Menekse Gencer

The Mobile Money Movement

Catalyst to Jump-Start Emerging Markets

Whenever I travel to other countries, I like to conduct informal primary

research around mobile payments with my taxi drivers. Are they familiar with

mobile money? Do they use it? How important is it to their daily lives? In the

United States, when I tell people that I work in mobile payments, I am met with

a confused response. Mobile payments, or mobile money, is still a relatively

unknown industry in the U.S. At best, people may associate this industry with

buying music or games over iPhones. In contrast, in some emerging markets,

mobile money is so pervasive that my taxi drivers can recount transaction fees

from memory. On a recent trip to Kenya, I was startled to hear my taxi driver

refer to Michael Joseph, the man associated with launching M-PESA and the

former CEO of Safaricom, by name. How many CEOs of mobile operators in

developed markets are household names? There is something profound taking

place with mobile money in emerging markets. There is now a “Mobile Money

Movement” with the potential to substantially alter the economic paths of the

poor, and of emerging economies at large.

For this reason, the private and public sectors alike are now taking notice of

this industry. Mobile finance is becoming an increasingly important topic for

the World Economic Forum and at the G20 summit. Nearly two-thirds of the

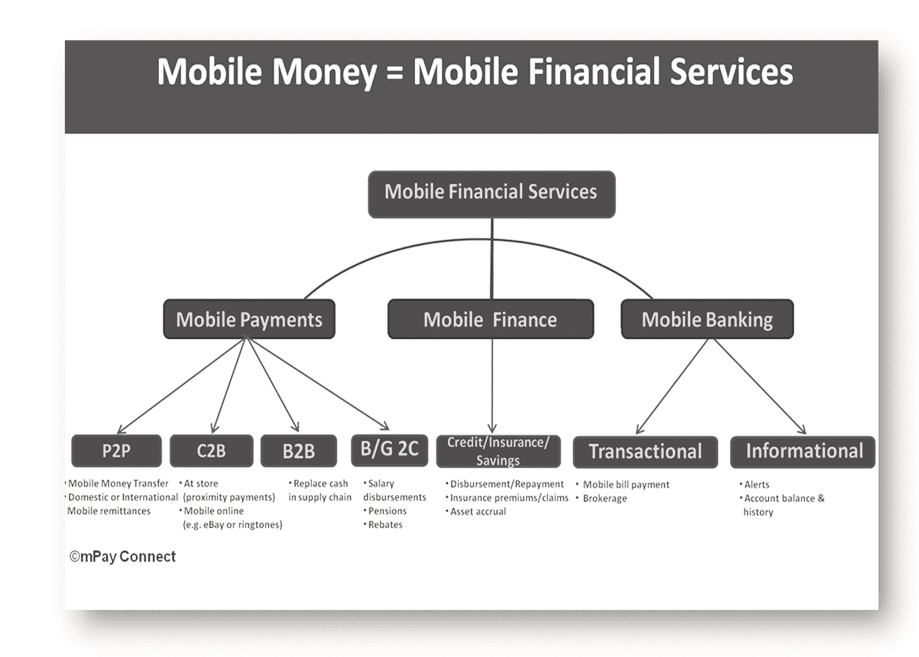

world’s population lives in poverty: four billion people live on less than $8.00 USD per day.1 Most do not have bank accounts, but they do have mobile phones (1.7 billion people by 2012).2 Mobile money provides an opportunity Menekse Gencer is the founder of mPay Connect, a consulting service for clients seek- ing to launch mobile payments. Her consulting service advises banks, mobile network operators, governments, development agencies, and third parties on regulations, go- to-market strategy, product design, business cases, and business development. She is also a managing partner at Arc Spring Group, which advises clients in industries such as healthcare, agriculture, and clean technology on how to leverage mobile financial services to improve their efforts in developing markets. Her most recent publication on the intersections between mHealth and mobile financial services will be presented by the World Economic Forum at its 2011 annual meeting. © 2010 Menekse Gencer innovations / volume 6, number 1 101 Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 Menekse Gencer Figure 1. Mobile Financial Services for financial inclusion to the unbanked base of the economic pyramid—the majority of the global population who have lived in the informal financial sec- tor and have relied on cash to conduct all financial transactions. As such, they lack access to credit, insurance, and savings. This wave of mobile money momentum, if not slowed down by other challenges inherent in these markets, will undoubtedly positively impact the course of economic growth in emerging markets for a number of reasons that are inherent within mobile money itself. DEFINING MOBILE MONEY What is mobile money? Ask this question of ten people in the mobile industry, and you will hear ten different definitions. For the purposes of this discussion, I am defining mobile money as follows: In the simplest form, mobile money, or mobile financial services, is the ability to access and utilize electronic financial services, or digital cash, using the mobile phone. It is a unique money account that is separate from the airtime minutes or post-paid mobile billing accounts that are often used as source for micropayments associated with services and applications used on the mobile phone. Mobile money spans a number of financial categories, including mobile payments, mobile savings, insurance, credit, and mobile banking. Within mobile payments, “P2P” indicates pay- ments between people domestically or internationally in the form of remit- 102 innovations / Data Democracy Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets tances; “C2B,” or consumer-to-business, indicates payments to merchants by customers (either online or in the store); “B2B” indicates payments between businesses to reduce cash in the supply chain upon inventory delivery; and “B/G2C” indicates business or government salary payments to employees, and government benefit and pension disbursements to citizens. Each of these categories represents varying global market opportunities. Retail purchases are by far the largest market, bringing approximately $21 tril-

lion in volume globally in 2007 and expected to grow to $30 trillion by 2014.3 An additional large market includes international remittances, which is expect- ed to grow from $230 billion in current volume to $1 trillion in volume by 2012.4 Many mobile money systems in emerging markets have focused on the P2P remittance space. This focus is driven by the informal P2P money flows, which the people in those markets depend. Mobilizing remittances enables a substantially higher value proposition over existing cash transfer services, due to greater reliability, less likelihood of theft, and greater speed in reaching remote recipients. Mobile microfinance loan disbursement, repayment, micro- insurance, and asset accrual services are additional areas that are receiving sig- nificant attention in emerging markets. They represent $6.6 billion in assets.5

FORECASTING THE IMPACT ON EMERGING MARKET REAL GDP:

THE M-PESA CASE STUDY

Although Kenya’s was not the first mobile money system to launch P2P mobile

money services, it has become the most prolific case study. In March 2007, the

mobile network operator Safaricom commercially launched the M-PESA

mobile money system for the Kenyan market, where the vast majority of the

population was unbanked (81 percent).6 While only 19 percent of the popula-

tion had access to a bank, 55 percent had access to mobile phones.7 It was

believed that mobile financial services, provided by the mobile network opera-

tor Safaricom, which had much better market penetration than banks, could

reach customers who had been left out of the formal financial services system

through their agent airtime top-up networks—otherwise known as their

human ATM system. They were correct.

By October 2010, the M-PESA mobile money transfer system had over 12

million users out of 17 million mobile phone subscribers, representing over 70

percent penetration of the mobile subscriber market, or 57 percent of the adult

population.8 The adoption rates of the payments system were so staggering that

Vodafone, the parent company of Safaricom, had difficulty meeting the

demand.

Not only did the adoption rates of the system grow exponentially, so too did

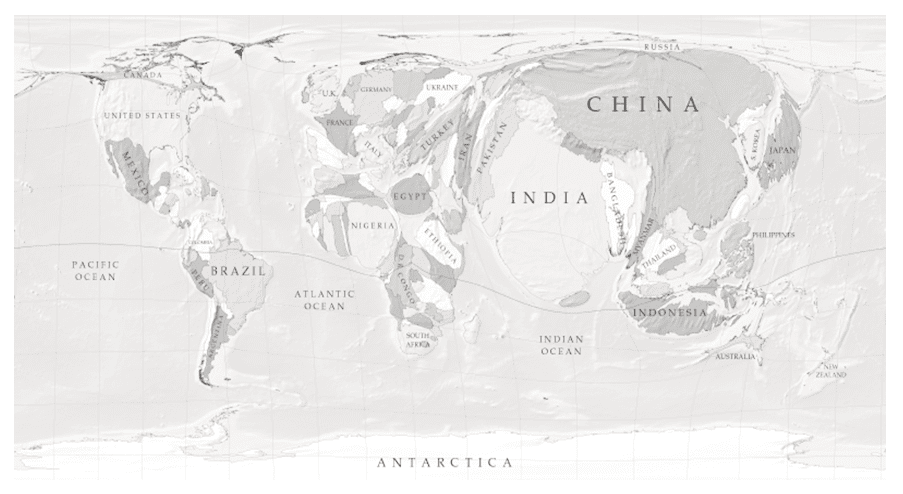

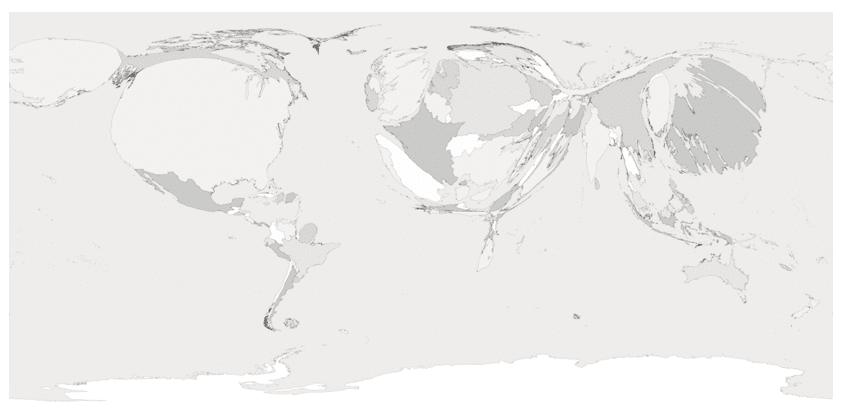

the volume of transactions. By 2010, the equivalent of $400 million USD, or 21 percent of Kenya’s GDP,9 was passing through the M-PESA system monthly in a innovations / volume 6, number 1 103 Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 Menekse Gencer Figure 2a. Today’s GDP Cartogram… Figure 2b. Example of Future GDP Cartogram14 market where the per capita yearly GDP is approximately $868.10 Compare this vol-

ume with PayPal Mobile’s claims of $600 million in volume passing through the mobile channel for the entire year of 2009,11 in a country where the per capita GDP is nearly 60 times that of Kenya’s.12 Many argue that no other emerging market will enjoy the same level of exponential mobile money growth that Kenya has witnessed. They believe that Kenya had the “perfect storm” of demographic, socioeconomic, political, and business factors that led to this adoption rate. Whether this is true is yet to be seen. However, regardless of the speed, mobile money adoption will occur in 104 innovations / Data Democracy Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets other markets with similar socioeconomic factors, including significantly high unbanked populations (dependent on cash) and high mobile penetration rates. The impact that mobile money systems will have other markets similar to Kenya’s will positively affect the GDP growth for those markets as well. In fact, one can imagine that the relative GDP sizes of developed versus emerging mar- kets will change substantially in the next decade, due in large part to the posi- tive economic effects mobile money will unleash.13 LINKAGES BETWEEN MOBILE MONEY AND GDP Mobile money is the intersection between mobile telephony and digital currency. Studies have shown that mobile telephony leads to a rise in GDP. Similarly, digital currency, as a replacement for cash, is recognized to have the same effect. A number of studies have concluded that a 10 percent rise in mobile sub- scribers in emerging markets will lead to a .6 percent to 1.2 percent increase in GDP in those markets, due to the productivity gains associated with commu- nication and new jobs.15 The studies further noted that the effect mobile teleph- ony has on GDP is greater in emerging markets, where connectivity is critical- ly dependent on mobile telephony (where computer-based Internet penetra- tion lags significantly). Moody’s conducted a similar study in 2009 (mostly focused on developed countries with credit and debit cards) that cited that digital currency, as a replacement for cash, delivered an additional $1.1 trillion to the global econo-

my from 2003 to 2008, representing a .5 percent increase in GDP globally (dur-

ing a period when the real global GDP rose only 3.4 percent, on average).16 This

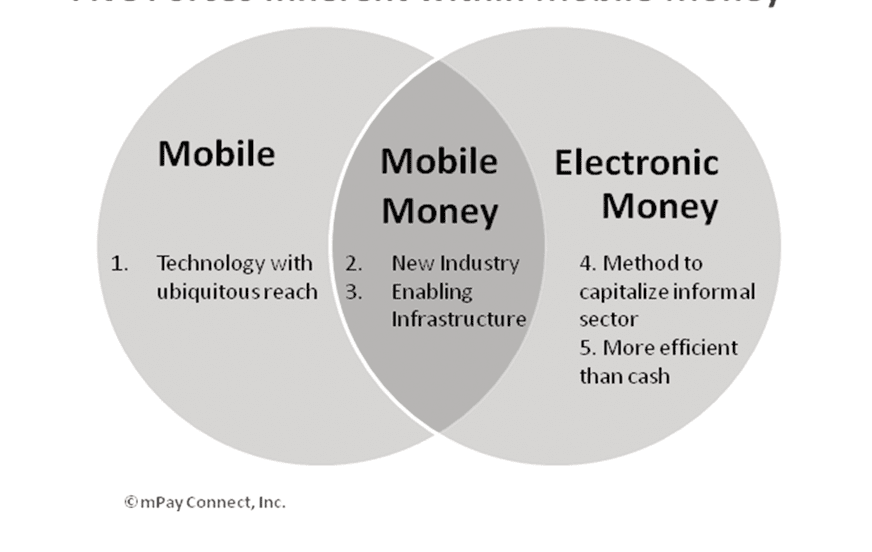

$1.1 trillion increase represented 4.9 million new jobs and helped drive con- sumption. In China and Brazil, large emerging markets, the effects on GDP were even more substantial, with an increase of more than one percent to their GDP. The study cites that the reasons GDP increased were due to efficiencies that digital currency provided over cash, including increased convenience, deposited assets kept in accounts rather than “under the mattress,” the reduc- tion of the untaxable “gray economy,” and reduced risk of fraud. Specifically, providing financial access to the poor has a significant impact on per capita GDP as well. Economists Robin Burgess and Rohini Pande first published research in 2003 on the impact of providing financial access to the poor in India. They indicated that every “1 percent increase in the number of rural locations banked per capita reduced rural poverty by 0.42 percent.” In addition, they noted that economic activity increased by .34 percent.17,18 Mobile money has many other secondary effects, that can lead to a rise in GDP, including reducing the costs of money transfers, which can result in high- er remittance inflows, and capturing cash in the market for savings, investment, and further remittances. It also bolsters adjacent industries. For example, innovations / spring 2010 105 Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 Menekse Gencer mobile money enables conditional cash transfers, performance-based funding, prepaid savings, credit, and micro-insurance. These financial tools significant- ly boost the healthcare industry by enabling better quality healthcare, better accessibility to services, and better affordability of those services. Better health- care results in healthier people, who can be more productive. More productiv- ity boosts GDP. All of these effects stemming from mobile money, as well as others noted later, positively impact GDP growth. At the time of writing this article, no quantitative research had been pub- lished that directly linked mobile money with GDP growth. Studies had shown, however, that within 2-½ years of launching M-PESA, the income levels of Kenyan households using that mobile money service had risen by 5 percent to 30 percent.19 Combining the reach, connectivity, and cost benefits of mobile with the efficiencies of digital currency will lead to overall economic growth. In the next section, we explore the forces inherent in mobile money that affect the levers that drive GDP. THE FIVE FORCES INHERENT WITHIN MOBILE MONEY THAT DRIVE GROWTH Mobile money will spur economic growth in emerging markets because of the forces inherent to mobile money itself. Specifically, these forces include: 1. The ubiquity of data transmission that mobile provides 2. Mobile money as a new industry 3. Mobile money as an infrastructure supporting new businesses and other industries 4. The infusion of new capital from the informal sector 5. The efficiency gains that digitization of money enables 1. Mobile money leverages mobile devices/networks to reach people who were previously unreachable. Mobile money leverages another infrastructure, namely mobile, which is the most ubiquitous data-transmission device in history. Indeed, mobile service reaches people far out of reach of traditional banks. In March 2009, there were 4.1 billion mobile users out of the global population of 6.5 billion.20 In Africa, the number of mobile subscribers is now 450 million, larger than the aggregate populations of the United States, Canada, and Mexico.21 To put this in further perspective, by 2013 there will be over 5 billion mobile phones globally. In con- trast, there will be only 2 billion computers, 1 million ATMs, 500,000 bank branches, and 250,000 Western Union outlets.22 Not only do mobile payments have the ability to reach these customers, it can do so with a device that is already in the customers’ hands and uses a data 106 innovations / Data Democracy Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets Figure 3. The Five Forces Inherent within Mobile Money connectivity network that already is set up with a cash-in (and, eventually, cash-out) network of agents. In other words, the cost to distribute the mobile financial service is no longer tied to additional hardware deployments, new ATMs, or new branch offices. This does not suggest that the cost of mobile money is trivial. The up-front investment to set up mobile money services is not trivial. However, these costs are lower than the costs associated with setting up branch stores, building the electricity infrastructure needed for those stores to operate, and the roads that would need to be built to support these bank branches. The ongoing costs of doing business are also reduced dramatically. A study released by Fiserv, a Fortune 500 financial services technology platform company, compared the costs to support a financial transaction. In the U.S., if the transaction was serviced by a bank branch, the cost to the bank was $4. If

serviced by a live customer service representative over the phone, the cost was

$3.75. The same transaction cost $1.25 if serviced by an automated voice-

response system, and only $.08 if a mobile phone was used.23 It is true that the bank and live customer service costs would likely be less in emerging markets, due to lower labor costs, but the cost differential between branches and mobile even in these markets is still on the order of 100+ times. Furthermore, the return on investment of setting up a retail branch in remote areas that lack basic infrastructure is a non-starter. innovations / volume 6, number 1 107 Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023 Menekse Gencer Of course, this cost differential becomes exceedingly important when con- sidering financial inclusion for the base of the world economic pyramid. Low- cost setup and servicing is critical to support low-income people who are most likely to hold and transact small amounts. Because of mobile money, customers whose transactions were always unprofitable to banks become profitable. This is a substantial portion of the global population. The Consultative Group to Assist the Poor estimates that by 2012, 1.7 billion people with mobile phone access will still have no bank account.24 Note that the profitability of serving the poor is heavily influenced by mobile network operator tariff prices and trans- action fees in markets that are led by multi-national organizations. 2. Mobile money is a new industry that attracts investment and spurs new revenue. Mobile money is a new industry that is precipitating new investments for new ven- tures, new jobs, and new revenue streams for existing companies. In Kenya, exist- ing airtime top-up agents are adding M-PESA cash-in and cash-out services to their existing businesses. By October 2010, 20,000 agents had joined the M-PESA network to add this new revenue. By March 2010, Safaricom believed that over 36,000 new agent and telecommunications jobs had been created due directly to M-PESA.25 This statistic does not take into account new ancillary businesses that are now possible, due to the digitization of payments. With the substantial success that M-PESA has seen in Kenya, large and small companies alike seek to emulate Safaricom’s achievements elsewhere with new mobile money services. McKinsey & Co. and CGAP estimate that mobile operators will enjoy $5 billion/year of additional direct revenue due to mobile money serv-

ices, and an additional $2.5 billion/year for indirect revenue streams due to mobile money.26 Some 160+ mobile money initiatives were underway globally in 2009, with 49 commercially deployed. They were driven not only by mobile network operators but also by banks and third parties.27 Most of these initiatives have been targeting emerging countries. New funds are emerging to invest in the mobile money industry, from Silicon Valley to Africa. In addition, a range of strategic investments by large companies and grants by various nonprofits are gaining momentum. In June 2009, IBM announced $100 million in investments for cell phone research

(mobile payments).28 Sybase purchased PayBox, and Nokia invested in

Obopay.29 On the grant side, the UK Department for International

Development, CGAP, and the International Fund for Agriculture Development

announced the Africa Enterprise Challenge Fund. The GSM Association,

CGAP, and the Clinton Foundation announced the “Mobile Banking Call to

Action,” which calls for $100 million to provide financial inclusion for the unbanked through mobile financial services. The GSMA and the Gates Foundation pledged $12.5 million for “Mobile Money for the Unbanked” ini-

108

innovations / Data Democracy

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets

tiative to provide mobile financial services to 20 million people earning less

than $2 per day. By mid-2010, the Gates Foundation and USAID had set up a $10 million Haiti Fund to motivate organizations to launch mobile money

services in Haiti.

According to CGAP, “For the first time, Africa is becoming a bigger lure for

investors than for aid donors. Africa’s poverty rate has been declining by 1 per

cent annually since the 1990s, and investment is growing dramatically. A

decade ago, Africa was receiving less than $5-billion (U.S.) in foreign invest- ment annually. By 2008, it was attracting nearly $40-billion in direct foreign

investment – more than it received in foreign aid. One survey found that 40 per

cent of emerging-market equity investors are putting money into Africa today,

compared with 4 per cent in 2006.”30 Most of this investment is coming from

India and China.

The level of foreign investment by venture firms, large global companies,

and nonprofits is spurring new economic activity and bolstering new innova-

tions and ventures around mobile money, which, in turn, are adding new jobs

and income within these markets.

3. Mobile money is a foundational infrastructure that supports the

sustainability of new businesses.

Iqbal Quadir, the founder of GrameenPhone in Bangladesh, states that “con-

nectivity is productivity”31 because of the business efficiency gains that connec-

tivity provides. Mobile money accelerates this phenomenon because it is the

enabler of business. If mobile connectivity is the “how” to communicate infor-

mation necessary to conduct commerce and business, mobile money is the

“why”…so that we can make money.

The ability to remotely pay for goods and services through mobile pay-

ments is unleashing a new stream of profitable and sustainable businesses.

Mobile and mobile payments enable a degree of automation and cost savings

that substantially impacts the profitability of certain services. Mobile health, for

instance, relies on payments in a variety of ways—from conditional cash trans-

fers and micro-insurance for patients to performance-based funding and salary

disbursement for healthcare providers. The ability to take payments using the

mobile phone will enable new business models for healthcare to the poor, ulti-

mately enabling these services to be self-sustaining by being able to charge and

be paid for services remotely consumed. By creating an electronic financial

account for the first time, small businesses that sell items such as pharmaceuti-

cal drugs will soon be able to access credit for inventory purchases to reduce

issues around stockouts. In addition, off-grid energy initiatives in remote loca-

tions are now relying on mobile payments to provide more creative methods to

finance expensive investments, such as solar panels for the rural poor. With the

ability to prepay for solar electricity using mobile payments, rural villagers can

innovations / volume 6, number 1

109

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

Menekse Gencer

now have access to “lease-to-buy” financing. Finally, mobile money is now

being used by the micro-insurance industry for smallholder farmers, a segment

that lacked insurance access in the past, due to the prohibitive costs of admin-

istration and management associated with this group, which made them

unprofitable to service prior to electronic claims and premium payments. Now,

with systems like those launched by Syngenta Foundation, mobile bar codes

associated seed bags are easily sent and tracked via MMS.32 Farmers are able to

register and pay for premiums using their mobile phones at the point of seed

purchase. Claims payouts and notifications are made automatically to the M-

PESA account when weather station data and index insurance calculate adverse

conditions for crops. Risk of crop failure and loss of assets is now reduced for

farmers, enabling them to focus on investing in better fertilizer and farming

methods, thus increasing crop output.33 As one can imagine, mobile money

becomes the backbone of all commerce and economic activity. Eliminate the

“friction” of cash, and new profitable businesses are possible.

Mobile money itself relies on foundational building blocks. In order to

launch a mobile money system, certain elements must be in place. For instance,

mobile money requires a level of identity management, or an understanding of

who the person is and tracking of data regarding that individual. In many of

the emerging markets, mobile money initiatives are the impetus to develop

such systems, including the regulatory policies and technologies underlying

them. One can imagine that the building blocks of mobile money, such as iden-

tity management, spur additional businesses. For example, ID Management

and data tracking of individuals is critical for e- and m-Health.

The synergies between m-Health and mobile financial services is a growing

area of interest. Understanding common user bases; business operations; infra-

structures such as ID management, authentication, security, and fraud man-

agement; and policy concerns can lead to cross-sector efficiency gains between

m-Health and mobile money.34

People in these markets already understand this phenomenon. A new wave

of entrepreneurism is developing where mobile money infrastructure exists. At

mobile money conferences, I am continuously approached by Kenyans who are

starting new businesses that leverage the M-PESA infrastructure. New incuba-

tors, similar to “dot-coms” launched in California in the 1990s, are hatching

small businesses in Kenya.35 Nairobi is becoming the new Silicon Valley.

The question of where entrepreneurs in emerging markets will receive seed

funding and institutional funding is a topic that will become increasingly

important. Many of the biggest opportunities for entrepreneurs exist in mar-

kets deemed as too risky or without good exit strategies. Thus, they typically fall

outside of the typical Silicon Valley venture capitalist model. This will be an

ongoing topic to address moving forward.

110

innovations / Data Democracy

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets

4. Mobile money formalizes the informal financial sector, enabling savings,

loans, and investments in lieu of “cash under the mattress.”

Bringing cash into bank deposits through mobile money services enables the

use of that money for investments, lending, and savings (assuming the holder

of the funds has the regulatory ability to enable such financial services). In their

research report titled “Mobile Money: The Economics of M-PESA,” Tavneet

Suri and William Jack state that 77 percent of Kenyans stored their money

informally around their homes prior to M-PESA, but now find M-PESA to be

a much safer method for storing their funds safely.36

In 2005, Freund and Spataforma conducted research that estimated the size

of informal remittances in more than 100 developing market countries to

amount to 35 percent to 75 percent of formal remittances.37 Capturing the

equivalent of hundreds of billions of dollars in cash remittance inflows into

deposit mobile money accounts will have a substantial impact on GDP growth.

In addition, by leveraging mobile as the channel for remittances, many believe

that the cost structures of the agent network can be greatly reduced.

Furthermore, increased entrants may put pressure on existing pricing rates.

This cost savings can be given back to consumers. During the G8 summit in

2010, it was noted that if average end-consumer transaction costs could be

reduced from 10 percent to 5 percent in five years, then an additional $15 bil- lion/year would be available for potential inflows into emerging markets. 5. Mobile money enables efficiencies associated with digitization and reduces frictions associated with cash. Cash is difficult to move and store, unsafe (due to theft), and difficult to track. Mobile money relies on electronic transmission, which eliminates these issues. Eliminate “Shoe Leather Costs” Economists often refer to the time and productivity wasted in physical cash movement as “shoe leather costs.” In the case of emerging markets, the term can be used quite literally, as people have to walk for hours and transport cash for days via trucks to reach the intended recipient. For example, a Kiva fellow in Liberia had to ride his motorcycle for days to disseminate cash loans to micro- finance recipients in remote villages.38 In Kenya, 47 percent of people indicate that due to M-PESA, they now save three hours, or the equivalent of $3, per

transaction.39 This statistic is profound when considering an average per capita

GDP of $868. This is also the case for healthcare workers and others in remote

villages who must travel to get their salary disbursements and pensions. For

healthcare workers, the time spent traveling means less time assisting sick

patients, who cannot be productive until they get healthy. Mobile money elim-

inates this cost by digitizing cash. By reducing this friction, more money is able

innovations / volume 6, number 1

111

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

Menekse Gencer

to circulate in the system in a faster, more efficient way. Owners of businesses

and healthcare workers depositing or receiving their cash from banks do not

need to shut their doors during those hours when they would have walked to

the branch. Money can be moved anywhere in a matter of seconds, and at any

time.

Smooth Out Transactions by Enabling Profitable Micropayments

In addition to eliminating the shoe leather cost phenomenon, the ease of

money moving and the reduced cost structure associated with digitized cash

enables more transactions to happen more often and as needed. This is critical

for enabling frequent transactions among the poor, who have uncertain cash

flows, and for reducing risks associated with their businesses.

For unbanked customers with unreliable cash flows, being able to pay and

receive small amounts of money when they most need it is critical. In their

research, Suri and Jack studied the changes that occurred in the Kenyan market

as it related to money flows before and after M-PESA’s launch.40 What they

found was that many of the informal networks used for lending among closed

networks continued (for instance, in the agricultural segment, where banks

viewed farmers as too risky for credit, but where they would lend to one anoth-

er as needed during erratic weather conditions). What did change upon M-

PESA’s introduction was the elimination of the friction that was caused by the

physical distance among those lending to one another. This in turn led to a

smoothing out of lending at the point that the money was needed, not when

the cash could be attained, sent, and received. In fact, a similar pattern was

noted by Olga Morawcynski, a graduate of the University of Edinburgh who

has studied the transactions taking place between urban and rural family mem-

bers with M-PESA.41 She noted that users of M-PESA sent moeny more often

in smaller amounts, leading to an increase in overall volume sent. CGAP notes,

“On a positive note, users report increases of 5 to 30 percent in their incomes

thanks to transfers through M-PESA. By making smaller, but more frequent

transfers, urban migrants on average are sending more money home than

before. This represents a significant boost for rural recipients, for whom remit-

tances can represent up to 70 percent of their household income.”

If farmers can receive money when needed, then that farmer may not miss

the time window to buy and plant the seeds for his crop before the weather

changes. Similarly, if retailers can receive money from friends or get access to

credit when they have stockouts, then they can ensure that they have sufficient

inventory to sell to customers at the point when the products are needed. This

in turn leads to more output in the economy.

With lower per-transaction costs, people are able to pay smaller amounts

more often, thus reducing emergencies for low-income populations, particu-

larly when impacted by crisis situations that may require large cash outlays.

112

innovations / Data Democracy

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets

This certainly applies in the case of micro-insurance for smallholder farmers

who could be affected by adverse climate conditions, and in healthcare.

Similarly, in Kenya, expectant mothers can now use mobile financial service

tools to prepay into savings accounts as a way to save for their upcoming deliv-

ery, rather than opting out of healthcare facilities due to the costs and risking

home birth, which results in higher mortality rates.

Provide a safer, more traceable, and less risky method to store value and make

payments

The value of mobile money to consumers is highest in markets with the least

banking penetration. These markets can also be the most unstable economical-

ly and politically. Where people are desperate, crime may be rampant. To add

to the safety issue, people may have little or no alternatives to carrying cash.

Storing assets and transacting electronically rather than carrying cash (or stor-

ing it at home) can mean the difference between not only loss of wealth, but

also loss of life in some of these countries. Suri and Jack noted in their research

that 11 percent of Kenyans storing money have had it stolen, whereas only 2

percent have had issues with M-PESA (e.g., accidentally sending it to the wrong

recipient).42 So, too, is the tragedy witnessed with the loss of assets due to flood-

ing, fire, or other natural disasters, as occurred in the Bangladeshi floods of

2007, the Haitian earthquake of 2010, and the tsunami of 2004. Digitization

and safe storage of assets will ultimately reduce GDP loss during these times. In

addition, digitization enables better tracking of money, which can reduce fraud

and make it easier to track business revenues for tax collection.

Digitization of transactions and the traceability of those transactions alone

do not prevent fraud. Rather, such systems will require a robust authentication

and ID management system. These core functions will become increasingly

important areas of concern, not only to the mobile money industry but to

other adjacent industries, such as m-Health.

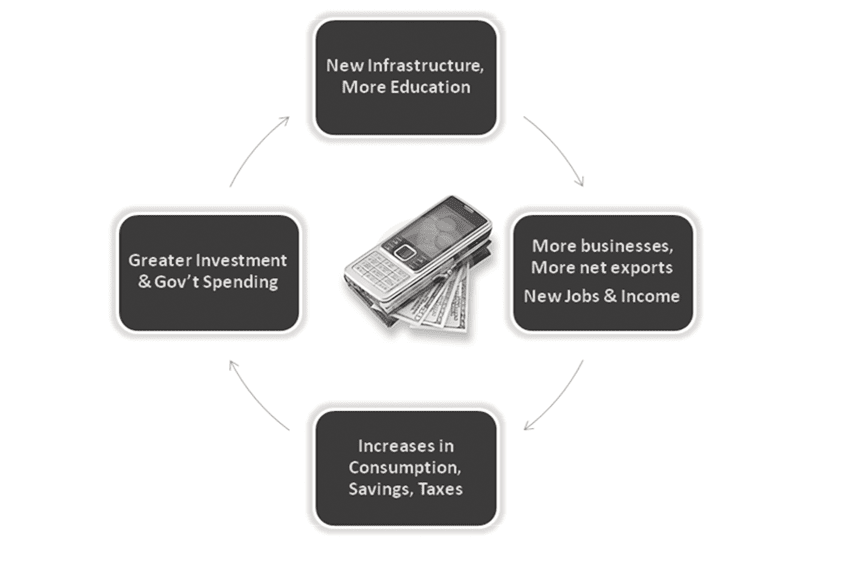

THE POSITIVE SPIRAL OF GROWTH

The five forces described above affect the levers of GDP, igniting a spiral of eco-

nomic growth. Mobile money as an industry is attracting new investment.

Mobile money as an infrastructure is enabling new businesses, which in turn

are producing more jobs and income that can be consumed, saved, or taxed.

The outputs of these businesses will lead to an increase in net exports. Mobile

technology is reaching new segments of the population with money services in

a cost-effective method, which is stimulating new businesses to offer financial

services and capture new deposits from the informal sector. Capturing these

deposits is further stimulating additional savings, loans, taxes, and investments.

Finally, the digitization of cash, is eliminating the frictions and costs associated

innovations / volume 6, number 1

113

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

Menekse Gencer

Figure 4. GDP = Consumption + Investment + Government Spending + Net

Exports

with cash which is increasing consumption, money transfers, and supply-chain

payments, and reducing business risk. This in turn is smoothing out transac-

tions and increasing the velocity of money circulating within the market.

CHALLENGES REDUCING MOBILE MONEY’S IMPACT

Of course, the reality of this situation is still less optimistic than it may appear.

The optimism expressed in this paper does not, by any means, seek to trivialize

the challenges ahead in expanding these services and achieving GDP growth

throughout the globe. On the contrary, there are many hurdles. Kenya is the

example mobile money success that all other countries strive to replicate, but

none have done so yet. Kenya’s success has set high expectations by investors,

who may soon grow impatient without similar outcomes in other markets. In

addition, the growth of sectors spurred by mobile money will be hindered by

the lack of infrastructure, such as electricity, roads, etc. Until other infrastruc-

tures are addressed, GDP growth will be affected.43 Similarly, policy-makers

may significantly limit what can be done in many markets, should the regula-

tory bodies decide to take a significantly conservative stance on AML/CFT and

KYC documentation required to open an account or in other relevant regula-

114

innovations / Data Democracy

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets

tory areas. In such instances, services will likely not reach the poor.

Government corruption is another key area of concern that can prevent GDP

growth. From the perspective of infrastructure, mobile money is a new chan-

nel that relies on existing IT infrastructure. However, IT systems may be lack-

ing within organizations. If these organizations do not address the underlying

IT issues, the mobile money services will have less impact. Successfully launch-

ing mobile money systems is no small feat—it requires a deep level of under-

standing of what it means to combine and execute mobile payments, and

emerging technology operationally, and in a manner that will be adopted by a

new customer base. As of May 2010, of the 164 pilots and 49 commercially

deployed mobile money systems, only 10 have reached adoption levels of 1 mil-

lion customers. The ability to replicate successful models is yet to be achieved.

Most payment professionals will admit that to be successful in the business,

“The devil is in the details.” This level of complexity is further exaggerated

when combining payments with mobile, since the complexities span two

industries. Finally, the fragmented nature of these new mobile money systems,

mainly due to mobile network operators who choose to roll out closed systems,

will continue to limit the usefulness and likelihood of success. In the absence of

interoperability at the domestic and international levels, required scalability

will remain unachievable.

CONCLUSION

Similar to the hype that was witnessed in Silicon Valley in the late 1990s during

the dot-com boom, so too is there a high degree of hype in this industry—this

time in a much more global arena. Make no mistake, as was seen in the dot-

com crash in the early 2000s, there will be many failures and consolidations in

the mobile money industry. However, the few who do survive will drive the

industry forward. It has been said that people overestimate the impact of a new

industry/technology in the five-year time horizon, but underestimate its

impact over a decade. Although in the short term the mobile money move-

ment™ will continue to face challenges noted above, I am optimistic that, with

the focus the world is currently seeing in the mobile money industry, over the

next decade we will see the profound impact on GDP that mobile money will

have on those markets most in need of economic growth and development.

1. International Finance Corporation (IFC), “The Next Four Billion: Market Size and Business

Strategy at the Base of the Pyramid,” 2010.

2. Consultative Group Assisting the Poor (CGAP), 2009.

3. Visa, 2007.

4. GSMA, “Global Money Transfer Pilot Uses Mobile to Benefit Migrant Workers and the

Unbanked,” February 12, 2007.

5. CGAP, “Microfinance Funds: Still growing—with increased focus on social transparency,”

innovations / volume 6, number 1

115

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

Menekse Gencer

September 17, 2009.

6. CGAP.

7. Wireless Intelligence, World Bank, WMM, Global Insights, EIU, Euromonitor.

8. Safaricom news, CGAP.

9. World UIN Blog, October 23, 2010.

10. Safaricom news, Wireless Intelligence, World Bank, WMM, Global Insights, EIU, Euromonitor.

11. PayPal News, February 2010.

12. CGAP, CIA WorldFacts.

13. At the point when international remittances become mobile enabled, if the new mobile interna-

tional remittance providers can undercut current cost structures through mobile and provide

that savings back to the emerging market recipients, inflows into emerging markets will

increase, further positively impacting GDP of emerging markets.

14. Pictures are for illustrative purposes only. Actual cartograms were based on population.

15. International Telecommunications Union (ITU), “Speech by ITU Secretary General”, April 6,

2010, and Indian Council for Research on International Economic Relations (ICRIER.)

16. Moody’s Economy.com Study: “The Positive Economic Impact of Digital Currency,” 2008.

17. Robin Burgess and Rohini Pande, 2003. “Do Rural Banks Matter? Evidence from the Indian

Social Banking Experiment,” STICERD—Development Economics Papers 40, Suntory and

Toyota International Centres for Economics and Related Disciplines, LSE.

18. Jamie M. Zimmerman, Jamie Holmes, “Why cell phones will do more for the developing world

than laptops ever could,” New America Foundation, August 27, 2010.

19. The Economist, “The Power of Mobile Money,” September 2009.

20. United Nations Report, March 2009.

21. CGAP, Jim Rosenburg, “Mobile phones, broadband, and Africa’s surprising numbers for donors

and investors: Headlines for May 10.”

22. CGAP, Forrester, and Bank for International Settlements.

23. Tower Group, Fiserv/M-Com Data: Mobile transaction costs based on actual data from M-Com,

the international mobile banking and payments solutions provider and Fiserv partner.

24. GSMA, Quarterly Report, March 2009.

25. Safaricom presentation at Safaricom Headquarters, May 7, 2010.

26. McKinsey & Co., GSMA, CGAP, June 2009.

27. Gavin Krugel of GSMA, May 4, 2010, at the World Economic Forum in Tanzania.

28. IBM Press Release, June 17, 2009.

29. Sybase and Nokia Press Releases.

30. Rosenburg, “Mobile phones, broadband, and Africa’s surprising numbers for donors and

investors.”

31. Iqbal Quadir, TED conference speech, October 2006.

32. “First Micro-Insurance Plan Uses Mobile Phones and Weather Stations to Shield Kenya’s

Farmers,” ScienceDaily, March 4, 2010.

33. The World Economic Forum publication, “Amplifying the Impact: Examining the Intersection

of Mobile Health and Mobile Finance,” (January 2011, by Menekse Gencer, mPay Connect)

identifies areas of commonality that can lead to cross-sector gains.

34. In February of 2010, the Syngenta Foundation launched Kilima Salama Micro-Insurance pro-

gram for smallholder farmers in Kenya. Within three months of commercial launch, 11,000

smallholder farmers were utilizing the program. (Rose Goslinga interview, May 2010.)

35. “Start-up incubators hatching in Kenya, ” Africa News, April 2007.

36. Tavneet Suri, William Jack, “Mobile Money: The Economics of M-PESA,” October 2009.

37. Freund and Spatafora, “Remittances: Transaction Costs, Determinants, and Informal Flows,”

World Bank Working Paper No. 3704, 2005.

38. Interview with Dave McMurtry, Kiva Fellow, 2009.

39. Safaricom presentation at Safaricom Headquarters, May 7, 2010.

40. Suri and Jack, “Mobile Money: The Economics of M-PESA,” October 2009.

41. Olga Morawcynski, “Designing Mobile Money Services: Lessons from M-PESA,” April 2009.

116

innovations / Data Democracy

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023

The Mobile Money Movement: Catalyst to Jump-Start Emerging Markets

42. Suri and Jack, ““Mobile Money: The Economics of M-PESA,” October 2009.

43. On October 4, 2010, “Country Risk Service Select” issued by the Treasury Department wrote the

following: “The spread of banking, especially telebanking, to the unbanked will help to under-

pin household spending. However, infrastructure bottlenecks, skills shortages, corruption and

political uncertainty will persist. We expect growth to accelerate to 5.8% in 2012 as the global

recovery gains traction, although this will exacerbate domestic structural deficiencies (especial-

ly in the transport and power networks), while key reforms could fall victim to election-related

in-fighting. Growth is likely to edge down to 5.2% in 2013-14, as there is little prospect of Kenya

eliminating infrastructural constraints or dependence on rain-fed agriculture during the fore-

cast period, although the rate of expansion will remain relatively buoyant.”

innovations / volume 6, number 1

117

Downloaded from http://direct.mit.edu/itgg/article-pdf/6/1/101/1626154/inov_a_00061.pdf by guest on 08 September 2023