Guy Stuart

Regulatory Innovation in Microfinance

The MACS Act in Andhra Pradesh

If the past is any guide, continued progress in addressing public chal-

lenges will require continued innovations—the efforts of individuals,

groupes, and communities who creatively employ new organizational

forms, and in many cases new technology, to effect discontinuous

changement.

—Philip Auerswald and Iqbal Quadir

from “Introduction to the Inaugural Issue,” Innovations Winter 2006

What has been is what will be, and what has been done is what will be

fait; and there is nothing new under the sun. Is there a thing of which

it is said, “See, this is new”? It has been already, in the ages before us.

—Ecclesiastes, 1.9 et 1.10

This paper is about an institutional innovation in microfinance. The innovation is

a law regulating cooperatives under which savings and credit cooperatives provid-

ing microfinance services can operate—the Mutually Aided Cooperatives Societies

Acte (MACS Act). The law was enacted in the state of Andhra Pradesh in India in

1995, and has since been replicated, with adaptations, in eight other Indian states.1

The focus of this paper will be on the Act in Andhra Pradesh, and its implementa-

tion there.

This innovation is different from many others that one sees in microfinance

because it is not directly concerned with innovations in techniques for delivering

microfinance services, but rather with providing an innovative enabling environ-

Guy Stuart is an Associate Professor of Public Policy. He received his PhD from the

University of Chicago in 1994 and then worked for four years in Chicago in the field

of community economic development. During this time he served as the Director of the

FaithCorp Fund, a nonprofit community loan fund. At the Kennedy School he teach-

es courses on management and community financial institutions, which cover such

topics as microfinance and credit unions. He is currently conducting research on racial

and economic segregation in the United States and on microfinance and thrift coop-

eratives in India and Latin America.

© 2007 Guy Stuart

nouveautés / winter & printemps 2007

181

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

ment in which cooperatives can provide such services. Nevertheless, it relates indi-

rectly to innovations in techniques because a touchstone of the law is that is pro-

vides a liberal regulatory framework in which cooperatives are able to experiment

with different organizational structures and techniques for delivering services.

There is an irony in calling the MACS Act an innovation. It is more an enact-

ment of time-worn and time-tested cooperative principles that cooperatives

around the world, especially in Europe and North America, have been operating

under for over 100 années. But in the context of India at the end of the 20th Century,

the act is an innovation, because it is a radical departure from the top-down, sta-

tist management of cooperatives that has plagued Indian cooperatives since the

British first enacted the Credit Cooperatives Societies Act of 1904. This and subse-

quent acts, as will be documented in more detail below, espoused the fundamen-

tal principles of cooperatives related to self-help and mutual aid, but instituted a

system of regulation in which members’ rights, responsibilities, and risks were

emasculated by the control exerted over the cooperatives by the state registrar of

cooperatives. Par conséquent, members had very little interest in ensuring the effective

functioning of the cooperative, and the ability of the cooperative to deliver goods

and services to its members was wholly contingent on the willingness and ability

of the registrar and his designees to deliver such goods and services.

The argument of this paper is that the MACS Act is an innovation because it

radically alters the rights, responsibilities, and risks of cooperative members.

Spécifiquement, it has given the members of the cooperative the rights and responsi-

bilities to manage their own cooperatives to improve their own lives, and has

diminished the powers of the state registrar to the point where his office is largely

a depository of information about the cooperatives operating under the act, avec

some powers of inquiry. In taking on these rights and responsibilities the members

are exposed to new risks that are not small. The paper also argues that though the

innovation is a regulatory and institutional one—it changes the “rules of the

game”— it is not sufficient for its success to simply put it in place and “let the chips

fall as they may.” The MACS Act requires organizational capacity to succeed.

Members of the cooperatives can supply some of that capacity, but civil society

more generally has a role. And it remains an open question whether the innova-

tion will survive its own initial success because there remain serious organization-

al capacity issues. Enfin, building on these first two points, the paper makes clear

that the innovation is not an uncontroversial one both within the arenas of state

and national politics, d'un côté, and among microfinance practitioners on

the other. Despite this controversy, I argue that the innovation is consistent with

other innovations in microfinance and that it would be foolish, at this point in its

histoire, to undermine it.

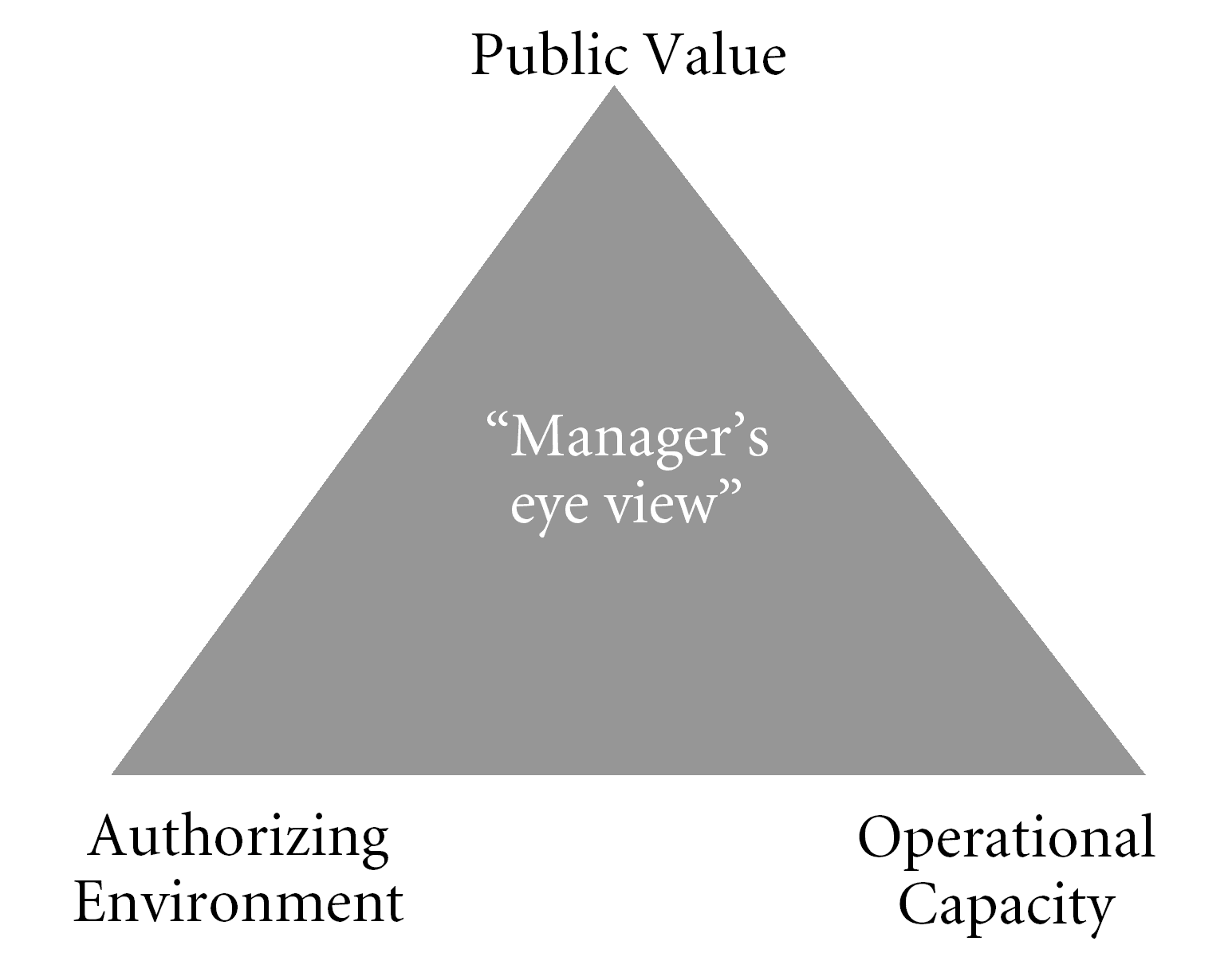

Implicit in the construction of these three points is an analytic framework that

I will make explicit in the next section of this paper, as a way to orient the reader.

The framework is that of public value, which provides the analyst of public policy

questions with a way to understand the major concerns facing a practitioner in

dealing with those questions on a day to day basis. The framework highlights the

182

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

need to pay attention to the value proposition ineherent in the policy, the source

of the authority for the policy and for the activities required to implement it, et

the operational capacity to implement the policy.2 Having explained this frame-

travail, the paper will describe the MACS Act and show how it is an innovation in

comparison to other cooperative laws. It will then describe the organizational

capacity that a particular NGO, the Cooperative Development Foundation, a

brought to bear in promoting and supporting thrift cooperatives in three districts

in Andhra Pradesh, and raise questions about the support that a large number of

other thrift cooperatives registered under the MACS Act are or are not receiving.

The paper will then discuss the current political and policy debate regarding the

regulation of MFIs in India, and its relevance to the MACS Act. It will conclude by

summarizing the arguments and the implications for the future of this regulatory

innovation.

INNOVATION AND PUBLIC VALUE

One way to think about public policy is to look at it from the perspective of a sen-

ior manager, or an executive director of an NGO. Such a manager in a public sec-

tor or non-profit environment is in the business of producing public value using

the operational capacity that is available to her and the authority vested in her by

her authorizing environment.3 Public value is very simply what people value, comme

recipients of specific services and citizens. Operational capacity is the capacity to

deliver something of value to the citizenry, whether they are direct clients of the

organization delivering services, or citizens who have voted for and support the

nouveautés / winter & printemps 2007

183

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

delivery of a set of services or the enforcement of a set of regulations. The author-

izing environment is the set of actors, decisions, and existing institutions that pro-

vide legitimacy and support to the manager engaged in the creation of public

valeur. To succeed the manager must ensure the continued support of the author-

izing environment.4

Microfinance has made its mark within the field of international economic

development because of its innovations in defining new types of public value, et

in developing new methodologies (operational capacities) for delivering that

valeur. Microfinance began life as micro-credit. In that guise, it proposed and test-

ed the idea that the poor need loans, they are able to translate that need into effec-

tive demand for loans, and they are capable of repaying those loans with interest.

This ran contrary to the views or experience of mainstream banks and govern-

ment-run credit programs, respectivement, who either saw no market for loans among

the poor (banks) or saw a wide variety of credit programs go wildly awry as poor

farmers failed to repay loans (government programs). Microcredit proved that the

poor can and will borrow money and repay it. Ce faisant, microfinance institu-

tion (MFIs) developed a set of innovative practices that cost-effectively managed

the risk of lending to the poor without collateral and without formal documenta-

tion of their income and character. The most famous, and ubiquitous, of these is

the peer lending methodology, in which loans are made to individuals within

groupes, or the groups themselves, while holding each group accountable for the

repayment of the loans made to them or their members. Because prospective

clients of MFIs form the groups themselves, based on their mutual knowledge of

each other and their willingness to trust each other, MFIs have, in essence, subcon-

tracted out their risk management operations to the social structure of the market

in which they are operating. Another common innovation that MFIs have used is

the step-lending methodology, and the use of information systems that track the

repayment behavior of the borrowers very accurately to enable follow-up on those

clients who are even one day late on their payments.

In defining these new value propositions and developing these new opera-

tional capacities many MFIs did not find the need to innovate ways of managing

their authorizing environments, though they still had to manage that environ-

ment. Many flew and still fly “under the radar”—working at the grassroots beyond

the supervisory eye of government regulators. Others found ad hoc solutions. Le

most famous MFI, the Grameen Bank, managed its authorizing environment

through the personal relations its founder, Muhammad Yunus, had with

Bangladesh’s ruling elite. Such was his connectedness that since 1983 the Grameen

Bank has been operating under its own law.5 And still others transformed them-

selves into fully licensed and regulated banks, operating under their countries’ gen-

eral banking laws (for example Bancosol in Bolivia, and K-Rep in Kenya).

The strategy of “flying under the radar” worked well for many MFIs while they

engaged in the extension of micro-credit only. Government regulators had little

interest in regulating their activities. But MFIs have grown to a sufficient size and

importance in many local economies that this strategy has run its course, et, as a

184

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

result, government regulators have shown an increasing interest in their activities.

En outre, since the 1990s many MFIs have developed a new value proposition

and new capacities for creating that value. The new proposition is that the poor

can and do save, and that MFIs can mobilize funds from the poor to lend to the

poor, and do away with the need for external financing. Concomitant with this

value innovation, the MFIs have developed their operational capacity to manage

the receipt of large numbers of small amounts of cash, something in which they

already had some proficiency due to their micro-credit activities. But unlike with

the micro-credit innovations, MFIs can not so easily “fly under the radar” with

their micro-savings innovations—there are existing regulations in most countries

that restrict the ability of organizations to mobilize savings from the public. As a

result, MFIs have shown an interest in new regulations that allow them to mobilize

savings without having to comply with all the current regulations that apply to

mainstream banks.

The benefit of looking at innovation in any policy field through the public

value framework is that it forces one to acknowledge three central aspects of pub-

lic policy: its purpose, the source of its legitimacy, and the capacity required to

implement it. It allows one to identify the locus of the innovation and then deter-

mine its implications for the other parts of the strategic triangle. In the case of

microfinance, what we have is a situation in which the authorizing environment is

catching up with innovations in the value proposition and the operational capac-

ities of MFIs. In contrast, the MACS Act is an innovation in the authorizing envi-

ronment that has as I will argue below, with some exceptions, required the coop-

eratives and the NGOs supporting them to build the organizational capacity to

perform successfully under the new regulatory framework. The value proposition

inherent in the MACS Act is not new—the idea of self-help and mutual aid, surtout-

cially through financial cooperatives, has been around for a long time.

BRIEF HISTORY OF COOPERATIVES IN INDIA

The first effort to create formal, legally recognized credit cooperatives in India was

le 1904 Credit Cooperative Societies Act passed under British rule. According to

Moore:

Under the provision of this Act, local governments were authorized to

appoint registrars with full powers to organize, register and supervise co-

operative credit societies, with the object of encouraging thrift, self-help

and cooperation among agriculturalists, artisans and persons of limited

means.6

Ilbert reports that the act was “designedly very general and elastic.”7 He contin-

ues, “[m]uch is left to rules and by-laws, and a very free hand is given to the regis-

trar, on whose personality much will depend,” giving an early indication of the reg-

istrar-centric nature of cooperative laws in India.8

Le 1904 act was superseded by the 1912 Cooperative Societies Act, lequel

nouveautés / winter & printemps 2007

185

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

extended the law to cooperatives in general, not just credit cooperatives. The act

was limited in its requirements, but it conferred on states extensive powers to make

rules regulating the activities of cooperatives under their jurisdiction, et le 1919

Government of India Act devolved all regulation of cooperatives to the states. Dans

the following years the various states in British India passed their own cooperative

laws, which imposed extensive regulation of the cooperatives, and vested powers in

the registrar. Throughout the early part of the 20th century there was a dramatic

increase in the number of cooperatives in British India and nine Indian states.9

From an average of just under 2,000 dans le 1906 à 1910 period to an average of

just under 94,000 dans le 1925 à 1930 period.10 Focusing on the post-1912 period

Qureshi notes:

During this period more stress was laid on quantity than on quality, et

the main criterion of promotion for the staff was the opening of more

societies…The result was that the movement developed without the peo-

ple realizing and feeling the need for the quality of the movement. Owing

to the great enthusiasm of the employees of the co-operative department

in persuading people to open societies, the movement indeed began to be

regarded as a Government responsibility….The most distinctive feature,

at least in theory, of co-operative credit is that it should be a controlled

credit and be of local origin. That is why the official title of co-operatives

societies is Credit and Thrift societies… In practice the thrift part of the

movement was neglected and all the members were borrowing members.

As no control over borrowings could be exercised in a group which was

overwhelmingly dominated by borrowers, the result was serious.11

Par 1936-7 the share of outstanding loan balances that were past due in British

India ranged from 40.8% in the Punjab to 92.5% in Bihar.12 Turnell also notes that

the Burmese cooperative system (also under British rule), after rapid growth in the

1910s and early 1920s began a collapse in the late 1920s that was completed by the

Great Depression.13

Qureshi summing up his argument on the wisdom of promoting cooperatives

in India on the eve of independence noted four reasons why he felt it was a bad

idea. D'abord, he argued that cooperatives were not suitable to “backward countries;»

second, that there was undue emphasis on credit in the way Indian cooperatives

were run; et, troisième, especially credit from external sources. En outre, he con-

cluded:

Fourthly, and this we regard as the most important, the movement was

entrusted to a type of civil servant who in spite of his proved ability and

character in other fields of administration, was most unsuitable by tem-

perament, environment and training to undertake an expert job of this

type… If one reads a co-operative Act one finds that, as to God Almighty,

all functions, responsibilities, directions guidance and control have been

entrusted to the Registrar of Co-operative Societies…14

186

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

In sum, the experience of cooperatives under British rule was one of consistent

failure. The cooperatives were promoted by zealous administrators who saw cred-

it cooperatives as the solution to the problem of rural credit. Those same cooper-

atives became conduits for external credit, and the result was organizations which

were cooperatives in name only and were burdened with overdue loans.

In the period after independence, 1950 à 1990, the lives of cooperatives

became even more complicated by state government interference:

State policy came to be premised on the view that the government should

ensure adequate supply of cheap institutional credit to rural areas

through cooperatives… As the financial involvement of the government

in cooperatives increased, its interference in all aspects of the functioning

of cooperatives also increased. The consequent interference with the

functioning of the co-operative institutions, often compelling them to

compromise on the usual norms for credit worthiness, ultimately began

to affect the quality of the portfolio of the cooperatives… Instead of tack-

ling the root cause of their weaknesses, the State took responsibility for

strengthening the institutions, by infusing additional capital and “profes-

sional” workforce. Both the State and the workforce then began to behave

like “patrons”, rather than as providers of financial services.15

It was during this phase that the state of Andhra Pradesh passed the

Cooperative Societies Act of 1964, which is still in force today. This act, like its

predecessor (le 1932 Madras Act), gave extensive powers to the registrar. In addi-

tion, as noted above, cooperatives remained the instruments of state policy, avec

little or no autonomy. Thus by the 1990s financial cooperatives were in a situation

in which their governance was subject to the whims of the registrar, they had

become the conduit of both state and national policies to push cheap credit into

the agricultural sector of the economy, et, as a result, they were rife with overdue

loans and corruption.

THE MACS ACT—A REGULATORY INNOVATION

The MACS Act is a reaction to this history. Its main advocate is the Cooperative

Development Foundation (CDF), an NGO headquartered in Warangal in Andhra

Pradesh, which also promotes and supports cooperatives. The CDF and its allies

were trying to solve a particular problem with the Act—the failure of cooperatives

in the state to serve their members effectively due to interference from the state.

The guiding principles behind the act were those of the International Cooperative

Alliance, an organization of cooperatives whose history dates back to the mid-19th

century and the northern England town of Rochdale.16 The result is an act that

alters the balance of power between the membership of the cooperatives and the

registrar, et, in doing so, also alters the respective responsibility for the effective

functioning of the cooperative. En outre, by prohibiting the government from

owning any share capital in the cooperatives, the act protects the cooperatives from

nouveautés / winter & printemps 2007

187

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

direct government influence through their financial stake.

There are three broad themes running through the MACS Act that make it dis-

tinctive from other efforts at regulating cooperatives: the autonomy of the cooper-

atives in how they govern themselves; the responsibilities and risks the members

take on when they join a cooperative; and the restrictions on the powers of the

Registrar and the government. The act requires a cooperative to develop a set of

by-laws that cover a long list of governance issues—section 9 of the act, lequel

specifies the by-laws that must be in place, lists 39 in total. A cooperative wishing

to register under the act must have by-laws covering each of these issues. But the

act does not specify the exact nature of the by-laws. The intent here is to ensure

that each cooperative have its own rules covering important issues in the gover-

nance and operations of the cooperative, but not to specify what those rules should

être.

The intent here is to ensure

that each cooperative have its

own rules covering important

issues in the governance and

operations of the cooperative,

but not to specify what those

rules should be.

This does not mean that

the act frees members to

make up all their own rules.

The act specifies the powers

of the general body of the

cooperative and its board of

directors. It also specifies the

timing of elections, the finan-

cial information each coop-

erative must keep, audit

requirements, and proce-

dures for amending the by-

laws. Ce faisant, the act pro-

vides some minimal gover-

nance infrastructure within

which the members of the cooperative have a say in the running of the organiza-

tion, through the membership in the general body, the election of the board of

directors, control over the amendment of the by-laws, and access to basic financial

information (assuming they are literate).

The central role of the by-laws in the governance of the cooperatives and the

minimal governance infrastructure uphold the sovereignty of the membership of

the cooperatives. Ce faisant, the act also requires that same membership to take

responsibility for the running of the cooperative, and exposes them to a number

of risks that come with that responsibility. Only members can contribute share

capital to the cooperative. Cooperatives are prohibited from accepting share capi-

tal from the government, though they are allowed to receive government loans and

guarantees, and the same from other non-members. Par conséquent, only the members

are the owners of the cooperative, and it is their capital that is most at risk. The act

also requires that members cover any deficit incurred in the operations of the

cooperative annually, through the use of reserve funds or by debiting the accounts

of members “in proportion to the services they had availed or were expected to

188

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

avail of the cooperative society during the year.”17 It allows the cooperative society

to invest its funds in any “non-speculative” investment, including its own business

ventures. The act specifies that the board of directors is responsible for the hiring,

monitoring, and firing of all staff, and that the membership take responsibility for

setting rules and procedures for settling disputes. Only once all internal remedies

have been exhausted can a dispute be referred to an external tribunal. Enfin,

cooperatives registered under the act are not protected from competition from

other cooperatives, whether new or old—the act does not provide cooperatives

with “jurisdictions” in which they have a monopoly and the Registrar has no pow-

ers to prevent another cooperative from providing the same services in the same

geographical area.

The strengthening of the rights and responsibilities of the membership and the

central role the by-laws play in the governance of the cooperatives have combined

to diminish the ability of the Registrar to control the cooperatives. En outre,

even in cases where the act specifies a role for the Registrar in the governance of

the cooperatives, the act ensures that the Registrar is not the sole arbiter of the

case—he cannot act as prosecutor, judge, and jury. The Registrar has the responsi-

bility to ensure that the cooperatives’ by-laws conform to the act, and that the

membership and board comply with the minimal governance rules specified in the

act.18 The Registrar is also an information depository. Every year, 30 days after the

annual general meeting, cooperatives must file certain reports with the Registrar.

But this is not for supervisory purposes; rather it is to ensure that there is one,

authentic copy of the reports held with a third party in case of any disputes with-

in the cooperatives about such reports. The Registrar does have powers to hold

inquiries into the operations of cooperatives, to conduct a special audit, and to

appoint a liquidator of a cooperative that is no longer viable. But in most cases,

these activities must be at the request of members of the cooperative itself or a

third party who has a clear interest in the operations of the cooperative in ques-

tion; and they must be carried out within a specified time period.19 Furthermore,

in many instances the Registrar must leave the disposition of the case to a tribunal.

Le 1995 act follows the 1964 act in specifying how to constitute tribunals. Enfin,

the act provides no rule-making power to the Registrar or the state government

overall—the act specifies all the rules necessary to implement the act, only the leg-

islature can change the way the act is implemented.

The MACS Act provides a regulatory umbrella under which savings and cred-

it cooperatives can operate. Sections 14.1 et 14.2 allow a cooperative society to

“mobilize funds in the shape of… deposits, debentures, loans and other contribu-

tions” from both members and non-members.20 As a result, a cooperative regis-

tered under the act can mobilize savings. En outre, the act places no restriction

on the services a cooperative can provide its members, hence it is permissible for

it to provide financial services, such as loans and insurance, so long as such provi-

sion is not in violation of other laws. Mais, as noted above, the MACS act limits the

extent to which the Registrar exercises supervisory control over the cooperatives.

Par conséquent, despite the fact that they mobilize savings, the financial cooperatives

nouveautés / winter & printemps 2007

189

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

registered under the act are not subject to any prudential regulations. The reason-

ing here is that because the cooperatives are restricted to providing services to their

members, and members have their share capital and deposits at risk, the general

governance framework required by the act, including the by-laws of the coopera-

tives, will ensure the cooperative operates in a prudent manner. The act requires

that members and their boards of directors take responsibility for the effective

functioning of a financial cooperative in the same way as they do for any other

cooperative.

There is an anomaly in the logic of Section 14: it allows cooperatives to mobi-

lize deposits from non-member individuals. This is inconsistent with the idea of

mutual responsibility—only members should have their deposits at risk, because

only members have the authority to supervise the organization. This clause does

not appear in the model act that CDF has promoted in other states, and does not

appear in those states’ Acts. It seems to be a product of a political compromise in

Andhra Pradesh.

There are also exceptions to the absence of prudential regulations. Ceux-ci sont

cooperative banks, which engage in “banking” as defined by the 1949 Banking

Regulation Act (Section 36-A). According to Section 5.1.b of the 1949 Banking

Regulation Act (referenced in Section 36-A of the MACS Act), “banking” means

the accepting, for the purpose of lending or investment, of deposits of money from

the public, repayable on demand or otherwise, and withdrawable by cheque, brouillon,

order or otherwise.” A cooperative that engages in banking is subject to Reserve

Bank of India prudential regulations.21

The lack of prudential regulation of financial cooperatives operating under the

MACS act is the subject of much political debate currently. I will discuss the argu-

ments for and against such regulation below when I describe the current debate

about the 2007 Microfinance Bill currently before the national legislature.

IMPLEMENTATION OF THE MACS ACT AND MICROFINANCE

As of January 31, 2006 there were 18,398 cooperatives registered under the

MACS act, of which 7,589 were financial cooperatives. There has been a very rapid

growth in the number of financial cooperatives registered under the MACS act

over the past few years due to the large number of self-help groups (SHGs), pro-

moted by the state government and NABARD, that have formed federations and

registered under the act. This section focuses on the implementation of the act

from the perspective of the thrift cooperatives promoted by the CDF, suivi de

a discussion of the SHG phenomenon. The argument of this section is that the

activities of the CDF demonstrate the need for active support for the cooperatives

as they develop their governance and information systems and their service

méthodologies. But those activities also demonstrate that this support has to be of

a particular type—it has to enable the cooperatives to function without undermin-

ing their autonomy. I then raise the question as to whether SHG federations are

190

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

receiving the same type of support, and what the risks are if they are not receiving

it.

CDF, Thrift Cooperatives, and the MACS Act

Upon passage of the MACS act in 1995 the CDF immediately started encouraging

the thrift cooperatives it had promoted up until then to register under the Act. Comme

of the end of 2005, 286 cooperatives were registered, 153 women’s thrift coopera-

tives (WTCs) et 133 men’s thrift cooperatives (MTCs). These were not all the

WTCs and MTCs in operation at that time: there were 269 WTCs with a member-

ship of 79,238, et 176 MTCs with a membership of 43,677 (CDF 2005, 2). During

2005 deux (2) WTCs and nine (9) MTCs were dissolved. The total funds in the

WTCs were almost Rs.176 million, of which Rs.152 million were out on loan to

members of the WTCs; the total funds in the MTCs were Rs.198 million, of which

Rs.169 million were out on loan. According to the CDF all cooperatives held their

annual meetings for 2005 by March 31, 2006, as stipulated in their by-laws: partic-

ipation rates in the cooperatives’ annual meetings were just under 50%, while par-

ticipation rates for the associations’ AGMs were about 75%.22 Enfin, the CDF

reports that only 37 cooperatives, out of a total of 445, held elections using secret

ballots to choose their board members; and only 45 cooperatives elected their pres-

idents through a secret ballot of their boards of directors. The amount of loans in

default at the end of 2005 was Rs.1.3 million in the WTCs and Rs.1.6 million in the

MTCs. The average outstanding loan balances were Rs.138 million and Rs.154 mil-

lion respectively, giving a default rate of about 1% in each case. The borrower

default rate was higher: à propos 8% in the case of the WTCs and just over 10% dans le

case of the MTCs.23 The default rate in terms of rupees is lower than in terms of

defaulters because defaulters may well have paid off some of their loans before they

went into default, and their thrift and other deposits served as collateral for part of

the loan.

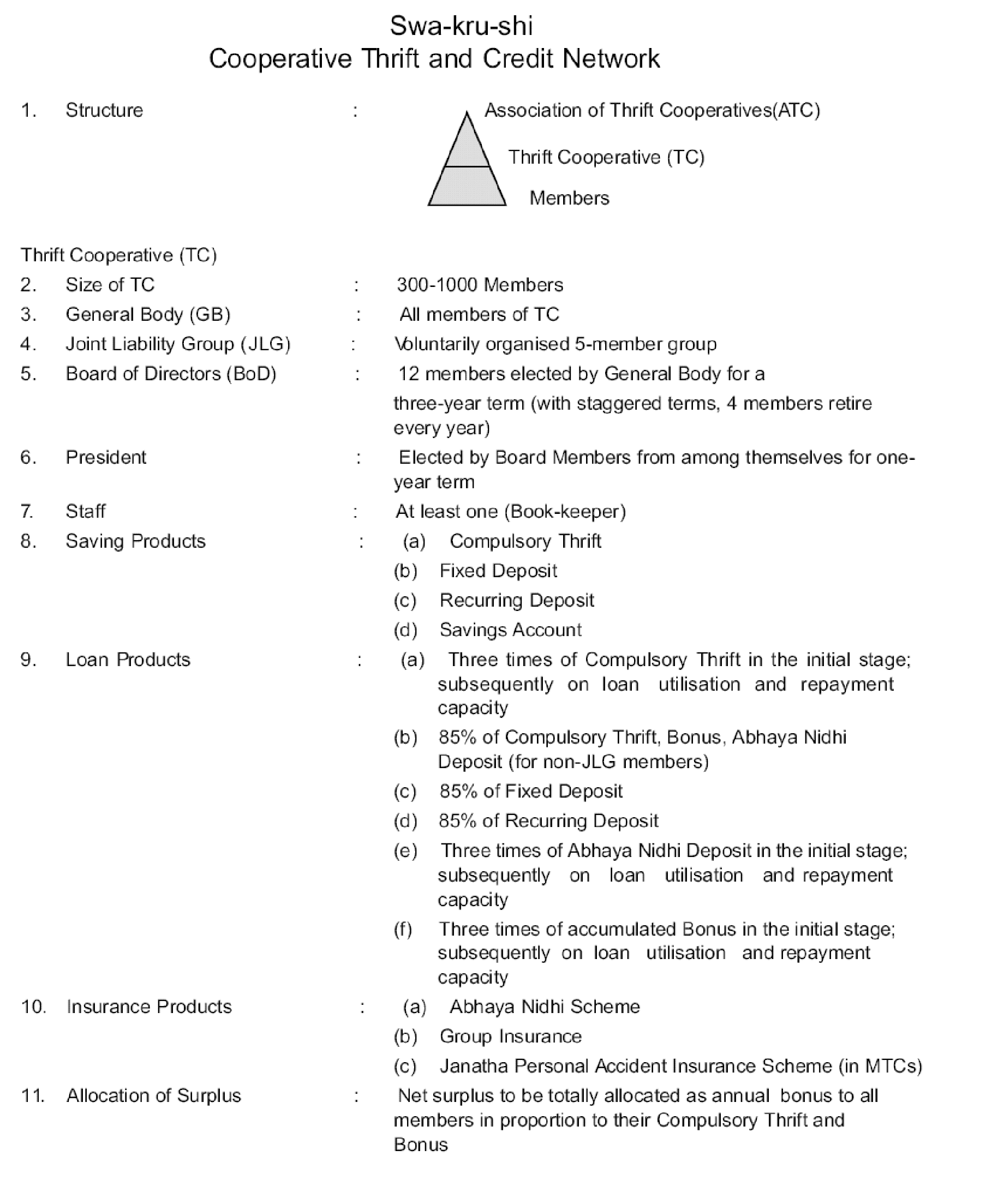

The individual, village-based cooperatives are organized into associations,

which are, à son tour, constituents of a confederation of associations. Chiffre 2

describes the structure of the cooperatives, associations, and confederation.

The cooperatives and associations are free to adopt their own by-laws and run

their operations as they see fit. Nevertheless, as Figure 2 implique, there is uni-

formity across all the cooperatives in their basic governance practices and in

the services they offer to their members. This is because of the role the con-

federation plays in setting policy for all the constituent entities. It is at this

level that the CDF provides the cooperatives with technical advice and assis-

tance. The CDF also provides auditing services to individual cooperatives and

associations, and has field workers actively monitoring the cooperatives and

associations.

These data raise three important issues about the development and viability of

cooperatives under the MACS. One issue concerns the role of the CDF as a pro-

moter of cooperatives and a provider of technical assistance to them; a second con-

nouveautés / winter & printemps 2007

191

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

Figure 2a. Governance and Operational Structure of Thrift Cooperatives

Promoted by CDF

cerns the governance of the cooperatives; and a third concerns their economic via-

bility.

As noted above, the CDF promotes cooperatives and has remained involved in

supervising and guiding the cooperatives it has promoted. When it first began this

work it sent an outreach worker into a village to talk to women in the village about

how they might help themselves through the formation of a thrift cooperative. Comme

the reputation of the cooperatives has grown the CDF has had to spend less time

conducting outreach and more time responding to requests for help in forming

192

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

Figure 2b. Governance and Operational Structure of Thrift Cooperatives

Promoted by CDF (a continué)

cooperatives. The CDF is very conscious of the role it plays in the promotion of

cooperatives, and the need to ensure that good governance policies are in place

while also respecting the self-help, mutual aid principles of cooperatives.

An example of this balance is how the CDF provides audit services to the coop-

eratives and associations. The CDF audits each association monthly. It audits a new

cooperative within an association every three months until it has matured to the

point where the association auditor can audit it. The CDF continues to conduct a

test audit of each cooperative in an association once a year, until the cooperative

nouveautés / winter & printemps 2007

193

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

has matured sufficiently not to need this level of supervision. At this point there is

little direct supervision of a cooperative by the CDF, but the CDF still receives

reports on the activities of each cooperative through monthly association reports.

En outre, the CDF also provides on-going training to the accountants, direc-

tors, and presidents of the cooperatives.

The purpose of these activities is to ensure that the cooperatives keep accurate

information about their activities and that the leaders of the cooperatives do not

de-fraud the members. Mais, as much as possible, these supervisory activities are

delegated to members of the cooperatives themselves, especially to those working

at the association level. These associations play a vital role in the workings of each

cooperative because they are composed of peer organizations, from different vil-

lages. En tant que tel, these peer organizations understand the challenges facing individ-

ual cooperatives, but they also have the ability to force the cooperatives to abide by

their own rules because there is a social distance between them—the fact that they

are from different villages enables them to hold each other to account without

damaging personal and social relationships within the village. A lesson from the

behavior of the CDF is that cooperatives operating under the MACS act still need

external supervision, but the preferred supervisor is a peer group of cooperatives

and/or an NGO.

It should also be noted that the 2005 CDF annual report states that 11 cooper-

atives failed in that year and were dissolved. This is not necessarily a bad sign. C'est

indicative of the fact that the CDF allows the cooperatives it promotes to fail—its

interest is not in having cooperatives exist for their own sake but in having success-

ful cooperatives actively serving the interests of their members.

As noted above, the CDF annual report identifies very few cooperatives where

elections for the leaders of the cooperatives (directors and presidents) are conduct-

ed by secret ballot. Most elections are in public meetings where people can see how

each person votes. This is less than ideal for organizations based on democratic

principles. En outre, Stuart documents that among the WTCs there is a ten-

dency for the presidents to be from the higher castes, though directors are more

representative of the membership of the cooperatives as a whole.24 He concludes

that one can not divorce the functioning of the cooperatives from the social struc-

ture within which they are operating, mais, despite flaws in the democratic process-

es of the cooperatives, many basic accountability measures seem to be working. Dans

particular, he finds that there is no caste bias in the distribution of loans, once one

takes into account the savings individuals have accumulated and the length of time

they have been members of the cooperatives, and that there is strong compliance

with a key lending rule relating loan size to the amount saved.25

A final issue raised by the data on the cooperatives promoted by the CDF is the

fact that the cooperatives have mobilized excess funds that they have not lent out

to their members. In many cases they have deposited these funds in commercial

banks. There is a concern within the cooperatives that the rule that stipulates that

a member can only borrow three times the amount they have deposited in the

thrift restricts the borrowing of some members, in particular higher income mem-

194

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

bers, who could productively use a larger loan. This policy stems from a strict

interpretation of the cooperative principles of the ICA and embodied in Section

3.d) of the MACS Act, which stipulates that:

The economic results, arising out of the operations of a cooperative society

belong to the members of that cooperative society and shall be distributed in such

a manner as would avoid one member gaining at the expense of others…

With the encouragement of the CDF, the cooperatives have maintained their

adherence to the “three times” rule, but with the result that not all the funds are

used for loans to members. As a way to address this issue, the CDF has promoted

dairy cooperatives in an effort to encourage widespread economic activity, lequel

will increase the demand for loan funds across all members of the thrift coopera-

tives. They have successfully promoted two dairies thus far, both of which supply

milk to the growing city of Warangal.

In sum, the activities of the CDF, the advocates behind the MACS Act, clearly

demonstrate that having the right authorizing environment is not enough to

enable the formation and effective management of cooperatives in rural Andhra

Pradesh. The cooperatives need advice and training—they need assistance in

building their operational capacity. The lesson does not stop here. A further

requirement is that these capacity-building efforts take place in a manner that

respects the autonomy of the cooperatives. The membership and the leaders of the

cooperatives cannot rely on the CDF to bail them out if they make mistakes; ils

have to rely on themselves and each other. This is the only way to build capacity

while staying true to the intent of the authorizing legislation.

MACS Act and Self-Help Groups

The Self-Help Group (SHGs) movement in India is massive and growing rapidly.

SHGs are groups of between 10 et 15 women who come together to engage in

activities of mutual benefit. A key component of the groups’ activities is mobiliz-

ing savings and gaining access to credit by linking to a bank. State governments,

NGOs, et, now, banks promote the SHGs and provide them with advice and sup-

port. According to the National Bank for Agriculture and Rural Development

(NABARD) there were 2.2 million Self-Help Groups linked to banks as of March

31, 2006, amounting to almost 33 millions de personnes (almost all women). In the peri-

od between March 2005 and March 2006 620,000 SHGs linked to banks.26 The

majority (54%) of SHGs are in the south of India, with half of these being in

Andhra Pradesh—about 500,000. In addition to linking SHGs to credit through

banks, the program of promoting SHGs also provides grant funding to those

organizations that promote them so that they, à son tour, can build the capacities of

the SHGs. The grant money also goes towards subsidizing the SHGs themselves

through subsidized credit and other subsidized goods or services.

Unlike in the case of the thrift cooperatives, the SHGs were not intended to

turn into cooperatives registered under the MACS act. The initial promotion of

SHGs began in Andhra Pradesh in 1995. In the late 1990s this effort attracted the

nouveautés / winter & printemps 2007

195

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

attention of the World Bank, which agreed to fund efforts to promote more SHGs

and to build their capacity. In the Bank’s planning documents for the Velugu pro-

gram, bank staff anticipated the formation of Village Organizations (VOs) made

up of 10 à 30 SHGs (or CIGs, Common Interest Groups, in the language of the

World Bank document) and federations of VOs called Mandal Samakya. But both

of these types of federation would be “unregistered and informal federations," et

there was no mention of the MACS act anywhere in the Bank’s 119 page docu-

ment.27 By 2003, in the mid-term reports from three of the six districts targeted by

the Velugu program, it is clear that those on the ground were encouraging VOs to

register as cooperatives under the MACS act. The mid-term report from the

Adilabad district suggests that all 1,076 VOs formed in that district were being

encouraged to register under the MACS act.28 In Mahabubnagar, the officers in

charge of implementing Velugu held a training regarding MACS for members of

SHGs and VOs, and have also encouraged the registration of VOs and mandal-level

federations under MACS. As of September 2003 they had formed 951 VOs.29 In the

Srikakulam district the Mid Term Review Report boasts the existence of 837 VOs

(down from 1643 dans 2002-3) lequel, according to the report, have registered under

the MACS act.30 The Chitoor and Ananthapur reports did not mention MACS, et

the Vizianagaram report only mentioned an exposure visit to another district to

learn about the operations of MACS.31 Overall, Adilabad, Mahabubnagar,

Srikakulam, and Vizianagaram have the largest number of thrift cooperatives reg-

istered under MACS in the whole of Andhra Pradesh, as of January 31st 2006.

The sheer volume of registrants under the MACS act as of 2006 is not neces-

sarily a positive sign. There are serious concerns about whether members of the

VOs registered under MACS even know that their VOs are registered, and what

rights and responsibilities this registration confers on them. A study by Mahila

Abhivruddhi Society, Andhra Pradesh (APMAS) dans 2003 concluded that:

Governance is a key area, which requires immediate attention…

Federations and Village Organisations are being registered under the

APMACS Act, and almost all Board members are unaware of the bylaws

and compliance of the same along with compliance of the APMACS Act.

In certain situations, legally, the Board ceases to exist, due to noncompli-

ance of the Act, which could create a legal problem.32

APMAS also observed a heavy reliance of members and directors of federa-

tions on the staff of the promoting NGO, and noted that staff working for the fed-

erations tended to see NGO staff as their bosses, not the directors of the federation.

The report also noted that:

Systems and Operating Processes is another area requiring immediate

focus. Quality and regularity of book keeping and MIS are the two major

areas which need to be improved. Though the records maintained at the

SHG level are adequate, accuracy and timeliness in recording informa-

tion is low.

196

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

The APMAS findings are from research conducted in 2003, and from a small

sample. Since then the state government and NGOs have continued to provide

support and capacity building to SHGs, VOs, and MSs. But it is unclear whether

these efforts are sufficient, especially given the fact that the number of SHGs con-

tinues to grow rapidly. The rapid promotion of VOs across the state harkens back

to the experience with cooperatives under the British, in that the enthusiasm for

the cooperatives comes from the promoters not the members. En outre, un

chief motivation behind the formation of VOs is to enable the SHGs’ access to

external funding from government and commercial banks. As in the past, le

emphasis is overly focused on credit activities, while ignoring the controlling hand

that having one’s savings at risk plays in ensuring that members manage the risks

inherent in lending to each other. Enfin, as Sinha et al. report the SHGs them-

selves, on which the VOs and MSs are built, are not in the best condition. Pour

Andhra Pradesh, where they studied 60 SHGs in 28 villages, they report that 45%

of SHGs have good or adequate records, 59% have up-to-date passbooks (dans lequel

savings are recorded) and the portfolio at risk is 35% of outstanding loans.33 Given

these developments there is a distinct possibility that a spate of scandals involving

the mismanagement of cooperatives promoted under the Velugu program will

occur. And this may prompt a rethinking of the wisdom of the MACS Act’s liberal

approach to cooperatives’ regulation. What this suggests is that the innovation that

MACS has brought to the authorizing environment in Andhra Pradesh requires

continued attention to the operational capacity of the cooperatives and the NGOs

that support them. But this point may be moot, because the MACS act faces anoth-

er, more powerful threat, that of being superseded by legislative and regulatory

efforts at the state and national levels.

THE FUTURE OF THE MACS ACT

Apart from the challenges outlined in the previous section, the MACS Act faces

challenges from policy changes at both the state and national levels. At the state

level the legislature passed a bill in 2005 to remove dairy cooperatives from the

MACS Act, and return them to the supervision of the 1964 Cooperative Societies

Acte. Though the bill does not apply to thrift cooperatives there is a concern that if

the legislature is successful in removing the dairy cooperatives from the MACS Act,

it can then move on to other cooperatives, such as thrifts. As this article went to

press, the High Court of Andhra Pradesh decided in favor of allowing the dairy

cooperatives to remain under the MACS Act.

At the national level on February 22, 2007 the Union Cabinet (the cabinet of

the national government) approved the Micro Financial Sector (Development And

Registration) Bill 2007, the intent of which is to provide a legal framework for the

entities engaged in micro finance and facilitate an environment for development

of micro finance services in the country with greater transparency, effective man-

agement and better governance.34

The bill poses a challenge to the MACS Act because it proposes that NABARD

nouveautés / winter & printemps 2007

197

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

regulate microfinance organizations that “offer thrift services.” The regulations

contain a number of requirements such as a minimum capital requirement of

Rs.500,000, that it be well managed, that it have an annual audit, and that it build

up a reserve fund. But most importantly it includes the phrase “any other condi-

tion, which may be specified by regulations in this behalf.” This clause essentially

gives NABARD the power to promulgate regulations beyond those specified in the

bill. The bill also requires that all MFOs, including those not providing “thrift serv-

ices” submit certified financial reports to NABARD. Should the bill pass it would

apply to the over 7,000 thrift cooperatives currently accepting thrift deposits from

their members, and registered under the MACS Act, and also Village Organizations

registered under the Societies Act (1860). It would also, it seems, apply to self-help

groups that collect savings from their members.

If this act becomes law, then the

VOs in Andhra Pradesh will have come full circle, back to where cooperatives were

before the MACS Act: they will be cooperatives with little membership support,

accessing external credit, and subject to a regulator with extensive powers to inter-

vene in its operations.

CONCLUSION

The MACS Act is a regulatory innovation in microfinance. It is not an uncontro-

versial one, in that its purpose is to give member-owned and member-financed

cooperatives the freedom to manage their own operations with little government

regulatory supervision, even though they are mobilizing savings. En même temps,

the act does enable the membership of the cooperatives to provide as much over-

sight of their own operations as they see fit, and exposes them to potential losses if

they fail to do so. En tant que tel, the MACS Act is very similar to the intent of micro-cred-

it operations whose purpose is to put the tools of development, in the form of

credit, in the hands of the poor, allows them to decide how best to use the money,

and requires them to bear the risk entailed by that decision. The borrower takes

on the rights and responsibilities for the use of that money. En outre, peer

lending is, essentially, contracting out the management of risk to the peers of the

borrower, because it is asking the borrower’s peers to: screen the borrower before

they enter into a loan contract with the MFI, support the borrower if she gets into

trouble with her loan, and hold the borrower accountable if she proves unwilling

to repay the loan. As such it is taking advantage of local knowledge and the mutu-

al accountability structures already in existence within the community to manage

In the same way, the MACS Act allows members of a cooper-

the risk of the loan.

ative to formulate their own by-laws by which they will hold each other account-

capable. The assumption is that the members will adopt by-laws that best suit their

own situation, including the pre-existing accountability structures in their com-

munity.

Despite this similarity, there is one major difference between the MACS Act

and a micro-loan in terms risk and responsibility. In the case of a micro-loan the

borrower is not likely to have to manage a complex organizational structure with

198

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

which she is unfamiliar. It is likely that the money will be used in the context of her

household and enterprise—two organizations with which she is highly familiar. Dans

the case of the member of a thrift cooperative, she is signing on to a new organi-

zation that requires a governance structure, information systems, and the willing-

ness and ability on the part of the member to participate in decisions within that

governance structure based upon the information emanating from the systems.

This is a more complex requirement. As a result, it is not surprising that the

Cooperative Development Foundation, which fought hard for the MACS Act, et

has promoted a large number of well-run cooperatives, provides the cooperatives

it has promoted with advice and technical assistance. The members of these coop-

eratives and their leaders need such advice and assistance. The CDF meets that

need, but it does so in a way that attempts, as far as possible, to respect the auton-

omy of the cooperatives and their associations. In doing so, it is attempting to

comply with the spirit of self-help and mutual aid that is the central tenet of the

principles on which the MACS Act is founded, and to ensure that the cooperatives

develop to a point that they no longer need the advice and assistance of the CDF.

One potential threat hanging over the success of the MACS Act is that the large

number of cooperatives recently registered under the MACS Act have not had the

benefit of the same type of advice and assistance. The APMAS evaluation suggests

that the registration of the VOs and MSs under the MACS Act has not always

stemmed from the efforts of the membership and their duly elected leaders, mais

rather from the efforts of the NGOs that promote and support those federations.

Par conséquent, the membership may not have a full sense of their rights and responsi-

bilities under the act. For now, they have the support and oversight of the NGOs

that promoted them. But it is unclear whether this support and oversight will

result in increasingly autonomous cooperatives.

The other potential threat hanging over the MACS Act is from those who

believe that it is not an innovation, but bad policy. As noted above, the parallels

between the MACS Act and the innovation inherent in extending uncollateralized

credit to the poor are strong. So it is harder for the critics to make the case. This is

especially so because the cooperatives are mobilizing savings and extending serv-

ices to their members, who have the rights and responsibilities defined by their by-

laws and the basic governance infrastructure required by the act, and they are not

engaging in regular “banking” activities that might impact the broader financial

système. If there is one weakness in this argument, with respect to the MACS Act, it

is that the Act allows the mobilization of savings from non-members who are indi-

viduals. This should be changed, because it opens the door for individuals who

have no say in the running of the organization to put their money at risk. But his-

tory tells us that this weakness is small compared to the weakness of cooperatives

that are heavily regulated by a government entity that emasculates the rights,

responsibilities, and risks that belong to the membership.

1. These are: Bihar, Chhattisgarh, Jammu and Kashmir, Jharkhand, Karnataka, Madhya Pradesh,

Orissa and Uttaranchal. Government of India (2004). “Task Force on Revival of Cooperative

nouveautés / winter & printemps 2007

199

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Guy Stuart

Credit Institutions. Draft Final Report.”

2. M.H. Moore (2000) “Managing for Value: Organizational Strategy in For-Profit, Nonprofit, et

Governmental Organizations.” Nonprofit and Voluntary Sector Quarterly 29(1): 183-204.

3. Ibid..

4. Ibid., p. 15.

5. See chapter 7 of Muhammad Yunus (2003), Banker to the Poor: Micro-Lending and the Battle

Against World Poverty. (New York: Public Affairs), to read a description of how the law was passed.

6. F. Moore. (1954). “Money Lenders and Cooperators in India.” Economic Development and Cultural

Changement 2(2): 139-159.

7. Ilbert, C. (1906). “Review of Legislation 1904, British India.” Journal of the Society of Comparative

Legislation 7(1): 81-89.

8. Ibid., 85.

9. The nine states covered by Qureshi’s data were: Mysore, Baroda, Hyderabad, Bhopal, Gwalior,

Indore, Kashmir, Travancore, and Cochin.

10. A.I. Qureshi, The Future of the Co-Operative Movement in India. Madras (Chennai), (Oxford

Presse universitaire, 1947).

11. Ibid., p. 17-18.

12. Ibid., p. 58.

13. No reference in bibliography

14. Qureshi, The Future of the Co-Operative Movement in India, p. 63.

15. Government of India (2004). “Task Force on Revival of Cooperative Credit Institutions. Draft

Final Report.”

16. These principles are explicitly stated in section 3 of the act under “Cooperative principles and

byelaws.”

17. MACS Act, 17.2

18. Par exemple, when a cooperative registers under the act it must provide the registrar with a copy

of the by-laws which should cover the 39 issues specified in the act.

19. It is no longer possible for a Registrar to decide to wind up a cooperative on his own volition,

appoint a liquidator and then allow the liquidator to take years to do his job, while receiving pay-

ments for the work from the assets of the cooperative. (CDF Comment 44)

20. References to sections, sub-sections, and clauses of the Act will be according to the following:

Section 14.1.b refers to section 14, sub-section 1, clause b of the Act.

21. The difference between such a bank and a thrift cooperative is that the latter plays no active role

in the monetary system of the economy—it can not issue “money” that is accepted outside the

cooperative, whereas a bank whose customers write cheques, enable their clients to create

“money” by writing a cheque drawn on a bank.

22. Cooperative Development Foundation, Thrift Cooperatives around Warangal City, Andhra

Pradesh, Performance Report: 2005, (Warangal, Andhra Pradesh: Cooperative Development

Fondation, 2005).

23. Author’s calculations based on data in Cooperative Development Foundation, Thrift

Cooperatives around Warangal City, p. 13-14 et 19-20.

24. Guy Stuart (2006). “Caste Embeddedness and Microfinance: Savings and Credit Cooperatives in

Andhra Pradesh, India.” Cambridge, MA, Harvard University-John F. Kennedy School of

Government, KSG Working Paper No. RWP06-037.

25. Ibid., p. 29

26. National Bank for Agriculture and Rural Development, Annual Report, (Mumbai, 2006).

27. World Bank, Project Appraisal Document on Proposed Credit in the Amount of SDR 82.9 mil-

lion (US$111.0 million equivalent) to India for the Andhra Pradesh Poverty Initiatives Project,

(Delhi, World Bank, 2000).

200

nouveautés / winter & printemps 2007

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023

Regulatory Innovation in Microfinance

28. Adilabad, Mid-Term Review Report, Velugu, Society for the Elimination of Rural Poverty

(SERP), (Adilabad, Andhra Pradesh 2003).

29. Mahabubnagar, Mid-Term Review Report, Velugu, Society for the Elimination of Rural Poverty

(SERP), (Mahabubnagar: Andhra Pradesh, 2003).

30. Srikakulam, Mid-Term Review Report, Velugu, Society for the Elimination of Rural Poverty

(SERP), (Srikakulam: Andhra Pradesh, 2003).

31. Vizianagaram, Mid-Term Review Report, Velugu, Society for the Elimination of Rural Poverty

(SERP), (Vizianagaram: Andhra Pradesh, 2003).

32. C. Reddy and L. Prakash, Status of SHG Federations in Andhra Pradesh: APMAS Assessment

Findings. (Hyderabad, Andhra Pradesh, Mahila Abhivruddhi Society, Andhra Pradesh

(APMAS), 2003).

33. Ibid., p. 23.

34. F. Sinha, and M. Harper, et coll., Self Help Groups in India: A Study of the Lights and Shades, (CARE,

Catholic Relief Services, GTZ, USAID, 2006).

35. Press Information Bureau, Government of

India, Press Release February 22, 2007,

http://pib.nic.in/release/release.asp?relid=25021&kwd=, Accessed March 13 2007.

nouveautés / winter & printemps 2007

201

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/2/1-2/181/704149/itgg.2007.2.1-2.181.pdf by guest on 08 Septembre 2023