Anne Hastings, with James Kurz and Katleen Felix

A Bank the Poor Can Call

Their Own

Innovations Case Narrative:

Fonkoze

Most large institutions in Haiti locate their offices in the hills overlooking Port-au-

Prince, far away from civil strife and potential risk. Fonkoze has always chosen to

locate its central offices in the heart of the capital, most recently on Avenue

Christophe, just a few blocks from Champs de Mars, Port-au-Prince’s central park,

and the presidential palace. This vibrant area is where the city comes alive each day

with commerce, where hundreds of students pass on their way to the universities

and primary schools that line the street.

On the afternoon of January 12, 2010, most of Fonkoze’s leadership team was

gathered on the third floor at Avenue Christophe. We heard a low groan, and then

the full power of a 7.0 earthquake sent everything, including chunks of the ceiling

and walls, violently flying through the air, falling and crashing around us. The walls

of the building bent and split, pulverizing the concrete into a fine dust that filled

the room and made it impossible to see or breathe. Those who were not trapped

ran for the staircase and the lone exit from the building, tripping and falling into

the courtyard as the ground continued to sway beneath our feet. Five of Fonkoze’s

employees perished that day, including three from the transfer services depart-

ment, which would become one of the institution’s most important functions in

Anne Hastings is the CEO of Sèvis Finansye Fonkoze and was the Director of Fonkoze

from 1996 to 2009. She was recently named a Social Entrepreneur of the Year 2010 in

Latin America during the President’s Plenary session of the World Economic Forum

on Latin America.

James Kurz is a Senior Analyst for Fonkoze. As an advisor, he focuses on financial and

operational performance across all of Fonkoze’s programs and activities.

Katleen Felix is a Consultant Project Director and Diaspora Liaison for Fonkoze. She

works primarily on two projects for Fonkoze: Zafen (www.zafen.org) and Fonkoze

Prepaid Card. She has a special interest in migration and development and works

closely with Haitian Hometown Associations around the world to improve projects in

rural areas.

© 2010 Fonkoze

innovations / fall 2010

13

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

Anne Hastings, with James Kurz and Katleen Felix

the days after the quake. Ten branches had to be abandoned, and Fonkoze’s head-

quarters on Avenue Christophe was rendered uninhabitable.

And yet, while the large commercial banks closed their branches for up to two

weeks, 34 Fonkoze branches remained open in the days after the earthquake. They

were restocked with cash in 11 days so they could pay out to Fonkoze clients the

enormous flow of remittances coming from abroad—transfers of cash that provid-

ed immediate relief for the most vulnerable in the days just after the disaster.

Fonkoze, “the bank the poor can call their own,” was built in a country always

teetering on the edge. Founded in 1994 with two part-time employees, by 2010

Fonkoze had more than 750 employees, 45,000 loan clients, 200,000 savers, and a

national network of 41 branches, most of them rural. In keeping with its founder’s

edict—“You can’t simply give a woman a loan and walk away, you have to accom-

pany her on her journey out of poverty”—Fonkoze provides more than just loans.

It also sees access to reasonably priced savings, remittance transfer, and currency

conversion as a right of even the poorest, not just a privilege for customers with

large amounts of money. Fonkoze offers all of these services at each branch, at

some of Haiti’s most competitive rates. For example, its least expensive remittance

option costs just $6 per transfer for any amount of money up to $2,500, a price far

lower than any other money transfer operator. In addition to financial services for

the poor, Fonkoze provides programs ranging from preparation for microfinance

for the ultra poor, to micro-insurance, to health care and education.

This article tells the story of how—after the devastation of the 2010 earth-

quake—Fonkoze found itself positioned to serve Haiti’s rural population before

other banks were back on their feet. First I describe Fonkoze’s beginnings and dis-

cuss the many challenges facing Haiti’s poor. I then turn to Fonkoze’s core finan-

cial services, and to a number of trials Fonkoze faced during its growth. I describe

updates to the basic model in place by 2010, and conclude with Fonkoze’s response

to the earthquake while reflecting on its future path toward sustainability.

FONKOZE’S BEGINNINGS

In the early 1990s, Haiti was in the midst of a struggle for freedom and equality. Its

first democratically elected president was living in exile, and the country was ruled

by a brutal military regime. Members of the hundreds of grassroots organizations

that had worked tirelessly in the late 1980s and early 1990s to bring democracy to

Haiti had confidence that their president would soon be restored to power and the

military regime would depart. These people were targets of repression: at least

8,000 were killed during this time, and many more lived in hiding or in constant

fear of reprisal.

A group of grassroots leaders led by Father Joseph Philippe, a Spiritan priest

and founder of the Peasant Association of Fondwa, envisioned a Haiti where indi-

viduals were given a chance at both economic and political democracy.

Father Philippe recognized that while the majority of poor people in Haiti now

knew how to organize themselves politically, they knew nothing about how to

14

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

A Bank the Poor Can Call Their Own

organize themselves economically. Even though the people might control who was

president, they had no control over the economy. The poor lacked access to banks

and the financial services they needed to rebuild their lives and their country from

the ground up. Father Philippe saw that the strong grassroots movement organized

to bring about political change could also be harnessed to bring about economic

change on behalf of Haiti’s poor. He called them “the organized poor.”

An illiterate poor peasant or ti machann (a street or market vendor, usually a

woman) who had no collateral and made only small banking transactions was not

welcome in any of the commercial banks. Where would a coffee cooperative get

enough credit to buy and process coffee harvests for export? Where would a ti

machann get a small loan to buy her merchandise and increase the size of her busi-

ness? Where could the poor open a savings account and earn interest, receive

money transfers in a remote rural community from family in the U.S., or convert

money into Haitian currency at a reasonable rate?

In 1994, the founders of Fonkoze—some 32 grassroots leaders—drew up the

official papers to launch their efforts, and in 1995 Fonkoze (Fondasyon Kole Zepòl,

or the Shoulder-to-Shoulder Foundation) was officially recognized as a founda-

tion under Haitian law. Although the founders envisioned a business solution to

poverty, they established several principles that would ensure that profit would

never be the organization’s sole consideration: the movement would be national in

scope, it would reach the very poorest and empower them, and it would proceed

according to the concept that all people are entitled to a fair price for financial

services, no matter the size of their business or how remote their location.

At about the same time, I was applying for the Peace Corps in the U.S. I was an

experienced Washington, D.C., management consultant with a successful business,

but something was missing in my life and I felt the calling to give back after hav-

ing been so fortunate. I was accepted into the Peace Corps and assigned to an

African country, but a client of mine encouraged me to speak to the director of

International Operations at the Peace Corps before making a final commitment.

Once the director learned of my background he asked, “Do you have any interest

in Haiti?” I was very interested in Haiti, I said, but the Peace Corps wasn’t working

in Haiti at the time. He said, “Forget the Peace Corps . . . I know a priest in Haiti

who is doing amazing work.” He convinced me to send my resume to Father

Philippe. Three days later I received a message on my voice mail: “This is Father

Joseph Philippe. Thank you for your willingness to work with my people. Thank

you for your courage. You may be director of our new bank, Fonkoze.”

Soon after the call, I met with Father Joseph Philippe in Haiti. Within 15 min-

utes I realized that he had more vision than all the top executives who had been my

clients in D.C. put together. He pulled a rickety typing table between us, and with

paper and pencil in hand said, “Let’s get to work.” We organized a meeting in

Miami, inviting leaders from the Haitian diaspora, developed a strategy for mov-

ing forward, and raised Fonkoze’s first $20,000 from another priest and from Regroupement des Organismes Canado-Haïtiens, a federation of Haitian organi- zations in Montreal. innovations / fall 2010 15 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 Anne Hastings, with James Kurz and Katleen Felix Next we set out together in old pickup trucks, spending days bouncing along Haiti’s horrible roads so that Father Joseph could give speeches about his idea for a bank the poor could call their own. Most of the places we visited felt like the end of the earth, more remote and desolate than I had ever imagined possible. “How will they know to come?” I asked on our first trip. Father Joseph’s eyes twinkled a bit. “They’ll know.” And they did, hundreds of people walked for hours from the hills all around to listen to a priest they did not know and an American who hard- ly spoke their language. “Talk to the people,” he would tell me. I stood in front of the group and explained to them why this blan, less a statement on the color of my skin than on the fact that I was a foreigner, had come to speak to them about a bank for the poor. (Those first days gave me a very strong impetus to learn Haitian Creole quickly.) At the time, I couldn’t understand what Father Joseph was saying to the peas- ants when he introduced me to the crowd. It wasn’t until four months later that I understood that he was explaining that the Holy Spirit had sent me to help him open this bank. Once my year-long commitment had turned into a decade and then more, I came to agree with him. When I first arrived in Haiti, Fonkoze had just two part-time employees and a handful of clients. We had two computers, both of which were my personal com- puters from the United States. We used Quicken, a personal finance program, to track the loan portfolio. Within a year of my arrival, we opened 11 branches in Haiti’s largest cities and towns. More often than not, Fonkoze pushed the barriers of what others thought reasonable or even possible, opening twice as many branches as we had originally planned by conserving in every possible way. Expansion across the country was as rapid as could possibly be implemented while maintaining financial soundness. But, there were those who had their concerns. One day I received a phone call from a stakeholder I had known since the very first meeting in Miami. He was deeply concerned about the new branches Fonkoze was opening in some smaller towns. “You can’t open a branch in a place like that with- out doing a market study first,” he insisted. “You need to be sure that the branch can eventually become sustainable.” Indeed, Fonkoze opened branches in places that had nothing else going for them. Although no branch was ever sustainable on its first day, and some branch- es are still unsustainable today, Fonkoze made the case to its shareholders that a lack of sustainability was not a reason to close. If all it takes is a small subsidy to keep a branch operating and its impact on the local economy is profound, why should operations be shut down? In many ways, taking risks others may have avoided was a part of Fonkoze’s DNA—and may help to explain its success. Once we demonstrated that there was in fact a healthy demand in some rural villages, the commercial banks followed and also opened in those communities. Other com- munities were not commercially attractive, so the large banks stayed away. But without financial services, how could the community’s economy ever grow? Most of Haiti’s rural countryside was too poor to be interesting to business and thus increasingly poor. 16 innovations / fall 2010 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 A Bank the Poor Can Call Their Own Father Joseph Philippe and Anne Hastings (May 2006). Haiti has two distinct economic zones: Port-au-Prince, which functions as the center of commerce and trade with some functioning government services, and the rest of the country, with far less economic activity. As a result, hundreds of thousands of families have come to Port-au-Prince over the past few decades, caus- ing a surge in population density and forming Port-au-Prince’s slums, such as the well-known Cité Soleil or Belair, which are known around the world as some of the most unstable and insecure in the world. This trend has further centralized the country around a single city, virtually halting economic growth in rural towns throughout the country and perpetuating the destructive cycle of migration. Fonkoze’s mission is to create stronger, more robust economies in these rural areas by providing financial services that serve the public interest. In a fair, trans- parent marketplace, competitors take market share from those who overprice. In many of Haiti’s rural areas, however, very few have the capital and the means to provide basic financial services; they can exercise monopoly-like power for these essential services, and collusion is rampant. Such people can buy dollars for 10 per- cent below the market rate, place surcharges on remittance payments, and charge 300 percent to 400 percent interest on loans. They discriminate about who can be their clients, and vary pricing based on volume and social stature. In contrast, Fonkoze’s rates and pricing, by policy, are the most competitive in the local mar- ket and are evenly applied regardless of volume or customer. Rates and prices are innovations / fall 2010 17 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 Anne Hastings, with James Kurz and Katleen Felix transparently posted, and clients are educated in how to read and understand interest rates and fees. By accepting the risk of lending in the rural areas, provid- ing capital, and opening basic financial services to everyone, Fonkoze creates the conditions that allow an economy to grow. Achieving these results in some of Haiti’s poorest, most rural areas is very expensive and requires scale to become commercially viable. As a foundation, Fonkoze raises money to reach the very poorest and to start and sustain new branches. Money is raised not only in the United States by organizations like Fonkoze USA but around the world. Although the seed money is often charitable, scale is best reached through sustainable business practices, a goal for which Fonkoze continually strives. THE FONKOZE MODEL When Fonkoze opens a new branch in a rural area, it is sometimes the most eco- nomically stimulating enterprise ever started in that community, not to mention the largest employer. It provides a new, reliable point of service to receive money sent by family and friends abroad. It injects capital into the local economy by pro- viding as much as $500,000 in loans. Special programs like Chemen Lavi Miyo and

Ti Kredi, Fonkoze’s programs for the very poorest women, were first offered in

2007 to seek out the economically inactive, thereby growing the capacity of the

local economy.

Fonkoze begins the process of opening a branch by going to the community’s

leaders—the priests, the pastors, the elders, the elected officials, and the leaders of

grassroots organizations—to tell them about Fonkoze and its plan to open a

branch. We explain what Fonkoze will do to develop the economy of the commu-

nity and how many jobs Fonkoze will create. To the people of the town, particular-

ly the women, Fonkoze explains that its goal is to attack lamizè, the misery of

poverty.

Each Haitian town is dominated by markets full of small, mostly female ven-

dors, the ti machann. They travel to Port-au-Prince to buy inventory and then rush

to the market, sit on the ground, and sell their goods. In order to provide food and

other basic necessities for their family, the ti machann must buy and sell each day.

These bustling markets are everywhere in Haiti and are the principal supply chain

for goods going into rural areas. Fonkoze tries to locate branches close to the pri-

mary market of a town but not actually inside the market. Each branch is painted

in Fonkoze’s distinctive palette of purple and orange, and a sign with Fonkoze’s

name and logo is hung in front of the building. Banners are placed across the

streets, a common sight in all Haitian towns, and an employee walks through the

market with a megaphone announcing Fonkoze’s opening and answering ques-

tions.

At all its branches, Fonkoze has always provided three core financial services:

micro-loans, remittances, and savings.

18

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

An Organization Founded on Rights, Trust, and Solidarity

Fonkoze seeks to hire employees who are literate; that is, they can read and write

confidently in Haitian Creole. At first, Father Joseph would perform informal

interviews with potential new employees, but over time Fonkoze has formalized

the process. Each potential employee must pass a test on which they demonstrate

that they can use a calculator, they know what a bank is, and they understand

what Fonkoze is doing in Haiti. Fonkoze looks for an understanding of its mis-

sion and its philosophy of how to achieve it. All employees of Fonkoze must

agree to this philosophy.

The most important attribute, however, is honesty. Not only do Fonkoze

employees handle banking transactions, which for obvious reasons require a

high level of integrity, but they also are placed directly in front of Haiti’s mem-

ber clients, who are vulnerable and in need of extreme professionalism. The

entire organization is founded on the rights, trust, and solidarity with Fonkoze’s

members; any missteps that violate the pact the organization has with its mem-

bers would be devastating.

Micro-loans

In rural parts of Haiti, banks have no interest in making small loans or taking on

the perceived high risks of lending to ti machann. As a result, many women are

forced out of the economy and into seclusion by a system that cannot offer them

opportunity. A miniscule money supply and no access to credit chokes off what lit-

tle economy exists and leads to a cycle of stagnation that drives people from their

homes to Port-au-Prince in search of work.

In 1994, when Fonkoze began operations, group lending was new to Haiti. In

Fonkoze’s group model, each Fonkoze loan client is a member of a Solidarity

Group with four other women. Starting in 2001, these groups were organized into

Solidarity Centers composed of 6-10 groups, which meet near clients’ homes for

loan disbursement, repayment, education, and Solidarity meetings. The women,

who are all dealing with many of the same challenges, develop a tremendously

powerful sense of community. These centers, initially organized with the assistance

of Mr. Salam of Grameen Bank in Bangladesh, caused an explosion of growth in

membership and dramatically lowered delinquency.

The Solidarity Centers also make Fonkoze a truly democratic institution. Each

center elects a chief who represents it at caucuses for the entire branch. These

branch-wide caucuses elect representatives to a national assembly that meets once

a year in Port-au-Prince and, among other functions, elects the majority of the

Fonkoze board of directors. Thus, Fonkoze is not only creating economic condi-

tions for democracy, but is also training democratic leaders. The centers also have

an unexpected benefit: they provide an enormously strong point of service for pro-

grams other than microfinance, such as education and health screenings. They

provide an excellent system for spreading complex information to people living in

extremely rural areas.

innovations / fall 2010

19

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

Anne Hastings, with James Kurz and Katleen Felix

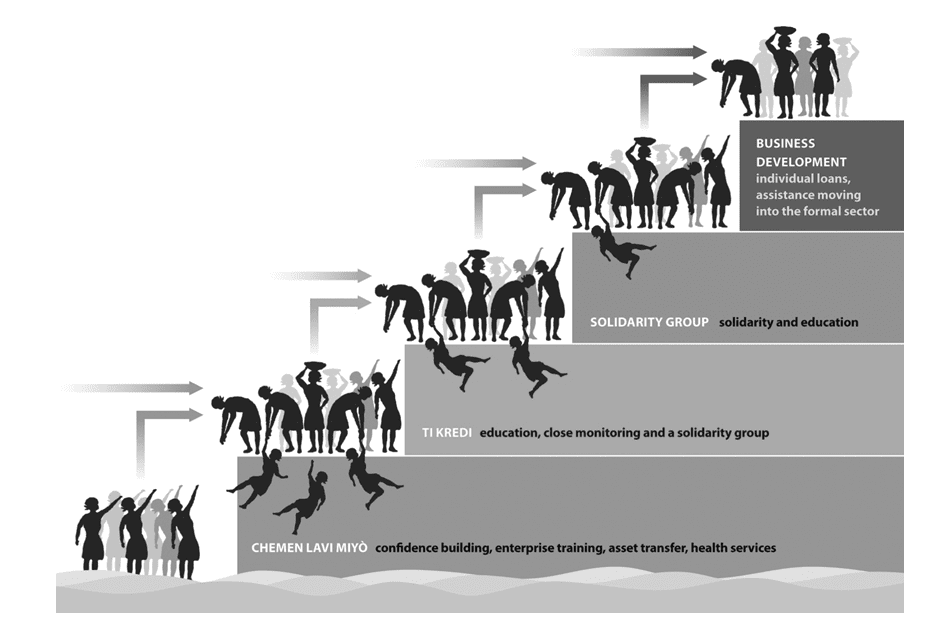

Figure 1. The Staircase Out of Poverty.

From the base program designed for the ultra poor—women who are among

Haiti’s absolute poorest and who do not have a productive asset with which to start

a business—to ti kredi, where loans begin at $25, all the way to business develop- ment, where individual loans can reach $100,000 or more, Fonkoze meets clients

where they are and tries to give them the tools they need to continue.

Remittances

Many Haitians rely on money transfers from family abroad. A least two million

Haitians have left Haiti for political or economic reasons since the early 1960s,

forming a large foreign diaspora. As much as 80 percent of Haiti’s professional

workforce has emigrated to France, Canada, or the United States. The money they

send home supports basic needs like food, school fees, and basic health care. The

diaspora also remits collectively through Hometown Associations to support

building projects, schools, orphanages, churches, and other organizations.

The cost of sending remittances is very high, and many communities lack

places to receive money transfers. This reduces the amount of money that flows

into the community and often forces people to travel hours to access their

money—time that could be spent working but is instead spent packed like live-

stock in the back of rusty pickup trucks and on top of second-hand school buses.

By offering a cheaper payment point in the community, Fonkoze increases both

the availability and the velocity of money.

20

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

A Bank the Poor Can Call Their Own

Savings

Savings has long been a core tenet of the power of banking. Savings provide secu-

rity, as money can be sheltered through difficult times. A savings account also

makes money more portable. When a client travels from home in the north of

Haiti to Port-au-Prince to buy merchandise, she can leave her money in her

Fonkoze account instead of carrying cash, which is vulnerable to theft, and then

withdraw money in Port-au-Prince to pay for merchandise.

As I mentioned previously, Father Joseph teaches that “you can’t simply give a

woman a loan and walk away, you have to accompany her on her journey out of

poverty.” With this in mind, Fonkoze amplified the three basic financial service

offerings with education, health, and other innovative services designed to build

solidarity and client success. In many countries, microfinance institutions can

comfortably play the specialized role of financial institution because other essen-

tial services are made available by the government. To meet its dream for the peo-

ple of Haiti, Fonkoze is committed to filling the gaps in services such as education

and healthcare, in addition to providing badly needed financial services at a fair

price.

Fonkoze developed comprehensive services tailored to meet women wherever

they may be on their journey out of poverty. At each level, the package of loans,

education, health services, and mentorship is designed to meet the needs of that

demographic. Fonkoze calls this approach the “staircase out of poverty” (see figure

1).

CHALLENGES ALONG THE WAY

Fonkoze’s attitude toward risk is simple: as long as the ti machann are in the streets,

Fonkoze is open. Fonkoze built trust in a country because at all times, even the

most extraordinary, it has been stable, responsive, and open. Although part of a

large organization, each branch is intimately part of and created by the communi-

ty. The branch managers live in the communities. Many of the branches’ staff

members grew up knowing their clients. At Christmas, a holiday Haitians celebrate

vigorously, Fonkoze branches host community events. The pact that Fonkoze has

worked so hard to build and maintain with its clients and its communities has paid

off many times. In this section I discuss a number of the challenges that Fonkoze

has faced.

The Credit Cooperative Bubble

Following legislation passed in 1995 that lowered reserve requirements for banks

and removed interest rate caps, the idea of investment cooperatives emerged in

Haiti, but regulations were loosely written and poorly enforced. In the early

months of 2001, enabled by drug money, new credit cooperatives multiplied all

across the country, promising huge returns on savings and investments for anyone

who could make a deposit. Even members of the diaspora, persuaded that they

were investing in their country, were mortgaging their houses and cashing in their

innovations / fall 2010

21

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

Anne Hastings, with James Kurz and Katleen Felix

Maintaining Stability in a Tumultuous Environment

Since Fonkoze was founded, Haiti has suffered through tremendous political

upheaval time and time again. For much of Fonkoze’s history, Haitian political

life has revolved around Jean-Bertrand Aristide, the first democratically elected

president of Haiti who was deposed in a coup d’état in 1991, reinstalled as pres-

ident by the United States in 1994, and then led Haiti from 2000 through 2004,

when he was again forced from power. Against this highly politicized backdrop,

Fonkoze has remained completely outside of Haitian party politics, which no

doubt has contributed to its stability. In fact, Fonkoze has a policy that any

employees who run for public office, no matter how minor, must resign from

Fonkoze without any guarantee of being able to resume their jobs, even if they

lose the election.

Clients, investors, and colleagues have often asked for my views on Haitian

politics. My response has always been that these are questions for the Haitian

people to decide, not me. On U.S. policy toward Haiti, however, I have been will-

ing to offer my opinion as a U.S. citizen.

Economic stratification has been a feature of Haitian life since the first

Europeans landed on the island and quickly began importing slave labor from

Africa. Even after Haiti won its independence and all slaves were freed, a massive

divide continued between those of mixed race and those of direct African dis-

sent. This pattern has survived to the present day. A small handful of families

and private companies own an overwhelming share of Haiti’s mechanized

industry and assets, and control access to credit. The implications of this consol-

idation of economic life are utter control and denial of financial services to the

mass of Haiti’s population. For decades, this has left Haitian poor with terrible

options for financial services: loan shark gangs that charge interest percentages

in the hundreds per annum with severe penalties for nonpayment, and unsavory

schemes of investment and savings that enriched a privileged few while leading

to a virtual confiscation of what wealth the poor could accumulate.

Fonkoze is an institution founded on the principle that economic freedom

is the foundation of democracy. If a political democracy is to survive, every

Haitian must have the right and the opportunity to participate in the country’s

economic development.

401(k)s to invest. Credit agents and branch managers wrote letters and came to my

office to tell me that if we did not compete with these rates of return, we’d lose

business. I told our staff the yields being advertised could not be sustained, and

these institutions would put themselves out of business. In the summer of 2002,

the scales tipped and the pyramid scheme that had spread across the country col-

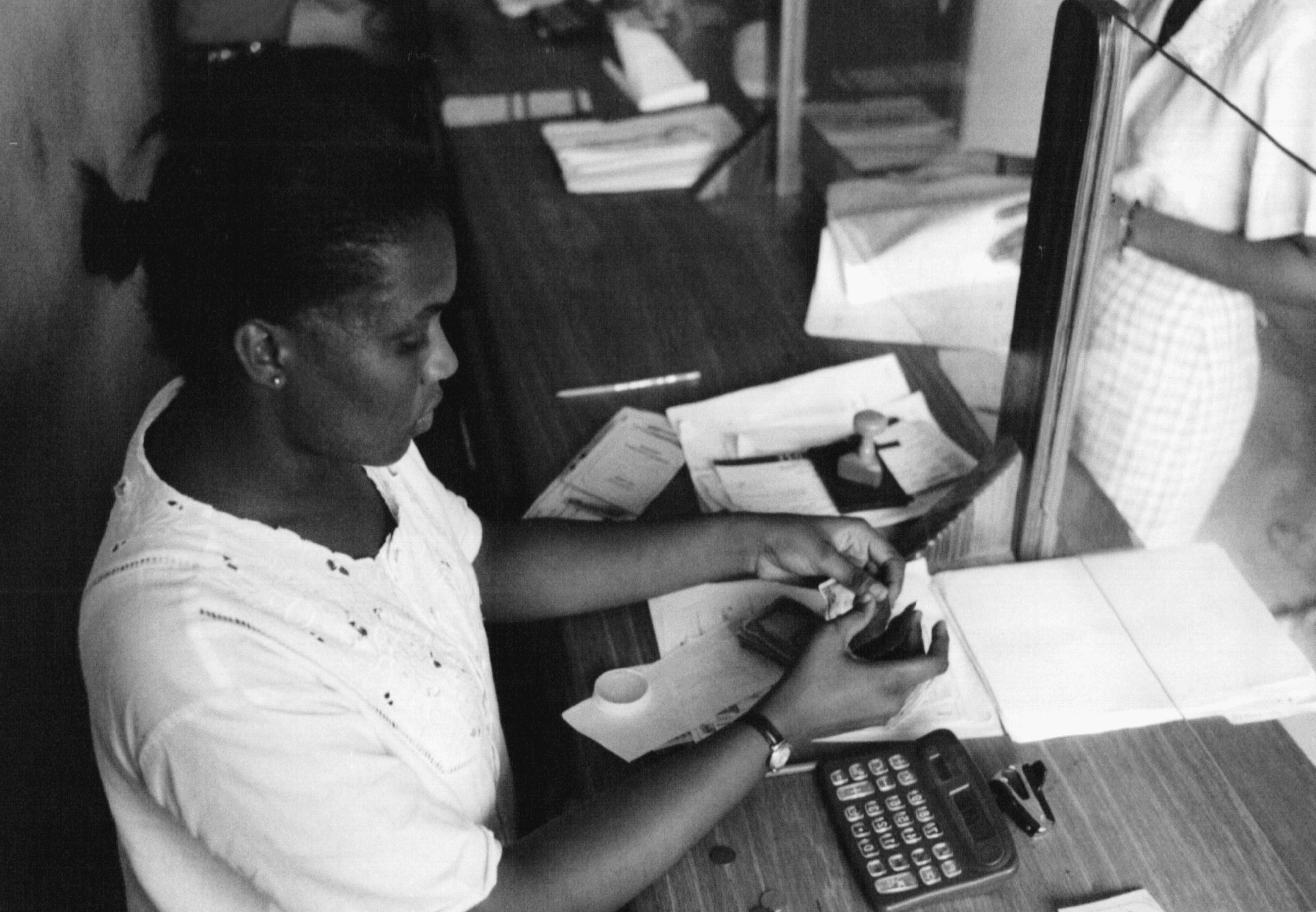

lapsed. Some $200 million in Haitian savings disappeared overnight, resulting in widespread suffering and protest and sowing the seeds of the government’s even- 22 innovations / fall 2010 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 A Bank the Poor Can Call Their Own tual collapse. For Haitians, distrust of financial institutions and the elites who ran them grew even deeper. The 2004 Political Crisis In early 2004, when the former military’s militia, the National Revolutionary Front for the Liberation of Haiti, crossed the border from the Dominican Republic into northern Haiti and captured the town of Hinche, the paramilitary group marched on Fonkoze’s branch. Three of Fonkoze’s clients who saw the men marching on the branch ran in front of the door and insisted the paramilitaries stop, boldly stating, “You will have to burn us to burn this branch down.” Shockingly, the militia relent- ed and the branch was spared. This is a beautiful illustration of Fonkoze’s philos- ophy regarding security: the only true security comes from the community. Technology Travails Fonkoze began the process of installing an electronic information system in 2001. This was no small feat. Even in Port-au-Prince, Haiti suffers from multiple long power outages each day; in some parts of the country, power outages can last for days. Even when power is flowing, it is riddled with surges that can melt silicon and cause tiny bumps that restart computers. Every branch with computers also need- ed an expensive system of batteries, inverters, and generators that was time-con- suming to get right. Data connectivity was more difficult. A live banking system requires an Internet connection to process transactions. When a teller makes a transaction on a customer’s account, she uses her computer terminal to request account informa- tion from a centrally located server. She then processes the transaction, which updates the client’s account and automatically timestamps the transaction. Unfortunately, a live Internet connection in Haiti is difficult to obtain in 2010, much less in 2003. Branches would go offline for days at a time, forcing staff to keep records manually and then scramble to enter transactions (with the wrong timestamp) when the system came back online. The results were crippling when the branch could not regain its connection for weeks. It wasn’t until 2005 or 2006 that Fonkoze finally had a reasonably reliable Internet connection in about half of its branches. Even then, the branch director of one small branch, Latwazon, would need to scale a mountain each day to get sufficient cellular phone coverage to call the central office. Finally, in 2007, the Multilateral Investment Fund of the Inter-American Development Bank provided a grant that allowed Fonkoze to install high-tech satellite equipment in the last 17 branches of the institution, giving staff the ability to get the software working as originally intended. THE FONKOZE MODEL, TAKE 2 As Fonkoze grew, the complexity of its financial challenges grew as well. The financing mechanism Fonkoze had been utilizing—low-interest, socially responsi- innovations / fall 2010 23 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 Anne Hastings, with James Kurz and Katleen Felix ble loans borrowed in U.S. dollars—had to be rethought when the Haitian gourde began devaluing in 2000. It doesn’t make sense to borrow in dollars and then lend in gourdes if by the time the gourdes are repaid they no longer have the same value. In addition, there was simply not enough capital to reach the scale that would be necessary to make the institution profitable. Even with only 15 branches at the time, the market for Fonkoze’s loans exceeded its capital base—and its capital base consisted of 100 percent debt! Another financing strategy had to be devised. Other foundations and micro-credit institutions throughout the developing world had faced the same challenges of sustainability, scale, and capital. Prodem in Brazil, the Grameen Bank in Bangladesh, and CARD in the Philippines all had begun as foundations or not-for-profits but had made the transition to full- fledged micro-credit commercial banks. Fonkoze was having no trouble mobiliz- ing savings in the communities in which it was operating. Each year since 1996, the volume of savings had more than doubled. By the end of 2000 it stood at almost $2 million. A commercial bank license would allow Fonkoze to access those

deposits for lending. With another $2-3 million in capital from abroad, Fonkoze would have a stable base from which to reach scale. Toward a Commercial Bank License In the early stages of our exploration, I, along with Gordon McCormick, a major donor and Wall Street investment banker, and other members of the Fonkoze USA board consulted with attorneys in Haiti and the United States, donor institutions, and international microfinance consultants from Development Alternatives, Inc. The private offering we devised for the commercialization of the institution was a tremendous success. Two million dollars in equity capital were raised in the United States and the Netherlands to successfully spin off Fonkoze’s sustainable branches into a full-service institution, with the mission of providing Haiti’s rural population with a full range of financial services. The name of this new institution was Sèvis Finansye Fonkoze (SFF), which translates as Fonkoze Financial Services. SFF operates as a non-bank financial services institution, although we hope some- day to receive a commercial bank license. Today, Fonkoze (the foundation) incubates new branches, nurtures them to sustainability, and pilots new products and services. When a branch or product becomes mature, it is transferred to SFF, where it can be scaled further. In addition, the foundation is responsible for delivering our non-financial services, especially education, to all Fonkoze and SFF clients. And, it carefully measures the extent to which we are meeting our mission of helping the poor escape poverty by checking on the poverty status of our clients over time. In December 2005, Fonkoze convened its key stakeholders and management team to lay out a vision for the bank’s future, which included building a network of 60 branches within five years and serving 200,000 loan clients (or one million Haitians, including the family members of those clients). Following the hurricanes in 2008 and the earthquake in 2010, Fonkoze has slowed its growth, but the net- 24 innovations / fall 2010 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 A Bank the Poor Can Call Their Own Early Teller. Before Fonkoze became computerized in all of its branches, tellers kept meticulous manual records, which had to be reconciled by hand. work has still grown from just 26 branches in 2005 to 41 branches in 2010. Over the rest of 2010 and into 2011, Fonkoze will grow aggressively once again, reach- ing even deeper into Haiti’s most remote rural areas and bringing Haitians access to financial services. Leadership Development An additional part of Fonkoze’s updated model is a new expression of its commit- ment to leadership development. In fall 2007, Fonkoze opened a full-function branch in the rural town of Limbe, but with a twist. The staff was comprised of some of Fonkoze’s most experienced and accomplished employees. A dormitory was included upstairs in the branch so the employees could build teamwork and camaraderie. The branch is a model, with space for apprentices from across the Fonkoze system to come and learn from the staff at Limbe. Limbe also serves as an active learning center and one of Fonkoze’s launching points for new product pilots. The branch’s diverse array of unusual products is unique in Fonkoze’s branch system. Fonkoze has piloted loans specifically targeted at people living with HIV/AIDS in Limbe, for example, and experimented with housing loans and a cel- lular phone business concept. New education modules and ti kredi, now a major part of Fonkoze’s approach, were given early pilots at Limbe. Fonkoze Limbe seeks to document duplicable ideas and techniques for alleviating poverty. innovations / fall 2010 25 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 Anne Hastings, with James Kurz and Katleen Felix The Evolution of Microinsurance in Fonkoze In Fonkoze’s strategy of poverty alleviation, Fonkoze meets each client with a suite of services to help her take the next step forward. But when a disaster strikes or a family member dies, the poor often slip back down the staircase. The process of rebuilding their lives can take years. So, Fonkoze decided to extend its financial services to include insurance, beginning with life and credit insurance. Although Haiti is relatively sheltered from tropical storms by mountains and the Dominican Republic, tropical weather can be devastating. Decades of defor- estation, poor infrastructure development, and clogged waterways lead to massive flooding. In 2004, Hurricane Jeanne killed over 3,000 people in Haiti. Many Fonkoze clients’ businesses were devastated, their inventories washed away as the waters surged. After careful consultation with clients and employees, Fonkoze quickly recapitalized its clients’ businesses by disbursing capital to restart their loans with the amount they originally borrowed, realizing that the only way they could restart their lives was to restart their commerce. Some of the capital used to achieve this was donated money, which allowed Fonkoze to perform the disburse- ment without jeopardizing its financial position. What was lost in short-term self- sufficiency was made up for in a desirable outcome. Fonkoze learned that not only did this lead to a high repayment rate among clients who had been in a grave sit- uation, it achieved that outcome because it helped clients rebuild their lives. This successful experiment laid the groundwork for a much larger crisis in which Fonkoze rallied to help its clients in the face of disaster. During the hurricane season of 2008, Haiti was struck by four consecutive tropical storms: Fay, Gustav, Hannah, and Ike. Almost 14,000 Fonkoze clients lost their businesses. Hundreds of thousands suffered for months, their homes under water, their city coated in a thick layer of waist-deep mud. I flew by helicopter to Gonaives, the most devastated city, on September 11, 2008, days after the hurri- canes. I made my way through the high waters to meet with Fonkoze employees, bringing them just $250 each and the promise that perhaps more would come.

Even as their own houses lay in shambles or were washed away by the raging water,

Fonkoze employees mobilized to help clients. With the assistance of the United

Kingdom’s Department for International Development, the U.S. Agency for

International Development (USAID), and many other concerned partners,

Fonkoze raised $4 million to recapitalize client’s loans and make them interest free. Nearly 90 percent of clients successfully repaid these renewed loans, and Fonkoze used $1 million of the repaid funding to establish a long-term catastrophe fund.

One of our clients from Gonaives spent almost a decade successfully working

her way out of poverty. With microfinance loans, she created a business selling

plastic containers. In 2004, she and her children watched from their roof as flood-

ing from a tropical storm washed away her livelihood. She rebuilt her business with

another micro-loan, proving that her spirit, while bruised, was not broken. Then

in 2008, she again lost everything and had to start over. This vicious cycle traps so

many in Haiti. Having thousands of our clients suffer through similar stories fol-

26

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

A Bank the Poor Can Call Their Own

lowing storms and turmoil, Fonkoze turned to innovation to help clients stay on

the staircase, even when disaster strikes.

In April 2007, in partnership with Alternative Insurance Company (AIC) of

Haiti, Fonkoze began to develop Haiti’s first micro-life-and-credit insurance prod-

uct: an indemnity and loan forgiveness in the event of a client’s death. When a per-

son in Haiti dies with debts, they leave their family with one less productive fami-

ly member, costs for funeral expenses, and the outstanding balance of their loan.

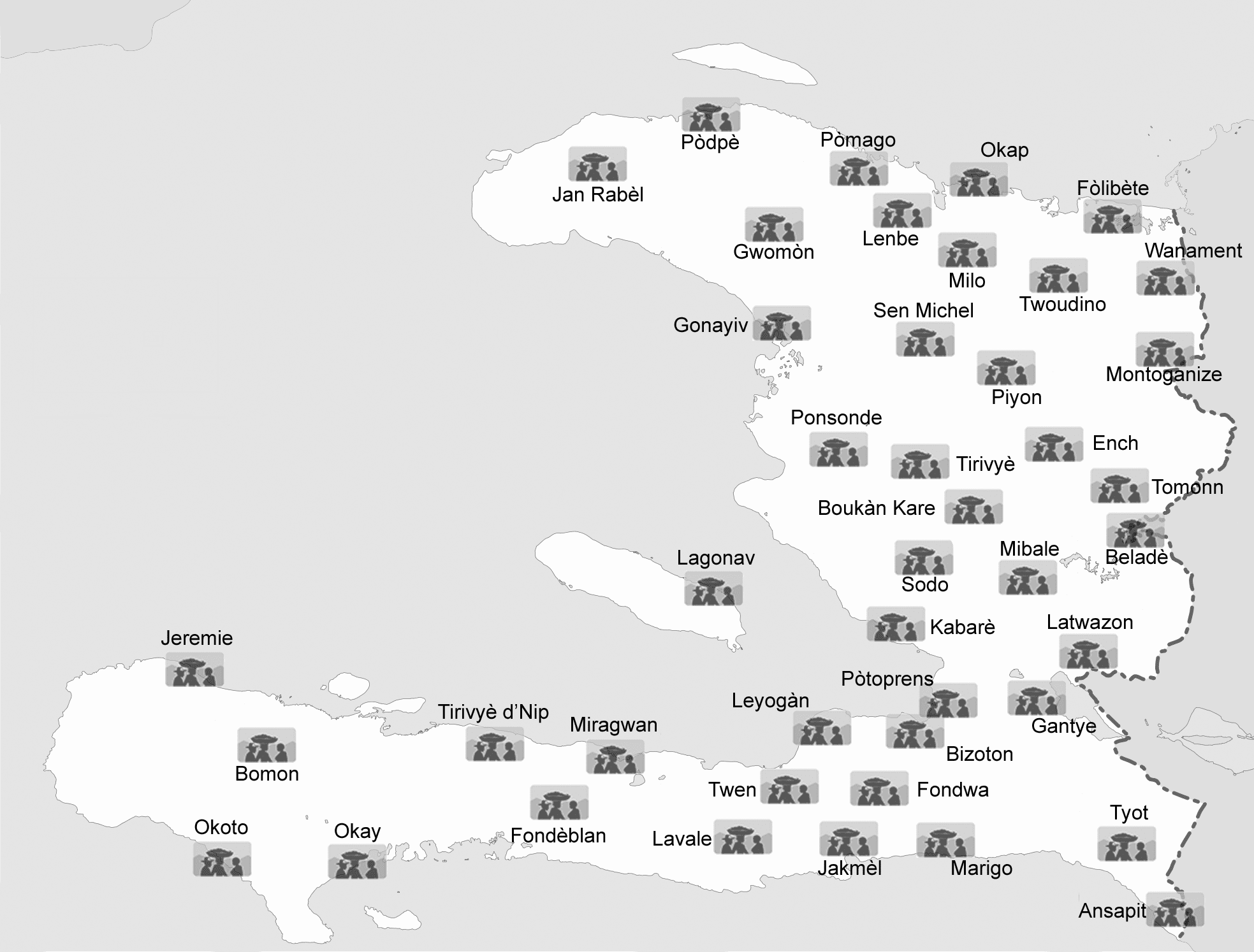

Fonkoze’s micro-insurance provides an indemnity of 5,000 HTG (about $125) and full forgiveness of the loan. This micro-life-insurance has helped hundreds of families of Fonkoze clients since it was rolled out, but it does nothing to help clients who lose their business- es, their homes, or their assets in a disaster. So in 2008, Fonkoze, again in partner- ship with AIC, started to develop catastrophic insurance for its clients—unfortu- nately not quite in time to be ready for Haiti’s largest natural catastrophe. The Earthquake As the dust cleared, Fonkoze employees helped those who had been injured and then everyone slowly set off into the growing darkness to reach their loved ones. Rubble and traffic blocked car traffic, so cars were abandoned by the side of the road. Everywhere across the city were the dead, dying, and maimed. Most of Fonkoze’s employees did not reach their homes until the middle of the night. For hundreds of them, home was gone, a mere pile of rubble. On January 13, I went to the branch to try to secure the most important doc- uments and IT equipment. Nearly all other employees spent the day searching for friends and family by car and by foot. Friends told friends who told others whether someone was alive or dead—a human chain of communication was the only source of news throughout the country. On January 14, Georgette Jean-Louis, Fonkoze’s CFO, received a cell phone call for the first time since the earthquake. The call was from the manager of the small La Toisin branch. He had a personal cell phone from one of the smaller cell phone providers, and had climbed up the side of a mountain to get a signal to reach his boss in Port-au-Prince. To Georgette’s shock, the La Toisin branch was open, credit agents had been going to meetings with clients, and both disbursements and reimbursements were ongoing. Port-au-Prince lay in ruins, but not every part of the country was destroyed. Yet Port-au-Prince is the center of commerce for the country; people throughout the country rely on the food and products that enter from the port. Georgette sprang back from the edge of despair and set out to find me. We were unable to find each other until the next day, when we established a work schedule and planned the first steps of what needed to be done. In the days after the earthquake, Haitians living abroad sent millions of dollars in remittances to their friends and family in Haiti. Each year, nearly 24 percent of Haiti’s GDP enters the country as remittances from abroad. Few other countries in innovations / fall 2010 27 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 Anne Hastings, with James Kurz and Katleen Felix Fonkoze Branch Map, Fall 2010. the world are so dependent on this source of income. Along with the immediate effects of the quake, many people had no money in their pockets, had lost their assets and resources, and had lost key family members. Following the earthquake, accessing remittances was for many a matter of life and death. As one of the leading payers of remittances and with over 200,000 savings accounts, especially in some of the more remote places in Haiti, Fonkoze knew that it needed to open its branches and provide access to its clients’ money as soon as it possibly could. Most of Fonkoze’s central office staff was now homeless, water was increasingly scarce, and food was a luxury, but everyone showed up to work in the days after the quake. Many employees came in to work 12-hour days and then returned to the street to sleep on the sidewalk. There were two primary challenges. First, with Internet cut in many branches, power becoming more and more scarce, and hardly any telephone service, com- pleting the necessary back-office functions of remittance payment were tremen- dously challenging. Second, the paying agent needed cash to pay out to the recipi- ents. Haiti’s large commercial banks suffered tremendously in the quake. In the days immediately afterward, the biggest concerns of many commercial bank branches was security and how to protect bank assets and staff from an increasingly desper- ate population. It was not until January 23, fully 11 days after the earthquake, that 28 innovations / fall 2010 Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023 A Bank the Poor Can Call Their Own a few branches in some parts of Port-au-Prince began to open their doors to their best customers. Fonkoze holds deposits in Haitian and U.S. banks. Its primary bank in Haiti held the critical liquidity needed in Fonkoze’s branches, but instead of providing Fonkoze with access to its money it treated it like a regular customer, limiting with- drawals to just $5,000 per day—a trivial amount for a financial institution trying

to pay over $250,000 in remittances each day. After four days of negotiations that began on January 18, we secured approval to airlift $2 million in cash from Fonkoze’s accounts in the City National Bank of

New Jersey direct to our branches throughout the country. It then took less than

24 hours for the U.S. Military and the United Nations to complete the delivery, air-

dropping disguised boxes of cash across Haiti. The cash was packaged in Miami

and transported aboard a military C-17 to Haiti. The operation, unprecedented for

a microfinance institution, was widely reported in the media.

As January gave way to February, the long-term challenges began. With just

months before the start of Haiti’s rainy season, hundreds of thousands remained

without a home; months later, virtually all of them continue to live in tents, sub-

jected to the torrential rains and floods. While more and more people gained

access to emergency food supplies provided by relief agencies, their small business-

es lay under the rubble, their inventory stolen or consumed in the emergency, or

lost in the desperate attempt to find family members.

One client, Dienna Cidrac, told Fonkoze’s staff a story similar to that of 18,000

Fonkoze member clients:

Sitting in front of her little brick house she had “worked so hard to build,”

Dienna tells me she is so grateful to God for having spared her life and

those of her loved ones, but now she has to start working. The small

depot where she keeps her merchandise near the open market was ran-

sacked and she lost her business completely. “Worse than my home, I lost

my business. My children and grandkids are O.K., and I can put up some

wood eventually to cover our heads, but how do I start over without my

business?”

In 2009, Fonkoze had been working hard to provide catastrophic insurance to all

of its clients. Clients who lived within the most severely affected areas of a disaster

or who lost their business, home, or both would be eligible to claim an indemnity

payment of 5,000 HTG, reimbursement of their loan, and a new loan when they

were ready. Fonkoze was just weeks away from starting the program when the

earthquake struck. After consulting with its employees, however, Fonkoze part-

nered with the American Red Cross, MasterCard Foundation, Mercy Corps, Citi

Foundation, Plan International, and countless others to simulate the catastrophic

insurance product as if it had already been in place with capital, expense offsets,

and technical assistance.

Since January, Kore Fanmi Fonkoze (Haitian Creole for the Program to

Reinforce the Fonkoze Family) has been administered to more than 18,000 mem-

innovations / fall 2010

29

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

Anne Hastings, with James Kurz and Katleen Felix

An Emergency Airlift of Cash

Friday, January 22

4:52 p.m. Operation is cleared by U.S. State Department, United Nations, and the

U.S. Military

9:25 p.m. Boxes with cash separated into 34 packets successfully delivered to

Homestead Air Force Base in Miami.

10:15 p.m. A military C-17 is diverted from Langley, Virginia, en route to Port-

au-Prince to pick up the cash.

Saturday, January 23

3:30 a.m. Military C-17 plane arrives in Port-au-Prince with boxes of cash.

1:30 p.m. Military helicopters finish dropping off boxes at designated points

across Haiti and return to Port-au-Prince.

bers. To avoid disputes and to recognize the varying impact the earthquake had in

the different zones, clients of the ten branches in the area most severely affected by

the earthquake were automatically eligible.

Fonkoze also did all it could to take care of its employees, nearly 450 of whom

were rendered homeless by the earthquake. Those whose homes collapsed received

$1,000, and those whose homes were damaged received $500, provided with the

assistance of Fonkoze USA and other partners. These sums are not nearly enough

to build new homes, but they helped to stabilize employees’ lives.

As Haiti begins a long, painful rebuilding process, the world is changing rap-

idly. New advancements are opening up great potential to Fonkoze’s clients, many

of whom have developed leadership and business skills that will make them key

community leaders in Haiti’s future. Change is also coming in the form of new

technology, enabled by renewed investment in infrastructure. Fonkoze is actively

engaging with the emerging mobile branch and mobile banking industry, which

has shown great promise in Kenya and other countries.

THE LESSONS LEARNED

Fonkoze is in the business of getting people out of poverty. I have personally devot-

ed the last 14 years of my life to learning how to do that most effectively in Haiti,

one of the most fragile countries in the world. By definition, a fragile country is

one in which the government either cannot or will not provide its people, especial-

ly the poor, with even the most basic services—water, roads, health care, education.

These countries are characterized by extended internal conflicts, corruption in the

public and private sectors, a huge backlog of investment needs, and a breakdown

in the rule of law. Haiti is one of only 11 countries that have been on the list of

fragile countries continuously since the phrase was first coined.

30

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

A Bank the Poor Can Call Their Own

Haiti is further encumbered by frequent natural disasters made all the worse

by an environment that, according to USAID experts, “is suffering from a degree

of degradation almost without equal in the entire world.”

We set out to build a sustainable institution—an institution on which the poor

can rely long into the future. But it was to be an institution that worked, that actu-

ally succeeded in its business of getting people out of poverty. And it was to accom-

plish that in a fragile, environmentally devastated country wracked by natural and

manmade disasters on a very regular basis. Was it even possible?

I think all of us at Fonkoze would respond with a resounding “Yes!” We haven’t

achieved it yet, to be sure, but we have made significant strides. We have endured

violence, a disastrously weak economy, hurricanes, earthquakes, and attacks

against our people and our work. But through it all we have learned a tremendous

amount, lessons that will take us into the future.

We learned that when you offer very poor people convenient, accessible,

affordable financial services—by that I mean savings accounts, very small loans,

and a way for them to receive transfers from their family members living abroad—

some amazing things begin to happen. Their businesses begin to grow, their chil-

dren start going to school, and they put food on their table every day.

When you combine those financial services with educational programs in

which those who know how to read and write teach those who do not, even more

amazing things begin to happen. Watching a woman with tears in her eyes sign her

name for the very first time on a deposit slip as she adds money to her savings

account is a profound example of just how much these services can change lives.

When you combine such financial and educational services with health care

services, even more amazing things being to happen. People’s health improves,

their children’s health improves, and that in turn leads to stronger, healthier busi-

nesses.

In short, we learned that if our members are to make progress, the poor and

the poorest need a full range of financial services and a full range of support serv-

ices. Many of those support services are normally provided by the state, but in

Haiti they are not, so Fonkoze has no choice but to take them on too if it hopes to

achieve its mission.

We also learned a great deal about what sustainability really means in our busi-

ness in a country like Haiti. Providing the services the poor need to make their way

out of poverty is an expensive proposition. It’s hard to make much money on a $25

loan, especially when you have to provide your own energy, your own transporta-

tion, your own telecommunications, and your own security.

We learned that the solution to this problem is not to lose sight of one’s mis-

sion and provide larger loans to fewer poor people—it is to become more efficient,

to increase the number of borrowers, and to seek better ways of providing the same

services.

We learned that we were much more likely to achieve sustainability if we

worked harder at helping our clients on their journey out of poverty. The better

job we did for them, the more loyal they would become to us, the longer they

innovations / fall 2010

31

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023

Anne Hastings, with James Kurz and Katleen Felix

would stay with us, and the more likely they would become profitable clients for

us. Focusing on the needs of our clients is not only a mandate of our mission; it is

also good business.

We learned that our conclusions about our sustainability depend upon the lens

through which we view sustainability. Fonkoze’s commercial entity is not yet prof-

itable, but pre-earthquake it was on the verge of sustainability. In fact, we believe

that we are stronger today than we were on January 1, but that may not be appar-

ent if one looks at the traditional measures of financial performance highlighted

in financial statements. We are stronger because:

• Despite tremendously difficult conditions, we have survived when others fore-

cast our demise and maintained extraordinary operational performance across

the entire country. Our ability to withstand future disasters is even greater.

• We learned a significant lesson about the importance of helping our clients

manage risk.

• The personal and professional experiences of the past six months have brought

out a new paradigm for our employees and managers who have learned valu-

able lessons about their co-workers and themselves in the face of crisis.

• Our members have a new reason to see the value of our model, of being a

Fonkoze member, and of our level of commitment to our clients in the darkest

hours.

Still, the earthquake made it clear that Fonkoze will never fulfill its mission

until it finds a way to offer its clients a responsibly priced catastrophic insurance

policy so they can cope with the inevitable natural disasters. I have seen too many

of our clients start at the bottom of the staircase out of poverty, make their way

almost to the top, only to be knocked all the way back down because of a flood, a

hurricane, or an earthquake. Disasters come every two to four years, and some-

times even more often than that. I simply cannot continue to preach the impor-

tance of good financial management and wise investment decisions if Mother

Nature can wipe that all out in 35 seconds. There must be a better way for Fonkoze

and its members to weather natural disasters than what we can offer at this

moment. Our history has been one of searching for the causes of poverty and

addressing them one by one until they can be solved and we can move to the next.

That will not change.

It would be a huge mistake to proclaim that we’ve achieved sustainability

before we learn what it takes to show people the path out of poverty.

32

innovations / fall 2010

Downloaded from http://direct.mit.edu/itgg/article-pdf/5/4/13/704653/inov_a_00039.pdf by guest on 07 September 2023