Resetting Social Security

S. Jay Olshansky, Dana P. Homme d'or & John W. Rowe

Abstrait: Social Security retirement bene½ts were ½rst introduced in 1935 as a ½nancial safety net for a

large and rapidly growing older American population. The program was intended to be economically self-

sustaining, but population aging and rising life expectancies threaten the program’s solvency. Le 1983

Social Security Amendments mandated that the full retirement age increase to 67 by the year 2027. Dans

this essay, we present evidence demonstrating that the rate of improvement in life extension at older ages

accelerated after 1983. Si le 1935 ratio of working years to retired years is maintained, early and full

retirement ages of 66.5 et 69.4, respectivement, were justi½ed in 2009. Additional delays in the age of eligi-

bility beyond those currently in ef fect would place signi½cant ½nancial burdens on individuals with lower

life ex pectancies, the poor and near-poor, and the very old, and–absent additional reform–would exac-

erbate existing unequal access to entitlements within the system.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

In the future when there are a great many persons over

65, most of the able-bodied individuals will and should

continue working to age 70 ou 75 if their services seem

needed.

–Robert J. Myers, Chief Actuary (1947–1970) and Deputy

Commissioner (1981–1982) of the Social Security Admin-

istration (ssa) and leader of the National Commission on

Social Security Reform (1982–1983)1

Has the time arrived to reset the age of eligibility

for Social Security retirement bene½ts? When Pres –

ident Roosevelt signed the Social Security Act (ssa)

dans 1935 in the wake of the Great Depression, unem-

ployment was 34 pour cent, savings accounts were dec –

imated, and almost 50 percent of the older popula-

tion was dependent on family and friends for ½nan-

cial support. There was reason to believe large seg-

ments of the population–particularly the elderly–

were facing destitution.2

To address this concern, the Committee on Eco-

nomic Security was established by executive order

dans 1934. What we know today as Social Security began

simply as a federally administered social insurance

retirement program for older people, nominally ½ –

nanced through payroll taxes and paid for by work-

© 2015 by the American Academy of Arts & les sciences

est ce que je:10.1162/DAED_a_00331

S. JAY OLSHANSKY is Professor

of Epidemiology at the School of

Public Health, Division of Epide –

miology and Biostatistics at the

Uni versity of Illinois at Chicago.

DANA P. GOLDMAN is Professor

of Public Pol icy, Pharmacy, et

Economics at the University of

Southern California.

JOHN W. ROWE, un membre du

Académie américaine depuis 2005, est

Professor at the Columbia Universi-

ty Mailman School of Public Health

and Chair of the MacArthur Foun-

dation Research Network on an

Aging So ciety.

(*See endnotes for complete contributor

biographies.)

68

/

e

d

toi

d

un

e

d

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

1

4

4

2

6

8

1

8

3

0

5

8

5

d

un

e

d

_

un

_

0

0

3

3

1

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

ers and their employers. As the program

was originally structured by the Social Se –

curity Act of 1935, people would earn ben –

e½ts as they continued to work. If death

occurred before age sixty-½ve, or before

they received what they paid into the sys-

tem even after retirement, their estate

would receive the difference plus interest

in the form of a one-time lump-sum pay-

ment. At the program’s inception, no ben –

e½ts were provided to spouses or children.

Although Social Security was originally

designed to protect a limited number of

American workers against loss of earnings,

President Roosevelt indicated from the

start that the program was expected to

grow and evolve with changing economic

and demographic conditions.3 The ½rst

study published by the Of½ce of the Actu-

ary at the Social Security Board claimed

that “when it is realized that too large a

proportion of the population would prob –

ably be left idle with a retirement age of 65,

the general feeling will undoubtedly be

that a constant retirement age should be

banished, or that it should be left as a bal-

ancing item.”4 A subsequent publication

by Robert J. Myers, Chief Actuary and Dep –

uty Commissioner of the ssa–from which

we quote in our epigraph–made a more

forceful statement about raising the Social

Security Retirement age.5

Social Security has evolved extensively

since its inception. While the program is

best known for providing ½nancial assis-

tance to retirees, amendments to the pro-

gram also added life insurance, payments

for spouses and dependents, and disability

bene½ts for those who are unable to work

but are not yet eligible by age for regular

bene½ts. The ½rst signi½cant change to the

program was introduced in 1939, quand

Con gress passed amendments to change

the ½nancing of the program so that work –

ers paid into Social Security incrementally

as they worked, allowing for immediate

pay ments of bene½ts without increasing

Social Security tax rates.6 Coverage was

also extended to dependents of retired

work ers or workers who died prematurely.

Dans 1948, bene½ts to dependents, survivors,

and those with severe and long-lasting dis –

ability were increased or extended and cov –

erage was expanded considerably.7 In 1950,

a revised schedule of gradual increases in

tax rates for employers and employees was

implemented to increase the likelihood

that Social Security would remain self-

supporting; coverage was also extended

to several additional major categories of

workers such as farmers and government

workers.8 Legislation in 1954 et 1956 ex –

tended coverage to 90 percent of all work –

ers, and coverage became nearly universal

in the early 1960s.9 The eligibility age for

Social Security was reduced from age 65 à

âge 62 for women in 1956 and for men in

1961, and automatic cost-of-living adjust-

ments were authorized in 1972.10 Enfin,

in direct response to gains in life expectan-

cy and improvements in health (increases

in active and disability-free–or what we

prefer to call “healthy”–life expectancy)

since the program began, amendments ap –

proved in 1983 authorized gradual increas-

es in the age of full eligibility for workers

born after 1937, with provisions fully ef –

fective for all workers born after 1959.11

These amendments gradually increased

the age of eligibility for full Social Security

bene½ts from 65 à 67 and lowered the ben –

e½ts for those who choose to begin receiv-

ing them early (entre 62 and the full re –

tirement age). There have been no lon –

gevity- or health-related adjustments to

the retirement age since 1983. It is also im –

portant to emphasize that, aujourd'hui, approx-

imately 72 percent of new bene½ciaries

draw bene½ts before the full retirement age

et 46 percent draw bene½ts at the earliest

possible age of 62.12 Despite the program’s

evolution, donc, the question remains

whether eligibility changes have kept pace

with the substantial gains in life expec –

S. Jay

Olshansky,

Dana P.

Homme d'or

& John W.

Rowe

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

d

un

e

d

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

1

4

4

2

6

8

1

8

3

0

5

8

5

d

un

e

d

_

un

_

0

0

3

3

1

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

144 (2) Spring 2015

69

Resetting

Social

Sécurité

tancy and healthy life expectancy that have

occurred since the program’s inception

et, en effet, since the last retirement-age

adjustment in 1983.

The current debate about raising the age

of ½rst eligibility above 62 and the age of

full-bene½t eligibility above 67 has been

driven by a combination of factors, inclure –

ing: ½nancial stress placed on the solvency

of the Social Security trust fund by a much

larger number of bene½ciaries than antic –

ipated (in turn caused by an unexpected

baby boom and larger-than-anticipated in –

creases in life expectancy); a substantial

proportion of bene½ciaries who elect early

bene½ts; political reluctance to increase

payroll taxes; and a growing number of

very long-living older people who depend

fully or nearly so on Social Security (called

“longevity risk”). Aujourd'hui, two-thirds of

ben e½ciaries rely on Social Security for

more than half of their total income, et

25 percent rely on it for over 90 percent of

their total income.13 The shift toward re –

tirees relying fully on the program for ½ –

nancial support was neither anticipated

nor intended at the program’s inception.

Taken together, these considerations

lead to the four central questions we ad –

dress in this essay:

1) How well did the two-year increase in

eligibility age for full retirement bene½ts

from the 1983 amendments correspond to

the proportional rise in life expectancy at

âge 65 depuis 1935 à 1983?

2) From a demographic perspective, does

the rise in life expectancy at older ages

observed since 1983 warrant a further ad –

justment to the age of eligibility for early

and full Social Security bene½ts?

3) How would subgroups of the U.S. pop –

ulation with different survival prospects

be differentially influenced by further in –

creases in the age of early and full retire-

ment ages?

4) And what would the early and full re –

tirement ages be today if they had been

indexed directly to rising life expectancy

since the program’s inception, maintaining

a constant proportion of adult life spent

working to life spent in retirement?14

Improvements in health care and increas-

es in well-being at older ages have accel-

erated in the United States since Social Se –

c urity began in 1935 with a set retirement

age of 65. À ce moment-là, the average expec –

ted remaining years of life for someone

reaching age 65–notated as e(65)–for men

and women combined in the United States

était 12.6 années, and the probability of sur-

viving to age 65 (averaged for men and

wom en) conditional on having survived to

âge 25 (referred to as “conditional sur-

vival”) était 62.4 pour cent (Tableau 1). Par 1983,

e(65) for the total population had risen to

16.6 années (meaning that each year during

this time frame, 30 days were added to the

life of a person reaching 65 years of age),

while conditional survival to age 65 rose

à 79.4 pour cent. Entre 1983 et 2009,

life expectancy past 65 rose an additional

2.3 years to 18.9, which means that the

annual increase in life expectancy accel-

erated to 31.8 extra days added to the life

of a 65-year-old per year; conditional sur-

vival to age 65 also increased to 84.8 par-

cent between 1983 et 2009.

Since many bene½ciaries now retire at

the earliest possible retirement age of 62,

it is worth noting that e(62) increased by 4.3

years between 1935 et 1983, and by 2.5

years between 1983 et 2009 (see Table 1).

This means 32 additional days of life were

added each year to those reaching age 62

depuis 1935 à 1983, et 35.2 additional days

of life were added each year for those

reach ing age 62 depuis 1983 à 2009.

Conditional survival to the full Social

Sec urity retirement age of 65 varies consid –

erably by sex and level of completed educa –

tion; trends in conditional survival be –

tween 1990 et 2008 reveal large differ enc –

es among population subgroups (Tableau 2).

70

Dédale, le Journal de l'Académie américaine des arts & les sciences

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

d

un

e

d

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

1

4

4

2

6

8

1

8

3

0

5

8

5

d

un

e

d

_

un

_

0

0

3

3

1

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Tableau 1

U.S. Life Expectancy at Age 62 [e(62)], Life Expectancy at Age 65 [e(65)], et

Conditional Survival from Age 25 to Age 65 [S(25–65)], by Sex; 1935, 1983, 2009

e(62)

e(65)

S(25–65)

M F T

1935

1983

2009

M F T M F T

13.6 15.1 14.4 11.9 13.2 12.6 59.5 67.3 63.3

16.3 20.9 18.7 14.3 18.6 16.6 74.8 85.7 80.2

19.7 22.6 21.2 17.5 19.9 18.9 81.9 88.7 85.3

S. Jay

Olshansky,

Dana P.

Homme d'or

& John W.

Rowe

M = Male; F = Female; T = Total (average). Source: U.S. Social Security Administration, Historical Life Tables

developed by the Of½ce of the Chief Actuary for use in estimates and analysis in The 2013 Annual Report of the

Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds (2014); voir

http://www.ssa.gov/oact/TR/2013/tr2013.pdf.

Tableau 2

Percent of Total U.S. Population Surviving to Age 65 Conditional on Having Survived to Age 25,

by Level of Completed Education; 1990, 2008

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

Years of Education at Age 25

<12 12 13–15 16+

1990

2008

75.7

74.4

78.3

78.7

88.1

89.2

86.0

92.1

Source: Calculations done by the MacArthur Foundation Research Network on an Aging Society.

In 1990, only 75.7 percent of 25-year-old

men and women with less than a high

school education were expected to reach

age 65. In contrast, about 87 the

most highly educated 25-year-olds in that

year survive age In

2008, least experienced a

slight reduction survival 65 (down

to 74.4 percent) while most ed -

ucated signi½cant additional

improvement (to 92.1 percent). Condition-

al increased from 1990 through

2008 as function level completed

education; biggest jump oc -

curred among those who have any college

education. Thus, 25.6 least

educated subgroup population will

not live long enough draw retirement

ben e½ts Social Security at current eli -

gibility ages. 5.9 percent

of group will die before

the early retirement age.

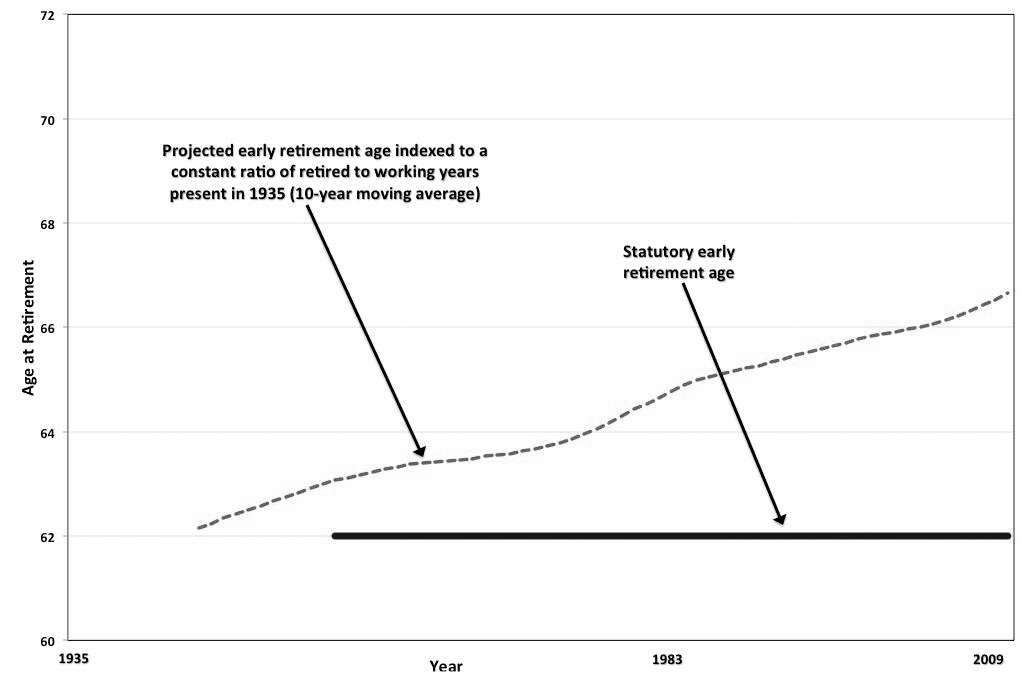

The observed full 67

mandated 1983 not be implemented

until 2027. If had

been indexed exclusively e(65) (that is, if

the was raised pro-

portion increase life expectancy

at using 10-year moving average), a

full 67.7 would been

justi½ed (see Figure 1). re -

tirement again 2009 to

life expectancy 65, tirement

age 69.4 been jus ti½ed. And

144 (2) Spring 2015

71

>