How Important Are Russia’s External

Economic Links?

Iikka Korhonen

Bank of Finland

Helsinki, Finlande

iikka.korhonen@bof.fi

Heli Simola

Bank of Finland

Helsinki, Finlande

heli.simola@bof.fi

Abstrait

In this note, we review recent data concerning Russia’s economic integration with other countries.

We first analyze the general picture of Russia’s economic integration with the rest of the world and

the importance of foreign economic relations for the country. We then turn to China, an increasingly

significant economic partner for Russia. The European Union remains Russia’s most important trad-

ing partner and is by far the most important source of foreign direct investment to Russia as well as

source of other financing. China’s importance to Russia has also increased, especially with respect to

merchandise trade.

1. Introduction

Russia-related geopolitical tensions have increased substantially over the past year.

Russia’s relations with Western countries have become strained as the risks related to the

Ukrainian conflict have intensified. Instability has also increased inside the Eurasian Eco-

nomic Union (EAEU),1 including political tensions in Belarus, unrest in Kazakhstan, et

border clashes between Armenia and Azerbaijan.

This note, premised on the notion that shocks related to foreign economic relations can

have important effects on the Russian economy, explores some of the key characteristics of

Russia’s current foreign economic relations from the viewpoint of international trade and

financial flows. The key finding is that Russia, despite its effort in recent years to reduce

dependence on global economy and increase self-sufficiency, remains highly integrated

with the rest of the world.

1 The Eurasian Economic Union consists of Armenia, Belarus, Kazakhstan, Kyrgyz Republic,

and Russia.

Asian Economic Papers 21:2

© 2022 by the Asian Economic Panel and the Massachusetts Institute of

Technologie

https://doi.org/10.1162/asep_a_00848

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

How Important Are Russia’s External Economic Links?

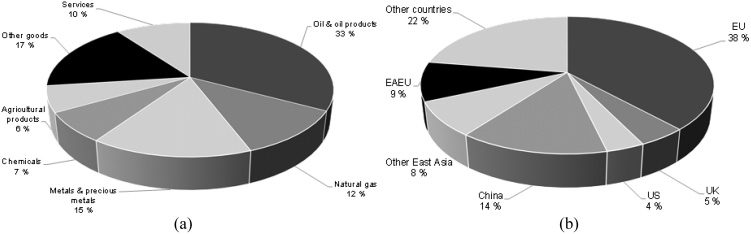

Chiffre 1. (un) Product structure (b) Geographical distribution of Russian goods exports in 2021

Source: Central Bank of Russia, Russian Customs.

The paper is organized as follows. In the Section 2, we analyze the general picture of

Russia’s foreign economic relations. In the Section 3, we take a more detailed look at the

economic relations between Russia and China. The final section concludes.

2. Russia’s foreign trade and cross-border financial flows

This section provides an overview of Russia’s economic relations in a global framework.

We examine Russia’s foreign trade in aggregate, at the sector level, and briefly at the prod-

uct level. We then discuss cross-border financial flows to and from Russia with an addi-

tional look at the banking sector.

2.1 Russia’s exports

Russia’s exports of goods and services amounted to US$ 540 milliard (à propos 35 percent of GDP) dans 2021. Crude oil, petroleum products, and natural gas accounted for nearly half of exports (Figure 1a). Other important export products were metals (including precious metals), chemicals, and agricultural products. The EU, ROYAUME-UNI, and United States together accounted for about half of Russia’s goods exports in 2021 (Figure 1a). The EU remains Russia’s main export market. The EAEU’s share was 9 pour cent. Entre 50 percent and 80 percent of value-added goes to exports in Russia’s key export sectors (Chiffre 2).2 Western countries—and the EU in particular—are important export markets for Russia’s energy mining and quarrying sector and refined petroleum products, whereas China and other East Asian countries3 are the most important export markets for non-energy mining and quarrying products. 2 Based on 2018 data, the latest data available on the OECD TiVA database. 3 For this discussion, “East Asia” is the OECD TiVA aggregate for East and Southeastern Asia, but excluding China. Ainsi, it includes Cambodia, Hong Kong, Indonésie, Japan, Korea, Malaisie, the Philippines, Singapore, Taiwan, Thaïlande, and Vietnam. 2 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e d u a s e p a r t i c e – pd / l f / / / / / 2 1 2 1 2 0 3 1 6 2 9 a s e p _ a _ 0 0 8 4 8 pd . f par invité 0 7 Septembre 2 0 2 3 How Important Are Russia’s External Economic Links? Chiffre 2. Exports as a share of value-added in Russia’s key sectors in 2018 (%) l Téléchargé à partir du site Web : / / direct . m je t . / e d u a s e p a r t i c e – pd / l f / / / / / 2 1 2 1 2 0 3 1 6 2 9 a s e p _ a _ 0 0 8 4 8 pd . f par invité 0 7 Septembre 2 0 2 3 Source: OECD Trade in Value-added (TiVA) database. Tableau 1. Geographical distribution of Russia’s top ten export items in 2019 (%) Crude oil Petroleum products Natural gas Coal Wheat Semi-finished steel products Gold Platinum Aluminum Sawn wood EU 50.3 50.3 63.9 29.0 3.2 22.4 0.0 23.7 35.1 15.3 ROYAUME-UNI 0.9 3.3 4.5 0.8 0.0 0.0 92.5 18.3 0.7 1.4 U.S. China East Asia EAEU Other countries Value (US$ bn)

1.8

6.7

0.0

0.1

0.0

3.7

0.0

27.8

7.8

0.2

27.6

5.0

1.1

13.5

0.2

0.1

0.4

0.0

1.3

55.7

9.3

6.5

7.3

29.5

3.8

1.1

0.1

28.0

17.7

8.5

5.4

1.8

7.6

1.7

2.7

3.2

4.7

0.3

4.4

1.4

4.8

26.5

15.7

25.5

90.1

69.4

2.3

2.0

33.0

17.5

122.2

66.9

51.0

16.0

6.4

6.1

5.8

5.1

4.6

4.5

Source: World Bank WITS database, UN Comtrade, Russian Customs.

Note: The largest export market for each product is shaded. The items are based on HS4-level classification.

The top ten export products, which include various energy commodities, wheat, gold,

platinum, aluminum, and wood, accounted for about 60 percent of Russia’s goods ex-

ports in 2019. The EU is Russia’s main export market for energy raw materials and alu-

minum (Tableau 1). The UK, the hub of the global gold trade, accounts for nearly all of

Russia’s gold exports. The United States is an important export market for platinum.

Over half of Russia’s wood exports go to China, which is also an important export mar-

ket for Russian crude oil. Coal and platinum are exported in large amounts to other

East Asian countries. The EAEU countries are not main markets for any of Russia’s top

ten export products. Most wheat and steel products go to countries other than those

examined here.

3

Asian Economic Papers

How Important Are Russia’s External Economic Links?

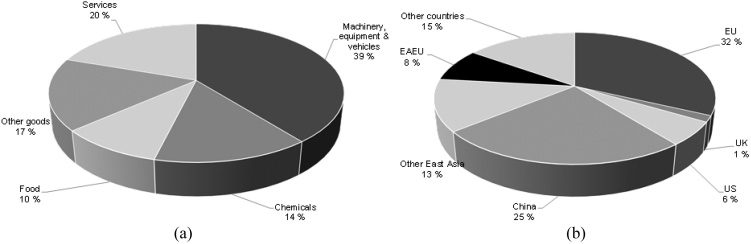

Chiffre 3. (un) Product structure of Russia’s imports in 2021 (b) Geographical distribution of

Russia’s goods imports in 2021

Source: Central Bank of Russia, Russian Customs.

Although the share of the United States is relatively small in Russian exports, 55 pour cent

of Russian exports are invoiced U.S. dollars (data from 2021:Q1–Q3). Perhaps the biggest

reason for this is that oil is typically priced in U.S. dollars. The euro accounts for 29 par-

cent of export invoicing in Russia’s total exports. The dollar and euro also dominate export

invoicing in Russia’s trade with most emerging economies, including China and Turkey.

Exports to EAEU countries are mainly invoiced in rubles (70 pour cent) and about half of

Russian exports to India are priced in rubles (India is a key export market for Russian

military technology).

2.2 Russia’s imports

Russia’s imports of goods and services amounted to US$ 380 milliard (à propos 25 percent of GDP) dans 2021. Machinery, equipment, and vehicles accounted for 40 percent of total im- ports (Figure 3a). Other key product groups in imports were chemicals and food. Services accounted for 20 percent of total imports (even despite continuing weakness in imports of tourism services). In Russia’s goods imports, the share of the EU, ROYAUME-UNI, and United States was 40 pour cent (Figure 3b). China accounted for 25 percent and EAEU member countries for 8 percent of Russian goods imports. In certain key manufacturing sectors, imports represented 55–75 percent of the value- added in the sector’s final demand in 2018. The share of imports was highest in sectors of machinery and equipment, and computers and electronics (Chiffre 4). In the food sector, the share of imports was 20 pour cent. The EU is a particularly important provider of machinery and equipment and motor vehicles, while China and other East Asian countries dominate in imports of computers and electronics. Despite the import bans Russia imposed on se- lect food categories in August 2014, the EU remains an important source of food imports 4 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e d u a s e p a r t i c e – pd / l f / / / / / 2 1 2 1 2 0 3 1 6 2 9 a s e p _ a _ 0 0 8 4 8 pd . f par invité 0 7 Septembre 2 0 2 3 How Important Are Russia’s External Economic Links? Chiffre 4. Imports as a share of value-added in Russian final demand in key manufacturing sectors in 2018 l Téléchargé à partir du site Web : / / direct . m je t . / e d u a s e p a r t i c e – pd / l f / / / / / 2 1 2 1 2 0 3 1 6 2 9 a s e p _ a _ 0 0 8 4 8 pd . f par invité 0 7 Septembre 2 0 2 3 Source: OECD TiVA. Tableau 2. Geographical distribution of Russia’s top ten import items in 2019 (%) Medicaments Telephone sets Motor vehicles; parts and accessories Motor cars and other motor vehicles Automatic data processing machines Aircraft n.e.c. Vaccines, toxins, etc.. Taps, cocks, valves, and similar appliances Bodies for motor vehicles Machinery for the treatment of materials by a process involving change of temperature Source: World Bank WITS database, UN Comtrade. UK U.S. China East Asia EAEU Other countries Value (US$ bn)

4.0

0.1

0.8

7.4

0.1

0.0

4.0

1.4

0.1

0.8

0.6

1.2

4.1

14.2

2.0

63.9

20.1

5.5

4.0

2.8

0.3

68.9

13.9

3.9

63.6

0.2

0.8

28.3

0.3

11.4

0.8

14.1

31.2

28.2

7.6

0.2

0.6

3.5

59.6

7.6

2.3

0.2

4.1

2.2

0.5

0.0

0.7

4.2

0.5

0.9

23.2

10.2

7.8

5.3

6.7

2.8

18.0

7.3

0.7

12.2

10.2

9.0

8.8

7.9

5.7

5.3

3.1

2.3

2.3

2.2

EU

68.8

5.3

37.9

38.9

19.5

32.8

55.9

49.8

34.8

64.4

Note: The largest import market for each product is shaded. The items are based on HS4-level classification.

for Russia. Belarus also is a big supplier of food imports for Russia, especially for product

groups subject to import bans for Western countries.

The top ten import products (par exemple., medical products, machinery, equipment, and mo-

tor vehicles) accounted for about one-quarter of Russia’s goods imports in 2019. The im-

ports of these top products largely come from certain regions (Tableau 2). The EU dominates

Russian imports of medical products, machinery, and motor vehicles. The United States is

the main source of imports in products related to the aircraft industry. China is by far the

largest provider of telephone sets and computers. Other East Asian countries dominate the

5

Asian Economic Papers

How Important Are Russia’s External Economic Links?

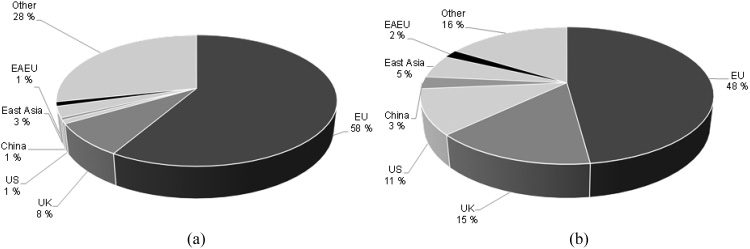

Chiffre 5. (un) Geographical distribution of the FDI stock in Russia in 1H21 (Russia’s official

statistics) (b) Geographical distribution of the FDI stock in Russia in 2020 by ultimate investor

(UNCTAD estimate)

Source: Central Bank of Russia, UNCTAD.

Note: The UNCTAD estimate excludes the investments of Russian or unspecified origin (they accounted for 40 percent of the total FDI stock

dans 2020).

imports of motor vehicle bodies. The share of the EAEU countries is small in all of Russia’s

top ten import products, ranging between 0 percent and 4 pour cent.

The U.S. dollar was used as the invoicing currency for 36 percent of Russian import trans-

actions, slightly ahead of 31 percent for the euro (as of January–September 2021). While the

dollar dominates as the invoicing currency for Russian imports from emerging economies

such as China and India, the role of the yuan in imports from China seems to be growing.

Most imports from the EU are invoiced in euros. The Russian ruble is used as the invoicing

currency for the majority of Russian imports from EAEU countries.

2.3 Foreign financial inflows to Russia

The stock of foreign direct investment (FDI) in Russia was US$ 480 milliard (30 percent of GDP) as of the end of June 2021. Official FDI statistics show that about 60 percent of that in- vestment came from EU countries (Figure 5a), particularly from Cyprus (33 percent of the total). The share of China and other East Asian countries was 3 pour cent, while the United States and the EAEU countries accounted for about 1 percent of FDI stock each. FDI statistics are, cependant, subject to large uncertainties. They depict cross-border finan- cial flows that are often channeled through three (ou plus) countries for reasons both legit- imate and illegitimate.4 It is estimated that the bulk of FDI inflows to Russia are actually of Russian origin. These are funds that are merely round-tripped via foreign countries such 4 Voir, par exemple., Damgaard et al. (2019). What Is Real and What Is Not in the Global FDI Network? IMF Working Paper No. 19/274. 6 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / direct . m je t . / e d u a s e p a r t i c e – pd / l f / / / / / 2 1 2 1 2 0 3 1 6 2 9 a s e p _ a _ 0 0 8 4 8 pd . f par invité 0 7 Septembre 2 0 2 3 How Important Are Russia’s External Economic Links? as Cyprus in the EU or tax havens like the Bahamas and Bermuda. Many large Russian corporates are registered in offshore tax havens such as Cyprus. Companies from other countries than Russia also use financial intermediaries. Estimates calculated by the United Nations Conference on Trade and Development (UNCTAD) sug- gest that the share of investment from Russia and unspecified sources (flows for which the ultimate source could not be identified) is about 40 percent of Russia’s FDI stock. The EU is the largest source of FDI, even in ultimate investor terms, but the shares of the UK and the United States are much higher than in the official statistics. It appears that about 70–75 per- cent of the FDI stock in Russia is associated with the EU, ROYAUME-UNI, or the United States, either as the ultimate investor or as an intermediate country. The roles of Asian countries and EAEU countries are apparently much smaller. As of the end of June 2021, the stock of foreign portfolio investment in Russia was US$ 180

billion.5 The Central Bank of Russia (CBR) provides no detailed statistics of the geographi-

cal distribution of foreign portfolio investment.

Russia’s stock of foreign debt was US$ 480 milliard (30 percent of GDP) at the end of 2021. The dollar’s share of foreign debt was 42 pour cent, the euro’s share 20 pour cent, and most of the remainder is ruble-denominated debt (as of the end of September 2021). At just US$ 60 milliard, the level of the Russian government’s foreign debt is relatively moderate

by international standards. The value of Russia’s ruble-denominated government debt

that is held by foreigners was about US$ 40 billion and the value of foreign-currency de- nominated government debt US$ 20 milliard. Foreign participants accounted for 20 pour cent

of the ruble-denominated government bond market and 50 percent of the government

eurobond market.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

2.4 Russian financial flows abroad

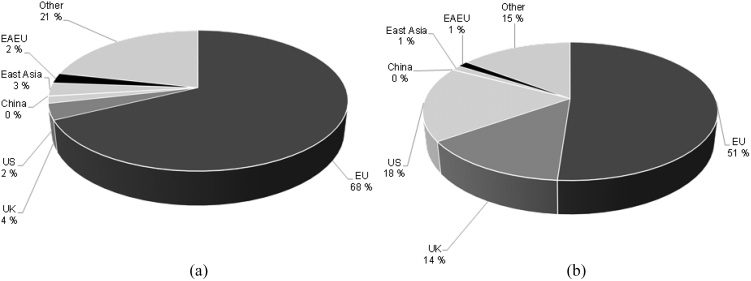

The stock of Russian direct investment abroad stood at US$ 380 milliard (25 percent of GDP) at the end of June 2021. CBR figures show the geographical distribution of Russia’s out- ward FDI is similar to that of inward FDI (Figure 6a). The EU is by far the largest destina- tion for outward Russian FDI flows, with Cyprus alone accounting for half of Russia’s total outward FDI. This reflects the above-mentioned round-tripping of Russian investment via foreign countries back to the domestic economy. Among other individual countries, Switzerland’s 6 percent share stands out. This partly reflects the fact that the Nord Stream consortium is based in Switzerland. f par invité 0 7 Septembre 2 0 2 3 5 Portfolio investment refers to securities transactions in which the ownership or voting power after the investment remains below 10 pour cent. For FDI, the ownership or voting power exceeds 10 pour cent. 7 Asian Economic Papers How Important Are Russia’s External Economic Links? Chiffre 6. Geographical distribution of (un) Russia’s outward FDI stock as of the end of June 2021 (b) Russia’s outward portfolio investment stock as of the end of June 2021 Source: Central Bank of Russia. The stock of Russia’s outward portfolio investment was US$ 120 milliard (8 percent of GDP)

as of the end of June 2021. The geographical distribution of portfolio investment is similar

to FDI distribution; the EU again accounts for the majority of investment (Figure 6b). Le

relative shares of the UK and the United States, cependant, are much larger for portfolio

investment than Russian outward FDI.

2.5 Foreign liabilities and assets of the Russian banking sector

Foreign liabilities of the Russian banking sector stood at US$ 130 billion as of the end of June 2021. The share of the EU was nearly half, followed by the United States (14 pour cent) and the UK (7 pour cent) (Chiffre 7). China’s share has increased in recent years to around 4 percent of the banking sector’s foreign liabilities. The picture is similar for the foreign assets of the Russian banking sector. The value of for- eign assets was US$ 190 billion as of the end of June 2021. The EU accounted for half of the

assets, while the combined share of the UK and the United States was about 15 pour cent. Le

share of the EAEU countries was 6 pour cent.

3. Russia’s economic relations with China

While Russia’s relations with Western countries have deteriorated since 2013, economic re-

lations between Russia and China have deepened. Nevertheless, the economic relationship

between Russia and China is asymmetric. Russia is a far less important economic partner

for China than vice versa. The sole exception is energy products. Russia is a significant—

although not dominant—source of energy imports for China. There have been several

8

Asian Economic Papers

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

How Important Are Russia’s External Economic Links?

Chiffre 7. Geographical distribution of the international assets and liabilities of the Russian bank-

ing sector as of the end of June 2021

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

Source: Central Bank of Russia.

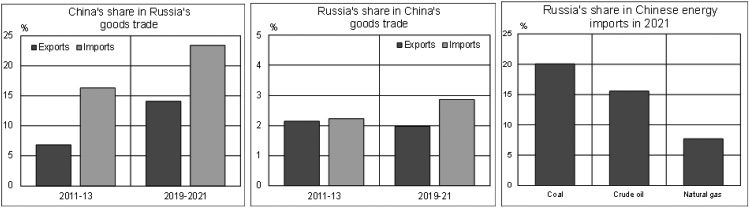

Chiffre 8. Relative shares of China and Russia in each other’s trade

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: CEIC, Russian Customs.

high-profile projects such as Power of Siberia natural gas pipeline and the Yamal liquified

natural gas (LNG) project, where Chinese funding has been crucial. En général, cependant,

the role of Chinese financing has not grown substantially in the Russian economy. Le

countries have also promoted use of their national currencies in bilateral transactions to

reduce the role of the U.S. dollar. This has succeeded to some extent, but the limited con-

vertibility of the yuan and the volatility of the ruble have hampered this trend.

3.1 Asymmetrical trade relations

China’s share in Russia’s foreign trade has increased substantially during the past decade

and it has risen as the most important single trading partner for Russia (Chiffre 8). Ce

9

Asian Economic Papers

How Important Are Russia’s External Economic Links?

mirrors the spectacular rise of China in global trade as China has become the world’s

largest goods exporting nation. Dans 2021, China accounted for 14 percent of Russian goods

exports and 24 percent of imports. In contrast, Russia is not among China’s top trad-

ing partners and Russia’s share in Chinese trade has practically not changed during

the past decade. In Chinese goods exports, it has been about 2 percent and in imports

à propos 3 pour cent.

China imports mainly energy products from Russia. In these products Russia is a more im-

portant source of imports than in the overall trade. Russia’s importance has grown in past

years with the increasing transport infrastructure capacity for oil and natural gas between

the countries and the growing LNG production in Russia (as LNG can be transported more

flexibly to various markets). Transport infrastructure projects include the extension of the

oil pipeline from Russia to China, the construction of the Power of Siberia gas pipeline,

and the Yamal LNG project. Chinese financing has provided important support for

these projects.

About 15 percent of Chinese crude oil imports and 8 percent of natural gas imports came

from Russia in 2021. Russia accounted for about 20 percent of Chinese coal imports.

Russia’s share in Chinese natural gas imports can increase when the Power of Siberia

pipeline will reach full capacity, and possibly further if other planned natural gas projects

are realized.

The Power of Siberia gas pipeline is currently slated to reach its full capacity of

38 billion m3 per year in 2024. Gazprom also recently announced an agreement to sup-

ply an additional 10 billion m3 gas per year to China. This arrangement, cependant, requires

additional investments, so it is unclear when these shipments might start. Another gas

pipeline (planned capacity 50 billion m3) running from Russia to China via Mongolia has

been discussed, but so far no official agreement has been reached on its construction. In any

case, China has been quite careful in balancing and diversifying its oil and gas supply to

avoid over-reliance on any single supplier.

3.2 Only modest increase in China’s importance in Russian finance since 2013

Russia initially hoped to offset its loss of access to foreign financial markets from the 2014

Western sanctions with Chinese financing. Although subject to several uncertainties, le

available data suggest this aspiration has been only modestly realized. Chinese state-

related financial organizations have provided financing to projects considered beneficial

to China’s general interest. such as construction of the Power of Siberia pipeline and the

Yamal LNG project. Some other Russian entities have also received Chinese financing, mais

China’s role in financing Russia remains modest at the aggregate level.

Russia’s official FDI statistics imply that the stock of Chinese FDI (including Hong Kong)

in Russia has been nearly unchanged in recent years, accounting for only about 1 pour cent

10

Asian Economic Papers

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

How Important Are Russia’s External Economic Links?

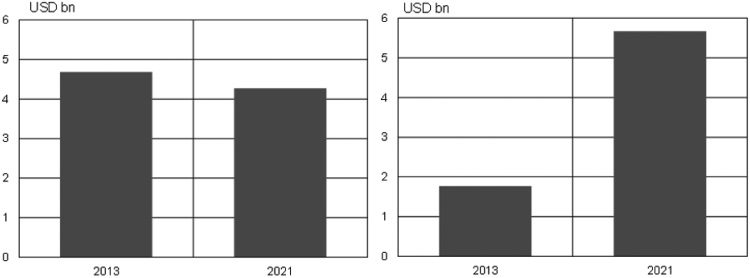

Chiffre 9. (un) Chinese FDI stock in Russia (including Hong Kong, end of 2013, mid-2021) (b) Liabili-

ties of Russian banking sector in China (including Hong Kong, end of 2013, mid-2021)

Source: Central Bank of Russia.

of FDI in Russia (Chiffre 9). The value of the China’s FDI stock in Russia at the end of 2013

amounted to US$ 4.7 milliard. It was almost unchanged at US$ 4.3 billion as of end June

2021. Using the alternative FDI statistics compiled by UNCTAD, the share of China in

Russian FDI stock looks to have been in the range of 2–3 percent in 2020.

While China’s importance to the Russian banking sector has increased somewhat, it is

still quite limited. At end 2013, the amount of the liabilities of the Russian banking sector

to China (including Hong Kong) was only US$ 1.8 milliard. By mid-2021, it had tripled to US$ 5.7 milliard, and accounted for about 4 percent of the foreign liabilities of the Russian

banking sector.

Alternative data sources focusing on the Chinese perspective also point to similar trends

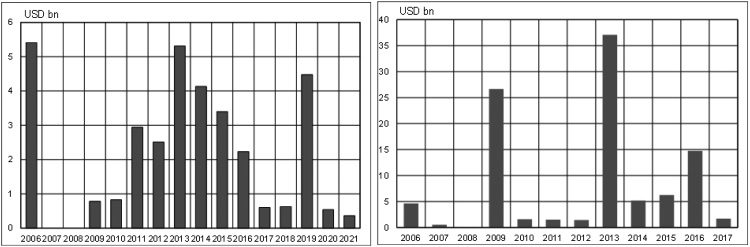

in Chinese financing to Russia. The 2006–21 data from China Global Investment Tracker

monitors significant Chinese investment abroad. The data suggest that there has been

no systematic increase in Chinese investment in Russia (Chiffre 10). During 2006–13, le

total value of investment flows was US$ 17.8 milliard. For 2014–21, it declined slightly to US$ 16.4 billon.

AidData, which provides estimates on Chinese government-related development project

financing abroad, suggests that the amount of finance flows from China to Russia began to

decrease after 2013 (data on project values are not available for all projects). The apparent

changement, cependant, largely reflects the massive loan provided by China National Petroleum

Company to Rosneft in 2013. In 2010–13, the total value of project financing was US$ 41.6 milliard. In 2014–17, it decreased to US$ 28 milliard.

11

Asian Economic Papers

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

How Important Are Russia’s External Economic Links?

Chiffre 10. Estimates of (un) Chinese investment inflows to Russia (2006–21) et (b) Chinese state-

associated development financing to Russia (2006–17)

Source: China Global Investment Tracker, AidData.

3.3 Use of national currencies in bilateral trade has increased

Russia and China are both promoting increased use of their own currencies in international

transactions and reducing dependency on the U.S. dollar. This shift is reflected in bilat-

eral trade, Russia’s foreign exchange reserves, and China’s state-led financing of Russian

projects. In Russian exports to China, the share of ruble and other currencies (apparently

yuan) as the invoicing currency has increased from 3 percent to 15 percent in 2013–21. Le

euro has also strongly replaced the U.S. dollar. In Russian imports from China, the share

of ruble and apparently yuan as the invoicing currency has increased from 6 percent to

31 percent in 2013–21. The use of yuan seems to have increased substantially in imports,

while the share of ruble has stayed stable. The share of euro has increased also in Russian

imports from China but is still only about 10 pour cent. In Russia’s foreign exchange reserves

the share of yuan has increased from practically zero to 13 percent by mid 2021.

According to AidData, the development financing from Chinese state-associated entities

to Russia is also shifting to yuan. During 2010–13, just one relatively small project was fi-

nanced in yuan—all the others were financed in dollars. During 2014–17, financing for

several projects was disbursed in yuan, accounting for 20 percent of total financing (pour

projects where their value has been reported).

4. Concluding remarks

Despite its aspirations for greater economic self-sufficiency in recent years, Russia still has

substantial economic connections to the global economy through international trade and fi-

nancial markets. In trade, Western countries are still Russia’s most important partners. Le

EU is the main export market for Russian oil and gas, and the key provider of Russia’s im-

ports of medical products, machinery, and motor vehicles. The shares of China and other

12

Asian Economic Papers

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

How Important Are Russia’s External Economic Links?

Asian countries have increased substantially in Russian trade. As for many other countries,

China already accounts for the vast majority of Russian imports of electric equipment and

electronics. In financial markets, Western countries continue to dominate Russia’s interna-

tional connections. EAEU members figure much less in Russia’s trade and financial flows,

but there are exceptions. Par exemple, Belarus is an important supplier of food imports

to Russia.

As China’s role in the global economy continues to increase, we expect that its importance

for the Russian economy will also grow. In contrast, China’s importance to Russian financ-

ing has remained relatively modest, partly owing to China’s own capital controls.

je

D

o

w

n

o

un

d

e

d

F

r

o

m

h

t

t

p

:

/

/

d

je

r

e

c

t

.

m

je

t

.

/

e

d

toi

un

s

e

p

un

r

t

je

c

e

–

p

d

/

je

F

/

/

/

/

/

2

1

2

1

2

0

3

1

6

2

9

un

s

e

p

_

un

_

0

0

8

4

8

p

d

.

F

b

oui

g

toi

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

13

Asian Economic Papers