CAPITALIZATION OF CHARTER SCHOOLS

INTO RESIDENTIAL PROPERTY VALUES

Abstract

Although prior research has found clear impacts of schools and

school quality on property values, little is known about whether

charter schools have similar effects. Using sale price data for

residential properties in Los Angeles County from 2008 to 2011

we estimate the neighborhood level impact of charter schools

on housing prices. Using an identification strategy that relies

on census-block fixed effects and variation in charter penetration

over time, we find little evidence that the availability of a charter

school affects housing prices on average. We do find, however,

that when restricting to districts other than Los Angeles Unified

and counting only charter schools located in the same school

district as the household, housing prices fall in response to an

increase in nearby charter penetration.

Margaret Brehm

Department of Economics

Michigan State University

East Lansing, MI 48824

orourk49@msu.edu

Scott A. Imberman

(corresponding author)

Department of Economics

Michigan State University

and NBER

East Lansing, MI 48824

imberman@msu.edu

Michael Naretta

Department of Economics

Michigan State University

East Lansing, MI 48824

manaretta@gmail.com

doi:10.1162/EDFP_a_00192

C(cid:2) 2017 Association for Education Finance and Policy

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

1

Capitalization of Charter Schools

I N T R O D U C T I O N

1 .

The charter school movement began about twenty years ago and was driven by the

belief that privately run and publicly financed schools could be superior to traditional

public schools. Proponents argue that charters can adapt more smoothly in times

of financial hardship than traditional schools (e.g., by reducing nonunionized labor

force or changing administrative policies). They also argue that charters are leaders

in methodological innovations in education. On the other hand, opponents argue that

charters are able to restrict admission to make them look better than they are and

they divert necessary resources from public schools. Existing research has generally

shown charter effectiveness to be mixed (e.g., Bettinger 2005; Bifulco and Ladd 2006;

Sass 2006; Hoxby and Murarka 2009; Abdulkadiro˘glu et al. 2011; Dobbie and Fryer

2011; Imberman 2011b; Angrist et al. 2012; Angrist, Pathak, and Walters 2013), yet

the impacts of these schools on the wider economy is not well known. In this paper,

using data from Los Angeles County (LA County), California, we attempt to establish

the extent to which charter schools impact residential property markets by examining

how charter penetration rates in a community are capitalized into surrounding home

prices. Understanding whether housing markets are responsive to charter availability

is important given the increasing prevalence of charter schools across the country.

Indeed, California has seen significant growth in the number of charter schools since

they were authorized in 1992; the overall number of charters has increased from 299

in 2000 to 912 in 2010, with 242 of those in LA County alone. This is the highest

number of charter schools in any county in the United States.1

There is also a substantial literature relating housing values and school characteris-

tics (e.g., Black 1999; Gibbons and Machin 2003; Figlio and Lucas 2004; Kane, Riegg,

and Staiger 2006; Bayer, Ferreira, and McMillan 2007; Gibbons, Machin, and Silva

2013; Imberman and Lovenheim 2016), but only Buerger (2014), in an unpublished

working paper, specifically considers homeowners’ valuation of charter schools. To

identify the impact of charters on housing prices, we use data on single-family home

sales from 2008 to 2011, obtained from the LA County Assessor’s Office. We estimate

the impacts of both the number of charters and the share of public enrollment in char-

ters within various distances of a property, up to 2 miles. To account for endogenous

charter locations and changes in the geographic distribution of sales we include census-

block2 fixed effects along with a set of housing and school characteristics to account

for the nonrandom location of charter schools. Month-by-year fixed-effects account for

any general changes to the education and housing markets over time in LA County.3

Thus, our identification comes from houses sold in the same census block at different

times as charters open, close, expand, and shrink. As a result, we note that our study

does not identify how existing charter enrollment affects housing prices but rather how

contemporaneous changes in charter enrollment and the number of charters affect

housing prices in localized areas, specifically within census blocks.

1. See California Charter Schools Association Web site at www.ccsa.org/.

2. Census blocks are the smallest geographic area used by the U.S. Census Bureau and typically cover a single

city block in urban areas.

3. We acknowledge, nonetheless, that because we do not have neighborhood controls that vary over time, our

model does not account for changes in neighborhoods independent of changes in local schools that may affect

charter penetration. We discuss this issue in more detail in section 6.

2

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

/

f

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

Overall, our results suggest that neither the increase in the number of char-

ter schools nor the expansion in charter enrollment relative to public school

enrollment—our proxy for the availability of charter school slots to local residents—is

capitalized into housing prices on average. This holds both for Los Angeles Unified

School District (LAUSD) and other parts of LA County. It also holds for both startup

charters (new schools that begin as charters) and conversion charters (public schools

that convert to charter status), though we caution that very few schools convert dur-

ing our sample period. Further, we find no evidence that capitalization varies with

income level, minority population, or achievement levels of the local public elementary

school.

We do find, however, that when we count charters located only within the house-

hold’s school district’s boundaries and exclude LAUSD there is a significant negative

effect of additional nearby charter schools on housing prices. This restriction is rea-

sonable as students who reside within the charter’s authorizing school district (which

is almost always the district in which they are located) have admissions priority, thus

generating a link between these schooling options and local district boundaries. A po-

tential explanation for this finding is that opening a nearby charter school reduces the

value of a local community school, thus weakening the link between the availability of

local schooling as a public good and house prices.

2 . C H A R T E R S C H O O L S B A C K G R O U N D

Charter schools are public schools that are tuition-free and managed by an independent

operator. Typically, they are open to any student wishing to attend, regardless of where

they live, though some schools give preference to students who reside nearby. Many

schools require an application, and those in high demand will often have a waitlist.

Charters are typically governed by parents, teachers, members of the local community,

or a private company, and are reviewed for renewal every few years by an authorizer,

usually the state or a local school district. In California, charters are funded through

a mix of block grants and a state-based funding formula that provides funding at the

same per-pupil rate to all charters of a given grade level across the state (see CDE 2016).

There is substantial heterogeneity across schools in the way they are managed, their

goals, their targeted student population, and level of autonomy from the local school

system.

An important distinction to recognize among charter schools is they are either

brand new schools (startup charters) or were previously a traditional public school that

switched to a charter model (conversion charter). According to the California Charter

Schools Association, there are many reasons why traditional schools decide to convert

to charter status, but above all is the appeal of increased flexibility and autonomy.

Conversion charters must satisfy the same legal requirements and processes as startup

charter schools. This involves submitting a charter petition establishing features, such

as the school’s goals, finances, and governance plan, as well as obtaining signatures

of at least 50 percent of the permanent teachers currently employed at the school.

California law does require that conversions give priority to students in the school’s

district, and many districts (including LAUSD), give priority to students in a local

catchment area. Typically, startup charters do not have catchment areas, but if they

are oversubscribed they are also required to give priority to students who reside in the

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

3

Capitalization of Charter Schools

authorizing school district and may choose to give priority to those in the local school

zone if the neighborhood school has high rates of economic disadvantage.

As of the 2010–11 school year, conversion charters represented 16 percent of Califor-

nia’s charter schools, enrolling about 25 percent of all charter school students (CCSA

2012). Charter school facilities vary with type of charter, with some building brand new

structures, renting available spaces in churches, community centers, or commercial

buildings, or occupying a previously traditionally run public school campus.4 When a

school converts to charter status, it usually remains in the same building and retains

teachers, staff, and students. In contrast, startup charters need to recruit a student body

because parents have the option to enroll their child in the charter or in the assigned

public school.

Another important distinction between types of charter schools that has drawn

interest recently is the role of larger charter management organizations (CMOs). CMOs

are nonprofits that operate multiple charter schools and charters within an organization

and are able to pool management and resources in order to gain economies of scale—a

benefit often shared by schools within a traditional public school district. Evidence of

the impacts of these types of charters on student outcomes suggests that effectiveness

varies substantially across CMOs and students (Angrist et al. 2012; Furgeson et al. 2012).

Another heterogeneous distinction between charter schools is whether a charter has

a waiting list. Recent work using oversubscription lotteries has indicated that waitlist

charters perform better than local public schools but are unable to assess the impacts

of non-waitlist charters (Hoxby and Murarka 2009; Abdulkadiro˘glu et al. 2011; Dobbie

and Fryer 2011; Angrist et al. 2012; Angrist, Pathak, and Walters 2013). Unfortunately,

although it would be interesting to see whether housing prices respond differently to

these two ways charters vary, we do not have data on whether charters are operated by

CMOs or have waitlists.

3 . T H E O R Y O F C H A R T E R I M P A C T S O N H O U S I N G P R I C E S

The theory behind the relationship between housing prices and local school quality pre-

dicts that, because of the close link between residential location and the school attended

via attendance zones, higher quality schooling will generally lead to an increase in hous-

ing prices, though the extent of this increase depends on a number of factors (Rosen

1974; Black and Machin 2011). This relationship has been well established through em-

pirical analyses (Black 1999; Downes and Zabel 2002; Figlio and Lucas 2004; Kane,

Riegg, and Staiger 2006; Bayer, Ferreira, and McMillan 2007; Gibbons, Machin, and

Silva 2013). Because charter schools do not typically have attendance zones and be-

cause typically students may attend a charter regardless of their location of residence,

the theoretical link between charter schools and housing prices is ambiguous.

Despite a less obvious link between charter schools and housing prices, economic

theory suggests homeowners may respond to charters in a neighborhood for a few

reasons. First, charters provide an option value. Even if a child does not attend a charter

school, the availability of charters nearby may make a location more attractive for

parents. Charters rarely offer busing, therefore travel distance is especially important if

transport costs are expensive, as is the case in LA County where there is limited public

4. See California Charter Schools Association’s Web site at www.ccsa.org/.

4

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

transportation, heavy traffic congestion, and high gas prices. Further, as previously

mentioned, in California oversubscribed charters give priority to students who reside

in the school district containing the charter, and this could increase the option value to

living in the district.

Second, charters may have an indirect effect on housing prices if they affect the

performance of local public schools. Evidence on how charters affect local public schools

is mixed. Whereas Booker et al. (2008), Bifulco and Ladd (2006), and Sass (2006) find

positive effects of charters on nearby public schools, Imberman (2011a) finds negative

effects. Thus it is unclear how this mechanism might influence housing prices.

Third, the public may value the direct infrastructure and community improvements

charters sometimes provide. Indeed, Cellini, Ferreira, and Rothstein (2010) show that

housing prices respond to non-charter public school facility investments. Many charters

rent or use donated space, whereas some build their own facilities or convert abandoned

properties for use as schools. Even those that rent will often fill up vacant properties

in locations like strip malls (Imberman 2011a). Thus, the additional economic activity

generated by the charters may influence local housing prices.

Another theory is that charter schools may serve to break the connection between

local public schools and housing prices. In so doing we might expect additional char-

ters (and more school choice options more broadly) to lead to increased housing

prices where existing schools are low-performing because these locations would have

artificially low housing values due to the poor school quality. Alternatively, in high-

performing areas, additional charters may actually reduce housing prices as the avail-

ability of nearby charters weakens a key benefit of being zoned to a high-performing

school if, through attending charters, high-quality schools become available to house-

holds outside the attendance zone (Nechyba 2003). Another possibility, however, is that

by severing this link, the availability of having a public school option at all, irrespective

of school quality, is less valuable. The public good of a local school provides less utility

and, thus, without a commensurate reduction in property taxes, lowers the value of

residing near that school.

These theories indicate that it is unclear how charter schools may affect housing

prices because some economic effects may be positive and some may be negative.

As such, understanding the overall effect on local property markets is necessarily an

empirical question. We should also note that although it may be tempting to interpret

housing price responses as measures of how much people value charters, the complexity

of the underlying processes makes it difficult to do this. In fact, the theories described

above of how charter schools may sever the link between local public schools and

property values highlight that the effects could be showing something entirely different

from valuation.

4 . P R E V I O U S L I T E R A T U R E

Most of the existing literature on charter schools focuses on the effect of charters

on student achievement. Early research relying on panel data methods found mixed

results, with some researchers finding insignificant or significant negative impacts on

student test scores of attending a charter school (Bifulco and Ladd 2006; Sass 2006;

Zimmer and Buddin 2006; Hanushek et al. 2007; Imberman 2011b), and others

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

5

Capitalization of Charter Schools

finding positive impacts (Hoxby and Rockoff 2004; Booker et al. 2008). More recent

research using random lotteries (Hoxby and Murarka 2009; Abdulkadiro˘glu et al.

2011; Dobbie and Fryer 2011; Angrist et al. 2012; Angrist, Pathak, and Walters 2013)

and natural experiments (Abdulkadiro˘glu et al. 2014) have found large positive effects.

Some research has also recognized the distinction between conversion and startup

charters and suggests there is a differential impact on performance across the two

types (Buddin and Zimmer 2005; Sass 2006; Zimmer and Buddin 2009).

There are two studies in particular that are similar to ours. First, Chakrabarti and

Roy (2010) try to use the impact of charter schools on enrollment in private schools

as a proxy for how much parents prefer charters to other schooling options. They find

modest declines in private school enrollment when charters locate nearby. Second, in

an unpublished working paper Buerger (2014) looks at differences in housing prices

across school districts in New York due to charter penetration and finds positive effects.

His identification relies on differences in charter penetration across school districts and

census-tract fixed effects.

Nonetheless, our paper is distinct from Buerger’s in a few key ways. First, the focus

on differences across districts, although useful in areas with many school districts,

is less relevant to areas like Los Angeles that are dominated by a large central core

district. Indeed, most charter schools tend to locate in urban core areas dominated

by large urban districts. Thus, our analysis allows for identification of charter impacts

within these urbanized areas. Second, Buerger looks at the impacts on housing prices

from the entry of the first charter school into the district. In our analysis, we look

at capitalization of marginal changes in charter penetration using multiple charter

penetration measures. Third, our inclusion of census-block fixed effects instead of the

geographically larger census-tract fixed effects allows us to account for more potential

sources of time-invariant unobserved characteristics.

A separate branch of literature focuses on the relationship between housing prices

and school characteristics. There is ample evidence from previous work that housing

prices are responsive to test score differences across schools.5 Both Black (1999) and

Bayer, Ferreira, and McMillan (2007) estimate regression discontinuity models across

school zone boundaries to identify how school-average test scores are capitalized into

housing prices. Figlio and Lucas (2004) examine the effect of the release of “school

report card” data in Florida on property values. These report cards rated schools from A

to F based on average performance on statewide exams. All three studies find sizable,

positive impacts of higher school test scores on home values, suggesting parents place

significant value on this school-quality measure. Gibbons, Machin, and Silva (2013)

find similar results in England using boundary discontinuities using test score gains.

On the other hand, Imberman and Lovenheim (2016) find little impact of the release

of teacher and school value-added information on housing prices in Los Angeles.

Several studies have considered the effects of other school characteristics, such as

student demographics, per-pupil spending, and pupil-teacher ratio, on housing prices.

In the footsteps of Oates’ (1969) seminal paper, which uses per-pupil spending and

pupil-teacher ratio as measures of school quality, much of this research has found posi-

tive relationships between similar measures and housing prices (Bogart and Cromwell

5. For a comprehensive review see Black and Machin (2011).

6

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

1997; Bradbury, Mayer, and Case 2001; Weimer and Wolkoff 2001). Clapp, Nanda,

and Ross (2008), using panel data from Connecticut, find that an increase in the per-

centage of Hispanic students has a negative effect on housing prices. Using data from

Chicago, Downes and Zabel (2002) find that households do not capitalize per-pupil

expenditures.

Bogart and Cromwell (2000) exploit school redistricting in Ohio and find that

disruption of neighborhood schools—in terms of student demographics, changes in

transportation services, and geographic location within the neighborhood—reduces

house values by nearly 10 percent. Reback (2005) analyzes the effect of adoption of

a public school choice program in Minnesota to estimate the capitalization effects

related to changes in school district revenues, because districts’ state revenues depend

on enrollment. He finds that a 1 percentage point increase in outgoing transfer rates is

associated with an increase in house prices of about 1.7 percent.

Our analysis builds off the approaches of these studies by estimating the impact

of charter schools on local housing prices while carefully accounting for selection of

charters into neighborhoods. In particular, our baseline specification includes census-

block fixed effects to account for unobserved heterogeneity across local neighborhoods

in the propensity for charters to open or close nearby.

5 . D A T A

Our home price data come from the Los Angeles County Assessor’s Office (LACAO).

The data contain the most recent sale price of every home in LA County as of Octo-

ber 2011. In addition to LAUSD, the second largest district in the country, the data

encompass 75 other school districts. Because our data are based on most recent sales,

to avoid endogenous selection into the sample and small sample sizes in early years,

we restrict our data to include only residential sales that occurred between 1 September

2008 and 30 September 2011. From LACAO, we also obtained parcel-specific property

maps, which we overlay with school zone maps from 2002 (the most recent year such

data are available for the whole county).6 The data also include home and property

characteristics, such as the number of bedrooms, the number of bathrooms, units on

the property, square footage, and the year the structure was built.

We drop all properties with sale prices above $1.5 million in order to avoid results being driven by home-price outliers. Further, about 25 percent of the residential prop- erties in the dataset do not have a sale price listed. Usually, these are property transfers between relatives or inheritances. Hence, we limit our sample to those sales that have “document reason codes” of “A,” which denotes that it is a “good transfer” of property. We also drop all properties with more than either eight bedrooms or eight bathrooms. The charter school data are from the California Department of Education. We rely on two measures of charter school penetration: the counts of the number of charter schools within a specified distance from a home and the percentage of total enrollment in the public sector attributable to charter schools within a specified distance from a home. For the former measure, we calculate the distance between each charter and 6. The 2002 LA County maps come from the Los Angeles County GIS portal at http://egis3.lacounty .gov/dataportal/. The maps were created using a variety of sources and thus may not match precisely to actual school zones. l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / / f e d u e d p a r t i c e – p d l f / / / / / 1 2 1 1 1 6 9 1 0 9 5 e d p _ a _ 0 0 1 9 2 p d . f f b y g u e s t t o n 0 8 S e p e m b e r 2 0 2 3 7 Capitalization of Charter Schools Table 1. Schools in LA County Panel A. Schools by Grade Level Elementary Middle High Multiple Levels Non-charter public schools Total charter schools % charter schools Conversion charters Startup charters 1,196 113 8.6 21 92 243 390 48 16.5 1 47 88 18.4 10 78 68 35 34.0 3 32 Panel B. Schools by Years of Operation Non-charter Public Conversion Startup % Charter Schools 1,743 1,758 1,777 1,809 19 23 24 26 127 147 181 213 7.7 8.8 10.3 11.7 2008 2009 2010 2011 Notes: Schools included in panel A are those open and active at any point September 2008 through September 2011. Data obtained from California Department of Education. the home, and count the number of charters falling within a specified distance. For the latter measure, we use enrollment figures for all public schools in LA County from the Common Core of Data, managed by the Institute of Education Sciences at the U.S. Department of Education. An explanation for why we choose these variables and our specified distances is provided in section 6. We combine these data with school-by-academic year data on Academic Perfor- mance Index (API) scores, API rank, school average racial composition, percent on free- and reduced-price lunch, percent disabled, percent gifted and talented, average parental education levels, and enrollment. The API score is California’s summary in- dex of school test score performance. These covariates, which are available through the California Department of Education, control for the differences in charter school penetration that are correlated with underlying demographic trends in each school. Our main analytic sample consists of 158,211 house sales occurring from September 2008 through September 2011. Of these, 65,170 are sales of homes zoned to an elemen- tary school in LAUSD and 93,041 are sales of homes zoned to an elementary school in another school district in LA County. Table 1 provides information on the types of charter and public schools that operate in LA County over our sample period. Panel A provides schools by grade level. Charters are more common for middle and high schools but still account for a substantial portion of elementary schools, at 9 percent. Conversion charters in particular are common for elementary schools but not middle and high schools. Panel B shows that over the time period of our study, the percent of schools that are charters grows from 7.7 percent in 2008 to 11.7 percent in 2011. Tables 2 and 3 provide sample means and standard deviations at the property level for several of the variables we include in our regressions. In table 2 we see that properties in LA County have an average sale price of $383,546 and tend to be of modest size, averaging

around three bedrooms, two bathrooms, and 1600 square feet. We also have a ranking

of the quality of the structures on the property, which will be useful for conducting

validity tests. The property is given a rating on a scale of 1 to 12.5 by LACAO assessors,

8

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

Table 2.

Sale Prices

Summary Statistics of Properties with

Property characteristics

Sale price, $ Number of bedrooms Number of bathrooms Square footage Quality Number of charters 0–0.5 miles 0.5–1 mile 1–1.5 miles 1.5–2 miles Charters as percentage of enrollment 0–0.5 miles 0.5–1 mile 1–1.5 miles 1.5–2 miles Observations 383,546 (247,685) 2.98 (1.05) 2.11 (0.92) 1,573 (718) 6.45 (1.25) 0.16 (0.54) 0.47 (1.11) 0.78 (1.59) 1.06 (2.04) 0.05 (0.18) 0.06 (0.15) 0.06 (0.13) 0.06 (0.12) 158,211 Notes: Summary statistics are means for sales from September 2008 through September 2011. Property sample excludes homes with a sale price exceeding $1.5 million, and a bedroom or bathroom count in

excess of eight. Homes are divided into the “LAUSD”

or “Rest of LA County” samples via the location of

the elementary school to which the property is zoned.

Standard deviations in parentheses.

where a rating of 12.5 is the highest assessed quality. Not surprisingly, the average

quality of a property in LA County is close to the midway point on this scale, at 6.45.

For charter penetration, the number of charters in each distance ring increases as we

go further out, primarily because of the larger amount of land area in larger distance

rings. When we look at charters as a percentage of total public school enrollments, the

rates are relatively constant across distance rings at 5 to 6 percent.

We note that our data cover some periods of abnormal rigidity in the Los Angeles

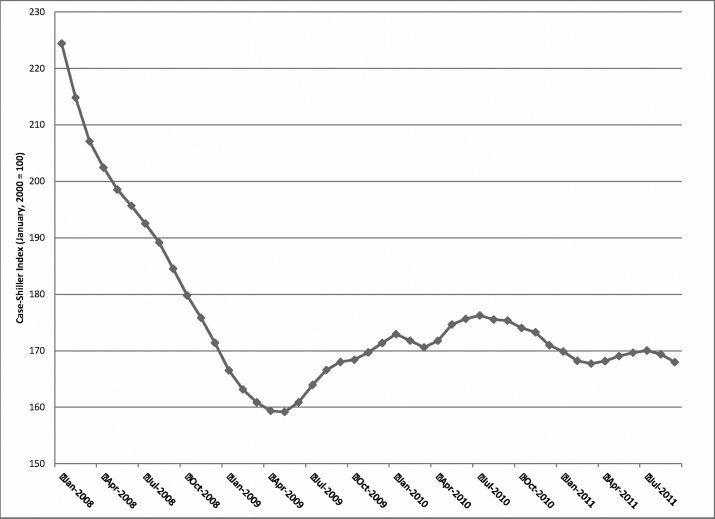

housing market due to the housing collapse of 2008 and the Great Recession. Figure 1

shows the Case-Shiller House Price Index for the Greater Los Angeles area from 2008

through 2011.7 Even though housing prices in Los Angeles fell dramatically until May

7. Acquired from http://us.spindices.com/indices/real-estate/sp-case-shiller-ca-los-angeles-home-price-index.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

/

f

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

9

Capitalization of Charter Schools

Table 3.

Summary Statistics: Schools Near Properties with Sale Prices

Panel A: Characteristics of Zoned

School

Panel B: Characteristics of Charters

Within 1 Mile (Enrollment Weighted)

Elementary

Middle

High

Elementary

Middle

High

440.5

(165.6)

805.6

(73.6)

10.9

(14.4)

58.2

(28.5)

7.1

(12.6)

11.4

(4.5)

8.4

(7.3)

64.7

(30.0)

28.1

(17.2)

158,211

1,197.4

(488.0)

746.1

(90.3)

10.1

(11.9)

62.9

(24.7)

7.0

(12.0)

11.4

(2.8)

13.8

(9.7)

66.9

(25.7)

19.8

(11.5)

127,558

2,002.6

(680.6)

707.0

(88.2)

11.2

(13.3)

60.1

(24.8)

7.6

(12.3)

10.3

(3.1)

11.4

(8.8)

55.9

(26.9)

18.0

(10.5)

141,212

443.0

(138.0)

800.1

(64.5)

10.6

(13.2)

62.0

(25.7)

7.2

(12.0)

11.8

(4.1)

7.5

(5.4)

68.7

(26.6)

30.3

(15.2)

136,546

1,121.3

(435.7)

744.7

(93.0)

10.3

(11.6)

63.6

(25.2)

7.7

(13.2)

11.1

(2.7)

12.6

(8.6)

67.5

(26.6)

20.2

(11.7)

81,204

1,140.5

(814.3)

663.7

(112.4)

11.1

(12.6)

65.2

(23.9)

5.9

(11.5)

10.6

(12.2)

7.3

(7.0)

61.2

(24.1)

20.8

(12.2)

83,079

158,211

127,174

140,866

136,536

80,686

80,979

Enrollment

API score

% Black

% Hispanic

% Asian

% Disabled

% Gifted

% Free or reduced price lunch

% English language learner

Observations

for API score:

Notes: Summary statistics are means for sales from September 2008 through September 2011. Sample excludes

homes with a sale price exceeding $1.5 million, and a bedroom or bathroom count in excess of eight. School

zones are based on 2002 zoning. See text for details on how to access school zone maps. Standard deviations

in parentheses.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Figure 1. Case-Shiller House Price Index for Greater Los Angeles.

10

Margaret Brehm, Scott A. Imberman, and Michael Naretta

2009, afterwards they had begun to rebound, increasing by 11 percent through July

2010. The prices fell slightly thereafter until the end of our data in September 2011.

Thus, the housing market had been in recovery for most of our sample period. Even

so, we may be worried that market rigidities would continue to limit capitalization.

To address this we provide results in a separate online appendix (accessible on Ed-

ucation Finance and Policy’s Web site at www.mitpressjournals.org/doi/suppl/10.1162

/EDFP_a_00192) that vary by year of sale and show that our estimates are similar to

baseline in later years of the sample when the market had more fully recovered.

In panel A of table 3 we provide information on the characteristics for the elemen-

tary, middle, and high schools to which each property is zoned. Panel B provides a

comparison with charters at each grade level within one mile of the property. For ele-

mentary and middle schools, the characteristics of charters are pretty similar to those

of the zoned school in terms of enrollment, API score, and demographics. For high

schools, however, there are some differences. Charter high schools tend to be substan-

tially smaller (1,140 students versus 2,002) but lower-performing as measured by API

score. Zoned and charter high schools are demographically similar, though high school

charters tend to have fewer gifted students.

6 . E M P I R I C A L S T R A T E G Y

Our identification strategy relies on variation across households and over time within

a census block in the number of charters within various distance radii. To achieve this,

in addition to controls for characteristics of the local elementary school and property

characteristics, we include census-block fixed effects along with month-of-sale fixed

effects. Including census-block fixed effects allows us to compare the sale prices of

properties that are geographically very close; the mean land area for census blocks in

LA County is 108,322 square feet with a median of 19,283 square feet. Although it

may be preferable to use repeated sales on the same property, this is not possible with

our data because we only have sale price information for the most recent sale. Even

if we did have repeated sales, given the short timeframe, restricting to those types of

households would create a selected sample since a disproportionate number of those

properties may be distressed, in fast changing neighborhoods, or houses that are often

“flipped.”

We believe that multiple sales within census blocks provide a reasonably small

geographic area to closely mimic repeated sales for specific properties while avoiding

the potential selection issues generated by using repeated sales. For example, in our

final estimation sample the median census block in LA County has three sales during

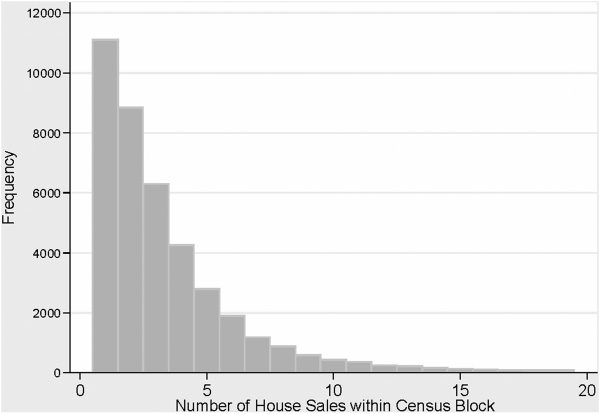

the study period with a mean of 3.9. Figure 2 provides a histogram of the distribution

of sales within census blocks, conditional on having any sales, over the study period.

While our econometric strategy identifies the effect of charter penetration only from

blocks with more than one sale, a substantial number of census blocks provide this

identification. There are 29,512 blocks with at least two sales and of those, 14,494 blocks

have at least four sales and 7,387 blocks have at least six sales. Further, of all blocks with

at least one sale, 73 percent have multiple sales, providing wide geographic variation

in blocks that contribute to identification. Finally, we conduct an analysis of variance

of property characteristics to assess the within- and between-census-block variance. In

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

11

Capitalization of Charter Schools

Figure 2. Distribution of House Sales by Census Block During Sample Period Conditional on Census Block Having any Sales.

our estimation sample, only 39 percent of the variance in house size and 20 percent of

the variance in housing quality are within a census block, along with less than half of

the variation in bedrooms and bathrooms.8 These results suggest that different houses

within a block have largely similar characteristics.

By including census-block fixed effects, our identification strategy assumes there are

no changes in neighborhood conditions over time that are correlated both with housing

prices and charter penetration. Of course, housing prices are increasing in general in

Los Angeles during our analysis period, as is the number of charter schools. Hence,

to account for general changes in house prices related to overall market conditions, we

include year-by-month indicators in all of our regression models.

Even with census-block fixed effect and year-by-month fixed effects, it is possible

that there are factors changing locally that could bias our estimates. Of primary concern

is the possibility that charters select into neighborhoods where the local public school is

under-performing and the poor quality of the school is reflected in lower housing prices.

Ideally, we would be able to at least control for changes in neighborhood characteristics

as we do for school characteristics and housing supply. Unfortunately, the data available

to us are very limited. To our knowledge, only the American Communities Survey (ACS)

provides neighborhood data at a small enough geographic level (e.g., census tract) to be

relevant for this analysis. The ACS only provides five-year estimates at the census-tract

level, however, because estimates based on smaller periods of time are too imprecise. As

a result, the ACS data do not provide temporal variation in neighborhood characteristics

over our three-year time period and any data on neighborhood characteristics would be

absorbed by the census-block fixed effects. Thus, we assume that selection of charter

location is unrelated to time-varying neighborhood characteristics that are themselves

not captured in our housing and school characteristics controls. We cannot test this

8. An analysis of variance using the residuals from regressions of the characteristics on month-by-year indicators

provides similar results.

12

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

assumption directly, but we do attempt to address it indirectly by testing whether our

observable measures of housing characteristics change when more charters move in,

and by testing whether charter penetration can be explained by prior changes in house

prices. If time-varying neighborhood characteristics are correlated with prior house

prices and the types of houses put on the market then we should expect to see some

impact on these observables, and indeed we do not find evidence for this. Nonetheless,

although we do not have temporal variation in neighborhood variables, we do have

such variation for local elementary school characteristics. Thus in table A.1 of the online

appendix, we look at how charter entry relates to public school characteristics when

we condition on school fixed effects. Without school fixed effects, the estimates show

that charters tend to locate in the zones of elementary schools with fewer minorities,

more gifted students, more English language learners, and more disabled students.

When school fixed effects are added some characteristics are statistically significant,

but importantly they are all economically small. The largest statistically significant

coefficient is on percent of black residents in the public school zone, but this coefficient

is still rather small. For a one charter increase in the school zone, there would need to

be a percent black student increase of 84 percentage points. Given this pattern and the

general shift in the coefficients toward zero as the school fixed effects are added, these

results suggest that lower levels of geographic fixed effects, specifically census-block

effects, should reduce these correlations further to the point where they are negligible.

Another difficulty in this analysis is deciding how to measure charter penetration.

There are two key factors here. First, there is the question of whether the important

factor is the existence of a charter school as a whole or the relative size of a charter

school. Arguably, whereas the former is the most visible aspect of the school to the wider

public (people in the neighborhood know that a school exists but may be uncertain as

to how large it is), the latter is a potentially better indicator of the supply constraints on

a family that wishes to send a child to the charter. The second issue is that it is unclear

how far from the charter a household must be before we can be confident the household

should not care about the charter’s existence. To deal with both of these issues we follow

the prior literature on the effects of charter schools on public schools (Bifulco and Ladd

2006; Sass 2006; Booker et al. 2008; Imberman 2011a). The analyses in these studies

estimate the effects of charter schools on traditional public schools within concentric

rings of various distances. Because it is not obvious whether what matters is relative

enrollment in charters or the number of charters, they estimate the effects of both

charter counts and enrollment in the charters as a share of total enrollment.

We use measures of charter penetration equal to (1) the number of charters and

(2) the share of all public school enrollments in charters in concentric rings between 0

and 0.5 miles, 0.5 and 1 mile, 1 and 1.5 miles, and 1.5 and 2 miles from a property. We

focus our attention on charters within relatively short distances of properties because

of the urbanicity and size of school zones in LA County. The mean elementary school

zone in LA County has an area of 3.2 square miles. With this area, if school zones were

circular, the radius of the average zone would be 1.0 mile. The median school zone has

an area of 0.8 square miles, translating into a radius of 0.5 miles. Hence, given the size

of school zones in LA County, these are reasonable distances within which to measure

the effect of charters. Indeed, in a large southwestern city that is less densely populated

than Los Angeles, Imberman (2011a) shows charters only impact enrollment of public

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

13

Capitalization of Charter Schools

schools within 2 miles of the charter. Further, in an analysis of charter applicants in

Boston, Walters (2014) finds that 40 percent of applicants apply to the closest charter

school and a further 22 percent apply to the second closest. Although we do not have

data on who actually applies to or attends charters, we note that in LA County the

median property is 1.35 miles from the nearest charter and the second closest charter

is 2.18 miles away. Because these measures include all properties, it is likely that the

average distances for charter attendees are substantially smaller. Based on these factors,

we believe 2 miles is a reasonable maximum distance, though we also report distances

between 2 and 5 miles in the online appendix.

Our baseline model estimates the impact of charter penetration on the log of the

sales price of property i in census block s at time t as

Ln(SalePriceist) = α + Charteritβ + Xit(cid:3) + Hi(cid:4) + λt + γs + εit,

(1)

where Charter is a vector of charter penetration variables calculated as the number

of charters or the share of public school enrollment in charters between 0 and 0.5

miles, 0.5 and 1 mile, 1 and 1.5 miles, and 1.5 and 2 miles from the property. The β

coefficients can be interpreted as jointly identifying a house price gradient that captures

the differential valuation of charter penetration by homeowners over distance. X is a

vector of school-by-year observables, where the school is the elementary school to which

the property is zoned. H is a vector of house-specific characteristics, such as the number

of bedrooms, the number of bathrooms, age, quality, and square footage. The model

also includes month-by-year fixed effects (λt) to control for common time trends and

census-block fixed effects (γ s) to control for time-invariant neighborhood quality and

quality of the locally zoned school.9 We cluster standard errors at the school-zone

level to account for correlation between prices of properties in the same census block.

An adjustment to this model also restricts to charter schools within school-district

boundaries. This is relevant because, as previously mentioned, California requires

oversubscribed charters to give admissions priority to within-district students.

We expand the baseline model to account for heterogeneous effects on housing

price by disaggregating our charter penetration variables by type of charter: conversion

or startup. In this model, the charter penetration vector is split into two:

Ln(Pist) = α + StartupCharterit

β1 + ConversionCharteritβ

2

+ Xit(cid:3) + Hi(cid:4) + λt + γs + εit.

(2)

In this setup, the β 1 coefficients will provide a gradient for startup charters and the

β

2 coefficients will provide a gradient for conversion charters. We include the same

controls as in equation 1. As mentioned earlier, we would expect to find differing

valuation of these two types of charters if homeowners place different weights on the

inputs of each type—conversion charters often remain in the same building, with

the same student body and staff, and adopting new operating styles, whereas startup

charters are often in rental spaces, tend to be smaller than conversions and traditional

9. The baseline model excludes school-zone fixed effects because most census blocks do not straddle school

zones. Nonetheless, inclusion of school-zone fixed effects has a negligible impact on the results.

14

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

Table 4.

Effect of Charters on Log Sale Prices for Los Angeles County

Los Angeles County

Number of Charters

Charter Seats as Percentage of Enrollment

(i)

(ii)

(iii)

(iv)

(v)

(vi)

A. Distance Gradient

0–0.5 miles

0.5–1 mile

1–1.5 miles

1.5–2 miles

B. Condensed 0–2 Miles

0–2 miles

−0.00725

(0.0131)

0.00858

(0.00748)

0.0252∗∗∗

(0.00578)

0.0239∗∗∗

(0.00494)

−0.0353∗∗∗

(0.00800)

−0.0253∗∗∗

(0.00609)

−0.0149∗∗∗

(0.00387)

−0.00460

(0.00309)

−0.00543

(0.00827)

0.000950

(0.00476)

0.00223

(0.00313)

−0.00110

(0.00279)

0.0741∗

(0.0438)

0.117∗∗

(0.0564)

0.140∗∗

(0.0616)

0.120

(0.0770)

0.00648

(0.0249)

−0.0166

(0.0270)

−0.0442∗

(0.0268)

−0.0217

(0.0340)

−0.00134

(0.0194)

−0.0128

(0.0195)

−0.0123

(0.0239)

−0.00470

(0.0255)

0.0193∗∗∗

(0.00321)

−0.0101∗∗∗

(0.00255)

−0.00010

(0.00207)

0.328∗∗∗

(0.112)

−0.0301

(0.0609)

−0.00750

(0.0544)

Observations

158,211

158,211

158,211

158,211

158,211

158,211

Housing characteristics

School characteristics

School fixed effects

Census-block fixed effects

Y

Y

N

N

Y

Y

Y

N

Y

Y

N

Y

Y

Y

N

N

Y

Y

Y

N

Y

Y

N

Y

Notes: Sample includes property sales from April 2009 through September 2011. The independent variable denotes either the

number of charters in operation or the share of enrollment in operating charters as of the sale date in various distance rings from

the property. Housing characteristics include number of bedrooms, bathrooms, square footage, and quality. School characteristics

include API levels overall, lags and second lags of overall API scores, percent of students of each race, percent free lunch,

percent gifted, percent English language learners, percent disabled, and parent education levels for elementary school zoned to

the property in 2002. All regressions include month-by-year fixed effects. Robust standard errors clustered by elementary school

zone in 2002 in parentheses.

∗Significant at the 10% level; ∗∗significant at the 5% level; ∗∗∗significant at the 1% level.

public schools, and need to recruit students and staff in addition to operating under a

new management style.10

7 . R E S U L T S

Effect of Charter Penetration on Housing Prices

Table 4 provides the baseline results of our analysis using variations of equation 1 and

the sample of homes sold across all of LA County. The table includes two panels, one

for each charter measure, overall numbers of charters, and percentage of total enroll-

ment attributed to charters. Each specification in the table includes month-by-year time

dummies, housing controls (square footage, number of bedrooms, number of bath-

rooms, and quality) and controls for the locally zoned elementary school (enrollment,

API score, school demographics, percentage disabled, gifted, free- or reduced-price

lunch eligible, and English language learners). All standard errors are clustered at the

school-zone level, where the school is the elementary school to which a property was

zoned in 2002.

10. The fact that conversions usually maintain the same attendance zone after converting suggests the potential

for using a difference-in-differences approach to assessing the impacts of these schools on housing prices.

Unfortunately, only five schools in LA County convert to charter status during our study period, making the

estimates from this type of analysis too imprecise.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

15

Capitalization of Charter Schools

In columns (i) and (iv), respectively, of table 4, we regress the log of the house

price on charter counts and the share of public school enrollment in charters within

half-mile diameter rings without geographic fixed effects. The estimates suggest there

is a positive relationship that strengthens as the distance from the property increases.

In columns (ii) and (v), we include elementary school-zone fixed effects to account

for characteristics of the locally zoned school. In these models the patterns differ

depending on how we measure charter penetration. When using charter counts, the

results indicate charters negatively impact housing prices, becoming more negative the

closer charters are to the property. The coefficient on the zero to half-mile radius charter

measure indicates that an additional charter is associated with a statistically significant

3.5 log point decrease in the sale price. When using enrollment share, however, only 1

to 1.5 miles is significant.

We may still be concerned that there are endogenous differences within school

zones, but across neighborhoods, that affect both housing prices and charter penetra-

tion. Thus, in columns (iii) and (vi) we provide our preferred estimates that replace

school-zone fixed effects with census-block fixed effects. In this model, estimates are

all statistically insignificant and small. The largest estimate in column (iii) suggests,

when taken at face value, an additional charter school increases housing prices between

1 and 1.5 miles away by 0.2 percent, with smaller values for other distances. For the

enrollment share measure, all of the values are negative, insignificant, and economi-

cally small with a 10 percentage point (pp) increase in charter share reducing housing

prices by less than 0.2 percent at all distance levels. To provide additional context, if we

focus on charter penetration within 0.5 miles of the property, the 95 percent confidence

interval for the impact of an additional charter is [–2%, 1%] and for a 10 pp increase in

charter enrollment share it is [0.4%, –0.4%].

One potentially important issue in interpreting the estimated effect of charter pen-

etration is that as the distance increases, the area in which the charter could locate

increases. This is not a substantial concern when focusing on share of enrollment

but it does indicate there may be more variation in the number of charters in farther

rings, making comparison of the estimated effects of charter penetration at different

distances difficult. To address this we also provide estimates using charter penetration

within the full 2-mile radius around the property in panel B. The results are similar to

those in panel A and show no impact of charters on housing prices when we include

census-block fixed effects. It is also interesting to note that the standard errors decrease

when we add census-block (or school) fixed effects. This is another indicator that there is

substantial identifying power within blocks and that including between-block variation

adds uninformative noise to the analysis.

Table 5 provides results for our preferred model that includes census-block fixed

effects when we split the sample by whether the properties are within the boundaries

of LAUSD, which is the largest district in LA County, or all other school districts in the

county. We may suspect that there are different property effects for the two samples

because LAUSD covers the main urban core of the county, and recent evidence suggests

urban charters are more effective than suburban charters (Angrist, Pathak, and Walters

2013). Our results, however, provide little evidence that house price effects vary via this

location difference. Only one estimate—for charter counts in LAUSD from 1 to 1.5

miles—is statistically significant.

16

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

/

f

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

Margaret Brehm, Scott A. Imberman, and Michael Naretta

Table 5.

Effect of Charters on Log Sale Prices for Los Angeles County by School District

LAUSD

Rest of LA County

Number

of

Charters

Charter Seats

as Percentage

of Enrollment

Number

of

Charters

Charter Seats

as Percentage

of Enrollment

0.000504

(0.00970)

0.00591

(0.00559)

0.00712∗∗

(0.00349)

0.00233

(0.00342)

65,170

0.83

Y

Y

N

Y

0.00923

(0.0236)

−0.00620

(0.0278)

−0.00607

(0.0314)

−0.0130

(0.0408)

65,170

0.83

Y

Y

N

Y

−0.0143

(0.0169)

−0.00447

(0.00869)

−0.00225

(0.00632)

−0.00375

(0.00470)

93,041

0.91

Y

Y

N

Y

−0.0220

(0.0373)

−0.0114

(0.0241)

0.000579

(0.0351)

0.0259

(0.0206)

93,041

0.91

Y

Y

N

Y

0–0.5 miles

0.5–1 mile

1–1.5 miles

1.5–2 miles

Observations

R2

Housing characteristics

School characteristics

School fixed-effects

Census-block fixed effects

Notes: See table 4 for a description of baseline sample and controls. Robust standard errors

clustered by elementary school zone in 2002 in parentheses.

∗∗Significant at the 5% level.

Table 6 provides the results for equation 2, splitting the charter penetration variable

by charter type (conversion and startup) for homes in all of LA County. As in our

regression split by school district, we focus on our preferred model with census-block

fixed effects, zoned elementary school controls, and housing controls. As in the pooled

model, none of the coefficients is statistically significant and the magnitudes and signs

of the estimates do not reveal a consistent relationship between charter counts or

charter enrollment rates and sale price for either charter type.

In table 7 we provide estimates that look at how charters affect house prices when

we restrict the charters included in the count and enrollment share variables to those

located in the same school district as the household. In California, within-district

students get priority for charter enrollment and so there may be a stronger link with

housing prices for these charters than those outside the district. Because LAUSD is

especially large with most properties located far from district boundaries, when we

estimate this model for LAUSD the estimates are little changed from baseline. Hence,

in table 7 we only provide estimates using the districts in LA County outside LAUSD.

These estimates are the only ones in this paper that provide a consistent indicator of

a charter impact on housing prices. Intriguingly, this estimated effect is negative. An

additional charter school within 2 miles reduces house prices by 1.9 percent and a 10 pp

increase in charter share of enrollment within 0.5 miles reduces prices by 1.2 percent.

This analysis provides some evidence that charters weaken the link between public

schools and housing prices.

We build on this analysis further by testing whether we see larger effects in areas

with higher quality schools. Tables A.2 and A.3 in the online appendix provide estimates,

respectively, that are allowed to differ by terciles of income and school API score

counting all charters, and counting only within-district charters. Although there are

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

f

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

17

Capitalization of Charter Schools

Table 6.

Effect of Charters on Log Sale Prices by Charter Type

Los Angeles County

Number of

Charters

Charter Seats as

Percentage of Enrollment

Startup charters

0–0.5 miles

0.5–1 mile

1–1.5 miles

1.5–2 miles

Conversion charters

0–0.5 miles

0.5–1 mile

1–1.5 miles

1.5–2 miles

Observations

R2

Housing characteristics

School characteristics

School fixed effects

Census-block fixed effects

−0.00450

(0.00952)

0.00253

(0.00537)

0.00341

(0.00357)

−0.00110

(0.00299)

−0.0137

(0.0133)

−0.0110

(0.0103)

−0.00664

(0.00854)

−0.00225

(0.00788)

158,211

0.881

Y

Y

N

Y

0.00389

(0.0226)

0.000917

(0.0241)

0.00269

(0.0240)

0.0273

(0.0234)

−0.0226

(0.0362)

−0.0432

(0.0311)

−0.0397

(0.0456)

−0.0506

(0.0513)

158,211

0.881

Y

Y

N

Y

Notes: See table 4 for a description of baseline sample and controls.

Robust standard errors clustered by elementary school zone in 2002

in parentheses.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

–

p

d

l

f

/

/

/

/

/

1

2

1

1

1

6

9

1

0

9

5

e

d

p

_

a

_

0

0

1

9

2

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

8

S

e

p

e

m

b

e

r

2

0

2

3

some marginally significant estimates in the low income schools in table A.3, overall

the evidence for a pattern across school types is weak. One possibility is that the district

quality is what matters. In table A.4 in the online appendix we investigate this by

extending the model in table 7 to allow for different estimates by tercile of district API

score. Here a clearer pattern emerges. In fact, the estimates suggest that there is a

small increase in property values for high-performing districts but a reduction for low-

performing districts. The relationship remains weak, however, with only one estimate

for bottom tercile schools significant at the 5 percent level. It is unclear why such a

pattern emerges but one possibility is that the low-achieving districts competing with

LAUSD, which is also low-performing (12th percentile API), benefit from a premium

over LAUSD that is weakened by charters. Or it could be the relationship between

housing prices and school quality is more sensitive to charters in low-performing

districts. Nonetheless, it is unclear to what extent this restriction to within-district

charters should matter. Although district students get priority, this is only relevant if

charters are oversubscribed. Hence, given the null results when we do not make this

restriction we think it is best to consider these estimates to be a bound on the potential

negative effect of charters.

18

Margaret Brehm, Scott A. Imberman, and Michael Naretta

Table 7.

Sale Prices for Los Angeles County, Excluding LAUSD

Effect of Charters Within the Home’s School District on Log

Panel A. Half-mile Increments

0–0.5 miles

0.5–1 mile

1–1.5 miles

1.5–2 miles

Number of

Charters

Charter Seats as

Percentage of Enrollment

−0.0387

(0.0284)

−0.0123

(0.0149)

−0.0178∗

(0.0098)

−0.0186

(0.0156)

−0.118∗∗∗

(0.0431)

−0.0786∗

(0.0409)

−0.0758∗

(0.0433)

−0.0670

(0.0541)

Panel B. Condensed 0–2 Miles

0–2 miles

−0.0192∗∗

(0.0090)

−0.0292

(0.1540)

Observations

93,041

93,041

Housing characteristics

School characteristics

School fixed effects

Census-block fixed effects

Y

Y

N

Y

Y

Y

N

Y

Notes: Sample includes property sales from April 2009 through Septem-