Chinese Corporate Debt and Credit

Misallocation*

Ninghua Zhong

School of Economics and Management

Tongji University

1239 Siping Road, Shanghai

P.R. China 200092

zhongninghua@tongji.edu.cn

Mi Xie

School of Economics and Management

Tongji University

1239 Siping Road, Shanghai

P.R. China, 200092

ashley_mi@yeah.net

Zhikuo Liu

China Public Finance Institute & School of Public Economics and Administration

Shanghai University of Finance and Economics

777 Guoding Road, Shanghai

P.R. China, 200433

lzhikuo@163.com

Abstract

This paper analyzes various data, especially that of 4 million Chinese manufacturing company samples

during the period of 1998 to 2013, to present detailed evidence regarding two questions of China’s

leverage issue. First, where is the leverage? We find that within the 16-year period, most sample firms

have been significantly deleveraged, with the average leverage ratio declining from 65 percent in 1998

to 51 percent in 2013. In contrast, only several thousand companies have significantly leveraged, mostly

large-scale, state-owned, listed firms. Second, has the change of leverage been supported by the firms’

fundamentals? We find that for private firms, changes of firm characteristics are consistent with their

leverage changes, whereas firm-level factors can hardly explain the leverage of state-owned enterprises.

We provide further evidence from aggregate-level data, which suggest that the huge amount of credit

being allocated to the state sector is the reason for the declining credit efficiency in China.

* We thank Wing Thye Woo and other seminar participants at the Asian Economic Panel (AEP) for

valuable comments and suggestions. Ninghua Zhong acknowledges financial support sponsored

by the National High-Level Talents Special Support Program (Young Top-notch Talent Program),

the Fok Ying-Tong Education Foundation of China (grant 161081), the National Social Science

Foundation of China (grant 13& ZD015) and the Start-Up Research Grant of Tongji University

(grant 180144). Zhikuo Liu (corresponding author) acknowledges financial support sponsored by

the National Natural Science Foundation of China (grant 71503159) and Program for Innovative

Research Team of Shanghai University of Finance and Economics.

Asian Economic Papers 18:1

© 2019 by the Asian Economic Panel and the Massachusetts Institute of

Technology

doi:10.1162/ASEP_a_00652

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

1. Introduction

After the 2008–09 global financial crisis (GFC), the efficiency of credit allocation in China’s

financial system has dropped significantly. According to Figure 1, it took about RMB 1

(US$ 0.14) new credit for every additional GDP by 2008, but this credit intensity has risen sharply after that and recently reached more than RMB 3 (US$ 0.48).

Meanwhile, China’s broad measure of money supply (i.e., M2) surged after 2008, from

RMB 47 trillion (US$ 6.77 trillion) in 2008 to RMB 155 trillion (US$ 23.33 trillion) in 2016

(Figure 2). That is, in eight years, M2 increased by more than RMB 100 trillion (US$ 16.56 trillion). Recently, China’s M2 has exceeded US$ 20 trillion, and surpassed the largest

economies in the world such as the United States in absolute terms. In addition, the ratio

of M2 to GDP in China has reached over 200 percent.

Combined, these data indicate that although the total amount of credit and financial re-

sources are skyrocketing, the efficiency of the allocation is significantly deteriorating.

In other words, large amounts of money have been allocated to inefficient areas or even

wasted, resulting in a phenomenon called “finance does not support entities,” which is

heatedly discussed in mainland China.

With the declining efficiency of the credit allocation, the overall leverage of China is on the

rise. According to the estimation of the Chinese Academy of Social Sciences and various

organizations,1 China’s total debt has reached RMB 168 trillion (US$ 26.97 trillion), and the ratio of total debt to GDP was up to 249 percent by the end of 2015. This level was in line with some developed countries, including the United States, the United Kingdom, and the euro area, but was much higher than that of developing countries such as Brazil (146 percent) and India (128 percent). It is estimated that this ratio is still currently above 250 percent—that is, the total debt has exceeded RMB 200 trillion (US$ 30.11 trillion).2

Quite intriguingly, against the soaring trend of China’s corporate debt, many Chinese

small- and medium-sized firms, as well as private firms, have found it increasingly difficult

to obtain loans from the formal financial sector. On the other hand, the overall economy

urgently needs to transform toward being innovation-driven. Thus, more financial support

is needed, and it is therefore argued that China should continue to be leveraged.

1 See the briefing meeting held by the Information Department of State Council: http://finance

.sina.com.cn/roll/2016-06-15/doc-ifxtfmrp2071493.shtml; and the report by Financial Times:

http://www.ftchinese.com/story/001067266?full=y.

2 Source: “Is China’s total debt exceeds 200 trillion and ranked second worldwide true?,” Sohu Fi-

nance and Economics, 18 February 2017.

2

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

Figure 1. Credit intensity rising further

Source: CEIC and China’s National Bureau of Statistics.

Figure 2. Funds supply surged

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: CEIC and China’s National Bureau of Statistics.

Considering these factors, it is difficult to conclude whether China should continue lever-

aging. In fact, for a complicated economy such as China, any general conclusion could be

biased, and any unified policies and measurements may be inefficient. Perhaps, rather

than discussing the overall “optimal debt ratio” of the Chinese economy, we should

first pin down some basic facts, such as: Across different sectors, industries, regions,

ownerships and periods, where is the leverage? It is the first question that we want to an-

swer in this paper.

3

Asian Economic Papers

Chinese Corporate Debt and Credit Misallocation

Several recent reports have pointed out that across different sectors (e.g., enterprises, resi-

dents, and governments), the debt of non-financial enterprises in China is the highest and

has risen rapidly since 2008. During the period of 2004–08, such debt accounted for less

than 100 percent of China’s GDP,3 whereas it reached 105.4 percent in 2010 and surpassed

all other major countries.4 It continued to soar in the following years and reached 163 per-

cent in June 2015.5 Moreover, according to the estimates by Standard and Poor’s (2014),6 by

the end of 2013, the total debt of non-financial enterprises in China was US$ 14.2 trillion, which has exceeded that in the United States (US$ 13.1 trillion). They further predict that

by the end of 2018, China’s corporate debt will account for more than one-third of the total

corporate debt worldwide.

This paper further examines the changes of corporate leverage in China, mainly using the

data of China’s all industrial enterprises that are above designated scale during 1998 to

2013,7 which comes from the Annual Survey of Industries Firms conducted by China’s

National Bureau of Statistics.8 We first analyze the debt ratio (i.e., total liabilities / total

assets) of nearly 4 million observations in this set of data. As can be seen from Figure 3, the

simple average and median of debt ratio decreased from 65 percent in 1998 to 51 percent in

2013, representing a decline of 14 percentage points in 15 years and an average descending

of nearly 1 percentage point annually.

Furthermore, breaking down total debt into short-term debt (matured within one year) and

long-term debt, we find that the average short-term debt to total assets ratio decreased

from 55 percent in 1998 to 47 percent in 2013 (see Figure 4), and the average long-term

debt ratio decreased from 11 percent in 1998 to 6 percent in 2013 (see Figure 5). That is, the

short-term debt ratio contributes more to the decline in total debt ratio; whereas, given

the very low initial level of long-term liabilities, it takes a much larger decrease indeed.

3 Source: “Li Yang’s View on De-leveraging: Monetary Policy Will Be Tight,” Sina Finance, 23

September 2017.

4 Source: “Li Yang: Liabilities of Chinese Enterprises Have Exceeded the Warning Line,” China

News, 18 May 2012.

5 Source: “Huang Yiping: Cracking Down China’s High-leverage Trap,” Caixin, 14 March 2016.

6 Standard and Poor’s, “Credit Shift: As Global Corporate Borrowers Seek $60 Trillion, Asia-Pacific Debt Will Overtake US and Europe Combined,” RatingsDirect, June 2014. 7 During the period of 1998–2006, those above designated scale enterprises referred to the entire state-owned industrial sector and the non–state-owned enterprises (non-SOEs) with an annual operating income of RMB 5 million (US$ 0.62 trillion) or more. From the beginning of 2007, it ex-

cluded those whose annual operating income was less than RMB 5 million (US$ 0.62 trillion) even if they were SOEs. Furthermore, the standard has been raised from the annual operating income of RMB 5 million (US$ 0.62 trillion) to RMB 20 million (US$ 3.10 trillion) since 2011. 8 This survey covers all firms with more than RMB 5 million (US$ 0.75 million) in revenues in the

industrial sector, and it includes nearly 4 million observations for this period.

4

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

Figure 3. Average debt ratio of China’s non-listed industrial enterprises, 1998–2013

Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics.

Figure 4. Short-term debt ratio of China’s non-listed industrial enterprises, 1998–2013

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics.

Noteworthy is that the median of the long-term debt ratio was zero for most of the years,

indicating that more than half of the sample enterprises were not able to obtain any

long-term debts.

This declining trend is inconsistent with the rising corporate debt ratio that we have ob-

served in the aggregate data. We thus deduce that it is a small sample of firms that have

raised their leverage significantly. We thus divide the whole sample according to different

5

Asian Economic Papers

Chinese Corporate Debt and Credit Misallocation

Figure 5. Long-term debt ratio of China’s non-listed industrial enterprises, 1998–2013

Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics.

standards and give detailed statistical descriptions, which are provided in Section 2. After

elaborative examination, we summarize the following six facts.

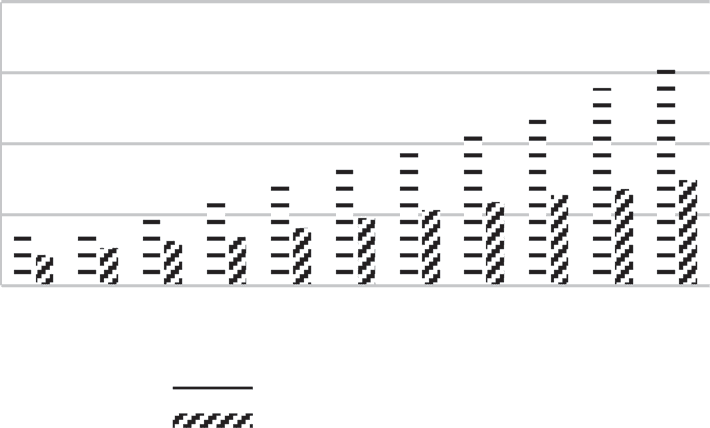

Fact 1: The longer a firm exists in the sample, the smaller the decline in debt ratio.

Fact 2: The debt ratio of large enterprises decreased slightly, whereas that of small- and

medium-sized enterprises (SMEs) dropped significantly.

Fact 3: The decreasing range of debt ratio in heavy industrial enterprises was generally

much smaller than that of light industrial enterprises; and the average debt ratio of

public utility enterprises was on the rise.

Fact 4: The average debt ratios of enterprises in northeast and central regions decreased

the most, by more than 20 percent, whereas that of those enterprises in developed

eastern regions was quite stable.

Fact 5: The average debt ratio of state-owned enterprises (SOEs) was always higher

than that of private enterprises, which was, in turn, higher than that of overseas-

funded enterprises. Among all types of enterprises, the average debt ratio of SOEs

dropped the most. Noteworthy is that the average debt ratio of SOEs that have been

in existence for a long time was stable and rose after 2009.

Fact 6: The average debt ratio of manufacturing enterprises that listed on the Main

Board was on the rise and surpassed that of non-listed companies after 2009.

Although these facts are simple statistical descriptions, they may provide some important

factual basis for discussing the debt ratio in China and correct some of the existing main-

stream views. First, in recent years, many media and institutional reports have focused on

6

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

the record-high debt ratio in China after the GFC, creating an illusion that the debt ratio

of Chinese enterprises is generally on the rise. In fact, the six facts show that the increase

in debt ratio is sharply concentrated on thousands of enterprises, most of which are large,

state-owned and listed companies.

The following statistics can best emphasize the sharp concentration of Chinese corporate

debt. The data of Chinese industrial enterprises contains around 345,000 enterprises for

2013; in total, those enterprises had debts totaling RMB 49.1 trillion (US$ 7.37 trillion). With the enterprises that held the most debt, nearly half of the total debt was in the top 2,000 en- terprises (RMB 13.5 trillion) and more than a quarter was held by the top 500 enterprises (RMB 23.5 trillion). We have also analyzed the second data set, the Chinese listed firm database, and obtain similar findings. According to our estimation, in 2015, the top 300 heavily indebted listed enterprises owed 82 percent of all debt, amounting to RMB 16 tril- lion (US$ 2.40 trillion), and the top 50 enterprises owed 54 percent of all debt, amounting to

RMB 11 trillion (US$ 1.65 trillion). l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Among them, Petro China Co. is China’s largest oil and gas producer and is the most in- debted listed company, owing RMB 1 trillion (US$ 0.15 trillion) in 2015. It is followed by

China State Construction Engineering Corp., China Petroleum & Chemical Corp., China

Railway Construction Corp., China Railway Group Ltd., and China Communications Con-

struction Corp. (which was listed in 2012 and did not release data prior to 2011). In 2015,

those five companies held total debts of more than RMB 3 trillion (US$ 0.45 trillion). In ad- dition, according to the Beijing News, by the end of 2015, the total debt of the seven major coal enterprises in Shanxi exceeded RMB 1.1 trillion (US$ 0.18 trillion).9

Thus, China’s corporate debt issue is highly “structural.” Most debts are held by a small

fraction of companies, whereas debt ratio is declining in most companies.

After establishing the basic facts, Sections 3 and 4 of this paper attempt to further explore

the question about whether the change of debt ratio is supported by economic fundamen-

tals using both the firm-level (i.e., the micro-level) and the aggregate-level data (i.e., the

macro-level). China is not an exception to the rule that rapid growth of developing coun-

tries is usually accompanied by an increase in the debt of the enterprises sector. Therefore,

we need more precise analysis to answer the question of whether the rising leverage of

non-financial enterprises is supported by their fundamentals. Especially because in the

past few decades, with the rapid marketization process in China, some of the main char-

acteristics of Chinese enterprises have undergone very significant changes. For example,

9 See reports: “Shanxi’s Seven Major Coal Enterprises’ Debts Reach Y1.1 Trillion, and Rely on Gov-

ernment’s Subsidies to Pay Wages,” http://www.rmlt.com.cn/2016/0517/425866_3.shtml.

7

Asian Economic Papers

Chinese Corporate Debt and Credit Misallocation

their profitability has improved significantly (see Figure 16 later in this paper). It is reason-

able for an enterprise to borrow more money from outside based on its rising profitability,

because its expected cash flows could repay more debt.10 Similarly, some enterprises in

China, mainly large SOEs, have experienced a rapid process of capital deepening. In other

words, they have more fixed assets. It is also reasonable for these enterprises to borrow

more because they have more collateral; if they cannot repay, they can sell the fixed assets.

Such increases in leverage are backed by economic fundamentals.

On the contrary, there are some increases in leverage, which are not supported by eco-

nomic fundamentals, and are thus widely concerning. For example, many recent discus-

sions have referred to state-owned “zombie” enterprises. According to Tan, Huang, and

Woo (2016), in 2007 the number of zombies in Chinese industrial enterprises accounted for

12.1 percent, and the proportions of assets and liabilities were 10.7 percent and 13.4 per-

cent, respectively.11 It is estimated that these proportions significantly rose after the GFC.

The profitability of these enterprises is extremely low or even negative continually; nev-

ertheless, even with the high debt, they could survive through receiving substantial loans

from the banking system. Meanwhile, many much-more-profitable private enterprises

are unable to borrow from banks. Such a contrast leads to reasonable conjectures about

increasing credit misallocation.

To explore this issue, in Section 3, we start by referring to the literature on Western capital

structure and examining the changes in six important corporate characteristics that deter-

mine the credit financing. We find that the average scale of Chinese enterprises during the

period of 1998–2013 has been much larger and the operational risk has been on the rise; the

proportion of tangible assets (mainly including fixed assets and inventories) has been de-

clining, and profitability has been continuously increasing. These changes are the results at

the firm-level (i.e., micro-level) of the transformation of China’s overall economy toward

being market-oriented. As the competition in the domestic and foreign product markets is

becoming more and more intense, the risks of operation are increasing, while the profitabil-

ity and scale of those surviving enterprises are becoming stronger and larger. In addition,

the market competition also forces enterprises to adopt a more competitive approach to

production. Therefore, Chinese enterprises are constantly transforming to labor-intensive

and light capitalization, which is shown in the declining share of tangible assets.

These changes of firm characteristics have varying influence on the changes of leverage,

therefore we further refer to the standard regression models in the literature of Western

10 On the other hand, enterprises with high profitability tend to rely less on external capital because

they can generate enough cash flow.

11 The methodology for identifying zombie enterprises refers to the CHK approach presented in

Caballero, Hoshi, and Kashyap (2008).

8

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

capital structure to examine collectively the relationships between these variables and

the debt ratio. We find that in the sample of private enterprises, the regression results are

highly consistent with the Western literature; also, the changes in firm characteristics are

consistent with changes in the debt ratio. For example: (1) the operating risk is negatively

related to the debt ratio, so the rise of business risk may result in the decrease of the debt

ratio; (2) the tangible asset is the collateral of debt financing and is positively related to the

debt ratio, whose decline may lead to a decline in the debt ratio; and (3) the average profit

margin of an enterprise is negatively related to the debt ratio—that is, the relationship be-

tween internal cash and external financing is an alternative. Therefore, the increase in prof-

itability may also be the reason for the descending debt ratio. We hence draw a preliminary

conclusion, that the financing decisions of private enterprises are in line with the principle

of marketization.

In the sample of SOEs, however, except for the profit margin, other important firm char-

acteristic variables are insignificant or even have an unexpected sign; we can hardly ex-

plain the change in the debt ratio of SOEs by the changes in the firm characteristics. Apart

from these analyses, we have also examined Chinese listed enterprises, and find that there

were about 160 listed SOEs whose profits (earnings) before interest and tax (EBITs) are not

enough to pay off interest. These enterprises could only keep borrowing new debts to re-

pay the old ones; as a result, the “snowball of debt” grows larger and larger. This evidence

also indicates that the liabilities of some SOEs are indeed too high, which eventually results

in excessive interest burden.

In Section 4, we use the aggregate-level data (i.e., macro-level) to provide further evidence

on SOEs’ over-leverage. We find that state-owned industrial enterprises as a whole have

been increasing their leverage after 2008 and their overall debt ratio has risen from 58 per-

cent in 2008 to 62 percent in 2016, whereas the private sector has been under accelerated

deleveraging, with the overall average debt ratio falling from 58 percent to 52 percent. In

other words, the private sector has been deleveraging for more than a decade. Moreover,

recently, private industrial enterprises as a whole contribute nearly 40 percent of the to-

tal profit in all industrial enterprises, while their liabilities only account for 20 percent of

the total amount. In contrast, state-owned industrial enterprises as a whole contribute less

than 20 percent of the total profit, while their liabilities account for more than 40 percent of

the total amount. According to the Ministry of Finance, the total debt of the Chinese state-

owned sector has reached RMB 100 trillion (US$ 15.14 trillion), whereas the return on total assets (ROA) is only 1.91 percent. Therefore, we draw a preliminary conclusion that lever- age of SOEs is not supported by economic fundamentals, and there are some non-market factors that are driving up their leverage. It is noteworthy that this conclusion is also consistent with another important phenomenon that emerged after the GFC: SOEs are heavily involved in shadow banking activities such 9 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation as entrusted lending or loans.12 Such involvement suggests that these enterprises do not have good investment opportunities themselves but can borrow large amounts of money from the financial system at a lower cost and then lend to others (e.g., to the private sector) to obtain the interest spread, which also proves from the sidelines that the debt ratio of these SOEs is indeed too high. This article differs significantly from existing research on the capital structure of Chinese enterprises. Much of the research has been made by applying some standard empirical tests from Western literature directly to Chinese enterprises and examining the explana- tory power of the mainstream capital structure theories such as “pecking order theory” and “trade-off theory” on Chinese corporate debt. For example, Chen (2004) finds that the capital structure of listed companies in China is not in line with the classic pecking order theory, their order of financing is: retained earnings, equity financing, and debt financing. Chen and Strange (2005) find that unlike the expectation of trade-off theory, Chinese listed companies do not show a stable optimal debt ratio. Newman, Gunessee, and Hilton (2012) examine 1,539 private-owned SMEs in Zhejiang Province and find that firm size was posi- tively correlated with the debt ratio, and there is a significant negative correlation between profitability and debt ratio, which are consistent with the expectation of pecking order the- ory. However, the relationship between the proportion of fixed assets and the debt ratio is not significant. Other literature focuses on whether the main determinants of the firm’s capital structure in developed countries can similarly explain the capital structure of Chinese listed compa- nies. For example, Huang and Song (2006) find that the correlations between the debt ratio of listed companies in China and firm size, and between the debt ratio and the proportion of fixed assets, profitability, non-debt tax shield, and growth are basically consistent with the empirical findings of developed countries; the main difference is that the share of long- term debt in Chinese companies is very low. Bhabra, Liu, and Tirtiroglu (2008) examine the long-term debt ratio of listed companies in China especially and find that it is positively related to the firm size and the proportion of tangible assets, but negatively correlated with profitability and growth. Compared with this research, Li, Yue, and Zhao (2009) take more unique institutional fac- tors in China into consideration and is the most like our paper. The sample they study is the capital structure of Chinese industrial firms during the period 2000–03. They find that the state-owned and private enterprises have higher debt ratios than overseas-funded ones. In addition, in areas where the legal environment and the banking system are more developed, enterprises have lower total debt ratios. 12 See “The Popularity of State-Owned Enterprises Participating in the Shadow Banking,” http://finance.sina.com.cn/money/bank/bank_hydt/20110910/121410464849.shtml. 10 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation The existing literature has focused on the cross-sectional differences, whereas our paper examines the changes in the time-series—that is, to understand the significant changes in the debt ratio of Chinese enterprises in the context of China’s overall economic transfor- mation. As we will show later: During the relatively short sample period of 1998–2013, the debt ratio and key characteristics of Chinese enterprises have changed dramatically. Such dramatic changes may only happen in countries with rapid transformation such as China. In mature economies such as the United States, both the financing and the main features of enterprises are much more stable; therefore, the studies on the capital structure of Western enterprises naturally focus more on the cross-sectional differences. More importantly, the main purpose of this paper is not to test or develop the Western cap- ital structure theories, but to provide valuable analysis and suggestions on the issues of whether to deleverage China and how to deleverage. For these complicated issues, our re- search is still relatively preliminary. Our results indicate that a complete answer should include at least two parts. First, the financing decisions of some enterprises, mainly private enterprises, are generally in line with the principle of marketization. For these enterprises, adequate capital supply should be guaranteed so that the enterprises with fundamental supports can borrow enough money. Second, there are many “non-market-oriented” fac- tors in the determinants of the debt of SOEs. Thus, we should cease the blood transfusion to inefficient ones as soon as possible and allocate new loans to the most efficient areas. Mean- while, we suggest selling SOEs’ stock assets to repay the stock liabilities. Considering the already very high total leverage ratio of China, the efficiency of the incremental fund’s allo- cation would determine the potential of China’s medium- and long-term economic growth in the future. 2. Where is the leverage? l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . 2.1 The data The first data set at firm-level that we examine comes from the Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics from 1998 to 2013 (the data from 2010 is missing because of very poor quality), and the total number of observations was 3,911,364 originally. We first examine the major accounting identities,13 requiring that the absolute value of [total liabilities + owner’s equity – total assets] be less than 1 percent of total assets, resulting in 82,783 observations being deleted. Second, we check the identity of the total debt, requiring that the absolute value of [total debt – short-term debt – long-term debt] be less than 1 percent of total assets, and delete 203,920 observations. Third, we delete 4,774 observations with current liabilities larger than total liabilities; 3,141 observations f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 13 In the data of 2008 and 2011–13, there is a large amount of missing data of short-term liabilities and long-term liabilities, so only non-missing samples are considered for the proofreading of debt identities. 11 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 6. Debt ratio: Classified by the years of consecutive existence l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. with long-term liabilities larger than total liabilities; and 30 observations with negative main operating income. Then, we delete 82,197 observations because of missing regression variables. Thus the total number of the observations is 2,325,703. In addition, some of the analyses in this paper use the data of listed firms during 1998 to 2013 from CSMAR. We delete the observations of non-industrial enterprises, and exclude firms listed on the Small- and Medium-sized Enterprises Board and on the Growth Enter- prise Market, which results in a total of 20,306 observations. We also do 1 percent and 99 percent winsorization for each firm-level variable. 2.2 Descriptive statistics on sub-samples: Six sets of facts In this section, we present six facts about the changes in debt ratio of Chinese enterprises in sub-samples sorted by various standards. These facts are fundamental to further explore China’s leverage issues. Fact 1: The longer a firm exists in the sample, the smaller the decline in its debt ratio. Fact 1 is the conclusion drawn by grouping the whole sample according to the years in which the enterprises continuously exist in the database. We divide the enterprises into four groups, with the existing years of the sample firms being 3, 7, 11, and 15, respec- tively. Figure 6 depicts the changes in the average debt ratio of these sub-samples, and the 12 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 7. Debt ratio: Classified by enterprise scales l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. average debt ratio of the enterprises with continuous existence of more than 3 years was 67 percent in 1998 and dropped to 48 percent in 2008, suffering a decrease of 19 percentage points. However, the average debt ratio of those that have existed for more than 15 years declined from 58 percent to 54 percent during this period, only experiencing a decline of 4 percentage points. Fact 2: The debt ratio of large enterprises decreased slightly, whereas that of SMEs dropped significantly. We then classify the whole sample according to the size of the enterprises and conclude Fact 2. The division of large- and medium-sized enterprises is based on the principle of “Interim Provisions on Standards for Small- and Medium-sized Enterprises” formulated by the State Economic and Trade Commission, the State Development Planning Commis- sion, the Ministry of Finance, and the National Bureau of Statistics in 2003. Accordingly, companies with fewer than 2,000 employees, or annual revenues of less than RMB 300 million (US$ 45 million), or total assets of less than RMB 400 million (US$ 60 million) are defined as SMEs, while the others are defined as large enterprises. Figure 7 shows that the debt ratio of large enterprises saw a slight decrease to 57 percent in 2013 from 61 percent in 1998, whereas that of SMEs saw a sharp decrease to 51 percent in 2013 from 65 percent in 1998. That is, the debt ratio of SMEs has significantly decreased. 13 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 8. Debt ratio: Three typical industries Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. Fact 3: The decreasing range of debt ratio in heavy industrial enterprises was generally much smaller than that of light ones; and the average debt ratio of public utility enterprises was on the rise. Fact 3 is the conclusion drawn by grouping the whole sample according to the industry of the enterprises. We divide all sample companies into 39 groups referring to the two- digit industry classification number in the national economy. Because of the large number of industry groups, we do not report the results one by one. In general, the debt ratio of heavy industrial enterprises bore a much smaller decline than light industrial enterprises. Figure 8 reports the debt ratio of several typical industries. For example, the debt ratio in the coal mining and washing industries fell to 58 percent in 2013 from 61 percent in 1998, and farm and sideline food processing industries saw their debt ratio drop to 44 percent in 2013 from 72 percent in 1998. The average debt ratio of public utility enterprises was on the rise, however. For example, water production and supply enterprises saw their average debt ratio rising to 55 percent in 2013 from 40 percent in 1998. Fact 4: The average debt ratios of enterprises in the northeast and central regions decreased most, by more than 20 percentage points; whereas enterprises in developed eastern regions were quite stable. We conclude Fact 4 by dividing the whole sample according to the province in which the enterprises are located. The average debt ratios of enterprises in the northeast and cen- tral area have decreased by 20 percentage points, marking the maximum decline among 14 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 9. Debt ratio: Classified by enterprise region l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. different regions. Average debt ratios in the northeast, central, and western regions were all about 69 percent in 1998. The ratios declined to 45 percent in the northeast and central regions by 2013 and to 55 percent in the western region. The average debt ratio in the east- ern region dropped by the minimum to 55 percent from 63 percent in 1998 (see Figure 9). We have also examined the average debt ratio for each province and find the following six provinces different from others: The average debt ratio in Beijing kept a quite stable trend; Shanghai and Tianjin declined slightly while the average debt ratios in the coast dis- tricts such as Guangdong and Zhejiang increased slightly; in addition, Xizang was the only province with a significant increase (see Figure 10). Fact 5: The average debt ratio of SOEs was always higher than that of private enterprises, which was, in turn, higher than that of overseas-funded enterprises. Among all types of enterprises, the average debt ratio of SOEs dropped the most. Noteworthy is that the aver- age debt ratio of SOEs that have existed in the sample for a long time was stable and rose after 2009. Fact 5 is the conclusion drawn by grouping the whole sample by the registration type of enterprises and then examining their average debt ratio.14 During 1998 to 2013, the 14 The state-owned group includes SOEs, state-owned-joint enterprises, state- and collective-owned enterprises, and wholly SOEs. The private sector includes private-owned enterprises, private- partnership enterprises, private-limited enterprises and the enterprises limited by shares. The overseas-funded sector includes joint ventures, cooperative enterprises, Hong Kong-, Macao-, 15 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 10. Debt ratio: Several special provinces Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. average debt ratio of SOEs dropped from 73 percent to 62 percent, compared with the de- cline from 58 percent to 50 percent for private enterprises, and from 55 percent to 50 per- cent for overseas-funded enterprises (see Figure 11). The average debt ratio of SOEs has always been significantly higher than the private sector, while that in the private sector is generally higher than overseas-funded enterprises.15 In addition, it is worth noting that it is becoming increasingly difficult for private enterprises to borrow money, and this trend seems to have begun earlier in 2004, not just after the GFC.16 Figure 11 also suggests that the decline in the debt ratio of SOEs is the largest during the period of 1998–2013. However, a more interesting result about the correlation between ownership and firm capital structure is shown in Figure 12. By narrowing the sample down to stable enterprises that always exist in the database between 1998 and 2013 (i.e., exist over 15 years), we find the debt ratio of stable SOEs rose to 62 percent in 2013 from 59 percent in 1998, whereas the debt ratios of stable firms with other ownership were all declining. and Taiwan-owned enterprises and Hong Kong, Macao and Taiwan Investment Co., Ltd. (if the investors from Hong Kong, Macao, and Taiwan gain the investment ratio of more than 25 per- cent), and Sino-foreign cooperative ventures, Sino-foreign joint ventures, wholly foreign-owned enterprises and foreign investment Co., Ltd. (if the proportion of foreign investment exceeds 25 percent). The mixed sector includes collective enterprises, joint-stock limited enterprises (domestic capital), and other enterprises. 15 Regarding to this result, Li Yue, and Zhao (2009) make a very careful discussion based on the data set from Industrial Census during 2000–03. 16 Of course, the GFC significantly affected the private sector’s exports and reduced its profitability, thereby enhancing their demand for external funds. This makes the issue of private financing constraints more prominent. 16 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 11. Debt ratio: Classified by ownership Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. Figure 12. Debt ratio: Stable and persistent enterprises grouped according to ownership l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. Noteworthy also is the division within the state-owned sector in terms of the access to loans. The average debt ratio of SOEs as a whole has decreased significantly, whereas only a small part among them has increased sharply. Based on this result, the reform of SOEs that was implemented in the past few decades seems to have broken the soft budgetary constraints of small- and medium-sized SOEs. However, large SOEs still have easier access 17 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 13. The opposite tendency of debt ratio of listed and non-listed firms Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. to capital, which could be the result of a policy—namely, “managing the big, liberating the small”—that the Chinese central government took since the late 1990s. Fact 6: The average debt ratio of listed manufacturing enterprises was on the rise, and sur- passed that of non-listed companies after 2009. Finally, we put the debt ratios of listed and non-listed firms into one figure to conclude Fact 6. We use listed manufacturing companies that are traded on the main board of China’s stock market, which is the only board that existed before 2004. The contrast is obvious for both the level and the trend (see Figure 13). In 1998, the average debt ratio of listed man- ufacturing companies was 39 percent. This amount is not unusual, because listed firms raise money through equity financing, and thus their proportion of debt financing is usu- ally lower than non-listed firms.17 However, a more important finding is that whereas the average debt ratio of non-listed manufacturing companies is declining, that of the listed manufacturing companies has continued to rise and has reached 55 percent, further ex- ceeding that of non-listed manufacturing enterprises since 2009.18 17 Huang and Song (2006) compare the debt ratio of listed companies in China with that of other countries. They find that the total debt ratio and long-term debt ratio of listed companies in China are significantly lower while the proportion of equity financing is significantly higher. They pro- pose that one of the reasons for this is the high valuation of listed companies in China. Relatively, some literature (such as Chen 2004) proposes that one of the characteristics of the financing in Chinese listed companies is that equity financing has priority over bond financing. 18 The rise of the debt ratio in Chinese listed companies during this period is mentioned in some literature, such as Huang and Song (2006). The explanation they give is the development of the 18 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation 3. Is the leverage supported by economic fundamentals? Evidence from micro-level data 3.1 Changes in the important firm characteristics After describing the heterogeneous changes in the corporate debt ratio in China, we then try to examine whether these changes are consistent with the changes in the characteristics of the enterprises. Hence, we focus on four key features of enterprises that are commonly tested in the literature of Western capital structure (see Rajan and Zingales 1995; Frank and Goyal 2003), including operational risk (volatility of profit), proportion of tangible assets, profitability, and firm scale. Referring to previous research on the capital structure of Chinese enterprises (e.g., Wu and Yue 2009), we also examine tax rates and non-debt tax shields. The changes in these six aspects over the period 1998–2013 are reported in Figures 14 to 19. As these six factors are the major dependent variables in the regressions reported later, we do not report their summary statistics, which have been reported by the figures. What needs to be explained is as follows. (1) Our intention in this section is to explore whether changes of debt ratios are consistent with the changes of firm characteristics rather than to set up causal relationships. To strictly demonstrate the causal relationships between various enterprise factors and the debt ratio probably requires exogenous shocks and well-designed identifications. The evidence provided in this paper is mainly the correlation and therefore is relatively preliminary. Furthermore, our conclusion relies more on the results of the fixed-effects regression in Section 3.2 rather than the descriptive analysis in Section 3.1. (2) The two mainstream capital structure theories, including pecking order theory and trade-off theory, have different predictions on the relationships between these vari- ables and the debt ratio. We do not elaborate here due to space limitations. (3) Given a positive or negative relationship found between a factor and the debt ratio, different interpretations can be presented based on different theories. In this section, we provide only one explanation that we consider to be the most intuitive, avoiding more detailed discussions intended to distinguish between different theories, which would take much more space. (4) Analyzing changes in these characteristics is, in and of itself, important for under- standing the overall economic transformation that has taken place in China during this period. However, the focus of this article is on discussing whether these changes in time-series are consistent with the change in debt ratio. As for the reasons behind the changes, we only make some speculations that may not be regarded as rigorous analyses and conclusions. bond market. Nevertheless, they (along with other researchers) do not dig deeply into the analysis of this phenomenon. 19 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 14. Operational risk: Classified by the years of consecutive existence Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. 3.1.1 Operational risk We first examine the changes in operational risk, measured by the company’s standard deviation of ROAs over the past three years. This risk keeps rising since the late 1990s, soaring further around 2008, and then declining slightly (see Figure 14). The overall increase in this risk is partly due to the intense competition in China’s do- mestic product market, and also due to Chinese enterprises being more involved in the competition of the international market. The fierce competition makes it increasingly diffi- cult for an individual enterprise to control the market and maintain a stable profit margin. Fluctuations in profits thereby enhance the uncertainty of future cash flows, which in turn reduce the probability of enterprises to obtain external funds. Therefore, the rise of opera- tional risk may be one of the reasons for the overall decline in debt ratio. Furthermore, Figure 14 also suggests that the shorter the duration of existence, the greater the increase in the operational risk. For example, the operational risk of enterprises that exist continuously for more than three years has risen from 4.9 percent in 2000 to more than 10 percent in 2011; however, this risk of those existing for more than 11 years has changed by a much smaller margin. The reason behind this may be that the shorter an enterprise exists, the greater the probability of withdrawing from the sample, indicating that the en- terprise has a greater risk of bankruptcy and probability of default, which also reduces the probability of obtaining external financing. Therefore, Figure 14 is consistent with Fact 1 that we observed in Figure 6—that is, the shorter a firm exists in the sample, the greater the decline in its debt ratio. 20 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 15. The proportion of tangible assets in Chinese enterprises Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. 3.1.2 Proportion of tangible assets The proportion of tangible assets (i.e., the sum of net fixed assets and net inventories) in total assets of Chinese enterprises declines from 63 percent in 1998 to about 48 percent in 2013, namely, there is a decrease of 15 percentage points in total (see Figure 15). The ratio of fixed assets to total assets and the proportion of inventories fell by about 9 and 6 percentage points, respectively. The decline in the proportion of fixed assets in enterprises is an important manifestation of China’s economic transformation, indicating that the mode of firms’ production is chang- ing towards more consistent with their comparative advantages. More specifically, they move from a capital-intensive mode in the planned economy period that violates compar- ative advantages to a labor-intensive one (see Lin, Cai, and Li, 1998). The reasons for the decline in inventories are more complicated, which may be due to the improvement in lo- gistics or the decline of expected demand in the future. Both fixed assets and inventories can be used as collateral for debt financing, so the scale of tangible assets is an important factor in determining the financing ability of an enterprise. The higher the proportion of tangible assets, the lower the degree of information asymme- try between the enterprises and the banks—thereby the stronger the borrowing ability a firm has, the easier it would be to obtain debt financing. So, the proportion of tangible as- sets in Chinese enterprises decreasing significantly in the period of 1998–2013 is also likely to be an important reason for the overall decline in debt ratio.19 19 The changes in tangible assets can also explain Fact 3, that the debt ratio of typical heavy indus- trial enterprises is lower than that of typical light industry enterprises in Figure 6. This may be 21 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 16. Sales profit margin: Enterprises grouped according to ownership Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. Figure 16 depicts the sales profit margin (i.e., total profit / main 3.1.3 Profitability business revenue) in four groups of enterprises classified by ownership. The profit margin of all types of enterprises in China continued to rise as a whole and reached a peak by 2011, after which it began to decline slightly. In terms of ownership, the average profit margin of SOEs rose from –1 percent in 1998 to more than 3 percent in 2011, whereas that of private enterprises was always the highest among the four categories—it started from less than 3 percent in 1998 and went up to more than 6 percent in 2011. An increase in the level of profitability means more internal funds, which reduces the need for external financing. Therefore, the continuous rising average profit margin in Chinese enterprises may also be one of the reasons for the overall debt ratio declining. Furthermore, the increase in the profit margin of SOEs is the most significant among the four groups, which is consistent with the largest drop in their debt ratio observed in Figure 11. 3.1.4 Size by the natural logarithm of the total assets. The scale of Chinese enterprises as a whole Figure 17 shows the size of four groups of enterprises, which is measured due to the fact that the proportion of fixed assets of heavy industrial enterprises has declined by a relatively small margin. In addition, Figure 3 shows that the decline in the long-term debt ratio is even greater. Compared with short-term liabilities, long-term liabilities require the higher level of collateral. Bhabra, Liu, and Tirtiroglu (2008) examine the capital structure of Chinese listed companies in different industries and find that capital-intensive firms such as manufacturing and utilities use more long-term debt. Therefore, the decline in tangible assets may also be an important reason. 22 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 17. Size: Enterprises grouped according to ownership l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. was getting larger—in particular, SOEs have increased their average size by nearly 20 times from 1998 to 2013. Generally, the larger the company is, the lower the probability of bankruptcy and the higher the debt ratio. Therefore, the change in scale does not seem to explain the decline in the overall debt ratio of Chinese enterprises. 3.1.5 Tax rate Western literature finds that tax rate is a very important factor in de- termining the capital structure of enterprises. Wu and Yue (2009) examine Chinese listed companies and find that the change of taxation can lead to the change of the debt ra- tio. Enterprises should pay interests on debt financing, and these expenses reduce the pre-tax profits, thereby reducing the income tax. Thus, debt financing can offset part of the tax, which acts as a tax shield and it is the main benefit of debt described by the trade-off theory. Figure 18 displays the income tax rate (income tax payable / total profit) of sample en- terprises.20 It shows that the average income tax rate of the whole sample rose during the period 1998–2013. At the same time, we also notice that there are a certain proportion of the sample enterprises having the negative rate. To eliminate the influence of these enter- prises, we then calculate the tax rate for those enterprises with positive income tax payable 20 Strictly speaking, the actual income tax rate (income tax expenses / total profit) should be used here. However, this index is not available in the data set of Chinese industrial firms, so we could only approximate it with the total income tax payable. In addition, income tax expenses include current income tax payable and deferred income tax. 23 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 18. Income tax rate of Chinese enterprises l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. (see Figure 18). It shows that the average tax rate for this group of companies stabilized at around 27 percent before 2006, and then decreased sharply in 2007 and 2008, after which it stabilized again at around 22 percent. In short, it shows that there was no significant de- crease in tax that can be shielded by debt, so that the change in taxation does not appear to be the main reason for the declining debt ratio. Like tax shields, depreciation can also reduce the pre-tax 3.1.6 Non-debt tax shield profits of an enterprise, thereby reducing the tax payable; hence, it is called a non-debt tax shield, which has a substitute relationship with the debt tax shield and is measured by (de- preciation / main operating revenue). It shows that the non-debt tax shields of the sample enterprises have significantly dropped as a whole (see Figure 19), which is consistent with the continuous decline in the proportion of fixed assets that we have reported earlier and should increase the incentive for companies to use debt shields to avoid taxation. Accord- ing to Figures 18 and 19, the motivation for Chinese enterprises to use debt to avoid tax expenses has not been reduced, thus the consideration of tax is not the main reason for the sharp decline in the debt ratio of Chinese enterprises. 3.2 Regression analysis: Enterprise characteristics and debt ratio Our analyses indicate that the overall decline of Chinese companies’ debt ratio may be partly due to the significant changes in the main characteristics of the enterprises, espe- cially the operational risks, profitability, and the proportion of the tangible assets. In the 24 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation Figure 19. Non-debt tax shield of Chinese enterprises l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Source: Annual Survey of Industries Firms conducted by China’s National Bureau of Statistics. Table 1. Debt ratio of various enterprises in China: Benchmark regression Variables L.TotLev L.STDROA L.Size L.Tng L.Npr L.tax Nonpositive × L.tax Observations R2 Number of firm fixed effects Year dummies Province × Year dummies Industry × Year dummies (1) All 0.269*** (0.002) −0.028*** (0.005) 0.003*** (0.001) 0.010*** (0.001) −0.158*** (0.003) −0.020*** (0.001) 0.056*** (0.004) 1,203,426 0.825 328,727 YES YES YES (2) State 0.365*** (0.006) 0.017 (0.021) −0.004* (0.002) 0.003 (0.005) −0.088*** (0.005) −0.028*** (0.003) 0.043*** (0.008) 159,188 0.879 47,290 YES YES YES (3) Private 0.194*** (0.003) −0.046*** (0.006) 0.005*** (0.001) 0.004** (0.002) −0.184*** (0.006) −0.015*** (0.002) 0.065*** (0.006) 675,955 0.821 212,433 YES YES YES (4) Foreign 0.314*** (0.004) 0.025** (0.010) 0.010*** (0.001) 0.027*** (0.003) −0.168*** (0.006) −0.029*** (0.003) 0.043*** (0.010) 288,118 0.818 70,412 YES YES YES Note: Standard errors are presented in parentheses. ***Statistically significant at the 1 percent level; **statistically significant at the 5 percent level; *statistically significant at the 10 percent level. following analysis, we use regression analysis to examine more rigorously the relationship between these characteristic variables and debt ratio. The explained variable TotLev in Table 1 is the debt ratio of each enterprise in the cur- rent year. We further control the debt ratio in the previous year (L. TotLev), based on the 25 Asian Economic Papers Chinese Corporate Debt and Credit Misallocation existence of the “optimal debt ratio” (Lev∗ t ) which is indicated by the trade-off theory. It means that if the previous year debt ratio (Levt−1) deviates from the optimal one, the en- terprises will adjust the actual debt ratio (Levt) to the optimal level in the current period, which is described by the following formula: Levt − Levt−1 = λ(Lev ∗ t − Levt−1) + εt. Here, λ is used to measure the speed of adjustment to the optimal level, depending on the characteristics of the enterprises and the macro situation (see Cook and Tang 2010). A more detailed explanation of this formula can be found in Flannery and Rangan (2006). The econometric model we use is the fixed-effect regression model. Because the debt ratio of the previous period is controlled, there may be a problem of first-order autocorrelation. However, Flannery and Rangan (2006) carefully examine various econometric models and then conclude that sequence-related problems are not serious (see p. 479), whereas it is nec- essary to control the firm fixed effect and the annual dummy variables. Therefore, we refer to their study as well as the follow-up ones (including Cook and Tang 2010), and use the ordinary fixed effect regression model. The number of firm fixed effects controlled by each regression is reported in the table; for example, a total of 328,727 different enterprises are included in the full-sample regression. It is worth noting that because we control the vari- able STDROA, the sample firms that are included in the regression should have existed for at least three consecutive years. We also control a set of dummy variables, including the annual ones (15 in total), (province × year) (465 in total), and (industry × year) (570 in total). Using these dummy variables and the firm fixed effects, not only do we control the effects of certain fixed characteristics of the enterprises (e.g., the ownership or political connections) on debt ratio, but also con- trol the regional factors that affect the adjustment of corporate debt ratio in each province every year (e.g., the overall credit situation of each province in the year), as well as the in- dustrial factors (e.g., the prosperity of each industry in the year). In addition, the set of (in- dustry × year) being controlled in the regressions equals to the average annual debt ratio of each industry being controlled. Frank and Goyal (2009) find that the average debt ratio of the industry has a reliable and stable explanatory power on the corporate debt ratio. By controlling these groups of dummy variables, we try to minimize various endogenous is- sues between enterprise characteristics and debt ratio. Firm characteristics are one-period- lagged to reduce the reverse causalities between these variables and the debt ratio. Because of the control of these firm characteristics and many dummy variables, the R2 of regres- sions are all above 80 percent. The results using the full sample are reported in column (1), and columns (2), (3), and (4) report the results using the sub-sample of state-owned, private, and overseas-funded 26 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation enterprises, respectively.21 Our findings are as follows: (1) The coefficient of L.TotLev is (1 − λ), which means that the adjustment speed of private enterprises (1 − 0.194) is higher than that of SOEs (1 − 0.365). (2) The variable of STDROA is the standard deviation of ROA over the past three years, which is significantly negative in both the full sample and private enterprises, whereas it is not significant in the sample of SOEs. (3) Size is measured by the logarithm of the total assets and significantly positive in the full sample and private enter- prises, while being negative in the sample of the SOEs (significance at the 10 percent level). (4) As for the proportion of tangible assets to the total assets, Tng is significantly positive in the full sample and private enterprises, but not significant in the sample of the SOEs. (5) Npr represents the sales profit margin and is negative in all sets of samples, while its magnitude in the sample of private enterprises is more than twice the effect in SOEs. In sum, in the private sector, the relationships between these four variables and the debt ratio are consistent with the findings in Western literature. The results in columns (1)–(4) indicate that the financing decisions in Chinese private enterprises are more in line with Western companies—in other words, more market-oriented. Nevertheless, only the result of the sales profit margin coincides with the Western empirical findings in the sample of Chinese SOEs. In addition to these four factors, we divide the sample into two groups according to whether the income tax payable of the enterprise is positive in the previous period. Thus, one group includes the enterprises with positive tax rate (i.e., Nonpositive = 0), and the other includes those with a negative rate (Nonpositive = 1). In the group with a positive tax rate, the variable of L.Tax that represents the tax rate in the previous period is negatively correlated with the debt ratio, and the negative effect in the sample of SOEs is even greater. In the other group, because the tax rate itself is non-positive and the estimated value of L.Tax is positive, the actual effect is also negative. Briefly stated, as for the Chinese enter- prises, the higher the income tax rate in the previous period, the lower the debt ratio in the latter period. This seems to indicate that Chinese industrial enterprises do not deliberately add liabilities to reduce taxation, which is contrary to the conclusions obtained from the ex- isting literature that examines China’s listed companies, including Huang and Song (2006) and Wu and Yue (2009). This issue is worth studying more carefully. Through this analysis, we draw a preliminary conclusion that the financing decisions of some enterprises, most of which are private enterprises, are in accordance with the prin- ciple of marketization. Meanwhile, the financing decisions of other enterprises that are mostly composed of SOEs contain many non-market factors. The financing behaviors of these enterprises lack the support from economic fundamentals. In other words, these 21 There is also a type of enterprise with mixed-ownership; because of the unclear ownership and space limitations, we do not report the relative results. 27 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 1 8 1 1 1 6 8 7 2 8 6 a s e p _ a _ 0 0 6 5 2 p d . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 Chinese Corporate Debt and Credit Misallocation Figure 20. SOEs: With heavy interest burden Source: CSMAR and authors’ calculation. firms have borrowed too much, which is not an ideal position for them because it also car- ries a high interest burden. We have also examined Chinese listed companies to provide further evidence supporting our conclusions. According to our calculations, in 2015 there were more than 160 listed SOEs that did not have enough profit to cover their interest expenses (see Figure 20). What is worse, these enterprises had to borrow more to repay the capital and interest; as a result, more and more debt is accumulated. We found that from 2010 to 2015, the total liabilities of these 160 enterprises rose from RMB 980 billion (US$ 144.77 billion) to RMB 1.68 tril-

lion (US$ 0.27 trillion). In other words, the 160 deficit enterprises have borrowed RMB 700 billion (US$ 0.13 trillion) additional debts during the six years. This also means the debt

ratio of these enterprises is so high that it finally leads to heavy burdens of interest. Note-

worthy is that our estimates are consistent with the estimates made in 2016 by Wang and

Zhong,22 that the proportion of non-financial companies listed in the main board that had

lower EBITs than interest expenses was 11.7 percent in the first half of 2015. This means

that about 160 to 200 large Chinese listed firms, most of which are state-owned, did not

have enough profits to pay their interest.

22 Tao Wang and Jennifer Zhong, “What Are the Real Problems with China’s Debt?,” UBS Global

Research, April 2016.

28

Asian Economic Papers

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Chinese Corporate Debt and Credit Misallocation

Figure 21. The average debt ratio: State-owned vs. private enterprises

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

e

d

u

a

s

e

p

a

r

t

i

c

e

–

p

d

/

l

f

/

/

/

/

/

1

8

1

1

1

6

8

7

2

8

6

a

s

e

p

_

a

_

0

0

6

5

2

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Source: The National Bureau of Statistics.

4. Is the leverage supported by economic fundamentals? Evidence from

aggregate-level data

In this section, we provide more evidence regarding who should be deleveraging and who

should be leveraged. As shown in Figure 21, the state-owned sector as a whole has con-

tinuously increased its leverage after 2008, as its average debt ratio rose from 59 percent

in 2008 to 62 percent until 2016. Moreover, the total debt of the state-owned sector has still

been rising. According to the data released by the Ministry of Finance, by November 2017,

the total liabilities of the Chinese state-owned sector have reached RMB 100 trillion (US$ 15.14 trillion). Among them, the total liabilities of the central SOEs were RMB 51.5 trillion (US$ 7.80 trillion), which have soared by nearly 9.6 percent compared with a year ago;