TRADE AND UNCERTAINTY

Dennis Novy and Alan M. Taylor*

Abstract—We offer a new explanation as to why international trade is so

volatile in response to economic shocks. Our approach combines the idea of

uncertainty shocks with international trade. Firms order inputs from home

and foreign suppliers. In response to an uncertainty shock firms dispro-

portionately cut orders of foreign inputs due to higher fixed costs. Im

aggregate, this leads to a bigger contraction in international trade flows

than in domestic activity, a magnification effect. We confront the model

with newly compiled US import and industrial production data. Our results

help to explain the Great Trade Collapse of 2008–2009.

ICH.

Einführung

THE recent global economic crisis saw an unusually large

and rapid decline in output across the world. Yet even

more striking, the accompanying decline in international

trade volumes was sharper still and almost twice as big.

Globally, industrial production fell 12% and trade volumes

fell 20% in the twelve months from April 2008, shocks

of a magnitude not witnessed since the Great Depression

(Eichengreen & O’Rourke, 2010). Just as the causes of the

trade collapse in the 1930s are hotly disputed to this day,

so too, we think, the recent reprise will be an object of de-

bate by economists for years to come. Warum? Already one

clear reason stands out: standard models of international

trade and macroeconomics fail to account for the severity

of the events in 2008–2009 now known as the Great Trade

Collapse.

As we explain in the next section, it is quite easy for these

models—based on standard first-moment shocks, which we

do not deny are clearly in operation—to explain why trade

falls in proportion to output, or demand. But without the

addition of auxiliary arguments based on the composition

Received for publication June 16, 2016. Revision accepted for publication

Mai 1, 2019. Editor: Amit K. Khandelwal.

∗Novy: University of Warwick and CEPR; Taylor: University of Califor-

nia, Davis; NBER and CEPR.

We thank the Souder Family Professorship at the University of Virginia,

the Center for the Evolution of the Global Economy at the University of

Kalifornien, Davis, the Economic and Social Research Council (ESRC grant

ES/P00766X/1) and the Centre for Competitive Advantage in the Global

Economy (CAGE, ESRC grant ES/L011719/1) at the University of Warwick

for financial support. Travis Berge and Jorge F. Chavez provided valuable

research assistance. We thank Ian Dew-Becker and Robert Feenstra for shar-

ing data with us. We thank the editor and three anonymous referees for con-

structive comments. We thank Nicholas Bloom for helpful conversations.

We are also grateful for comments by Nuno Limão, Giordano Mion, Veron-

ica Rappoport, and John Van Reenen, as well as seminar participants at the

2011 Econometric Society Asian Meeting, Die 2011 Econometric Society

North American Summer Meeting, Die 2011 LACEA-LAMES Meetings,

Die 2012 CAGE/CEP Workshop on Trade Policy in a Globalised World,

Die 2013 Economic Geography and International Trade Research Meeting,

the NBER ITI Spring Meeting 2013, Die 2013 CESifo Global Economy

Conference, Die 2013 Stanford Institute for Theoretical Economics Sum-

mer Workshop on the Macroeconomics of Uncertainty and Volatility, Die

Monash-Warwick Workshop on Development Economics, Boston College,

LSE, Nottingham, Oxford, Penn State, the University of Hong Kong and

Warwick. All errors are ours.

A supplemental appendix is available online at http://www.mitpress

journals.org/doi/suppl/10.1162/rest_a_00885.

of trade—plus a theory as to why some components fall

disproportionately—such models cannot easily explain why

trade typically falls roughly twice as much as GDP in mas-

sive downturn episodes like the post-2008 years or the early

1930S.

In diesem Papier, we examine why international trade is so

much more volatile in response to economic shocks. And

rather than assuming composition effects, we provide a the-

ory as to why some components of trade are more volatile than

Andere. On the theoretical side, we combine the uncertainty

shock concept due to Bloom (2009) with a model of interna-

tional trade. This real options approach is motivated by high-

profile events that trigger an increase in uncertainty about

the future path of the economy, Zum Beispiel, Die 9/11 terror-

ist attacks or the collapse of Lehman Brothers. In the wake

of such events, firms adopt a wait-and-see approach, slowing

their hiring and investment activities. Bloom shows that bouts

of heightened uncertainty can be modeled as second-moment

shocks to demand or productivity and that these events typi-

cally lead to sharp recessions. Once the degree of uncertainty

subsides, firms revert to their normal hiring and investment

patterns and the economy recovers.

We bring the uncertainty shock approach into an open

economy. Unlike the previous closed-economy setup, ours

is a theoretical framework in which firms import nondurable

(Material) and durable (capital) inputs from foreign and do-

mestic suppliers. This structure is motivated by the observa-

tion that a large fraction of international trade now consists of

goods such as industrial machinery or capital goods, a feature

of the global production system that has taken on increas-

ing importance in recent decades.1 In the model we develop,

due to fixed costs of ordering associated with transportation,

firms hold an inventory of inputs, but the ordering costs are

larger for foreign inputs. Following Hassler’s (1996) inven-

tory model with time-varying uncertainty, we show that in

response to a large uncertainty shock in business conditions,

whether to productivity or the demand for final products,

firms optimally execute their inventory policy by cutting or-

ders of foreign inputs much more than for domestic inputs.

Somit, in the aggregate, this differential response leads to

a bigger contraction and subsequently a stronger recovery

in international trade than in domestic trade—that is, trade

exhibits more volatility. In a nutshell, uncertainty shocks

1Sehen, Zum Beispiel, Campa and Goldberg (1997), Feenstra and Hanson

(1999), Eaton and Kortum (2001), and Engel and Wang (2011). The World

Bank WITS database reports that in 2014, capital goods made up 31% von

global trade, compared to 33% for consumer goods, 21% for intermediate

goods, Und 11% for raw materials. Levchenko, Lewis, and Tesar (2010)

stress that sectors with goods used as intermediate inputs experienced sub-

stantially bigger drops in international trade during the Great Recession.

Likewise, Bems, Johnson, and Yi (2011) confirm the important role of

trade in intermediate goods.

The Review of Economics and Statistics, Oktober 2020, 102(4): 749–765

© 2019 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. Veröffentlicht unter einer Creative Commons Namensnennung 4.0

International (CC BY 4.0) Lizenz.

https://doi.org/10.1162/rest_a_00885

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

R

e

S

T

_

A

_

0

0

8

8

5

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

750

THE REVIEW OF ECONOMICS AND STATISTICS

magnify the response of international trade, given the dif-

ferential cost structure.

of the unusually large decline in trade in 2008–2009 was in

response to this spike in uncertainty.2

This is a new prediction that has never been tested be-

Vordergrund, or even proposed, but we show that it is matched by

the data. On the empirical side, we confront the model with

high-frequency monthly US import and industrial production

Daten, some new and hand-collected, going back to 1962. Unser

results suggest a tight link between uncertainty shocks and

the cyclical behavior of international trade when we employ

an identical VAR empirical framework to the one pioneered

by Bloom (2009) but applied here to trade as well as output

Daten. Konkret, we find that imports respond negatively,

and in a statistically significant way, and more than output,

when there is a shock to a standard uncertainty measure: Die

VXO stock market option-implied volatility index.

We can further show that our proposed model generates

a wider array of additional and original testable predictions,

which we also take to the data and test in this paper. The mag-

nification effect should be muted for industries characterized

by high depreciation rates. Nondurable goods are a case in

Punkt. The fact that such goods have to be ordered frequently

means that importers have little choice but to keep ordering

them even if uncertainty rises. Umgekehrt, durable goods can

be seen as representing the opposite case of very low depre-

ciation rates. Our model predicts that for those goods, Wir

should expect the largest degree of magnification in response

to uncertainty shocks. Intuitively, the option value of waiting

is most easily realized by delaying orders for durable goods.

We find strong evidence of this pattern in the data when we

examine the cross-industry response of imports to uncertainty

shocks using US disaggregated monthly trade data, also a first

result of its kind.

We stress that the magnification effect is in operation

within industries by varying extent as predicted by the model.

Using disaggregated data, we find that the effect is strongest

in the durable and capital goods sectors and weak to nonex-

istent in other sectors. Our results are therefore not driven by

composition effects—that is, they arise not merely from the

fact that international trade is heavier in durable goods.

To wrap up, we show how our proposed mechanism helps

to quantitatively explain a part of the Great Trade Collapse

of 2008–2009. We use the VAR model in a simulation exer-

cise and impose shocks that reproduce the exceptional rise in

uncertainty in 2008 (from the subprime crisis to the collapse

of Lehman Brothers). Using standard Cholesky ordering to

ensure identification of the response in the trade equation

to an uncertainty shock while simultaneously controlling for

first-moment shocks to business conditions proxied by em-

ployment, we show empirically that second-moment shocks

have a sizable and independent effect on trade. The result

holds also for just the exogenous shocks (terror/war/oil) Das

Bloom (2009) identified. Crucially, using disaggregated data,

we can show that these uncertainty effects are concentrated in

exactly the traded sectors needed to match the compositional

variation seen in the trade collapse. The results suggest that if

we place a lot of emphasis on uncertainty shocks, up to half

Daher, the recent downturn is qualitatively quite comparable

to previous postwar contractions in international trade and

can be modeled similarly. Tatsächlich, we think that our approach

may advance our understanding of trade contractions and

volatility over the long run, not only during the Great Trade

Collapse.

The paper is organized as follows. In section II, we re-

view the literature. In sections III, IV, and V, we outline our

theoretical model, do comparative statics, and present simu-

lation results. Section VI presents our empirical evidence. In

section VII we ask to what extent uncertainty shocks can em-

pirically account for the recent Great Trade Collapse. Abschnitt

VIII concludes. We also provide a detailed online appendix.

II. The Literature on the Great Trade Collapse

Departing from conventional static trade models, wie zum Beispiel

those based on the gravity equation, our paper focuses on

the dynamic response of international trade. The novelty is

that shocks to the volatility of idiosyncratic disturbances (d.h.,

second-moment shocks) can be the driver of very different

changes in imported and domestic inputs. Previous theoret-

ical and empirical work has almost exclusively focused on

first-moment shocks, such as to productivity, exchange rates,

or trade costs. Our approach is relevant for researchers and

policymakers alike who seek to understand the crash and re-

covery process in response to the Great Recession, and it may

also be relevant for understanding historical events like the

Great Depression. It could also help account for the response

of international trade in future economic crises.

We are not the first authors to consider uncertainty and

real option values in the context of international trade, Aber

so far the literature has not focused on uncertainty shocks.

Zum Beispiel, Baldwin and Krugman (1989) adopt a real op-

tions approach to explain the hysteresis of trade in the face

of large exchange rate swings, but their model features only

standard first-moment shocks. More recently, the role of un-

certainty has attracted new interest in the context of trade pol-

icy and trade agreements (Handley, 2014; Handley & Limão,

2015; Limão & Maggi, 2015). Closer to our approach, in in-

dependent and contemporaneous work, Taglioni and Zavacka

(2012) empirically investigate the relationship between un-

certainty and trade for a panel of countries using quarterly as

opposed to monthly data. But they do not provide a theoretical

mechanism and do not speak to variation across industries.3

2Ähnlich, Bloom, Bond, and Van Reenen (2007) provide empirical ev-

idence that fluctuations in uncertainty can lead to quantitatively large ad-

justments of firms’ investment behavior.

3While Bloom (2009) considers US domestic data, Carrière-Swallow and

Céspedes (2013) consider domestic data on investment and consumption

across forty countries and their response to uncertainty shocks. Gourio,

Siemer, and Verdelhan (2013) examine the performance of G7 countries in

response to heightened volatility. None of these papers consider interna-

tional trade flows.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

R

e

S

T

_

A

_

0

0

8

8

5

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

TRADE AND UNCERTAINTY

751

The Great Trade Collapse of 2008–2009 has been docu-

mented by many authors (see Baldwin, 2009, for a collection

of approaches, and Bems, Johnson, & Yi, 2013, for a survey).

Eaton et al. (2016) develop a structural model of interna-

tional trade where the decline in trade is attributed to various

combined first-moment shocks, in particular a decline in the

efficiency of investment in durable manufactures, a collapse

in the demand for tradable goods, and an increase in trade

frictions.4 They find that the first explains the majority of de-

clining trade. Our approach is different in that the collapse in

demand is generated by a second-moment uncertainty shock,

and we can endogenize the differential response across sec-

tors. Firms react to the uncertainty by adopting a wait-and-see

Ansatz, and we do not require first-moment shocks or an

increase in trade frictions to account for the excess volatility

of trade.

Our approach is consistent with the view that trade fric-

tions did not materially change in the recent crisis. Evenett

(2010) and Bown (2011) find that protectionism was con-

tained during the Great Recession. This view is underlined

by Bems et al. (2013). More specifically, Kee, Neagu, Und

Nicita (2013) find that less than 2% of the Great Trade Col-

lapse can be explained by a rise in tariffs and antidumping

duties. Bown and Crowley (2013) find that compared to pre-

vious downturns, during the Great Recession governments

notably refrained from imposing temporary trade barriers

against partners that experienced economic difficulties.

Amiti and Weinstein (2011) and Chor and Manova (2012)

highlight the role of financial frictions and the drying up of

trade credit. Jedoch, based on evidence from Italian manu-

facturing firms, Guiso and Parigi (1999) show that the nega-

tive effect of uncertainty on investment cannot be explained

by liquidity constraints. We do not incorporate credit fric-

tions here, but such mechanisms may be complementary

to our approach, and we do not rule out a role for other

mechanisms.

As Engel and Wang (2011) point out, the composition of

international trade is tilted toward durable goods. Building

a two-sector model in which only durable goods are traded,

they can replicate the higher volatility of trade relative to

general economic activity. Im Gegensatz, we relate the excess

volatility of trade to inventory adjustment in response to un-

certainty shocks. As this mechanism applies within an in-

dustry, compositional effects do not drive the volatility of

international trade in our model.

Our paper is also related to Alessandria, Kaboski, Und

Midrigan (2010A, 2011) who rationalize the decline in inter-

national trade by changes in firms’ inventory behavior driven

by a first-moment supply shock and procyclical inventory in-

vestment (Ramey & Westen, 1999). Im Gegensatz, we focus on the

role of increased uncertainty when second-moment shocks

are the driver of firms’ inventory adjustments. In our US data,

heightened uncertainty stands out as a defining feature of the

Great Recession, and we employ an observable measure of it.

Jedoch, as we show, there is little evidence in the US data

of a major first-moment TFP shock coincident with the onset

der Krise.

Endlich, Alessandria et al. (2015) model second-moment

shocks, but their framework does not have inventory. As far

as we are aware, ours is the first paper to jointly model inven-

tory holdings and uncertainty shocks in one framework. Un-

like in our paper, a second-moment shock in Alessandria et al.

(2015) is a shock to the variance of the heterogeneous pro-

ductivity distribution. They find that trade rises in response to

a second-moment shock. This result is driven by the differen-

tial impact of the rising productivity dispersion on exporters

versus nonexporters. Intuitively, exporters tend to be at the

upper tail of the productivity distribution. Increases in the

dispersion of productivity shocks thus confer an even greater

advantage to exporters compared to nonexporters.5 This is

different from our setting, where the probability of getting

hit by a shock changes symmetrically for all firms, und Handel

falls in response to a second-moment shock.

III. A Model of Trade with Uncertainty Shocks

We adopt Hassler’s (1996) setting of investment under un-

certainty and embed it into a model of trade in capital inputs.

We then introduce second-moment uncertainty shocks.

Hassler’s (1996) model starts from the well-established

premise that uncertainty has an adverse effect on investment.

In our setup, we model investment as firms’ investing in in-

ventory of capital inputs required for production. Due to fixed

costs of ordering, firms build up an inventory that they run

down over time and replenish at regular intervals. Some in-

puts are ordered domestically, and others are imported from

abroad. Daher, we turn the model into an open economy.

Zusätzlich, firms will face uncertainty over “business con-

ditions” (using Bloom’s terminology), which means they

experience unexpected fluctuations in productivity or de-

mand, oder beides. What’s more, the degree of uncertainty varies

im Laufe der Zeit. Firms might therefore enjoy periods of calm

when business conditions are relatively stable, or they might

have to weather uncertainty shocks that lead to a volatile

business environment characterized by large fluctuations.

Gesamt, this formulation allows us to model the link between

production, international trade, and shifting degrees of uncer-

tainty. Hassler’s (1996) key innovation is to formally model

how changes in uncertainty influence investment. His model

therefore serves as a natural starting point for our analysis of

uncertainty shocks.

4Leibovici and Waugh (2019) show that the increase in implied trade

frictions can be rationalized by a model with time-to-ship frictions such

that agents need to finance future imports upfront (similar to a cash-in-

advance technology) and become less willing to import in the face of a

negative income shock.

5As Alessandria et al. (2015) recognize, they uncover “a puzzle for the

standard business cycle model used to understand micro-level trade dynam-

ics: Increases in firm-level dispersion lead to large increases in trade rather

than the steep declines typically observed during recessions.”

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

R

e

S

T

_

A

_

0

0

8

8

5

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

752

THE REVIEW OF ECONOMICS AND STATISTICS

A. Production and Demand

Each firm has a Cobb-Douglas production function,

F (A, KD, KF ) = AK α

DK 1−α

F

,

(1)

where A is productivity, KD is a capital input sourced domes-

tically, and KF is a capital input sourced from foreign sup-

pliers. We assume that KD and KF are differentiated through

the Armington assumption so that firms need to import both

types. These capital inputs depreciate at rate δ (so “durable”

would map to low δ, “nondurable” to high δ). Each firm faces

isoelastic demand Q for its output, with elasticity σ, so that

Q = BP−σ,

(2)

where B is a demand shifter. As we focus on the firm’s short-

run behavior, we assume that the firm takes the prices of the

production factors as given and serves the demand for its

product.6 We thus adopt a partial equilibrium approach to

keep the model tractable.

B.

Inventory and Trade

The factors KD and KF are capital inputs—say, special-

ized machinery from domestic and foreign suppliers. Later

An, in our empirical trade and production data at the four-

digit industry level, examples include electrical equipment;

engines, turbines, and power transmission equipment; com-

munications equipment; and railroad rolling stock. We can

consider the firm described in our model as ordering a mix

of such products.7

Since the inputs depreciate, the firm has to reorder them

once in a while. Because the firm has to pay a fixed cost

of ordering per shipment, it stores the inputs as inventory

and follows an s, S inventory policy. Scarf (1959) zeigt, dass

in the presence of such fixed costs of ordering, an s, S pol-

icy is an optimal solution to the dynamic inventory problem.

Ordering inputs leads to domestic trade flows and imports,

jeweils. We assume that ordering foreign inputs is asso-

ciated with higher fixed costs compared to domestic inputs,

0 < fD < fF . This assumption is consistent with evidence by

Kropf and Sauré (2014), who show that fixed costs per ship-

ment are strongly correlated with shipping distance, and they

are substantially higher between countries speaking different

6We do not model monetary effects and prices. This modeling strategy is

supported by the empirical regularity documented by Gopinath, Itskhoki,

and Neiman (2012) showing that prices of differentiated manufactured

goods (both durables and nondurables) barely changed during the Great

Trade Collapse of 2008–2009. They conclude that the sharp decline in the

value of international trade in differentiated goods was “almost entirely a

quantity phenomenon.” In contrast, prices of nondifferentiated manufac-

tures decreased considerably. In the empirical part of the paper we most

heavily rely on differentiated products. For a sample that also includes non-

US countries, Haddad, Harrison, and Hausman (2010) find some evidence

of rising manufacturing import prices, consistent with the hypothesis of

supply-side frictions such as credit constraints.

7This setup is related to a situation where inventories are seen as a factor

of production (Ramey, 1989).

languages and not sharing a free trade agreement. Otherwise,

we treat the two types of fixed costs in the same way.8

Given the input prices, the Cobb-Douglas production func-

tion, equation (1), implies that the firm’s use of KD and KF

is proportional to output Q regardless of productivity and de-

mand fluctuations. Similar to Hassler (1996), we assume that

the firm has target levels of inputs to be held as inventory,

denoted by M∗

F , which are proportional to both Q, as

well as KD and KF , respectively. Thus, we can write

D and M∗

m∗

D

= cD + q,

(3)

≡ ln(M∗

where cD is a constant, m∗

D) denotes the log inven-

D

tory target, and q ≡ ln(Q) denotes log output. Grossman and

Laroque (1990) show that such a target level can be rational-

ized as the optimal solution to a consumption problem in the

presence of adjustment costs.9 In our context, the target level

can be similarly motivated if it is costly for the firm to adjust

its level of production up or down. An analogous equation

holds for m∗

F , but, for simpler notation, we drop the D and F

subscripts from now on.

We follow Hassler (1996) in modeling the dynamic inven-

tory problem. In particular, we assume a quadratic loss func-

tion that penalizes deviations z from the target m∗ as 1

2 z2 with

z ≡ m − m∗. Note that the loss function is specified in loga-

rithms such that when expressed in levels, negative deviations

from the target are relatively more costly. Losses associated

with negative deviations could be seen as the firm’s desire to

avoid a stockout. Losses associated with positive deviations

could be seen as a desire to avoid excessive storage costs. We

refer to the theory appendix where we discuss stockout avoid-

ance in more detail and introduce an asymmetric loss function

based on Elliott, Komunjer, and Timmermann (2005).

Clearly, in the absence of ordering costs, the firm would

choose to continuously set m equal to the target m∗, with 0

deviation. However, since we assume positive ordering costs

( f > 0), the firm faces a trade-off: balancing the fixed costs,

on the one hand, and the costs of deviating from the target, An

the other. Changes in inventory are brought about whenever

the firm pays the fixed costs f to adjust m.10

We solve for the optimal solution to this inventory problem

subject to a stochastic process for output q. The optimal con-

trol solution can be characterized in the following way: Wann

the deviation of inventory z reaches a lower trigger point s,

8Guided by the empirical evidence on the importance of adjustment

through the intensive margin (Behrens, Corcos, & Mion, 2013; Bricon-

gne et al., 2012), we do not model firms’ switching from a foreign to a

domestic supplier, or vice versa. As we discuss in section V, this would

arguably reinforce the negative impact of uncertainty shocks on imports.

9In their model, consumers have to decide how much of a durable good

they should hold given that they face fluctuations in their wealth. Adjustment

is costly due to transaction costs. Under the assumption of the consumers’

utility exhibiting constant relative risk aversion, the optimal amount of the

durable good turns out to be proportional to their wealth.

10As an alternative interpretation, we could also regard the firm’s problem

as a capital investment problem. The firm faces a fixed adjustment cost due

to the ordering costs and a quadratic penalty for deviating in investment

from the target. This interpretation is more closely in line with Engel and

Wang (2011).

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

R

e

S

T

_

A

_

0

0

8

8

5

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

TRADE AND UNCERTAINTY

753

the firm orders the amount φ so that the inventory rises to a

return point of deviation S = s + Phi. 11 Formally, we can state

the problem as follows:

(cid:4)

(cid:5)

(cid:6)

(cid:2)

(cid:3) ∞

e−rt

1

2

z2

T

+ It f

dt

,

(4)

min

{Es ,zt }∞

0

E0

0

subject to

z0 = z;

(cid:7)

zt+dt =

(cid:7)

frei

zt − δdt − dq otherwise;

if mt is adjusted,

It dt =

1 if mt is adjusted,

0 ansonsten.

It is a dummy variable that takes the value 1 whenever the

firm adjusts mt by paying f , r > 0 is a constant discount

rate, and δ > 0 is the depreciation rate for the input so that

dKt /K = δdt. Note that the input depreciates only if used in

production, not if it is merely in storage as inventory.

C. Business Conditions with Time-Varying Uncertainty

Due to market clearing, output can move due to shifts in

productivity A in equation (1) or demand B in equation (2).

We refer to the combination of supply and demand shifters

as business conditions. Konkret, we assume that output q

follows a stochastic marked point process that is known to

the firm. With an instantaneous probability λ/2 per unit of

time and λ > 0, q shifts up or down by the amount ε:

⎧

⎪⎨

⎪⎩

qt+dt =

qt + ε with probability (λ/2)dt,

with probability 1 − λdt,

qt

qt − ε with probability (λ/2)dt.

(5)

The shock ε can be interpreted as a sudden change in business

Bedingungen. Through the proportionality between output and

the target level of inventory embedded in equation (3), a shift

in q leads to an updated target inventory level m∗. Following

Hassler (1996), we assume that ε is sufficiently large such

that it becomes optimal for the firm to adjust m.12 That is,

a positive shock to output increases m∗ sufficiently to lead

to a negative deviation z that reaches below the lower trigger

11Das ist, in full notation, we have sD, SD, φD for domestic inputs and sF ,

SF , φF for foreign inputs.

12Hassler (1996, Sek. 4) reports that relaxing the large shock assumption,

while rendering the model more difficult to solve, appears to yield no qual-

itatively different results. Choosing different values for ε does not affect

our simulation results in section V as long as ε is sufficiently large to trig-

ger adjustment. The reason is that in the aggregate across many firms, Die

idiosyncratic shocks wash out to 0. We note that the shock is permanent,

but the frequency with which the firm gets hit by the shock is subject to a

stochastic transition process as given in expression (6). We are not aware

of evidence in this context as to whether firms get predominantly hit by

transitory or permanent shocks.

point s. Infolge, the firm restocks m . Vice versa, a negative

shock reduces m∗ sufficiently such that z reaches above the

upper trigger point and the firm destocks m.13 Thus, to keep

our model tractable, we allow the firm to both restock and

destock depending on the direction of the shock.

The process of equation (5) has a first moment equal to 0

and constant, independent of ε. In what follows, we hold ε

fixed. Daher, the arrival rate of shocks λ is the main measure

of uncertainty and will be our key parameter of interest. It de-

termines the second moment of shocks. We interpret changes

in λ as changes in the degree of uncertainty. Note that λ

determines the frequency of shocks, not their size. Higher

uncertainty here does not mean an increased probability of

larger shocks.

Konkret, as the simplest possible setup, we follow Has-

sler (1996) by allowing an indexed level of uncertainty λω to

switch stochastically between two states ω ∈ {0, 1}: a state

of low uncertainty λ0 and a state of high uncertainty λ1 with

λ0 < λ1. The transition of the uncertainty states follows a

Markov process,

(cid:7)

ωt+dt =

ωt with probability 1 − γωdt,

ωt with probability γωdt,

(6)

where ωt = 1 if ωt = 0, and vice versa. The probability of

switching the uncertainty state in the next instant dt is there-

fore γωdt, with the expected duration until the next switch

given by γ−1

ω .

Below, when we calibrate the model, we will choose pa-

rameter values for λ0, λ1, γ0, and γ1 that are consistent

with uncertainty fluctuations as observed over the past few

decades.14 We assume the firm knows the parameters of the

stochastic process described by equations (5) and (6) and

takes them into account when solving its optimization prob-

lem (4).

The theory appendix shows how the Bellman equation for

the inventory problem can be set up and how the system can

be solved. We have to use numerical methods to obtain values

for the four main endogenous variables of interest: the bounds

s0 and S0 for the state of low uncertainty λ0 and the bounds

s1 and S1 for the state of high uncertainty λ1.

IV. Time-Varying Uncertainty and Firm

Inventory Behavior

The main purpose of this section is to explore how the

firm endogenously changes its s, S bounds in response to

13To keep the exposition concise, we do not explicitly describe the upper

trigger point, and focus on the lower trigger point s and the return point S.

But it is straightforward to characterize the upper trigger point.

14Overall, the stochastic process for uncertainty is consistent with Bloom

(2009). In his setting, uncertainty also switches between two states (low

and high uncertainty) with given transition probabilities. But he models

uncertainty as the time variation of the volatility of a geometric random

walk.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

754

THE REVIEW OF ECONOMICS AND STATISTICS

increased uncertainty. Our key result is that the firm lowers

the bounds in response to increased uncertainty. In addition,

we are interested in comparative statics for the depreciation

rate δ and the fixed cost of ordering f . As just explained,

the model cannot be solved analytically, so we use numerical

methods.

A. Parameterizing the Model

We choose the same parameter values for the interest

rate and rate of depreciation as Bloom (2009): r = 0.065

and δ = 0.1 per year. The interest rate value corresponds

to the long-run average for the US firm-level discount rate.

Based on data for the US manufacturing sector from 1960 to

1988, Nadiri and Prucha (1996) estimate depreciation rates

of 0.059 for physical capital and 0.12 for R&D capital. As

reported in their paper, those are somewhat lower than esti-

mates by other authors. We therefore take δ = 0.1 as a rea-

sonable baseline, although NIPA-based estimates are usually

lower.

For the stochastic uncertainty process described by equa-

tions (5) and (6), we choose parameter values that are con-

sistent with Bloom’s (2009) data on stock market volatility.

In his table II, he reports that an uncertainty shock has an

average half-life of two months. This information can be ex-

pressed in terms of the transition probabilities in equation (6)

with the help of a standard process of exponential decay for

a quantity Dt :

Dt = D0 exp(−gt ).

12 years yields a rate of decay g = 4.1588

Setting t equal to 2

for Dt to halve. The decaying quantity Dt in that process

can be thought of as the number of discrete elements in a

certain set. We can then compute the average length of time

that an element remains in the set. This is the mean lifetime

of the decaying quantity, and it is simply given by g−1. It

corresponds to the expected duration of the high-uncertainty

state, γ−1

1 , which is then given by 4.1588−1 = 0.2404 years

(88 days) with γ1 = g = 4.1588.

Bloom (2009) furthermore reports a frequency of sev-

enteen uncertainty shocks in 46 years. Hence, an uncer-

= 2.7059 years.

tainty shock arrives on average every 46

17

Given the duration of high-uncertainty periods from above,

in our model this would imply an average duration of low-

uncertainty periods of 2.7059 − 0.2404 = 2.4655 years. It

follows from this that γ0 = 2.4655−1 = 0.4056.

The uncertainty term λdt in the marked point process,

equation (5), indicates the probability that output is hit in

the next instant by a supply or demand shock that is suffi-

ciently large to shift the target level of inventory. Thus, the

expected length of time until the next shock is λ−1. It is diffi-

cult to come up with an empirical counterpart of the frequency

of such shocks since they are unobserved. For the baseline

level of uncertainty, we set λ0 = 1, which implies that the

target level of inventory is adjusted on average once a year.

This value can therefore be interpreted as an annual review

of inventory policy.

However, we point out here that our results are not partic-

ularly sensitive to the λ0 value. In our baseline specification,

we follow Bloom (2009, table II) by doubling the standard

deviation of business conditions in the high-uncertainty state.

This corresponds to λ1 = 4.15 In the comparative statics be-

low, we also experiment with other values for λ1. An uncer-

tainty shock is defined as a sudden shift from λ0 to λ1, with

the persistence of the high-uncertainty state implied by γ1.

Finally, we need to find an appropriate value for the fixed

costs of ordering, fF and fD. Based on data for a US steel

manufacturer, Alessandria, Kaboski, and Midrigan (2010b)

report that “domestic goods are purchased every 85 days,

while foreign goods are purchased every 150 days.” To match

the behavior of foreign import flows, we set fF to ensure

that the interval between orders is on average 150 days in

the low-uncertainty state.16 This implies fF = 0.00005846

as our baseline value. Matching the interval of 85 days for

domestic flows would imply fD = 0.00001057. These fixed

costs differ by a large amount (by a factor of about 5.5), and

that difference might seem implausibly large. However, in

the theory appendix, we show that quantitatively, we can still

obtain large declines in trade flows in response to uncertainty

shocks even with values for fF that are not so high as in this

baseline specification. That is, we are able to obtain a large

decline in trade flows for a ratio of fF / fD that is lower than

implied by the above values and might be considered more

realistic.

B. A Rise in Uncertainty

Given the above parameter values, we solve the model

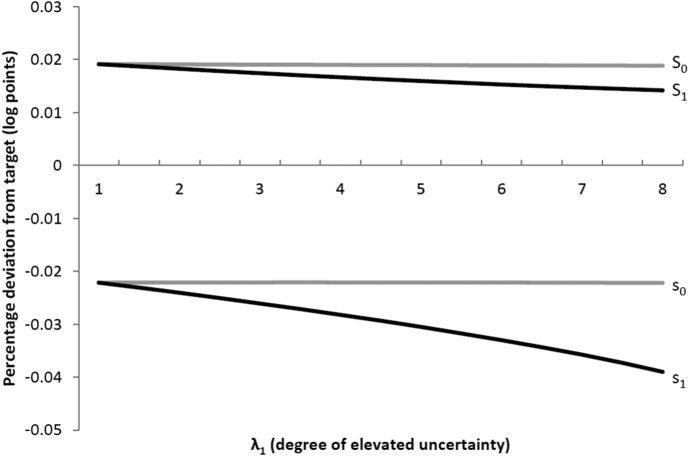

numerically. Figure 1 illustrates the change in s, S bounds in

response to rising uncertainty. The vertical scale indicates the

percentage deviation from the target m∗. Note that there are

two sets of s, S bounds: one set for the low-uncertainty state

0 and the other for the high-uncertainty state 1. The level

of low uncertainty is fixed at λ0 = 1, but the level of high

uncertainty λ1 varies on the horizontal axis (as our baseline

value, we will use λ1 = 4 in later sections). At λ0 = λ1 = 1,

the bounds for the two states coincide, by construction. As

the s, S bounds are endogenous, all of them in principle shift

15For a given λ, the conditional variance of process (5) is proportional

to λ so that the standard deviation is proportional to the square root of

λ. Thus, we have to quadruple λ0 to double the standard deviation. This

parameterization is also consistent with Bloom et al. (2018, table V). They

roughly double the standard deviation in the high-uncertainty state at the

aggregate level. They more than triple it based on an idiosyncratic shock

process and microlevel data. But since there are no idiosyncratic shocks in

our model, we prefer to side with the more conservative rise.

16In the model, the interval between orders corresponds to the normalized

bandwidth, (S0 − s0 )/δ. In the case of fF , we set it equal to 150 days,

or 150/365 years. Hornok and Koren (2015) report that the average time

for importing across 179 countries, excluding the actual shipping time, is

around one month. Longer shipping times are associated with less frequent

shipments. Also see Kropf and Sauré (2014) for estimates of substantial

fixed shipment costs based on transaction-level data.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TRADE AND UNCERTAINTY

755

FIGURE 1.—CHANGE IN s, S BOUNDS (TRIGGER POINT, RETURN POINT) DUE TO HIGHER UNCERTAINTY. THE LOW-UNCERTAINTY

STATE IS IN GRAY, THE HIGH-UNCERTAINTY STATE IN BLACK.

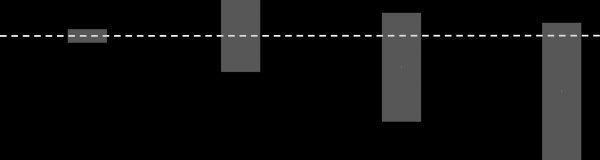

FIGURE 2.—SUMMARY: HOW UNCERTAINTY PUSHES DOWN THE s, S BOUNDS AND INCREASES THE BANDWIDTH

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

in response to an increase λ1. But clearly the bounds for the

low-uncertainty state are essentially not affected by a rising

λ1.

Two observations stand out. First, the lower trigger point

always deviates farther from the target than the return point.

This is true for both states of uncertainty (i.e., |s0| > S0 and

|s1| > S1). As we show in the theory appendix, in the pres-

ence of uncertainty, a symmetric band around the target (d.h.,

|sω| = S0) would not be optimal. The reason is that with un-

certainty, there is a positive probability of the firm’s output

getting hit by a shock, leading the firm to adjust its inventory

to the return point. Daher, the higher the shock probability,

the more frequently the firm would adjust its inventory above

target. To counteract this tendency, it is optimal for the firm

to set the return point relatively closer to the target.

Zweite, the bounds for the high-uncertainty state decrease

with the extent of uncertainty, das ist, ∂S1/∂λ1 < 0 and

∂s1/∂λ1 < 0. The intuition for the drop in the return point

S1 is the same as above: increasing uncertainty means more

frequent adjustment so that S1 needs to be lowered to avoid

excessive inventory holdings. The intuition for the drop in

the lower trigger point s1 reflects the rising option value of

waiting. Suppose the firm is facing a low level of inventory

and decides to pay the fixed costs of ordering f to stock up. If

the firm gets hit by a shock in the next instant, it would have

to pay f again. The firm could have saved one round of fixed

costs by waiting. Waiting longer corresponds to a lower value

of s1. This logic follows immediately from the literature on

uncertainty and the option value of waiting (McDonald &

Siegel, 1986; Dixit, 1989; Pindyck, 1991).

Figure 2 summarizes the main qualitative results in a com-

pact way. Case 1 depicts the (hypothetical) situation where

both fixed costs f and uncertainty λ are negligible. Due to

the very low fixed costs the bandwidth (i.e., the height of the

box) is tiny, and due to the lack of uncertainty, the s1 and S1

bounds are essentially symmetric around the target level m∗.

756

THE REVIEW OF ECONOMICS AND STATISTICS

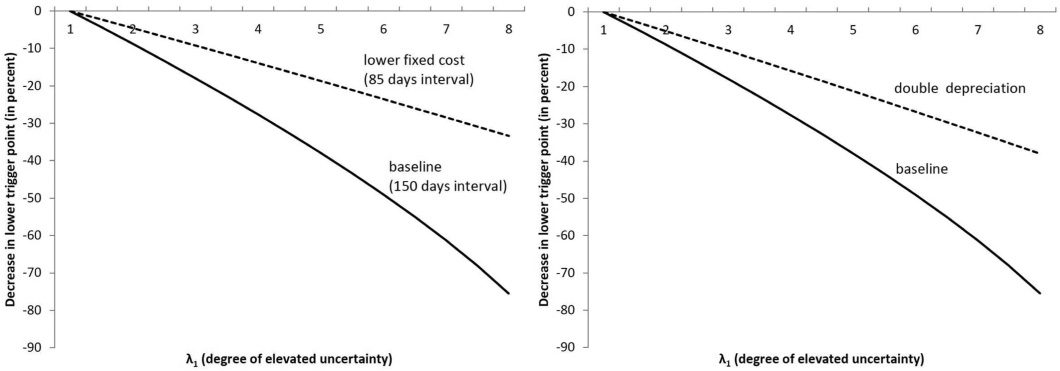

FIGURE 3.—THE EFFECT OF LOWER FIXED COSTS (LEFT) AND A HIGHER DEPRECIATION RATE (RIGHT) ON THE DECREASE IN THE LOWER TRIGGER POINT

In case 2, the fixed costs become larger, which pushes both

s1 and S1 farther away from the target but in a symmetric

way. Cases 3a and 3b correspond to the situation we con-

sider in this paper with nonnegligible degrees of uncertainty.

The uncertainty in case 3a induces two effects compared to

case 2. First, both s1 and S1 shift down so that they are no

longer symmetric around the target. Second, the bandwidth

increases further. A shift to even more uncertainty (case 3b)

reinforces these two effects.

C. Comparative Statics

We have assumed fixed costs of ordering to be lower when

the input is ordered domestically: fD < fF . The left panel of

figure 3 shows the effect of using the value fD from above

that corresponds to an average interval of 85 days between

domestic orders compared to the baseline value fF that cor-

responds to 150 days. Lower fixed costs imply more frequent

ordering and therefore allow the firm to keep its inventory

closer to the target level. This means that for any given level

of uncertainty, the optimal lower trigger point with low fixed

costs does not deviate as far from the target compared to the

high fixed cost scenario.

Some types of imports observed in the data are inher-

ently difficult to store as inventory—for instance, nondurable

goods. We model such a difference in storability with a higher

rate of depreciation of δ = 0.2 compared to the baseline value

of δ = 0.1. In general, the larger the depreciation rate, the

smaller the decreases in the lower trigger point and the return

point in response to heightened uncertainty. Intuitively, with

a larger depreciation rate the firm orders more frequently. The

value of waiting is therefore diminished. The right panel of

figure 3 graphs the percentage decline in the lower trigger

point s1 relative to s0 for both the baseline depreciation rate

and the higher value. We provide more comparative statics

results for changes in f and δ in the theory appendix.

V.

Simulating Uncertainty Shocks

So far we have described the behavior of a single firm. We

now simulate an economy of 50,000 firms in partial equilib-

rium where each individual firm receives shocks according

to the stochastic uncertainty process in equations (5) and (6).

These shocks are idiosyncratic for each firm but drawn from

the same distribution. The firms are identical in all other re-

spects. We use the same parameter values as in section IVA,

and we focus on the foreign-sourced input KF and the asso-

ciated fixed costs fF .

We simulate an uncertainty shock by permanently shifting

the economy from low uncertainty λ0 to high uncertainty λ1.

A key result from section IVB is that firms lower their s, S

bounds in response to increased uncertainty. This shift leads

to a strong downward adjustment of input inventories and

thus a strong decline in imports.

In figure 4 we plot simulated imports, normalized to 1 for

the average value, in continuous time (focus on the solid line;

we will explain the dashed and dotted lines below). Given our

parameterization, imports decrease by up to 25% at an instant

in response to the shock. The decrease happens quickly within

one month, followed by a quick recovery and, in fact, an

overshoot (we comment on the overshoot below). This pattern

of sharp contraction and recovery is typical for uncertainty

shocks. In the theory appendix, as a comparison, we express

the same simulated data in discrete time at monthly frequency.

There, we also allow for a temporary shock where uncertainty

shifts back to its low level.

In our model, the reaction of aggregate imports can be

more clearly thought of in terms of two effects, depicted in

figure 4. The dashed line (at the bottom) represents a “pure”

uncertainty effect, and the dotted line (at the top) is a volatility

effect. The volatility effect is responsible for the overshoot,

and we comment on it in more detail in the theory appendix.

While the trade collapse and recovery happen quickly in

the simulation, this process takes longer in the data. For

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

FIGURE 4.—SIMULATING AND DECOMPOSING THE RESPONSE OF AGGREGATE IMPORTS TO AN UNCERTAINTY SHOCK: THE TOTAL EFFECT (BASELINE), THE “PURE”

UNCERTAINTY EFFECT, AND THE VOLATILITY EFFECT

TRADE AND UNCERTAINTY

757

instance, during the Great Recession, German imports peaked

in the second quarter of 2008, rapidly declined by 32%,

and returned to their previous level only by the third quar-

ter of 2011.17 Greater persistence could be introduced into

our simulation by staggering firms’ responses. Currently,

all firms perceive uncertainty in exactly the same way and

thus synchronize their reactions. It might be more realis-

tic to introduce some degree of heterogeneity by allowing

firms to react at slightly different times. In particular, firms

might have different assessments as to the time when un-

certainty has faded and business conditions have normalized

(see Bernanke, 1983). This would stretch out the recovery of

trade, and it would also diminish the amplitude of the impact.

Moreover, delivery lags could be introduced that vary across

industries. We abstracted from such extensions here in order

to keep the model tractable.

Apart from being heterogeneous in terms of when they re-

act to a shock, firms could also differ in more fundamental

ways. Consistent with the literature on heterogeneous firms

and trade, aggregate imports tend to be dominated by the

most productive firms in an economy. Only those firms are

able to cover the higher fixed costs of sourcing inputs from

abroad. In the current model, we do not model an exten-

sive margin response, that is, firms do not switch from a for-

eign to a domestic supplier over the simulation period, or

vice versa.18 Allowing for extensive margin responses would

be an important avenue for future research. We conjecture

17Most high-income countries experienced similar patterns. US and

Japanese imports declined by 38% and 40% over that period, respectively

(source: IMF, Direction of Trade Statistics).

18This approach is motivated by empirical evidence based on micro-

data. Examining Belgian firm-level data during the 2008–2009 recession,

Behrens et al. (2013) find that most of the changes in international trade

across trading partners and products occurred at the intensive margin, while

that the extensive margin would amplify uncertainty shocks.

Firms would likely switch to domestic suppliers in the face

of higher uncertainty, thus reinforcing the effects of higher

uncertainty. But since changing suppliers entails switching

costs, an extensive margin response might also make the ef-

fect of an uncertainty shock more persistent in the aggregate.

Firms will not switch to domestic suppliers immediately but

rather wait a while such that the overall effect on international

trade flows is more drawn out. Moreover, once the uncer-

tainty shock has subsided, firms might be slow in switching

back to foreign suppliers, delaying the recovery. Of course,

to trace this mechanism, we would need firm-level data on

foreign and domestic input orders, both at a reasonably high

frequency. Alternatively, and trivially, persistence might arise

by having multiple persistent uncertainty shocks arrive one

after the other. This may well match the reality of 2008 and

is an approach we explore in section VII.

In the theory appendix, we provide further simulation re-

sults involving comparative statics (changes in fixed costs

and the depreciation rate). We also explore the role of first-

moment shocks.

VI. Empirical Evidence

We now turn to the task of providing more formal empirical

evidence for the new theoretical channels linking uncertainty

shocks to domestic activity and foreign trade that we have

proposed. Specifically, we set out to explore the dynamic re-

lationship of uncertainty, production, and international trade

trade fell most for consumer durables and capital goods. Bricongne et al.

(2012) confirm the overarching importance of the intensive margin for

French firm-level export data. Haddad et al. (2010) present similar evidence

for US imports, which we consider in our empirical analysis.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

758

THE REVIEW OF ECONOMICS AND STATISTICS

by estimating vector autoregressions (VARs) with US data.

Here, for comparability, we deliberately follow current state

of the art, and we follow the canonical framework established

by Bloom (2009) in running a VAR to generate an impulse

response function (IRF) relating the reactions of key model

quantities—in this case, not only industrial production but

also imports—to the underlying impulses that take the form

of shocks to uncertainty.

We contend that as with the application to production, the

payoffs to an uncertainty-based approach can be substantial

in the new setting we propose for modeling trade volatility.

Why? Recall that in the view of Bloom (2009, p. 627):

More generally, the framework in this paper

also provides one response to the “where are

the negative productivity shocks?” critique of

real business cycle theories. In particular, since

second-moment shocks generate large falls in

output, employment, and productivity growth,

it provides an alternative mechanism to first-

moment shocks for generating recessions.

The same might then be said of theories of the trade col-

lapse that rely on negative productivity shocks.19 Moreover,

by the same token, the framework in our paper provides one

response to the “where are the increases in trade frictions?”

objection that is often cited when standard static models are

unable to otherwise explain the amplified nature of trade col-

lapses in recessions, relative to declines in output.

The model above, and evidence below, can thus be

seamlessly integrated with the closed-economy view of

uncertainty-driven recessions, while matching a separate and

distinct aggregate phenomenon that has long vexed interna-

tional economists. Our new approach tackles an enduring

puzzle, a crucial and recurrent feature of international eco-

nomic experience: the highly magnified volatility of trade,

which has been a focus of inquiry since at least the 1930s and

since the onset of the Great Recession has flared again as an

object of curiosity and worry to scholars and policymakers

alike.

A. Testable Hypotheses

To sum up the bottom line, our empirical results expose

new and important stylized facts that are consistent with our

theoretical framework.

First, trade volumes do respond to uncertainty shocks, and

the impacts are quantitatively and statistically significant. In

addition, trade volume responds much more to uncertainty

shocks than does the volume of industrial production; this

magnification shows that there is something fundamentally

different about the dynamics of traded goods supplied via

19Of course, first-moment demand shocks are less controversial in the

context of the Great Trade Collapse.

the import channel, as compared to supply originating from

domestic industrial production.

Second, we will confirm that these findings are true not just

at the aggregate level, but also at the disaggregated level, indi-

cating that the amplified dynamic response of traded goods is

not just a sectoral composition effect. In addition, we find that

the impact and magnification are greatest in durable goods

sectors as compared to nondurable goods sectors, consistent

with the theoretical model where a decrease in the depreci-

ation parameter (interpreted as a decrease in perishability)

leads to a larger response.

The subsequent parts of this section are structured as fol-

lows. The first section briefly spells out the empirical VAR

methods we employ. The second section spells out the data

we have at our disposal, some newly collected, to examine

the differences between trade and industrial production in this

framework. The subsequent sections discuss our findings.

B. Computing the Responses to an Uncertainty Shock

In typical business cycle empirical work, researchers are

often interested in the response of key variables, most of all

output, to various shocks, most often a shock to the level of

technology or productivity. The analysis of such first-moment

shocks has long been a centerpiece of the macroeconomic

VAR literature. Bloom’s (2009) innovation was to construct,

simulate, and empirically estimate a model where the key

shock of interest is a second-moment shock, which is con-

ceived of as an uncertainty shock of a specific form. In his

setup, this shock amounts to an increase in the variance, but

not the mean, of a composite business conditions disturbance

in the model, which can be flexibly interpreted as a demand

or supply shock.

For empirical purposes, when the model is estimated us-

ing data on the postwar United States, changes in the VXO

US stock market volatility index are used as a proxy for the

uncertainty shock. The VXO, and its newer cousin, VIX, pro-

vided by the Chicago Board Options Exchange, have formed

the basis of the most widely traded options-implied volatility

contracts, and they reference the daily standard deviation of

the S&P 500 index over a thirty-day forward horizon. With an

implicit nod to rational expectations, realized volatility was

used to backfill a proxy for VXO in historical periods before

1986 back to 1962 when the VXO is not available. A plot

of this series, scaled to an annualized form and extended to

2012 for use here is shown in figure 5.20

20As Bloom (2009, figure 1) notes, “Pre-1986 the VXO index is unavail-

able, so actual monthly returns volatilities are calculated as the monthly

standard deviation of the daily S&P500 index normalized to the same mean

and variance as the VXO index when they overlap from 1986 onward. Ac-

tual and VXO are correlated at 0.874 over this period. The asterisks indicate

that for scaling purposes the monthly VXO was capped at 50. Uncapped

values for the Black Monday peak are 58.2 and for the credit crunch peak

are 64.4. LTCM is Long Term Capital Management.” For comparability,

we follow exactly the same definitions here and thank Nicholas Bloom for

providing us with an updated series extended to 2012.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TRADE AND UNCERTAINTY

759

FIGURE 5.—THE UNCERTAINTY INDEX: MONTHLY US STOCK MARKET VOLATILITY, 1962–2012

VXO index and proxies. Capped at 50 (*). From Bloom (2009) and updates. See the appendix.

log(S&P500 stock market

We evaluate the impact of uncertainty shocks using VARs

on monthly data from 1962 (the same as in Bloom) to

February 2012 (going beyond Bloom’s end date of June

2008). The full set of variables, in VAR estimation Cholesky

ordering, are as follows:

in-

dex), stock market volatility indicator, Federal Funds rate,

log(average hourly earnings), log(consumer price index),

hours, log(employment), and log(industrial production). We

do not find our results are sensitive to the Cholesky order-

ing.21 For simplicity, the baseline results we present are esti-

mated using a more basic quadvariate VAR (log stock market

levels, the volatility indicator, log employment, and the log

industrial production or trade indicator).

C. Data

Many of our key variables are exactly as in Bloom (2009):

log industrial production in manufacturing (Federal Reserve

Board of Governors, seasonally adjusted), employment in

manufacturing (BLS, seasonally adjusted), a monthly stock

market volatility indicator as above, and the log of the S&P

500 stock market index. All variables are HP detrended, with

parameter λ = 129,600. Full details are provided in the data

appendix. Collection of these data was updated to February

2012.

However, in some key respects, our data requirements are

much larger. For starters, we are interested in assessing the

21We follow Bloom (2009) exactly for comparability. As he notes, “This

ordering is based on the assumptions that shocks instantaneously influence

the stock market (levels and volatility), then prices (wages, the consumer

price index (CPI), and interest rates), and finally quantities (hours, employ-

ment, and output). Including the stock-market levels as the first variable in

the VAR ensures the impact of stock-market levels is already controlled for

when looking at the impact of volatility shocks.”

response of trade, so we needed to collect monthly import

volume data. In addition, we are interested in computing dis-

aggregated responses of trade and industrial production (IP)

in different sectors, in the aftermath of uncertainty shocks, to

gauge whether some of the key predictions of our theory are

sustained. Thus, we needed to assemble new monthly trade

data (aggregate and disaggregate) as well as new disaggre-

gated monthly IP data.

We briefly explain the provenance of these newly collected

data, all of which are also HP filtered for use in the VARs, as

above. More details of sources and construction are given in

the data appendix.

• US aggregated monthly real import volume. These data

run from 1962:1 to 2012:2. After 1989, total imports

for general consumption were obtained from the USITC

dataweb. From 1968 to 1988, data were collected by hand

from FT900 reports, where imports are only available

from 1968 as F.A.S. (free alongside ship) at foreign port

of export, general imports, seasonally unadjusted; the se-

ries change to C.I.F. (cost, insurance, and freight) in 1974,

and the definition changes to customs value in 1982. Prior

to 1968, we use NBER series 07028, a series that is called

“total imports, free and dutiable” or else “imports for con-

sumption and other”; for the 1962 to 1967 window, this

NBER series is a good match, as it is sourced from the

same FT900 reports as our hand-compiled series. The en-

tire series was then deflated by the monthly CPI.

• US disaggregated monthly real imports. These data run

only from 1989:1 to 2012:2. In each month, total imports

for general consumption disaggregated at the four-digit

NAICS level were obtained from the USITC dataweb.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

2

4

7

4

9

1

8

8

1

3

4

6

/

r

e

s

t

_

a

_

0

0

8

8

5

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

760

THE REVIEW OF ECONOMICS AND STATISTICS

All series were then deflated by the monthly CPI. In this

way, 108 sector-level monthly real import series were

compiled.

• US disaggregated monthly industrial production. These

data run only from 1972:1 to 2012:2 at a useful level of

granularity. Although aggregate IP data are provided by

the Fed going back to 1919, the sectorally disaggregated

IP data start only in 1939 for 7 large sectors, with ever finer

data becoming available in 1947 (24 sectors), 1954 (39

sectors), and 1967 (58 sectors). However, it is in 1972 that

IP data are available using the four-digit NAICS classifi-

cation, which permits sector-by-sector compatibility with

the import data above. From 1972, we used Fed G.17 re-

ports to compile sector-level IP indices, yielding data on

98 sectors at the start, expanding to 99 in 1986.

D.

IRFs at Aggregate Level for Trade and IP

The world witnessed an unusually steep decline in inter-

national trade in 2008–2009, the most dramatic since the

Great Depression. International trade plummeted by 30% or

more in many cases. Some countries suffered particularly

badly. For example, Japanese imports declined by about 40%

from September 2008 to February 2009. In addition, the de-

cline was remarkably synchronized across countries. Bald-

win (2009) notes that “all 104 nations on which the WTO

reports data experienced a drop in both imports and exports

during the second half of 2008 and the first half of 2009.”

This synchronization hints at a common cause (Imbs, 2010).

The first evidence we present on the importance of uncer-

tainty shocks for trade uses aggregate data on US real imports

and industrial production (IP). We estimate a vector autore-

gression (VAR) with monthly data from 1962 through 2012,

following the main specification in Bloom (2009) exactly, as

explained above and more fully in the appendix.

Figure 6 presents our baseline quadvariate VAR results

for the aggregate US data, for both log real imports and log

IP, as well as their ratio, all in a row. The impulse response

functions (IRFs) from the VAR are based on a one-period

uncertainty shock where the uncertainty measure increases

by one unit (the measure is an equity market option implied-

volatility index, VXO, all data are HP filtered). In figure 6a,

the upper panel, we employ Bloom’s standard uncertainty

shock series. In figure 6b, the lower panel, to support the idea

of causality, we rely on his “exogenous” uncertainty shock

series that only uses events associated with terrorist attacks,

war, and oil shocks.

The bottom line is very clear from this figure. Look first

at figure 6a. The uncertainty shock is associated with a de-

cline in both industrial production and imports. However, the

response of imports is clearly many times stronger—about

five to ten times as strong on average in the period of peak

impact during year 1. The response of imports is also highly

statistically significant. At its peak, the IRF is 3 or 4 standard

errors below 0, whereas the IRF for IP is only just about 2

standard errors below 0, and only just surmounts the 95%

confidence threshold. To confirm that the response of im-

ports is more negative than the response of IP, the third chart

in row 1 shows the IRF computed when using the log ratio of

real imports to IP: clearly this ratio falls after an uncertainty

shock, and the 95% confidence interval lies below 0.

To provide further evidence and a robustness check, con-

sider figure 6b, where now only the exogenous “clean” un-

certainty shocks indicator from Bloom (2009) is used, scaled