Roubini in his articles (par exemple., China’s Bad Growth Bet, Project Syndicate, 14 Avril 2011). Others who have commented on the issue include John Aziz (Is China’s Economy Headed for a Crash? The Week, 13 Janvier 2014), l Téléchargé à partir du site Web : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 33 Chiffre 1. Growth Rates of Exports and Investments of the PRC, 2000–2013 PRC = People’s Republic of China. Source: National Bureau of Statistics. 2014. China Statistical Yearbook 2014. Beijing: China Statistics Press. cyclical factors—specifically, the slow recovery of advanced economies after the 2008 global financial crisis, which has repressed export growth, and the slowdown of the country’s investment growth due to the completion of projects supported by the fiscal stimulus in the aftermath of the 2008 crise (Chiffre 1). These same factors triggered growth deceleration in other emerging market economies and in high-income economies. As seen in Figure 2, the slowdown in the PRC had been relatively mild compared to that in other countries. Facing the potential of a “new normal” in high-income countries (c'est à dire., pro- tracted low growth), export growth will likely be subdued in the coming years. The PRC’s growth will therefore have to depend on domestic demand—investment as well as consumption. How high the country’s growth will be in the coming years meanwhile will depend on its potential growth rate. III. Theories on Sustaining Growth in the Long Run The development of theories of economic growth in the long run has been remarkable in the past half century. Dans cette section, we review the basic features of some of the major theories in a framework of economic development. Nathan Bell (How to Prepare for a China Crash, The Age, 24 Septembre 2012), Vitaliy Katsenelson (How China Will Crash and Burn, Forbes, 6 Juillet 2011), and John Mauldin (The Only Question about the China Crash is When, Business Insider, 24 Novembre 2010). Some observers point to the collapse of the PRC as the biggest risk to the world economy, par exemple, as articulated by George Soros in one of his articles (par exemple., The World Economy’s Shifting Challenges, Project Syndicate, 2 Janvier 2014). In these articles, ADB recognizes China as the People’s Republic of China. l Téléchargé à partir du site Web : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 34 ASIAN DEVELOPMENT REVIEW Figure 2. GDP Growth in the PRC and Selected Countries in 2010–2013 GDP = gross domestic product, PRC = People’s Republic of China. Source: World Bank. World Development Indicators database. The neoclassical growth model, developed in the mid-20th century, is an ex- ogenous growth model of long-run growth set within the framework of neoclassical economics. In these models, the long-run growth rate is exogenously determined by either the savings rate (the Harrod–Domar model) or the rate of technical progress (the Solow model). Solow’s model assumes that factors of production are paid ac- cording to the value of their marginal products. The marginal product of capital will fall if capital rises faster than labor, which is normal for a growing economy, leading to a fall in the growth rate of output. Neoclassical growth theory therefore indicates a convergence or catch-up process in which developing countries acquire techniques and learn how to use them efficiently. This supports arguments for the PRC’s long-run growth slowdown. In the late 1980s, a number of economists began to analyze the nature and role of the residual element in neoclassical growth theories by making it endogenous (Romer 1986 et 1990, Lucas 1988). In endogenous growth theory, connaissance (technologie) is the instrument of production that is not subject to diminishing returns. The theory tries to explain the lack of convergence by introducing the role of human capital, maintaining that economic growth is primarily the result of endogenous forces—e.g., investment in human capital, innovation, and knowledge—and not external forces. Economic growth and convergence will be faster the more the economy is invested in human capital. Aghion and Howitt (1992) developed a model of growth through creative destruction in which innovations serve as the underlying source l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 35 of growth. In their model, the amount of research in any period depends on the expected amount of research next period, which comes from created destruction. The growth rate and the variance of the growth rate are increasing functions of the size of innovation and skilled labor force, and the productivity of research. Development economics uses growth theory to analyze economic growth in developing countries. The theories have come in three waves since the 1950s. The first wave involved structuralism (Rosenstein-Rodan 1943, Prebisch 1950, Chanteur 1950). Based on this thinking, governments were advised to develop industries that were too far advanced compared to their corresponding countries’ level of devel- opment and that went against comparative advantage. Firms were thus nonviable in competitive markets and needed government policy support for initial investment and continuous operation (Lin 2009). The second wave of development thinking, neoliberalism, was encapsulated in the Washington Consensus. The term originally referred to the reform package put together by financial institutions based in Washington, DC and recommended to developing countries mired in crisis in the late 1990s. It has since been used to refer to a more general orientation toward a strongly market-based approach. The Washington Consensus set up a standard for developing countries based on the successful practices of developed economies. It opposed governments playing a proactive role in facilitating entry of firms into sectors even if consistent with a country’s comparative advantage. It also failed to recognize that distortions in developing countries may be endogenous and advised governments to immediately eliminate them, causing the collapse of previously prioritized sectors. The third wave involved what is known as the new structural economics. This development theory argues that each country needs to adjust its economic structure in the process of development according to its comparative advantage as determined by factor endowments (Lin 2012b). It applies a neoclassical economics approach to understand the determinants of economic structure and its evolution. Industrial structure is assumed to be endogenous to the endowment structure, which is given at any specific time and changes over time. New structural economics argues that, following comparative advantage, which is determined by the endowment structure, developing industries is the best way to upgrade the endowment structure and sustain industrial upgrading, income growth, and poverty reduction. If economic structure upgrading lags behind changes in endowments, the economy will be less competitive, and growth will be lower than the potential growth rate. Improvement of the economic structure provides new sources of growth by reducing the inefficiency within and between sectors. Struc- tural upgrading needs a competitive market system and a facilitating state. New structural economics also postulates that industrial policy is desirable, and that target industries should be in line with an economy’s latent comparative advantage. The theory points out that as long as its government chooses the right set of policies, a developing country has the potential to grow continuously at 8% l Téléchargé à partir du site Web : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 36 ASIAN DEVELOPMENT REVIEW or more for several decades and to become a middle-income (or even high-income) country in one or two generations. A review of growth theory in the framework of development tells us that sustaining growth depends on many factors, not just the productivity of physical capital. It is influenced as well by human capital, technologie, and structural change in the economy. All these factors help to determine growth at the dynamic path. IV. The PRC’s Potential for Sustained Growth in the Long Run By adopting correct policies, the PRC has the potential to sustain dynamic growth in the coming decades. This section presents possible reasons for the coun- try’s sustained long-run performance. These are the “advantage of backwardness,” the effect of capital investment, and structural readjustment. UN. The Advantage of Backwardness A backward country has an advantage in economic development because it can borrow from a large backlog of technological innovations from advanced countries and adopt the latest technology without facing resistance from users of old technologies (Gerschenkron 1962). It can thus reduce the costs and risks of technological innovation, allowing it to grow faster than advanced countries. Since the late 1970s, the PRC has achieved high growth by tapping into this advantage of backwardness. After 35 years of dynamic growth, does the PRC still have the potential to grow dynamically? The answer depends partly on whether or not the advantage of backwardness still exists. One way to measure this is by the gap between per capita GDP of the PRC and of the United States (NOUS). Per capita GDP represents a country’s average labor productivity, which in turn reflects the country’s average technological level. The PRC’s per capita GDP measured in purchasing power parity (PPP) dans 2008 as a percentage of that of the US was similar to that of Japan in 1951, the Republic of Korea in 1977, and Taipei,China in 1975 (Tableau 1). Annual GDP growth reached 9.2% in Japan during 1951–1971, 7.6% in the Republic of Korea during 1977–1997, et 8.3% in Taipei,China during 1975–1995. After 20 years of growth, Japan’s per capita income measured in PPP was 66% that of the US in 1971. The corresponding percentage for the Republic of Korea was 50% dans 1997, while that for Taipei,China was 54% dans 1995. Chiffre 3 shows the per capita GDP of Asian economies relative to the US per capita GDP from the year these economies started to take off—1951, 1975, 1977, et 1980, respectivement, for Japan; Taipei,Chine; la République de Corée; and the PRC. Tableau 2 meanwhile indicates the degree of the advantage of backwardness l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 37 Tableau 1. Asian Economies’ Per Capita GDP as a Percentage of the US Per Capita GDP (%) 1951 1967 1971 1975 1977 1987 1995 1997 2008 21 8 9 5 50 11 14 5 Japan Republic of Korea Taipei,China PRC GDP = gross domestic product, PRC = People’s Republic of China, US = United States. Note: GDP per capita is measured in 1990 international Geary-Khamis dollars. Sources: Authors’ calculations; Maddison, Angus. 2011. Historical Statistics of the World Economy: 1–2008 A.D. Tables 2c and 5c. Available online at: www.ggdc.net/maddison/Historical_Statistics/horizontal-file_02-2010.xls. 69 21 24 5 66 15 18 5 70 19 22 5 75 32 39 8 80 50 57 12 81 48 54 12 73 63 67 22 Chiffre 3. Asian Economies’ Per Capita GDP as a Percentage of the US Per Capita GDP—Since Takeoff l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e du a d e v / art – pdlf / / / / / 3 2 1 3 1 1 6 4 1 1 0 6 a d e v _ a _ 0 0 0 4 5 pd . f par invité 0 8 Septembre 2 0 2 3 GDP = gross domestic product, US = United States. Note: Per capita GDP is based on purchasing power parity valuation of the GDP of an economy. Sources: Authors’ calculations; Maddison, Angus. 2011. Historical Statistics of the World Economy: 1–2008 A.D. Available online at: www.ggdc.net/maddison/Historical_Statistics/horizontal-file_02-2010.xls. in terms of stocks of capital and human capital per person (c'est, by disentangling the extent that output per worker might be driven by differences in these stocks or other features). We extend growth accounting analysis for the PRC using the Penn World Table (PWT), which decomposes growth in GDP per worker according to various sources—namely, growth of physical capital per worker k, human capital per worker hc, and TFP A. This can be represented by the following equation: (cid:2) ln yit = αit (cid:2) ln kit + (1 − αit ) (cid:2) ln hcit + (cid:2) ln Ait . (1) 38 ASIAN DEVELOPMENT REVIEW Table 2. Comparison of the PRC and the US—Capital Stock and Human Capital Per Capita in 2011 GDP Per Capita (2005 $)

Capital

Stock Per

Capita (2005 $)

Human

Capital Per

Persona

Non. of Persons

Engaged

(millions)

TFP at Constant

National Prices

(2005 = 1)

3.619

2.579

42,446

9,324

22.0%

131,347

33,134

25.2%

NOUS

RPC

PRC/US

PRC = People’s Republic of China, TFP = total factor productivity, US = United States.

aIndex based on the number of years of schooling and returns to education.

Sources: Center for International Comparisons at the University of Pennsylvania. Penn World Table 8.0. 2014.

Available online at: http://www.rug.nl/research/ggdc/data/penn-world-table (accessed January 2015). National Bureau

of Statistics. 2012. China Statistical Yearbook 2012. Beijing: China Statistics Press.

141.8

784.4

1.020

1.193

Tableau 3. Forecasts of the PRC’s GDP Growth and Growth Components

Real GDP

(constant

2005

national

prices, %)

7.8

10.4

Capital

Stock

(constant

2005

national

prices, %)

8.1

11.8

Human

Capital

Per

Persona (%)

Nombre

of Persons

Engaged

(%)

TFP at

Constant

National

Prices (%)

1.2

0.9

2.3

0.8

2.0

3.0

Average

1952–2011

Average

2001–2011

High

High

High

High

Low

8.1

7.6

7.3

6.1

5.4

Low

9.1

8.8

8.3

6.8

5.5

Forecasts

2012

2013

2014

2015–2020

8.8

2021–2028

7.5

GDP = gross domestic product, PRC = People’s Republic of China, TFP = total factor productivity.

aIndex based on the number of years of schooling and returns to education.

Note: We use a capital coefficient of 0.59 for 2015–2028.

Source: Authors’ computations.

Low

0.3

0.0

0.0

0.0

0.0

Low

1.1

1.1

1.1

1.0

1.0

1.2

1.2

8.0

7.6

0.0

0.0

Low

2.0

2.0

2.0

1.7

1.7

High

2.3

2.3

We use the average of the capital coefficient in the past 5 years estimated

by the PWT for the period 2015–2028 and calculate the growth of GDP and its

components from 2012 à 2028 assuming zero growth rate in the number of workers

during the forecasting period (see Table 3).

We assume the following in our economic analysis: a zero growth rate for the

number of workers during 2015–2028, which is consistent with the population trend

and age structure of the PRC, and a 1%–1.2% increase in human capital per person

during 2015–2028, or slightly lower than the actual annual growth of human capital

de 1.2% during 1952–2011.

We also assume that the country’s capital stock will keep growing albeit

at a moderate rate based on the assumptions of continued structural upgrading

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 39

Tableau 4. A Comparison of Growth Rates in Different Economies in Similar Growth Stages

Real GDP

(constant 2005

national

prices, %)

Capital Stock

(constant 2005

national

prices, %)

Human

Capital

Per

Persona (%)

Nombre

of Persons

Engaged

(%)

TFP at

Constant

National

Prices (%)

0.8

3.6

8.3

3.8

1.3

11.8

Japan

1951–1971

Republic of Korea

1977–1997

Taipei,Chine

1975–1995

GDP = gross domestic product, TFP = total factor productivity.

aIndex based on the number of years of schooling and returns to education.

Sources: Authors’ computations; Center for International Comparisons at the University of Pennsylvania. Penn

World Table 8.0. 2014. Available online at: http://www.rug.nl/research/ggdc/data/penn-world-table (accessed

Janvier 2015).

10.7

2.6

8.3

2.5

1.1

1.3

1.1

1.4

0.9

and discovery of new investment areas. The increase will be 6.8%–8.8% during

2015–2020 and 5.5%–7.5% during 2021–2028, lower than the actual growth rate of

capital stock during 2001–2011 (11.8%) et 2013 (8.8%).

TFP growth will similarly decline slightly during the forecast period, comme

the PRC approaches the world technological frontier. We assume a growth rate

of 1.7%–2.3% during 2015–2028, lower than the actual growth rate of 3% pendant

2001–2011.

Our growth accounting analysis shows that the GDP growth rate of the PRC

will be in the range of 6.1%–8.0% before 2020 and 5.4%–7.6% during 2021–2018

if capital stock increases by 6.8% à 8.8% during 2015–2020 and by 5.5% à

7.5% during 2021–2028, human capital per person increases by 1% à 1.2% pendant

2015–2028, and TFP increases by 1.7% à 2.3% during 2015–2028. The assumptions

are reasonable and conservative compared to growth rates in previous periods, lequel

are also shown in Table 3.

To support our forecasts, we calculate using PWT data the average annual

growth rates of physical capital, human capital, and TFP in Japan; the Republic

of Korea; and Taipei,China during the same development stage that the PRC finds

itself in currently. The results are shown in Table 4. Since the PRC is in a similar

development stage as the Republic of Korea during 1977–1997 and Taipei,Chine

during 1975–1995, it is likely that the country’s capital stock and TFP will grow at

similar rates in the near future.

To prevent mistakes in forecasting, our assumptions about the growth rates of

the PRC’s capital stock are tailored to be more conservative than the actual growth

rates of capital stock in the Republic of Korea during 1977–1997 (11.8%) et

Taipei,China during 1975–1995 (10.7%).

If the PRC maintains an 8% growth in the next 2 decades, par 2030, the PRC’s

per capita income measured in PPP may reach about 50% of that of the US. Le

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

40 ASIAN DEVELOPMENT REVIEW

exploitation of the advantage of backwardness has and will allow the PRC to achieve

extraordinary economic growth by reducing the costs of innovation, industrial up-

grading, and social and economic transformation.

B.

Large-Scale Infrastructure Investment

Public investments, say in infrastructure, may have a positive influence on

long-run growth if it raises the marginal productivity of private capital. Barro (1990)

develops a closed-economy endogenous growth model where government service is

viewed as an input in private producers’ production function. The effects of public

investment on private producers have also been analyzed in many empirical studies.

Aschauer (1989), par exemple, studied the US economy during 1949–1985 and

found that public investment in infrastructure had maximum explanatory power for

the productivity of private capital.

Continued large-scale infrastructure investment, which began when the Chi-

nese economy started to reform and open up, could be another possible factor behind

sustained growth in the near future. The PRC has made large-scale infrastructure

investments over the past several decades, which updated the country’s infrastruc-

ture in all sectors and raised productivity, with continued positive effects on future

growth. Tableau 5 shows the gross capital formation in the PRC from 1991 à 2013.

A rough comparison with the US shows that the PRC’s gross investment

during 2010–2013 measured in US dollars and using official annual average

exchange rates was greater than the US gross domestic investment during the

period. Although the share of physical investment in GDP declined slightly in

recent years, it will remain relatively high in the near future. The quality of physical

investment also remains quite high in terms of operating profit, although it declined

slightly in recent years.

Real estate investment has been an important part of investment in the PRC

in the past 20 années. Tableau 6 shows the operating statistics of real estate firms in the

country. The share of taxes and profits increased dramatically beginning in 2005 et

continued to be relatively high until 2012. This suggests that investments in real estate

and physical capital will keep growing at a comparatively high rate in the near future.

From the most recent data, we expect that returns on investment will gradually

fall but will stay at a level high enough to attract investment. Basé sur ceci, nous

forecast that investment in physical capital will continue to grow at a rapid pace in

the near term.

Many economists worry that the PRC’s economic growth relies too heavily

on saving and investment. They posit that a large contribution of capital means a

small contribution to technological progress, a condition that may not be sustain-

capable. Cependant, none of the existing methods measuring technological progress has

successfully accounted for the technological progress embedded in capital. Capital

investment brings about new approaches of production as well as new teams of

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 41

Tableau 5. Investment in the PRC during 1991–2013

Gross Capital Formation

(CNY billion)

% of GDP

(expenditure approach)

786.80

1,008.63

1,571.77

2,034.11

2,547.01

2,878.49

2,996.80

3,131.42

3,295.15

3,484.28

3,976.94

4,556.50

5,596.30

6,916.84

7,785.68

9,295.41

11,094.32

13,832.53

16,446.32

19,360.39

22,834.43

25,277.32

28,035.61

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

GDP = gross domestic product, PRC = People’s Republic of China.

Source: National Bureau of Statistics. 2014. China Statistical Yearbook

2014. Beijing: China Statistics Press. Tables 2–18.

34.8

36.6

42.6

40.5

40.3

38.8

36.7

36.2

36.2

35.3

36.5

37.8

41.0

43.0

41.5

41.7

41.6

43.8

47.2

48.1

48.3

47.8

47.8

workers, which together increase productivity and bolster growth. There may also

be a time lag between capital investment and the functioning of capital stock.

The potential role of physical capital in development depends on the rela-

tionship between investment and technical progress. Scholars working on growth,

especially those focusing on technology diffusion and TFP, have been studying this

potential role. Caselli and Wilson (2004) found strikingly large differences in in-

vestment composition across countries, with the composition of capital accounting

for large observed differences in TFP across countries. They also found that the

differences were based on each equipment type’s degree of complementarity with

other factors whose abundance differs across countries (Caselli and Coleman 2001).

Comin and Hobijin (2004) observed a trickle-down mechanism in the dif-

fusion of technologies across countries, which meant that although most of the

technologies originating from advanced economies were adopted there first, other

countries that lag economically could still benefit subsequently. The determinants

of the speed at which a country adopts technologies include the country’s human

capital endowment, type of government, degree of openness to trade, and adoption

of predecessor technologies.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

42 ASIAN DEVELOPMENT REVIEW

Tableau 6. Operating Statistics of Real Estate Firms

Revenue from Principal Business

(CNY100 million)

Share of Taxes and Profits

(%)

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

528.56

1,135.91

1,288.19

1,731.66

1,968.79

2,218.46

2,951.21

3,026.01

4,515.71

5,471.66

7,077.85

9,137.27

13,314.46

14,769.35

18,046.76

23,397.13

26,696.84

34,606.23

42,996.48

44,491.28

51,028.41

19.9

22.2

20.4

13.5

5.6

4.2

4.3

3.6

6.4

7.3

8.8

10.1

9.5

13.2

15.5

17.5

19.7

21.1

22.3

21.6

20.8

Source: National Bureau of Statistics. 2014. China Statistical Yearbook 2014. Beijing:

China Statistics Press. Tables 5–38.

Jorgenson and Vu (2010) introduced a new framework for projecting the

potential growth of the world economy, emphasizing the contribution of information

technologie. Investment in information and communications technology (ICT) raises

the amount of capital available for labor, thus increasing labor productivity, likely

increasing economic growth. It also introduces new technologies into the production

processus.

Inklaar and Timmer (2013) discuss new measures of capital stocks in PWT

version 8.0, while Aghion (2014) notes the positive relation between ICT share (dans

value-added) and economic growth, using panel data. The contribution of investment

in ICT has increased in all regions of the world, but especially in industrialized

economies and developing Asia.

To explore the sustainability of the PRC’s future growth in physical capital

investment based on the composition of capital, we collected data on the growth of

ICT capital services. Data show that ICT capital services grew at a more rapid pace

in the country than in Japan, la République de Corée, and the US during 2000–2013

(Tableau 7).

This suggests that the potential exists for further increases in productivity and

capital investment in the PRC in the near future. The average annual contribution

of ICT capital services to overall growth in capital services in the country was 1.06

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 43

Tableau 7. Growth in ICT Capital Services

(in difference, %)

RPC

Japan

Republic

of Korea

NOUS

6.62

7.24

6.74

5.27

5.64

4.76

3.30

3.69

5.62

7.84

8.66

8.94

9.89

10.73

28.73

26.44

24.90

24.48

25.78

26.46

25.17

22.06

20.92

19.71

17.18

15.52

15.82

17.39

20.07

17.30

10.75

6.13

3.39

4.62

7.27

8.93

8.32

6.39

6.05

7.87

9.42

10.50

2000

18.44

2001

13.86

2002

8.12

2003

5.94

2004

6.59

2005

7.31

2006

8.06

2007

9.19

2008

9.00

2009

6.59

2010

5.10

2011

5.58

2012

6.87

2013

8.21

ICT = information and communications technology, PRC =

People’s Republic of China, US = United States.

Source: The Conference Board Total Economy Database. Available

online at: http://www.conference-board.org/data/economydatabase/

(accessed January 2014).

percentage points from 2004 à 2013, compared with 5.57 percentage points for

non-ICT capital services during the same period.

In addition to rapid physical capital accumulation, the PRC has seen large-

scale human capital accumulation. The country has been improving its stock of

human capital over the past 30 années, owing to government commitment and in-

creasing returns to education. Education spending by the Chinese government in

terms of the share of total government spending is lower than that in the US but

higher than in the United Kingdom and Japan (Bai, Wang, and Qian 2010).

Higher education in the PRC has grown at a faster pace than both primary

and secondary education. College admission and enrollment has increased tenfold,

avec 6.4 million bachelor’s and 514,000 master’s and PhD degree holders produced

by Chinese universities in 2013 (Tableau 8). The quality of human capital investment

in the country has also improved through the years. The number of college students

graduating as a percentage of the total has risen in the 2010s compared to the 1990s.

Tableau 9 similarly shows that the number of graduates from college and senior

secondary schools in the PRC has increased dramatically in recent years. Ce

trend, which has greatly improved the country’s quality of education, is expected to

continue in the near future. As Aghion (2014) and other authors have pointed out,

education is important in bolstering economic growth.

C.

Structural Readjustment

The PRC has been experiencing structural changes in the past 3 decades.

Structural readjustment, which allows a transfer of resources from sectors with

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

44 ASIAN DEVELOPMENT REVIEW

Tableau 8. Graduates in the PRC

(thousands)

Collège

MA and PhD

MA and PhD/

Undergraduates (%)

32.5

31.9

58.8

189.7

514.0

614.0

805.0

949.8

3068.0

6,387.2

1991

1995

2000

2005

2013

MA = Master of Arts, PhD = Doctor of Philosophy.

PRC = People’s Republic of China.

Sources: National Bureau of Statistics of China. 2010. Sixty Years of New

Chine. Beijing: China Statistics Press; National Bureau of Statistics of China.

2014. China Statistical Yearbook 2014. Beijing: China Statistics Press.

5.0

3.8

5.8

5.8

7.4

Tableau 9. Number of Graduates by Level and Type of School

(millions)

Regular

Collège

Regular Senior

Secondary

Schools

Secondary

Vocational

Éducation

Junior

Secondary

École

Regular

Primary

École

1978

1990

2000

2010

2012

2013

0.165

0.614

0.950

5.754

6.247

6.387

6.827

2.330

3.015

7.944

7.915

7.990

11.230

16.335

17.504

16.608

6.653

6.749

22.879

18.631

24.192

17.396

16.416

15.811

Source: National Bureau of Statistics. 2014. China Statistical Yearbook 2014. Beijing: Chine

Statistics Press. Tables 20–9.

Tableau 10. Annual Growth Rate of Patents Granted

Period

1985–1989

1990–1994

1995–1999

2000–2004

2005–2009

1985–2009

Source: Xie and Zhang 2014.

(%)

27

17

15

20

19

19

lower productivity to sectors with higher productivity, serves as another source of

economic growth.

Brandt, Hsieh, and Zhu (2008) decomposed the PRC’s growth according to

agriculture and non-agriculture sources during 1978–2004 and found that labor

reallocation from agriculture to non-agriculture contributed 24.6% to the country’s

overall growth. They attribute this to the large productivity gap between agriculture

and non-agriculture sectors during the period.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 45

Theoretically, GDP growth in a multisector model can be divided into four

components—the contributions of capital, labor, pure technical progress (weighted

average of technical progress in all sectors), and structural change.

The current Chinese economy is still far from its long-term steady state. Large

productivity gaps still exist between sectors of the economy, while endowments

continue to change as income rises. The production structure clearly needs to change

to follow the changes in endowments. These structural readjustments should be able

to provide new sources of economic growth and raise the potential for a relatively

high growth rate in the medium to long run.

Heterogeneity at the firm level is a source of productivity growth. Aghion

(2014) points out that the heterogeneity between firms is much larger than that be-

tween sector averages. In the US, the productivity of the top 10% most productive

firms is twice that of the bottom 10%. Hsieh and Klenow (2009) find the corre-

sponding multiple to be as high as 5 times in the PRC. This huge difference shows

the country’s potential for structural improvements in the future.

The enormous size of the Chinese economy benefits structural readjustment,

as a wide enough industrial spectrum makes an update of the industrial structure and

a widening of product variety possible. The huge product space makes it possible

for the country to upgrade its industrial structure at a wide scale. This feature

differentiates the PRC from mid-sized countries such as Japan and the Republic of

Korea.

Aside from well-functioning markets and continued structural upgrading,

there are other factors that contribute to the structural improvement of the Chinese

economy and that help drive future growth. These include private sector development

and privatization of state-owned enterprises to spur greater competition, greater pro-

tection of intellectual property rights and other legal support to encourage R&D and

innovation in the manufacturing sector, bilateral investment treaties and free trade

zones to foster greater openness of the economy, and deregulation and introduction

of greater competition to improve productivity in the services sector.

Innovation is a key driver of long-run growth, one that is particularly important

for middle-income countries such as the PRC. Xie and Zhang (2014) find that

domestic Chinese firms have become increasingly more innovative in terms of

patent applications, and that private firms, rather than state-owned firms, have been

the engine of innovation. Facing increasing wages, the firms have had to invest more

in technologies to substitute the more expensive labor. The annual growth rate of

patents granted during 1985–2012 averaged at 19%, almost twice the annual growth

rate of GDP during the same period (Xie and Zhang 2014).

Dans l'ensemble, on one hand, the PRC is still far behind the world technology frontier

and will continue to enjoy the advantage of backwardness. On the other hand, it is

closer to the world technology frontier than at any time previously and possesses

greater capital and skilled labor than it did 30 years ago. This provides a basis for

updating industries and further economic development.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

46 ASIAN DEVELOPMENT REVIEW

V. Preconditions for the PRC’s Sustained Growth and Policy Suggestions

The PRC has the potential to sustain a relatively high growth rate in the long

run provided government adopts the right policies. There are a number of general

preconditions or prerequisites that must be met in order to achieve this goal.

The PRC needs to narrow income disparities and fight corruption to main-

tain social stability. Greater income disparity and corruption are the results of the

dual-track transition strategy where the government continues to provide subsidies

and protection to nonviable firms in prioritized capital-intensive sectors, creating

distortions in factor markets and monopolies in certain service sectors while allow-

ing or facilitating the entry of new firms to the labor-intensive sector that had been

previously repressed. Such an approach allows the country to achieve stability and

dynamic growth simultaneously.

Cependant, distortions in factor markets and monopolies in telecommunications

and financial sectors create rents and encourage rent-seeking, leading to greater

income disparity and corruption. Many capital-intensive firms in the old prioritized

sectors have become viable because of the change in the endowment structure, lequel

was a consequence of rapid growth and capital accumulation over the past 35 années.

It is time for the country to eliminate these distortions and complete the transition

to a well-functioning market economy, allowing prices to play a decisive role in

resource allocation to improve efficiency and eliminate the root of income disparity

and corruption (Lin 2012a).

The PRC needs to continue investing in physical and human capital in order

to change its endowment structure. It also needs to continue upgrading technologies,

transforming its industrial structure, and tapping latecomer advantages. As devel-

opments continue, factor endowments and industrial structure will keep changing,

and the country will need to update its infrastructure accordingly. The inconsistency

between the two means leaving the equilibrium path and lowering trend growth.

Enfin, the Chinese government also needs to play an enabling role in future

développement économique. It needs to help firms reduce transaction costs by improving

both soft and hard infrastructure. A sound fiscal position, at both central and local

government levels, will be beneficial to economic growth. An enabling government

is also essential to overcome inherent externalities of technological innovation and

industrial upgrading. State effort is also needed to improve the country’s environ-

mental quality and achieve environmental sustainability.

VI. Concluding Remarks

In sum, the PRC can sustain a relatively high growth path over a long period

based on three basic arguments. D'abord, since a substantial technological gap still

exists between the PRC and major developed countries, it can continue to enjoy the

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

SUSTAINING GROWTH OF THE PEOPLE’S REPUBLIC OF CHINA 47

advantage of backwardness. Deuxième, the long period of large-scale infrastructure

investment that began several decades ago can still continue and provide the country

a basis for further growth. Troisième, structural readjustment, which is needed in many

fields, should be able to bolster economic growth in the long run. These arguments

are supported by growth accounting analysis.

We argue that to realize the potential for sustained growth, a number of general

preconditions or prerequisites need to be fulfilled. These include well-functioning

marchés, an appropriate rate of investment, continued structural upgrading, and an

enabling government that can facilitate the appropriate structural transformation.

If the economic adjustments are done correctly and in a timely manner, sustained

growth should be possible in the medium- and long-term.

References∗

Aghion, Philippe. 2014. In Search for Competitiveness: Implications for Growth Policy Design in

Chine (in Chinese). Comparative Studies 74(5).

Aghion, Philippe, and Peter Howitt. 1992. A Model of Growth through Creative Destruction.

Econometrica 60(2):323–51.

Aschauer, David. 1989. Is Public Expenditure Productive? Journal of Monetary Economics

23(2):177–200.

Aziz, John. 2014. Is China’s Economy Headed for a Crash? The Week. 13 Janvier.

Bai, Chong-En, Dehua Wang, and Zhenjie Qian. 2010. Several Issues for Public Finance to

Speed up Structural Change (in Chinese). Comparative Studies 3(48):30–72. Available at

http://bijiao.caixin.com/2014-10-08/100735759.html

Barro, Robert. 1990. Government Spending in a Simple Model of Endogenous Growth. Journal

of Political Economy 98(5):S103–S125.

Cloche, Nathan. 2012. How to Prepare for a China Crash. The Age. 24 Septembre.

Brandt, Loren, Chang-Tai Hsieh, and Xiaodong Zhu. 2008. Growth and Structure Change in

Chine. In Loren Brandt and Thomas Rawski, éd.. China’s Great Economic Transformation.

New York: la presse de l'Universite de Cambridge.

Caselli, Francesco, and Wilbur Coleman. 2001. Cross-country Technology Diffusion: The Case

of Computers. American Economic Review 91(2):328–35.

Caselli, Francesco, and Daniel Wilson. 2004. Importing Technology. Journal of Monetary Eco-

nomics 51(1):1–32.

Comin, Diego, and Bart Hobijin. 2004. Cross-country Technology Adoption: Making the Theories

Face the Facts. Journal of Monetary Economics 51(1):39–83.

Gerschenkron, Alexander. 1962. Economic Backwardness in Historical Perspective. Cambridge,

Mass.: Belknap Press and Harvard University Press.

Hsieh, Chang-Tai, and Peter Klenow. 2009. Misallocation and Manufacturing TFP in China and

India. Quarterly Journal of Economics 124(4):1403–48.

Inklaar, Robert, and Marcel Timmer. 2013. Capital, Labor, and TFP in PWT8.0. Available:

www.rug.nl/research/ggdc/data/penn-world-table

∗ADB recognizes “China” as the People’s Republic of China.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

48 ASIAN DEVELOPMENT REVIEW

Jorgenson, Dale, and Khuong Vu. 2010. Potential Growth of the World Economy. Journal de

Policy Modeling 32(5):615–31.

Katsenelson, Vitaliy. 2011. How China Will Crash and Burn. Forbes. 6 Juillet.

Krugman, Paul. 2013. Hitting China’s Wall. New York Times. 18 Juillet.

Lin, Justin Yifu. 2009. Economic Development and Transition: Thought, Strategy, and Viability.

Cambridge, ROYAUME-UNI: la presse de l'Universite de Cambridge.

——. 2012un. Demystifying the Chinese Economy. Cambridge, ROYAUME-UNI: la presse de l'Universite de Cambridge.

——. 2012b. New Structural Economics: A Framework for Rethinking Development and Policy.

Washington, CC: World Bank Press.

Lucas, Robert. 1988. On the Mechanics of Economic Development. Journal of Monetary Eco-

nomics 22(1):3–42.

Maddison, Angus. 2011. Historical Statistics of the World Economy: 1–2008 A.D. Available online

à: www.ggdc.net/maddison/Historical_Statistics/horizontal-file_02–2010.xls

Mauldin, John. 2010. The Only Question about the China Crash is When. Business Insider. 24

Novembre.

National Bureau of Statistics. 2010. Sixty Years of New China. Beijing: China Statistics Press.

——. 2012. China Statistical Yearbook 2012. Beijing: China Statistics Press.

——. 2014. China Statistical Yearbook 2014. Beijing: China Statistics Press.

——. 2014. China Statistical Abstract. Beijing: China Statistics Press.

Prebisch, Raul. 1950. The Economic Development of Latin America and its Principal Problems.

New York: United Nations.

Romer, Paul. 1986. Increasing Returns and Long-run Growth. Journal of Political Economy

94(5):1002–37.

——. 1990. Endogenous Technological Change. Journal of Political Economy 98(5):S71–102.

Rosenstein-Rodan, Paul. 1943. Problems of Industrialization of Eastern and South-eastern Europe.

Economic Journal 53(210/211):202–11.

Roubini, Nouriel. 2011. China’s Bad Growth Bet. Project Syndicate. 14 Avril.

Chanteur, Hans. 1950. The Distribution of Gains between Investing and Borrowing Countries.

American Economic Review (Papers and Proceedings) 40(2):473–85.

Soros, George. 2014. The World Economy’s Shifting Challenges. Project Syndicate. 2 Janvier.

Xie, Zhuan, and Xiaobo Zhang. 2014. The Patterns of Patents in China. IFPRI Discussion Paper

Non. 01385. Washington, CC: International Food Policy Research Institute.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

d

e

v

/

un

r

t

je

c

e

–

p

d

je

F

/

/

/

/

/

3

2

1

3

1

1

6

4

1

1

0

6

un

d

e

v

_

un

_

0

0

0

4

5

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3