Pradip Kumar Sarmah

Rickshaw Bank: Empowering the

Poor through Asset Ownership

Innovations Case Narrative:

Rickshaw Bank

Seven years ago, a simple incident not only impacted me personally, but also led

me to completely change my profession. I am trained as a veterinary doctor, and

have a well-established practice in the city of Guwahati, Assam, in northeastern

India. As an outcome of my deep interest in animal husbandry and agribusiness, I

established and ran the Centre for Rural Development (CRD), a not–for-profit

organization.

To attend to work outside the office, I usually took a cycle rickshaw, a tricycle

commonly used on Indian roads to carry people or goods for short distances; this

transport would cost me five rupees one way. I often wondered how much the rick-

shaw “pullers” were earning. One day, while taking a ride, I asked one of them

“Who owns your rickshaw?” He gave a name that was clearly not his own. He said

he had been working for 16 years as a puller and was paying 25 rupees a day in

rental, about 65 U.S. cents. As he talked, I began to understand more about the

overall suffering and precarious living conditions of the rickshaw-pulling commu-

nity. As I got out of the rickshaw and moved on to my own work, I forgot about it,

but when I went to bed that evening, his words came back to me. So, I got up and

took out my calculator. I could quickly see that the driver paid nearly half his earn-

ings to rent his vehicle and had paid out, many times over, the cost of a rickshaw,

roughly6,500 rupees. For me this was a call to action.

After doing some research among pullers, I founded the Rickshaw Bank (RB)

as one of the flagship programs of CRD on the philosophy that income-producing

assets are critical if individuals are to break the vicious cycle of poverty. The pro-

gram is designed to provide a means of self-employment for members of the poor

and marginalized rickshaw community who live in urban slums. The central idea

A veterinarian by profession, Pradip Kumar Sarmah is founder of the Centre for Rural

Development (CRD) in Assam, in the northeastern region of India. He is currently

focused on scaling up the Rickshaw Bank Project, one of CRD’s flagship programs. Dr.

Sarmah became an Ashoka Fellow in 2001.

© 2010 Pradip Kumar Sarmah

innovations / winter 2010

35

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

The Rickshaw in Action

Photo by Enrico Mochi.

is to issue an asset-based loan to the rickshaw puller, who can repay the debt in

daily installments over 18 months. Full and timely repayment leads to ownership

of the rickshaw being handed over to the puller.

This concept contradicts the existing practice, in which a puller pays an equiv-

alent daily fee to rent the vehicle, possibly for a lifetime, with no possibility of own-

ership. The innovation lies in its unique style of service delivery and a design that

addresses underlying causes of poverty through asset-based entrepreneurship

development. To comprehensively meet the needs of the rickshaw puller and his

family, the daily repayment is a “one-window repayment,” a simple transaction at

the same place each day. This system provides convenient and efficient service and

creates the opportunity for the pullers to gain security through more of our loan

products. The repayment goes towards their eventual ownership of the rickshaw,

and the program provides accident insurance, a uniform and shoes, licenses, a

photo identity card, and related training. All these forms of “social security” help

protect the driver from the various threats connected with poverty, old age, disabil-

ity, and unemployment.

The Rickshaw Bank provides pullers with a technologically superior income-

generating asset: a vehicle we have dubbed the Dip-Bahan. Dip means light and

bahan means vehicle; thus this improved rickshaw gives light to the people. The

bank also provides allied services that promote micro-entrepreneurship among

urban poor and rural migrants. The bank has started programs in many parts of

36

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

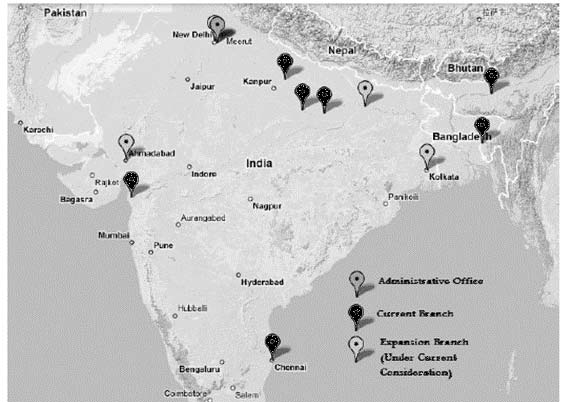

India: Guwahati (Assam), Agartala (Tripura), Chennai (Tamil Nadu), Surat

(Gujarat), Lucknow, Varanasi and Allahabad (Uttar Pradesh), and Chandni Chowk

(Delhi). It will soon add Noida (Uttar Pradesh) to the growing list.

MY ROAD TO THE RICKSHAW BANK

I was born in 1963 in Guwahati. My father worked at a university. When I was

about 10 years old, I worked as a sales agent, using my mother’s name, to distrib-

ute The Assam Tribune, a leading daily newspaper. I even hired two other boys

when the demand grew. In 1978, when the Students’ Movement was established to

deport illegal foreigners from Assam, I could not stop myself from becoming

involved in the movement. I also served as General Secretary of the Students’

Union at the Assam Agricultural University. To get students interested in science, a

few of us formed the Students’ Science Society.

After completing my degree in Veterinary Science, I became an assistant veteri-

nary surgeon in Assam’s Department of Animal Husbandry and Veterinary. I was

posted to the village of Hahim, about 90 kilometers from Guwahati. Transport to

the village was by a public bus, over muddy roads in hilly areas. My first “official

patient” was an elephant with a big, “matured” boil on its back. Theoretically, the

vet should operate and remove the pus, but the elephant was trumpeting in pain

and thrashing around. Many people came to see “the new veterinarian” in action.

There lay my prestige: between an elephant, with which I had no experience, and

the crowd. Finally, I sat on the back of the elephant just behind the boil, while the

mahout, the elephant driver, sat just in front of it, and I was able to make the inci-

sion and remove the pus. After continuous dressing and administration of antibi-

otics it was cured. My life as a veterinarian included many such stories. However,

I found it difficult to work within the constraints of the government machinery,

and resigned my job. For my parents, this was a moment of panic. For me, it was

the opening of a new chapter in my career as veterinarian.

Northeastern India is a land of blue mountains, green valleys, and red rivers.

Nestled in the eastern Himalayas, this region is abundant in natural beauty,

wildlife, flora and fauna, and different ethnic groups. As a veterinarian, I could

help the veterinary services reach out to the farmers at their doorsteps. I started my

journey by training some “para-vets,” who could provide artificial insemination

services to improve the unremarkable local cattle. I also started a business venture

in Guwahati, PET & VET, which provided new and innovative services for pet

lovers. Even today, it stands as the best veterinary clinic in the region. Among my

innovations were facilities for boarding pets and grooming services for dogs.

My professional experiences inspired me to reach the common people and

understand their social causes. To achieve my dreams, I established the Centre for

Rural Development (CRD), a registered society that has engaged in a range of pro-

grams and projects to promote rural development. It focuses especially on animal

husbandry and dairying, and concentrated on increasing livestock production.

Rashtriya Gramin Vikas Nidhi, a national-level organization that provides funding

innovations / winter 2010

37

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

and support, agreed to sponsor a project called the Vet-Aid Center, which CRD

operated in Guwahati and Mirza in the Kamrup district, and in Jagiroad in the

Morigaon district. The center focuses on providing artificial insemination for cat-

tle, deworming calves, vaccinating domestic animals and poultry, and insuring a

timely supply of quality feeds.

The CRD began humbly in 1994, aiming to create social entrepreneurs who

could reach the thousands of poor people in the region. On the basis of this work,

in 2001, Ashoka Innovators for the Public identified and selected me as one of their

Fellows. The three-year stipend that came with the recognition greatly helped me

to concentrate on my work.

November 20, 2004 was an important and happy night for me: the opening of

the Rickshaw Bank at Guwahati, the turning point of the project and also one of

the biggest challenges I faced with this innovative idea. As a vet I had very limited

knowledge about the mechanical and technical aspects of the rickshaw, so I

approached the Indian Institute of Technology (IIT) in Guwahati. I needed not

only to understand the mechanics of the rickshaw but also to have a better design

for the vehicle, including adequate space for advertisements that could help defray

the project’s costs. The prototype was manufactured, and 80 rickshaws were

assembled according to the same dimensions.

To inaugurate the project, the rickshaws were distributed to 80 pullers, but the

next day—November 21, 2004—they came to our office and created chaos. Their

major complaint was that the chain constantly fell off in spite of multiple repairs.

My team started to lose hope; with everyone staring at me, even I became

depressed—I had not expected this outcome on the first day of my dream project.

But I did find a way through this challenge; I motivated my team and assured the

pullers that all the rickshaws would be rectified based on their feedback. Then I

contacted the IIT Guwahati people, and the technical team came to our workshop.

But even after several examinations the solution was not apparent.

We then invited in a group of rickshaw pullers to get their feedback. One sug-

gested that the problem was occurring because the rickshaw chassis had been made

of hollow pipe to reduce the overall weight of the vehicle. After a puller took on

passengers, the pipe tended to bend slightly on the bumpy roads, leading the chain

to constantly fall off. The whole team saw his logic immediately and the hollow

pipe chassis was replaced with one made of solid iron bars; this increased the over-

all strength of the rickshaw and eliminated the problem with the chain. Within 10

days, all the rickshaws had been reconstructed, to the delight of the pullers.

RICKSHAW PULLERS AND THEIR SITUATION

Cycle rickshaws are modified tricycles used extensively as a cost-effective means of

transportation in urban areas. Cycle rickshaw drivers carry passengers or transport

goods, such as building materials or produce.

There are currently an estimated eight million rickshaw pullers in India. These

pullers, or drivers, are among the poorest of employed urban dwellers, with typi-

38

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

cal incomes of 50 to 80 rupees per day (US$1 to US$1.60), well within the target

demographic of the first UN Millennium Development Goal. Many have migrat-

ed to the cities, where they have no support networks and limited options for shel-

ter. They regularly spend the night on the pavement, or on their vehicles. Some

migrants drive rickshaws seasonally, during the off season for agriculture, to help

sustain their families, for example, but a large proportion are year-round drivers.

The work is extremely taxing physically, but requires no formal education.

Thus many pullers are attracted to the prospect of earnings slightly above those of

their unskilled peers. Such an income, however, rarely provides a driver with com-

pensation for an injury, or allows him to save for his family’s current needs, let

alone for the future, when he no longer has the physical ability to move passengers

or goods.

The millions of Indian rickshaw pullers are providing critical last-mile trans-

portation services to people in many cities. But, like me, riders rarely realize that

the pullers actually do not own their vehicles. They do not even lease them. They

hire them, one day at a time, paying high rents and bearing all the risks of doing

such work, including the need for repairs and the pain and loss from accidents.

The decision whether to rent or buy would be a no-brainer for any of us. Daily

rental costs Rs. 25; most pullers stay at the work for over 10 years. A quick back-

of-the-envelope calculation shows that they spend over Rs. 90,000 on rental over

10 years, a little less if the calculation involves net present value. Since a new rick-

shaw costs about Rs. 6,500, the average driver could have bought over 15 of them

in his 10 working years. There is something amiss in this picture, isn’t there?

A key issue is that the rickshaw-pulling community is one of the most margin-

alized sectors of Indian society. Because they have usually migrated from rural

areas to search for work, they lack identity cards or an official residential address.

Earning the equivalent of just over a dollar a day, they are not considered worthy

of credit and would not dream of approaching a bank for credit. Informal money-

lenders charge usurious rates that put them in cycles of debt. Hiring the vehicle for

Rs. 25 per day (20% of their earnings) for a lifetime of activity seems the most fea-

sible option.

With my colleagues at the Centre for Rural Development (CRD), I conducted

sample surveys that highlighted the problems this community faces. In addition to

lack of financing, we heard about the harassment they face in obtaining licenses,

the high costs for repairs and maintenance, the social exclusion they face and the

daily health hazards from pulling over 200 kilograms of weight, in all kinds of

urban terrains.

As migrants, these drivers usually cannot dream of owning a rickshaw in their

lifetimes, since they cannot access credit schemes through the formal banking sys-

tem. With little disposable income, they cannot access basic utilities for themselves

or their families, nor do they have a safe way to save their daily earnings.

Limited savings leave them vulnerable to even minor setbacks, a problem com-

pounded by a lack of insurance and access to fairly-priced emergency loans.

Without any property insurance, they must bear the cost of any accidental damage

innovations / winter 2010

39

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

to their vehicles. If they get sick and cannot drive, they generate no income to pro-

vide for their own care, nor do they have health insurance. When family members

encounter emergencies, they have no savings upon which to fall back. With no

access to formal sources of credit, they are forced to rely on informal moneylend-

ers, who charge usurious interest. Those who get into serious debt are often

harassed to the point that they have no choice but to flee to another locality.

THE INNOVATION: RICKSHAW BANK

Curious why rickshaw design had not been changed or improved in over 60 years,

I asked a friend at the premier Indian Institute of Technology (IIT) in Guwahati

about his views on the design elements of the rickshaws. I wanted to see if we could

reduce the vehicle weight, which was then around 95 to 105 kilograms. IIT took up

the initiative and formed a student team that worked out the technology. We inter-

acted with the IIT engineers, gave them feedback from the pullers, and even took

test drives. Six months later, the result was a rickshaw design that was 25 percent

lighter and had several improved features, including a sun/rain roof and more

storage space, providing more comfort to both pullers and passengers.

The next level of innovation came after my experience in raising funds for our

pilot. Banks were unwilling to give me a line of credit to manufacture the rick-

shaws. After being turned down by every major public or national bank, I finally

decided to tap the corporate social responsibility funding of three large Indian cor-

porations. The result was a win-win solution: each company would support a 100-

rickshaw pilot, and in return we would give them an exclusive 3-year agreement to

advertise on the back of the vehicle at an 86 percent discount. So we sold our pilot

on the basis of the advertisement space.

A complimentary innovation was inspired in late 2003, when I visited

Grameen Bank, met Professor Yunus, and saw the strength of his community

group model in carrying out microfinance activities. Working on a similar model,

I developed the garage system: the pullers have to come to us in groups of five to

request rickshaws. Once they have provided their basic information and we have

done the due diligence, we give each man a rickshaw on a lease-purchase basis.

They have to make payments of 25 rupees per day over a period of 18 months;

once we have recovered our investment and covered our financing costs, we trans-

fer the rickshaw ownership to them. In only 18 months, and usually less, they

become owners of a superior product.

Once the pilot succeeded, the banks offered us financial backing. This was a

bottom-of-the-pyramid opportunity for them: they could continue to earn com-

mercial rates of return while we provided the guarantee and carried out the on-

lending.1

Thus, the rickshaw pullers not only enjoyed access to a rickshaw and the

chance to own it for a lifetime; our program also covered their licensing fee, a uni-

form, and life insurance. They gained a common identity and dignity as a result of

the effort, which also facilitates their inclusion in the social fabric of the cities.

40

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

Subsidizing our Pilot with Advertisements.

Photo by Enrico Mochi.

Core Business Strategies

Five basic strategies drive our project, along with three core social-business princi-

ples. First, the strategies.

1. Provide technologically superior rickshaws to increase customer demand.

Designed by the Indian Institute of Technology in Guwahati and assembled by

CRD’s production center, our rickshaw is lighter and more aerodynamic than the

traditional vehicle, and the seating is safer. This makes it easier on the puller and

more comfortable for the passenger, thus raising the level of consumer demand for

Rickshaw Bank vehicles.

2. Provide rickshaws to pullers in groups of five. In our system, five pullers vol-

untarily form a group and five groups operate from one garage or meeting point.

The pullers, who are members of the Rickshaw Bank, form garages in different

parts of the city to manage their savings, repair the rickshaws, update their busi-

ness records, and collect rent.

3. Collect repayment on a daily basis. Since the puller earns money each day, the

repayment is collected on a daily basis. The Rickshaw Bank applies this revenue to

the cost of the vehicle, plus insurance premiums, drivers’ licenses, uniforms, and

operating costs.

4. Raise funds using a combination of loans and advertisements. Formal finan-

cial institutions provide us with loans at commercial rates; we use grant money to

innovations / winter 2010

41

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

Collecting repayments the Rickshaw Bank way.

Photo by Enrico Mochi.

leverage greater financial access to bank loans and to build internal capacity.

Meanwhile, we sell the ad space on the back of the vehicles to generate additional

revenue. The ad revenue also helps to reduce risk in case pullers cannot manage

their repayments on time.

5. Provide additional loans to the puller community to address other community

needs. Pullers own their rickshaws after a maximum of 15 to 18 months; most

manage to buy them within 10 to 12 months. Their links with the Rickshaw Bank

continue as they seek further loans, negotiate better advertisement rates with busi-

nesses, and access insurance services.

The RB’s innovative response follows three core social-business principles.

First, remove the constraints that prevent drivers from accessing capital and insur-

ance and owning their rickshaws. The RB works to release drivers from the con-

straints that restrict their access to basic financial services, including providing

proof of identify and licensing to protect them from harassment and associated

social stigmas. The RB has negotiated low-cost insurance, covering damage to the

rickshaw, as well as injury to the driver and his passengers. Finally, the RB provides

cash loans to drivers who have established a credit history with it.

Second, increase the community’s capacity to earn and save. The RB’s unique

rickshaw design is more comfortable for passengers and less taxing on drivers,

allowing a single driver to carry more passengers in a single day. Furthermore, after

42

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

he owns his vehicle, a driver may gain access to a stream of advertising revenues

negotiated by the Rickshaw Bank. By collaborating with local institutions, the

Rickshaw Bank has been able to reduce the costs of basic necessities: it arranges

free health care and affordable clothing, and procures cooking gas licenses.

The roughly 25 drivers who are assigned to a given garage or meeting point use

it as a place to make payments, keep records, manage their savings, repair their

rickshaws, etc. Sometimes the meeting point is a pan shop or tea shop. When it is,

the owner of the meeting point provides another point of entrepreneurship and

benefits from the increased earning potential of the driver community. Frequently,

loans from the RB support these entrepreneurs. After a driver gains ownership of

his rickshaw, all future income goes into his own pocket, to his family, and eventu-

ally back into the local economy.

Third, ensure that the program is sustainable and scalable. In the four and a half

years it has been operating, the RB has benefited 4696 rickshaw drivers directly and

23,480 people (dependent family members) indirectly. The project is now ready to

move forward on a much greater scale. The RB sees the driver community as an

underserved market and believes that offering market-oriented solutions will

enable it to reach the most drivers, while preserving the dignity of the population

it seeks to serve.

The Rickshaw Package

As the bank has evolved, we have been able to offer an expanding package of prod-

ucts and services.

Access to Asset Ownership

The Rickshaw Bank primarily provides financing so that rickshaw drivers can own

their vehicles. Rather than providing cash loans to drivers, the bank directly lends

newly manufactured rickshaws. The asset remains under the RB’s legal ownership,

providing security for the loan. Legal title is transferred after full repayment.

A Fairly-Priced, Technologically-Superior Cycle Rickshaw

The RB provides technologically superior rickshaws at fair-market prices, close to

cost. The current model is assembled at the RB’s production center. These lighter,

safer vehicles ease the job of the driver, increase consumer demand for Rickshaw

Bank vehicles, and allow drivers to carry more fares in the same day.

Licenses and Training on Rules and Regulations

The RB believes that formally-established legal status for drivers will reduce

harassment and increase the dignity of the community. Therefore, in each locality,

the RB forms a partnership with the municipal corporation and police to provide

licenses to rickshaw drivers in exchange for training them about local traffic rules

and regulations.

innovations / winter 2010

43

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

Madhab Kalita and his family.

Photo by Enrico Mochi.

Uniforms

The RB provides two uniforms to each driver along with his new vehicle. The bank

believes that attractive uniforms help passengers to identify drivers affiliated with

the Rickshaw Bank; they also reduce harassment and further increase the dignity

of the rickshaw-driver community.

Property and Casualty Insurance

Traditionally, rickshaw drivers had no access to property insurance; to cover the

cost of significant accidental damage to their vehicles, they often turned to infor-

mal money-lenders, who lend at extremely high rates of interest. Thus drivers

risked falling deeply into debt. To protect against this vicious cycle, the RB

arranged with insurance companies to provide property and casualty coverage for

drivers. Each rickshaw is insured for Rs. 9,000; the driver is insured against injury

or death for Rs. 50,000, and passengers are insured for Rs. 10,000 each. Realizing

that our vehicles are insured, passengers are more likely to hire them.

The Rickshaw Bank does not provide direct coverage, but it collects the premi-

ums and files claims on behalf of the drivers. Currently, the bank has formed part-

nerships with four leading national insurance companies: Oriental Insurance, New

India Assurance, United Insurance, and Royal Sundaram Insurance Company.

44

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Determination Shapes Destiny

A dignified livelihood was his dream. He hankered after work that could provide

him a handsome income and respect. Twenty years earlier, when he first migrat-

ed to Guwahati city in search of a job from a flood-affected village in Nalbari

District, Madhab Kalita, then at age 56, tried to earn money as a daily laborer.

But uncertainty dogged him, and his earnings could not support his family of

five. After a year, he started pulling a rickshaw, which he leased from a trader for

Rs. 20 per day. After paying the owner, he was left with around Rs. 30 to Rs. 50,

hardly enough to buy food. In his 18 years pulling a rickshaw, he could not think

of having one of his own. Instead, he got trapped in loans at usurious interest

rates when he borrowed from the rickshaw owner. He and his family live in a

dilapidated house on a hillock in the outskirts of city. Naturally, they all require

food and clothing. His wife worked as a domestic helper in the city, but still they

could not meet their family’s needs.

Finally, in 2005, he saw a ray of hope. The field-level workers of the Rickshaw

Bank project told Mr. Kalita about the different facilities the project provided. At

first, he couldn’t believe his ears: a poor man could be a sole owner of a rickshaw

after a year of paying Rs. 25 to 30 each day. On July 21, he grabbed the opportu-

nity to join the project. Wearing a neat, clean uniform and pulling an innovative

model of rickshaw, Mr. Kalita was determined to shape his own destiny. “The

rickshaw was comfortable for the passengers as well as the driver and that

enabled me to earn at least Rs. 200 a day,” he stated. Eventually, he became a full

member of the Rickshaw Bank and even started promoting the project in the

city. He encouraged many youths to join the project instead of searching for a

meager income elsewhere. Now, having secured ownership of his first rickshaw,

he has bought a second one through the project and he leases it out to a neigh-

bor. Meanwhile, his wife is close to owning a bhogjan, a fast-food cart. Together,

they now earn at least Rs. 8,000 per month. Six months ago, the Rickshaw Bank

also released a loan of Rs. 40,000 to renovate their house, which let them make

great improvements. Their sons and daughter are being educated, and their

neighbors respect them. Thus, Mr. Kalita and his wife shaped their destiny with

determination under the aegis of the Rickshaw Bank. What inspired him so

much? No one knows, but at age 76, he still goes out with his rickshaw, wearing

a uniform and smiling. He is an asset to the Rickshaw Bank, a source of inspira-

tion to the whole rickshaw-puller community, and a living example of earning a

dignified livelihood in an unorganized sector.

Advertising

A rickshaw provides a mobile billboard for private advertising. Attractive rick-

shaws designed to accommodate large ads can serve as an appealing and cost-effec-

tive means of advertising for both local and national businesses. To provide such

advertising, the RB has formed partnerships with four large firms: Oil & Natural

Gas Corporation, Indian Oil Corporation, Hindustan Leaver Limited and Punjab

National Bank. The Rickshaw Bank keeps 100 percent of advertising revenue to

innovations / winter 2010

45

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

subsidize operating expenditures until the driver achieves ownership. After this

point, the bank turns over 65 percent of the advertising revenue to the driver,

retaining the other 35 percent in exchange for arranging and producing the adver-

tisements. This gives drivers significant potential to enhance their income streams.

LPG Connectivity

During discussions with the driver community, RB staff identified a priority con-

cern: access to cooking gas. Because many drivers are migrants, and do not have

proof of address or investment capital, they cannot access connections to LPG

(Liquefied Petroleum Gas). Instead, drivers and their families typically use

kerosene and wood as cooking fuel. This issue was brought to the attention of the

Indian Oil Corporation, and after a series of discussions, the IOC agreed to con-

sider an identity card issued by the Rickshaw Bank as sufficient proof of address to

authorize an LPG connection. Loans from the RB provide partial support for the

investment.

Cash Loans

Once a driver has fully repaid his loan, and on time, he may apply for a cash loan

to provide for a range of family needs: children’s education, health emergencies,

the LPG connectivity mentioned above, land or housing purchases, etc. Cash loans

are typically under Rs. 15,000 and must be repaid in less than a year. Loans carry

1.5 percent monthly interest rates, and 0.5 percent monthly service fee. Pullers

with a good repayment history may be eligible for larger loans. The RB is current-

ly in discussions with the National Housing Bank of India to expand the housing

loan program.

Health Care Services

The Rickshaw Bank has also arranged for low-cost access to medical benefits for

including their parents, at various hospitals.

drivers and their families,

Arrangements have been made for free eye treatment (including surgery) at

Shankaradeva Netralaya, a leading eye hospital in Guwahati. The RB has also start-

ed a health unit to help the community with daily problems. And, through con-

tracts with pharmaceutical companies, it purchases generic medicines and makes

them available at affordable prices.

Clothing Distribution, AIDS Awareness, and Job Opportunities

In collaboration with GOONJ, a Delhi-based NGO, the RB has initiated a scheme

to distribute free and reduced-price clothing to the drivers and their families. With

support from the AIDS Control Society of Assam, the bank has made free con-

doms available to the drivers to promote family planning and safer sex. Finally, the

bank encourages selected drivers to apply to be field collectors, who collect other

drivers’ daily repayments. This system improves the Rickshaw Bank’s relationships

46

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

and familiarity with the driver community, and gives drivers an opportunity to

move into alternate avenues of employment.

The Rickshaw Bank Business Model

The Rickshaw Bank’s business model is based on revenue from loan repayments,

advertising revenues, and a growing portfolio of other services and fees. This

income covers our manufacturing, management, and finance costs.

The Revenue Drivers

Repayments from rickshaw pullers. The daily payments from pullers are a great

source of liquidity for the organization and the project. The mechanism of a com-

mon liability group ensures that approximately 85 percent of payments are made

on time.

Advertisement revenue. The space on the back of each rickshaw is as large as a

typical billboard along a street, but costs only a fraction as much to rent. This

makes it attractive both for large businesses and for small businesses that want to

post an ad for only a week or month.

Additional loan repayments. Many members with good credit history are eligi-

ble for other types of loans, and they make their repayments on a pre-agreed cycle.

Once the puller becomes the owner of his rickshaw, he has access to the second

phase of loans to clear his debts with the money lenders (at interest rates that range

from 10 percent to 15 percent per month). After he repays the second loan, he can

avail himself of those in the third and later phases to pay for household goods, his

children’s education, a marriage, or house repairs or renovation.

Member deposits and membership fees. The organization also obtains revenue

through a non-refundable deposit on the rickshaw, paid in one or two install-

ments, and a refundable membership deposit.

Revenue from franchises in return for capacity-building support. The RB believes

that the franchise model will make it possible to reach millions of poor people, and

quickly, through relationships with credible partners. For its technical support, RB

would derive a small percentage service fee, which would decline over the period

of business volume. As we scale up, we expect that the revenue from this stream

will grow.

Support from international donor organizations. Donors play a key role in pro-

viding funds that support initial set-up, capacity-building, and knowledge assimi-

lation and transfer. They are also supporting us with funds to deposit in commer-

cial banks and thus providing the leverage we need to engage in further outreach

with rickshaws. Donors are also investing in pilot models, such as testing of the

franchise model.

The Cost Drivers

The other half of the equation is our costs, for manufacturing, administration, and

finance.

innovations / winter 2010

47

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

Manufacturing vehicles. Currently, we produce rickshaws in-house so we can

influence the design. So far, we have produced them on a fairly small scale; howev-

er, our manufacturing costs are likely to increase when we outsource the produc-

tion, though it may fall as we increase our outreach. In some cities in the north-

east, production costs are higher because of higher charges for freight and cross-

border VAT payments. In comparison, in cities such as Uttar Pradesh, access to

materials is easier and cheaper.

Administrative and operational expenses. We believe that 1,200 is the maximum

number of pullers who can be served by one branch coordinator, but we have not

been able to reach this number because we need better software to reduce overhead

and paperwork. Over the past year we have decided to invest in such software, as

we have consolidated our progress, and we are now poised to expand.

Finance and insurance. The Rickshaw Bank’s access to finance has become sig-

nificantly easier, as many national banks have offered to extend loans at their com-

mercial interest rate. The RB pays premiums to insurance companies for the

pullers. It has not integrated an in-house product for this insurance, but instead

negotiates a competitive group rate with the companies.

Our Emerging Franchising Model

The Rickshaw Bank project has taken a new turn in a partnership with the

American India Foundation (AIF). AIF has provided capacity building and sup-

port in the form of a first loss deposit guarantee (FLDG) to leverage loans from

various banks. The CRD organized a meeting in Guwahati with AIF and various

organizations to share the experiences of the RB project. Out of the 16 NGOs we

invited, five came forward to start RB projects under a partnership model with

CRD in various locations in India. I introduced AIF to the Punjab National Bank,

whose chairman and managing director, Dr. K. C. Chakrabarty, was very respon-

sive. The PNB, AIF and CRD made a three-way agreement to expand the RB in

three cities in Uttar Pradesh, where CRD provided hands-on support to the new

NGOs to establish the assembly unit and to start up other related activities. In

2008, we launched the RB project in three cities in Uttar Pradesh: Varanasi

(February 2), Allahabad (June 1), and Lucknow (June 4). Ultimately, we handed

the projects over to Jan Mitra Nyas, Arthik Anusandhan Kendra, and Bharatiya

Micro Credit respectively.

Based on this experience, CRD plans to replicate the franchise model by creat-

ing and promoting new entrepreneurs. By becoming a franchisee, an entrepreneur

can save much of the time and resources needed to evolve a successful business

model. Thus franchises drastically reduce the chances of failure and save valuable

time and resources. Statistics reveal that the failure rate in business ventures is

much lower among franchises than among individual start-ups.2

48

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

Location of Rickshaw bank operations.

SCALING UP: EXPANDING GEOGRAPHICALLY AND ADAPTING

PRODUCTS AND SERVICES

Although we have now proven our model and are well into the growth phase, the

last four and half years have not been without challenges. But the initial skepticism

has evaporated, as the pullers’ repayments proved that they are creditworthy, and

as governments, commercial banks, and grant makers came to see the value of our

business model.

As we scale up, however, and especially as we do so in different cities and across

cultures, we see the need for a more standardized product and a structure that can

support the growth. Moving out of our home base of Assam put us in new territo-

ry, where we needed to get acquainted with different cultures and practices.

Realizing that we do not have the internal capacity to undertake the expansion

ourselves also pushed us to search for partnerships.

The project can be scaled within a given city, in response to the demand that

arises as drivers see how satisfied their peers are with the Rickshaw Bank projects.

The project in Guwahati, for example, has now established satellite offices in its

suburbs to meet the need there. The project can also be scaled across cities, as

NGOs, led by the bank, replicate the project in new cities.

The issue of scaling up has been much on my mind recently. Given our limit-

ed resources and internal capacity, we were reaching out to only a small propor-

innovations / winter 2010

49

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

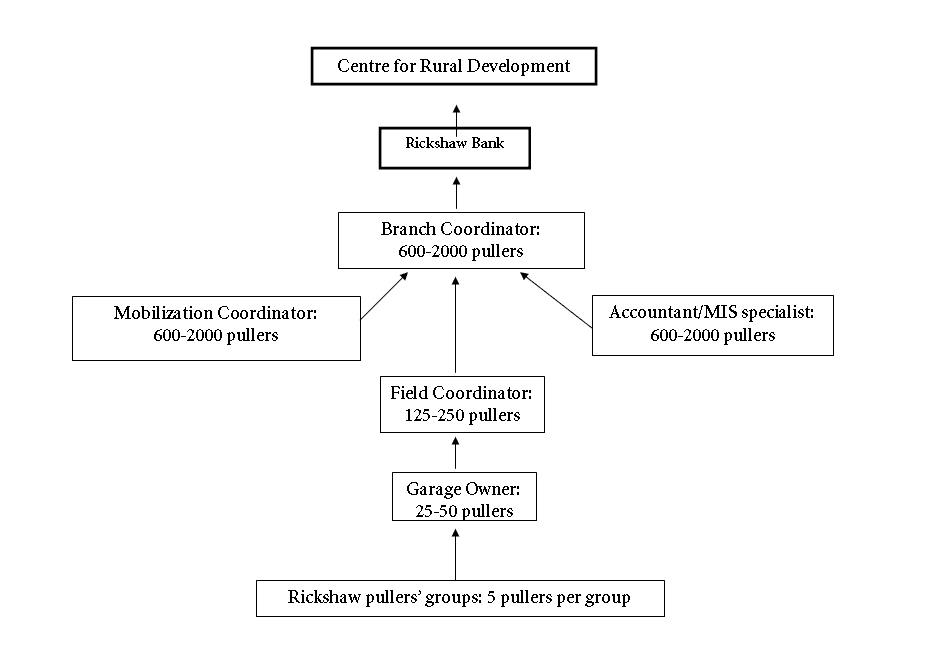

Figure 1. Daily Operations of CRD and Its Branches and Franchisees.

tion of India’s eight million rickshaw pullers. Not satisfied to reach such a small

fraction of people, the RB developed a unique partnership/franchise model. Under

the franchise system, CRD shares its vision, arranges financing, and provides

expertise to a local microfinance partner, which in turn provides a local network

of field and branch coordinators. The franchisee branches developed in Lucknow,

Allahabad, and Varanasi are examples of this arrangement.

To expand nationwide, we provide hand-holding support to interested NGOs

or entrepreneurs who want to begin working with pullers at their local level.

However, as we start our new expansion, we want to develop an operational sys-

tem, so either we identify an entrepreneur and provide him full support to carry

out the production and assembly for us, or we support our partner organization in

setting up its own production unit with all necessary facilities.

The day-to-day activities operate with a team, as shown in Figure 1.

How far can we scale the model? No official records state the number of rick-

shaw pullers in India, but people frequently mention a rough estimate of eight mil-

lion. On average, about five others depend on each puller, so 40 million people may

be directly related to this source of income. Similar figures apply to others who use

carts, including vendors of fruits and vegetables, sugarcane juices, fish, drinking

water, and other foods and goods.

50

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

THE IMPACT OF OUR WORK

Despite the challenges I have discussed here, what motivates me to continue is the

daily impact that I witness on the rickshaw-puller community. Although the pride

of ownership reflected on the faces of the pullers provides me with great satisfac-

tion, we have had other kinds of satisfying influence on both the community and

other stakeholders. Our impact can be seen in several ways.

Economic Mobility

The services that the RB offers were designed to have a positive impact on all

aspects of the triple bottom line. First, we have enabled pullers to own a rickshaw

in a reasonable timeframe. Before we launched this program, few could do so

because of the high daily fees and interest rates charged by corrupt businessmen.

Second, pullers can now make more money because they pay less each day for the

vehicle, and because the newer vehicles let them carry more passengers each day.

Third, pullers now have access to a sound financial organization where they can

borrow money for other ventures.

Social Status

The RB has also had a positive impact on the social conditions of pullers. It has

offered eye care for them and their families and driving insurance for him, and has

made the business more respectable. Through a combination of uniforms and

monthly discussion forums and peer groups, it has instilled a sense of pride among

pullers regarding their line of work. And passengers, especially the elderly and

those with children, prefer Dip-Bahan rickshaws because of their unique design

and the organizational identity attached to it.

We now have a total of nearly 5,000 clients throughout India, 1,700 of whom

have become owners, and many others are on their way to achieving that status in

coming months. The six cities of Agartala, Chennai, Surat, Varanasi, Allahabad,

and Lucknow all have 150 to 450 clients.

Governance

The project has improved law and order within the community in several ways.

First, by making licenses available to pullers, the RB has enabled the government

to better monitor its citizens and gain tax revenues. Second, it has reduced corrup-

tion because fewer policemen can now extract bribes from pullers for not having

proper registration. Third, it has created safer roads by offering driving tips to

pullers.

As a result of its comprehensive interventions, the RB is enabling pullers to

increase their standard of living and become more financially independent. Thus

it is a prime example of how an NGO can have a tremendous impact on the local

population by nurturing a native capability that already exists in the community

and making it financially sustainable.

innovations / winter 2010

51

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

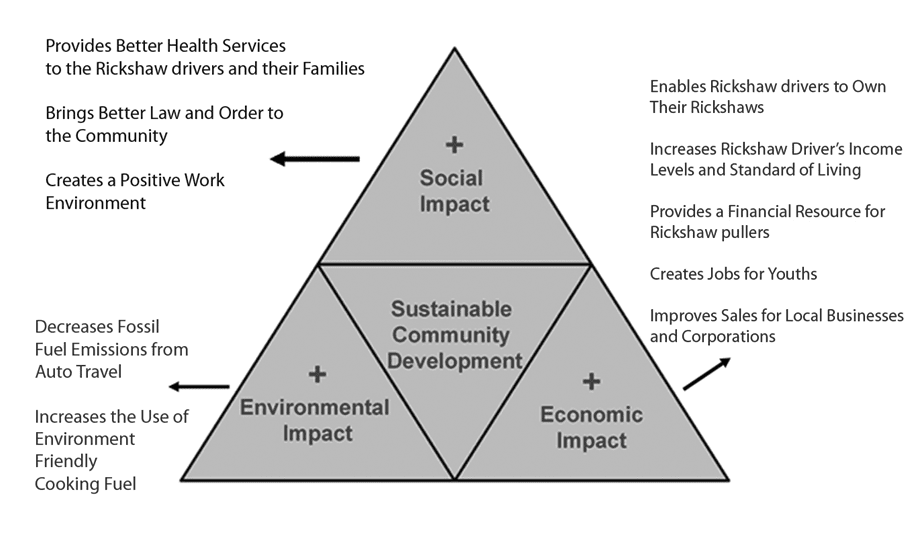

Figure 2. Rickshaw Bank’s Social, Environmental, and Economic Impact.

I feel proud that a little change in the design of rickshaws and delivery systems

made a large and visible impact within the rickshaw puller-community. Various

educational, financial, technical, and social institutes are now showing deep inter-

est in the overall growth of both the rickshaw and the puller. I envision that simi-

lar changes can be made in the lives of other people who depend on slow-moving

vehicles, including those who sell vegetables, fruit, fish, and fast food from carts.

We have already taken a further step in this direction by providing hath lorries, or

hand-pulled carts, to textile vendors at Surat in Gujarat. At Guwahati, Assam, we

have also introduced better-designed carts for selling fish and other food, and dis-

posing of garbage. A newly-designed cart for selling vegetables and fruits will soon

be rolling on Indian streets.

COLLABORATION WITH THE INDIAN GOVERNMENT

The government’s Department of Science and Technology has joined hands with

the Rickshaw Bank as part of the Science Technology and Entrepreneurship

Development (STED) project. It recognizes that the newly-designed rickshaw,

combined with the service delivery mechanism, is a successful tool for creating a

new generation of entrepreneurs. Within this project we envisage generating 80

entrepreneurs in 16 states of India within a four-year timeframe. A dedicated pro-

fessional team is already in action. We plan to identify potential entrepreneurs in

80 districts and cities and to support them in three ways—technically, financially,

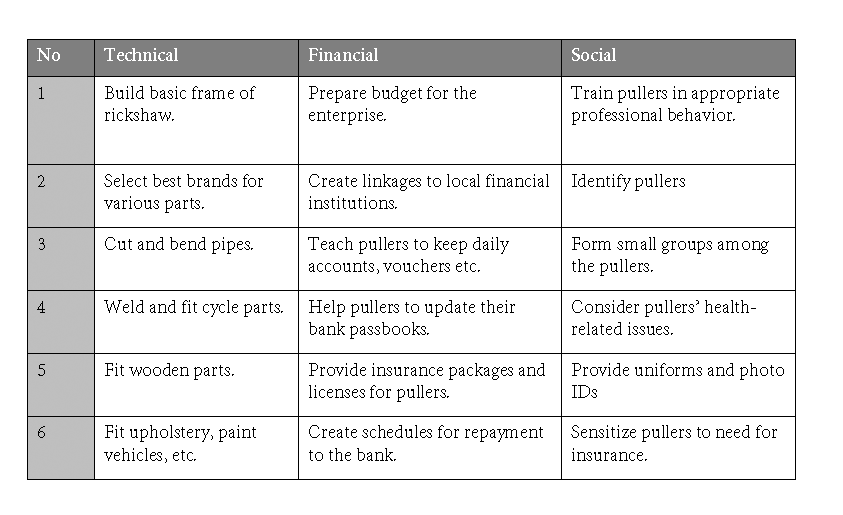

and socially—as they replicate RB activities. Table 1 shows the support the STED

project will provide entrepreneurs.

52

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

Table 1. Examples of Technical, Financial and Social Support through STED.

STRATEGY FOR THE FUTURE

In the next three to five years, I intend to focus on three initiatives. As an organi-

zation we need to tap equity capital to fund our scale-up efforts. Some immediate

issues in the Indian legal context suggest we will need to incorporate as a private

company and transition away from our non-profit, non-government status.

Simultaneously, we will be building internal capacity (human capital, a new set of

advisors, responsive systems and processes) to manage this change, as we bring in

a new set of stakeholders to participate in our growth.

Our second focus will be on making the Soleckshaw, our solar rickshaw, com-

mercially viable. We would like to be ready once we have overcome its technologi-

cal problems. We will be thinking of ways to lower its cost through partnerships

with local governments and banks.

As a team we have been extremely open to innovation; we’ve also been sensi-

tive to how the local demand has differed from city to city. In the story I tell here,

the Indian government showed an interest in piloting a solar-powered rickshaw in

Delhi.

The recently-launched initiative, partnering with the Central Mechanical

Engineering Research Institute and the Council of Scientific and Industrial

Research, was another important milestone for the Centre for Rural Development.

Soleckshaw, a pedicab, is a vehicle for urban transport that is operated by pedaling,

but has an assistive motor that emits zero carbon. It was launched on October 2,

2008 at Chandni Chowk, Delhi. Among those gracing the program at the launch

were the honorable Chief Minister of NCT (Delhi, or National Capital Territory)

innovations / winter 2010

53

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Pradip Kumar Sarmah

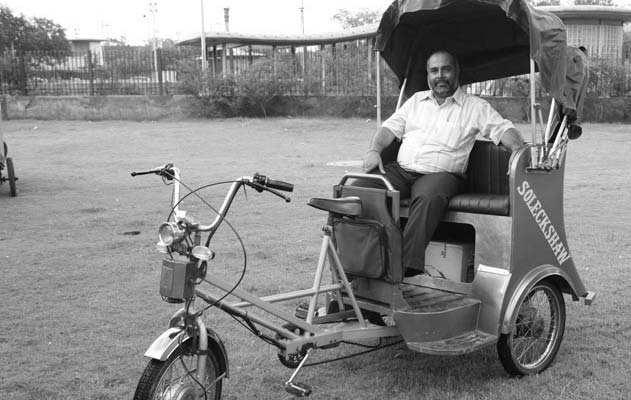

The author in a Soleckshaw.

Photo by Enrico Mochi.

Ms. Sheila Dikshit, and Sri Kapil Sibbal, then the Minister of Science and

Technology and Earth Sciences.

Soleckshaw is now in its pilot phase. At present, seven Soleckshaws, in three

models, are in use. CRD regularly reports their daily progress to the concerned

authorities. Their cost has not been finalized as commercial production has not

begun, but passengers and drivers both believe it will be revolutionary. The design

provides shade and comfort for passengers, and the motor relieves some of the

pullers’ drudgery. However, there is some way to go before this reaches commer-

cial scale.

A third, and integral, part of our organization strategy is to improve the over-

all lives and livelihoods of the pullers. We are working with an external group of

architects and social developers to offer low-cost housing.

WE’RE DOING OUR PART, NOW SOCIETY MUST JOIN US

In the technology-driven world of India’s most populous city, the sight of a prim-

itive caravan being pulled by a weary man is certainly surprising but not uncom-

mon. Around 1880, rickshaws appeared in India, first in Simla and then, 20 years

later, in Calcutta (now Kolkata). One would have expected rickshaws to disappear

with the fast growth of modern motorized transportation. Instead, their numbers

have increased phenomenally in the last couple of decades. In the absence of any

alternative mode of transportation for short distances, the rickshaws emerged as a

54

innovations / winter 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023

Empowering the Poor through Asset Ownership

vital public service. But their pullers still have to bear the burden of low wages and

subhuman living conditions.

Cycle rickshaws provide a much-needed and valuable public service. In the old

city area and in some congested areas meant for the poor where the roads are too

small for motorized vehicles, cycle rickshaws are the only available means of trans-

portation. In addition, they are convenient and available at virtually anyone’s

doorstep. They meet the need for urban mobility in middle- and lower-middle

income neighborhoods, and provide a low-cost way to transport household goods

and furniture. Even today, a kilometer-long ride in a cycle rickshaw costs no more

than five rupees, compared to 10 to 15 rupees for the same distance in an auto rick-

shaw. And cycle rickshaws reduce air pollution and climate change by avoiding

emissions.

Rickshaws can play a positive role in modern transport systems when mobili-

ty and a clean environment are the basic concern of policy makers. But when their

requirements are poorly understood and facilities are not built for them, the result

is congestion and inconvenience for all vehicles. Designing and building appropri-

ate roads and parking facilities for them in cities will also facilitate the movement

of other vehicles—and will enhance the positive role that rickshaws and other

non-motorized vehicles can play in a city’s transport system.

But pullers still have to bear the burden of low wages and subhuman living

conditions. Our pullers will probably get a better deal when our planners and gov-

erning authorities recognize that rickshaws are a non-polluting, cheap, and effi-

cient mode of public transport that provides employment for millions of people.

APPENDIX. RECOGNITION FOR RICKSHAW BANK

Rickshaw Bank has attracted the attention of organizations worldwide for its innovation and its

impact. In November 2003, it won the Citizen Base Investment Award 2003 for its concept at the

National Stock Exchange Building in Mumbai. In November and December of 2005, IIM Bangalore

selected us for its Microfinance Incubation Program. On April 5, 2006, it was celebrated at the

National Press Club in Washington D.C. as part of the Changemakers Innovation Award

Competition: Market-Based Strategies that Benefit Low-Income Communities. On April 7, 2006, in

New Delhi, it received the Micro Finance Process Excellency Award from Planet Finance and the

ABN Amro Bank. On November 13, 2006, in Singapore, it won an Asian Innovation Award. On April

25, 2007, at Hyderabad, RB won third prize in the Srijan 2007 Microfinance Business Plan

Competition. On July 27, again in Hyderabad, RB was a finalist for the Micro Insurance Awards. On

August 15, 2008, it won the Assam Chief Minister’s Best Community Action Development Award

for 2008. On March 30, 2009 RB won India NGO Award, 2008 for the medium category from the

Eastern Region by the Resource Alliance and Nand & Jeet Khemka Foundation. Rickshaw Bank was

also awarded as Best Innovative Project of the year, 2008.

1. Onlending is when an organization lends money that they have borrowed from another

organization or person.

2. http://articles.directorym.com/Franchise_System_Failure_New_York_NY-r852283-

New_York_NY.html.

innovations / winter 2010

55

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/1/35/1838394/itgg.2010.5.1.35.pdf by guest on 08 September 2023