Detección y cuantificación del uso de información privilegiada

and Stock Manipulation in Asian Markets∗

Gishan Dissanaike

University of Cambridge

Judge Business School

Trumpington Street

Cambridge CB2 1AG, Reino Unido

g.dissanaike@jbs.cam.ac.uk

Kim-Hwa Lim

University of Cambridge

Judge Business School

Trumpington Street

Cambridge CB2 1AG, Reino Unido

y

Penang Institute

10 Brown Road

10350 Penang, Malasia

kh.lim@jbs.cam.ac.uk, limkimhwa@penanginstitute.org

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Abstracto

This paper focuses on insider trading, where the perpetrators exploit market sensitive information to

earn profits or avoid losses. The paper’s objectives are as follows. Primero, we seek to examine whether

we can detect possible insider trading and stock manipulation and react in almost real time, incluso

though insider trading activity is intended to be evasive. Segundo, we also estimate the extent of il-

licit profits (or loss avoidance) that might have been earned. Finalmente, we analyze, if detection is possible,

the appropriate response for regulators and other market participants. We do not restrict our study

to cases where corporate events have materialized, as we hope to capture insider trading surrounding

market rumors and failed corporate events. Because insider trading is executed with the aim of being

evasive and undetected, it is impossible to conclude with certainty. Sin embargo, using a hypothe-

sized model based on how insiders and stock manipulators trade, we detect price patterns that are

consistent with their objective to maximize profits and at the same time be evasive.

1. Introducción

“Greed, for lack of a better word, is good.”

—Gordon Gekko, the main antagonist of the 1987 film Wall Street

The film mentioned in the epigraph revolves around insider trading and securities ma-

nipulation by Gordon Gekko, a fictional character modeled loosely after Ivan Boesky and

∗ We are grateful to Donald Hanna, Naoyuki Yoshino, and Iikka Korhonen for their helpful

comments.

Asian Economic Papers 14:3

C(cid:3) 2015 by the Earth Institute at Columbia University and the Massachusetts

Institute of Technology

doi:10.1162/ASEP_a_00368

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

Michael Milken. In real life, Boesky and Milken were, respectivamente, fined US$ 100m (about US$ 200m in today’s prices) en 1986 and US$ 600m (around US$ 1bn today) en 1990. El

magnitude of their fines indicates the amount of money involved in insider trading and

securities manipulation. Greed and the lure of big money have continued since, with re-

cent cases of insider trading and securities fraud in the United States such as Raj Rajarat-

nam in 2011, Angelo Mozilo in 2009, and Martha Stewart in 2004.

We take the mainstream view that insider trading is detrimental to the resource alloca-

tion mechanism of the market, is unjust, and distorts the integrity of the market. Mayoría

of the studies in the literature focus on legal insider trading where corporate insiders

(directors, company executives) trade their own stocks and such trades are reported to

the market.1

The type of insider trading undertaken by Gordon Gekko and company is illegal, cómo-

alguna vez, and is meant to manipulate stock prices for personal gain. Our paper focuses on the

Gordon Gekko type of insider trading and stock manipulation. The few studies in the

area of illegal insider trading tend to focus on specific corporate events, usually mergers

and acquisitions (METRO&A).2 We do not limit our study to cases of corporate events (METRO&A,

share repurchases, etc.) because this would exclude cases involving corporate events that

did not materialize or cases with price sensitive market rumors, which are outside the

purview of the regulators and are not reported by mainstream news providers.

Our research endeavor is challenging because illegal insider trades are difficult to detect

since they are structured to evade the regulators and other market participants, and insid-

ers can be widely dispersed both geographically and in identity thanks to the prevalence

of online trading and the ease in opening such accounts using real, “borrowed,” or stolen

identidades. Además, the syndicates are usually close knit groups and difficult to identify

and penetrate. There is also difficulty in collecting evidence because the spread of market-

manipulating rumours is usually through friends or via unregistered mobile phones,

avoiding fixed line phones (which are recorded in banks). Por último, most rumors are not

reported in mainstream media or main financial news providers such as Bloomberg and

Reuters, and hence data collection is difficult.

1 Some examples from the existing literature include the relationship between legal insider trading

and subsequent stock returns (Lakonishok and Lee 2001), accounting restatements (Badertscher,

Hribar, and Jenkins 2011), earnings management (Ke, Huddart, and Petroni 2003), mispricing (Alí,

Wei, and Zhou 2011), news announcements (Korczak, Korczak, and Lasfer 2010), or the effect of

the Sarbanes-Oxley Act (Brochet 2010).

2 Bris (2005) studies insiders’ behavior before tender offer announcements across many markets

entre 1990 y 1999. Rey (2009) analyzes insider trading around Canadian takeovers, y

Meulbroek and Hart (1997) focus on U.S. takeover premia in cases of insider trading.

2

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

The aforementioned insider trading cases came to light because of the amount of money

involved, the extent of evidence collected through wire taps, the use of witnesses as

part of their plea bargain, and the degree of resources devoted by the U.S. Securities

and Exchange Commission to these cases. Incluso entonces, most cases result in out-of-court

settlements—a fine instead of a conviction.3 To increase the chance of detecting in-

sider trading and stock manipulation, we focus on Asian markets as these markets are

similar to the U.S. markets in that insider trading is illegal in all these countries. asiático

regulators are less likely to pursue enforcement and detection, sin embargo, due to lack of

resources. There is a lower incentive to reveal insider trading because there are fewer

whistle blower/witness protection regulations,4 and insider trading is much more “ac-

ceptable” thanks to the importance of personal relationships in Asian culture5 and thus

less likely to be pursued legally. Además, equities are the easiest and most liquid in-

strument to express a bullish or bearish view since other instruments such as options

and convertible bonds are not widely traded.6 At the same time, the penalty for insider

trading is less stiff (p.ej., in Japan, the worst penalty a court can hand down under the

civil procedure prior to its revision in June 2013 is the offender’s return of trading profits

to the shareholders of the listed company). But Asia has become more integrated7 and

most Asian investors have a strong home bias. Por lo tanto, such behavior should be more

prevalent in Asian markets, which is supported by anecdotal evidence from non-Asian-

based fund managers that indicates pervasive insider trading and stock manipulation

in Asia.

This paper has three objectives. Primero, we seek to examine whether we can detect possi-

ble insider trading and stock manipulation and react in an almost real-time manner, incluso

though this activity is intended to evade market participants and regulators. Being able to

react in a close to real time manner is important so that remedial actions can be taken. Sec-

ond, we aim to estimate the extent of illicit profits that might have been earned. Finalmente,

if detection is possible, we also analyze the appropriate response of the regulators and

other market participants. This paper is significant because it is, a nuestro conocimiento, el

3 Por ejemplo, most UK cases are civil actions that encourage defendants to settle without going

to trial. The difficulties in onus of proof implies that criminal prosecutions are reserved for the

big scandals.

4 The environment in the United States is more conducive to whistleblowers to assist in the inves-

titigaciones. Por ejemplo, defendants in insider trading cases who agree to cooperate with investi-

gators, pay fines, or implement corporate reforms have charges against them dismissed if they

fully comply.

5 Por ejemplo, Liu, Wang, and Zhang (2013) find that Chinese firms with political connections have

a greater probability of engaging in M&Como.

6 A NOSOTROS. studies have found that informed insider traders might prefer to use the options market to

capitalize on their private information (Chakravarty, Gulen, and Mayhew 2004).

7 Chen and Woo (2010) find that trade and investment integration increased between 1990 y 2000,

weakened slightly to 2003, and has since picked up again.

3

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

first attempt to model the behavior of insider trading and stock manipulation without

restriction to corporate events that have materialized, and to empirically answer the

three objectives.

Setting the null hypothesis as the return on the stock is equal to that of the market port-

folio, we hypothesize a model using the typical pattern of insider dealing and stock ma-

nipulation, whereby stock prices fall regularly as insiders short the stock prior to some

negative news (such as a secondary equity offering); or stock prices rise constantly with-

out any news as insiders build up long positions and prior to a positive event (p.ej., a spe-

cial dividend or an M&A). Subsequent to the rise or fall, we hypothesize that the insider

will liquidate the position to maximize profits and then the stock may revert to its long-

term price. Through such a stock price pattern and trading, the insider will be able to

front-run other market participants, extract illicit profits, and outperform the market.

We recognize that it is impossible to detect and conclude that insider trading or stock ma-

nipulation has occurred with certainty. Based on our hypothesized model, sin embargo, nosotros

detect a certain price pattern that is consistent with what an insider or stock manipula-

tor may want to achieve. Setting the null hypothesis as the return on the stock is equal to

that of the market portfolio, we test and find that an insider who practices stock manipu-

lation in our hypothesized manner: 1) will outperform the market; y 2) may earn illicit

profits or avoid losses that amount to a mean daily return of 0.61223 por ciento (before trans-

action costs) across 12 markets in Asia between 1997 y 2010 (this daily return translates

to an annualized return of 366 percent per year). We also find that 3) market participants

who are alert to possible insider trading can react in an almost real time manner: Reg-

ulators can initiate investigations and investors can capitalize on the hidden news and

price changes while companies can make the necessary market disclosures. Over time,

this should reduce the profitability of engaging in insider trading and stock manipulation.

Our results are robust to market directions, company characteristics such as stock market

capitalization and liquidity, trading style, and aggressiveness of the investor. lo implícito-

cation of our findings is that regulators need to devote more resources to surveillance and

enforcement and support more research work in this area; investors need to be more alert;

and companies should be more careful in handling market sensitive information to avoid

information leakage.

This paper is organized as follows: Sección 2 presents our hypothesized detection model;

Sección 3 describes our methodology, datos, and analysis of the results from our hypoth-

esized model; Sección 4 reports some robustness tests; y Sección 5 concludes with the

key implications for the main market participants—regulators, sophisticated and na¨ıve

investors, as well as companies.

4

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

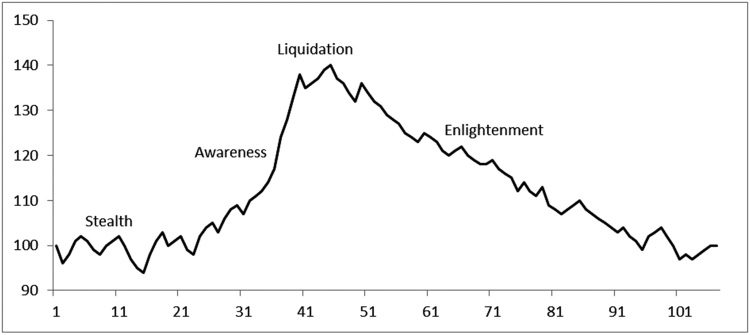

Cifra 1. Phases to our hypothesized insider trading stock price pattern

Fuente: Authors’ calculation.

2. Hypothesis development

We believe the insider and stock manipulator’s aim is to beat the market and max-

imize profits. Por lo tanto, we set the null hypothesis to be the return equal to the

market portfolio return. To maximize profits, the insider would want to buy in

before the price rises or when the stock price starts to increase—then liquidate

the positions almost at the peak before the price falls. This must be achieved sub-

ject to a few conditions such as being able to evade the regulators, to not star-

tle the market nor to alert other market participants, and to not exhaust their

own resources.

We hypothesize that there are four phases to price manipulation and insider trading

(Stealth, Awareness, Liquidation, and Enlightenment; ver figura 1), which if true, would

beat the null hypothesis of zero abnormal performance. To simplify, we describe our

hypothesis using the case when prices are manipulated upwards (the reverse is true for

downwards manipulation).

2.1 Stealth phase

At this stage, insiders buy the stock but keep their total positions below the disclosure

limit. The increase in position must not result in drastic and obvious price changes and it

has to be safe from attracting the attention of the regulator or other market participants.

Por lo tanto, prices are closing higher daily but the closing price must not be significantly

higher than its usual past price. The volume traded must also be close to the norm.

5

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

2.2 Awareness phase

At the earlier stage, rumors start to circulate due to insiders spreading rumors or an in-

crease in market knowledge of inside information. Por lo tanto, the volume traded will start

to rise above average as alert investors buy in. The gradual increase in prices will soon

become more intense as investors rebalance their portfolios and short positions on the

stock are bought back. Toward the end of this phase, there may be parabolic price rises

as investors jump onto the bandwagon and the media may report on the rumors and the

dramatic price increases.

2.3 Liquidation phase

As rumors become more prevalent and inside information is leaked to a wider audience,

the regulators may make inquiries. The company may be forced to issue an official denial

of the rumor(s) or confirmation of the event. With the new information, whether sub-

stantiated or rumored, analysts may revise their estimates and investors rebalance their

portfolios. The mainstream media starts to report the stock widely and the stock enjoys

maximum publicity. The insiders find this to be an opportune moment to exit for maxi-

mum profits as both the volume traded and prices are high.

2.4 Enlightenment phase

Liquidation by insiders needs to be gradual so as not to cause prices to crash. Na¨ıve and

other investors that are not part of the insider syndicate will not exit their positions and

will hold on to their positions, hoping that the fall in process is a temporary hiatus. Este

may be due to their being overly hopeful of the company’s prospects, or being blinded by

the rumors or overconfident of their ability to readjust their perceptions to the new reali-

corbatas. Such behavior is consistent with cognitive psychology in that individuals base their

decision excessively on recent historical data and do not fully acknowledge the uncertain-

ties of the future (Tversky and Kahneman 1992). The media and the company involved

may put undue emphasis on the significance of the M&A or divestment event. Over time,

sin embargo, price and volume traded will start to drift lower and fall toward their long term

significar.

3. Metodología, data description, and test results

We test our hypothesis against the null hypothesis that returns are equal to that of the

market. We initiate long or short positions after receiving a trigger and replicate the trade

as if we are the insider. If our hypothesis as depicted in Figure 1 is correct, we will then

be able to generate positive returns over and above the market, which acts as the con-

trol group. To quantify the returns, we will build up $1 in the long or short position, and gradually liquidate the position as if we are insiders with full knowledge of the manipu- lación. We use Figure 2 to illustrate the profile of our position. After receiving a bullish trigger on day 0, we commit $0.50 per day on day 1 and day 2 to buy into the stock,

6

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

Cifra 2. Illustration of a long position profile

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

Fuente: Authors’ calculation.

resulting in a long position of $1. Then we hold the position for five days and gradually liquidate a tenth of the long position over the next ten days. F / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . We adopt this method so that we can react the following day once we detect possible in- sider trading. The bullish/bearish triggers under the three different phases are computed differently and likewise our position’s profile (entry/held/liquidation days) are different. Because we use price and volume data, our triggers are not conditional to other corpo- rate events. Por eso, we will be able to capture market rumors as well as corporate events that have and have not materialized. We will use the case when prices are manipulated upward to show the trading profile. f por invitado 0 8 septiembre 2 0 2 3 Because we want to mimic how the insider trades, our trading direction must be in the same direction as the insider. So if we detect upward price manipulation during the Stealth and Awareness phases when the insider is taking a long position, we will also buy the stock but at different speed. As shown in Figure 3, because the Stealth phase is at the early stage of manipulation, we can afford to enter into position slowly, hold it longer, and liquidate our position gradually (see solid line with asterisks). If we only detect 7 Asian Economic Papers Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets Figure 3. Trading profiles depending on when we detect upward price manipulation l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . f por invitado 0 8 septiembre 2 0 2 3 Fuente: Authors’ calculation. Nota: Trading profiles to build up position when we detect upward price manipulation during Stealth (solid line), Awareness (solid line with asterisks) and Liquidation (dashed line) phases. upward price manipulation at the Awareness phase, sin embargo, we will need to get into position quickly, and hold it briefly before clearing off our position (solid line). But if we only manage to detect the upward price manipulation at the liquidation phase when in- siders are exiting the long position, we must quickly take a short position and slowly buy back the stock as we have not bought into the stock previously and we hypothesize that prices will fall (see the dashed line in Figure 3). De este modo, depending on when we manage to detect the upward price manipulation, the trading profiles will be different. The opposite position profile will hold for downward price manipulation. Our testing sample includes all constituents of the major indices from Japan, Australia, South Korea, Taiwán, Singapur, Hong Kong, Malasia, Tailandia, the Philippines, En- donesia, Porcelana, and India.8 This amounts to around 2,010 companies. The data span from 8 The indices, following the sequence of the countries as listed, are respectively: TOPIX 500, S&P/ASX 200, KOSPI 200, MSCI Taiwan, Singapore Straits Times index, Hang Seng Compos- ite Index, Bursa Malaysia KLCI, Thailand SET 50, the Philippines Stock Exchange PSEi (formerly named PSE Composite), Jakarta LQ45, Shanghai/Shenzhen CSI 300, and BSE 200. 8 Asian Economic Papers Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets Table 1. Stealth and awareness phase results Stealth Awareness Awareness, conditional on being detected during Stealth Awareness, conditional on being detected during Stealth—Illicit profits and loss avoidance 60,299 39,209 4,192 4,192 0.84 16.9 30.0 36630 23669 10 5 20 75.64 61.05 300.56 285.20 1.790 2.573 43.74 0.015 0.55 11.0 19.5 24430 14779 1 5 5 25.86 25.40 104.42 98.00 4.466 5.907 107.50 0.016 0.06 1.2 2.1 2886 1306 1 5 5 4.29 3.00 11.21 9.20 7.256 7.946 161.14 0.009 0.06 1.2 2.1 2886 1306 6 10 5 7.74 5.77 20.45 17.27 61.223 53.797 133.63 0.000 Number of triggers % of transaction days Mean triggers per day Mean triggers per stock Long triggers Short triggers Days to enter position Days holding the position Days to liquidate position Mean net position (US$)

Median net position (US$) Mean gross position (US$)

Median gross position (US$) Daily return: significar (bps) median (bps) std deviation (bps) t test p-value Source: Authors’ calculation. Nota: The triggers are generated when the stocks satisfy certain bullish and bearish conditions as described in the main text. We initiate the $1 long/short positions by entering/holding and liquidating the position linearly over days as described. Daily return

is calculated based on the profit divided by the gross exposure (long plus absolute of short). bps = one hundredth of a percent.

1 Enero 1997 a 31 Agosto 2010. Opening prices, closing prices, day’s high, day’s low,

volumen, and market capitalization are sourced from Datastream. We filter our data set to

exclude stocks with market capitalization less than US$ 50m, stocks with average daily volume traded in the past 40 days less than US$ 0.5m, and stocks with closing prices less

than US$ 0.50. The first two filters are to avoid low liquidity and small stocks that can be easily manipulated, and the latter filter avoids low-priced stocks that may suffer from bid–ask bounces. l D o w n o a d e desde h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . 3.1 Stealth phase Unless one is part of the insider syndicate, one cannot know a priori which stock will be manipulated. Por lo tanto, we expect this phase to be the least detectable as the insider will want to build up the long or short position stealthily. Por eso, in a bullish circumstance, the trade volume and opening, alto, bajo, and closing prices for the day are likely to be higher than the mean of the data for the past five days. Although the price return is posi- tivo, to avoid being too obvious and alerting others, the insiders must not buy too aggres- sively. Por eso, the mean past five days’ data are still less than the past 20 days’ data. If all these conditions are fulfilled, then it is a bullish trigger. The reverse conditions apply in a bearish case. f por invitado 0 8 septiembre 2 0 2 3 The first column in Table 1 reports our detection during the Stealth phase. We find that between 1997 y 2010, Había 60,299 (36,630 bullish and 23,669 bearish) triggers where insiders may be stealthily taking long/short positions among the 2,010 companies 9 Asian Economic Papers Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets (acerca de 0.84 percent of the transaction days). Over the period, the mean daily occurrence is across 16.9 companies; the mean occurrence per stock is 30 veces (about twice annually). Because the Stealth phase is at the beginning of stock manipulation, we can afford to build our position slowly and linearly over ten days, and then hold the position for five days before liquidating linearly over 20 días. The first column in Table 1 shows that the median daily gross (long plus absolute short) position held is US$ 285.20, with a bias towards being net long (median of US$ 61.05 a diario). This is unsurprising as we expect insiders can trade easier on a bullish signal and that it is more difficult to manipulate prices downward because there are short sale restrictions—no naked short-selling allowed, short-selling must be pre-borrowed, corto- selling is only allowed for certain stocks, and some markets have only allowed short- selling during the later period of our analysis. Además, Asian markets enjoyed a bull market for a period prior to the 2008–09 global financial crisis. By trading (entering/holding/liquidating the position) in this manner during the Stealth phase, the first column in Table 1 shows that the mean and median daily returns are 1.790 bps and 2.573 bps, respectivamente (1 bps is a hundredth of a percent). The daily return is calculated based on the profit for the day divided by the gross position for the day. To test if the triggers during the Stealth phase will beat our null hypothesis of zero abnormal performance, we also invest the equivalent gross position in the market index, thereby having a benchmark return from the same level of gross exposure, which also acts as our control return. Cifra 4 shows the cumulative profit if we trade using the hypothesized manner by in- siders (black line) and the cumulative profit from the market indices (dashed line). We find that although the triggers generated from our hypothesized manner yield small re- turns (annualized to 4.6 percent per year), they outperform the market cumulatively over the period. 3.2 Awareness phase In this phase, we hypothesize that the price movements have attracted the attention of other participants and they are rebalancing their portfolios accordingly. We expect it to be more detectable than during the Stealth phase. In a bullish case, it is detectable with the opening prices being higher than the previous two days’ and previous day’s open- En g, closing, and high prices. Asimismo, the high and low prices for the day are also higher than the previous two days’ and the previous day’s high and low prices. The closing price is also higher than the mean past five days’ closing price, with the mean of the previous five days’ closing price also being higher than the mean of the previous 20 days’ clos- ing price. The average return over the past five days is also positive. Such optimism is reflected in the volume being 50 percent more than the mean past 20 y 200 days’ vol- ume. The reverse idea applies in a bearish case. 10 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . f por invitado 0 8 septiembre 2 0 2 3 Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets Figure 4. Stealth phase: Cumulative profit and loss from the hypothesized model vs. market return (null hypothesis) l D o w n o a d e desde h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / Fuente: Authors’ calculation. Nota: The dashed line represents the profit and loss cumulated from investing the gross exposure (long plus absolute short) in the mar- ket indices and the black line represents the profit and loss cumulated from taking a long or short position hypothesized to be executed by insiders. / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . The second column in Table 1 shows that there were 39,209 (24,430 bullish and 14,779 bearish) triggers during the 14 years of this study. As we detected this during the Aware- ness phase, we enter our $1 long or short quickly within a day of receiving the signal;

hold it over five days before liquidating linearly over the next five days. Consistent with

our expectation that in the Awareness phase the triggers are more detectable and, albeit

a lower number, they are more informative and generate higher mean and median daily

return (4.466 bps and 5.907 bps respectively; second column in Table 1). The higher re-

doblar, annualized to 12 percent per year, is mainly because the triggers initiate positions

that latch on to the rapid price change during the Awareness phase as shown in Figure 1.

This is also confirmed in Figure 5 where the cumulative profits from our hypothesized in-

sider trading model beat a similar investment in the market indices. Due to fewer triggers,

the second column in Table 1 shows that the capital requirement is lower with the median

daily gross exposure falling to US$ 98.00 and the median daily net long position falling to US$ 25.40 as compared to the Stealth phase.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

11

Asian Economic Papers

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

Cifra 5. Awareness phase: Cumulative profit and loss from the hypothesized model vs. market

return (null hypothesis)

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

Fuente: Authors’ calculation.

Nota: The dashed line represents the profit and loss cumulated from investing the gross exposure (long plus absolute short) in the mar-

ket indices and the black line represents the profit and loss cumulated from taking a long or short position hypothesized to be executed

by insiders.

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

The triggers in the Awareness phase were calculated independent of the triggers dur-

ing the Stealth phase, meaning that the triggers do not consider any detection during the

Stealth phase. We now calculate the triggers in the Awareness phase to be conditional

upon being detected in the Stealth phase as well. Por lo tanto, we would initiate long/short

positions during the Awareness phase only if we have also detected suspicious signals in

the same direction during the Stealth phase.

The third column in Table 1 shows that being stricter in our analysis generates fewer

triggers (4,192 triggers) with lower capital requirement (median daily gross exposure of

US$ 9.20). Sin embargo, the fewer signals are more informative. The mean and median daily return improves to 7.256 bps and 7.946 bps, respectivamente, and outperformed the market (ver figura 6). The significance of this detection is that, an outsider who managed to de- tect the suspicious price activity during the Stealth phase and confirmed it again by the 12 Asian Economic Papers Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets Figure 6. Awareness phase, conditional on being detected during Stealth phase: Cumulative profit and loss from the hypothesized model vs. market return (null hypothesis) l D o w n o a d e desde h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / Fuente: Authors’ calculation. Nota: The dashed line represents the profit and loss cumulated from investing the gross exposure (long plus absolute short) in the mar- ket indices and the black line represents the profit and loss cumulated from taking a long or short position hypothesized to be executed by insiders. / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . suspicious signal during the Awareness phase, can join in, yielding an annualized return of 20 por ciento. Por lo tanto, by combining the information collected in the Stealth and Awareness phases, we believe we are detecting cases where the insider has stealthily taken a position ahead of the dissemination of the price-sensitive rumor or event news, which occurred during the Awareness phase. The third column in Table 1 shows that the frequency of such stock manipulation is low—on average 1.2 cases per day. De este modo, we believe we are focusing on those cases with a higher likelihood of actually being manipulated. f por invitado 0 8 septiembre 2 0 2 3 To get an idea of the potential illicit profits being earned and losses being avoided by the insider on these particular cases, we would initiate the long or short positions as if we are the insiders after we have detected the triggers in the Stealth phase. The last column in Table 1 shows that for these 4,192 casos, the mean and median daily returns increase 13 Asian Economic Papers Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets significantly to 61.223 bps and 53.797 bps, respectivamente. Assuming that the insider adopts a similar trading profile of entering, tenencia, and liquidating the position as we do, this daily return gives an estimate of the illicit profits being earned. A mean daily return of 61.223 bps translates to an annualized return of 366 percent per year. 3.3 Liquidation phase We hypothesize that during this phase, the inside information has become common news and the rumors have been confirmed or denied by the company. The insider believes that the prices have reached the highest or lowest and the stock is now traded actively. Allá- delantero, it is an opportune time to exit with maximum profits and minimal price impact. We detect the end of a bullish case when mean opening, closing, alto, and low prices for the past 40 days are higher than the same previous 100 days’ data, but the mean past 5 days’ data are lower than the mean past 20 days’ data and the day’s data is also lower than the mean previous 5 days’ data. Prices have fallen for the day compared with 5 days ago but remain higher compared with 20 o 40 days ago. Therefore this points to the end of the bull run. The lack of further upward price impetus is also backed up by elevated but diminishing trading activity with the mean five days’ volume being less than 150 por- cent but remain more than 120 percent of the previous 20 days’ volume; and the day’s vol- ume is less than 120 percent of the previous five days’ volume. The reverse idea applies at the end of a bearish case. The first column of Table 2 shows that there were 4,049 triggers (2,330 bullish and 1,719 bearish), with an average of 1.1 triggers per day and two triggers per stock over 14 años. Because insiders are exiting their long positions by selling down, so we must also sell. Ser- cause we only detected the trigger at this point and we do not have a long position, this will result in a short position. Por lo tanto, although receiving a bullish signal, we will initi- ate a short position quickly within a day and gradually buy back the stock over the subse- quent 40 días. Trading this way would yield mean and median returns of −2.638 bps and −0.750 bps, respectivamente. Cifra 7 shows the cumulative profit and loss. The returns are negative, and match the market initially but underperform the market after 2006. Yield- ing a negative return on a short position implies that stock prices have continued to rise. Sin embargo, because it is a small negative return (statistically not significant at 5 percent— see first column in Table 2), it shows that stock prices are not reverting and are plateau- En g. Por eso, we believe that the insiders are likely to have exited almost at the top/bottom of the price cycle. Similar to the earlier analysis in the Awareness phase, we also condition our Liquidation phase triggers to be detected in the Awareness phase; and at the Awareness and in the earlier Stealth phase. The second and third columns of Table 2 show that this will result in fewer triggers (1,362 y 435 triggers, respectivamente) and a largely similar returns profile 14 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . f por invitado 0 8 septiembre 2 0 2 3 Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets l a n o i t i d n o c , n o i t a d i u q i L g n i e b n o l a n o i t i d n o c , n o i t a d i u q i L d n a s s e n e r a w A g n i r u d s t fi o r p t i c i l l I — h t l a e t S e c n a d i o v a s s o l d n a d e t c e t e d g n i e b n o 1 0 . 0 1 . 0 2 . 0 5 3 4 5 1 3 0 2 1 6 2 5 2 0 4 7 6 . 3 0 5 . 1 8 0 . 8 8 3 . 5 2 5 2 . 4 1 9 9 4 . 3 1 0 0 0 . 0 5 1 . 1 3 1 t i c i l l I — s s e n e r a w A g n i r u d d e t c e t e d s s o l d n a s t fi o r p e c n a d i o v a % 2 0 . 0 4 . 0 7 . 0 2 6 3 , 1 0 5 . 7 7 4 . 3 2 6 . 4 2 3 1 . 0 2 2 1 1 . 2 1 4 6 7 . 1 1 8 8 . 5 9 0 0 0 . 0 8 8 8 4 7 4 6 2 5 2 0 4 n o l a n o i t i d n o c d e t c e t e d g n i e b h t l a e t S g n i r u d s s e n e r a w A d n a , n o i t a d i u q i L n o l a n o i t i d n o c d e t c e t e d g n i e b , n o i t a d i u q i L s s e n e r a w A g n i r u d n o i t a d i u q i L s t l u s e r e s a h p n o i t a d i u q i L . 2 e l b a T 2 6 3 , 1 9 4 0 , 4 1 0 . 0 1 . 0 2 . 0 5 3 4 1 0 0 2 1 5 1 3 4 4 . 1 − 0 7 . 0 − 0 4 2 0 . 0 4 . 0 7 . 0 1 0 4 7 4 8 8 8 8 7 . 2 − 3 1 . 1 − 0 4 3 2 . 3 3 1 . 9 3 9 . 1 4 1 7 . 2 − 7 0 1 . 3 − 5 2 . 7 1 6 2 . 3 − 9 8 4 . 4 − 2 1 4 . 0 2 2 . 6 7 1 4 5 1 . 0 8 0 . 9 2 1 4 8 0 . 0 9 7 . 9 8 6 0 . 0 1 . 1 0 . 2 0 8 . 3 8 5 . 2 8 8 . 4 2 1 0 0 4 0 3 3 2 9 1 7 1 3 2 . 9 1 8 3 6 . 0 5 7 . 2 − 0 − k c o t s y a d r e p r e p s r e g g i r t n a e M s r e g g i r t n a e M s y a d n o i t c a s n a r t f o % s r e g g i r t f o r e b m u N s r e g g i r t g n o L s r e g g i r t t r o h S n o i t i s o p e h t g n i d l o h n o i t i s o p e t a d u q i l i o t n o i t i s o p r e t n e o t s y a D s y a D s y a D ) $

S

Ud.

(

norte

oh

i

t

i

s

oh

pag

t

mi

norte

norte

a

i

d

mi

METRO

)

$ S U ( n o i t i s o p s s o r g n a e M ) $

S

Ud.

(

norte

oh

i

t

i

s

oh

pag

t

mi

norte

norte

a

mi

METRO

)

$ S U ( n o i t i s o p s s o r g n a i d e M ) s p b ( n a e m : n r u t e r y l i a D ) s p b ( n o i t a i v e d d t s e u l a v – p t s e t t ) s p b ( n a i d e m . n o i t a l u c l a c ’ s r o h t u A : e c r u o S . ) t r o h s f o e t u l o s b a s u l p g n o l ( e r u s o p x e s s o r g e h t y b d e d i v i d t fi o r p e h t n o d e s a b d e t a l u c l a c s i n r u t e r y l i a D . d e b i r c s e d s a s y a d r e v o y l r a e n i l n o i t i s o p e h t g n i t a d i u q i l d n a g n i d l o h / g n i – r e t n e y b s n o i t i s o p t r o h s / g n o l 1 $

mi

h

t

mi

t

a

i

t

i

norte

i

mi

W.

.

t

X

mi

t

norte

i

a

metro

mi

h

t

norte

i

d

mi

b

i

r

C

s

mi

d

s

a

s

norte

oh

i

t

i

d

norte

oh

C

h

s

i

r

a

mi

b

d

norte

a

h

s

i

yo

yo

tu

b

norte

i

a

t

r

mi

C

y

F

s

i

t

a

s

s

k

C

oh

t

s

mi

h

t

norte

mi

h

w

d

mi

t

a

r

mi

norte

mi

gramo

mi

r

a

s

r

mi

gramo

gramo

i

r

t

mi

h

t

:

mi

t

oh

norte

.

t

norte

mi

C

r

mi

pag

a

F

oh

h

t

d

mi

r

d

norte

tu

h

mi

norte

oh

=

s

pag

b

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

15

Asian Economic Papers

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

Cifra 7. Liquidation phase: Cumulative profit and loss from the hypothesized model vs. market

return (null hypothesis)

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

Fuente: Authors’ calculation.

Nota: The dashed line represents the profit and loss cumulated from investing the gross exposure (long plus absolute short) in the mar-

ket indices and the black line represents the profit and loss cumulated from taking a long or short position hypothesized to be executed

by insiders.

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

(mean of −3.261 bps and −2.714 bps, and statistically not significant). Our results in the

first three columns of Table 2 show that our hypothesized triggers are not successful in

detecting prices falling after being manipulated upwards, nor prices rising after being

manipulated downwards.

The results from Table 2 imply that insiders have already creamed off the best returns,

leaving na¨ıve investors to reap the average 2.638 bps return with a high standard devi-

ación (since the na¨ıve investors would be adopting the opposite trading profile to us).

Además, there are other participants, who are unaware of the price manipulation or suf-

fer from behavioral biases, taking the opposite position to us. Finalmente, it also implies that

detecting turning points in trend using only price and volume data has limited power.

For sake of completeness, using the same cases, we also estimate the illicit profits as if

we know the insider is exiting his position during the Liquidation phase but has entered

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

16

Asian Economic Papers

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

the position during the Awareness or Stealth phases. In an upward price manipulation

caso, the insiders are building long positions during the Awareness or Stealth phases

before exiting during the Liquidation phase. Therefore we mimic this by also build-

ing a long position in the earlier phases and then exiting in the Liquidation phase. Nosotros

therefore need not take the short position when we only detect a suspicious signal at the

Liquidation phase.

Our results in the fourth and fifth columns of Table 2 show that the daily mean / median

returns to be 12.112 bps / 11.764 bps and 14.252 bps / 13.499 bps, respectivamente. These rep-

resent the illicit profits when insiders trade in during the Awareness and Stealth phases,

respectivamente, and trade out during the Liquidation phase as detected purely using the con-

ditions in the Liquidation phase. The returns, though lower compared with the fourth

column in Table 1, still annualizes to a respectable 35 a 43 percent per year.

En resumen, we have shown in this section a certain price pattern that is consistent with

our hypothesis of what an insider or stock manipulator may want to achieve. We show

that if a stock manipulator trades in a similar pattern, he would outperform the market

as well as extract illicit profits or avoid losses that may amount to a mean daily return of

0.61223 por ciento (annualizing to 366 percent per year). For outsiders who managed to de-

tect the suspicious signals at the Stealth and then at the Awareness phase, they can also

extract a mean daily return of 0.07256 por ciento (annualizing to 20 percent per year). Allá-

delantero, it is imperative for regulators to be more alert to the possible price manipulations.

4. Robustness tests

We subject our results to robustness tests in this section. We focus on the Stealth and

Awareness phases, where most of the profits accrue.

4.1 Can our hypothesized model detect such behavior in large and liquid stocks?

A priori, we expect smaller and less liquid stocks to be more easily manipulated. En nuestro

main analysis, we excluded small (market capitalization less than US$ 50m), illiquid (av- erage daily volume in the past 40 days less than US$ 0.5m) and low priced stocks (closing

price less than US$ 0.50). These filters may be insufficient, sin embargo. We therefore re-ran our analysis to focus only on stocks exceeding US$ 500m market capitalization and with

average daily volume in the past 40 days exceeding US$ 5m. Our reduced sample yields results similar to our main findings, albeit with fewer in- stances of possible insider trading. Consistent with expectations, the mean and median daily returns are lower than our main results in Table 1. Sin embargo, we find that the in- siders may still be able to extract significant profits or avoid losses that average 58.535 bps daily (results not shown). An alert outsider who has spotted suspicious trading patterns 17 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / directo . mi t . / e d u a s e p a r t i c e – pd / l f / / / / / 1 4 3 1 1 6 8 4 3 9 4 a s e p _ a _ 0 0 3 6 8 pd . f por invitado 0 8 septiembre 2 0 2 3 Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets in the Stealth and Awareness phases may also be able to enjoy an average 4.867 bps return daily (results not shown). 4.2 Removing the liquidity, tamaño, and price filters because the stocks are constituents of the main benchmark in each country The 12 indices are the flagship/benchmark indices of the respective markets. So to gauge the prevalence of insider trading and stock manipulation throughout Asia and to increase the power of our tests, we do not impose any size and liquidity filters and re-run our analysis. Unreported results from our enlarged sample indicate findings that are stronger and consistent with our main findings in Table 1. 4.3 How much does the market direction affect our conclusion? In our main results in Tables 1 y 2, we notice that the mean net position is positive be- cause there were more long/bullish triggers than short/bearish triggers. Este, coupled with the general upward trend of the markets, may skew our returns upwards and give a false impression of the power of our hypothesized model in detecting stock manipula- ción. We did not neutralize this effect in the main analysis because in most of the markets there are short-sale restrictions and short-selling introduces additional costs and risks to the stock manipulator in a generally upward trending market. Besides, it is also easier to spread positive rumors to manipulate prices upwards. A further justification for not neutralizing the net long exposure is because there are days when only long or only short triggers were detected. On those days, there is no way of neutralizing this effect apart from deleting the triggers, although deletion will eliminate useful information and reduce the power of our analysis. Sin embargo, we re-ran our analysis using market neutral positions. We neutralize the net long (or short) position by proportionally reducing all the long (or short) positions for that day by the amount of the net exposure. Por ejemplo, si, on a certain day, the total long and short positions are $100 y $90 respectivamente, we obtain our market neutral ex-

posure by reducing each long position by 10 por ciento. Our additional tests show that our

main findings remain robust. Adopting strictly a market neutral position (zero net posi-

ción) at all times, our unreported results show that the mean and median daily returns fall

slightly compared with Table 1. This is expected because the overall markets were trend-

ing upwards. Sin embargo, the main crux of our analysis remains.

4.4 Are the results robust to alternative trading profiles (number of entering,

tenencia, and liquidating days)?

We hypothesized that insiders and stock manipulators trade in a certain way and, to esti-

mate the amount of illicit profits or loss avoidance, we create our position with our trad-

ing profile (days entering, tenencia, and liquidating the position). Sin embargo, this profile is

just our conjecture and not all insiders have the same trading style as us. For each column

18

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

of results reported in Tables 1 y 2, we undertook eight alternative trading profiles. Nuestro

unreported results show that although there are alternative trading profiles that would

yield higher returns, our main findings are valid and robust.

5. Conclusión

This paper focuses on insider trading where perpetrators exploit market-sensitive infor-

mation to earn profits or avoid losses. Our paper seeks to examine the detection of possi-

ble insider trading and stock manipulation and react in an almost real time manner, incluso

though this activity is intended to evade market participants and the regulators, así como

to estimate the extent of illicit profits that might have been earned. Finalmente, we also exam-

ine what response, if detection is possible, other market participants should make.

Setting the null hypothesis as the market return, using a hypothesized model based on

how insiders and stock manipulators might trade, we detect price patterns that are con-

sistent with their objective to maximize profits. Using our hypothesized model, nosotros también

estimate that insiders avoid losses and earn profits with a mean daily return of 0.61223

por ciento (annualized to 336 percent per year) and that such insider trading outperforms

the market.

With the lure of such high returns, insider trading and stock manipulation is likely to

continue and market participants have to respond accordingly. Regulators need to de-

vote more resources and support more research work in this area. Unless one is part of

el (ilegal) stock manipulation syndicate, investors can only detect this phenomenon in

the Awareness phase when prices have been moved by the rumors or news, and from

that point respond depending on their level of investment sophistication. Finalmente, compa-

nies have to be more careful in the dissemination of market-sensitive information even to

authorized personnel to avoid information leakage.

Referencias

Alí, Ashiq, Kelsey D. Wei, and Yibin Zhou. 2011. Insider Trading and Option Grant Timing in

Response to Fire Sales (and Purchases) of Stocks by Mutual Funds. Journal of Accounting Research

49(3):595–632.

Badertscher, Brad A., S. Paul Hribar, and Nicole Thorne Jenkins. 2011. Informed Trading and the

Market Reaction to Accounting Restatements. Accounting Review 86(5):1519–1547.

Bris, Arturo. 2005. Do Insider Trading Laws Work? European Financial Management 11(3):267–312.

Brochet, Francois. 2010. Information Content of Insider Trades Before and After the Sarbanes-Oxley

Acto. Accounting Review 85(2):419–446.

Chakravarty, Sugato, Huseyin Gulen, and Stewart Mayhew. 2004. Informed Trading in Stock and

Option Markets. Journal of Finance 59(3):1235–1257.

19

Asian Economic Papers

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Detecting and Quantifying Insider Trading and Stock Manipulation in Asian Markets

Chen, Bo, and Yuen Pau Woo. 2010. Measuring Economic Integration in the Asia-Pacific Region: A

Principal Components Approach. Asian Economic Papers 9(2):121–143.

Ke, Papelera, Steven Huddart, and Kathy Petroni. 2003. What Insiders Know About Future Earnings and

How They Use It: Evidence from Insider Trades. Journal of Accounting & Ciencias económicas 35(3):315–346.

Rey, Michael R. 2009. Prebid Run-Ups Ahead of Canadian Takeovers: How Big Is the Problem?

Financial Management 38(4):699–726.

Korczak, Adriana, Piotr Korczak, and Meziane Lasfer. 2010. To Trade or Not to Trade: The Strate-

gic Trading of Insiders Around News Announcements. Journal of Business Finance & Accounting

37(3/4):369–407.

Lakonishok, Josef, and Inmoo Lee. 2001. Are Insider Trades Informative? Review of Financial Studies

14(1):79.

Liu, Ningyue, Liming Wang, and Min Zhang. 2013. Corporate Ownership, Political Connections and

METRO&A: Empirical Evidence from China. Asian Economic Papers 12(3):41–57.

Meulbroek, Lisa K., and Carolyn Hart. 1997. The Effect of Illegal Insider Trading on Takeover Pre-

mia. European Finance Review 1(1):51–80.

Tverski, Amos, and Daniel Kahneman. 1992. Advances in Prospect Theory: Cumulative Representa-

tion of Uncertainty. Journal of Risk & Incertidumbre 5(4):297–323.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

mi

d

tu

a

s

mi

pag

a

r

t

i

C

mi

–

pag

d

/

yo

F

/

/

/

/

/

1

4

3

1

1

6

8

4

3

9

4

a

s

mi

pag

_

a

_

0

0

3

6

8

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

8

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

20

Asian Economic Papers