Coping with Rising Inequality in Asia

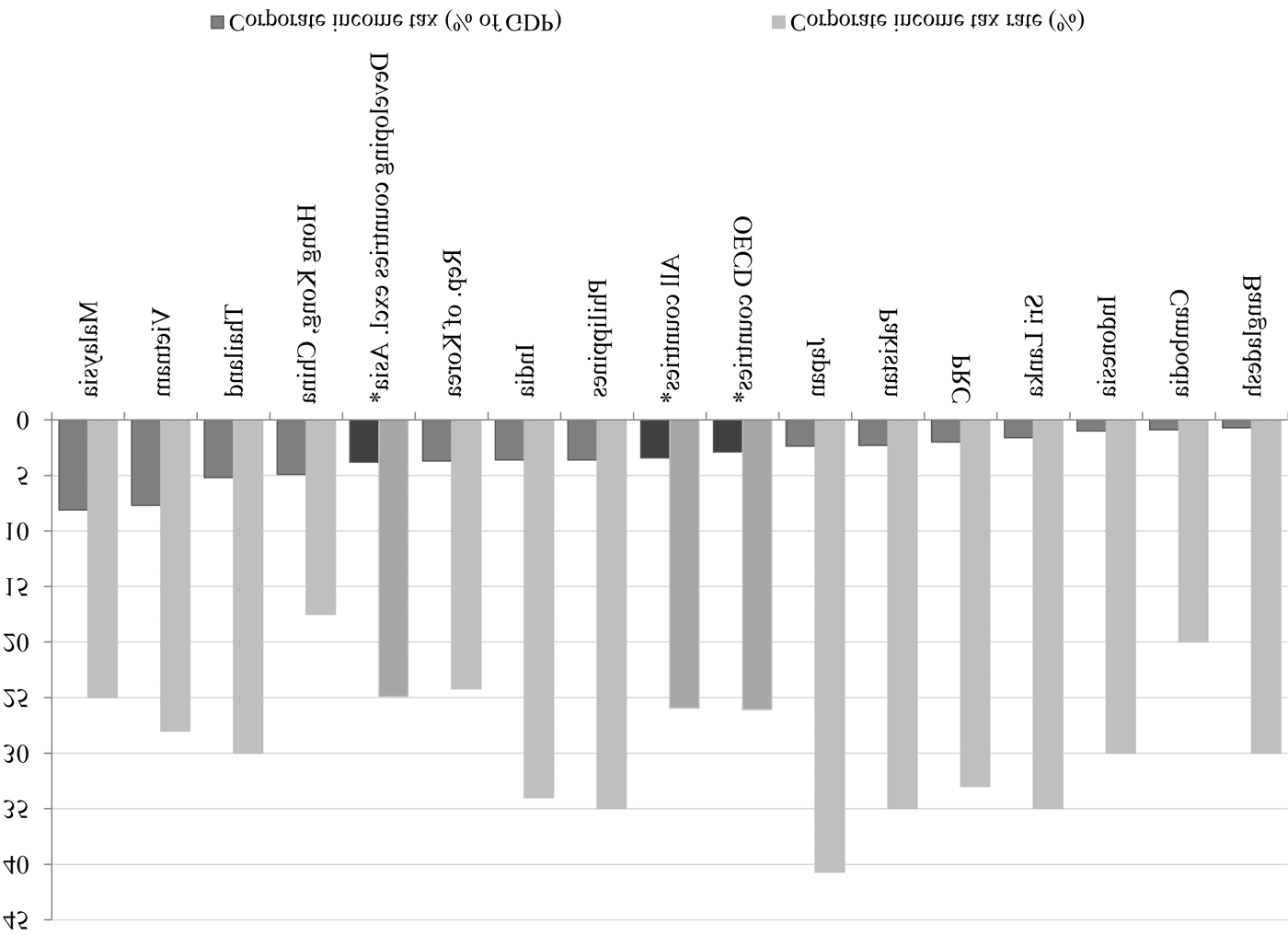

Coping with Rising Inequality in Asia

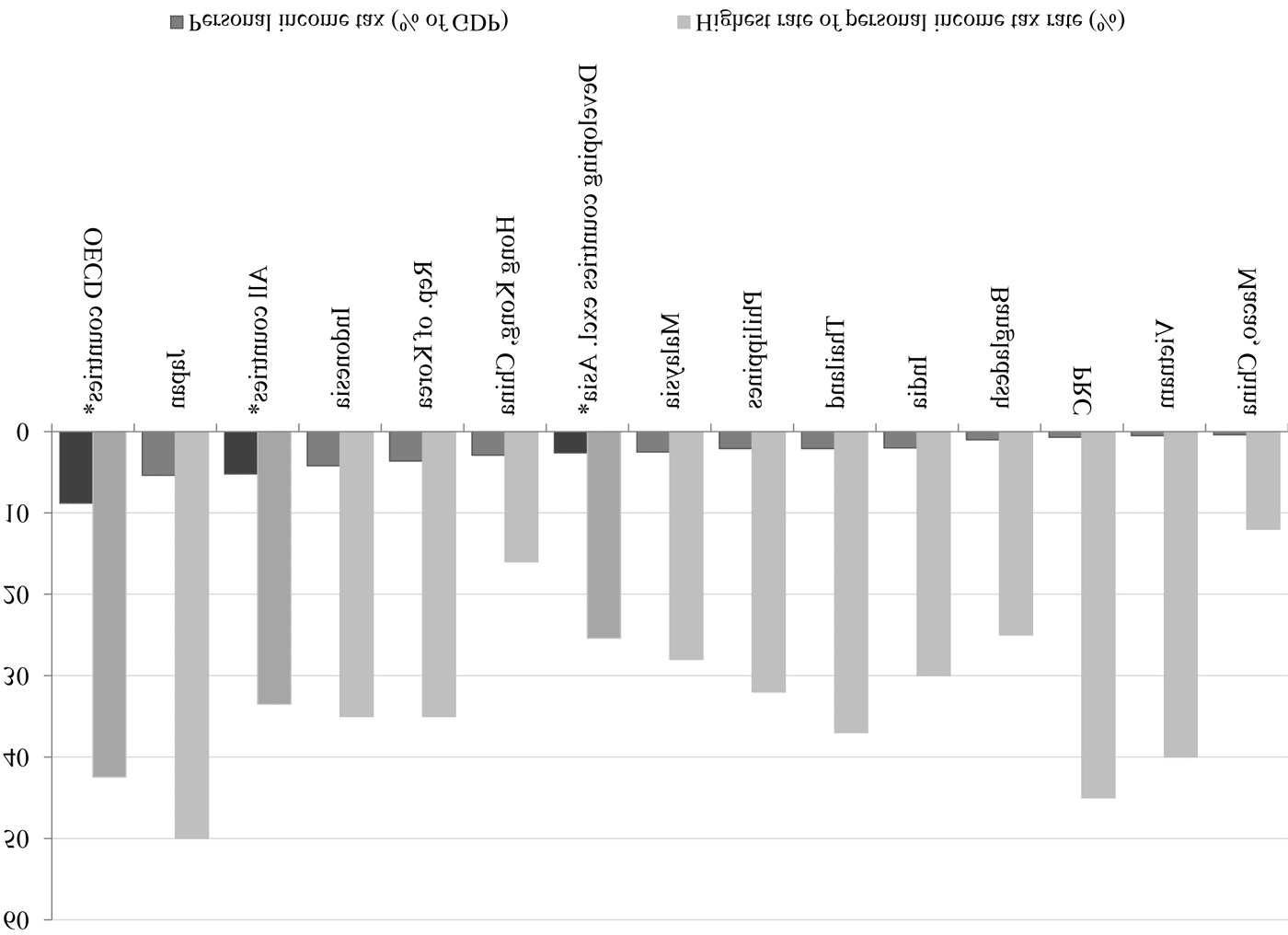

Iris Claus

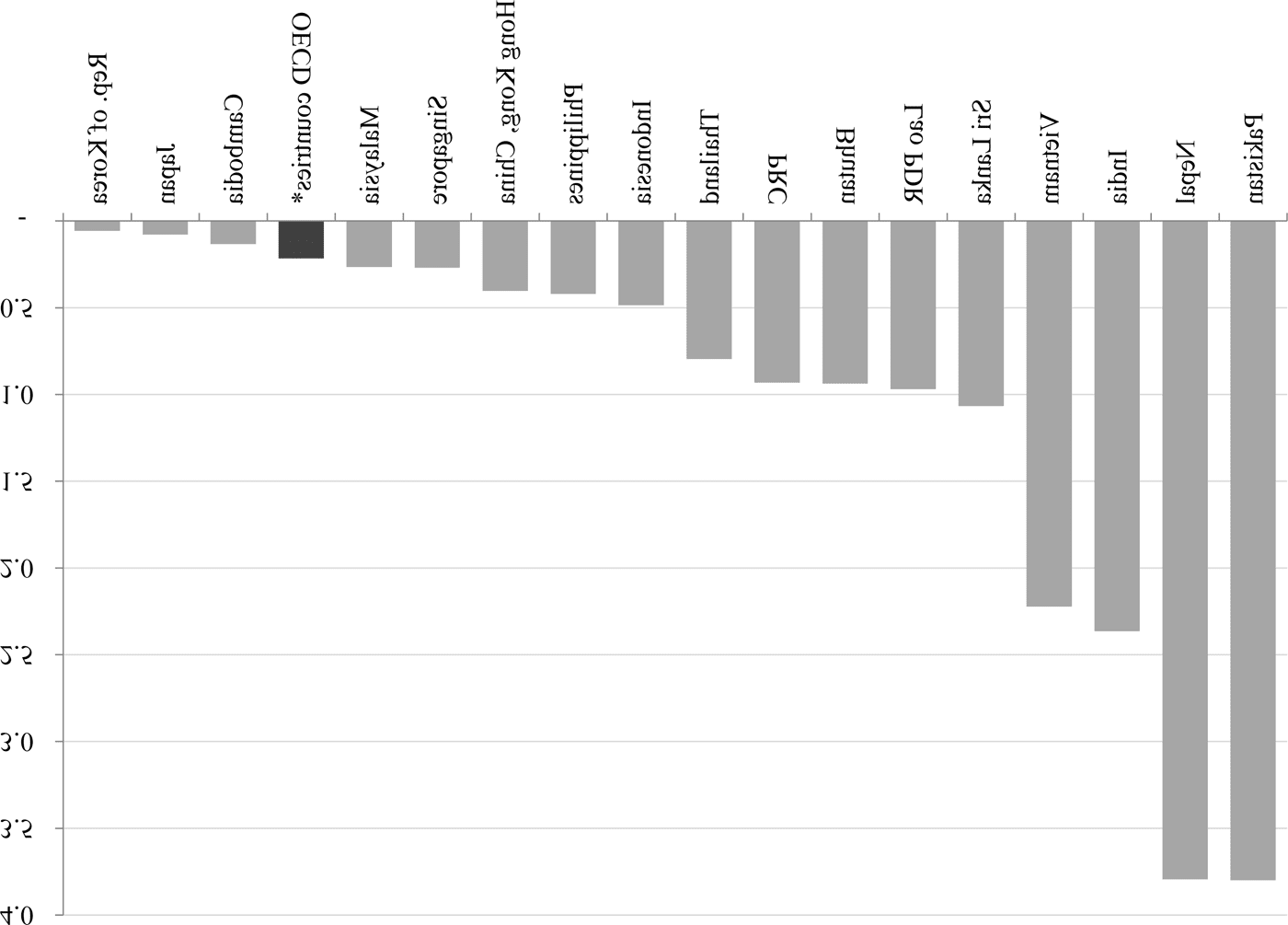

Economics and Research

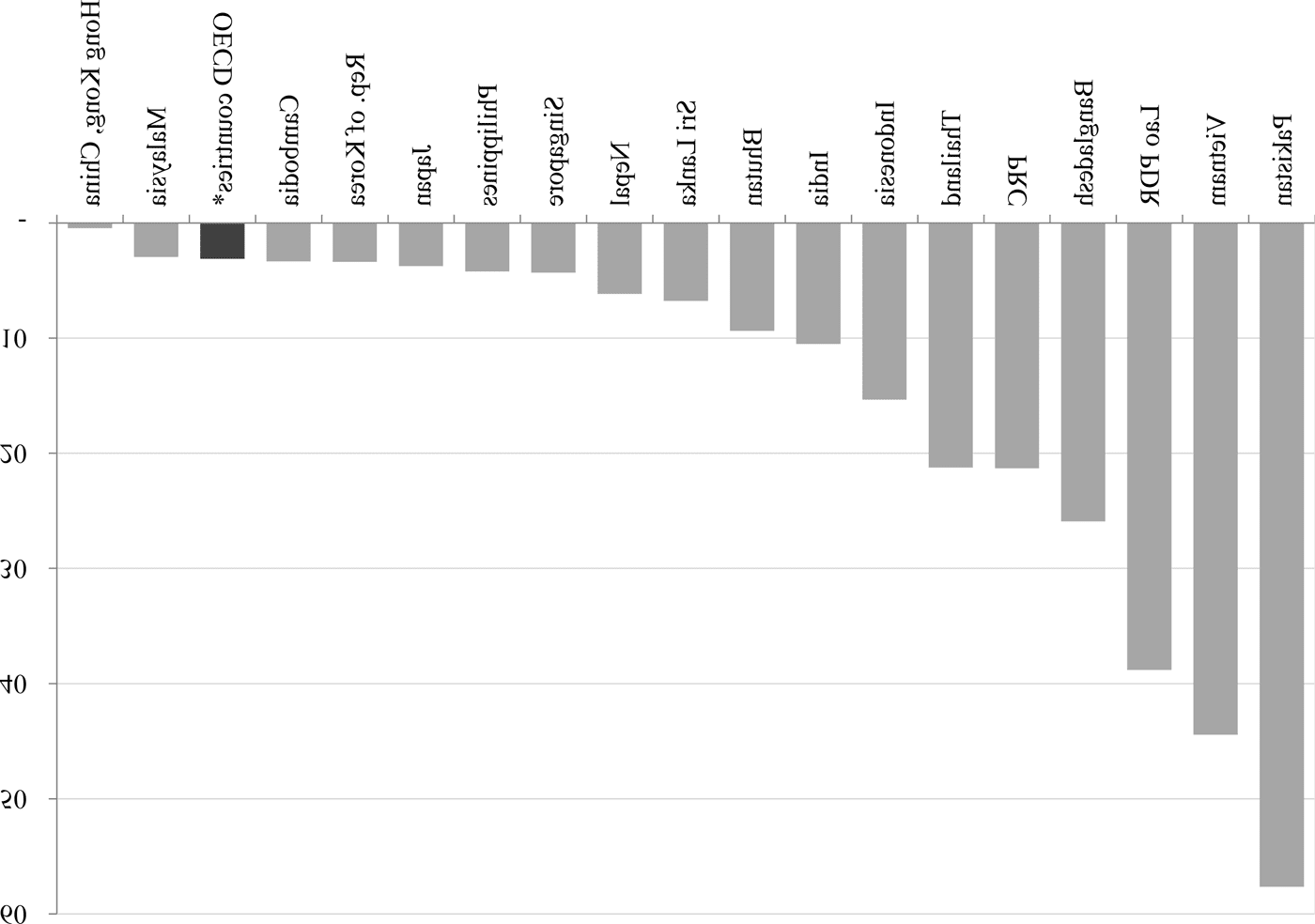

Department

Asian Development Bank

6 ADB Avenue

Manila, Philippines

iclaus@adb.org

Jorge Martinez-Vazquez

International Center for

Public Policy

Andrew Young School of

Policy Studies

Georgia State University

Atlanta, Georgia USA

jorgemartinez@gsu.edu

Violeta Vulovic

The World Bank

Bank Dunia

Gedung Bursa Efek Indonesia

Menara 2, Lantai 12

Jl. Jenderal Sudirman Kav. 53-53

Jakarta 12190, Indonesia

vvulovic@worldbank.org

Coping with Rising Inequality in Asia:

How Effective Are Fiscal Policies?*

Abstract

This paper discusses the role and effectiveness of redistributive

fiscal policies and provides estimates of the effects of taxation and

government expenditure on income inequality in Asia. Tax sys-

tems around the world tend to be progressive, but government

expenditure is generally found to be a more effective tool for re-

distributing income. In Asia, government spending on social pro-

tection has a distinctive differential distributive impact. Social

protection spending appears to increase income inequality in Asia,

whereas it reduces it in the rest of the world. Government ex-

penditure on housing is also adversely affecting the distribution of

income in Asia. Policy options for improving the redistributional

effectiveness of fiscal policies in Asia are discussed.

1. Introduction

Over the past two decades many countries in Asia have

experienced rapid economic growth, which has resulted in

a substantial reduction in poverty and a dramatic im-

provement in welfare and the standard of living for a large

proportion of the population. From 1990 to 2010 the re-

gion’s average per capita GDP in 2005 PPP terms rose

from US$ 1,633 to US$ 5,133, while the proportion of peo-

ple living on less than US$ 1.25 a day fell from around 54 percent to below 22 percent, lifting more than 715 mil- lion people out of poverty (ADB 2012). But widening income inequality is emerging as a concern as the * We would like to thank Suresh Narayanan, Shigeyuki Abe, and participants at the 2012 Asian Economic Panel meeting at Keio University for valuable comments and suggestions. The views expressed in this paper are our own and do not necessarily reºect the views or policies of the Asian Development Bank or the World Bank or their Board of Governors or the govern- ments they represent. Asian Economic Papers 12:3 © 2013 The Earth Institute at Columbia University and the Massachusetts Institute of Technology doi:10.1162/ASEP_a_00232 l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia performance in economic growth and reduction in poverty have been accompanied with rising income disparity in several developing Asian countries. At the same time, unequal access to basic social services, such as education and health, is seen as a signiªcant problem that may be exacerbating growing income inequality. The main purpose of this paper is to investigate the impact of redistributive ªscal policies in Asia, and compare that impact to what is observed in a broad set of other countries outside the continent. More speciªcally, the paper analyzes the effective- ness of taxation and selected government expenditure in reducing income inequal- ity in Asia and in the rest of the world, and the ªscal policies that might be adopted in Asian countries to help reduce income disparity. The rest of the paper proceeds as follows. Section 2 summarizes the literature on the role and effectiveness of redistributive ªscal policies. Section 3 discusses empirical estimates of the impact of taxation and government spending on income inequality in Asia. Section 4 reviews how the effectiveness of ªscal policies in Asia may be im- proved. The last section concludes with some policy lessons. 2. Review of the literature on the role and effectiveness of redistributive ªscal policies A great deal of research has gone into conceptualizing and measuring how the reve- nue and expenditure sides of government budgets affect the distribution of income among households and individuals and how effective they are in helping the poor. Formally, the study of these effects is known as tax and expenditure incidence. This section reviews the different approaches that have been used in the literature and summarizes the main empirical ªndings.1 2.1 Tax incidence analysis Tax incidence analysis investigates who ultimately bears the burden of government taxes in an economy. There are several key concepts. First is the distinction between “statutory” (or legal) incidence and “economic” incidence, or those taxpayers who are by law required to pay the tax versus those taxpayers who ultimately bear the tax burden. The latter is, of course, what really counts. The “shifting” of taxes hap- pens because the agents statutorily responsible to pay the taxes can alter their eco- nomic behavior and transfer or shift the burden of taxes to other agents via changes in prices charged to consumers, wages paid to workers, or the return paid on invest- 1 Some parts of this section draw on Martinez-Vazquez (2008) and Cuesta and Martinez- Vazquez (2011). 2 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia ments. The degree of shifting depends on the elasticities of demand, supply, and substitution in the use of inputs of production among the economic agents interact- ing in the activity or market being taxed. Economic agents with lower elasticities— that is, lower ability (or willingness) to react—are more likely to ultimately bear the burden of taxes. Because adapting or reacting to taxes takes time, the economic inci- dence of taxes tends to be different in the short and long run. For example, capital owners may bear the burden of increased proªt taxes in the short run, but this bur- den can be shifted to workers in the longer run as decreased investment leads to lower productivity and wages, and higher unemployment. Second, taxes impose total burdens that go beyond the amounts actually collected by governments. This difference receives the name “excess burdens” of taxes or “deadweight losses.” The excess burdens arise because taxes lead to less efªcient uses of economic resources and lower output and income in the economy as taxes distort the choices of economic agents. For example, income taxes affect labor– leisure choices and saving and investment decisions. Third, a signiªcant difªculty in measuring the impact of taxes is to ªgure out the appropriate “counterfactual” (i.e., the situation before the taxes were implemented that should be used as the benchmark in the measurement of the impact) and to ap- proximate the distribution of income that would have taken place in that counter- factual setting. Fourth, to have a complete view of tax incidence we need to take into account the impact of tax expenditures, negative income taxes, and in-kind transfers. Tax expen- ditures, which take the form of exemptions, rebates, special deductions, tax credits, and special lower tax rates, can make a tax system more progressive (i.e., increase income equality) or more regressive (i.e., reduce income equality), depending on a variety of public choice issues such as lobbying power. Moreover, an important con- sideration is that tax expenditures cannot help the poor unless they pay taxes. And many of the poor do not pay taxes. This point highlights some of the limitations of redistributional policies from the tax side of the budget. An important amount of redistribution can be implemented via negative taxes. These cash transfers are targeted to the poor and are by nature highly progressive. There are some caveats in their application, however. To minimize fraud, a sophisti- cated tax administration is required. In addition, stigma among the recipients can lead to low and uneven take-up of beneªts, which may affect the progressivity of this type of transfer. 3 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia For in-kind transfers, their incidence typically depends on the degree of participa- tion by income groups. In-kind transfer programs such as food stamps tend to be quite progressive. But not all in-kind transfer programs are progressive. For exam- ple, voucher programs for higher education tend to beneªt higher income groups more than lower income groups because their uptake of higher education typically is proportionally higher, and so in general voucher programs are regressive. 2.2 Three general methodologies for determining the impact of taxes on income distribution Three approaches have been used to estimate the distributional impact of taxes. The ªrst, and most widely used, is microsimulation analysis, which utilizes consumer or household data and conventional assumptions of tax incidence. The second is based on computable general equilibrium models for the entire economy and just a few representative individuals, and the third is based on econometric estimation models with more aggregate data. l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Microsimulation models of tax incidence These models allocate tax burdens to different income groups, ordered from rich to poor by deciles or quintiles of the population, on the basis of a series of assumptions about who bears the ªnal burden of taxes. For each tax, a portion of the revenues collected is imputed as tax burden to each income group in a way that exhausts the total revenues collected. For example, the revenues from excise taxes on tobacco products are allocated to different income groups in proportion to their relative share in the consumption of tobacco products. To arrive at an estimate of the incidence for the entire tax system, the incidence for each tax is calculated separately for each income group. These results are added up across all taxes for each income group to arrive at the total burden for each income group. Typically, the total burden is expressed as an average total tax rate—that is, the proportion of income paid in taxes by each income group. The information on total income, sources of income, and expenditure patterns are generally obtained from data in household or consumer income and expenditure surveys. Taxes col- lected are obtained from the tax administration authorities. The microsimulation approach to tax incidence presents advantages and disadvan- tages. On the plus side, the methodology is relatively simple and easy to implement, the underlying assumptions are transparent, and the implications of alternative as- sumptions can be easily compared. The analysis can also include large samples of taxpayers. On the minus side, good information on income distribution is not al- ways available, and general equilibrium second-round feedback effects are typically ignored. More importantly, the assumptions about who bears the ªnal burden of 4 Asian Economic Papers Coping with Rising Inequality in Asia taxes that play a critical role in the results have been criticized for “stipulating” the incidence of various taxes (Devarajan, Fullerton, and Musgrave 1980). General equilibrium models of tax incidence This approach to tax incidence was pioneered by Harberger (1962). It analyzes the incidence of taxes within the context of a general equilibrium model of the economy, without making explicit assump- tions about who bears the ªnal burden of taxes. Instead, tax incidence is determined by the initial structure of the economy with the ªnal outcome measured by observ- ing the differences in the vector of equilibrium prices before and after a tax change. Harberger’s model was operationalized by the development of computable general equilibrium models. They are numerically solved general equilibrium models using data from the national income accounts, household expenditure surveys and tax- payer ªlings (e.g., Fullerton et al. 1979; Ballard et al. 1985). General equilibrium models capture all the parameters that should play a role in ªnal tax incidence among different income groups: different demand patterns, different endowments in resources, and variations in capital–labor ratios in different economic sectors. The general equilibrium approach also has its advantages and disadvantages. On the positive side, it uses an explicit structural model of the economy with utility/ demand functions and production/supply functions. It offers transparency in how incidence results are linked to assumptions on fundamental parameters, such as the elasticity of substitution in production and the incidence results include measures of excess burdens. Moreover, general equilibrium models take into account indirect or second-round feedback effects of taxation or government expenditure changes. On the minus side, general equilibrium models are operationally intensive and the number of taxpayers represented needs to be small. And even though the approach does not stipulate incidence results it does stipulate a long list of critical parameters, including elasticities of substitution in production and demand and supply (Fullerton and Rogers 1991). Regression-based estimates of the impact of taxes on income distribution A limited number of recent studies have used multivariate econometric analysis to investigate the impact of the tax structure on the distribution of income across coun- tries, typically measured via Gini coefªcients. For example, Weller (2007) uses cross- country data from 1981 to 2002 and ªnds positive effects of progressive taxation on income distribution. Gwartney and Lawson (2006) use panel data on changes in marginal tax rates from 1980 to 2002 to examine their impact on the distribution of income and ªnd that countries with the most signiªcantly high tax brackets rate reductions have experienced the largest increases in inequality over the sample 5 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia period. Duncan and Sabirianova Peter (2008) derive a measure of income tax progressivity and ªnd that inequality in the distribution of income is signiªcantly affected by their measure of progressivity. Similarly, Martinez-Vazquez, Vulovic, and Liu (2011) ªnd that higher reliance on direct over indirect taxes improves the income distribution over time for a large number of countries. On the plus side, the econometric approach allows analyzing the impact of large variations in the level and structure of taxes across countries, variations that are un- likely observed within a single economy. Moreover, it has fewer data requirements than the microsimulation and general equilibrium approaches and uses information typically available for most countries including developing economies. A disadvan- tage of the approach, however, is that the impact of the different elements of the structure of taxes on income distribution cannot be examined in any detail, at least not to the extent allowed by the general equilibrium approach and especially micro- simulation models. In all, the econometric approach should therefore be considered a complement rather than a substitute for the other two approaches. 2.3 Expenditure incidence analysis From the perspective of redistributional policies, it is important to understand the incidence of public spending programs. The key difªculty in measuring the impact of public expenditure on individuals and households, however, is that with some rare exceptions, we are not able to measure output from government expenditures. How public expenditures impact different groups depends, among other things, on the composition of public expenditures, what programs are being implemented, and how much funding is going to each, such as basic education versus university-level education, or primary health care versus tertiary hospitals. The impact of public ex- penditure on the distribution of income depends also on the efªciency of govern- ment spending, the cost effectiveness of funds in delivering services, and the match- ing of real needs. The basic problem in expenditure incidence is how to measure the beneªts accruing to individuals from public goods and services. In the case of private goods and ser- vices, even though marginal private beneªts are not directly observable we can infer them from market prices. In the case of public goods and services, many are pro- vided without direct charges, and even when there is a fee or service charge, this price cannot be interpreted in general as the marginal beneªt for individuals, be- cause the supply of most public goods and services is subsidized or rationed, and it does not respond directly to demand. 6 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia 2.4 Three general methodologies for determining the impact of government expenditures on income distribution Three general approaches have been used in the estimation of expenditure inci- dence. The ªrst is the beneªt incidence approach, which measures how much the in- come of households or individuals would have to be raised if they had to pay for subsidized public goods and services at full cost. The second is the behavioral ap- proach, which derives estimates of households’ and individuals’ willingness to pay for those goods and services. The third approach uses econometric techniques with aggregate data to analyze their differential impact on income distribution. The beneªt incidence approach This approach, which is also known as the clas- sic or the nonbehavioral approach, was pioneered by twin World Bank studies by Selowsky (1979) for Colombia and Meerman (1979) for Malaysia. The essence of the approach is to use information on the cost of publicly provided goods and services together with information on their uses by different income groups to arrive at esti- mates of the distribution of beneªts. Individual beneªciaries are typically grouped by income level, but they can also be grouped by geographical area, ethnic group, urban and rural location, gender, and so on. Information on individual or household use of the public goods and services is typically obtained from surveys, and it is fundamental to know how effectively public expenditure programs target the poor. Because of the required information on unit costs in the provision of public goods and services and the rate of use of those services by different individuals, in prac- tice, beneªt incidence has been estimated for three main categories of public goods and services: education, health, and some types of infrastructure. The beneªt incidence approach has several strengths but it also has weaknesses. On the positive side, it provides simplicity and transparency of estimation procedures and allows study of which public expenditure programs are most effective in reach- ing and improving the status of the poor. On the negative side, the cost measures may not be a good enough approximation of true beneªts or marginal valuations of the public good or service provided, and it cannot incorporate changes in the behav- ior of individuals in response to changes in public expenditure. For example, we may ªnd that poor households do not send their children to school, but beneªt inci- dence cannot explain why that may be the case, nor does it provide a course of pol- icy action. Moreover, the scope is limited to public expenditure programs for which private beneªciaries can be identiªed. The approach can also ignore important inter- action effects with the private sector. For example, if the private education sector is able to attract a higher number of wealthier students, the beneªt incidence of public education becomes more progressive. On the other hand, if the quality of education depends, among other things, on peer effects, the lower number of children of better 7 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia educated and wealthier families in public schools may reduce the quality of public education for the poor. The behavioral approach: Marginal willingness to pay In essence, this approach uses individual preferences to derive marginal willingness to pay as the measure of individual beneªts from public expenditures. This approach was ªrst used in the es- timation of net ªscal incidence of taxes and expenditures at the local level by Aaron and McGuire (1970) and Martinez-Vazquez (1982) and more recently in expenditure incidence studies pioneered by Gertler and van der Gaag (1990), Gertler and Glewwe (1990), and Younger (1999). Econometric methods are used to exploit varia- tion in behaviors in the use of public goods and services, prices, incomes, and other household characteristics across individuals, and time to estimate demand functions for public goods and services. These demand functions generate price elasticities and willingness to pay, generally varying by income group. With that information, one can estimate the incidence of public spending programs, in particular whether they have a pro-poor incidence and whether the poor may have a more elastic re- sponse to any changes in costs associated with the use of the public good or service. The behavioral approach also has several strengths and weaknesses. On the positive side, it is more theoretically sound with clear foundations in microeconomics, and allows the estimation of incidence for public expenditures for which speciªc users cannot be identiªed. Furthermore, it incorporates individual behavioral responses and therefore can provide concrete guidance for policy reform to better target ex- penditures to the poor. On the negative side, this approach is more data-intensive and methodologically more complex. Regression-based estimates of the impact of government expenditures on in- come distribution Using cross-country or panel data, this approach investigates the impact of government expenditures on the distribution of income, typically measured via Gini coefªcients. Regression-based estimates, going as far back as Tanzi (1974), have shown that what in many instances would seemingly be per- ceived as redistributive government spending may do nothing to improve income inequality and may actually worsen it. For example, de Mello and Tiongson (2006) in a cross-country analysis (the sample running from 27 to 56 countries depending on availability of data) of the impact of government spending on income distribu- tion ªnd the overall effects of expenditures to be unequalizing. In fact, those countries where redistribution is most needed due to high inequality are also less likely to have effective redistributive policies in place. In a country case study for Brazil, Clements (1997) similarly ªnds that government social expenditures have in fact exacerbated income inequality. On the other hand, Jao (2000) ªnds that in the 8 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia case of Taipai, China, public expenditures on social assistance and social insurance contributed positively to reducing income inequality. Using panel data for a large number of countries, Martinez-Vazquez, Moreno-Dodson, and Vulovic (2012) ªnd that aggregate public expenditures on social welfare, education, health, and housing have a signiªcant effect on reducing income inequality.2 The multivariate regression approach to the analysis of public expenditure inci- dence also has some clear advantages and disadvantages, and therefore should be considered a complement rather than a substitute for the beneªt incidence and be- havioral approaches. It can analyze the impact on income distribution of large varia- tions in levels of expenditures and their composition across countries, variations that are often not observed within the context of country case studies. Multivariate analysis also allows examining the evolution over time of the impact of different government expenditures on income distribution within countries, and is less data- intensive. On the other hand, the analysis of income distribution at the aggregate country level does not allow the introduction in the analysis of speciªc details of policies and institutions that can make a signiªcant difference on the effectiveness and overall impact of public expenditure policies. For example, two countries can have similar expenditures on primary education and health, but one of these coun- tries may put greater effort into targeting the access to these services by poor rural or urban families. This type of information is typically not available for a large num- ber of countries and therefore is likely to be ignored in multivariate regression stud- ies. If the information is available, there may be the possibility of using dummy variables to account for those effects. Also, to the extent that institutions and policy approaches do not change over time, their impact can be controlled for by using ªxed-effect panel estimation. 2.5 Summary of ªndings of incidence analysis Although different tools and data have been used in the incidence literature, some general results and ªndings about the effectiveness of redistributive ªscal policies seem to hold across the different methodological approaches. Most tax systems tend to show a mildly progressive incidence impact. Around the world, however, taxes have not been an effective means of redistributing income. This is partly because of the potentially large excess burdens or economic losses as- sociated with highly progressive taxation. The international experience shows that 2 The data set covers a slightly shorter period, 1970–2006, than the one used in this study for which the results are reported in the next section. The estimation also does not differentiate Asian economies. 9 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia the expenditure side of the budget (including transfers) can have a more signiªcant impact on income distribution. Direct cash transfers and in-kind transfers can be quite progressive, unless there are serious targeting problems. Moreover, expendi- ture programs in the social sectors (education and health) are more progressive the more is spent in relative and absolute terms on those goods and services more frequently used by the poor (basic education and primary health care). The effec- tive targeting to lower income groups in expenditure programs is hard to design and to implement, however. Whether these general ªndings and conclusions about the effectiveness of redistributive ªscal policies also hold for Asian countries is discussed next. 3. Empirical estimates of the impact of ªscal policies on income inequality in Asia This section presents estimates of the impact of ªscal policies on income inequality in Asia. They are derived from multivariate regression analysis and quantify the ef- fects of taxation and selected government expenditures on income distributions. 3.1 Methodology and data Using data from 150 developed, developing, and transition economies between 1970 and 2009, Claus, Martinez-Vazquez, and Vulovic (2012) estimate the impact of ªscal policies on income distributions measured by Gini coefªcients.3 Of the 150 econo- mies, 22 are from Asia.4 To identify Asia-speciªc tax and government expenditure effects, dummy variables are used. Different regressions are estimated to assess the effects of taxes and government expenditures individually and jointly using ªxed-effect panel estimation methodology proposed by Blundell and Bond (1998). All regressions include lagged inequality to capture the persistence of income in- equality over time, various tax and government expenditure variables, and a set of observable control variables that are commonly used in the literature to explain in- come inequality. Based on data availability, the following control variables are included: population growth, youth dependency, old-age dependency, a globaliza- tion index, GDP per capita, long-term unemployment, perception of corruption, 3 Gochoco-Bautista et al. (2013) examine the relationship between income inequality and in- come polarization in Asian countries. 4 Economies in Asia included are Bangladesh; Bhutan; Cambodia; the People’s Republic of China; Hong Kong, China; India; Indonesia; Japan; the Republic of Korea; the Lao People’s Democratic Republic; Macao, China; Malaysia; the Maldives; Mongolia; Myanmar; Nepal; Pakistan; the Philippines; Singapore; Sri Lanka; Thailand; and Vietnam. 10 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia schooling, and size of government. The estimations also include dummy variables to account for differences in the computation of Gini coefªcients across countries.5 The following tax variables are considered: personal income tax, corporate income tax, social security contributions and payroll taxes, general taxes on goods and ser- vices, and excises and customs duties—all measured as a percent of GDP. Personal income taxes are generally thought to reduce income inequality. When evaluating their impact on income disparity, however, it is important to take into ac- count the progressivity of income tax scales (i.e., how fast the average tax rate rises with income). As a result, personal income tax revenue is interacted with a compre- hensive personal income tax progressivity measure (progressivity) constructed by Sabirianova Peter, Buttrick, and Duncan (2010). When assessing the impact of corporate income taxes on inequality, it is important to take into account that the progressivity of corporate income taxes may be affected by countries’ openness. In a closed economy, the owners of capital tend to bear the full burden of corporate income taxes. But in an open economy, where capital can ºow freely across international borders, the burden of corporate income taxes is likely to be shifted to workers. To allow for these effects, the corporate income tax variable is interacted with a globalization index. Social security contributions and payroll taxes are commonly shared between em- ployees and employers. But employers tend to almost entirely shift the burden to employees in the form of lower wages. Social security contributions and payroll taxes are expected to increase income inequality if there is a cap on income for con- tribution. The lower the cap, the more regressive are the taxes. The evidence for the impact of taxes on goods and services, including value-added taxes and excises, on income inequality is mixed. Studies that analyze current in- come generally ªnd that they are regressive, but this regressivity is reduced substan- tially and may even become neutral when analyzed over a longer time frame. The sign on the coefªcient for general taxes on goods and services and excises could therefore be negative or not signiªcantly different from zero. For lack of better infor- mation, customs duties are expected to have the same direction of effect on income inequality as general taxes on goods and services. 5 Gini coefªcients are computed from income/consumption distribution data. They can be based on gross or net income (i.e., income before or after the deduction of taxes and social contributions) or expenditure. 11 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia On the government spending side, four types of expenditure are considered: on so- cial protection, education, health, and housing—all expressed as a percent of GDP. Ideally, subcomponents of these expenditure categories would have been included (e.g., basic education versus university-level education, or primary health care ver- sus tertiary hospitals), as they are likely to affect income groups differently. Interna- tionally comparable disaggregated data on government spending are not available, however. Bearing this in mind, it is possible that higher aggregate government spending may in fact increase income inequality (e.g., in the case where that expen- diture is directed toward higher education), even though the intuitive expectation is that it would reduce it. The empirical analysis consists of three sets of estimation. The ªrst set focuses only on the effects of taxation and personal income tax progressivity on income inequal- ity. Similarly, the second set of estimates investigates only the effects of government spending on income distributions, and the third set includes both taxation and gov- ernment expenditure to evaluate their joint effect on income inequality in Asia and other countries. The results from the ªrst two sets of estimation are replicated in Appendices A and B and discussed next. Those from the joint estimation are not replicated as they conªrm the general ªndings. For a detailed description of the data and methodology and the results from the joint estimation see Claus, Martinez- Vazquez, and Vulovic (2012). 3.2 Taxation and income inequality Table 1 reports the estimated marginal impact of taxation on income inequality from alternative tax instruments. Table 1 shows that personal income taxes (PIT) have the expected negative impact on income inequality and that the effect is signiªcantly higher in Asia than in the rest of the world. A one-percentage-point increase in PIT revenue as a percent of GDP in Asia reduces income inequality by around 0.573 per- centage points compared with 0.041 percentage points in the rest of the world. The ªnding of a greater redistributive effect of personal income taxation may be due to a larger number of people not paying income tax in Asia because their income is below a tax-free threshold. A larger share of informal employment may also be a contributing factor. The overall impact of progressive income tax scales is modest and somewhat smaller in Asia than in the rest of the world. A one-percentage-point increase in PIT interacted with the progressivity measure reduces income inequality by around 0.002 percentage points in Asia compared to 0.005 in the rest of the world. Including corporate income tax (CIT) revenue as a percent of GDP in the estimation suggests that corporate income taxation reduces income disparity in the rest of the 12 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia Table 1. Estimated marginal impact of taxation on income inequality (in percentage points) Personal income tax Personal income tax*progressivity Corporate income tax Corporate income tax*globalization Social security and payroll taxes General taxes on goods and services Excises Customs duties Source: Claus, Martinez-Vazquez, and Vulovic (2012). Asia (cid:3)0.573 (cid:3)0.002 (cid:3)0.598 (cid:3)0.017 (cid:3)1.324 (cid:3)0.666 (cid:3)0.609 (cid:3)0.174 Rest of the world (cid:3)0.041 (cid:3)0.005 (cid:3)0.338 (cid:3)0.005 (cid:3)0.165 (cid:3)0.768 (cid:3)0.059 (cid:3)0.651 world, but that it is regressive in Asia.6 A one-percentage-point increase in CIT raises income inequality by around 0.598 percentage points. This regressivity of CIT in Asia may be due to larger tax concessions and subsidies for ªrms. Interact- ing CIT with globalization, however, reverses the sign. CIT interacted with global- ization lowers inequality, which is the opposite from what is expected and what is observed in the rest of the world. The ªnding may be due to proªt shifting by multi- national corporations to Asian countries. Social security contributions and payroll taxes are typically shifted to employees in the form of lower wages and are expected to result in increased income inequality when capped at higher incomes. The results in Table 1 provide support for this hy- pothesis, especially in Asia where the estimated effect of social security contribu- tions and payroll taxes as a percent of GDP (SSC(cid:2)Payroll) on income inequality is substantially larger than in the rest of the world (1.324 compared with 0.165). The larger coefªcient in Asia is likely due to two effects. First, social security contribu- tions are capped at relatively low incomes. Second, they are deductible for income tax purposes in several Asian countries, which raises the tax burden for low income people with earnings below a tax-free threshold. Empirical evidence regarding the effect of general taxes on goods and services on in- come inequality is mixed. The results for Asia and for the rest of the world support the hypothesis that they are regressive. The results suggest that a one-percentage- point increase in general taxes on goods and services as a percent of GDP (GTGS) in- creases income inequality by around 0.666 percentage points in Asia compared with 0.768 in the rest of the world. Somewhat less regressive GTGS could be due to lower tax compliance in Asia. Moreover, Asia may have a greater number of small busi- nesses not charging value-added taxes (VAT), for example, because their sales are below VAT registration thresholds. 6 The correlation coefªcient between the Gini coefªcient and CIT in Asia is about 0.06. 13 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia Table 2. Estimated marginal impact of government spending on income inequality (in percentage points) Social protection Education Health Housing Source: Claus, Martinez-Vazquez, and Vulovic (2012). Asia (cid:3)0.490 (cid:3)0.486 (cid:3)0.241 (cid:3)2.162 Rest of the world (cid:3)0.276 (cid:3)0.034 (cid:3)0.330 (cid:3)0.614 Excises and customs duties are also found to be regressive in Asia. The results in Table 1 show an estimated effect of 0.609 percentage points for excises and 0.174 per- centage points for customs duties. 3.3 Government spending and income inequality Table 2 reports the estimated marginal impact of the different types of government spending on income inequality. The estimates suggest that a one-percentage-point increase in social protection expenditure raises income inequality in Asia by 0.49 percentage points. In the rest of the world, social protection spending has the expected negative sign (i.e., it reduces income inequality). Social protection expenditures consist of two components: (i) services and transfers provided to individuals and households, and (ii) expenditures on services provided on a collective basis (IMF 2001). Collective social protection services include formu- lation and administration of government policy, formulation and enforcement of legislation and standards for providing social protection, and applied research and experimental development into social protection services. Asian countries provide relatively few services and transfers, and the second component is likely to domi- nate. The unexpected positive effect of social protection on income inequality sug- gests that government policies and legislative enforcement, and so forth—the sec- ond component of social protection expenditure—may beneªt higher-income households and individuals more than those with a lower income.7 Moreover, the unexpected positive effect of social protection may be due to a narrow beneªt cover- age and a lack of targeting to the poor for the few services and transfers that Asian countries provide. For education, the results suggest that government expenditures in Asia have a larger negative effect on income inequality than education spending in other coun- tries. In the case of expenditures on health, this type of expenditure has a somewhat lower negative effect on income inequality in Asia than in the rest of the world. On 7 To test this hypothesis, information on the structure of social protection expenditures would be needed, which, however, is not available. 14 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia the other hand, the estimates suggest that a one-percentage-point increase in hous- ing expenditure raises income inequality in Asia by 2.162 percentage points, com- pared with the rest of the world where housing spending has the expected negative sign (i.e., it tends to reduce income inequality). The adverse effect likely reºects the housing challenges facing governments in developing Asia that are arising from rapid urbanization. So far, large-scale government programs of direct housing pro- vision have only been successful in a few countries (e.g., Hong Kong and Singapore) and nearly a third of households in Asia continue to live in slums and informal set- tlements (UN-HABITAT 2011). 4. Improving the effectiveness of ªscal policies in Asia The review of the literature and the empirical results for Asia and the rest of the world suggest that more effective redistributional policies can be implemented with spending programs on social welfare and the social sectors, such as health and edu- cation policies, than with taxes. Taxation, however, is crucial to raise ªnancing for government expenditure to achieve distributional objectives. This section discusses the effectiveness of tax systems and tax administration in collecting tax revenue in Asia. Our focus is on corporate and personal income taxation and value-added taxes, as payroll and social security taxes are less important in Asian countries and tax revenues from foreign trade taxes, including custom duties, are declining with rising trade liberalization. The section also brieºy discusses government spending policies on education, health, and social protection to throw more light on the em- pirical ªndings presented in the previous section. Housing is excluded from the dis- cussion because of a lack of readily available data and information. 4.1 Tax systems Taxes create economic costs because they distort economic behavior. A theoretically optimal tax that minimizes the behavioral impact of taxation is one that taxes activi- ties according to their varying response elasticities to the tax. In practice, however, such an approach is not feasible because it is constrained by principles of fairness and simplicity, and because of the difªculties to reliably measure the tax sensitivity of particular activities. Practically speaking, an efªcient tax system is one that re- duces the disincentive effects of taxation to work, save, and invest by using broad bases and low, fairly uniform rates. A broad-base, low-rate system also lowers ad- ministration and compliance costs, leaving more resources for productive activities, and is often seen as fairer than a narrow-base system because of horizontal equity considerations (i.e., taxpayers who have the same income should pay the same amount in taxes) and vertical equity (i.e., people with different incomes should pay different amounts of tax). 15 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Coping with Rising Inequality in Asia Figure 1. Corporate income tax and corporate income tax rate (2009 or latest available year) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / Source: International Monetary Fund, KPMG, OECD, United Nations Economic Commission for Latin America and the Caribbean. Note: Sorted from highest to lowest tax revenue as a percent of GDP. *Unweighted average. GDP gross domestic product; OECD Organization for Economic Co-operation and Development; PRC People’s Republic of China. / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . 4.2 Composition of taxes Corporate income taxation is an important part of countries’ tax systems. Figure 1 plots corporate income tax revenue as a percent of GDP and (statutory) corporate in- come tax rates in Asia compared with three country averages: all countries, OECD countries, and developing countries excluding those in Asia. It shows that Malaysia at 8.1 percent and Vietnam at 7.7 percent have the highest level of CIT, and Indone- sia, Cambodia, and Bangladesh have the lowest, at 1.0 percent, 0.9 percent, and 0.7 percent, respectively. Corporate tax collection is low in Indonesia and Bangla- desh despite relatively high tax rates, partly because of various tax incentives and concessions that governments often provide for attracting investment and for activi- ties seen as having social or economic merit. f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Besides reducing tax revenue collections, there are other potential costs to tax incen- tive schemes. Tax incentives often become politicized with resources being captured 16 Asian Economic Papers Coping with Rising Inequality in Asia Figure 2. Personal income tax and top personal marginal income tax rate (2009 or latest available year) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Source: International Monetary Fund, KPMG, OECD, United Nations Economic Commission for Latin America and the Caribbean. Note: Sorted from highest to lowest tax revenue as a percent of GDP. *Unweighted average. GDP gross domestic product; OECD Organization for Economic Co-operation and Development; PRC People’s Republic of China. by interest groups. If lobbying power is concentrated among high-income groups, tax incentives and concessions would be expected to reduce the redistributive im- pact of corporate income taxation. Another difªculty with tax incentives schemes is that they are often poorly targeted and to a large extent just subsidize activities that ªrms would have undertaken regardless of the policies. Personal income taxation is another important part of countries’ tax collection. Figure 2 plots personal income tax revenue as a percent of GDP and the top personal (statutory) marginal income tax rate. It shows that PIT collection is low in Asia com- pared with the rest of the world, OECD countries, and developing economies ex- cluding those in Asia. On average, Asian countries collect about 2.2 percent of per- sonal income taxes as a percent of GDP compared with an all-country average of 17 Asian Economic Papers Coping with Rising Inequality in Asia Figure 3. Ratio of tax free threshold/individual allowance or deduction to gross national income per capita (2012) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l Source: International Bureau of Fiscal Documentation, Asian Development Bank, authors’ calculations. Note: Gross national income per capita for Asian countries is assumed to grow at the 2000–10 rates. *Unweighted average, data are for 2009 or 2008, no data are available for Turkey. Lao PDR Lao People’s Democratic Republic; OECD Organization for Economic Co-operation and Development; PRC People’s Republic of China. f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . 5.2 percent, and 8.8 percent, and 2.7 percent, respectively, in OECD and developing countries excluding those in Asia. Partly contributing to this relatively low tax take are higher tax-free (minimum exempt) thresholds and a higher threshold of income, above which the top marginal personal income tax rate applies. Figure 3 plots the ratio of the tax-free threshold/individual allowance or deduction to gross national income per capita. It shows that Nepal at 3.8 and Pakistan at 3.95 have the highest ratios. Only Cambodia, the Republic of Korea, and Japan have ra- tios below the average of OECD countries. The higher the tax-free threshold, the larger tends to be the number of lower-income people exempt from income taxation and the larger the redistributive impact of personal income taxes, but the higher the statutory tax rates that are needed to ªnance government expenditure. f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 18 Asian Economic Papers Coping with Rising Inequality in Asia Figure 4. Ratio of top personal income tax threshold to gross national income per capita (2012) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / Source: Asian Development Bank, International Bureau of Fiscal Documentation, OECD, authors’ calculations. Note: Gross national income per capita for Asian countries is assumed to grow at 2000–10 rates. *Unweighted average, data are for 2009 or 2008, no data are available for Turkey. Lao PDR Lao People’s Democratic Republic; OECD Organization of Economic Co-operation and Development; PRC People’s Republic of China. / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . Figure 4 plots the ratio of the top personal income tax threshold to per capita gross national income. At 0.45, Hong Kong, China, has the lowest ratio, and the Lao Peo- ple’s Democratic Republic, Vietnam, and Pakistan have the highest thresholds with ratios of 38.8, 44.4, and 56.7, respectively. A higher threshold, all else equal, would be expected to increase the redistributive impact of personal income taxes. Also contributing to the relatively low personal income tax take in some Asian countries are narrow tax bases, which exempt certain types of income or tax them at lower rates. In the People’s Republic of China (PRC), for example, only certain listed types of income (11 categories) are liable to tax. Some of these categories are taxed at progressive rates, whereas others are taxed at a ºat rate. For labor income, wages and salaries are taxed at a progressive rate with a top marginal rate of 45 percent, but the remuneration of personal services is taxed at a ºat rate of 20 percent after a f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 19 Asian Economic Papers Coping with Rising Inequality in Asia Figure 5. General taxes on goods and services and indirect tax rate (2009 or latest available year) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l Source: International Monetary Fund, KPMG, OECD, United Nations Economic Commission for Latin America and the Caribbean. Note: Sorted from highest to lowest tax revenue as a percent of GDP. *Unweighted average. GDP gross domestic product; OECD Organization for Economic Co-operation and Development; PRC People’s Republic of China. f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . deduction of 20 percent of the payment as deemed expense. Interest is also gener- ally taxed at a ºat rate (20 percent), whereas royalties and rental and lease income are taxed at 20 percent and 10 percent, respectively, with a 20 percent deduction be- ing allowed. Moreover, certain types of income (e.g., monetary awards, interest on government bonds and on savings in a deposit account with banks in the PRC) and certain beneªts in-kind (e.g., provision of or reimbursement for reasonable expenses on accommodation, travel expenses, and allowances for children’s education) are exempt from personal income taxation altogether. Tax concessions reduce the redis- tributive impact of personal income taxes if they are mainly captured by higher- income people. f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 A further important contributor to countries’ tax collection is general taxes on goods and services, which include value-added (goods and services) taxes, general sales taxes, and turnover taxes. They are plotted in Figure 5 as a percent of GDP together 20 Asian Economic Papers Coping with Rising Inequality in Asia Figure 6. VAT efªciency ratio (2009 or latest available year, percent) l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 2 3 1 1 6 8 3 3 7 6 a s e p _ a _ 0 0 2 3 2 p d . f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 Source: International Monetary Fund, Organization for Economic Co-operation and Development, KPMG, PricewaterhouseCoopers, Department of Statistics Singapore, authors’ calculations. Note: PRC People’s Republic of China; VAT value-added tax. with countries’ indirect tax rate, which generally coincides with the VAT standard rate. The ªgure shows that revenues from general taxes on goods and services, simi- lar to personal income taxes, are low in Asia, averaging 3.3 percent of GDP com- pared with an all-country average of 6.4 percent, and 6.9 percent and 6.6 percent, respectively, in developing countries excluding those in Asia and the OECD econo- mies. This lower tax take partly results from lower indirect tax rates. Among Asian countries, Japan and Singapore, both at 5 percent, and Thailand, at 7 percent, have some of the lowest indirect tax rates in the world. At 2.2 percent of GDP, the Philippines has the lowest collection of general taxes on goods and services (consisting of VAT) despite its 12 percent indirect tax rate. The low VAT revenues are largely due to a low efªciency of the VAT system. An efªciency ratio, plotted in Figure 6, can be calculated as VAT revenues to GDP di- vided by the standard statutory VAT rate (expressed as a percentage). A low efªciency ratio is taken as evidence of erosion by exemptions, reduced rates within 21 Asian Economic Papers Coping with Rising Inequality in Asia Figure 7. VAT registration threshold (2012, US$)

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

Source: International Bureau of Fiscal Documentation, Asian Development Bank, OECD, authors’ calculations.

Note: Average exchange rates for 2000–10 are used.

*Unweighted average, data are for 2011.

Lao PDR Lao People’s Democratic Republic; OECD Organization of Economic Co-operation for Development; PRC People’s

Republic of China; VAT

value-added tax.

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

the tax law, and/or low taxpayer compliance. Bangladesh has the second least

efªcient VAT system in Asia.

Singapore also has a relatively low efªciency given the breadth of its VAT base, re-

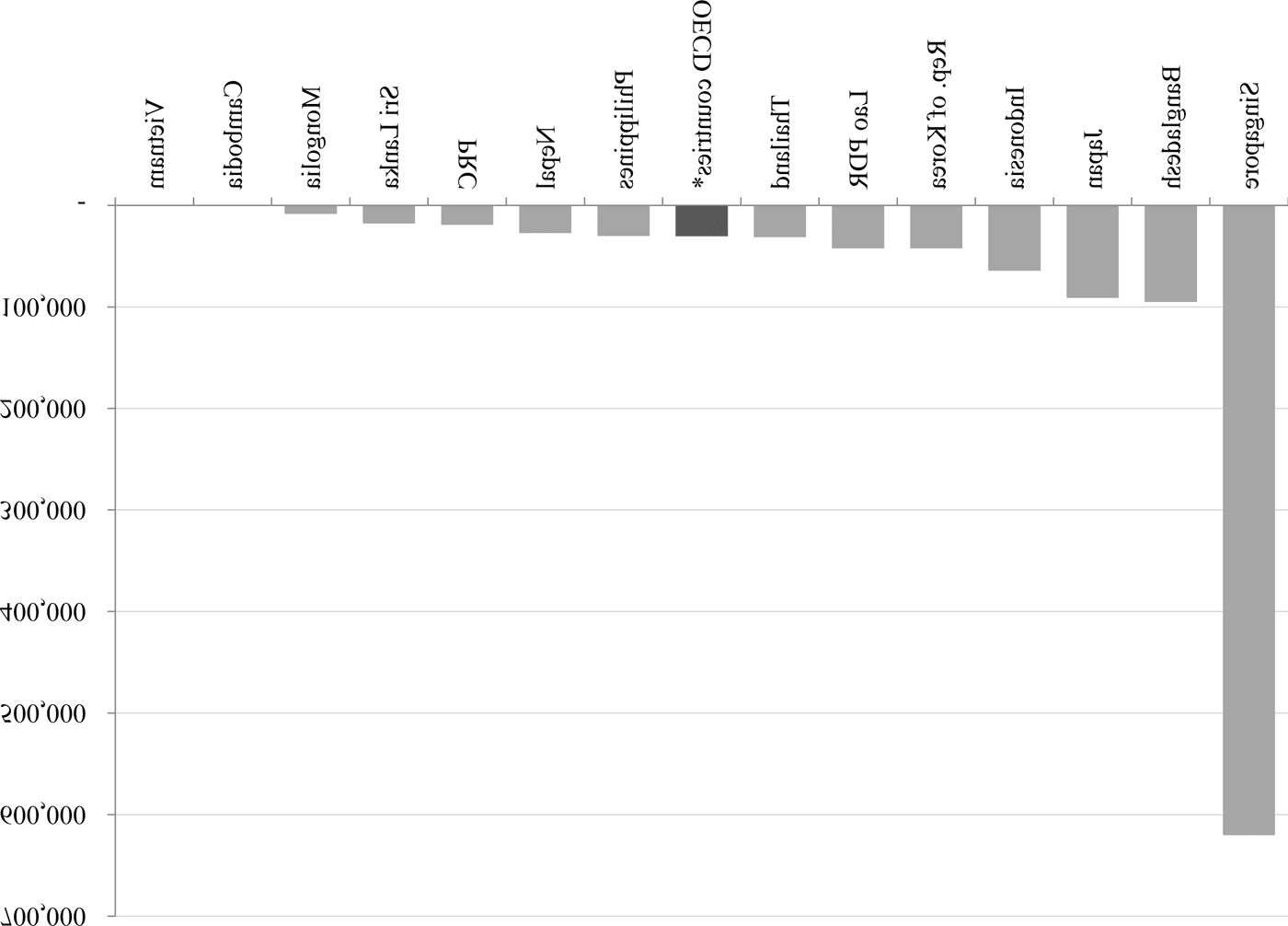

sulting from an extremely high registration threshold of annual taxable turnover

above SG$ 1 million or about US$ 620,000 (Figure 7).

Although the number of countries with a VAT system has been rising rapidly

(Martinez-Vazquez and Bird 2011), several Asian economies have not adopted a

VAT. They include Bhutan; Hong Kong, China; Macao, China; Malaysia; and

Myanmar. India also does not have a VAT in the traditional sense.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Less reliance on value-added taxes in Asian countries is likely to increase the eco-

nomic costs of taxation as value-added taxes are one of the least distortionary taxes.

22

Asian Economic Papers

Coping with Rising Inequality in Asia

Figure 8. Tax administration expenditure (2009, percent of GDP)

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Source: Organization for Economic Co-operation and Development.

Note: GDP

gross domestic product.

*Data are for 2007.

The economic costs of value-added taxes are lower because, typically, VAT is

charged at a uniform, relatively low rate to a (more or less) comprehensive and

broad base. This reduces the economic costs of taxation, which tend to increase with

higher tax rates and narrower tax bases. Moreover, value-added taxes, in theory, do

not distort business or export decisions. This is because the tax paid on production

inputs and exports is deductible. Also, value-added taxes are less distortionary than

other taxes because they do not affect savings and investment decisions—that is,

they do not distort choices between current and future consumption.

4.3 Tax administration and compliance costs

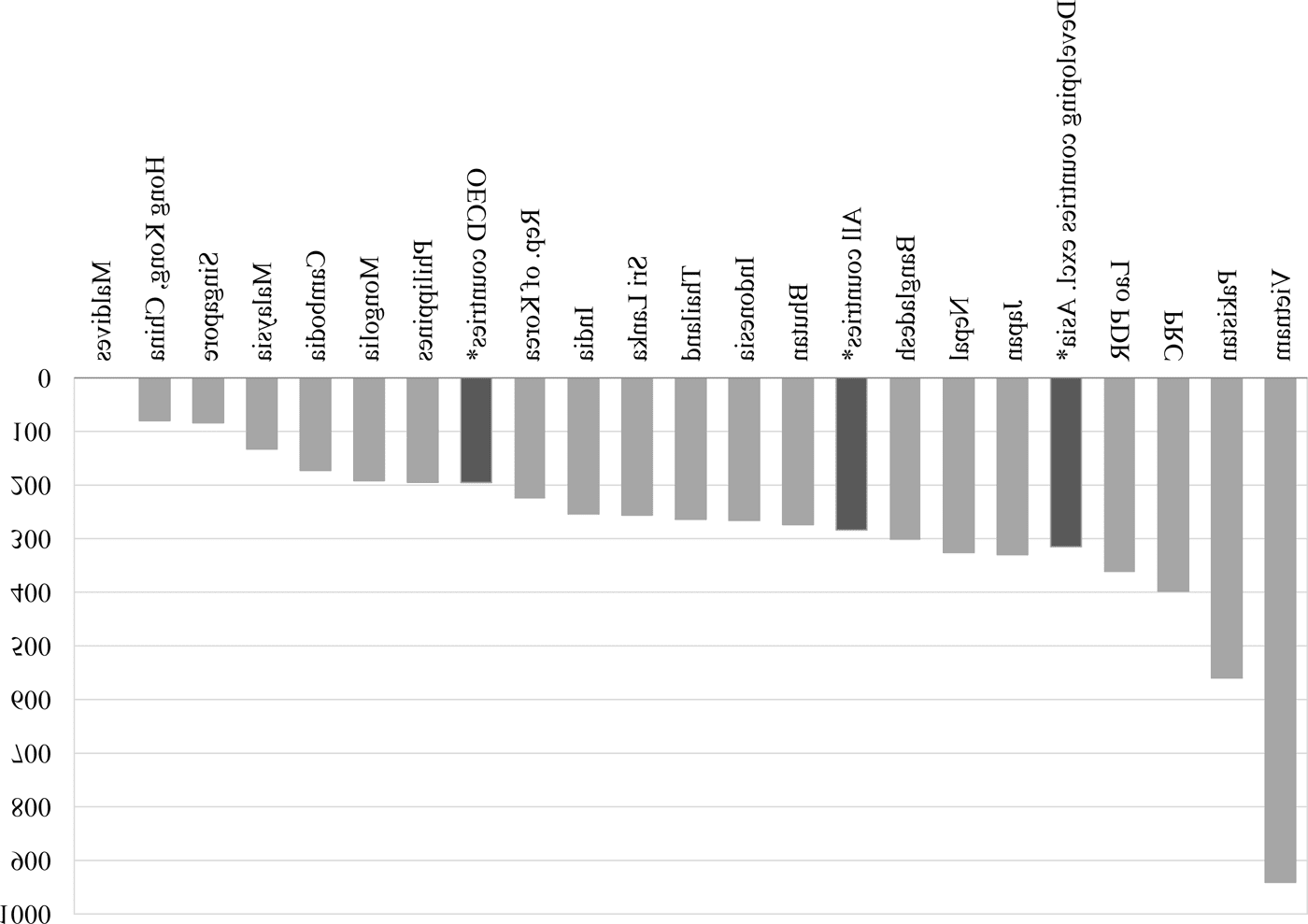

Limited information is available on tax administration costs in Asian countries.

Figure 8 plots tax administration expenditure as a percent of GDP for six Asian

countries (India, Indonesia, Japan, the Republic of Korea, Malaysia, and Singapore)

and the OECD economies. It shows that administration costs in Asia are relatively

low, at least in the countries for which data are available. This is partly because of

less revenue collection. Also contributing to the low tax administration expenditure

23

Asian Economic Papers

Coping with Rising Inequality in Asia

Figure 9. Tax administration costs to net revenue collections (2009, costs per 100 units

of revenue)

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Source: Organization for Economic Co-operation and Development.

Note: *Data are for 2004.

**Data are for 2007.

in Indonesia, India, the Republic of Korea, and Singapore is an efªcient tax adminis-

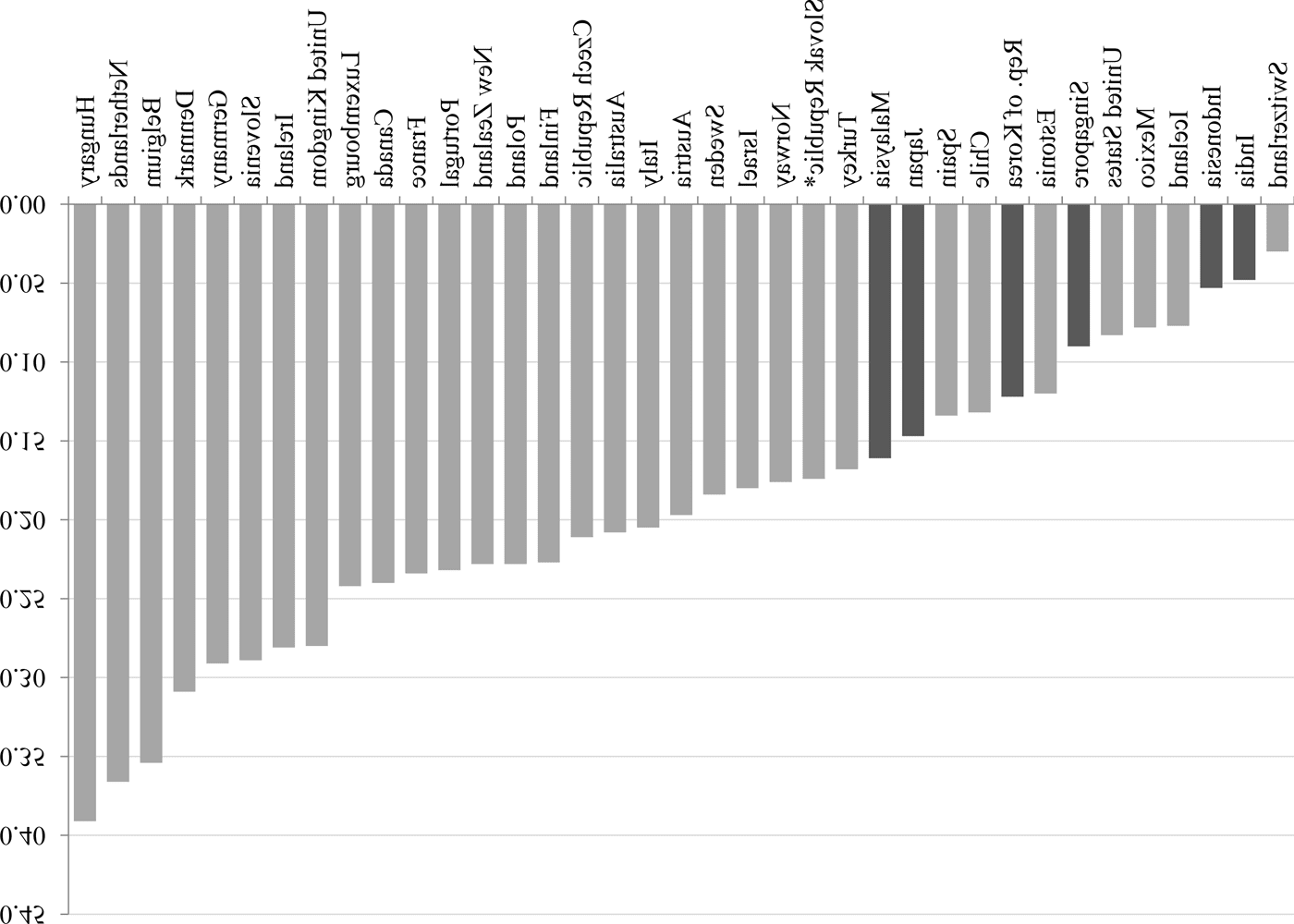

tration. This can be seen in Figure 9, which compares the administrative costs of col-

lecting 100 units of revenue. Indonesia has the 7th lowest costs, India the 10th low-

est, whereas Singapore and the Republic of Korea rank 13th and 14th, respectively.

The ease with which taxpayers are able to comply with the tax system also varies

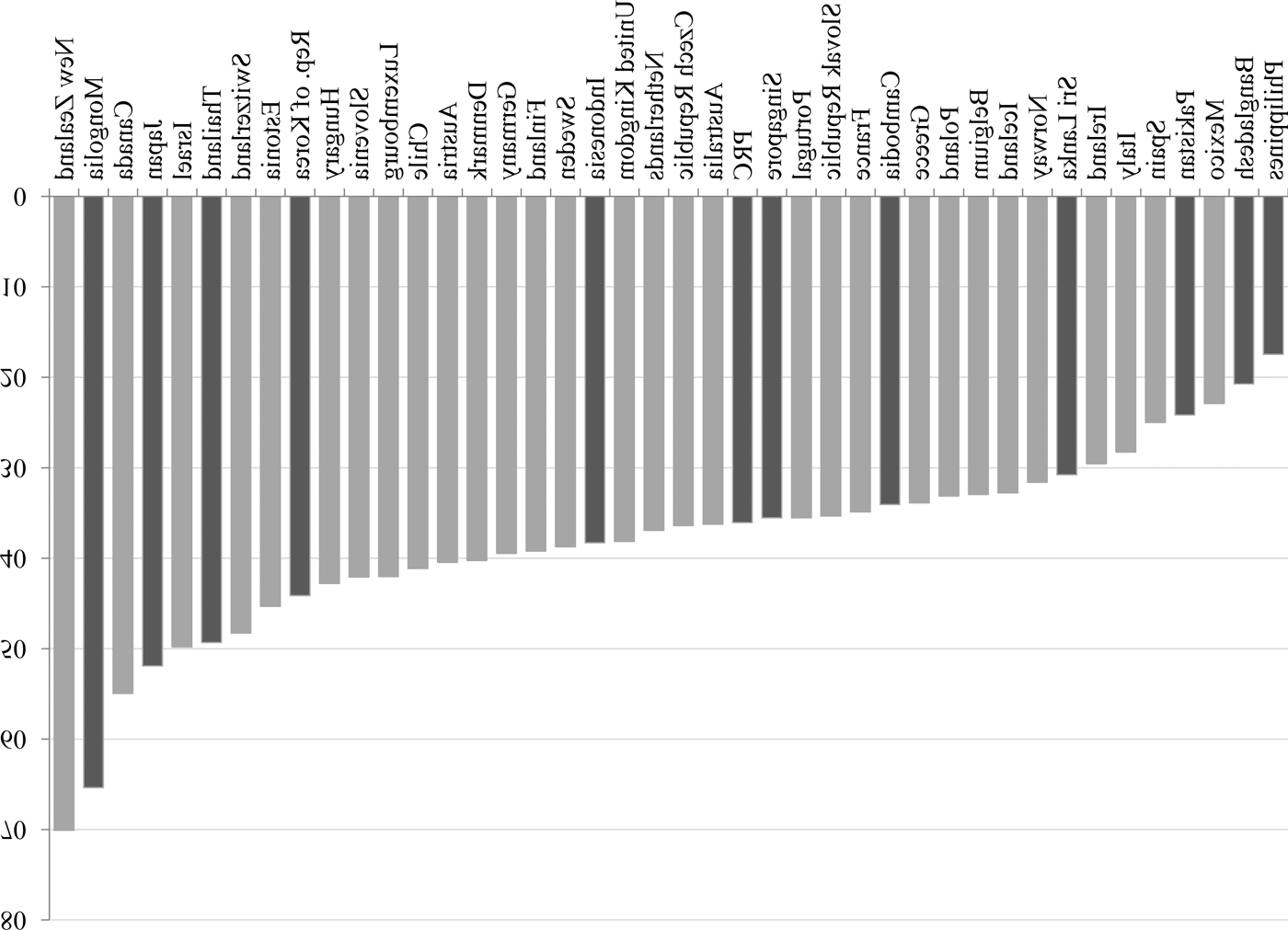

across countries. Figure 10 plots the total time to comply with taxes in hours per

year. Compliance costs in Asia are lowest in the Maldives (largely because in 2009

the Maldives did not levy taxes on goods and services or income taxes other than on

the net proªt of banks based on their annual ªnancial statements); Hong Kong,

China; and Singapore. They are highest in the PRC, Pakistan, and Vietnam, partly

because of complicated tax systems in these countries.

Complicated tax systems increase tax administration and compliance costs as well

as the opportunity for tax planning and tax avoidance. Moreover, narrow-base,

24

Asian Economic Papers

Coping with Rising Inequality in Asia

Figure 10. Total time to comply with taxes (2012, hours per year)

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Source: World Bank

Note: Lao PDR Lao People’s Democratic Republic; OECD Organization for Economic Co-operation and Development;

PRC People’s Republic of China.

*Unweighted average.

high-rate tax systems are often seen as unfair because higher-income taxpayers gen-

erally have greater scope and resources to shift income to avoid higher tax rates. Un-

fair tax systems can reduce individuals’ and businesses’ willingness to pay taxes and

hence the government’s ability to raise ªnancing to fund government expenditure.

4.4 Government expenditure policies

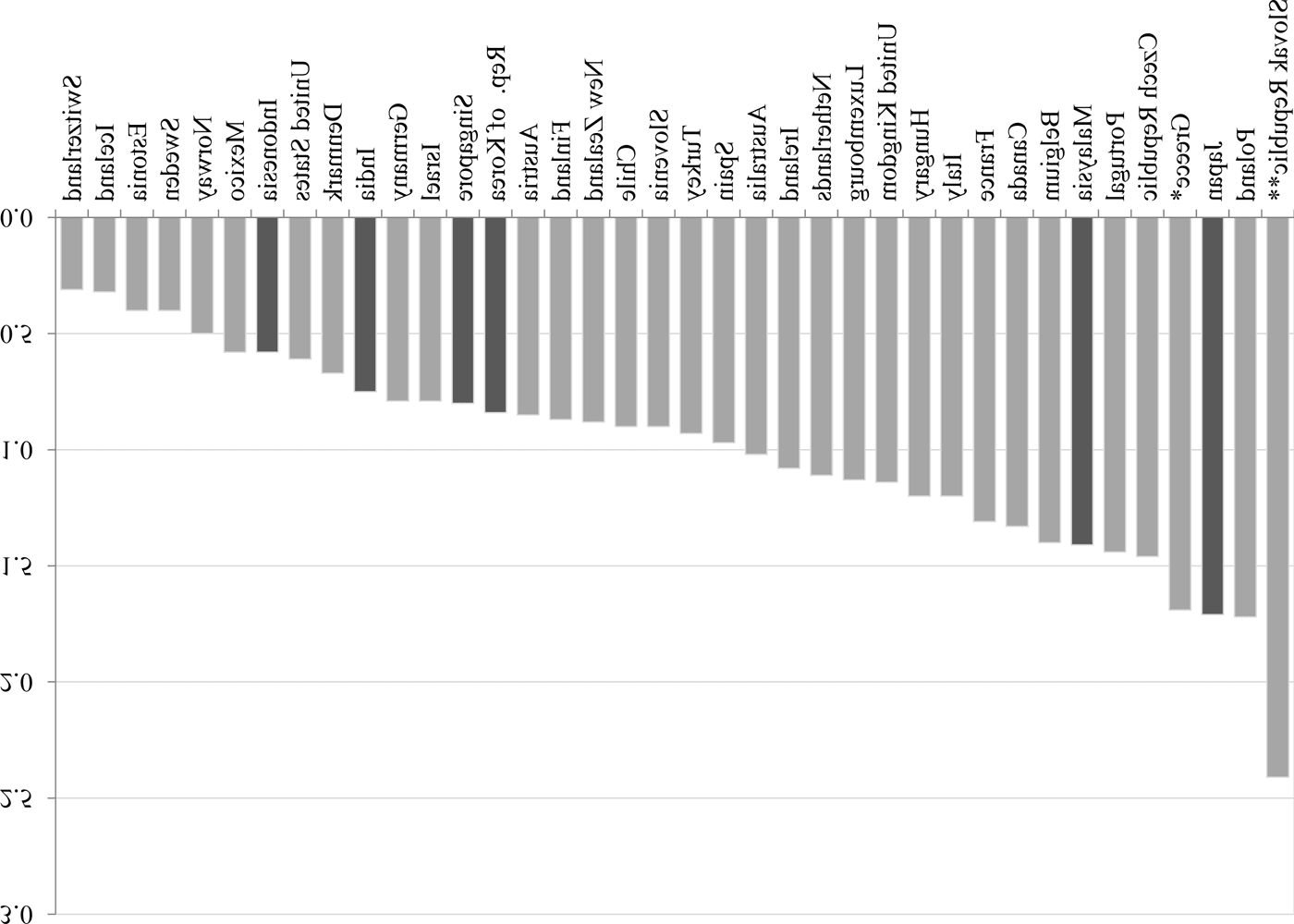

Turning to government expenditures, Asia has made considerable progress in im-

proving education and health outcomes and toward achieving the Millennium De-

velopment Goals (MDGs).8 The second MDG focuses on education (achieving uni-

versal primary education) and goals 4–6 center on health (reducing child mortality;

improving maternal health; and combating HIV/AIDS, malaria, and other diseases).

Progress in Asian countries has been substantial, particularly in education.

8 The MDGs were adopted by world leaders in September 2000 to reduce extreme poverty

with a deadline of achieving a series of targets by 2015.

25

Asian Economic Papers

Coping with Rising Inequality in Asia

Primary school enrollment and the number of students who start ªrst grade and

reach the last grade of primary education have been rising, and several countries

have achieved or are expected to reach the set goals by 2015. Moreover, literacy rates

in Asia are high. Most Asian countries have rates that are above the world average,

and those economies with rates below (Bangladesh, Cambodia, India, the Lao Peo-

ple’s Democratic Republic, Nepal, and Pakistan) have made considerable progress

to raise them. These achievements are likely to be a contributing factor in the ªnd-

ing that education expenditure is reducing income inequality in Asia as government

spending on primary education has been found to be progressive.

Progress has also been made toward improving health conditions. Maternal death

rates have fallen sharply in Asia, with better attendance at birth of trained health

professionals and improved antenatal care. Infant and child mortality rates are also

falling, although only a few countries so far have reached the MDG target. The

progress that has been made is likely to have beneªtted poor families in particular,

as infant and child mortality is closely related to household wealth. Infants in poor

households are often less than half as likely to survive their ªrst year of life as those

in higher-wealth households (ADB 2011). Death and incidence rates of tuberculosis

have also been declining. But HIV/AIDS remains a problem, with the percentage of

the population with comprehensive, correct knowledge about the illness and the

percentage of the population with advanced HIV infection who have access to anti-

retroviral drugs both being relatively low and only rising slowly in some countries

from a low base.

For social protection, overall coverage remains relatively low in Asia and generally

only available to formal sector workers in the civil service or large enterprises.

Moreover, the availability of social protection programs does not necessarily imply

that they are well designed or have wide coverage. Few countries have income sup-

port systems for the unemployed (e.g., the PRC; Hong Kong, China; Japan; the Re-

public of Korea; Mongolia; Thailand; and Vietnam) with coverage rates in terms of

the proportion of unemployed who receive beneªts being less than 10 percent on

average (ILO 2010). Effective coverage of work-related accidents and diseases is also

low with only a proportion of accidents being reported and compensated. In the in-

formal sector, unemployment coverage is virtually nonexistent, working conditions

and safety are typically poor, and work-related diseases are widespread.

With regard to income security in old age, although some Asian countries have

made efforts to extend coverage beyond the formal sector, the proportion of the

working-age population covered by contributory programs remains low at around

20 percent (ILO 2010), and few countries have social pensions to provide safety net

26

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Coping with Rising Inequality in Asia

retirement income for people who were not members of a formal scheme. Moreover,

pension systems in Asian countries, outside the OECD, are often quite generous due

to early retirement ages and relatively high pension levels (OECD 2012). According

to OECD estimates, replacement rates, which measure the value of a person’s pen-

sion as the percentage of their earnings when working, are well above OECD levels

for men in Asia, especially in the PRC, Pakistan, and Vietnam. The high replacement

rates are partly due to nearly all deªned-beneªt schemes being based on ªnal sala-

ries rather than average earnings. Such schemes tend to be particularly regressive

because the higher paid typically have salaries that rise more rapidly with age,

whereas the earnings of lower paid workers generally remain ºat or rise less fast.

Furthermore, the OECD estimates that the expected amount of time that people

spend in retirement, which can be calculated by combining information on national

pension ages and life expectancy, is relatively high in Asia. Pension eligibility ages

are particularly low for both men and women in Malaysia and Sri Lanka and for

women in the PRC and Thailand.

This discussion offers some potential explanation for the ªnding that education and

health expenditures in Asia have reduced income inequality, whereas social security

spending has mainly beneªtted those with a higher income. Basic education and

health services seem to be fairly universally available, whereas social protection

spending has been restricted to those already likely to be better off (i.e., people em-

ployed in the formal sector). This suggests that labor market reform that moves

workers from informal to formal employment may offer the greatest scope for re-

ducing income inequality in Asia. Higher formal employment should also raise per-

sonal income tax collection, which could further assist governments in achieving

redistributive objectives.

5. Conclusions and policy lessons

This paper assessed the impact of government ªscal policies on income inequality in

Asia. It discussed the role and effectiveness of redistributive ªscal policies and pro-

vided estimates of the effects of taxation and government expenditure on income

distributions in Asia and other countries.

Government expenditures on health and education have reduced income inequality

both in Asia and the rest of the world, but public spending on social protection

shows a distinctive differential distributive impact. Social protection expenditure in

Asia appears to increase income inequality, whereas it reduces it in the rest of the

world. Also adversely affecting the distribution of income in Asian countries is gov-

ernment expenditure on housing.

27

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Coping with Rising Inequality in Asia

For taxation, policies in Asia have a less distinctive differential distributive impact.

Empirical estimates provide some evidence that personal income taxes are more

progressive in Asia than in the rest of the world, possibly because of a larger num-

ber of people not paying income tax. Corporate income taxes, on the other hand,

may be less progressive. This could be due to larger tax incentives, exemptions, and

concessions for Asian ªrms.

Although taxes by themselves are less effective in redistributing income, taxation is

crucial to raise ªnancing for government expenditure to achieve distributional ob-

jectives through spending programs on social welfare and the social sectors, such as

health and education policies. The discussion in this paper suggests that taxes could

be raised more efªciently in some Asian countries. Practically speaking, an efªcient

tax system is one that reduces the disincentive effects of taxation to work, save, and

invest by using broad bases and low, fairly uniform rates. A broad-base, low-rate

system also reduces administration and compliance costs and is often seen as effec-

tively more fair than a narrow-base system because of horizontal equity consider-

ations (taxpayers who have the same income should pay the same amount in taxes)

and vertical equity concerns (people with different incomes should pay different

amounts of tax).

The tax systems in several Asian countries are characterized by relatively high tax

rates and narrow bases. Moreover, there seems to be greater reliance on corporate

income taxation, which tends to be more distortionary (because of internationally

mobile capital) than personal income taxation and VAT. Tax reform in Asia could fo-

cus on lowering income tax rates while broadening the tax base (i.e., abolishing tax

incentives, exemptions, and concessions). This would reduce the economic, compli-

ance, and administrative costs of taxation and likely lead to increases in tax revenue.

Increases in tax revenue, in turn, would allow greater government expenditure to

achieve distributional objectives. Further gains could be achieved in some countries

by shifting the tax burden from income taxation to VAT and broadening the VAT

base. Currently, VAT exemptions and/or reduced tax rates for necessities are often

used to address the potential regressivity of VAT. These are costly, however, and not

well targeted to the poor. A more effective policy would be direct cash transfer pay-

ments to those in need.

With respect to government spending policies, Asia has made considerable progress

in improving education and health outcomes. Social protection policies generally re-

main limited in Asia, however, and in countries where they exist they tend to have a

narrow beneªt coverage and lack targeting to the poor. For instance, unemployment

beneªts are typically restricted to those in formal employment and do not include

28

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

2

3

1

1

6

8

3

3

7

6

a

s

e

p

_

a

_

0

0

2

3

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Coping with Rising Inequality in Asia

the large proportion of those working in the informal sector. Pensions are another

example. In Asian countries, outside the OECD, pension systems are often quite

generous due to early retirement ages and relatively high pension levels, but they

are typically only available to a privileged minority.

Appendix A. Taxation and income inequality in Asia

(7)

(cid:3)0.029*

(0.017)

3.691*

(1.950)

3.981**

(1.713)

(cid:3)0.178**

(0.077)

(cid:3)0.017

(0.024)

(cid:3)0.511***

(0.119)

(cid:3)0.395***

(0.070)

0.097***

(0.012)

4.462***

(0.942)

(cid:3)0.335***

(0.085)

0.102***

(0.012)

0.348***

(0.030)

0.068***

(0.012)

(cid:3)0.053***

(0.013)

(1)

(cid:3)0.071***

(0.009)

4.257***

(0.494)

3.829***

(0.557)

(cid:3)0.084

(0.060)

(cid:3)0.015

(0.022)

(cid:3)0.197**

(0.079)

(cid:3)0.481***

(0.028)

0.093***

(0.010)

2.410***

(0.710)

(cid:3)0.192***

(0.074)

0.101***

(0.007)

0.405***

(0.028)

0.094***

(0.007)

(cid:3)0.015

(0.011)

Gini(cid:3)1

Net

Gross

Population growth

Youth dependency

Old-age dependency

Schooling

Unemployment

GDP per capita

(GDP per cap)^2

Globalization

Corruption

Inºation

Total revenues

PIT

PIT*Asia

PIT*Progress

PIT*Progress*Asia

CIT

CIT*Asia

CIT*Globalization

CIT*Globalization*Asia

SSC(cid:2)Payroll

SSC(cid:2)Payroll*Asia

GTGS

29

(2)

(3)

(4)

(5)

(6)

0.005

(0.023)

3.073**

(1.217)

3.580**

(1.522)

0.351**

(0.179)

(cid:3)0.027

(0.029)

(cid:3)0.290**

(0.138)

(cid:3)0.208**

(0.081)

0.105***

(0.013)

0.860

(1.014)

(cid:3)0.083

(0.102)

0.103***

(0.011)

0.395***

(0.057)

0.069***

(0.012)

(cid:3)0.046***

(0.018)

0.020

(0.015)

5.771***

(1.794)

5.091***

(1.587)

0.051

(0.179)

0.041**

(0.018)

(cid:3)0.512***

(0.178)

(cid:3)0.675***

(0.105)

0.139***

(0.017)

3.025***

(0.838)

(cid:3)0.242***

(0.079)

0.115***

(0.008)

0.328***

(0.043)