Mobile Payment in China: Practice

and Its Effects*

Yiping Huang

National School of Development / Institute of Digital Finance

Peking University

yhuang@nsd.pku.edu.cn

Xue Wang

National School of Development / Institute of Digital Finance

Peking University

xwang2017@nsd.pku.edu.cn

Xun Wang

National School of Development / Institute of Digital Finance

Peking University

xunwang@nsd.pku.edu.cn

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

Abstract

This paper offers a comprehensive review and careful assessment of China’s mobile payment busi-

ness. With broad access, low costs, and reliable transactions, mobile payments are creating a revolu-

tion of financial inclusion, changing people’s daily lives and commercial business models. This study also

confirms that mobile payment improves risk sharing among individuals and increases entrepreneurial

opportunities. These mobile payment successes can be traced to three key factors: supply shortages

of alternative payment services, a friendly regulatory environment, and recent technological develop-

ments. A number of outstanding issues remain, however, including data ownership, data inequality, and

regulatory shortcomings.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

1. Introduction

Mobile payment services, dominated by two leading players, Alibaba’s (now owned

by Ant Financial Services) Alipay and Tencent’s WeChat Pay, have become a fixture in

China’s daily lives and businesses. Both players have built eco-systems around their mo-

bile payment tools. People use Alipay or WeChat Pay to purchase goods, order coffee and

* Xun Wang is the corresponding author. The authors are grateful for the financial support by Na-

tional Social Science Foundation of China (project no. 18ZDA091) titled “Innovation, Risk and Reg-

ulation of China’s Digital Inclusive Finance.” The authors also would like to thank the anonymous

referees, Wing Thye Woo, Ninghua Zhong, and Iikka Korhonen as well as other participants at the

AEP Meeting on 18 September 2019 at Keio University for their insightful discussions and com-

ments. The authors declare that they do not have relevant or material financial interests related to

the research reported in this paper.

Asian Economic Papers 19:3

© 2020 by the Asian Economic Panel and the Massachusetts Institute of

Technology

https://doi.org/10.1162/asep_a_00779

Mobile Payment in China: Practice and Its Effects

food delivery, pay electricity bills, book taxis, buy air tickets, make donations, transfer

money, and even invest in financial products. Almost all commercial outlets in China, in-

cluding streetside stores, widely utilize mobile payment services’ Quick Response (QR)

codes to conduct business. Chinese tourists also use mobile payment services to purchase

souvenirs and luxury goods at international airports and major department stores around

the world. In 2018, the mobile payment service made a total of 60.5 billion transactions,

an increase of 61.2 percent from a year before, according to report by the People’s Bank of

China (PBOC).1

China was not the original inventor of mobile payment business—M-Pesa in Kenya and

PayPal in the United States are both older and well known. But Alipay and WeChat Pay

have turned mobile payment into a global phenomenon, attracting massive interest from

business practitioners, academics, and policymakers around the world. Why did it grow?

Can it be replicated in other countries? What are the major economic and financial con-

sequences? How should it be regulated? There is a growing literature addressing these

questions and more, looking at the effects of mobile money adoption on household welfare

(Aker et al. 2016; Munyegera and Matsumoto 2016; Beck et al. 2018), saving behavior (Aker

et al. 2016; Mbiti and Weil 2013), informal insurance network and risk sharing (Jack and

Suri 2014; Klapper and Singer 2014; Riley 2018), financial inclusion (Demirguc-Kunt et al.

2018), and monetary frameworks (Mbiti and Weil 2013).

The success of China’s mobile payment business could be attributed to three factors: a sup-

ply shortage of payment services, a friendly regulatory environment, and recent techno-

logical developments. With broad access, low cost, and reliable transactions, people’s daily

lives and commercial business models have been changed significantly. The empirical in-

vestigation also provides convincing evidence that mobile payment not only promotes

household entrepreneurship in China, but also enhance the ability of households to smooth

risks when experiencing negative idiosyncratic income growth shocks. Nevertheless, al-

though revolutionary financial inclusion has been created, China’s new mobile payment

business still needs to evolve further to address outstanding issues, including consumer

protection, data inequality, and regulatory arbitrage.

The rest of this paper is structured as follows. In the next section we introduce the inno-

vation and development of mobile payment in China. Section 3 reviews the literature re-

garding the development and effects of mobile money in different countries. In Section 4

we provide evidence that mobile payment system has been complementary to the tradi-

tional bank-based financial sector by improving individual and household risk sharing and

promoting entrepreneurship in China. Section 5 concludes.

1 Retrieved from: http://www.pbc.gov.cn/goutongjiaoliu/113456/113469/3787878/index.html;

accessed on 10 January 2020.

2

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

2. Background

In retrospect, 2005 might be identified as the first year of China’s mobile payment indus-

try, with Alipay coming online at the very end of 2004. Since then, mobile payments have

grown at a truly astonishing pace. A number of events played important roles in this devel-

opment. First, the release of Apple’s first iPhone in January 2007 marked the beginning of

the new era of smartphones, making it possible to use mobile payment services anywhere,

any time. Second, the success of Ant Financial’s money market fund Yu’E Bao significantly

boosted awareness of, and enthusiasm for, the financial technology (fintech) industry, in-

cluding mobile payment. Third, the distribution of red (cash) envelopes on WeChat Pay

during the Chinese New Year holiday in 2014 became almost viral and attracted hundreds

of millions of new users. And finally, the adoption of the QR code for mobile payment

made it possible for any businesses, formal and informal, to use mobile payment service

by simply printing out the code on a piece of paper.

In recent years there has been a rapid expansion of China’s mobile payment business, in

terms of active users, number of transactions, and transaction values. The number of active

users of Alipay increased from a little over 100 million in 2013 to 900 million in 2018, and

that of WeChat Pay grew from about 350 million to 1.1 billion. The total transaction value

jumped from RMB 14.5 trillion in 2013 to RMB 277.4 trillion in 2018, recording an annual

growth rate of 80 percent (Figure 1). The number of mobile payment transactions reached

60.5 billion in 2018, rising by 61 percent from the previous year. The share of mobile pay-

ment in total non-cash payment value rose from less than 1 percent in 2013 to 7.4 percent

in 2018, and the share of mobile payment in the total number of non-cash payment trans-

actions increased from 3.3 percent in 2013 to 27.3 percent in 2018. Some mobile payment

platforms also evolved into large ecosystems, covering a wide range of businesses such as

funding, financial management, credit reference and big data.

China has consistently ranked number one in mobile payment markets (whether in trans-

action volume or penetration rate) in the world. The proportion of adults using mobile

payment in China was as high as 76.9 percent in 2017, and even in rural areas the propor-

tion was 66.5 percent. According to Ipsos statistics, the penetration rate of mobile payment

in China was 77 percent in 2016, compared with rates in the United States, UK, Germany,

and France of 48 percent, 47 percent, 48 percent, and 38 percent, respectively. The penetra-

tion rate in Japan was only 27 percent. The leapfrogging of China’s mobile payment reflects

the underdeveloped social credit system in China. In advanced economies like the United

States, the primary method of payment is the credit card. Although China has the largest

credit card system in the world with nearly 7.6 billion cards, according to PBOC, 91 per-

cent of these are debit cards. The percentage of the population aged above 15 years with

a credit card was only 20.8 percent in China at 2017, significantly lower than that in Japan

3

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Figure 1. Transaction value of mobile payment in China, 2013–18 (RMB trillion)

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: CEIC; PBOC.

(68.4 percent), the United States (65.6 percent), the United Kingdom (65.4 percent), and

South Korea (63.7 percent).

The development of mobile payment services has contributed significantly to financial

inclusion. Delivering responsible and sustainable financial services, including payment

services, to small and medium-sized enterprises (SMEs) and low-income households is

a global challenge (Nanda and Kaur 2016; Demirguc-Kunt et al. 2018). Mobile payment

has overcome many difficulties, reaching massive numbers of SMEs and individuals. The

Mobile Payment Coverage Sub-Index of the Peking University Index of Digital Financial

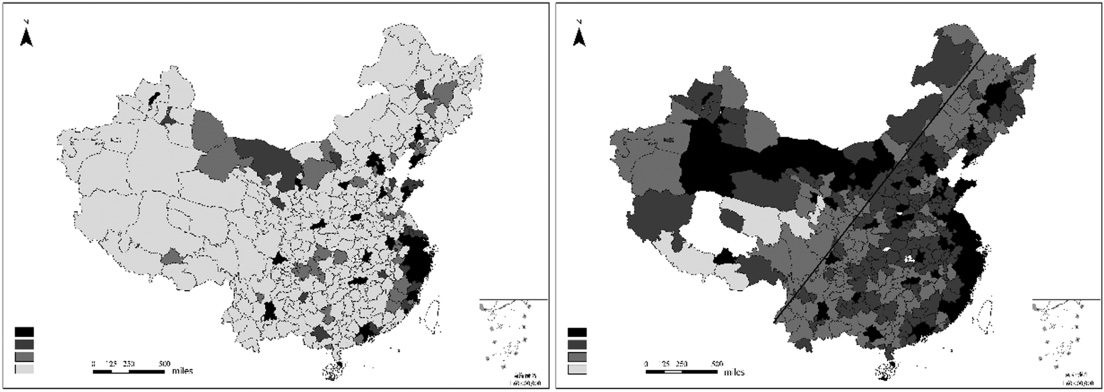

Inclusion showed significant convergence among Chinese prefectures between 2011 and

2018 (Figure 2). In 1935, economic geographer Hu Huanyong drew a line on China’s map

from Heihe in Heilongjiang to Tengchong in Yunnan, which was later known as the Hu

Huanyong Line (The line in the right panel of Figure 2).2 On the right side of this line, about

46 percent of total land area supported 96 percent of the population, and on the left side

of the line, about 54 percent of the land area supported only 4 percent of the population.

During the past decades, these numbers have changed somewhat, but the basic point of

extreme population concentration in one-half of the country’s geography remains largely

true. This was also true for the picture of mobile payment coverage in 2011 (the left panel

2 Hu Huanyong elaborated first presented the idea of this Hu Huanyong Line in the journal article

“Distribution of China’s Population” in Journal of Geographical Sciences (in Chinese) in 1935.

4

Asian Economic Papers

Mobile Payment in China: Practice and Its Effects

k

r

a

d

n

i

)

w

o

l

o

t

h

g

i

h

m

o

r

f

(

d

e

r

o

l

o

c

n

e

h

t

e

r

a

h

c

i

h

w

,

e

g

a

r

e

v

o

c

t

n

e

m

y

a

p

e

l

i

b

o

m

f

o

s

l

e

v

e

l

o

t

g

n

i

d

r

o

c

c

a

s

p

u

o

r

g

r

u

o

f

o

t

n

i

d

e

d

i

v

i

d

e

r

a

r

a

e

y

h

c

a

e

s

e

r

u

t

c

e

f

e

r

p

l

l

A

.

e

n

i

l

g

n

o

y

n

a

u

H

u

H

e

h

t

s

i

h

p

a

r

g

t

h

g

i

r

e

h

t

n

i

e

n

i

l

e

h

T

:

e

t

o

N

.

y

a

r

g

d

n

a

,

k

c

a

l

b

t

h

g

i

l

,

k

c

a

l

b

,

k

c

a

l

b

.

)

g

n

i

m

o

c

h

t

r

o

f

(

.

l

a

t

e

o

u

G

:

e

c

r

u

o

S

d

n

a

)

t

f

e

l

(

1

1

0

2

,

e

r

u

t

c

e

f

e

r

p

y

b

x

e

d

n

i

–

b

u

s

e

g

a

r

e

v

o

c

t

n

e

m

y

a

p

e

l

i

b

o

M

:

a

n

i

h

C

f

o

n

o

i

s

u

l

c

n

I

l

a

i

c

n

a

n

i

F

l

a

t

i

g

i

D

f

o

x

e

d

n

I

y

t

i

s

r

e

v

i

n

U

g

n

i

k

e

P

.

2

e

r

u

g

i

F

)

t

h

g

i

r

(

8

1

0

2

5

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

of Figure 2), in which we see that the mobile payment business was more developed on the

right side of Hu Huanyong Line. In the following seven years, however, mobile payment

coverage moved rapidly to western China—the gap between the regions on the right- and

left-hand side of the Hu Huanyong Line has been narrowed greatly (Figure 2).

The promotion of financial inclusion is at least partly due to the better risk assessment of

fintech companies having access to real-payments data—for example, social media activ-

ity and digital footprint. Fintech companies that offer payment services to consumers can

acquire more accurate information about their consumption behavior and income streams

to assess creditworthiness, and may therefore provide financing to borrowers who are un-

able to take personal loans from banks because of the lack of an established credit registry.

Using real-time payments data, big data, machine learning technology, and other complex

artificial intelligence algorithms, fintech credit platforms can also develop a more accurate

picture about people’s financial lives and creditworthiness both from the extensive (ex-

clusion) and intensive (default and price) margins (Gambacorta et al. 2019; Jagtiani and

Lemieux 2019). MYbank, an Internet-based commercial bank and one of the brands under

Ant Financial Services Group, has lent RMB 2 trillion to over 15.74 million small compa-

nies. Borrowers apply with a few taps on a smartphone and receive loans within three min-

utes if approved. The default rate so far is about 1 percent.3 The size of each loan is around

RMB 10,000, reflecting the inclusive nature of MYbank business loans. The world’s biggest

market for digital payments is changing the way in which banks interact with smaller com-

panies that were previously underserved by state-owned banking giants.

Three key factors contributed to the successful ascendancy of mobile payment in China:

lack of supply, regulatory policy, and technological development.

First, while the initial motivation of developing Alipay was to solve the problem of a lack

of trust among counterparties, there was generally a significant shortage of supply for pay-

ment services. Compared with financial systems in other countries, the Chinese system

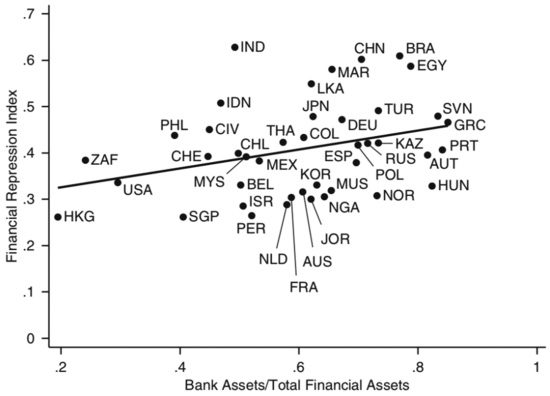

exhibits two unique features: the high proportion of banks in the financial sector (Zhong

et al. 2019) and the high degree of financial repression (Figure 3) (Herrala and Jia 2015). Im-

proving financial inclusion is an especially challenging task in China. For example, in the

past the average penetration rate of credit cards was relatively low, and traditional card

payment services, such as the point of sale machine, were often slow, inefficient and expen-

sive. Most SMEs and low-income individuals had to rely on cash for financial transactions.

When mobile payment services came online, they were immediately embraced by the mar-

ket. Nowadays, withdrawals up to RMB 20,000 are free, with amounts above that charged

with a 0.1 percent cost. Over 90 percent of residents in large cities use mobile payment as

3 Retrieved from: https://www.bloomberg.com/news/articles/2019-07-28/jack-ma-s-290-billion

-loan-machine-is-changing-chinese-banking; accessed on 31 December 2019.

6

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Figure 3. International comparison of financial systems, 2015

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: Huang and Ge (2019).

Note: The horizontal axis indicates share of banks in total financial assets and the vertical axis represents degree of financial repression.

their primary payment method, followed by cash and debit/credit card. For these reasons,

some experts argue that countries like the United States will not be able to replicate the

Chinese experience of mobile payment service (Klein 2019).

Second, a tolerant regulatory environment has also offered room for China’s mobile

payment system to experiment and grow. There were no strict regulatory restrictions on

mobile payment until PBOC released its “Measures for the Administration of Payment

Services for Non-Financial Institutions” report in June 2010. Since then, PBOC has issued

nearly 270 third-party payment licenses. Although it now looks that the number of licenses

is excessive, granting third-party payment licenses was an innovative policy step. In other

countries, this kind of experimental approach might not be possible.

And, finally, technological development has provided the necessary conditions for both

spread of payment coverage and improvement in service quality. According to a survey by

Nielson, the smartphone penetration rate in China was 66 percent in 2017, which was sim-

ilar to most developed countries but significantly higher than Brazil (36 percent), Turkey

(19 percent), and India (10 percent). The number of transactions that Alipay can handle

per second increased from about 200 in 2011 to 210,000 in 2017 and the fund-loss rate was

reduced to below one in a million. The adoption of QR codes also brought about revolu-

tionary changes to the extension of mobile payment services.

7

Asian Economic Papers

Mobile Payment in China: Practice and Its Effects

In sum, lack of supply, tolerant regulatory attitudes, and a relatively mature fintech in-

dustry have underpinned China’s domestic experience with mobile payment services.

Chinese payment technology has also started to support mobile payment businesses in

Asia. Alipay has cooperated with local partners to establish nine local e-wallets, includ-

ing Thailand (TrueMoney), the Philippines (GCash), Indonesia (DANA), India (Paytm),

Malaysia (TnGD), Pakistan (easypaisa), Bangladesh (bKash), Korea (Kakao pay), and Hong

Kong (Alipay HK). Cross-border payment of local wallets is also available between Hong

Kong and mainland China, and between Hong Kong and Japan, as are cross–border remit-

tances supported by block chain from Hong Kong to the Philippines, and from Malaysia

to Pakistan.

3. Relevant literature on mobile payments

Mobile payment in China is predominantly linked to pre-existing bank accounts but can

be more easily accessed through mobile devices, enabling mobile phone owners to trans-

fer money instantly, securely, and cheaply, leading to enormous changes in the organi-

zation of economic activity. The reduction in transaction frictions, including visible costs

and invisible attrition such as theft, makes remittances and payments easier and safer than

traditional payment methods, especially in developing economies. Suri (2017) notes that

mobile money provides a dramatic reduction in transaction costs, as well as improvements

in convenience, security, and time taken for the transaction.

The reduction in transaction frictions could facilitate trade by improving the existing trade

efficiencies and by enabling new transactions that would not have happened without

mobile money. For example, Plyler et al. (2010) find that M-Pesa in Kenya has promoted

the growth rates of small-scale firms at the community-level, largely driven by the in-

creased circulation of money. Beck et al. (2018) analyze the effects of payment technology

innovation on entrepreneurship and economic development, and conclude that broader

approaches to improving access to financial services, including payment services, are

important for alleviating financial constraints and stimulating business performance.

Convenience and lower transaction frictions could also play an important role in informal

insurance networks (Yang and Choi 2007; Aycinena et al. 2010); specifically, by connecting

individuals to the broader economy beyond those physically proximate, and strengthening

informal insurance networks (Klapper and Singer 2014). In developing and low-income

countries, informal risk sharing through mechanisms such as inter-household transfers,

marriage, precautionary saving, and state-contingent loan repayments provide impor-

tant means by which households mitigate risk (Rosenzweig and Start 1989; Udry 1994;

Townsend 1994, 1995). Despite intense academic and policy debates over the best way to

improve household risk bearing, few studies have incorporated the effect of digital finan-

cial inclusion into the analysis. A recent exception is Jack and Suri (2014), who estimate

8

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

the impact of using M-Pesa on risk sharing, and find that compared with non-users, the

consumption of M-Pesa users is unaffected when facing negative shocks. In addition, such

informal savings and insurance mechanisms could lead to more efficient business decisions

by relaxing the tradeoff between risk and return that households would otherwise face

(Jakiela and Ozier 2016; Di Falco and Bulte 2013).

We try to provide some preliminary evidence on the impact of mobile payment in China

by examining the household’s entrepreneurial decision and ability to smooth consump-

tion risks. Previous studies gauging the impact of mobile money have almost exclusively

focused on the adoption decision and welfare of the household, and few of them have ad-

dressed the importance of household entrepreneurial activity and risk sharing. Beck et al.

(2018) show significant quantitative implications of mobile money for entrepreneurial

growth and macroeconomic development. Using provincial-level data, Xie et al. (2018)

provide evidence that the development of digital finance promotes the registration of new

businesses. Yin et al. (2019) conduct cross-section analysis to study the impact of mobile

payment on household entrepreneurial decisions and business performance. We extend

further by using the panel data to better control for potential selection bias. And we exam-

ine how the transition between agricultural and business families changed due to mobile

payment. Moreover, as far as we know, there is a lack of statistical evidence on the impact

of digital financial instruments on household risk sharing.

4. Empirical analysis

It is not difficult to observe the positive changes that mobile payment has brought to the

Chinese economy, particularly to ordinary households and SMEs. In this section, we pro-

vide some empirical evidence, focusing on household entrepreneurship and risk sharing

among households. We use two sets of data: the China Household Finance Survey con-

ducted in 2013, 2015, and 2017; and the Peking University Index of Digital Financial Inclu-

sion for China (PKU-DFI) for the years between 2011 and 2018 (Guo et al. 2020).

The China Household Finance Survey is a nationally comprehensive household-level sur-

vey conducted via face-to-face interviews. The questionnaire is composed of four parts:

demographics, financial assets and liabilities, social security and insurance, and income

and expenditure. The survey tracks households every two years and adds new households

to the sample in each wave. The tracked sample allows us to construct a balanced panel us-

ing the 2011, 2013 and 2015 surveys (34,430 household-year observations) for the analysis

of household entrepreneurial activities. After controlling for the necessary non-missing

variables, 7,963 households were left in the 2013, 2015, and 2017 surveys. Because we fo-

cus only on the change of consumption and income, we then take the first difference of the

variables between three rounds, the final sample consists of 15,926 household-year obser-

vations (7,963 × 2) for the analysis of household risk sharing.

9

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

PKU-DFI is developed by Peking University’s Institute of Digital Finance, in collabora-

tion with Ant Financial Services Group of Alibaba. Using the data from Ant Financial, a

large representative mobile payment platform, PKU-DFI measures digital inclusive fi-

nance in China during 2011–18 at three levels (national, provincial, and municipal) and

from three dimensions (breadth of coverage, depth of usage, and level of digitization).4

The three dimensions include 33 dimensionless bottom indicators. More specifically, the

PKU-DFI is constructed from bottom to top using the bottom indicators. First, the coeffi-

cient of variation method is used when calculating the weights of each specific indicator.

Then, the analytic hierarchy process method is applied to calculate the weights for each

sub-dimension that are used to calculate the breadth of coverage, the depth of usage, and

the level of digitalization. Finally, the PKU-DFI Index is aggregated using these three di-

mensions whose weights are again determined by the analytic hierarchy process method.

The PKU-DFI is comparable both horizontally (in a regional dimension) and vertically (in a

time dimension).

4.1 Promoting entrepreneurship and informal business

With mobile payment, the rate of processing fees varies from 0 to 0.3 percent—the lower

transaction fees matter considerably for informal small-scale business. With the help of mo-

bile payments, there is no need to fumble for cash, write out checks, or wait for invoices,

which greatly improves settlement efficiency (Jack and Suri 2011). The reduction in trans-

action frictions could facilitate trade from two aspects: on the one hand, by improving the

efficiency on existing trade, and on the other, by enabling new transactions that would

not have happened without mobile money. These reductions in transaction costs, along

with the strengthening of informal insurance networks and increasing financial inclusion,

could help households make more efficient decisions by relaxing the trade-off between

risk and return that households would otherwise face (Di Falco and Bulte 2013; Jakiela

and Ozier 2016).

We examine the association between the adoption of mobile payment and business activity

from a micro perspective. We disaggregate business into formal and informal businesses.

Formal business includes four types: company limited by shares, limited liability company,

partnership enterprise, solely owned enterprise. Informal business includes two types:

registered self-employed business and unregistered business, such as market stalls or street

musicians. Compared with formal businesses, informal businesses are often small in scale

and without standardized management systems.

Although the mobile payment tool came out in 2004, mobile payment business exploded in

2013, after the advent of Yu’E Bao, and 2013 is always regarded as the start year of digital

4 See more in Guo et al. (2020).

10

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Table 1. Impact on entrepreneurial activity by pre-MP activity

Pre-MP activity

Agricultured

Informald

Formald

Informald

(2)

Dependent variables

Agricultured

(1)

−0.1275***

(−6.5412)

0.0016

(0.0882)

0.0533

(1.0125)

0.0852***

(4.4491)

0.0648***

(2.9864)

−0.2035*

(−1.7579)

Formald

(3)

Income

(4)

0.0008

(0.1277)

0.0091

(1.5550)

0.0515

(0.4777)

2998.1578***

(2.8294)

4175.3053**

(2.3724)

10100.00

(0.6050)

Note: Reported are coefficients on the interaction term MPd × Post-2013d. t-statistics are in

parentheses. Each row is a regression in sub-samples that split by households’ pre-MP period

activities. Regressions include time and household fixed effects, municipality × year dummies,

as well as household control variables. As the space is limited here, coefficients on control

variables are available upon request from the authors. The superscript “d” indicates a dummy

variable. MP = mobile payment.

***Statistically significant at the 1 percent level; **statistically significant at the 5 percent

level; *statistically significant at the 10 percent level.

finance in China. This allows us to use the following difference-in-difference estimation,

which compares households with and without mobile payment before and after the explo-

sive growth of mobile payment.

yict

= α + β

+ γ

t

+ δMPict

+ π Xict

+ η

ct

i

+ ε

ict

,

(1)

where yict is outcome variables for household i in municipality c in period t, β

hold fixed effect, γ

t is a year fixed effect, Xict is a matrix of household control variables, and

η

ct are a set of municipality-by-time dummies. The main variable of interest is the dummy

MPict, which is an interaction between a post-2013 dummy and a dummy that equals one

for households using mobile payment after 2013 and zero for all other households in the

sample. The coefficient δ estimates the effect of using mobile payment on outcomes. We

cluster the standard errors at the household level.

i is a house-

Table 1 shows how transactions between agricultural, informal business, and formal busi-

ness households changed through mobile payment adoption. To save space, only the co-

efficients on MPd×Post-2013d are reported. More specifically, each cell is the coefficient on

MPd×Post-2013d from the estimation of equation (1) in the subsamples split by households’

pre-mobile payment (pre-MP) period business participation.

The first row shows that households that engaged in agricultural production in the pre-MP

period are less likely to remain operating agricultural activities, but more likely to be in-

formal business owners after the adoption of mobile payment. Results in the second row

indicate that households who owned an informal business in the pre-MP period are more

likely to continue operating after adopting mobile payment than to transition into formal

11

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

business owners. This suggests that mobile payment mainly tends to help agricultural fam-

ilies start self-employed informal business and existing informal business to continue their

operations, rather than transition into formal business owners.5 In developing countries,

informal firms account for up to half of economic activity, and they provide livelihood for

billions of people (Porta and Shleifer 2014), thus the positive impact of mobile payments

on informal business that we found is both economically and statistically significant. Col-

umn (4) shows that those previously in the agricultural and informal business categories

experienced a significant increase in income following the use of mobile payments, which

confirms the finding of the positive impact on the probability of starting business. To better

understand how the support on the continuation of informal business could be associated

with an increase in income, there are some intuitive explanations. It is plausible that a more

convenient and safe payment tool improves the transaction efficiency and lowers the risk

of these informal business, among which most are businesses without a brick-and-mortar

storefront. In addition, the accumulated payment data enables the fintech companies to

profile the business owners who have no credit history, and makes providing further finan-

cial services for these business owners possible.

There are two possible explanations for the weak evidence on the previously formal busi-

ness owners. First, the payment efficiency gains from the lower transaction costs, shorter

settlement time, and lower possibility of losing cash are relatively subtle for those who

have owned a business with larger scale and more standardized management. Second, we

admit that there is some noise in our estimates because the fraction of households owning a

formal business is relatively small in our sample.

One of the channels through which mobile payment may affect household business ac-

tivity is the enhanced informal networks through transfers among friends and families

due to lower transaction costs. We examine whether there is any difference in the remit-

tance behavior across mobile payment users and non-users. The results in Table 2 show

that being a mobile payment user is associated with a significantly higher probability of

both transferring funds out and receiving remittances compared with non-users. The pro-

portion of households who transferred funds out is 3.51 percent higher among the mobile

payment adopters, and the difference in the proportion of households who received remit-

tances is even greater, at 6.82 percent higher for mobile payment users. Two-way flows of

remittances among friends and relatives are also more likely to be observed for households

using mobile payment. It is plausible that the increase in the proportion of households hav-

ing remittances among mobile payment users is more likely to reinforce and expand their

informal insurance network, which could relax the trade-off between risk and return that

they would otherwise face (Jack and Suri 2011).

5 More detailed analysis is conducted in Wang (2019).

12

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Table 2. Impact on remittance: Full sample

Dependent variables

Transfer outd

(1)

Remittance receivedd

(2)

Two-way flow remittanced

(3)

MPd×Post-2013d

Adj. R2

Observations

HH.Controls

HH.FE

Municipality × year

0.0351***

(3.9651)

0.19

34,098

Yes

Yes

Yes

0.0682***

(5.5972)

0.17

34,074

Yes

Yes

Yes

0.0619***

(5.0866)

0.18

33,992

Yes

Yes

Yes

Note: Reported are coefficients on the interaction term MPd×Post-2013d, and t-statistics are in parentheses. The

average proportion of households transferred out, received, and had two-way remittances in the pre-MP period are 81

percent, 48 percent, and 43 percent, respectively. Regressions include time and household fixed effects, municipality

× year dummies, as well as household control variables. As the space is limited here, coefficients on control variables

are available upon request from the authors. The superscript “d” indicates a dummy variable.

***Statistically significant at the 1 percent level.

4.2 Improving household risk-sharing

Enhanced informal social networks through more convenient remittances could provide

an important means by which households and individuals share risk, especially for those

previously underserved by the formal financial system. Having access to a transaction

account is the first step toward broader financial inclusion because it allows people to store

money and send and receive payments (Demirguc-Kunt et al. 2018). Rapid development

and acceptance of mobile payment could help individuals rapidly transfer purchasing

power within the ecosystems of Alipay or WeChat Pay, improving their financial inclusion,

and hence their ability to smooth risk.

We seek to identify the effects of digital financial inclusion on household risk-sharing. We

use a fixed-effect strategy to examine the impacts of digital finance development in China

and also of traditional banking credit on risk-sharing by investigating their role in affecting

the sensitivity of a household’s idiosyncratic consumption growth to idiosyncratic income

growth in the following specification (similar to that used by Kose et al. [2009], Jack and

Suri [2014], and Li and Liu [2018]):

(cid:9)log ˜Ci jt

= α

+ β(cid:9)log ˜Yi jt

i

+ γ (cid:2)

log(FI jt ) × (cid:9)log ˜Yi jt

+ ψZi jt

+ φZi jt

× (cid:9)log ˜Yi jt

+ α

t

+ ε

i jt

, (2)

(cid:9) log ˜Yi jt

− (cid:9) log ¯Ct

= (cid:9) log Yi jt

= (cid:9) log Ci jt

− (cid:9) log ¯Yt Ci jt and Yi jt repre-

where (cid:9) log ˜Ci jt

sent annual per capita consumption and annual per capita income (income) for household

i in city j at period t, respectively; ¯Ct and ¯Yt are the sample average of per capita household

consumption and income, respectively; and the subtraction of the common component of

each variable from household growth captures idiosyncratic household-specific fluctuation

in that variable (Sørensen et al. 2007). α

effect, FI jt is a vector of financial indices that measure the development of digital inclusive

finance (DFjt ) and traditional bank lending (BC jt), proxied by the ratio of bank credits to

i is the household fixed effect, α

t is the time fixed

13

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Table 3. The effect of digital finance on household risk sharing

Full sample:HH idiosyncratic consumption growth

(1)

(2)

(3)

(cid:9)log ˜Yi jt

logDFjt × (cid:9)log ˜Yi jt

logBCjt × (cid:9)log ˜Yi jt

Controls

Controls interactions

HH. FE, time FE

Observations

R2

0.849***

(0.285)

−0.147***

(0.055)

0.027

(0.017)

N

N

Y

15,926

0.30

0.678**

(0.285)

−0.114**

(0.055)

0.019

(0.017)

Y

N

Y

15,926

0.31

0.632**

(0.291)

−0.150***

(0.057)

0.019

(0.018)

Y

Y

Y

15,926

0.31

Note: Dependent variable: household idiosyncratic consumption growth. DFjt is the measure of digital

inclusive finance, and BCjt is the ratio of bank credits to GDP in city region. Controls: household

demographics, employment dummies, gender and age of the household head, the education level of

family members, smartphone ownership, the use of financial instruments (bank card, participation

in social insurance), and city level GDP growth. Control interactions are the interactions terms of

controls with (cid:9)log ˜Yi jt . Robust standard errors reported in brackets are clustered at household level.

***Statistically significant at the 1 percent level; **statistically significant at the 5 percent level.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

GDP in city region j in period t; and Zi jt is a vector of controls containing both household-

and city-level variables. Household demographics, employment dummies, gender and

age of the household head, education level of family members, smartphone ownership,

and the use of financial instruments (bank card, participation in social insurance) are at the

household level. Besides FI jt, the city-level variable GDP growth is also included to control

for local economic conditions. The interaction term captures other household factors that

might affect the ability of the household to smooth risks.

Therefore, β + γ (cid:2)log(FI jt ) captures the average level of co-movement between the id-

iosyncratic consumption growth and income growth across households; it can be used to

measure the degree of risk sharing/smoothing, as a smaller magnitude indicates a

greater degree of risk sharing across households. Table 3 presents the results of our base-

×(cid:9)log ˜Yi jt in-

line estimation. The negative coefficient on the interaction term logDFjt

dicates/suggests that the improvement of digital finance helps households reduce the

sensitivity of household idiosyncratic consumption growth to income growth (i.e., delink-

ing the fluctuations in household-specific consumption and income growth), which implies

that digital inclusive finance plays a significantly positive role in household risk-sharing.

The coefficient on the interaction of idiosyncratic income and digital finance is negatively

significant and robust through column (1) to column (3). In column (3), we include house-

hold fixed effects, time fixed effects, covariates, and the interactions between covariates

and idiosyncratic income growth. Households are estimated to suffer a 6.32 percent re-

duction in consumption when facing a 10 percent decrease in income growth, and a 1 per-

cent increase in digital financial inclusion index is able to help households smooth this

shock and leads only to a 4.82 percent reduction in consumption. This difference is both

14

Asian Economic Papers

Mobile Payment in China: Practice and Its Effects

Table 4. Mechanism: Where do remittances come from?

From parents

Full

sample

Low

income

0.381**

(0.166)

−0.074**

(0.033)

0.003

(0.010)

Y

Y

0.460**

(0.186)

−0.087**

(0.036)

0.014

(0.009)

Y

Y

High

income

0.078

(0.251)

−0.017

(0.050)

−0.028

(0.018)

Y

Y

2,560

0.73

1,118

0.70

1,442

0.75

(cid:9)log ˜Yi jt

logDFjt × (cid:9)log ˜Yi jt

logBCjt × (cid:9)log ˜Yi jt

Controls

Controls interactions

HH FE, time FE

Observations

R2

From relatives & friends

Low

Full

income

sample

0.136

(0.239)

−0.027

(0.047)

0.012

(0.014)

Y

Y

2,560

0.65

0.438*

(0.260)

−0.086*

(0.051)

0.033*

(0.017)

Y

Y

1,118

0.65

High

income

−0.249

(0.505)

0.044

(0.098)

−0.014

(0.025)

Y

Y

1.442

0.66

Note: Dependent variable: whether household received transfer from parents and parents in law (columns

1–3), received transfer from friends and relatives (column 4–6). DFjt is the measure of digital inclusive

finance, and BCjt is the ratio of bank credits to GDP in city region. Controls: household demographics, em-

ployment dummies, gender and age of the household head, the education level of family members, smartphone

ownership, the use of financial instruments (bank card, participation in social insurance), and city level GDP

growth. Control interactions are the interactions terms of controls with (cid:9)log ˜Yi jt . Robust standard errors

reported in brackets are clustered at household level.

**statistically significant at the 5 percent level; *statistically significant at the 10 percent level.

statistically and economically significant, which indicates that the improvement of digital

finance services significantly enhances the ability of the household to insure against shocks

of income growth. Households that suffer from negative income shocks exhibit a lower re-

duction in consumption growth in regions with better developed digital finance. For more

complete and detailed analysis, please refer to Wang et al. (2019).

Table 4 reports the results of the mechanism. Column (1) examines the response of trans-

fer from parents to income shocks in the full sample, then we divide the full sample into

poor households (with income below the median level) and rich households (with income

above the median level) in column (2) and (3), respectively. The interaction term of inter-

est is negative and significant in columns (1) and (2), implying that when suffering from

negative income shocks, households in areas with better-developed digital finance receive

more remittance from parents in terms of the probability of receipt, and this effect is more

significant for poor households. Columns (4) through (6) show similar evidence: It is more

likely for low-income households in areas with better-developed digital finance to receive

transfer from friends and relatives when facing income risks.

5. Conclusions

The mobile payment business in China is a revolution of financial inclusion. It connects

hundreds of millions of individuals and tens of thousands of SMEs that previously had

no access to payment services other than cash. The mobile payment business is also a rev-

olution in the broader financial industry. Building on mobile payment records and other

15

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

digital footprints, mobile payment service providers have developed comprehensive

ecosystems, covering all sorts of services. The financial industry itself has also started to

change with a new credit assessment system, online lending, digital insurance, robot in-

vestment advice, and more.

We believe this success can be attributed to three key factors: a significant supply shortage

of payment services in the traditional financial industry; a friendly regulatory environ-

ment that encourages and even supports payment innovation; and the rapid development

of internet technology, including smartphones, big data analyses, and cloud computing.

The empirical analysis in this study show that mobile payments significantly improve risk-

sharing among individuals, which is particularly important in a society where there are

massive numbers of migrant workers. Our study also provides preliminary evidence that

the adoption of mobile payment increases one’s chance of starting a new business and rais-

ing one’s income.

Second, although mobile payment strongly supports financial inclusion, it also creates

new problems because of digital inequality. Ono (2005) finds that pre-existing inequality

in other socioeconomic areas leads to inequality in information and communication tech-

nologies access, use, and skills. In fact, if one does not own a smartphone and have a mobile

payment account, life could become extremely inconvenient and even difficult. It is now

common in some Chinese cities for shops to refuse to accept not only credit cards but also

cash. Therefore, policymakers and business practitioners need to find ways to reduce the

negative consequences of digital inequality.

And, finally, financial regulation needs to adapt to the new characteristics of mobile pay-

ment specifically, and fintech more generally. Unlike in the United States and Europe,

China’s fintech industry is dominated by a number of unicorn Internet companies. Al-

though this has been helpful for promoting financial inclusion, it also complicates the task

of financial regulation. One problem relates to the speed and scope of risk transmission

of financial risks because of the new technology. Another problem is the possible/likely

abuse of market power by the unicorn firms’ duopoly. Although potential entry threats

motivate these firms to continue providing a more convenient and efficient market in-

frastructure and higher quality services, consumer protection will remain a large concern,

given the highly concentrated market structure. Additionally, the general universal bank-

ing business model pursued by these Internet companies can be a problem. The current

regulatory system in China, which is industry-segregated and institution-focused, is not

suitable for managing financial risks for this new business—as it tends to result in regu-

latory gaps and arbitrage. Regulatory authorities should improve the efficiency by trans-

forming the institution-based framework to functional-based regulation and adopting

more advanced supervision technology (so-called suptech). Finally, protection of financial

consumers should be emphasized and strengthened in China by regulating conducts of

financial institutions and improving consumers’ financial literacy.

16

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

References

Aker, Jenny C., Rachid Boumnijel, Amanda McClelland, and Niall Tierney. 2016. Payment Mech-

anisms and Antipoverty Programs: Evidence from a Mobile Money Cash Transfer Experiment in

Niger. Economic Development and Cultural Change 65(1):1–37.

Aycinena, Diego, Claudia A. Martinez, and Dean Yang. 2010. The Impact of Remittance Fees on Re-

mittance Flows: Evidence from a Field Experiment among Salvadorian Migrants. Unpublished Work-

ing Paper. Ann Arbor: University of Michigan.

Beck, Thorstan, Haki Pamuk, Ravindra Ramrattan, and Burak R. Uras. 2018. Payment Instruments,

Finance and Development. Journal of Development Economics 133(7):162–186.

Demirguc-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2018. The Global

Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution. Washington, DC: World

Bank.

Di Falco, Salvatore, and Erwin Bulte. 2013. The Impact of Kinship Networks on the Adoption of Risk-

Mitigating Strategies in Ethiopia. World Development 43(3):100–110.

Gambacorta, Leonardo, Yiping Huang, Han Qiu, and Jingyi Wang. 2019. How Do Machine Learning

and Non-traditional Data Affect Credit Scoring? New Evidence from a Chinese Fintech firm. BIS

Working Paper No. 834. Basel: Bank of International Settlements.

Guo, Feng, Jingyi Wang, Fang Wang, Tao Kong, Xun Zhang, and Zhiyun Cheng. 2020. Measuring

China’s Development of Digital Financial Inclusion: Index Construction and Space Characteristics.

Economic Quarterly [Chinese, Jingjixue Jikan] forthcoming.

Herrala, Risto, and Yandong Jia. 2015. Toward state capitalism in China? Asian Economic Papers

14(2):163–175.

Huang, Yiping, and Tingting Ge. 2019. Assessing China’s Financial Reform: Changing Roles of Re-

pressive Financial Policies. Cato Journal 39(1):65–85.

Jack, William, and Tavneet Suri. 2011. Mobile Money: The Economics of M-PESA. NBER Working

Paper No. 16721.Cambridge, MA: National Bureau of Economic Research.

Jack, William, and Tavneet Suri. 2014. Risk Sharing and Transactions Costs: Evidence from Kenya’s

Mobile Money Revolution. American Economic Review 104(1):183–223.

Jagtiani, Julapa, and Catharine Lemieux. 2019. The Roles of Alternative Data and Machine Learn-

ing in Fintech Lending: Evidence from the LendingClub Consumer Platform. Financial Management

48(4):1009–1029.

Jakiela, Pamela, and Owen Ozier. 2016. Does Africa Need a Rotten Kin Theorem? Experimental Evi-

dence from Village Economies. Review of Economic Studies 83(1):231–268.

Klapper, Leora, and Dorothe Singer. 2014. The Opportunities of Digitizing Payments. Working Paper.

Washington DC: World Bank. Available at https://openknowledge.worldbank.org/handle/10986

/19917.

Klein, Aaron. 2019. Is China’s New Payment System the Future? Working Paper. Washington, DC:

Brookings Institution.

Kose, M. Ayhan, Eswar S. Prasad, and Marco E. Terrones. 2009. Does Financial Globalization Promote

Risk Sharing? Journal of Development Economics 89(2):258–270.

17

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Mobile Payment in China: Practice and Its Effects

Li, Zhongda, and Lu Liu. 2018. Financial Globalization, Domestic Financial Freedom and Risk Shar-

ing Across Countries. Journal of International Financial Markets Institutions & Money 55:151–169.

Mbiti, Isaac, and David N. Weil. 2013. The Home Economics of E-Money: Velocity, Cash Manage-

ment, and Discount Rates of M-Pesa Users. American Economic Review 103(3):369–374.

Munyegera, Ggombe K., and Tomoya Matsumoto. 2016. Mobile Money, Remittances, and Household

Welfare: Panel Evidence from Rural Uganda. World Development 79(3):127–137.

Nanda, Kajole, and Mandeep Kaur. 2016. Financial Inclusion and Human Development: A Cross-

country Evidence. Management and Labour Studies 41(2):127–153.

Ono, Hiroshi. 2005. Digital Inequality in East Asia: Evidence from Japan, South Korea, and Singapore.

Asian Economic Papers 4(3):116–139.

Plyler, Megan, Sherri Haas, and Geetha Ngarajan. 2010. Community-level Economic Effects of M-Pesa

in Kenya: Initial Findings. Assessing the Impact of Innovation Grants in Financial Services Project. College

Park, MD: IRIS Center.

Porta, Rafael L., and Andrei Shleifer. 2014. Informality and Development. Journal of Economic Perspec-

tives 28(3):109–126.

Riley, Emma. 2018. Mobile Money and Risk Sharing Against Village Shocks. Journal of Development

Economics 135(11):43–58.

Rosenzweig, Mark R., and Oded Stark. 1989. Consumption Smoothing, Migration, and Evidence from

Rural India. Journal of Political Economy 97(4):905–926.

Sørensen, Bent E., Oved Yosha, Yi-Tsung Wu, and Yu Zhu. 2007. Home Bias and International Risk

Sharing: Twin Puzzles Separated at Birth. Journal of International Money and Finance 26(4):587–605.

Suri, Tavneet. 2017. Mobile Money. Annual Review of Economics 9(1):497–520.

Townsend, Robert M. 1994. Risk and Insurance in Village India. Econometrica 62(3):539–591.

Townsend, Robert M. 1995. Consumption Insurance: An Evaluation of Risk-Bearing Low-Income

Economies. Journal of Economic Perspectives 9(3):83–102.

Udry, Chrisiopher. 1994. Risk and Insurance in a Rural Credit Market: An Empirical Investigation in

Northern Nigeria. Review of Economic Studies 61(3):495–526.

Wang, Xun, Xue Wang, Yiping Huang, and Shilin Zheng. 2019. Digital Finance and Risk Sharing:

Household Level Evidence from China. Unpublished Working Paper. Institute of Digital Finance,

Peking University.

Xie, Xuanli, Yan Shen, Haoxing Zhang, and Feng Guo. 2018. Can Digital Finance Promote

Entrepreneurship?—Evidence from China. Economic Quarterly [Chinese, Jingjixue Jikan], 17(4):1557–

1580.

Yang, Dean, and Hwajung Choi. 2007. Are Remittances Insurance? Evidence from Rainfall in the

Philippines. World Bank Economic Review 21(2): 219–248.

Yin, Zhichao, Xue Gong, and Peiyao Guo. 2019. The Impact of Mobile Payment on

Entrepreneurship—Micro Evidence from China Household Finance Survey. China Industrial Eco-

nomics [Chinese, Zhongguo Gongye Jingji] 3:119–137.

Zhong, Ninghua, Mi Xie, and Zhikuo Liu. 2019. Chinese Corporate Debt and Credit Misallocation.

Asian Economic Papers 18(1):1–34.

18

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

9

3

1

1

8

4

7

0

0

8

a

s

e

p

_

a

_

0

0

7

7

9

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3