Journal of Interdisciplinary History, LII:4 (Spring, 2022), 513–536.

Matteo Pompermaier

Credit and Poverty in Early Modern Venice Credit

is more than a simple exchange of money with a promise of a

future repayment. Muldrew has referred to it as a “currency of rep-

utation,” a means by which trust is communicated to others. It is

an integral part of human relations, so difficult to study that it has

been compared to the dark matter “that makes up some eighty-

five percent of the universe but cannot be directly observed.”

Credit “irrigated society” well before the advent of banks, linking

people in an endless series of “networks of obligation” based on

trust and sustained through norms of collaboration and solidarity.

Credit is therefore a complicated issue, regulated by a mix of eco-

nomic and social norms. However, for many people it was, and still

is, distinctly pragmatic, an essential resource for survival, to facili-

tate consumption and to make ends meet.1

This article integrates our knowledge of pre-industrial credit

markets by examining an unusual form of lending in European

history. It sheds new light on how early modern societies dealt

with the problem of poverty, focusing on the pawnbroking service

that early modern Venetian inns and bastioni (warehouses where

wine was sold) offered to their customers. Retracing this credit

activity helps us to understand how Venice managed to give both

economic support and low-cost credit to the lower classes of its

population.

Interest in the credit markets of early modern societies has

increased since the global crisis of 2007/8. A wide literature ana-

lyzes the activity of many kinds of borrowers and lenders in several

Matteo Pompermaier is Post-Doctoral Fellow, Dept. of Economic History and International

Relations, Stockholm University. He is the author of L’économie du mouchoir: crédit et microcrédit

à Venise au XVIIIe siècle (Rome, 2022); co-author of, with Teresa Bernardi, “Hospitality and

Registration of Foreigners in Early Modern Venice: The Role of Women within Inns and

Lodging Houses,” Gender & History, XXXI (2019), 624–645.

© 2022 by the Massachusetts Institute of Technology and The Journal of Interdisciplinary

History, Inc., https://doi.org/10.1162/jinh_a_01765

1 Craig Muldrew, The Economy of Obligation: The Culture of Credit and Social Relations in Early

Modern England (Basingstoke, 1998), 7; Philip T. Hoffman, Gilles Postel-Vinay, and Jean-

Laurent Rosenthal, Dark Matter Credit: The Development of Peer-to-Peer Lending and Banking

in France (Princeton, 2019), 1; Laurence Fontaine, The Moral Economy: Poverty, Credit, and

Trust in Early Modern Europe (New York, 2014), 3–5.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

514

| MA TTEO P OMPERM AIER

contexts and periods. Many scholars have studied the consumer

credit activity of the Jewish communities that, for a long time,

were the most important lenders in many cities across Europe.

Many others have concentrated on the Monti di Pietà, institutions

of Christian inspiration, created in ideological opposition to what

was called the “Jewish usury.” These two essentially different

lenders often worked simultaneously in the same market, within

the borders of the same cities. They usually coexisted without

undue competition, since they eventually managed to diversify

their offers to meet the needs of different customers.2

Research about real-estate credit, particularly as associated with

the socioeconomic role of notaries, is also abundant. The pioneering

work of Hoffman et al. proves that between the eighteenth and

nineteenth century, French notaries were at the center of an extensive

private network in which they acted as brokers, matching lenders with

borrowers and certifying borrowers’ creditworthiness. Their research

shows that notaries compensated for the absence of banks, acting as

financial intermediaries and fostering economic development.3

We are now much better informed about the non-intermediated

peer-to-peer credit market that involved private individuals in dense

and extensive networks. In pre-industrial Europe, these networks

were at the center of economic life; financial exchanges were sustained

through strong norms of collaboration, fairness, and solidarity—in

the context of what has been defined as a “moral economy.”4

Notwithstanding the breadth of this literature, a large part of

the population is often excluded from the analysis. We still know

2 Giacomo Todeschini, La banca e il ghetto: Una storia italiana (secoli XIV–XVI) (Bari, 2016),

33–36; Reinhold C. Mueller, “The Jewish Moneylenders of Late Trecento Venice: A Revi-

sitation,” Mediterranean Historical Review, X (1995), 202–217. For the Monti di Pietà, see

Carmelo Ferlito, Il monte di Pietà di Verona e il contesto economico-sociale della città nel secondo

Settecento ( Venice, 2009); Mauro Carboni, Maria Giuseppina Muzzarelli, and Vera Zamagni

(eds.), Sacri recinti del credito: sedi e storie dei Monti di pietà in Emilia-Romagna ( Venice, 2005);

Carole Bresnahan Menning, Charity and State in Late Renaissance Italy: The Monte di Pietà of

Florence (Ithaca, 1993); Maristella Botticini, “A Tale of ‘Benevolent’ Governments: Private

Credit Markets, Public Finance, and the Role of Jewish Lenders in Medieval and Renaissance

Italy,” Journal of Economic History, LX (2000), 164–189. Maria Giuseppina Muzzarelli, Il denaro e

la salvezza: L’invenzione del Monte di Pietà (Bologna, 2001), 189–245.

3 Hoffman, Postel-Vinay, and Rosenthal, Priceless Markets: The Political Economy of Credit in

Paris, 1660–1870 (Chicago, 2000); idem, Dark Matter Credit. See also Elise Dermineur, “Trust,

Norms of Cooperation, and the Rural Credit Market in Eighteenth-Century France,” Journal

of Interdisciplinary History, XLV (2015), 485–506.

4

See Fontaine, Moral Economy.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 515

little about the lower strata of the society: Did they have access to

credit, and if so, which kind of credit? Even the Jewish money-

lenders and the Monti di Pietà, which, on the surface, seemed

poised to meet the demands of the lower classes, often chose to

serve only wealthier customers, a clientele whose patronage was

certainly safer and more profitable. Nor was the real-estate credit

market concerned with the lower classes, which usually lack the

required collateral. Even “informal” or peer-to-peer networks were

often inaccessible to them. Therefore, the literature has disregarded

the credit strategy of a sizeable share of the total population, which

was characterized by pressing needs and constraints. Mollat once

wrote that “the poor in history are voiceless individuals … hidden

in the folds of time,” because of the lack of sources—hence, the

importance of new perspectives that might portray the credit market

as more flexible and articulated than heretofore supposed.5

Inns and bastioni were the point of reference for a specific

demand for credit, in the context of what this article calls the

“handkerchief” economy (handkerchiefs being the most pawned

objects). It was characterized by the typically small amounts

loaned, the high frequency of their requests, and their mixed

nature, halfway between credit and barter. The study of this eco-

nomic context is of crucial importance in retracing the needs and

financial strategies of the lower classes. Moreover, the long lists of

objects pawned and stocked in the warehouses of inns and bastioni

provide us with an extraordinary insight into the material culture

and consumer behavior of the eighteenth-century Venetian pop-

ulation. This analysis aims to fill a gap in the current literature

about the early modern period from that point of view.6

5 Vittorino Meneghin, I Monti di Pietà in Italia dal 1462 al 1562 ( Venice, 1986); Massimo

Fornasari, Il ‘thesoro’ della città: il Monte di pietà e l’economia bolognese nei secoli XV e XVI

(Bologna, 1993), 24; Muzzarelli, Il denaro e la salvezza, 198–204; Michel Mollat du Jourdin,

“La notion de pauvreté au Moyen Age: position de problèmes,” Revue d’histoire de l’Église de

France, LII (1966), 5–23.

6 For the material culture of the lower strata of the society, see John Styles, “Lodging at the

Old Bailey: Lodgings and their Furnishing in Eighteenth Century London,” in idem and

Amanda Vickery (eds.), Gender, Taste and Material Culture in Britain and North America,

1700–1830 (New Haven, 2006), 61–80; Patricia Allerston “Reconstructing the Second-Hand

Clothes Trade in Sixteenth- and Seventeenth-Century Venice,” Costume, XXXIII (1999),

46–56; Paula Hohti, “‘Conspicuous’ Consumption and Popular Consumers: Material Culture

and Social Status in Sixteenth-Century Siena,” Renaissance Studies, 24–25 (Nov. 2010),

654–670.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

516

| MA TTEO P OMPERM AIER

INNS AND BASTIONI IN THE URBAN CONTEXT The problem of

meeting the demand from the poorer classes for low-cost credit

affected past societies as much as it affects those of the present.

Consider, for instance, the microcredit programs in several under-

developed countries since the 1980s: They often proved to be

unsuccessful in reaching the vulnerable poor, sometimes even

being detrimental to their interests.7

In the early modern period, this dire need for petty credit was

exacerbated by the scarcity of money in circulation. Moreover,

those who had cash usually preferred to invest it in operations of

relatively low risk and high return, rather than becoming entangled

in an endless series of small, scattered operations. The first lenders to

respond to the plight of the poor were private individuals who

were in daily contact with them for professional reasons; shop-

keepers, lodging-house keepers, and innkeepers became the first

and main providers of petty consumer credit, taking advantage of

what proved to be a profitable investment opportunity.8

Innkeepers were usually prominent and popular individuals

within a community if only because of the importance of their

premises to everyday life. They provided space for clients to store

their goods and acted as brokers for commercial deals and transac-

tions, “using their knowledge of the market to match buyers and

sellers from distant areas who would not have known each other.”

Because of the critical role that they played within the market,

innkeepers were often among the wealthiest men in the commu-

nity, and they usually had ready cash. To make ends meet, many

people went to taverns and inns to ask for money, securing their

loans with everyday objects of limited value.9

In Venice, innkeepers and bastioneri (the managers of the bas-

tioni, or warehouses where take-away wine was sold) assumed this

Sajeda Amin, Ashok Rai, and Giorgio Topa, “Does Microcredit Reach the Poor and Vul-

7

nerable? Evidence from Northern Bangladesh,” Journal of Development Economics, LXX (2003),

59–82; Milford Bateman, Why Doesn’t Microfinance Work? The Destructive Rise of Local Neolib-

eralism (New York, 2010).

8 Muldrew, Economy of Obligation, 98–103, 40; Attilio Milano, “I ‘banchi dei poveri’ a

Venezia,” La rassegna mensile di Israel, XVII (1951), 250–265; Richard H. Britnell, “Markets,

Shops, Inns, Taverns and Private Houses in Medieval English Trade,” in Bruno Blondé et al.

(eds.), Buyers and Sellers: Retail Circuits and Practices in Medieval and Early Modern Europe

(Turnhout, 2006), 109–124.

9 Marino Berengo, La società veneta alla fine del Settecento: Ricerche storiche (Florence, 1956),

69–71.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 517

dual function of primary-goods suppliers and moneylenders for

the lower classes. Yet, the Venetian case proves to be significantly

different from others. The Venetian public authorities did not sim-

ply tolerate or perfunctorily regulate this pawnbroking activity;

they officially recognized and institutionalized it, placing it under

the strict judicial control of the Provveditori e Sopraprovveditori alla

Giustizia Nuova, charged specifically with managing the wine mar-

ket and all activities related to it. In doing so, the Republic

allowed this system to grow and develop over time. The Venetian

inns were all located in a few parishes near the Rialto Bridge and

St. Mark’s Square, respectively the commercial and administrative

centers of the city. Here they enjoyed a lawful monopoly in food,

wine, and hospitality. As stated in their mariegola (the statutes of the

guild), inn services targeted a particular clientele, composed specif-

ically of wealthy people and foreigners, excluding apparently the

Venetian population at large. It stated that “the public authorities

ordered the establishment of the inns for the needs of foreigners

and for the comfort of morbinose [happy] and wealthy people.”10

For their part, the bastioni were scattered throughout Venice,

being at the core of the daily life of almost all the seventy-one

Venetian parishes. Whereas inns offered their customers a place

to eat, drink, and sleep, the bastioni could only sell wine to take

away. Yet, although the public authorities promoted domestic

wine consumption for reasons of security and public order, the

population seemed to treat the bastioni as places of sociability,

where people could meet, drink, talk, and, in case of need, ask

for loans.

Beyond the need for credit, wine in the early modern period

was a primary commodity characterized by inelastic demand. It

was a basic part of the daily diet, particularly among the lower

classes. Innkeepers and bastioneri were at the crossroads of three

different but equally important markets, namely, wine, credit,

and second-hand goods. Although it seems unusual, or illogical,

10

I Provveditori alla Giustizia Nuova (the superintendents and chief superintendents of the

Giustizia Nuova) worked with their supervisory body and appeal court, Sette Savi e Sopraprov-

veditori alla Giustizia Nuova (the seven sages and chief superintendents of the Giustizia Nuova).

Compilazione delle leggi, prima serie, b. 299, reg. 1, f.o 104, May 27, 1320, Archivio di Stato

di Venezia (hereinafter, ASVe). Giustizia Nuova (hereinafter, GN), b. 2, reg. 2, f.o 48r,

ASVe. Morbinose literally indicates people who want to laugh and make jokes. Arti, b. 430,

f.o. 95r, ASVe.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

518

| MA TTEO P OMPERM AIER

their conjunction is a key factor of this system. It integrated the

daily habits of individuals and their need for credit within a single

market. Every day, a large number of objects were pawned in

the inns and bastioni of the city, while hundreds of items not

redeemed in time by their owners were sold through public auc-

tions. This system allowed the poorer classes to have access also to

a dynamic and efficient second-hand market, one of the most

important prerequisites for the development of an efficient credit

market.11

“The innkeepers and tavern-keepers of

ORIGINS AND FUNCTIONS

this city have the right, and the freedom to take, and ask for a

pawn from those that have eaten and drunk in their taverns, and

they could also take their coats, and other things.” This rule,

written on the first page of the statutes of the bastioneri, is prob-

ably the first allusion to this credit activity. Unfortunately, it is just

an eighteenth-century copy of an older and non-dated parchment

that is almost certainly lost. It is undoubtedly older than the insti-

tution of the first bastione, established by the Republic in 1495. In

fact, none of the documentation produced before this date men-

tions the bastioneri, just innkeepers and generic tavern-keepers

(tavernieri). Nonetheless, the bastioni rapidly became the most

important locations for this unusual credit activity, to such an

extent that during the eighteenth century, 97 percent of total

lending exchanges took place in them.12

The first source related to this activity dates back to April 29,

1368. This rule, written by the Giustizieri Nuovi, specified that

innkeepers had to ask for collateral from those who bought more

than 100 soldi (5 lire) of wine on credit. An explicit reference to a

11 Malvasie and other more precious wines were not considered staples. Hence, their prices

were neither fixed nor subject to market fluctuations. The wine sold in the bastioni, called

terraneo, came from the Venetian mainland, imported for the poorer classes of the society. This

combination of markets was particularly efficient given the high consumption of wine in the

population at the time. For an estimate of the average wine consumption everyday per person

in 1683 (1.6 liters ), see Ugo Tucci, “Commercio e consumo del vino a Venezia in età

moderna,” in Il vino nell’economia e nella società italiana medioevale e moderna (Florence, 1987),

198–199. Tucci’s figure seems slightly exaggerated: At the beginning of the eighteenth

century, wine consumption was about 0.8 liter a day per person. See Pompermaier, “‘Le

vin et l’argent’: osterie, bastioni et marché du crédit à Venise au XVIIIe siècle,” unpub.

Ph.D. diss. (University of Venice, 2019), 107.

12 Arti, 405ter, f.o 1r, ASVe.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 519

more articulated lending system, regulating custody of the objects

pawned and imposing restrictions on their auction, dates from

April 2, 1388. This law established that innkeepers had to keep

an inventory of all the pawned objects in their warehouses and

forbade them from selling objects received as collateral without

first showing them to the magistrates of the Giustizia Nuova.

Any surplus derived from these sales—any profit that exceeded

the credit offered for them—had to be returned to the borrowers,

since they were the actual owners of the items sold. This law is

noteworthy because, even if it merely regulates a series of details,

it proves that innkeepers were already professional lenders work-

ing in the context of a “formalized” activity, at least since the end

of fourteenth century—just six years after Jewish moneylenders

were allowed in the city (1382) and more than seventy years

before the first Monte di Pietà was instituted in Perugia.13

Several factors pushed the Republic to promote this lending

activity and to include it within an institutional framework. The

first were its social implications; as stated in the documentation, it

was “officially authorized and formalized with the sole charitable

purpose that the poor could provide for their daily needs.” The

public authorities quickly understood that it also promoted wine

consumption, because people would keep going to inns and bas-

tioni to buy wine, even if they did not have the cash to do so.

Moreover, the more wine innkeepers and bastioneri sold, the

more they had to import into the city. Therefore, the Republic

was able to increase its annual revenue from the duty that every-

one had to pay when they brought wine into the capital. The

wine duty was an important entry in the annual budget of

the Republic; it represented, on average, 6 or 7 percent of all

annual revenue and 25 percent of total duties in the eighteenth

century.14

13 The rule was, “No innkeeper or tavern keeper may henceforth sell on credit more than

100 soldi of wine to anyone without asking for collateral” (author’s translation): GN, b. 2 reg. 3,

f.o 143v, ASVe. 1 lira = 20 soldi = 240 denari. GN, b. 2 reg. 3, f.o 140v, ASVe. Meneghin, I Monti di

Pietà in Italia dal 1462–1562, 19. Jews were officially expelled from Venice between 1397 and

1509, but they settled in the nearby city of Mestre. See Eliyahu Ashtor, “Gli inizi della Comu-

nità ebraica a Venezia,” La rassegna Mensile di Israel, XLIV (1978), 683–703.

14 GN, b. 2 reg. 4, f.o 329v;,

GN, b. 2 reg. 4, f.o 329v; GN, b. 2 reg. 4, fo. 191r, July 6, 1743,

ASVe. An estimate for the decade between 1718 and 1727 shows a duty of about 386,500

ducats per year for about 65,900 anfore of wine (about 39,600,000 liters).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

520

| MA TTEO P OMPERM AIER

As already mentioned, the uniqueness of this credit activity

does not lie specifically in its most practical feature, a pawnbroking

activity run by wine sellers, but in its special relationship with the

public authorities. Innkeepers and, at the end of the fifteenth cen-

tury, bastioneri had to follow a strict procedure, from the pawning

of an item to its redemption or sale through the auctions, under

the supervision of a specific magistracy. The public and “official”

nature of this activity strongly affected its development, since

lenders did not need to operate in the shadows, and borrowers

knew that they were protected by law. This offer of credit thus

had the perfect conditions to thrive. Moreover, its “official” nature

is the only reason why today we can rely on a rich and detailed

documentation to illustrate it.15

SMALL AMOUNTS AND BIG EFFECTS As in modern pawnshops, inn-

keepers and bastioneri provided secured loans to their customers,

using personal property as collateral. By helping to reduce infor-

mation asymmetry, this procedure also reduces the risk for lenders.

Each loan corresponded to just a fraction of the estimated value of

the object used as collateral—usually between one-half and

one-third of the whole. Whenever borrowers defaulted in their

debt, lenders were able to recover their investment easily by selling

the collateral.

The analysis of the archival documentation suggests that

borrowers did not have to pay any interest on their loans. Even

though public authorities did not specify or impose any interest

rate, this service was not provided for free. In his book Delle Istitu-

zioni di Beneficienza nella Città e nella Provincia di Venezia (On the

Charitable Institutions in the City and Province of Venice), Count

Pierluigi Bembo—mayor of Venice from 1860 to 1866 and mem-

ber of the Chamber of Deputies of the Kingdom of Italy from 1867

to 1876—provides a detailed description of the lending activity of

inns and bastioni. Intending to celebrate the Monte di Pietà of

Venice, Bembo took great pains to describe what he considered

15 For the (“informal”) credit activity of innkeepers in Siena, see Hohti, “The Innkeeper’s

Goods: The Use and Acquisition of Household Property in Sixteenth-Century Siena,” in

Michelle O’Malley and Evelyn Welch (eds.), The Material Renaissance (New York, 2007),

242–259.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 521

to be the terrible time when innkeepers and bastioneri were free to

indulge their greedy impulses. He claimed that at least one-third of

each credit operation was supplied in wine, and lenders profited

from the difference between its purchasing and selling price. The

wine was of such poor quality, however, that it generated an extra

loss in relation to the price, which was established monthly by the

public authorities. Bembo argued that the quality of the wine, the

short duration of the loans, and the presence of fixed costs made

this credit circuit particularly disadvantageous for borrowers, esti-

mating an incredible interest rate of 120 percent per year.16

Beyond this likely exaggerated and “romanticized” criticism

(Bembo claimed that the contaminated wine was capable of caus-

ing horrible diseases), his research is an extremely useful exposé of

how this credit activity worked, suggesting a way to estimate

roughly the interest rate charged on each loan. First, we need to

know the price of wine paid both by a lender—say, a bastionere—

and his customers. At that time, when wine was considered a

necessity, the public authority set its retail price each month to

avoid speculation; archival documentation allows us to retrace

an almost complete price series of wine throughout the eighteenth

century. From the ledger of a bastionere, we can also retrace a

series of wine prices on the Venetian mainland, at least in the

second half of the century. Comparison of these two values reveals

that the average profit of a bastionere in 1781 was about 1.42 soldi

per liter, including transport costs and duties.

Considering that one-third of each loan was supplied in wine,

1.42 soldi per liter means that in 1781 the interest rate on a loan was

about 7 percent on a quarterly basis and 28 percent per year. This

rate cannot be treated as a fixed value since it varied according to

the price of wine and its quality. The fact that these loans consisted

at least partly of wine is significant. It proves that they were a form

of credit for the poor, being functional for small, daily credit

16 Pierluigi Bembo, Delle istituzioni di beneficienza nella città e provincia di Venezia ( Venice,

1859), 135, 136. Bembo’s information seems reliable, since it is confirmed by Giuseppe Boerio

and Daniele Manin, “Dizionario del dialetto Veneto,” in idem (eds.), Dizionario del dialetto

veneziano di Giuseppe Boerio ( Venice, 1829), under the search term Magazèn. The monthly

wine monitoring was another task of the Giustizia Nuova, in concert with the judiciary of

the Governatori alle Entrate.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

522

| MA TTEO P OMPERM AIER

operations linked to consumption and subsistence but disadvanta-

geous in the case of larger amounts.17

Estimating the average value of loans supplied by inns and

bastioni would be a confirmation of this finding and would allow

us to understand the “quality” of the credit circuit and the nature

of the individuals and objects involved. The accounting docu-

ments produced by the officials of the Giustizia Nuova—the

numerous inventories of pawned items held in the warehouses

of bastioni and inns and the reports drawn up during the public

auctions—prove useful for this purpose. An extensive process of

data collecting and processing of more than 30,000 entries distrib-

uted throughout the eighteenth century finds the average and

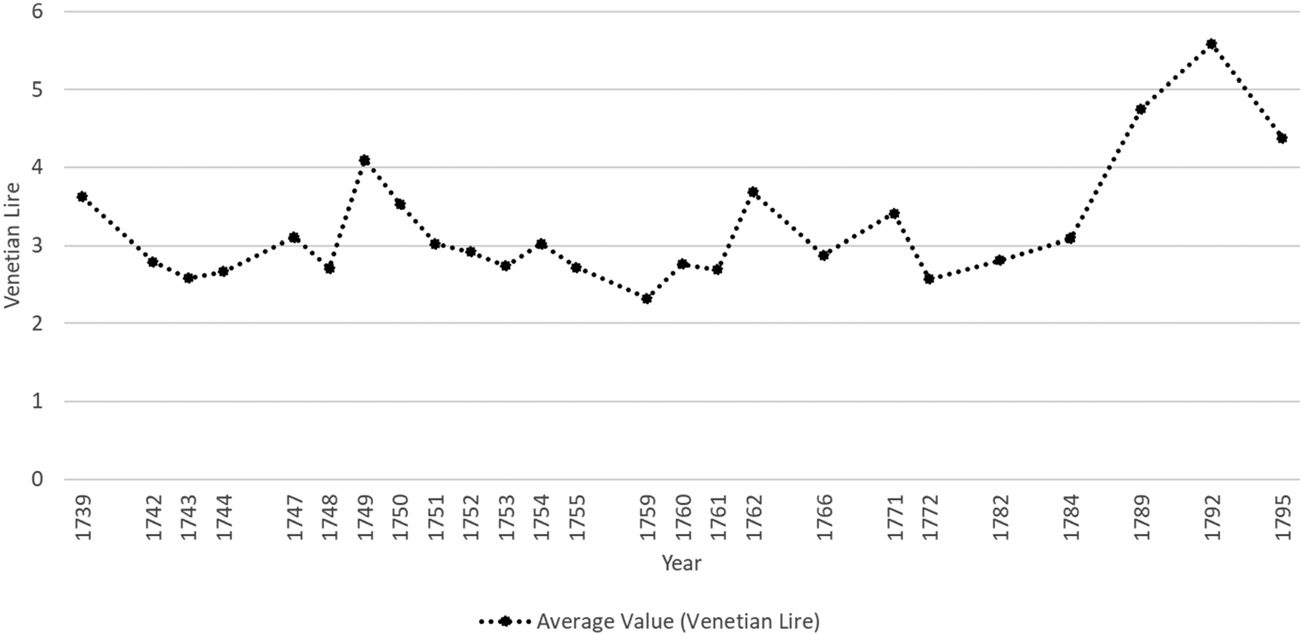

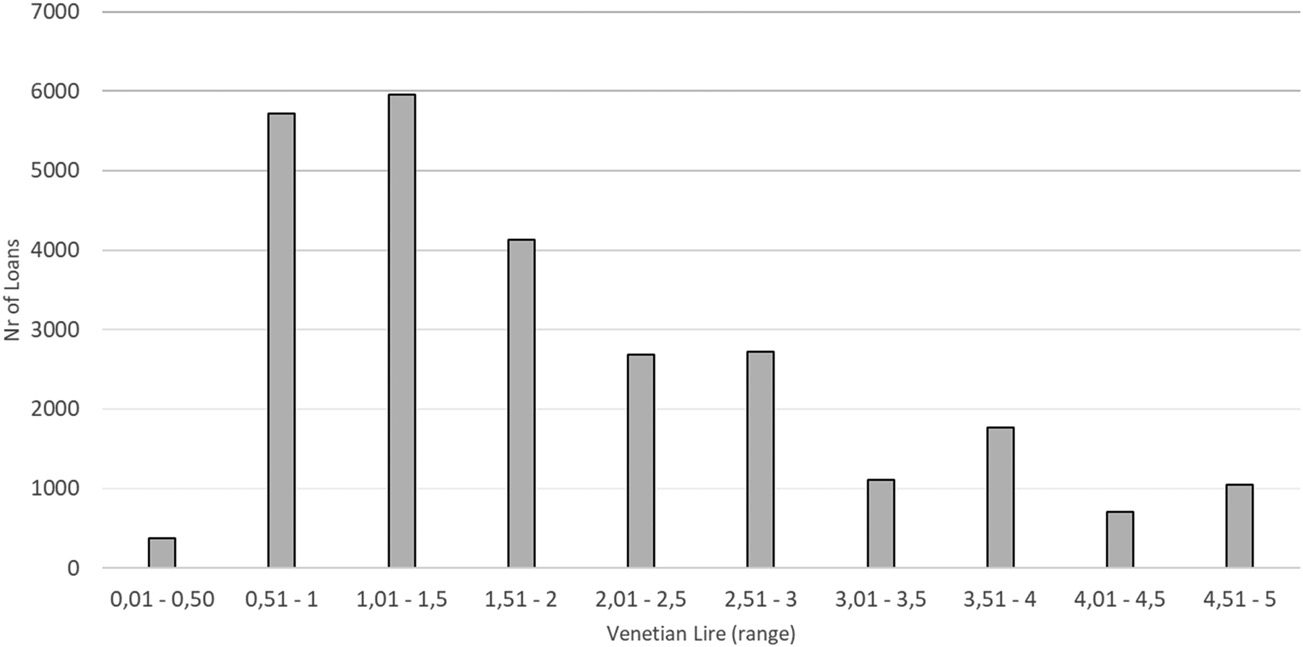

median value of a loan as equal to 3.32 lire and 2 lire, respectively

(see Figure 1).

As the significant difference between average and median

values suggests, the standard deviation is rather high, because loans

range from a minimum of one soldo (1/20 lire) to more than 200

lire. In any case, 96 percent of the loans were worth less than 10

lire, and in seven cases out of ten, even less than 3 lire. As Figure 2

shows, the majority of the loans—about 16,000 operations, or

52.14—of the total sample—were between 10 soldi (half a lira)

and 2 lire, thus confirming that this credit activity belonged to

the lower classes of society. Moreover, most loans involved much

lower values than the overall average due to the fact that although

transactions above 10 lire represented only 4 percent of cases, they

represented about 25 percent of the total volume of credit.18

But what did it mean to obtain a loan of 3.32 lire? In the mid-

eighteenth century, a person could buy a carpetta, a particular type

of long skirt typical of commoners, a vestina, a jerkin, or even two

17 Bembo, Delle istituzioni, 139; GN, b. 14, reg. 42, ASVe. As mentioned, a bastione could sell

terraneo wine, produced on the Venetian mainland. The most common type of terraneo wine

came from Padua, Vicenza, Mestre, and the Friuli region, each one selling at a different price.

A bastionere’s profit was hardly large given the several fixed costs that he had to meet—for

instance, the 1,500 to 3,000 lire a year in rent for the bastione, depending on its size, and the

200 lire per month for the salaries of four men, at that time the average number of employees.

The wage of a bastionere in 1732 was 130 to 150 ducats a year; other workers earned about 90

to 110 ducats and apprentices about 20 to 30 ducats: Governatori alle entrate, b. 447, reg. “Cost-

ituti dei bastioneri sul numero degli uomini impiegati in ogni bastione, e loro salario,” ASVe.

18 Between 1767 and 1771, the average salary of an unskilled construction worker was

about 40.91 soldi a day, a little over 2 lire; Andrea Zannini, “L’economia veneta nel Seicento:

Oltre il paradigma della ‘crisi generale,’” in La popolazione nel Seicento (Bologna, 1999), 490.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 523

Fig. 1 Average Value of an Eighteenth-Century Loan

SOURCE Giustizia Nuova, b. 3 regg. 5, 6; b. 6, b. 7, b. 9, b. 16, b. 17, b. 18, b. 22, b. 35 b. 40, b.

41, b. 42, b. 43, Archivio di Stato di Venezia.

pairs of cotton hose from the shop of a second-hand dealer. Wine,

however, provides the most logical and immediate point of com-

parison since at least one-third of each loan was supplied in this

product. During the eighteenth century, a person with about 3 lire

could purchase between 8 and 14 liters of wine. Between 1718

and 1727, Venice imported an average of 40 million liters of wine

every year to meet the demand of a population of about 145,000

Fig. 2 Number of Loans per Range of Value

SOURCE Giustizia Nuova, b. 3 regg. 5, 6; b. 6, b. 7, b. 9, b. 16, b. 17, b. 18, b. 22, b. 35 b. 40, b.

41, b. 42, b. 43, Archivio di Stato di Venezia.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

524

| MA TTEO P OMPERM AIER

to 150,000 inhabitants. From these data, we can estimate an average

consumption per capita of about 0.78 liters per day for every man,

woman, and child living in the city. Considering that each house-

hold, on average, comprised about five individuals, daily consump-

tion was about 3.9 liters of wine per day. A loan of 3.32 lire would

have purchased enough for about two or three days.19

But how were people most likely to use these small loans?

The sources suggest that this money primarily financed individual

wine consumption and sociability in an inn or a bastione. For

instance, in May 1761, when Antonio Maggini organized a dinner

for friends at the della Luna inn, he left a piece of silver cutlery as a

pledge since he had no cash. A few years later, Paola Lanari com-

plained to the Giustizia Nuova that she had never been able to

redeem her “inbotida di seda latesina bella” (most likely a beautiful

blue silk blanket), pawned a few months earlier at an inn in Rialto,

for which she received “a single bottle of wine.” These episodes,

among others, support what the official documentation states, that

the puropose of this credit circuit was to guarantee the poorest

people access to basic goods (usually glossing over the advantages

for the public coffers).20

Although one-third of each credit was always provided in

wine—every loan contributing, at least theoretically, to on-site

or domestic consumption—some loans also came in cash, which

was evidently not spent in the bastione or inn. As a case in point,

a thirty-five-year-old goldsmith named Bortolo Bodai went to

19 For a definition of carpetta, see Boerio and Manin, Dizionario del dialetto veneziano, 791; for

the other objects, GN, b. 42, inventory of the bastione of San Stae, ASVe. Tucci, “Commercio e

consumo del vino a Venezia in età moderna,” 202, 186. The high level of wine consumption

in Venice is evident in an official assessment of 1730, which estimated that a man and a

woman aged between eighteen and fifty drank about 1.34 and 0.69 liters of wine a day,

respectively. Daniele Beltrami, Storia della popolazione di Venezia dalla fine del secolo 16 alla caduta

della Repubblica (Padua, 1954), 186. This information about the pace of wine consumption

coincides with bastionere Pietro Bareggio’s declaration to the magistrates of the Giustizia

Nuova in 1730 that the bastioneri did not have registers of items pawned that indicated the

money they lent to each borrower, because once an object was pawned “in one or two days

they [the borrowers] come and redeem their stuff”: GN, b. 33, unnumbered folios, July 30,

1731, ASVe.

20 GN, b. 28, unnumbered folios, February 23, 1768, ASVe. Lanari referred to a “bozza” of

wine, which probably indicates not only the container but also the volume, roughly 2.5 liters.

GN, b. 2 reg. 4, f.o 329v, GN, b. 28, unnumbered folio, 29 May 1761, ASVe. Antonio Maggini

paid 50 Venetian Lire for the dinner.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 525

trial in 1762 for pawning in a bastione a series of silver objects that

eventually were found out to be worthless “pure metal.” Over

time, Bortolo had accumulated a debt of more than 160 Venetian

lire for food and wine in the bastione, as well as for 50 lire that he

obtained “on several occasions in actual cash,” about one-third of

the total loan that he had eventually spent elsewhere for other

unspecified needs.21

Wine was clearly important to social and economic life in

early modern Venice, and the connection between credit and

wine emphasizes the role of bastioni and inns in the urban context.

The average amount of the loans is a further confirmation of the

exceptional nature of this credit, which, thanks to its “mixed”

nature, halfway between credit and barter, was really aimed at

the poorer population of the city and thus often underestimated,

if not completely absent, from other credit circuits.

OBJECTS SOLD, PAWNED, AND REDEEMED According to public ordi-

nance, loans could not run for more than three months. If a bor-

rower did not repay his debt in time, the Giustizia Nuova arranged

to sell the item used as collateral at a public auction. Hence,

lenders could potentially invest their money up to four times a

year, even if the law required unredeemed objects to be sold at

least every six months. The sources, however, clearly show that

the reality was different from the official instructions mainly for

two reasons: First, because participating in auctions was costly,

lenders tried to accumulate as many pawned items as possible

before selling them. Second, the large quantity of unredeemed

objects made auctions extremely long; sometimes a single bastione

needed longer than a month to sell all its items.

Between January 1745 and December 1754, the Giustizia

Nuova organized 930 auctions during which fifty-six bastioni

and sixteen inns sold more than 530,000 objects for a total profit

of more than 1,296,000 Venetian lire. Altogether, auctions in this

period occurred on about 2,500 days (out of 3,652), an astonishing

number considering the 520 Sundays and the 216 days reserved

for the sale of the unredeemed objects pawned to the Jewish

21 GN, b. 35, unnumbered folios, September 20, 1760, ASVe. To compare the amount of

Bortolo’s reimbursement, the monthly wage of a bastionere at that time was about 170 lire

(Governatori alle entrate, b. 447, ASVe).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

526

| MA TTEO P OMPERM AIER

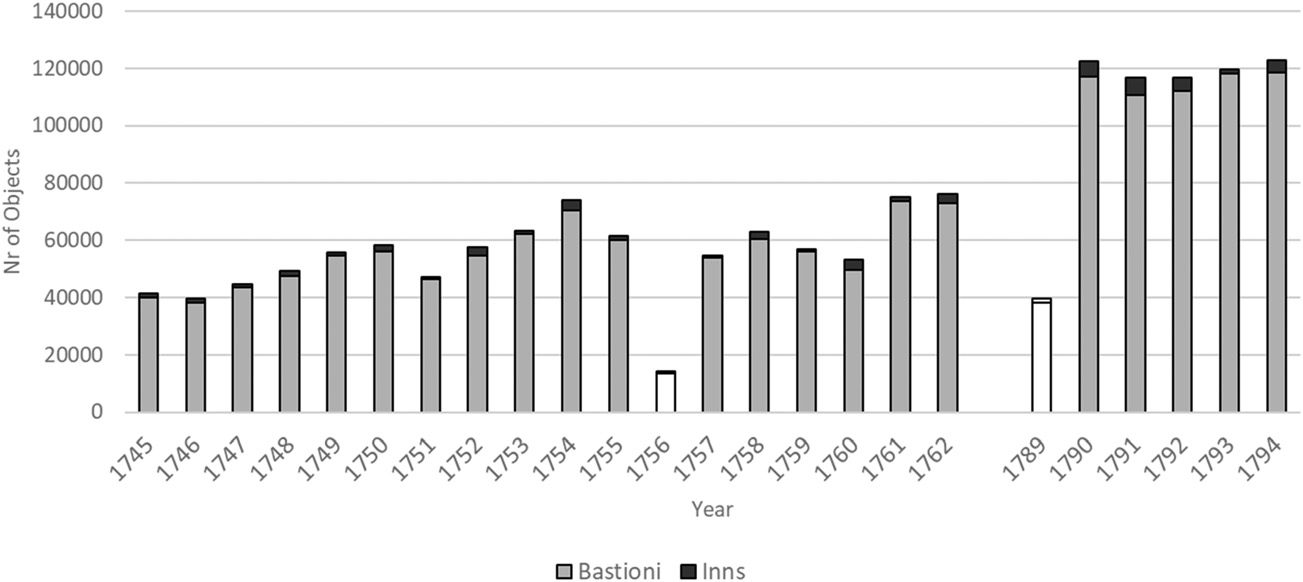

Fig. 3 Number of Items Sold through the Public Auctions, 1745–1762

and 1789–1794

NOTE White columns indicate partial data.

SOURCES Giustizia Nuova, b. 3 regg. 5, 6; b. 6, b. 7, b. 9, b. 16, b. 17, b. 18, b. 22, b. 35 b. 40,

b. 41, b. 42, b. 43, Archivio di Stato di Venezia.

moneylenders (three days a month), leaving, on average, only

about forty days per year without any sales. In this period, each

bastione participated in an average of 14.8 auctions, about one

every eight months, and the sixteen inns participated in only

5.8, one every two years. This schedule definitively proves that

the obligation to sell their items at least every six months was

generally disregarded.22

The data also demonstrate the disproportionate credit activity

of bastioni and inns. In fact, out of the 531,686 items sold in the

period mentioned above, bastioni had pawned 514,123 of them

(96.7 percent) and inns 17,563 (3.3 percent). The reason behind

this difference is more than likely the dissimilar social functions

of these two businesses—inns primarily concerned with foreigners

and wealthy people and the bastioni predominantly with cus-

tomers in the lower classes. Each bastione was, together with

the well and the bakery, central to the parish economy, an impor-

tant part of the daily routine that satisfied many of the basic needs

of Venetians. The data relating to public auctions testify to the

22 GN, b. 2, reg. 4, f.o 11r; GN, b. 2, reg. 4, f.o 139v; GN, b. 40, 42, 43; GN, b. 44, reg. “Per il

Magistrato de’ Provveditori alla Giustizia Nova contro il Consorzio Mercanti Bastioneri,”

f.o 160, ASVe.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 527

enormous volume of objects, money, and wine exchanged in this

credit circuit. The sources allow us to retrace almost completely

the trend of the auctions in two different periods of the eighteenth

century, between 1745 and 1763 and in the first years of the 1790s

(Figure 3). Every year, an extremely large number of objects was

sold, ranging from about 40,000 in 1745 to more than 120,000 in

1794. Figure 3 shows a considerable increase in the number of

objects sold between 1790 and 1795, possibly due to an increase

in the number of items pawned overall or to a drastic reduction

in the loan-repayment rate.23

Public auctions were popular events, well attended both by

private citizens looking for good deals and by professionals looking

for items that they could resell. They began at the ora di terza

(9:00 AM) and ended at noon, in the campo (square) adjacent to

the church of San Giovanni di Rialto the commercial heart of the

city. The few sources available in the archives present a detailed

description of frenetic and chaotic activity there. The comandador

(the auctioneer) stood on a wooden platform, showing and

describing hundreds of objects to a dense crowd who shouted their

bids back at him, while those who had owned the objects a few

months earlier hurled their insults and complaints about inade-

quate prices. Participants, especially the most inexperienced, could

easily be confused and misled. Elisabetta Zechini, for one, who

was in the market for household items, became so overwhelmed

by spirit of competition that she eventually ended up buying

something of “absolutely no value.” Her only recourse was to

ask the Giustizia Nuova for a refund on the grounds that so fraud-

ulent a “method of public sale, [which did not] allow those who

buy to see [the object on sale], [should not] be authorized by

law.”24

Among the ranks of bidders were not only private citizens

with various levels of experience but also strazzaroli, members of

the Venetian guild of second-hand dealers, who filled their shops

(or carts or bags) with goods for resale. The strazzaroli had their

own reserved area next to the stage of the auctioneer to restrict

their attempts to prevent others from participating in auctions,

23 Ennio Concina, Venezia nell’età moderna: Strutture e funzioni ( Venice, 1989), 168.

24 GN, b. 1, f.o 216v. ASVe. Unfortunately, Zechini’s trial is not dated, but many elements

suggest that it dates back to the second half of the eighteenth century: GN, b. 28, reg. “Sup-

pliche senza data,” ASVe.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

528

| MA TTEO P OMPERM AIER

keeping prices low. Not by chance did Giovanni Antonio Bagietti

go to the shop of a strazzarolo on the Calle dei Botteri in San Cas-

siano to retrieve the silver watch that he had pawned months ear-

lier elsewhere; Bagietti declared a loss of 13 lire compared to the

value of the loan.25

Public auctions were key events in the urban economy; they

allowed many low-cost items to be recirculated as pawned collat-

eral. As both supportive of and supported by the diffused need for

credit, the auctions completed the circle of exchanges that nour-

ished the handkerchief economy. Despite the high numbers, the

public auctions sold only those objects not redeemed in time by

their owners. Using these figures, we can estimate the total vol-

ume of exchanges and the redemption rate.

As in modern pawn shops, a loan’s link to personal items

makes borrowers subject to complex economic and psychological

phenomena. The rate of redemption is consistent with both a

rational decision-making model and a utility-maximization func-

tion in which sentiment plays an important part. For instance, loss

aversion, a concept according to which individuals consider avoid-

ing economic loss to be more important than pursuing a compa-

rable gain, readily applies in this case. Borrowers had the choice to

repay a loan or not. Whenever lenders’ estimates of an item’s value

was higher than their own, they had the option not to redeem it

but to try to buy it back for less at the public auction. By contrast,

when lenders’ estimates were too low, they might be more

inclined to repay the loan and redeem the object, thus avoiding

the risk of losing it at the auction. Given the characteristics of this

credit circuit, mere survival must have been a consideration for

many of the people involved—individuals who, for either physical

reasons (disability, old age, etc.), social ones (vagrants), or profes-

sional ones had neither money nor any hope of getting any in the

future. Hence, to get through difficulties, they would have

pawned objects deemed dispensable in the daily, exhausting fight

for survival. In this context, the chance of repaying a loan was

extremely unlikely.26

25 GN, b. 28, reg. “Suppliche senza data”; GN, b. 17, unnumbered folios, 21/05/1787, ASVe.

Susan P. Carter and Mary P. Skiba, “Pawnshops, Behavioral Economics, and Self-

26

Regulation,” Review of Banking and Financial Law, XXXII (2012), 193–220.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 529

Assessing the rate of redemption throughout the entire period

requires several different strategies: (1) comparing both the value

and the number of the objects stored in specific bastioni with

the corresponding figures at the auction in which they were

offered and then (2) comparing the overall stock held in all the

bastioni and inns. Although these estimates inevitably contain

inaccuracies that tend toward an over- or underestimation of the

actual redemption rate, we can safely claim that between 1745 and

1762, about two-thirds of the loans were reimbursed by the bor-

rowers, and just one-third of all objects pawned were sold at auc-

tion. In other words, more than 600 objects were pawned in the

city bastioni every day, and about 400 were redeemed. Each one of

the forty-eight bastioneri lent an average of 41.5 lire—one-third in

wine and a maximum of 27.7 lire in cash—for the approximately

twelve pledges that they received, and they collected 27.6 lire from

the eight objects redeemed by their respective owners.27

Applying the same methodology to the 1790s data, we notice

an increase in the number of items sold through public auctions,

which was probably due to both the general growth in the loans

supplied and the decrease in the redemption rate. Of the 217,000

objects pawned in 1790 and the 248,000 in 1791, the ones sold at

the public auctions numbered 122,000 in 1790 and 116,000 in

1791, about one-half the total in each case. The reasons for this

phenomenon seem to be linked to the overall instability and eco-

nomic decline that plagued the Republic in the last years of its

existence, as well as a general increase in the presence of paupers

and vagrants in the capital.

Applying a redemption rate of two-thirds in the middle of

the eighteenth century and one-half in the 1790s to the data of

the auctions, we obtain an average annual number of 171,551

between 1745 and 1762 and 239,384 for 1790s. These figures are

noteworthy in absolute terms and in the Venetian context per se.

27 Between 1745 and 1762, the average difference between the value of pawned items in

storage and those sold by each bastione shows that the redemption rate was about 68.07 per-

cent. Otherwise, if we estimate the number of pawned items on the basis of their value (cal-

culated from the average value of 3.32 Venetian lire), the rate falls to 53.03 percent. On May

15, 1761, the Giustizia Nuova ordered a check on the total value of the objects stored at the

bastioni’s warehouses, which turned up a total of 771,800 Venetian lire in pawned items: GN,

b. 39, reg. “Contabilità,” unnumbered folios, 15 May 1761, ASVe (2.000 bigonce are about

300.000 liters).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

530

| MA TTEO P OMPERM AIER

During the eighteenth century, the city had a population of about

150,000 inhabitants, divided into about 25,000 to 30,000 house-

holds. The average number of objects pawned per capita every

year ranged between 1.1 and 1.5, or between 6.8 and 9.5 loans

per household. Given the volume of exchanges and the number

of objects sold every year through public auctions, how could this

credit offering go almost unnoticed for so long?28

THE WEALTH OF THE POOR The average value of the operations

gives an indication of the quality of the objects that were

exchanged in this credit circuit. Once again, the rich corpus of

sources affords a glimpse into the hitherto hidden contents of

Venetian closets and trunks, or at least those objects that Venetians

were willing to sacrifice, permitting analysis of the material culture

of the lower classes in early modern Venice. Although some

objects certainly kept their value better than others, the landscape

of pawned items was not limited to jewelry or precious clothes and

fabrics; on the contrary, these items were in the minority. Hun-

dreds of objects of everyday use, such as handkerchiefs, shirts,

trousers, sheets, and pillows, passed over the counters of the bas-

tioni daily. The few objects banned from pawning were mainly

from the spheres of the sacred (religious ornaments), the public

(objects bearing St. Mark’s stamp, produced by a Venetian magis-

tracy in the performance of its duties), and the military (such as

weapons).29

In 1747, the authorities limited the maximum amount of a

loan for the first time. Since they noticed the presence of several

valuable items that were certainly beyond the reach of the poor,

they set a limit on the amount of money transacted in a single

operation. Innkeepers and bastioneri were forbidden to lend more

28 For a typically brief reference to the auctions, see Patricia Allerston, “L’abito come arti-

colo di scambio nella società dell’età moderna: alcune implicazioni,” in Anna Giulia Cavagna

and Grazietta Butazzi (eds.), Le trame della moda (Rome, 1995), 113–115. No one appears to

have understood the scope and special quality of this credit activity.

29 Renata Ago, Il gusto delle cose: una storia degli oggetti nella Roma del Seicento (Donzelli, 2006),

3–22. As the law states, “It is forbidden to any innkeeper or bastionere, to take as collateral any

of the things and furnishing that are used in the sacred temples or serve as decoration in the

same places, and especially those things marked with [religious] signs. In the same way, it is

forbidden to accept as collateral anything with the stamp of Saint Mark, and especially military

tools, weapons or other things belonging to the ‘house’ [lit. casa] of the Arsenale”: GN, b. 2,

reg. 4, f.o 228r, September 28, 1751, ASVe.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 531

than 10 ducats (62 Venetian lire) per operation, a much higher

limit than the one imposed on the Jewish moneylenders, set at

3 ducats since 1573. Moreover, considering the data used in this

study, only 0.1 percent of all loans supplied during the eighteenth

century exceeded the limit of 62 Venetian lire, thus confirming

that this credit line was functional for small, daily credit but not

at all for larger amounts.30

When an innkeeper or a bastionere was in debt for unpaid

taxes, the Giustizia Nuova kept a record of all the objects that he

stored in his warehouse for possible seizure and sale in case of

insolvency. To conduct these inventories, the Giustizia Nuova

followed two different methods. The fastest and most frequent

method was to register each item by numbering it and indicating

only its value. Sometimes public officers—usually a group of six or

seven assisted by at least one porter—also added information such

as a description of the pawned object and information about the

borrowers. These more accurate inventories enable the construc-

tion of a database of more than 3,400 objects pawned between

1689 and 1798, providing an exceptional opportunity to assess

the material culture of the lower classes from a unique point of

view. The study of consumption usually relies on probate inven-

tories which, as widely discussed in the dedicated literature, tend

to overestimate the richest strata and to underestimate, if not

completely exclude, the poorest ones.31

In this study, the data are divided into two macro-categories,

distinguishing jewelry and metal objects of various types (profes-

sional and household utensils) from clothes, fabrics, and other tex-

tiles such as sheets, blankets, etc. In general, out of the 3,431

objects collected in the database, 2,763 were textiles (84.83 per-

cent) and only 668 non-textiles (15.17 percent). The most numer-

ous objects were handkerchiefs (414), followed by shirts and

30 GN, b. 2, reg. 4, f.o 205r, September 28, 1751; Inquisitori sopra l’Università degli Ebrei, b. 45,

f.o 51v, ASVe.

31 The inventory procedure for items pawned was expensive, between 50 and 60 Venetian

lire: Governatori alle entrate, b. 448, ASVe. For information about the problems related to pro-

bate inventories, see Håkan Lindgren, “The Modernization of Swedish Credit Market, 1840–

1905: Evidence from Probate Records,” Journal of Economic History, LXII (2002), 810–832;

Alice H. Jones, “Estimating Wealth of the Living from a Probate Sample,” Journal of Interdis-

ciplinary History, XIII (1982), 273–300; Sebastian A. J. Keibek, “Correcting the Probate Inven-

tory Record for Wealth Bias,” Working Paper No. 28, Cambridge Group for the History of

Population and Social Structure & Queens’ College (March 2017).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

532

| MA TTEO P OMPERM AIER

blouses (298), hose (220), and doublets (the so-called velade, 210).

Clothing (including accessories like handkerchiefs, hats, shoes,

etc.) is the principal category (2,246 items, 67.46 percent),

followed by textiles for domestic use (574, 16.72 percent). The

clothes classified as feminine (355) include skirts (carpette, 173),

dresses (99), and shifts (26); on the men’s side (558) are mainly

trousers (160), jerkins (velade, 110), shirts (72), cloaks (70), and

coats (48). The analysis of fabrics and colors has to rely on a smaller

sample because such secondary information was reported on only a

few occasions. The clothes were predominantly woolen (213),

followed by silk (179), and printed calico (126), mostly in white

(66), red (50), black (46), and generic “colors” (26).32

As already mentioned, bastioni and inns were located in dif-

ferent parts of the city, offered different kinds of service (with, at

least theoretically, a different degree of sociability), and probably

targeted toward different customers. Hence, we might expect that

the objects pawned and stored in the warehouses to be different

qualitatively, too. Yet their average value is almost identical. As

Table 1 shows, the most common collateral in both bastioni and

inns were the same—clothing, “domestic textiles” (sheets, blan-

kets, pillows, curtains, etc.), and objects (like shoes, buckets, paint-

ings, dishes, coffee makers, etc). The proportion between these

categories, however, differed considerably; clothing represented

more than 80 percent of the total items stored in the warehouses

of the inns and 65 percent of the items in the warehouses of the

bastioni. Domestic and professional textiles, as well as non-textile

objects, were more likely to show up in the bastioni, probably

because the local population had more access to everyday domestic

and professional objects than did traveling foreigners. The reason

why jewels appear to have been pawned only in the bastioni is

more difficult to explain. This comparison suggests that even if

innkeepers and bastioneri had distinctive roles in the credit market

(as already mentioned, less than 3 percent of total loans came from

innkeepers), they were similar in the “quality” of the credit that

they supplied.

In general, even the humblest, most inexpensive objects rep-

resented real money reserves that people in need could quickly

32 For clothes and fabrics, see D. Davanzo Poli, Abiti antichi e moderni dei Veneziani ( Venice,

2001).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

C R E D I T A N D PO V E RT Y I N E A R L Y MO D E R N VE N IC E

| 533

Table 1 Categories of Objects Used as Collateral in Inns and Bastioni

CATEGORY

Clothing

Textiles (domestic)

Objects (non-textiles)

Textiles (professional)

Jewelry

Other and non-specified

Total

BASTIONI

64.56%

11.80%

10.58%

5.60%

1.67%

5.79%

100.00%

INNS

81.77%

6.08%

6.63%

2.21%

−

3.31%

100.00%

pawn. The accumulation of moveable goods was a form of savings,

mostly among the lower classes. This research demonstrates that

the wealth of the poor was not based on the quality of the objects

that they possessed but on their quantity, which was substantial

enough to suggest that the concepts that underlie the idea of

the consumer revolution as generally presented are in need of

rethinking, at least in the Italian context.33

LOANS, OBJECTS, AND PEOPLE The lending activity of Venetian

innkeepers and bastioneri was able to meet several needs that, at

first sight, seem incompatible—supporting the poor in their daily

needs, allowing lenders to make money without usurious prac-

tices, and substantially increasing the flow of money into the pub-

lic coffers. Through understanding the great potential of this credit

line and building an institutional framework to further its develop-

ment, the Venetian authorities demonstrated their well-known

pragmatism. Nonetheless, despite the key elements of the “hand-

kerchief” economy discussed thus far, we still have to determine

who were the real protagonists of this story. What do we know

about those individuals who, as described by the head of the bas-

tione of the Saint Martin, “at lunch time, or in the evening [are]

so crowded that I struggle to deal with them”? Even without

simple answers to this question, we do have some interesting clues.

In July 1702, the Giustizia Nuova commissioned the accountant

Zuanne Orzali to draw up a list of those borrowers who were still

to receive the sopravanzo (surplus) from unredeemed items sold

through the public auctions of 1699 to verify whether the

33 Muldrew, Economy of Obligation, 4; Jan de Vries, The Industrious Revolution: Consumer

Behavior and the Household Economy, 1650 to the Present (New York, 2008).

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

j

i

/

n

h

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

5

2

4

5

1

3

1

9

9

6

8

2

8

/

j

i

n

h

_

a

_

0

1

7

6

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

534

| MA TTEO P OMPERM AIER

difference between the sale price and the value of the loan had

been correctly returned to the borrowers.34

Notwithstanding the considerable data about the credit activ-

ity of innkeepers and bastioneri, Orzali’s list is particularly informa-

tive because it focuses not only on money and items but also on

the borrowers waiting for their cut. Of the 1,762 people listed, 30