BANGLADESH:

THE IMPORTANCE

OF DIGITAL

TRAJECTORIES

NICHOLAS HUGHES

Bangladesh celebrates its 50th anniversary at a time of unprecedented change,

not least in the ways that mobile technology is enabling the delivery of services

to millions of people who have previously been hard to reach. In this paper, I

consider the rapid uptake and the impact of mobile money in Bangladesh and

examine the factors that have enabled this new sector to emerge. I also look

ahead, based on some observable trajectories of change (plus a little guess-

work), to how the next wave of digital finance will play out: will it allow new

business models to emerge, ones that can drive a more inclusive digital land-

scape with a greater positive impact on peoples’ livelihoods?

INTRODUCTION

My view of the world around us is shaped

by optimism; not blind optimism, espe-

cially given the damage caused by

COVID-19 across the globe, but an opti-

mism that stems from unequivocal trajec-

tories that are visible, quantifiable, and (I

think) powerful because they represent

tools we can use to be innovative in the

way we design and build many services. I

refer to the digital tools that are quite lit-

erally in our hands today.

I have enjoyed visiting Bangladesh

frequently over the last 12 years and have

seen firsthand the emergence of its

vibrant digital financial economy. The

lead mobile money service, bKash, has

more than 55 million registered accounts,

which makes it one of the biggest digital

financial services in the world. Some 10

million financial transactions take place

through bKash every day, with usage

reaching 1,300 transactions per second on

average during peak hours. A network of

some 270,000 agents supports the cus-

tomers and provides, among other things,

the points at which cash enters and leaves

their bKash wallets. Customers use their

bKash wallets for many things, from per-

son-to-person transfers, to purchasing

airtime for phones or paying utility bills,

to making payments for all manner of

64

innovations / Bangladesh at 50

Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023

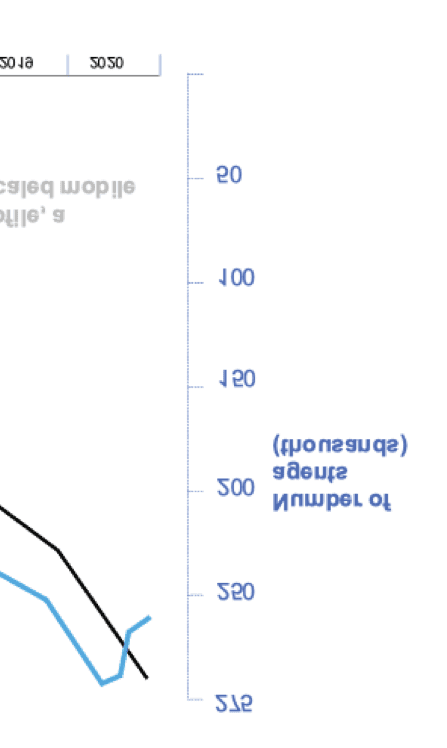

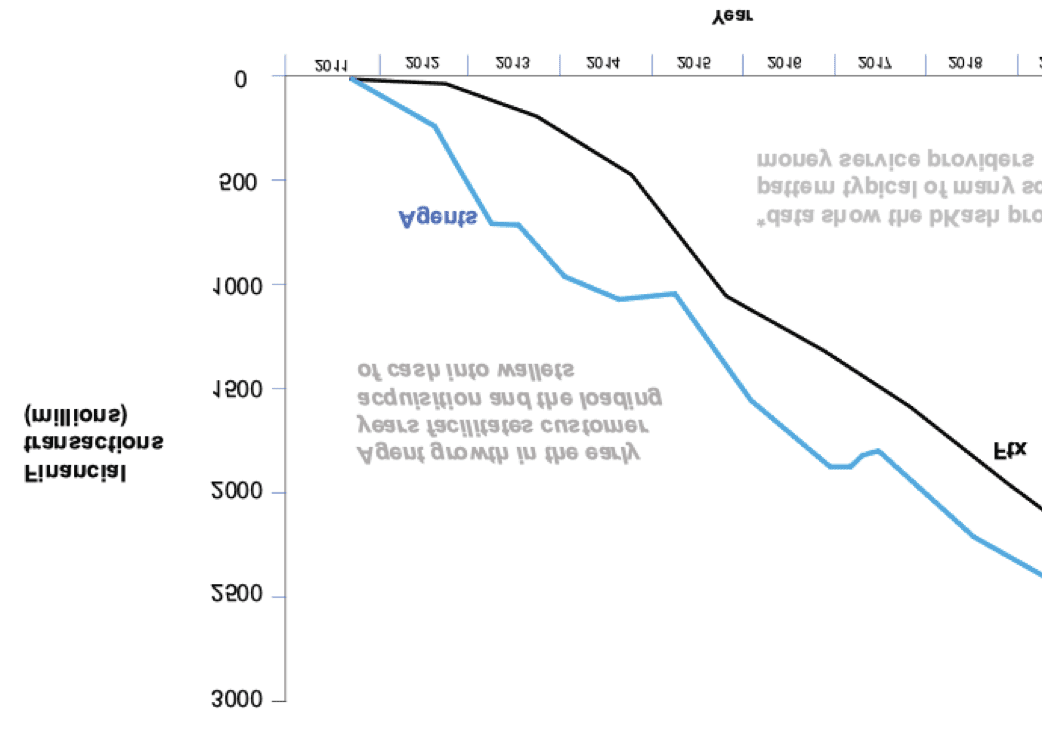

Figure 1. Mobile money growth trajectories: By financial transactions and number of

agents

goods and services at merchant locations.

Figure 1 depicts this remarkable growth

trajectory.

bKash is a bank-led model, with pri-

mary shareholder Brac Bank Limited pro-

viding the necessary regulatory compli-

ance. bKash works with all the mobile

network operators serving the country

and is integrated into a wide range of

financial institutions beyond Brac Bank.

While pioneered by bKash, the digital

financial sector in Bangladesh is increas-

ingly competitive. This new sector has

emerged because of factors that can be

looked at in two categories: external and

internal.

External: Economic, cultural, regula-

tory and technology factors have, in my

opinion, contributed to the supportive

framework that has enabled the digital

financial sector to emerge.

Internal:

I believe that some key

operational decisions made by the bKash

management team have helped the com-

ABOUT THE AUTHOR

Nicholas Hughes has been at the forefront of mobile commerce activities in emerging markets

for 20 years. He led the team that created M-PESA and he co-founded M-KOPA, which pioneered

pay-as-you-go digital asset financing. He currently leads a new B2B services company, 4R Digital

Ltd., which uses digital connectivity to unlock new business models. Nick holds a small number of

advisory roles, including being a board member of bKash. He has a PhD in Applied Science and

an MBA from London Business School. Nick was awarded an OBE in the Queen’s Birthday

Honours list for services to “innovation in Africa” in 2017.

© 2021 Nicholas Hughes

innovations / volume 13, number 1/2

65

Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023

Nicholas Hughes

pany emerge and grow into the mobile

money service we see today.

This is an exciting and fast-moving

sector; mobile money changes the way

consumers access and pay for services,

and it enables people to move from non-

consumers into full-fledged users of digi-

tal financial services.

It certainly hasn’t been an easy jour-

ney for bKash. Like all new enterprises, it

has demanded intense focus and dogged

determination to succeed. To adapt a

favorite quotation, bKash’s progress has

required unreasonable persistence (in the

best sense of the word) from the leader-

ship team.1. More bumps and twists no

doubt lie ahead on the path forward, but

the future will bring new innovations that

have been made possible by the digital

infrastructure that Bangladesh has today.

In the final section, I comment on a few of

these future opportunities.

First, some context for why trajecto-

ries matter, especially that of digital

finance. Indeed, the foundation of my

optimism comes from observing the rate

of change in this sector in the last ten

years. Few if any technologies throughout

history have seen the adoption rates we

have witnessed globally

for mobile

phones.

Nearly 20 years ago, my colleagues at

Vodafone (with heavyweight academic

support) squeezed out a small correlation

between mobile phone penetration (per-

centage of the population using phones)

and economic growth.2. Subsequent stud-

ies have taken this further to show, for

example, that a 10% increase in mobile

penetration increases total factor produc-

tivity in the long run by more than four

percentage points.3. A lot has happened in

the two decades since we did this early

work: there are now more mobile devices

than people on the planet; smartphones

are rapidly displacing feature phones in

most countries; 4G networks can now be

found in most urban areas; and network

access/usage is increasingly affordable.

And, of course, digital payments continue

to edge out cash in the real economy.

There is a long way to go before cash is

eliminated, but the GSMA now estimates

that some $2 billion move daily through mobile wallets, and more than a billion mobile money accounts were registered in 2019.4. Payments per se probably rank as one of the least interesting conversational top- ics for most people, despite the transfer of money being the lifeblood of economic progress since the demise of the barter system. Mobile payments, very simply, increase the velocity of money and make the transfer of value between two parties easier, safer, quicker, and (arguably) more affordable than cash when all factors are counted in. Of course, the ability to make a mobile payment is a prerequisite to pro- viding (or using) more sophisticated financial services, such as saving or lend- ing. It is easy to underestimate just how important payments are with respect to economic activity. Again, simply put, mobile money payments are an enabler of other activities; even if it’s a simple trans- fer of funds to someone else or the remote payment of a utility bill, someone, some- where in the value chain does something real with those funds in a time sequence that is much quicker and easier than if that transaction were done in cash. It is also hard to quantify the impor- tance of this, especially now that mobile telephony and digital payments are deeply embedded in day-to-day life—a fact that mitigates against rigorous quan- titative testing of “before and after.”5. Below, I provide a summary of work that has been done in Bangladesh and else- where to show the impact of mobile money on low-income households. These are data-based studies that confirm what is apparent in most people’s eyes: that digital payments can and do play a mate- 66 innovations / Bangladesh at 50 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Bangladesh: The Importance of Digital Trajectories rial role in shaping peoples’ livelihoods. Over the last 18 months, the restric- tions caused by COVID-19 have magni- fied the importance of digital services. This is especially apparent in Bangladesh, where the team at bKash integrated the digital service (technically) with more banks in 2020 than they had in the previ- ous eight years. This was born of necessi- ty, and of customers’ need to top-up their wallets from bank-to-wallet transactions, rather than through traditional over-the- counter cash transfers (done at agents, thus physically more difficult due to the lockdowns). This bigger network of digi- tally linked institutions will ultimately bring more benefits to digital wallet users because it increases the range of possible use cases and potential partners. So why has digital finance emerged so strongly in Bangladesh? Let me first address the external factors that have helped shape the foundation of the sector as it is today. EXTERNAL FACTORS THAT HAVE HELPED CREATE THE DIGITAL INFRASTRUCTURE Economy By any measure, Bangladesh today is very different from the country that won its independence 50 years ago. The country’s 164.7 million people make it the seventh most populous nation globally.6. Until the pandemic, the economy was growing at nearly 8% per year, one of the fastest growth rates in Asia.7. GDP growth in Bangladesh has been strong in recent years, relative to other countries in the region, reaching $2,401 per capita in mid-

2020.8. Life

in

expectancy

Bangladesh is three years more than in

India and well ahead of that in Pakistan,

Nepal, and Myanmar.9.

today

There is no doubt that the country’s

economic trajectory has been strong,

although admittedly it started from a low

baseline. This trajectory has been powered

by a garment industry riding the growth

in the global fashion sector, which,

together with agriculture, forms the

mainstay of the Bangladesh economy.

Unemployment in Bangladesh has

stayed relatively low, well under 5% for

much of the last five years. Notably, total

household consumption in Bangladesh, at

just over $200 billion, is higher than in countries like Vietnam and only slightly lower than in South Africa—in fact, it ranks 38th globally.10. Poverty rates have fallen from 44% in 1991 to around 18.1% in 2020.11. A final factor that has played a key role in the Bangladesh economy and will, I think, do so increasingly from a digital finance angle is the diaspora and the expatriates who remit many billions of dollars to their home country every year.12. Today, bKash helps facilitate the transfer of hundreds of millions of dollars in incoming remittances through its part- ner banks. These remittance flows have increased during COVID-19, and the numbers would be more significant if we took into account informal money-trans- fer channels. Needless to say, this pro- vides a stream of funds to drive consump- tion—and, potentially, investment in new enterprises. Culture Though hard to quantify, there is some- thing in Bangladeshi culture that is prac- tical, adaptive, and hardworking. Just think, Dhaka was the center of the Mughal empire for centuries before the advent of Western influences.13. Through the muslin fabric trade, it became one of the most prosperous cities in the 17th-cen- tury world. It is difficult to put my finger on this “something,” but I experienced a similar culture in Kenya, where I helped roll out M-PESA. It is characterized by people being entrepreneurial and practi- cal, and not afraid to take on new ways of innovations / volume 13, number 1/2 67 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Nicholas Hughes doing something when it can help them save money or make money. An interesting observation is that women today play a key role in the Bangladesh workforce. They made up some 36% in 2019, a higher proportion than in many other, more conservative course, Asian markets. And, of Bangladesh was the birthplace of micro- credit, an innovation designed for lower income consumers. Powerful nongovern- ment organizations, such as BRAC, have been more instrumental in Bangladesh than in any other markets in Asia in directing government and foreign income streams toward the neediest, and with good effect.14. These organizations have a great deal of reach, influence, and brand power, and their adoption of digital serv- ice models could be instrumental in con- tinuing the shift to a digital economy. Regulatory Factors Bangladesh Bank, the country’s central regulatory bank, has taken a careful, pro- gressive route to allow the emergence of mobile financial services to help drive financial inclusion. The mobile financial services regulations are measured, and they draw from best practices elsewhere to provide solid ground rules to protect consumers, mitigate systemic fraud, and ultimately allow the progression from cash toward an e-money economy. Followers of mobile money schemes will be well aware that those run by firms such as bKash do not create any new cur- rency; instead, they rigorously match e- money with real money in a float account and use digital identity and connectivity to create a secure messaging layer that moves ownership of e-money between the participants scheme. The Bangladesh Bank has been open to tack- ling head on some of the harder chal- lenges that confront scaling-up business models like bKash; a notable example is embracing digital biometric monitoring the in technology, which enables agents to com- plete the customer due diligence and ID processing necessary to open a new account. Work is ongoing on other elements of the digital ecosystem that should facili- tate further growth; notably, the deploy- ment of a centralized/unified switch, sim- ilar to the unified payment interface in India, that will enable all service providers to integrate more easily and, ultimately, to reduce the cost of moving e-money to end customers. adopted by More broadly, a forward-looking, long-term plan the Government of Bangladesh has digital services at its core.15. These services are central to its objective of moving the country to upper-middle-income status by 2031. Technology Factors At the market level, Bangladesh has seen a rapid uptake of digital services over the last ten years. This particular trajectory of change has been steep, and it is clear that the current digital infrastructure enables more and more services to be delivered across a wide range of verticals, from health to education to general e-com- merce. Building on the pioneering work of Grameen and Telenor in the 1990s, mobile networks now mean that mobile subscription penetration exceeds 100% of the adult population in Bangladesh. The Bangladesh Telecommunications Regulator Commission data indicate that there were 176 million mobile connec- tions in July 2021. Of these, an estimated 100 million were people accessing mobile internet services, where the use of social media is a proxy for internet usage. In a more traditional measure of internet sub- scribers, approximately 68% of the popu- lation can be counted in. Smartphones are increasingly afford- able and the primary channel for internet 68 innovations / Bangladesh at 50 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Bangladesh: The Importance of Digital Trajectories access. Smartphones now account for 40% penetration of the user base in Bangladesh, and usage is growing month- ly. Smart and semi-smart phones, such as the Kia-OS models available across Asia that start at around $10 for some models,

give consumers a user interface that

opens up accessibility to a wide range of

phone-based services. To a degree, this

has helped to tackle some of the chal-

lenges a lack of literacy brings to the

uptake of digital financial services.

Applications are easily designed and

deployed on these smartphone platforms,

which has spawned the development of a

host of consumer products and offers.

A recent report estimated that mobile

technology and services in Bangladesh

created economic value equivalent to

5.3% of the country’s GDP in 2019, which

today could amount to nearly $21 bil- lion.16. To sum up, there are strong external factors—economic, cultural, regulatory, and technological—that have created market conditions for the continued rise of digital services in Bangladesh. In the following section, I look at some strategic business choices that have been made by bKash to help establish the largest in- country mobile money service. INTERNAL BKASH FACTORS THAT MAKE THE PLATFORM SUCCESSFUL Deploying a mobile money platform across multiple carrier networks and inte- grating the platform directly with finan- cial-sector partners, utility companies, and a large number of merchants is not a simple exercise. Technology is only a frac- tion of the challenge. Success—or, per- haps more accurately, sustainable com- mercial success—comes from staying absolutely focused on the end customer and giving them a reliable and secure service. To achieve the required service level and build trust with customers, bKash has focused intently on the foundational parts of the business. Below I describe a few of the factors and operational issues that have contributed to making bKash both a strong brand and a leading employer. Distribution, Distribution, Distribution From day one of operations, bKash has had a dedicated focus on the creation of a highly efficient agent network. The com- pany took lessons from the practices of successful mobile network operators around the globe, such as deploying air- time top-up services through a vast net- work of informal sales people, supported by a hierarchy of retail distributors. These agents are the interface between cash and e-money. Without them, digital financial platforms will simply not function well in economies where cash is still important. Obvious as it seems, this is often a painful lesson for many would-be digital plat- form providers, who create wonderfully sophisticated platforms but forget how cash gets in or out of the system. bKash did not make this mistake. The team drove hard to build its network, and to train, incentivize, and support its agents to work with end customers in opening and topping up their bKash wal- lets, often referred to as cash-in/cash-out services. This meant designing and run- ning a large cash-collection network to ensure that agents had functioning e- money and real money floats to allow cash-in/cash-out to happen. Today bKash has a network of more than 270,000 agents. This provides a plat- form that can be leveraged further as the country moves toward a more active e- commerce-led economy, where well- functioning distribution networks will play an important role in bridging online innovations / volume 13, number 1/2 69 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Nicholas Hughes Box 1. A Typical Day for a CICO Agent A typical agent will start their day around eight o’clock in the morning, selling inexpensive, high- turnover items out of a small shop to customers on their way to work. On average, an agent may perform fifteen cash in/cash-out (CICO) transactions in any one day. Providing these mobile money services alongside their daily retail business offers them a signif- icant addition to their income. Agents will customarily have several regular customers for CICO services. Just before lunchtime, agents may experience a rush hour. However, the period during which the platform evidences the highest rate of transactions per second is in the evening, between 5pm and 9pm, when customers use it to make payments. Most agents with shops outside of business hubs in metro areas will take a short break during lunch, closing until the afternoon. During lock down, under COVID-19 curfews, hours of business were limited, but agents still provided the critical CICO service. They also supported customers in responding to queries— guiding them on how to use the service and helping to onboard new customers. Most bKash agents use a dedicated Agent App to do this work. The chart above, at right, shows a gradual increase over time in cash in versus cash-out transac- tions, both by volume (top) and transaction size (bottom). Such trends are typical of a maturing mobile money service as more funds are left in the wallet to be used in digital format to pay for the increasing number and variety of services linked to a platform. markets to the last-mile delivery of physi- cal products (see Box 1). The Importance of a Rolling Roadmap and Micro Services A second factor that has played a signifi- cant role in the bKash model, and will continue to keep the firm’s trajectory going the right way, is the fact that bKash has not sat back and rested on its basic person-to-person offer. Rather, the lead- ership team has been constantly design- ing, testing, and deploying more con- sumer digital services, building off the customers’ comfort with a basic mobile money offer. Over time, as new use cases are devel- oped and new services offered to cus- tomers, the revenue flowing into bKash has moved away from cash-in/cash-out commissions and toward higher margin, value-adding propositions. A greater level of customer segmentation is becoming apparent. For example, in the last two years, following Ant Group’s investment in bKash, the team has pushed hard to deliver bKash services through a well- designed user app. Of course, this 70 innovations / Bangladesh at 50 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Bangladesh: The Importance of Digital Trajectories requires the end customer to be a smart- phone user, who is typically younger and urban based, but the trajectory toward more and more affordable smartphones is clear, along with a downward trajectory in network access costs. While the pan- demic has made customers a little more cautious with their disposable income, over the next few years, increased smart- phone usage will begin to displace the more clunky USSD menu access model that provided the foundation for service in Bangladesh. The bKash technology team has con- trolled all key aspects of the digital value chain, relying on a robust, scalable core transaction platform that has been upgraded over several years to provide ample financial transaction capacity. There are several key external tech- nologies for which bKash has had to build high-performance integrations; notably, the network operator platforms and billing engines. More recently, the techni- cal trajectory bKash is following is deter- mined by the use of a micro-services deployment in which well-defined, sepa- rate functional blocks of technology are managed and developed efficiently; cloud-based services are deployed to manage data securely and facilitate prod- uct development; and application inter- face protocols provide the means by which new functionality can be added to the core infrastructure. All of this technology requires con- tinuous management and improvement to run internal and third-party commis- sioned security assessments, and to pro- vide 24-hour business continuity and dis- aster recovery facilities to ensure the integrity of the whole suite. Like all complex systems, there are challenges in achieving near 100% avail- ability. Without over-simplifying the solidity of this achievement, digital plat- forms like the one deployed by bKash provide a superb enabling layer for the continuous development of new products and services. This includes offering ever more places (merchants) where cus- tomers can spend their e-money through more sophisticated products, such as the nano loans bKash can offer through regu- lated partners. QUANTIFYING THE IMPACT As I mentioned in the introduction, quantifying the impact of mobile money is a difficult thing to do using the rearview mirror and extracting control data, given the rapid uptake of services within a com- pressed period of time. That said, an aca- demic-grade, randomized control trial- type experiment completed in Bangladesh in 2015 demonstrated some important effects on rural households that had from urban received migrants.17. remittances Urbanization has been a feature of development across much of Asia. Dhaka has effectively doubled in size over the last decade to become the fourth most densely populated city in the world, with an esti- mated population of 21.7 million. This growth rate has come not just from organic population increases but from migrants entering the city in search of higher paid work, typically the younger generation drawn to work in the garment industry. These migrant workers were able to send money back to their families in rural areas. The impact of these money trans- fers was manifold. First, households that received remittances were able to with- stand economic shocks, such as someone in the household falling ill, with more resilience. Monies were available for the family to seek medical advice and direct intervention, and so to deal with a health crisis in a more timely and beneficial way. Mobile money remittances also improved recipients’ resilience in dealing with agricultural shocks, such as sudden innovations / volume 13, number 1/2 71 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Nicholas Hughes price changes for inputs or outputs, or weather-related events. The study also showed that children in households that received mobile money payments studied for longer periods of time each week, probably due to a reduced need for them to help support the family by working in agriculture or doing other chores if/when a shock event occurred. This study indi- cates that receiving mobile money can help even out household consumption, which, at a micro level, has a positive eco- nomic effect on the family. The data underpinning this study show that bKash and services like it can be effective tools for alleviating poverty. This phenomenon was observed in Kenya as the mobile money system M-PESA rolled out to rural areas, where there was evidence of an especially marked positive impact on women in the household.18. One example is that around 180,000 women moved from subsistence-type farming to micro-retail and other forms of employment because of the liquidity mobile money transfers provided them. A LOOK FORWARD digital trajectories In this penultimate section, I come back to the reasons for my optimism about the observed in Bangladesh. The digital infrastructure in place there today provides an amazing opportunity to design more and more enhanced solutions to meet real needs in the market. Digital money platforms like that operated by bKash can drive oppor- tunities for new products. For example, bKash has been testing and refining a salary disbursement program for workers in the garment industry, where regular salary payments are made on behalf of the business owner to employees, who typi- cally are unbanked workers excluded from any sort of financial service. This certainly saves money and reduces the administrative burden for the garment business owners, but it also introduces new end customers to the benefits of a digital wallet. If a worker follows a normal pattern of usage, they may well cash out the first few salary payments at an agent for the “folding money.” But, as the employee gains trust in their digital wallet and realizes what other services can be availed, such as money transfers or the purchase of micro-insurance, they are likely to become a more active wallet user. To underline my thoughts on new opportunities, I would like to refer to a concept introduced by one of the greatest minds on innovation, the late Clayton Christensen. Famous for his work on the innovator’s dilemma, he also introduced the concept of market-creating innova- tion.19. This can be defined as a change in the process by which an organization transforms labor, capital, materials, and information into products and services of greater value. In my view, this is exactly what digital financial services offer us today. Because we can move a small amount of money around at a relatively low cost and across great distances, we have the opportunity to rethink the way value moves in exchange for products and services. I think bKash will increasingly be able to maximize value from the large net- work of agents it has created. These men and women, many of whom are keen to grow their businesses and further build their own livelihoods, exist today as part of a huge informal retail network. This informal retail sector will become more important as we witness the emergence of distributed e-commerce services. Done well, these agents can be collection points for all sorts of goods distributed from an online (digital-only) marketplace. I draw again from my earlier point about not for- getting the last mile: building an online marketplace is one thing, but making that work in the physical world is another. Connected distribution networks become 72 innovations / Bangladesh at 50 Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023 Bangladesh: The Importance of Digital Trajectories essential in a world of new distributed business models. Let me take one more example that is linked to international remittances, per- haps a more future-orientated example that builds on an increasingly connected global community. bKash today already facilitates the transfer of funds from the Middle East and other sending corridors into the wallets of men and women in Bangladesh. What is there to prevent these flows of digital funds from being used to pay directly for in-country servic- es, such as health care or education, with- out the need to move across fiat curren- cies, which always adds costs? This takes the urban-to-rural remittance that we have seen have a very real impact to an international level. We have the technolo- gy in place to democratize cross-border remittances and allow the sending side to see exactly where and how funds get allo- cated on the receiving side. Of course, regulations on international money flows exist for good reason. However, there is no technical barrier to this category of service that is so very relevant to Bangladesh, given the volume of remit- tances its citizens receive and their impor- tance to millions of people. FINAL THOUGHTS To sum up, the last 50 years have seen a great deal of change in Bangladesh. The next 50 are impossible to predict, given the rate of change experienced in just the last ten! We have seen positive change in the digital sector, as exemplified by organizations like bKash. My optimism is balanced by my knowledge that the sector is still in its infancy—or perhaps now its teenage years—and reaching its full potential will require more hard work and strong leadership. With a consistent set of ground rules and a level playing field for all operators, digital finance can underpin real economic growth. If we can harness the country’s current unprecedented trajectories, I am sure we will see sustain- able benefits for the people of Bangladesh, including better services, improved liveli- hoods, and a more inclusive society. 1. “The reasonable man adapts himself to the world: the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man.” George Bernard Shaw, Man and Superman. 2. Diane Coyle, The Impact of Telecoms on Economic Growth in Developing Markets, Vodafone Policy Paper Series No. 2, 2005. 3. GSMA, “What Is the Impact of Mobile Telephony on Economic Growth?” Deloitte, 2012. 4. “State of the Industry Report on Mobile Money (for 2019),” GSMA, 2020. 5. It’s a large topic, but a so-called digital productivity paradox exists; this may have more to do with how we measure productivity, given the complexity of defining measures that capture aspects of digital services. 6. See https://data.worldbank.org/indicator/SP.P OP.TOTL?locations=BD; https://bangladesh.unfpa.org/en/node/2431 4. 7.See https://www.economist.com/leaders/2021/0 3/27/bangladeshs-growth-has-been- remarkable-but-is-now-at-risk. 8. GDP at the end of June 2020 was $395.4

billion, and the population at the end of

that year was 164.7 million

(https://data.worldbank.org/).

9. “Life Expectancy at Birth, Total (years)-

Bangladesh” (worldbank.org).

10. The Economist Intelligence Unit, “Country

Report,” June 2021.

11. See

www.worldbank.org/en/country/banglades

h/overview#1.

12. The Economist Intelligence Unit estimates

this to be more than $20 billion in 2021.

innovations / volume 13, number 1/2

73

Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023

Nicholas Hughes

13. For a sobering read, see William

Dalrymple, The Anarchy: The Relentless

Rise of the East India Company,

Bloomsbury Publishing, 2019.

14. BRAC stands for the Bangladesh Rural

Advancement Committee.

15. “Making Vision 2041 a Reality: Perspective

Plan of Bangladesh,” Planning

Commission Government of the People’s

Republic of Bangladesh

(www.plancomm.gov.bd).

16. “Achieving Mobile-Enabled Digital

Inclusion in Bangladesh,” GSMA, March

2021.

17. J. N. Lee, J. Morduch, S. Ravindran, A. S.

Shonchoy, and H. Zaman, Poverty and

Migration in the Digital Age: Experimental

Evidence on Mobile Banking in Bangladesh,

International Growth Centre, 2017.

18. T. Suri and W. Jack, “The Long Run

Poverty and Gender Impacts of Mobile

Money,” Science 354 (2016): 1288-1292.

19. C. M. Christensen, E. Ojomo, and K.

Dillon, The Prosperity Paradox: How

Innovation Can Lift Nations Out of Poverty,

Harper Collins, 2019.

74

innovations / Bangladesh at 50

Downloaded from http://direct.mit.edu/itgg/article-pdf/13/1-2/64/1978750/inov_a_00283.pdf by guest on 07 September 2023