David Porteous

Mobilizing Money through

Enabling Regulation

Money will be fully mobile only when everyone has a safe place to store it, et le

capability to receive and make payments, quickly and affordably, from and to any

other person or entity from that store of value—in other words, to use mobile

money.1 We are a long way from that goal today. Bank accounts are regarded as the

traditional safe place to store money, yet a 2006 study estimated that globally

perhaps only 1.5 billion people have bank accounts.2 Not all of these accounts have

the level of speed or convenience—mobility—that comes from electronic banking,

although the usage of e-banking channels has grown with the issuance of ATM and

debit cards over the past two decades: in some developing countries, people still

have passbook-based or domiciled accounts in which their money is effectively

immobilized to cash access at one branch.

En même temps, we have witnessed the amazing rates of adoption of mobile

phone communications even in the poorest and most remote countries: dans 2009,

by far the majority of the earth’s population will live in areas with wireless recep-

tion, and four billion people will be mobile subscribers, most of them prepaid.

Even if we account for the double counting that occurs because of multiple mobile

subscriptions,3 it is clear that many more people are now in real-time voice or SMS

contact with others across the globe, compared to the numbers using electronic

financial services.

What would it take to mobilize money fully? D'abord, people need easy and

affordable universal access to wireless telephony. This is not yet available: même

though subscriber bases continue to grow rapidly in many developing countries,

that growth may be limited by income, topography and market structure.

Cependant, the limits to mobile penetration are clearly not the binding constraint on

David Porteous is Founder and Director of Bankable Frontier Associates, a consulting

firm based in Boston, Massachusetts. The author wishes to thank the UK’s

Department for International Development (DFID), which financed BFA involve-

ment in several projects that lead to some of the conclusions in this article; and CGAP,

the Consultative Group to Assist the Poor (especially Tim Lyman, Gautam Ivatury

and Mark Pickens), with whom Porteous has worked directly or in collaboration on

many of the issues in this paper over the last three years.

© 2009 David Porteous

nouveautés / winter 2009

75

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

the growth of mobile money at present. Deuxième, providers must have robust busi-

ness models that give them incentives to provide small-value financial services,

even to low-income people who have never before used banks. This is where the

transformational potential of mobile money lies: enabling hundreds of millions,

even billions, of new clients to use appropriate formal financial services. If mobile

money were only another channel for the already banked customer, ce serait

much less transformational.

The good news is that across different parts of the world a range of providers—

banks, microfinance entities, mobile network operators, and third-party payment

providers—have been actively experimenting with new business models for

mobile money. Many are still at an early stage, so we do not yet know all the char-

acteristics of the models that will prove successful over time. Some are beyond this

early stage: the incredibly rapid adoption of Safaricom’s M-Pesa’s mobile money

transfer service in Kenya has set new records and raised expectations about what is

possible. Entre-temps, the early pioneers of mobile money in countries like the

Philippines and South Africa are maturing and evolving as they learn more about

what works and what doesn’t.

The level of interest in mobile money is now strong enough to ensure that new

business models will still emerge and some, though not all, of the existing models

will evolve and become robust. Cependant, both the providers and close observers of

the sector agree that inappropriate regulation constrains the development of trans-

formational mobile money models in many places.4 Or to put this another way, un

enabling policy and regulatory environment is vital if transformational branchless

banking is to emerge and develop. This was the key argument of an early report

BFA (2006) wrote for Britain’s Department for International Development (DFID)

almost three years ago. Three years later, much more research has been done to

understand the regulatory issues affecting mobile money across a number of coun-

tries, much of it undertaken or supported by CGAP (the Consultative Group to

Assist the Poor) and DFID.5 We have come to understand much better how to diag-

nose the regulatory environment for mobile money in a country, and consequent-

ly how to identify and recommend the necessary changes.

En effet, we are now in a position to test a hypothesis that is implicit in the

statement above: if regulation is indeed a key constraint on the development of

mobile money models, then we would expect to see more activity and develop-

ment in those jurisdictions that are more conducive to the emergence of these

models, and less development in those that are not. The problem with testing this

hypothesis has been how to rate the “conduciveness” of a regulatory environment

on a consistent basis to facilitate the comparisons. Building on the general

approach we proposed in 2006, in this article I develop a rating system that pro-

vides a basis for comparison across countries and describes the initial results from

four countries with active mobile money models. These results confirm the

hypothèse: having an enabling environment matters for the emergence and devel-

opment of mobile money. The rating approach also provides a basis on which

countries can be encouraged and supported to make moves in this direction.

76

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

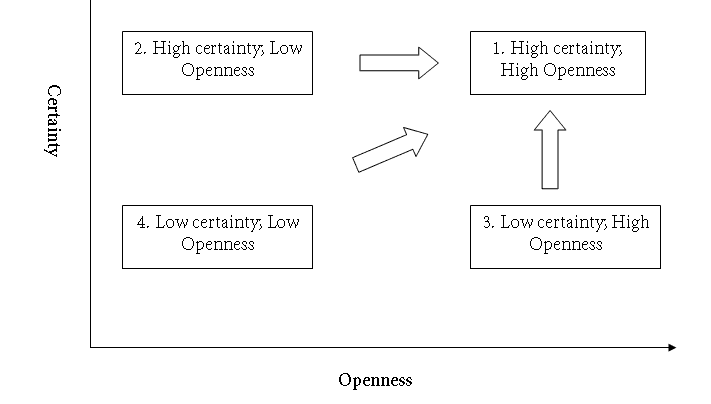

Chiffre 1. Dimensions of an Enabling Environment. Source: Based on BFA 2006.

WHAT IS AN ENABLING ENVIRONMENT FOR MOBILE MONEY?

An enabling environment is one that allows, and may even encourage, the intro-

duction and development of new business models that meet a defined public pol-

icy objective. In this case, the objective espoused by many countries is that of

increasing financial inclusion—that is, the proportion of people with appropriate

formal financial services. In our 2006 report for DFID, we proposed two key

dimensions for an enabling environment in a new sector like mobile money. These

étaient:

Openness: the extent to which new models that had the potential to be trans-

formational were not prohibited from starting up.

Certainty: the extent to which policymakers and regulators provide clarity that

reduces the level of risk for private sector operators, not only at startup but over

temps.

In that report, we depicted the possible combinations by placing each of these

dimensions on one axis, as shown in Figure 1 (au-dessus de). Dividing the space into high

and low zones on each axis produces the four quadrants indicated.

Quadrant 1 (high certainty and high openness) is clearly the most suitable sit-

uation to facilitate mobile money, hence the direction of the arrows. Cependant,

based on early diagnostic work in two African countries (South Africa and Kenya),

we hypothesized that middle-income countries like South Africa were more likely

than low-income countries to be in quadrant 2 (high certainty, low openness)

because they typically have more developed regulatory regimes. C'est, they usu-

ally have a range of regulatory institutions that have issued regulations or guidance

on mobile money or related issues, increasing the certainty, but they face the real

nouveautés / winter 2009

77

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

risk that a plethora of overlapping and sometimes obsolete regulations will reduce

the space in which they can innovate. Inversement, we hypothesized that in low-

income countries like Kenya, there was simply less on the books in the way of leg-

islation and regulation, usually resulting in more discretion for regulators (et

correspondingly, less certainty for providers), but this lack of regulation could also

create more openness for the development of innovative models. The report sug-

gested which regulatory domains were affected by mobile money but did little to

prioritize among them.

Recently, Tim Lyman, Mark Pickens and I (2008) went further, suggesting how

to prioritize the factors based on identifying two necessary conditions for branch-

less banking to emerge from the range of country diagnostic missions undertaken

dans 2007. These conditions are:

Agents must be allowed to operate on behalf of banks and others to open accounts

and handle cash-in and cash-out functions. As Lyman, Ivatury, and Staschen (2006)

argued convincingly, this particular arrangement greatly extends the potential

reach of the financial system, since existing businesses, such as local merchants, peut

function as financial service points at much lower cost than if a bank had to set up

a new branch or even an ATM infrastructure.

Regimes to oppose money laundering and the financing of terrorism (AML-CFT)

should be proportionate. Spécifiquement, the due diligence procedures required under

Know Your Customer (KYC) règlements (now present in most countries) pour

opening new deposit accounts or taking payments must allow for reduced identi-

fication and verification procedures for low-risk customers. Otherwise,

faible-

income people could never meet the standards set in developed countries, lequel,

for example, require them to verify a physical address by presenting a utility or

other bill.

Lyman et al. (2006) identified four more regulatory areas (“next generation

issues”) that would affect the trajectory of development. There should be an

appropriate space to issue e-money and other stored value instruments, along with

effective consumer protection, an inclusive system to regulate payments, et

appropriate competition rules for new payment systems.

They also affirmed the earlier observation that, because the regulation of

mobile money cuts across many regulatory domains, the risk of coordination fail-

ure is higher. Without the clear leadership and policy direction that will enable this

space to develop, there is less prospect of necessary changes being coordinated

across different regulatory agencies, or even across divisions within one agency,

such as a central bank of a particular country. Lack of coordination among regu-

lators remains one of the biggest obstacles to progress. Even if one agency is posi-

tive about the prospects for mobile money, and wants to enable it, changes in one

area alone are often not sufficient to enable change. This situation is common, pour

example, among payment system supervisors who want to make their retail pay-

ment systems more efficient.

78

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

FROM INFORMATION TO RATING

Thanks to such research, we now have greater clarity about the balance of factors

that are more likely to result in the emergence of transformational models for

mobile money. Cependant, it remains hard to compare the situation across countries

based on qualitative information alone. The value of cross-country ratings in cre-

ating a focus on the underlying issues has been amply demonstrated in recent years

by the World Bank’s annual Doing Business Surveys. These surveys, now per-

formed in some 181 des pays, annually collect information that the World Bank

then uses to populate a scorecard for each country across 11 components of the

business environment. The resulting relative overall and sectoral scores can then be

compared and analyzed in depth. The website, www.doingbusiness.org, provides

tools to facilitate this comparison and analysis.

The success of a rating scale derives from the clarity of its purpose. For Doing

Business, the scores seek in essence to measure the extent to which private sector

development is possible and likely in a country. Our objective here is in some ways

a specialized subset of this aim: we want to compare the extent to which transfor-

mational mobile money models of all forms are allowed and enabled across coun-

tries.

To proceed from the general insights about regulatory factors above to a coun-

try rating model for mobile money, we took two steps:6

We designed a simplified questionnaire that collects answers about the status

of policy or legislation (including regulation or guidance) across the two dimen-

sions of openness and certainty and in the main domains bearing on mobile

money in a definitive “yes,” “no,” or “maybe” format. En général, the questions were

designed to be factual and clear so that a “yes” answer was positive, and a “no” was

negative. To produce clear results, a questionnaire like this has to sacrifice some of

the underlying complexity. Part of this questionnaire appears in the Annex.

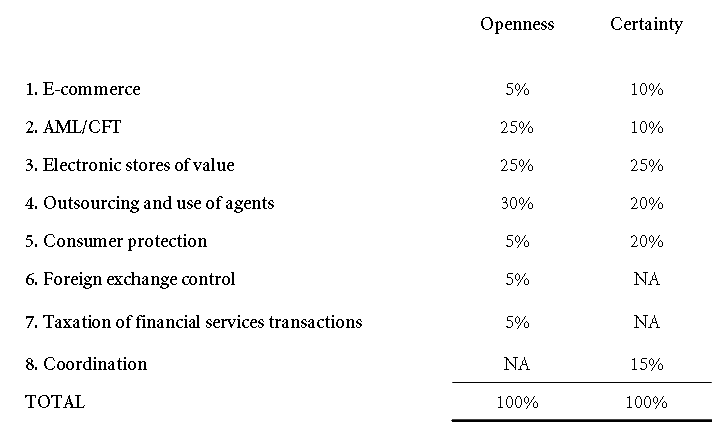

We then developed a scoring model that weights the answers obtained relative

to the purpose of the rating expressed above: the weights we use for each of the

eight domains are shown in Table 1. We used our judgment to develop the weight-

ing, which clearly prioritizes the two necessary conditions described above

(AML/CFT and use of agents, in items 2 et 4 below), as well as the environment

for issuing e-money (item 3 below).

INITIAL RESULTS

There are different ways to collect the data necessary to populate the diagnostic

questionnaire, as described in the Text Box titled “Collecting the Data.” Depending

on the level of published material, the information can be difficult and expensive

to obtain. Donc, we focus here on using publicly available information from

diagnostics in four key countries, chosen because of their scale and the levels of

interest and activity in mobile banking. They include three leading countries that

are mobile money pioneers in the developing world—Kenya, the Philippines, et

nouveautés / winter 2009

79

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

Collecting the Data

Because of the complexity introduced by the cross-cutting regulatory domains

involved in mobile money, collecting accurate data can be time-consuming and

expensive. At least three methodologies have been tried.

In-country mission. A team of skilled external experts, supported by local

legal advisors, can meet with key regulators and market players to understand

the environment in order to produce a comprehensive view. CGAP commis-

sioned seven such diagnostic missions in 2007, resulting in country notes that

are available at http://www.cgap.org/p/site/c/template.rc/1.11.1772. Ce

approach is certainly likely to result in the best quality of information, mais

requires having a skilled mission team in-country for up to ten days, making the

process expensive and time-consuming.

Desk review. Researchers can review available published information, même

using the local resources in a country. We tried this approach as part of the

Mobile Money Transfer Project, which involved cooperation between CGAP,

DFID and GSMA in 2006 et 2007. We found, d'abord, that it is not easy for a local

person to make sense of what is sometimes a thicket of laws, règlements, et

guidance. Deuxième, the easy availability of published regulations or guidelines

declines steeply with a country’s level of income. C'est, researchers can be over-

whelmed by the task of collating the available information for say, the UK;

meanwhile they find that for most low-income countries, little is publicly avail-

capable. Ainsi, they need to engage with policymakers and regulators to get a sense

of their intentions and attitudes.

Self diagnostic. Regulators themselves can be asked to complete a diagnostic

questionnaire, on the assumption that they are best placed to answer the ques-

tions authoritatively. We designed what we call a “diagnostic lite” questionnaire

for the payment regulators of

le 15 Southern African Development

Community (SADC) countries in a 2007 DFID-funded project. This is an

improvement on the desk review approach because the regulator is directly

involved. Cependant, the underlying issues in the questionnaire cut across regula-

tory boundaries, making it hard for one agency or one division within an agency

(such as the Payment Systems Divisions) to complete all the aspects of a diag-

nostic with equivalent levels of knowledge or certainty.

In the results reported here, we draw on published information that relies on

data we collected in 2007 for the four countries, using the methodologies

described above, to reach our own answers to the questions in the diagnostic lite.

South Africa—and India. In India, interest in mobile money has exploded in the

past three years, after mobile subscriptions took off in that massive country with

its great infrastructural challenges for traditional models of extending the financial

système. Several Indian banks have introduced various mobile channels for their

customers, although mass usage of those channels reportedly remains low and is

80

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

Tableau 1. Weighting of domains in the scorecard.

certainly not yet transformational. Entre-temps, other service providers (third party

and mobile network operators) have been developing plans to enter the space.

While this is a small sample, these four countries offer sufficient variation in terms

of income level per capita and extent of activity and development in mobile money

to test our hypotheses about enabling environments and the growth of mobile

money.

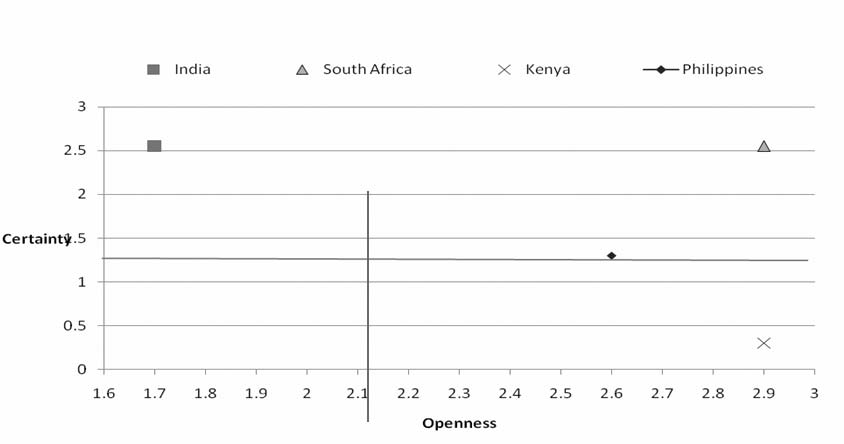

Chiffre 2 plots the scores we obtained for each of the four countries when we

applied the rating to the diagnostic questionnaire on each of the two dimensions.

The space is divided into four quadrants using median scores on each axis for six

countries.7 Clearly only the relative scores have meaning.

The outcome of the scoring summarized in Figure 2 supports several of the

hypotheses I advanced earlier. Three points are especially important. D'abord, le

openness of the environment does indeed matter: in all of the three countries that

are ranked much higher on the openness axis (c'est à dire. to the right-hand side), mobile

money models have been relatively more active for longer and are more widely

used, compared to India, which lies lower on the openness axis.

Deuxième, cependant, the countries classified as middle income by the World Bank

(Afrique du Sud, the Philippines, and India) all lie higher on the certainty scale than

low-income Kenya, which is clearly in the bottom right quadrant (high openness

but low certainty). The Philippines is positioned just inside the top right quadrant,

reflecting the fact that while its environment is very open, some of the models have

been authorized based on bilateral letters of agreement, although the Central Bank

of the Philippines is now seeking to move beyond this level of discretion toward a

nouveautés / winter 2009

81

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

Tableau 2. Comparing the sample countries.

Sources: World Development Indicators, World Bank, Honohan (2007), Finscope,

and local sources.

Specific sources of data are as follows.

• GNI per capita is from World Development Indicators (WDI) pour 2007.

• Country classifications are from the World Bank website.

• Mobile penetration is from WDI 2007, section on mobile penetration.

• Percentage banked is from Honohan (2007); that for Kenya and South Africa comes from

FinScope household survey data for 2006 et 2007 respectivement (voir

http://www.finscope.co.za/southafrica.html. For background and publications from FinScope

SA and http://www.fsdkenya.org/finaccess/index.html for Kenya).

• Estimates of number of mobile money users were compiled from a range of local sources: dans

Kenya, registered M-Pesa subscribers reported as of October 2008, which understates the num-

ber since there are other but much smaller m-banking services available; in South Africa, press

reports in September, 2008; in the Philippines, aggregates of active customer numbers of G-

Cash and SmartMoney in 2008.

broader framework in key areas like e-money issuance by non-banks. In some

ways, South Africa’s position is surprising: experiments began there comparative-

ly early and several well-known pioneering models such as Wizzit and MTN

Mobile Money emanate from there, but the role that non-banks can play in issu-

ing e-money is circumscribed by the current guidance note on e-money, which has

frustrated some potential innovators. To further enhance its environment, South

Africa would have to amend its position, Par exemple, by creating a category of reg-

ulation for non-bank e-money issuers, or “narrow banks,” a step that has in fact

been considered. En général, common law countries have an advantage in terms of

openness because of the presumption that whatever is not prohibited is in fact

allowed; in civil law countries, the reverse applies.8

Enfin, India has a plethora of legislation. Its laws, règlements, and guidelines

across a range of areas provide certainty, but limit the openness on key issues; pour

example, what types of entities can serve as agents? The Reserve Bank of India first

allowed agents to function in 2006, et en 2008 issued further guidelines to clari-

82

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

Chiffre 2. Rating scores.

Source: BFA scoring methodology based on information for each country obtained

dans 2007.

fy the restrictions on this role.

While it is easy to make the case for openness, recent events in Kenya also show

the importance of certainty. Par exemple, M-Pesa, perhaps the largest single

mobile money model in these four countries based on number of users, is not for-

mally regulated but operates at a system-wide scale under a no-objection letter

from Kenya’s Central Bank. The bank has expressed its intention to introduce the

necessary laws and regulations to bring greater certainty, but as recently as

Décembre 2008, the minister of finance called for a special audit, announcing con-

cerns over the fact that M-Pesa is unregulated.9

Clairement, openness and certainty alone are not sufficient to ensure the sustain-

able development of mobile money. The safety of clients’ deposits matters too, comme

Lyman, Pickens, and Porteous (2008) point out. In the absence of a framework that

creates certainty about which types of entities can enter and how they must

behave, too much openness to innovative models from new entrants can be risky,

especially once these models move beyond the small-scale pilot stages. Dans 2006,

BFA argued for a phased approach that is more open to a range of models at early

stages of market development but then introduces successively increasing certain-

ty, together with client safeguards, as the market scales up. À ce jour, the Philippines

is probably the best country example of this phasing. But the speed at which

Kenyans have adopted M-Pesa should wake up regulators who think they can post-

pone a response to mobile money: appropriate models can scale up very quickly,

and policymakers and regulators must explicitly consider this possibility in

advance so that they have prepared their options to ratchet up their responses over

nouveautés / winter 2009

83

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

temps.

David Porteous

IMPLICATIONS AND CONCLUSIONS

I have described a simple method for rating country environments for mobile

money. By demonstrating the results of our scoring for four developing countries

that lie at the heart of much activity in mobile money, I have shown how the

methodology appears quite robust in locating the countries, compared to earlier

expectations. Clairement, the scoring model would benefit from being extended to

include data from other countries in order to broaden the sample and define the

medians of openness and certainty based on more variety. En fait, we have already

applied the methodology to an additional four countries, as well as to the ten

SADC countries other than South Africa that completed self-diagnostic question-

naires in late 2007, but we cannot yet publish these results.10 But this extension

would allow us to further refine our questions and weightings.

For now, the rating methodology offers a promising means to compare coun-

tries in a simple but clear way. This has clear implications for each of two main sets

of users.

D'abord, for international mobile money providers looking to enter new markets,

this rating system is a relatively low-cost tool to screen for (or at least understand)

a choice of country in terms of some of the most vital regulatory issues that can so

hamper or facilitate subsequent development.

Deuxième, for policymakers and regulators, this methodology, like other country

ratings, should stimulate pointed discussions about how to facilitate the develop-

ment of mobile money. The answers to the underlying diagnostic questions pro-

vide a way for regulators to assess their own situation and to consider what they

can do. Whether or not policymakers are concerned about their country’s relative

ranking on any rating, they should be concerned about improving their enabling

environment for mobile money. High-level policymakers can take an important

first step by creating a task force across the involved regulatory agencies. This task

force should have the mandate of preparing a road map that shows how the nec-

essary enabling changes can be sequenced and coordinated, proportionately to the

level of market development. If most regulators took this approach, then money

would indeed begin to be fully mobilized.

Endnotes

1. Following the definition set out, Par exemple, by Beth Jenkins (2008) in Developing Mobile

Money Ecosystems (available via

the term mobile money to refer to models of financial service provision involving mobile

phones, including both m-banking and m-payments.

2. Littlefield, Helms and Porteous. (2006). “Financial Inclusion 2015: Four scenarios for the future

of microfinance,” Focus Note No. 39, available at

http://www.cgap.org/p/site/c/template.rc/1.9.2579.

3. The mobile industry counts numbers of subscriptions to determine the number of users. Though

banking uses no single approach, we advocate counting the number of individuals with bank

84

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

accounts, not the number of accounts as some surveys have done, since individuals are likely to

have multiple bank accounts. From analyzing data from national surveys in Africa, we learned that

the number of subscribers per individual with a mobile varies from 2 in more developed markets

like South Africa to 1.2 in Kenya. See BFA (2007), Tableau 15 and surrounding. Ewan Sutherland

(2008) provides a useful note in Counting mobile telephones, SIM cards and customers, a report

pour

à

http://www.researchictafrica.net/images/upload/Mobile%20numbers_Ewan.pdf. He suggests that

the number of people who have phones may as low as one sixth of the number who have subscrip-

tion.

available

Centre

LINK

le

4. To give just one recent example, in a poll of 30 experts at a CGAP-MicroSave workshop held in

Août 2008, including representatives of some of the pioneers of mobile money, presque 80%

agreed or strongly agreed that “regulatory constraints are restraining the growth of m-banking

solutions.”

5. Plus récemment, the Asian Development Bank and the Inter-Asian Development Bank, among oth-

ers, have done similar research.

6. We first did this in a DFID-financed report for 15 SADC countries using responses from each cen-

tral bank to questionnaires, although the country-specific results have not yet been published and

hence are not used here.

7. The other two countries are middle-income Mexico, and lower-income Papua New Guinea. Ils

broaden the sample medians, although we do not specifically report on them here.

8. En effet, this is our experience of rating two unnamed civil-code countries: un (a LIC) falls into

the bottom left corner, the lowest potential quadrant. This is of course in line with the general

findings of doing business that common law environments are usually more enabling for business

than civil-code countries.

9. Business Daily, 10 Décembre 2008, page 1, available at

http://www.bdafrica.com/index.php?option=com_content&task=view&id=11685&Itemid=5812

10. We are cooperating with the Spanish consulting firm AFI to rate six Latin American countries at

different stages of development, and expect the results after the first quarter of 2009.

Les références

Bankable Frontier Associates (BFA) (2006). “The enabling environment for mobile banking in

Africa.” Report for DFID available at www.infodev.org/en/Document.76.aspx.

Bankable Frontier Associates (2007). “Financial service access and usage in Southern and East

Africa: What do FinScopeTM Surveys tell us?” Report for FinMark Trust, available at

http://www.finscope.co.za/documents/2007/CrossCountryreport.pdf.

Bankable Frontier Associates (2008). “The environment for transformational mobile banking in

SADC.” Unpublished report for DFID.

FinScope, www.finscope.co.za

Honohan, Patrick (2007). “Cross country variation in household access to financial services.” Paper

presented at World Bank Conference on Access to Financial Services, Mars 2007.

Lyman, Timothy, Gautam Ivatury, and Stefan Staschen (2006). “Use of agents in branchless banking

for the poor: Rewards, risks and regulation.” CGAP/DFID Focus Note 38. Washington, CC:

Consultative Group to Assist the Poor (CGAP).

Lyman, Timothy, Mark Pickens & David Porteous (2008). “Regulating transformational branchless

banking.” CGAP/DFID Focus Note 43. Washington DC: Consultative Group to Assist the Poor

(CGAP).

World Development Indicators (Accessed for 2007) Available via

nouveautés / winter 2009

85

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

ANNEX.

DIAGNOSTIC SELF-ASSESSMENT QUESTIONNAIRE

B. OPENNESS

B1 E-commerce

B1.1

Question: Are electronic signatures (e.g. PIN numbers to authorize transactions)

widely accepted in practice for financial transactions?

Why does this matter? If PINs are already widely used and accepted, then the lack

of an e-signature law may not stop initial developments to e-payments.

B2. AML/CFT

B2.1.

Question: Is there provision for lighter CDD procedures for those opening low-

value bank accounts or making low-value payments?

Why does this matter? Unless CDD procedures are appropriate to the risks and sit-

uation of the unbanked, they may rule out any transformational approaches.

B2.2

Question: Is the remote opening of bank accounts allowed (c'est à dire. outside of bank

premises and/or by agents of bank)?

Why does this matter? For reasons of cost and perception, regimes that explicitly

allow accounts to be opened outside bank branches are more likely to be transfor-

mational.

B3. Electronic stores of value

B3.1

Question: Are pre-paid cards allowed that can be used at multiple sites other than

the issuer?

Why does this matter? Pre-paid cards or instruments that can be used other than to

buy the goods and services of the issuer are already a form of e-money.

B3.2

Question: Are non-banks allowed to offer and operate general use pre-paid stores

of value (whether accessed by card or other instrument such as mobile phone)?

B3.3

Question: Are telephone companies able to provide services (such as ringtones or

information) to mobile phone users for which they may pay from their pre-paid

accounts?

86

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

Why does this matter? In some circumstances, this may already constitute the use

of e-money.

B4. Outsourcing and use of agents

B4.1

Question: Are agents allowed to open new accounts on behalf of banks?

Why does this matter? Agents may offer another lower-cost distribution channel for

opening accounts.

B4.2

Question: Are agents allowed to handle cash-in/cash-out transactions on behalf of

Banks?

Why does this matter? Agents may offer another lower-cost distribution channel for

withdrawals and deposits from bank accounts.

B4.3

Question: Are agents allowed to handle cash-in/cash-out transactions on behalf of

non-banks that operate payment services/store of value?

Why does this matter? Agents may offer another lower-cost distribution channel for

withdrawals and deposits from these stores.

If answer to B4.2 or B4.3 above is yes, do the legal requirements for doing so allow

a wide range of types and sizes of agent?

B4.4

Question: Are banks allowed to outsource the maintenance of account-level

account management to third parties?

Why does this matter? Outsourcing may provide cheaper models.

B4.5

Question: Are banks allowed to co-brand or offer their banking products under

brand names different from their own?

Why does this matter? Variable branding may increase the reach of products.

B5. Consumer protection

B5.1.

Question: Is there a requirement that paper statements be mailed on a regular basis

to holders of bank accounts/stores of value?

Why does this matter? Disclosure requirements will affect the cost and flexibility of

new offerings.

nouveautés / winter 2009

87

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

B6. Foreign exchange control

B6.1

Question: Are there foreign exchange controls that apply to either incoming or out-

going international remittances by individuals of low value?

Why does this matter? Foreign exchange controls affect the cost and process

involved with foreign remittances.

B7. Taxation of financial transactions

B7.1

Question: Are transactions involving a transfer of monetary value treated the same

whether the transfer service is provided by a bank or by a non-bank?

Why does this matter? Differential taxation by sector will affect whether it is viable

to offer payment services.

C. CERTAINTY

C1. E-commerce

C1.1

Question: Is there legislation in effect that provides for the validity of electronic sig-

natures?

Why does this matter? This provides certainty of legal treatment for electronically

authorized transactions, which is necessary for scale usage.

C2. AML/CFT

C2.1

Question: Are the AML/CFT exemptions codified in regulations or official guid-

ance?

Why does this matter? A clear AML/CFT regime will not leave providers exposed to

undue uncertainty as to how to apply the laws.

C2.2

Question: Is the provision for remote account opening codified in regulation or

official guidance?

C3. Electronic stores of value

C3.1

Question: Is there a clear legal definition of “payment”?

Why does this matter? While a deposit is usually defined in the main banking law,

certainty requires a clear distinction between a payment and a deposit.

88

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

Mobilizing Money through Enabling Regulation

C3.2

Question: Is there a law governing the provision of payment services?

Why does this matter? This follows from 3.1, to cover the activities of those in the

business of offering payment services

C3.3

Question: Is there a clear legal or official definition of “e-money”?

Why does this matter? E-money takes various forms, and an official definition,

whether in policy or law, will help to provide clarity.

C3.4

Question: Is there a defined law or policy stating which entities may issue e-money?

Why does this matter? This follows from C3.3 and provides clarity on how e-money

may be issued.

C4. Outsourcing and use of agents

C4.1

Question: Are there regulations that specify which services banks can outsource?

Why does this matter? Outsourcing regulations provide a framework within which

to consider what may be outsourced and on what terms.

C4.2

Question: Are there regulations that govern the banks’ appointment of banking

agents/correspondents?

Why does this matter? Specific regulations may be required to provide certainty as

to the obligations of agents and principals in this relationship.

C5. Consumer protection

C5.1

Question: Are there any particular consumer protection laws, regulations or codes

that apply to the provision of bank accounts or payments services?

Why does this matter? This will provide clarity about what the obligations of the

service provider may be, and about the risks to which the customer may be

exposed.

C5.2

Question: Are there laws or regulations that specifically govern electronic transac-

tions by retail customers?

Why does this matter? Electronic transactions bring new risks, and specific regula-

tions may be required to provide certainty and standardization in how they are

addressed.

nouveautés / winter 2009

89

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023

David Porteous

If so, do they specify the following:

C5.3

Customer liability for unauthorized transactions.

Why does this matter?The liability should clearly rest on one party, usually the

provider.

C5.4

Dispute resolution procedures.

Why does this matter? It is often necessary to specify channels other than the courts

for fast, cost-effective resolution of consumer grievances.

C6. Coordination

C6.1

Question: Does the country have a policy paper or discussion paper setting out

policy towards m-payments or m-banking?

Why does this matter? This should increase certainty by indicating the questions

and issues that concern policy makers, even if it does not provide answers.

C6.2

Question: Has a lead regulator for m-banking and m-payments been clearly iden-

tified?

Why does this matter? Having one agency able to provide regulatory leadership may

increase certainty, and reduce risk of coordination failure.

C6.3

Question: Has a policy-making ministry for m-banking and m-payments been

clearly identified?

Why does this matter? Having one ministry responsible for producing policy is like-

ly to increase certainty and reduce risk of coordination failure.

C6.4

Question: Have regulators and policy makers from different agencies whose

domains are affected met to discuss policy coordination around m-payments and

m-banking?

Why does this matter? Even meeting together can improve coordination and

increase certainty.

90

nouveautés / winter 2009

Téléchargé depuis http://direct.mit.edu/itgg/article-pdf/4/1/75/704319/itgg.2009.4.1.75.pdf by guest on 08 Septembre 2023