THE DYNAMIC EFFECTS OF TAX AUDITS

Arun Advani, William Elming, and Jonathan Shaw*

Abstract—We study the effects of audits on long run compliance behavior

using a random audit program covering more than 53,000 tax returns. Wir

find that audits raise reported tax liabilities for five years after audit, Effekte

are longer-lasting for more stable sources of income, and only individuals

found to have made errors respond to audit. A total of 60%–65% of revenue

from audit comes from the change in reporting behavior. Extending the

standard model of rational tax evasion, we show that these results are best

explained by information revealed by audits constraining future misreport-

ing. Together these imply that more resources should be devoted to audits,

audit targeting should account for reporting responses, and performing au-

dits has additional value beyond merely threatening them.

ICH.

Einführung

AUDITS are a widely used public-policy tool for reduc-

ing corruption (Bobonis, Cámara Fuertes, & Schwabe,

2016; Avis, Ferraz, & Finan, 2018), improving public ser-

vice delivery (Zamboni & Litschig, 2018; Lichand, 2016;

Gerardino, Litschig, & Pomeranz, 2020), ensuring environ-

mental standards (Duflo et al., 2013, 2018), and improving tax

compliance (Kleven et al., 2011; Pomeranz, 2015; Asatryan

& Peichl, 2017; Bergolo et al., 2020; Sarin & Summers, 2020,

unter anderen). But audits are costly, so determining how

many to do and how best to allocate them are key policy

Fragen (Slemrod & Yitzhaki, 2002). In tax, the standard

approach to setting the number of audits is to compare their

costs with the expected missing tax uncovered at audit—

the static gain from an audit (Allingham & Sandmo, 1972;

Kolm, 1973; Yitzhaki, 1987; Bloomquist, 2013). Jedoch,

audits may change taxpayer behavior. A field experiment in

Denmark, which followed taxpayers for a year after audit,

found an increased reported liability worth 55% of the au-

dit adjustment (Kleven et al., 2011). This suggests that static

gains may understate the total gains from audit. Jedoch,

without a longer horizon, it is hard to know by how much,

Received for publication December 16, 2019. Revision accepted for pub-

lication April 8, 2021. Editor: Rema N. Hanna.

∗Advani (Korrespondierender Autor): University of Warwick, CAGE Research

Centre, the Institute for Fiscal Studies (IFS), and the Tax Administration

Research Centre (TARC); Elming: IFS and TARC at the time of involvement

in this work; Shaw: Financial Conduct Authority.

The authors thank Michael Best, Richard Blundell, Tracey Bowler, Mo-

ica Costa Dias, Dave Donaldson, Mirko Draca, James Fenske, Clive Fraser,

Claus Kreiner, Costas Meghir, Gareth Myles, Matthew Notowidigdo, Áureo

de Paula, Andreas Peichl, Imran Rasul, Chris Roth, Joel Slemrod, Hannah

Tarrant, and seminar participants at the Tax Systems Conference, Royal

Economic Society, Louis-André Gérard-Varet, European Economic As-

sociation, Warwick Applied Workshop, OFS Empirical Analysis of Tax

Compliance, International Institute of Public Finance, Econometric Soci-

ety European Meetings, and National Tax Administration Conferences for

helpful comments. We also thank Yee Wan Yau and the HMRC Datalab

team for assistance with data access. This work contains statistical data

from HMRC which is Crown Copyright. The research data sets used may

not exactly reproduce HMRC aggregates. The use of HMRC statistical data

in this work does not imply the endorsement of HMRC in relation to the

interpretation or analysis of the information.

A supplemental appendix is available online at https://doi.org/10.1162/

rest_a_01101.

or even whether this effect is reversed in subsequent years,

as some lab experiments suggest (Maciejovsky, Kirchler, &

Schwarzenberger, 2007; Kastlunger et al., 2009).

This paper studies the long-run effect of tax audits on tax-

payer compliance behavior. We combine confidential admin-

istrative data on the universe of UK tax filers over thirteen

years with a randomised audit programme. We show three

main results. Erste, audits raise subsequent tax reports, Aber

the effect declines to zero over five to eight years. The ag-

gregate additional revenue after audit is at least 1.5 times the

underpayment found at audit, implying substantially more

resources should be dedicated to audit than a static compari-

son would suggest. Zweite, the revenue gain is longer-lasting

for more stable income sources. This highlights the impor-

tance of dynamics for targeting audits, as well as for setting

their level. Dritte, using an event study strategy, we show that

these effects are driven by individuals who were found to be

underreporting, while there is no response for those found to

have reported correctly. These three results can be explained

by a model in which audits provide the tax authority with

information about a taxpayer’s income at the time of audit.

This makes later misreporting more difficult, particularly for

stable income sources.

To estimate the long-run effect, we exploit a random audit

programme run by the UK tax authority (HM Revenue and

Customs, HMRC). Über 53,000 individual tax filers were un-

conditionally randomly selected for audit by the programme

zwischen 1998/1999 Und 2008/2009, allowing us to address

the common concern that audits are typically targeted to-

wards taxpayers believed to be underreporting. Ähnlich zu

Denmark (Kleven et al., 2011) and in contrast to the United

Zustände (Slemrod, Blumenthal, & Christian, 2001; DeBacker

et al., 2018; Perez-Truglia & Troiano, 2018), taxpayers are

not told these audits are random. This is important as tax-

payers may respond differently—likely less—to audits they

know are random, relative to when they think the tax au-

thority is concerned about something on their return. Wir

combine these audit data with data on the universe of UK

self-assessment taxpayers—individuals who self-file taxes

rather than having all tax collected via withholding—from

1998/1999 Zu 2011/2012. This allows us to follow individ-

uals for many years after audit. For our first identification

strategy, we construct a control group for each year of the

programme from individuals who could have been selected

for a random audit that year but were not. We then study the

difference in reporting behavior over time.

Our first result is that dynamic effects are positive and sub-

stantial: taxpayers report higher levels of tax for five to eight

years after audit. We see an initial increase, and then a steady

Abfall, in total tax reported over time. By eight years af-

ter audit there is no difference in average tax paid between

audited and unaudited taxpayers, though differences are not

The Review of Economics and Statistics, Mai 2023, 105(3): 545–561

© 2021 The President and Fellows of Harvard College and the Massachusetts Institute of Technology. Veröffentlicht unter einer Creative Commons Namensnennung 4.0

International (CC BY 4.0) Lizenz.

https://doi.org/10.1162/rest_a_01101

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

546

THE REVIEW OF ECONOMICS AND STATISTICS

statistically significant beyond five years. A total of 60%–

65% of the total revenue received as a result of audit comes

from this change in reporting behavior. Taking into account

this effect, tax authorities should do many more audits: ac-

counting for dynamic effects, even random audits provide a

return equal to 80% of their cost to the tax authority. Given the

recent focus on the value of audits purely as a threat (Slemrod,

Blumenthal, & Christian, 2001; Fellner et al., 2013; Dwenger

et al., 2016; Mascagni, 2018; Bergolo et al., 2020; Lichand,

2016); this highlights a benefit of actually performing the

audits.

Zweite, we show that dynamic effects fall to zero slower

for more stable income sources. Pension income, welches ist

highly autocorrelated (“stable”) in the absence of audit, Re-

sponds permanently. At the other extreme, the effect on self-

employment and dividend income returns to zero within three

Jahre. This is important for two reasons. Erste, it has impli-

cations for the targeting of audits. Going after a smaller sus-

pected discrepancy on a more stable income source can have

high returns once dynamic effects are included. Reauditing

is also more likely to produce additional yield for individu-

als with less stable income sources. Zweite, it is relevant for

understanding why people respond to audits, as we describe

below. A natural concern in treating this difference causally,

and using it to interpret behavior, is that individuals with dif-

ferent types of income may respond differently. We account

for this by using pairwise comparisons of income sources

within individuals who have both sources, and we demon-

strate that the less stable source still declines more quickly.

Dritte, we show that audits only change the behavior of

those who are found to have misreported. To do this we use

an event study approach. We compare individuals who were

audited at some point in our sample and who ultimately all had

the same audit outcome, for example were found to be non-

compliant. Allowing for individual and calendar time fixed

Effekte, the comparison is essentially between those whose

noncompliance has already been uncovered by a random au-

dit and those who will have it uncovered in the future. Wir finden

that being audited only changes the behavior of those who

are found to have misreported, and this is true whether or

not they received a penalty. Wichtig, this tells us that the

effect of audits comes not merely from scaring all taxpayers

into paying more, but specifically from changing the behav-

ior of those who were previously misreporting. It also allows

us to rule out audits reducing tax reports, even for those who

were found compliant, in contrast with results using alterna-

tive identification strategies (Gemmell & Ratto, 2012; Beer

et al., 2020).

These results are consistent with audits providing the tax

authority with information at a point in time, which constrains

future misreporting. To see this, we extend the canonical

model of tax evasion (Allingham & Sandmo, 1972; Yitzhaki,

1987; Kleven et al., 2011) to incorporate (simple) dynam-

ics in the response to audit. This allows us to study the dis-

tinct predictions of three different mechanisms that might

drive changes in reporting: (ich) changes in beliefs about the

underlying audit rate or penalty for evasion (“belief updat-

ing“); (ii) changes in the perceived reaudit risk following au-

dit (“reaudit risk”); Und (iii) updates to the information held

by the tax authority (“information”). Kleven et al. (2011) Notiz

that their observed increase in reported tax one year after au-

dit could be explained by some combination of beliefs and

reaudit risk, but they cannot disentangle the two. We note that

a response to belief updating should be permanent, as taxpay-

ers revise the expected cost of noncompliance (up or down).

This is inconsistent with the declining pattern of dynamic ef-

fects we see. A response to reaudit risk would decline over

Zeit. Whether it took the form of a “bomb crater” (Mittone,

2006)—that the probability of audit is lower in the years fol-

lowing an audit before rising back to baseline—or a worry of

higher levels of short-term scrutiny, we should see the same

effect across all income sources. We see a positive dynamic

Wirkung, ruling out “bomb craters,” and we see a differential

decline across income sources, even within individuals, rul-

ing out an effect driven purely by reaudit risk. Instead we

propose a third, novel, possibility. As Kleven et al. (2011)

Notiz, when taxpayers know the tax authority has access to

third-party information about some income source, they are

much less likely to underreport. Ähnlich, when the tax au-

thority performs an audit, it gets a snapshot of income at a

point in time. Implausibly large deviations in reported income

in following years are likely to trigger an audit, because tax

authorities (partly) condition audit selection on differences

between reported income and their expectation of that in-

come based on other sources of information (Advani, 2022).

As time passes, the snapshot becomes less informative about

what current income is likely to be. This is particularly true

for less stable income sources. In this case, we should see a

decline in dynamic effects over time, with less stable income

sources showing a faster decline. We should also only see

responses from individuals who were found to have misre-

portiert, because no new information about the other taxpayers

is revealed to the authority. These are precisely the patterns

that are observed.

Our results imply that audits themselves are important,

beyond the “fear” or “threat” of audit. Much of the recent lit-

erature studying the administration of taxes and the policies

that can improve taxpayer compliance has focused on “letter

experiments”: how different forms and content of informa-

tion provided to taxpayers can change their behavior (see Blu-

menthal, Christian, & Slemrod, 2001; Slemrod et al., 2001 für

early work, and Mascagni, 2018; Alm, 2019; Pomeranz and

Vila-Belda, 2019; Slemrod, 2019 for recent surveys of this

Literatur). These all aim to change the perceived probability

of audit. They have the benefit that they are a very low-cost

policy for a tax authority, yet show substantial (short-term)

gains. Zum Beispiel, Bergolo et al. (2020) find, in the con-

text of VAT in Uruguay, that firms do not respond to the

actual probability of audit when sent letters informing them

davon. Stattdessen, firms increase compliance because thinking

about the audit scares them into compliance. This raises a

question: can high levels of compliance be achieved, while

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

THE DYNAMIC EFFECTS OF TAX AUDITS

547

reducing the number of audits, by directing more resources

towards information campaigns? Our results imply that this

is harder than previously thought, as much of the gain from

audit is the change in behavior it promotes. This response is

driven by the information received by the authority through

actually conducting the audit. Threat letters do not provide

this information benefit. To understand any substitutability

with audits, more information is needed on the long-term

effects of such letters: for how long do threats raise com-

pliance, and can repeated threats continue to maintain high

compliance rates?

Im Gegensatz, third-party information is a more direct sub-

stitute for audits. Recent work has shown the importance

(and limits) of third-party information for improving compli-

ance (Kleven et al., 2011; Pomeranz, 2015; Kleven, Kreiner,

& Saez, 2016; Carrillo, Pomeranz, & Singhal, 2017; Slem-

rod et al., 2017; Naritomi, 2019). Since this directly reduces

the information asymmetry between taxpayer and authority,

it will also reduce the information value of audits, welche

drives the dynamic effects. Umgekehrt, for income sources

where third-party information can be hard to come by, au-

dits can be a partial alternative to gathering information from

other sources. They will not only improve contemporaneous

compliance, but also reduce the scope for future noncompli-

ance. This contrasts with work on firms, which finds comple-

mentarity between monitoring and enforcement (Almunia &

Lopez-Rodriguez, 2018).

We find no evidence of “backfire” effects, where audits re-

duce compliance. Worries about backfire effects are common

across areas of tax policy (Perez-Truglia & Troiano, 2018). In

our context they raise the risk that poorly targeted audits may

reduce compliance. Gemmell and Ratto (2012) suggest some

reduction in tax reported by individuals who are audited and

found compliant, relative to individuals not audited. Similar

results are found in the United States by Beer et al. (2020) us-

ing a matched difference-in-difference approach. Our event

study strategy allows for potential differences in unobserv-

able characteristics between compliant and noncompliant

individuals, and finds no backfire. The difference in our

results, compared to existing work, also suggests that unob-

servable differences are important in explaining compliance

behavior. Since we find no reduction in overall tax paid, Es

also suggests that lab experimental evidence of bomb crater

effects is not reflected in real-world settings (Maciejovsky

et al., 2007; Kastlunger et al., 2009), although we note that

not all lab experiments find evidence of such effects (Choo,

Fonseca, & Myles, 2013).

Endlich, we provide a new theoretical mechanism for why

audits have the observed effects. Understanding what moti-

vates compliance is a key question for public policy, und da

are rich debates on the extent to which moral versus economic

calculations drive behavior (Alm, 2019). We focus on the nar-

rower question of why audits affect compliance, and we find

that information is the key. Um dies zu tun, we use evidence from

random audits to look at both the time path of dynamic ef-

fects across income sources and the effects by audit outcome.

Though earlier work has (separately) studied both of these is-

sues, we show how they can be used to understand why audits

change behavior.1 Our results complement those of Bergolo

et al. (2020) and Lichand (2016), who find that the threat of

audit works through fear and belief-updating, jeweils. In

Kontrast, receipt of audit works through a change in ability to

misreport without being caught, an effect that cannot occur

in the absence of actual audit.

The remainder of the paper is organised as follows. Sec-

tion II outlines the policy context and data sources. Section III

provides evidence on who is noncompliant. Section IV shows

how audits affect reporting behavior in overall tax, und von

different income sources. Section V uses an alternative iden-

tification strategy to estimate the impact by audit outcome.

Section VI outlines a model of tax evasion with dynamics

in the response to audits, to show which mechanisms might

rationalise the observed behavior. Section VII concludes.

II. Context and Data

A. The UK Self-Assessment Tax Collection

and Enforcement System

In diesem Papier, we focus on individuals who file an income

tax self-assessment return in the UK. Over our sample pe-

Riod (1999–2012) this comprised around nine million indi-

viduals, one-third of all individual income taxpayers in the

UK.2 Income tax is the largest of all UK taxes, konsequent

contributing a quarter of total government receipts over this

Zeitraum. Most sources of income are subject to income tax, In-

cluding earnings, retirement pensions, income from property,

interest on deposits in bank accounts, dividends, and some

welfare benefits. Income tax is levied on an individual basis

and operates through a system of allowances and bands. Jede

individual has a personal allowance, which is deducted from

total income. The remainder—taxable income—is then sub-

ject to a progressive schedule of tax rates. Tisch 1 zeigt die

share of individuals in our sample reporting nonzero values

for each component of income. When we later study income

components separately, we focus on those components where

mindestens 5% of the population report nonzero values.

Since incomes covered by self-assessment tend to be

harder to verify, there is a significant risk of noncompliance.

1A number of studies consider dynamic effects for one or two years after

audit (Long & Schwartz, 1987; Erard, 1992; Tauchen, Witte, & Beron,

1993; Kleven et al., 2011; Løyland et al., 2019). Concurrently with this

Studie, DeBacker et al. (2018) have a longer (six-year) horizon, and they

also consider income stability, albeit with U.S. audits where taxpayers are

explicitly told they are random, which Slemrod (2019) notes “would likely

trigger different revaluations of how likely a future audit is, and therefore

trigger different behavioral changes” (a similar point is made in Kleven

et al., 2011). Effects by audit outcome are studied by Gemmell and Ratto

(2012) and Beer et al. (2020).

2Filers include self-employed individuals,

those with incomes over

£100,000 (lower at the start of the sample period), company directors, Land-

lords, and many pensioners. The remainder have all their income tax col-

lected directly via withholding, so are not required to file. Note that UK tax

years run across calendar years—we denote tax years using the later year.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

548

THE REVIEW OF ECONOMICS AND STATISTICS

TABLE 1.—SHARE OF TAXPAYERS WITH EACH SOURCE OF INCOME

Income component

Interest

Employment

Self employment

Dividends

Pensions

Property

Foreign

Trusts and estates

Share schemes

Other

Proportion

.587

.482

.375

.370

.300

.136

.048

.010

.002

.030

Annual averages for tax years 1998/1999–2008/2009. Includes only control observations, das ist, those

selected for placebo audit.

Quelle: Authors’ calculations based on HMRC administrative datasets.

Infolge, HM Revenue and Customs (HMRC, the UK tax

authority) carries out audits each year to deter noncompliance

and recover lost revenue. HMRC runs two types of audit: “tar-

geted” (also called “operational”) and “random.” Targeted

audits are based on perceived risks of noncompliance. Ran-

dom audits are unconditionally random from the population,

and are used to ensure that all self-assessment taxpayers face

a positive probability of being audited, as well as to collect

statistical information about the scale of noncompliance and

predictors of noncompliance that can be used to implement

targeting.

The timeline for the audit process is as follows. The tax

year runs from 6th April to 5th April. Shortly after the end

of the tax year, HMRC issues a “notice to file” to taxpayers

who they believe need to submit a tax return. This is based

on information that HMRC held shortly before the end of the

tax year. Random audit cases are provisionally selected from

the population of individuals issued with a notice to file. Der

deadline by which taxpayers must submit their tax return is

31 January the following calendar year (z.B., 31 Januar 2008

für die 2006/2007 tax year). Once returns have been submit-

ted, HMRC deselects some random audit cases (z.B., due to

severe illness or death of the taxpayer). Gleichzeitig,

targeted audits are selected on the basis of the information

provided in self-assessment returns and other intelligence.

Random audits are selected before targeted audits, and indi-

viduals cannot be selected for a targeted audit in the same tax

year as a random audit. The list of taxpayers to be audited is

passed on to local compliance teams who carry out the au-

dits. Up to and including 2006/2007, audits had to be opened

within a year of the 31 January filing deadline, or a year from

the actual date of filing for returns filed late. For tax returns

relating to 2007/2008 oder später, audits had to be opened within

a year of the date when the return was filed. Taxpayers subject

to an audit are informed when it is opened, but they are not

told whether it is a random or targeted audit, in contrast to

work done with U.S. random audits (Long & Schwartz, 1987;

DeBacker et al., 2018). Even after audit, taxpayers are lim-

ited in what they can learn about the audit process because no

details of the programme are made public.3 Approximately

one-third of taxpayers on the list passed on to local compli-

ance teams end up not being audited, largely due to resource

constraints.4

Those who are audited initially receive a letter requesting

information to verify what they have reported. If this does not

provide all the required information, the taxpayer receives a

follow-up phone call, and ultimately in-person visits until the

auditor is satisfied.

Where errors are uncovered, individuals are required to

pay the additional tax due, and interest. If noncompliance

is deemed to be deliberate, the taxpayer might also face an

additional penalty of up to 100% of the value of the underpaid

tax.

B. Data Sources

We exploit data on income tax self-assessment random

audits together with information on income tax returns. Das

combines a number of different HMRC datasets, linked to-

gether on the basis of encrypted taxpayer reference number

and tax year.

Audit records for tax years 1998/1999–2008/2009 come

from Compliance Quality Initiative (CQI), an operational

database that records audits of income tax self-assessment

returns. It includes operational information about the audits,

such as start and end dates, and audit outcomes: ob

noncompliance was found, and the size of any correction,

penalties, and interest.

We track individuals before and after the audit using infor-

mation from tax returns for the years 1998/1999–2011/2012.

This comes from two data sets: SA302 and Valid View. Der

SA302 data set contains information that is sent out to tax-

payers summarising their income and tax liability (the SA302

tax calculation form). It is derived from self-assessment re-

turns, which have been put through a tax calculation process.

It contains information about total income and tax liability as

well as a breakdown into different income sources: employ-

ment earnings, self-employment profits, pensions, und so weiter.

For all of these variables, we uprate to 2012 using the Con-

sumer Prices Index (CPI) to account for inflation, and trim

the top 1% to avoid outliers having an undue impact on the re-

sults.5 We supplement these variables with information from

Valid View, which provides demographics and filing infor-

mation (z.B., filing date). Note that we cannot identify actual

compliance behavior after the audit: the number of random

audit taxpayers that are reaudited is far too small for it to be

possible to focus just on them.

An explicit control group of “held out” individuals was not

constructed at the time of selection for audit. We therefore

draw control individuals from the pool of individuals who

actually filed a tax return (d.h., those who appear in SA302).

This creates some differences in the filing history between

those selected for audit and those who we deem as controls.

In a given year, first-time filers may be issued a notice to file

3Until the publication of this study, even the audit rates were not public

4We address the implications for identification in section IVA.

5In online appendix C.2 we show our results are robust to alternative levels

Information.

of trimming.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

THE DYNAMIC EFFECTS OF TAX AUDITS

549

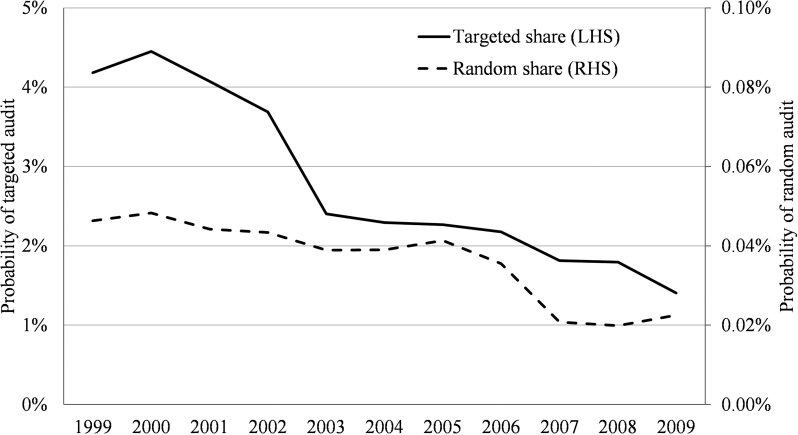

FIGURE 1.—CHANGE IN THE PROBABILITY OF AUDIT OVER TIME

Constructed using data on individuals who received an audit of their self-assessment tax return for a tax year between 1998/1999 Und 2008/2009, and the full sample of self-assessment returns for the same period.

Quelle: Calculations based on HMRC administrative data sets.

after selection for audit has taken place. They may also end

up back-filing one or two returns. Since we cannot directly

observe the first year in which a notice to file was issued, In

our empirical strategy it is necessary for us to control for the

length of time each taxpayer has been in self-assessment.

More details—including tests to demonstrate this ensures

samples are balanced—are given in section IVA below.

III. Tax Evasion in the UK

In diesem Abschnitt, we first provide some descriptives on the

probability and timeline of audits. We then show that there is

significant noncompliance among individual self-assessment

taxpayers, both in the share of taxpayers who are found

noncompliant and the share of tax that is misreported. More

than one-third of self-assessment taxpayers are found to be

noncompliant, equal to 12% of all income taxpayers.

A. Audit Descriptives

Figur 1 shows the share of individuals per year who face

an income tax random audit over the period 1998/1999–

2008/2009. On average over the period, the probabilities of

being audited are 0.04% (4 In 10,000) for random audits and

2.8% for targeted audits.

Table A1 provides some summary statistics for lags in, Und

durations of, the audit process among random audit cases. Als

described above, up to and including the 2006/2007 return,

HMRC had to begin an audit within 12 months of the 31

January filing deadline; since then, HMRC has had to begin

an audit within 12 months of the filing date. The average lag

between when the tax return was filed and when the random

audit was started is 8.9 months, Aber 10% have a lag of 14

months or more. The average duration of audits is 5.3 months,

TABLE 2.—RANDOM AUDIT OUTCOMES

Proportion of audited returns deemed

Correct

Incorrect but no underpayment

Incorrect with underpayment (noncompliant)

Mean additional tax if noncompliant (£)

Distribution of additional tax if noncompliant

Share £1–100

Share £101–1,000

Share £1,001–10,000

Share £10,001+

Beobachtungen

Mean

Std. dev.

.532

.111

.357

2,314

.116

.483

.361

.039

.499

.314

.479

7,758

.320

.500

.480

.194

34,630

Annual averages for tax years 1998/1999–2008/2009. Includes all individuals with a completed random

audit.

Quelle: Authors’ calculations based on HMRC administrative data sets.

Aber 10% experience a duration of 13 months or more. Taken

together, this means that the average time between a return

being filed and an audit being concluded is 14.3 months, Aber

there are some taxpayers for whom the experience is much

more drawn out: for almost 10% it is two years or more. Das

means that individuals will generally have filed at least one

subsequent tax return before the outcome of the audit is clear,

and some will have filed two tax returns. This will be relevant

for interpreting the results in section IV.

B. Evidence of Noncompliance

We begin by studying the direct results of random audits,

using data on 34,630 completed random audits of individual

self-assessment taxpayers from 1998/1999 Zu 2008/2009.6

Tisch 2 summarises the outcomes of these random audits.

More than half of all returns are found to be correct, 11%

653,400 cases were selected for audit over the period, of which 35,630

were implemented.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

550

THE REVIEW OF ECONOMICS AND STATISTICS

are found to be incorrect but with no underpayment of tax,

Und 36% are “noncompliant,” that is, incorrect and have a

tax underpayment.7 Whilst this is a much higher rate of

noncompliance than has been found in other developed coun-

try contexts, it should be noted that the self-assessment tax

population is a selected subset of all taxpayers. Insbesondere,

it covers those for whom a simple withholding of income at

source is not sufficient to collect the correct tax. This may be

either because some income cannot be withheld (z.B., prop-

erty or self-employed income), or because PAYE struggles

to assign the correct withholding codes (z.B., for people with

multiple sources of pension income). Despite this, since self-

assessment taxpayers make up a third of all UK taxpayers, Das

implies an overall noncompliance rate of 8%–12% among all

taxpayers.8

Turning to the intensive margin, the average additional tax

owed among the noncompliant is £2,314, oder 32% of aver-

age liabilities. Since just over a third of random audits find

evidence of noncompliance, the average additional tax owed

from an audit is then £826.9 However, the distribution is heav-

ily skewed: 60% of noncompliant individuals owe additional

tax of £1,000 or less, whilst 4% owe more than £10,000. In

terms of total revenue, those owing £1,000 or less make up

nur 9% of the underreported revenue; Die 4% owing more

than £10,000 collectively owe more than 42% of the revenue.

Equity concerns around noncompliance are well-known: Es

is seen as unfair that some are not “paying their fair share.”

But this variation in noncompliance is also important for eco-

nomic efficiency. Noncompliant individuals previously acted

as though there was a lower tax rate. This makes their activi-

ties seem relatively more productive than those of compliant

individuals, so it can lead to resource misallocation.

IV. Dynamic Impacts of Audits

In this section we establish two main results. Erste, we show

that audits lead to an increase in reported incomes and taxes in

subsequent years. Looking at total income and total tax, Das

increase lasts five to eight years after the tax year for which

the audit was done. Zweite, we show variation in this impact

by income source. Insbesondere, more autocorrelated income

sources (such as pensions) seem to respond permanently to

audit. Im Gegensatz, income sources that are less autocorre-

verspätet, such as self-employment income, more quickly return

7Incorrect with no underpayment includes those who, Zum Beispiel, owed

no taxes because they had legitimate losses, but had overstated those losses

so would owe less in future years. Anecdotally, it also includes some cases

where actual overpayments of tax were made, although we cannot separately

identify which.

8This is a lower bound, since it assumes everyone who should be in self-

assessment does register, all noncompliance is picked up at audit, and those

who do not need to register are also fully compliant. The range from 8% Zu

12% depends on the assumptions made about the implementation of audits.

Wenn, among those selected for audit, implementation of audit were random,

this would imply a 12% noncompliance rate. Andererseits, if there is

perfect compliance among those for whom audits were not implemented,

this would imply an 8% rate.

9This is the additional tax owed. A further £101 is owed, on average, In

penalties. This is highly concentrated, with less than 7% of those audited

owing any penalty amount.

to baseline. This second result will later help explain why

we see these dynamic responses. Before describing these re-

sults in detail, we first discuss the empirical approach taken.

Briefly, we compare individuals selected for random audit

with those not selected but who could have been selected.

We control for filing history to account for the way the sam-

ple was selected.

A. Estimation

To understand how audits affect future tax receipts, Wir

want to estimate the change in tax paid in the years after

audit that is caused by the audit. We recover this using the

“random audits program” run by the tax authority (HMRC).

This programme selects for audit a random sample of taxpay-

ers from the pool of taxpayers known to be required to file for

a given tax year. One can therefore compare those selected for

audit with others who were not selected but who could have

been.

In each audited tax year we select a sample of individuals

who were not audited and could have been. We assign them

a “placebo audit” for that tax year. We can then compare

them over time to individuals actually selected for audit for

that year. Our sample, daher, consists of individuals who

were selected for random audit in some year between 1999

Und 2009, and individuals who could have been selected in

those same years but were not. Our data on tax returns go

up to 2012. For every individual selected for audit in a given

tax year, we draw six control individuals from the popula-

tion of those who could have been audited in the same tax

year.10

In der Praxis, a little more than two-thirds of those selected

for random audit are actually audited. This is explained by

the high workload faced by the compliance teams implement-

ing audits. Zusätzlich, a small fraction of the control group

(around 2%) is also audited. Random audits are selected be-

fore targeted audits, and no explicit control group was con-

structed to “hold out” some individuals from targeting. To

our knowledge, in prior work only Kleven et al. (2011) have

an explicit control group. This explains why they can only

study a single year after audit—tax authorities are unwilling

to hold off on high-value audits for multiple years. Somit

we compare those selected for a random audit to a “business

as usual” group, rather than a pure control group. This will

tend to reduce the estimated impacts, since individuals in the

control group who are most likely to be noncompliant are

audited.

In the empirical work to follow, we focus on the local av-

erage treatment effect (LATE), instrumenting receipt of audit

with selection for random audit. This is the relevant number

for a tax authority thinking about simultaneously expanding

the size of the random audit programme and the number of

auditors. It gives the average impact h years after audit for an

10In principle, the entire population of taxpayers who could have been

audited could have been used. Jedoch, because the data could be accessed

only in a secure facility at the tax office, computational constraints given

the available hardware limited the sample size that could be used.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

e

D

u

/

R

e

S

T

/

l

A

R

T

ich

C

e

–

P

D

F

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

R

e

S

T

_

A

_

0

1

1

0

1

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Years after audit

Female

Alter

In London or SE

Has tax agent

Total taxable income

Total tax

Employment

Self-employment

Interest and dividends

Pensions

Property

THE DYNAMIC EFFECTS OF TAX AUDITS

551

TABLE 3.—SAMPLE BALANCE, CONDITIONING ON FILING HISTORY

−5

.274

−.005

.236

49.2

.0

.472

.333

−.003

.159

.628

−.003

.522

−4

Characteristics

.276

−.006

.212

49.3

.0

.600

.334

.001*

.026

.614

−.001

.500

Income and tax totals

35,075

−2

.979

9,646

14

.982

34,670

35

.469

9,539

12

.288

Income components

22,508

11

.758

6,546

56

.298

4,007

−26

.667

3,493

−23

.806

869

−5

.282

22,534

−57

.023

6,379

38

.435

3,905

16

.189

3,542

−23

.482

844

−6

.209

−3

.278

−.005

.292

49.3

.1

.188

.335

.003

.015

.603

−.001

.376

34,030

−163

.012

9,321

−40

.061

22,266

−98

.152

6,200

−49

.033

3,895

−27

.235

3,561

−3

.681

811

0

.525

−2

.282

−.006

.234

49.4

.1

.170

.333

.002

.317

.589

.002

.675

32,912

71

.280

8,979

12

.261

21,708

112*

.049

5,950

−18

.161

3,759

7

.958

3,562

4

.463

769

6

.072

−1

.287

−.005

.338

49.5

.1

.110

.331

.002

.190

.573

.002

.606

31,755

56

.439

8,635

15

.887

21,145

43*

.05

5,581

29

.684

3,645

4

.086

3,531

22

.523

726

0

.518

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

Mean

Difference

p-value

“Years after audit” measures time relative to audit, or placebo audit for controls. “Mean” is the mean outcome in the control (not selected for audit) group across all years. “Difference” is the coefficient on the

treatment dummy in a regression of the outcome on a treatment dummy and dummies for whether the taxpayer filed taxes in each of the four years before audit (or placebo audit for controls). Treatment dummy equals

1 if taxpayer was selected by HMRC for a random audit. p-values are derived from an F-test that coefficients on interactions between treatment and tax year dummies are all zero in a regression of the outcome of

interest on tax year dummies, interactions between treatment and tax year dummies, and dummies for whether the taxpayer filed taxes in each of the four years before audit (or placebo audit for controls). Das ist ein

stronger test than just testing the coefficient on treatment not interacted. Monetary values are in 2012 Preise. Standard errors are clustered by taxpayer. * P < .05, ** p < .01, and *** p < .001.

Source: Authors’ calculations based on HMRC administrative data sets.

additional random audit case that might be worked, against

which the cost of the audit would be compared.

One limitation of our data is a slight mismatch between our

treated and control samples in terms of their probability of fil-

ing in previous years, for reasons relating to the audit timeline

and when they were first issued a notice to file, as described

in section IIB. This can be seen in table A2, which docu-

ments (unconditional) sample balance between five and one

years before audit, for income and tax totals, income compo-

nents, and individual characteristics. Overall balancing statis-

tics suggest that the samples are fairly well-balanced: the p-

value of the likelihood-ratio test of the joint insignificance

of all the regressors is 0.181, while the mean and median

absolute standardised percentage bias across all outcomes of

interest are low at 2.4% and 1.7%, respectively.11 However,

11The standardised percentage bias is the difference in the sample means

between treated and control groups as a percentage of the square root of

the likelihood of being in the sample in previous years (“sur-

vival”) differs between our treatment and control groups. This

difference is consistent with how the treatment and control

groups were selected, so it might reflect real differences in

the samples. We therefore include controls for presence in

the data in the years before audit.12 Table 3 shows that once

we condition on past survival, the sample is balanced.

the average of the sample variances in the treated and control groups (see

Rosenbaum & Rubin, 1985). Rubin’s B and R statistics are also well within

reasonable thresholds to consider the samples to be balanced, at 10.8 and

0.983, respectively. Rubin’s B is the absolute standardised difference of the

means of the linear index of the propensity score in the treated and control

group. Rubin’s R is the ratio of treated to control variances of the propensity

score index. Rubin (2001) recommends that B be less than 25 and that R be

between 0.5 and 2 for the samples to be considered sufficiently balanced.

12In online appendix C.1, we show the results taking a different ap-

proach, where we instead use stratified random sampling conditioning the

stratification on filing history. Point estimates are similar, and never statisti-

cally significantly different from our main approach, although they decline

more rapidly from year four.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

r

e

s

t

_

a

_

0

1

1

0

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

552

THE REVIEW OF ECONOMICS AND STATISTICS

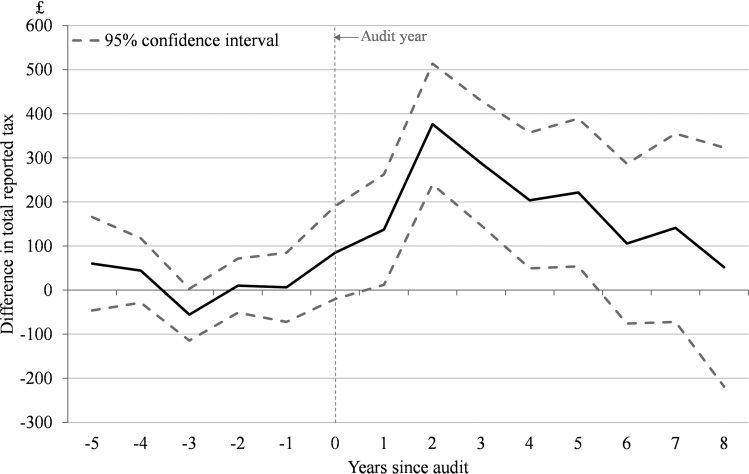

FIGURE 2.—DYNAMIC EFFECT OF AUDITS ON TOTAL REPORTED TAX OWED

Sample includes individuals selected for a random audit between 1998/1999 and 2008/2009, and control individuals who could have been selected in the same years but were not. It uses tax returns from 1998/1999 to

2011/2012. The solid line plots the point estimate for the difference in average “total reported tax” between individuals who were and weren’t audited, for different numbers of years after the audit. This comes from

a regression of total reported tax on dummies for years since audit (or placebo audit for controls), dummies for years since audit (or placebo audit for controls) interacted with treatment status, tax year dummies, and

dummies for whether the taxpayer filed a return in each of the four years before audit, with audit status instrumented by selection for audit. Standard errors are clustered at the individual level.

Source: Calculations based on HMRC administrative data sets.

We therefore estimate the following specification:

8(cid:2)

Yihs =

αhηh +

8(cid:2)

βhηhDi +

2012(cid:2)

−1(cid:2)

γsTs +

δsSis + εihs,

h=−5

h=−5

s=1999

s=−4

(1)

where Yihs is the outcome for individual i, h years after the

tax year selected for audit (with control observations having

h = 0 for the tax year for which they were drawn as controls),

when the current calendar year is s ≡ t + h. ηh are indicators

for being h years after the tax year selected for audit; Di is an

indicator for whether the individual is actually audited; Ts is

a calendar time indicator for tax year s; and {Si,−1, . . . , Si,−4}

are indicators for whether the individual was in the data in

each of the four years before audit. The error term, εihs, is

clustered at the individual level. Audit status, Di, is instru-

mented by (random) selection for audit, Zi. The coefficients

of interest are βh ∀h. These estimate the impact of the audit

on the outcome variable h years after the tax year selected

for audit, measured as the difference in the mean outcome

for those actually audited and those who would have been

audited only if selected for a random audit.

impact on those who were actually audited (i.e., the LATE).

The difference in the share audited between the treated and

control group is around 66 percentage points, so the LATE is

around 1.5 times the intention to treat estimate.

The impact of an audit peaks two years after the tax year

for which the audit is conducted. This is consistent with the

fact that many audits are not started until after the following

year’s tax return has already been submitted.13 Reported tax

among audited taxpayers is significantly greater than among

nonaudited taxpayers for five years after the audit, and the

point estimate appears to decline relatively smoothly, getting

close to zero by the eighth tax year after the audited year. This

pattern of effects is robust to changes in the level of trimming,

although, when lower levels of trimming are used, standard

errors are larger and consequently some significance levels

are lower (see online appendix C.2 for details).

From figure 2, we can estimate how much revenue audits

raise on average by changing the behavior of audited indi-

viduals. Over the five (eight) years after the audited year, the

dynamic effects bring in an additional £1,230 (£1,530), 1.5

(1.8) times the direct effect of audit. Although taxpayers in

the United States are explicitly told that the random audits

B. Overall Impact of Audits

Beyond the direct effects of the audit, described in sec-

tion II, we also see clear evidence of dynamic effects. Com-

paring individuals who were randomly selected for audit with

individuals who could have been (but were not) selected,

those selected for audit on average report higher levels of tax

owed in the years after audit. Figure 2 shows the estimated

13In our sample, almost a quarter of audits are not opened for more than

12 months from the date of filing (see table A1). Additionally, there can

be some lag between the tax authority “taking up” a case for audit and

notification being received by the taxpayer. If taxpayers each consistently

file at the same time every year, this implies at least one-quarter would

have filed without knowledge of the audit. More than half will have filed

without knowing the result of the audit (table A1). One could instead set

h = 0 as the time at which audit begins, but this information is not available

for controls, so it risks creating bias if the timing of opening audits among

individuals selected for audit is nonrandom.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

r

e

s

t

_

a

_

0

1

1

0

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE DYNAMIC EFFECTS OF TAX AUDITS

553

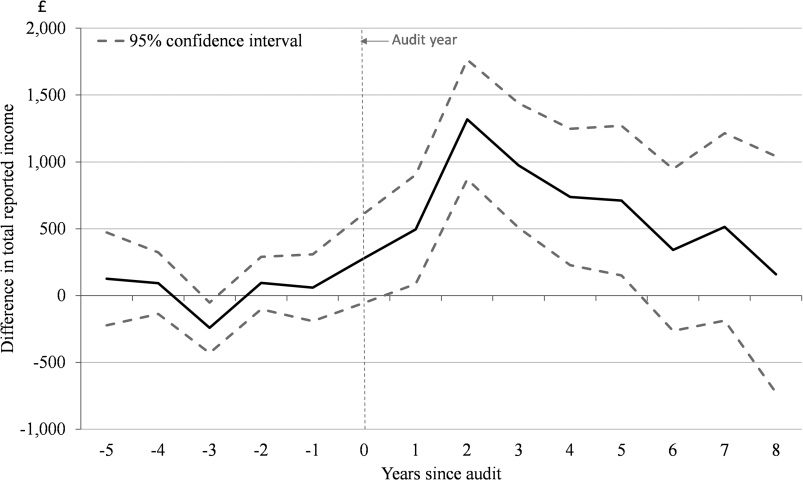

FIGURE 3.—DYNAMIC EFFECT OF AUDITS ON TOTAL REPORTED INCOME

Sample includes individuals selected for a random audit between 1998/1999 and 2008/2009, and control individuals who could have been selected in the same years but were not. It uses tax returns from 1998/1999 to

2011/2012. The solid line plots the point estimate for the difference in average “total reported income” (income from all sources) between individuals who were and weren’t audited, for different numbers of years after

the audit. This comes from a regression of total reported income on dummies for years since audit (or placebo audit for controls), dummies for years since audit (or placebo audit for controls) interacted with treatment

status, tax year dummies, and dummies for whether the taxpayer filed a return in each of the four years before audit, with audit status instrumented by selection for audit. Standard errors are clustered at the individual

level.

Source: Calculations based on HMRC administrative data sets.

are random, DeBacker et al. (2018) find a similar ratio be-

tween direct and indirect effects of audit. Ex ante one might

have expected smaller behavioral effects, because taxpayers

are aware that the authority is not acting based on any suspi-

cion of wrongdoing. Our exploration of the mechanism driv-

ing these dynamics will explain why, ex post, these effects

should be so similar: the dynamics are driven by constraints

to misreporting caused by audit, rather than belief-updating

or perceived reaudit risk, both of which may respond to the

reasoning behind the audit.

These dynamic effects highlight the policy importance of

studying the long-term impact of audits: when determining

the audit strategy, the revenue-raising effects of audits would

be grossly understated without considering the impact on fu-

ture behavior. This would imply too few audits taking place.

It is important to note that the optimal number of audits

will in general not equate the marginal return on audit to

the marginal cost of an audit. Audits require real resource

costs, while the direct benefits are a transfer of resources

from citizens to the state (see Slemrod & Yitzhaki, 1987 for

a longer discussion of this point). There are likely also indirect

benefits in terms of maintaining overall compliance, as well

as potentially intrinsic value placed in upholding the rule

of law (Cowell, 1990). Additionally, the social cost of audit

must incorporate not only the cost to the tax authority, but

also the cost to the taxpayer for which accurate figures are

difficult to come by (Burgherr, 2021). We therefore do not

attempt a full welfare analysis. Instead we merely note that

dynamic effects increase the resources that are transferred to

the state without increasing the administrative costs of audit.

Assuming that a positive weight is placed on such transfers,

taking into account dynamic effects increases the number of

audits that should be undertaken.

Figure 3 shows that a very similar pattern holds for the im-

pact on total income reported. Again there is a clear dynamic

effect, peaking two years after the audited year and declin-

ing to zero by year eight, though not significantly different

from zero by year five. This provides additional support to

the previous result for tax, and is not purely by construction,

because expenses can often be used to offset income to reduce

tax (Carrillo et al., 2017; Slemrod et al., 2017).

C.

Impact by Income Source

We repeat the previous estimation separately by income

sources, focusing on income sources for which at least 5% of

the sample report nonzero amounts.14 This will be one way

in which we discriminate between different possible expla-

nations for why we see dynamic effects.

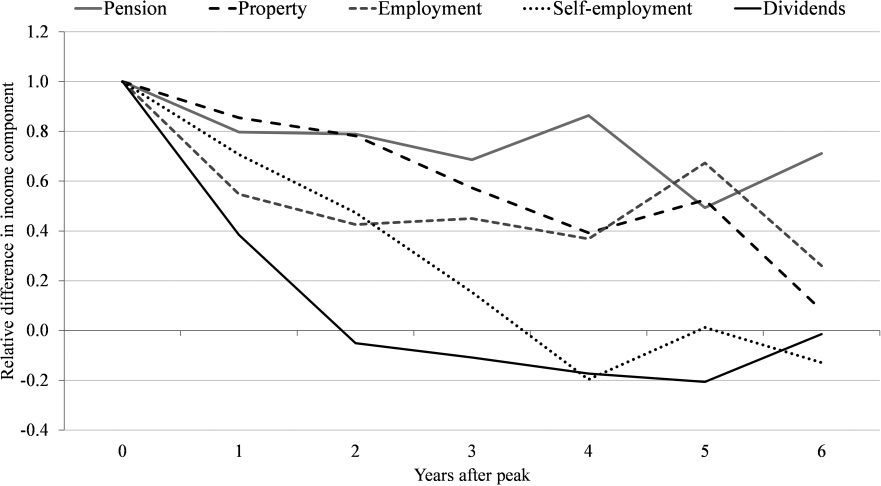

Figure 4 shows how the impact of an audit changes over

time for the different components of income. Since the mag-

nitudes of these incomes are different, for comparability we

rescale them relative to the peak impact for that income

source.

We see that, relative to the peak, self-employment income

and dividends decline relatively quickly. Three years later

point estimates for these are close to zero, that is, reporting is

14We exclude interest income, because it is very small and not everyone

needs to report this, making it hard to compare. See table 1 for information

on the share of individuals with each income source.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

r

e

s

t

_

a

_

0

1

1

0

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

554

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 4.—RELATIVE DYNAMICS BY INCOME SOURCE: LESS AUTOCORRELATED SOURCES OF INCOME SEE FASTER DECLINES

Sample includes individuals selected for a random audit between 1998/1999 and 2008/2009, and control individuals who could have been selected in the same years but were not. It uses tax returns from 1998/1999

to 2011/2012. Each line plots the point estimate for the difference in the average of a particular component of income between individuals who were and weren’t audited, for different numbers of years after the peak

impact for that income source. This comes from a regression of each income component on dummies for years since audit (or placebo audit for controls), dummies for years since audit (or placebo audit for controls)

interacted with treatment status, tax year dummies, and dummies for whether the taxpayer filed a return in each of the four years before audit, with audit status instrumented by selection for audit.

Source: Calculations based on HMRC administrative data sets.

TABLE 4.—AUTOCORRELATION BY INCOME SOURCE

Corr(t, t − 1) Corr(t, t − 2) Corr(t, t − 3)

Pension income

Property income

Employment income

Interest income

Self-employment income

Dividend income

Observations

.946

.896

.862

.835

.832

.813

4,506,548

.904

.836

.769

.722

.728

.723

4,506,548

.864

.790

.690

.640

.644

.657

4,506,548

Annual averages for years 1998/1999–2011/2012.

Source: Calculations based on HMRC administrative data sets.

not different to the control group. In contrast, pension income

exhibits little decline. Six years later it retains 80% of the

impact, and this is not statistically different from 100%. This

pattern is suggestive of the importance of autocorrelation:

income sources that one would expect to be more correlated

over time appear to show weaker declines.

Table 4 shows the autocorrelation for each income source.

Pension income is highly autocorrelated because it will typi-

cally be an annuity and therefore fixed over time; property in-

come is slightly less stable because rents may vary more; and

at the other extreme, self-employment and dividend income

are considerably less stable. The relative autocorrelations of

income sources line up exactly with their speeds of decline.15

There are two caveats to these results. The first is that these

measures are noisy, so if confidence intervals were added to

15Note that a comparison of pensions versus property income is helpful

in distinguishing this effect of autocorrelation compared with the effect of

third-party information. Both have a high autocorrelation, but pension in-

come was third-party reported while property income was not. In figure 4

we see essentially the same effect for both sources, despite the large dif-

ference in third-party information. Conversely, comparing property income

and dividend income—which, like property, is also not third-party reported

but has a low autocorrelation—we see very different effects.

figure 4 for each income source, many would overlap. The

second is that individuals with different income sources may

have different propensities for noncompliance.

To tackle these concerns, we next use two alternative strate-

gies. First, we compare within individuals who have multiple

income sources. This immediately solves the second problem

above because our results will be within individuals. It will

also lead to ten pairwise comparisons: every unordered pair

of the five income sources studied. For each pair, our sample

is composed of individuals who had both sources sometime

in the three years before audit. We then study the relative

fall in reporting of each of these income sources four years

after the peak. In each case, we expect to find that the less

autocorrelated source falls fastest.

We find this result in eight out of ten cases. If there were

no relationship, we should find this to be true in around five

of the tests. The probability of this result under the null of

no relationship is 5.5%, close to standard significance thresh-

olds. Hence more autocorrelated income sources do seem to

decline more slowly than less autocorrelated ones.

Our second strategy to tackle concern about heterogene-

ity in who receives different income sources is to reweight

individuals based on individual characteristics. This ensures

that the distribution of observed characteristics is the same

across recipients of different incomes. We divide individuals

into groups by sex, age band (below 40, 40–65, and above

65—the UK state pension age at which people typically re-

tire), and quartiles of filing history. We then run weighted

regressions so that the weighted samples match closely the

distribution of these characteristics seen among individuals

with self-employment income. We replicate figure 4 using

the results of the reweighted regression, shown as figure A2.

The results look very similar—the only noticeable effects are

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

5

3

5

4

5

2

0

8

9

9

7

9

/

r

e

s

t

_

a

_

0

1

1

0

1

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE DYNAMIC EFFECTS OF TAX AUDITS

555

that property income appears to decline slightly faster than

previously, and dividend income much faster.

Our interpretation for this result, which we formalise be-

low, is that audits provide the tax authority with information.

Where errors are uncovered, taxpayers file amended returns.

Although we do not know, and would not be allowed to reveal,

precisely how audit targeting is done, it is clear that “surpris-

ing” deviations from recorded historic reports are part of this.

The amended return is therefore creating a new benchmark

against which future returns will be compared. Hence, income

from highly autocorrelated sources will—once uncovered—

be hard to hide again, as deviations from the truth will be

easily noticed. In contrast, declines in less autocorrelated in-

come sources are less informative to the authority because

they may well be real for an individual taxpayer. Viewed in

aggregate, falls and rises should be equally likely, because

the control group will account for any trends in the income

source. Hence when we observe a decline in aggregate in-

come reports (e.g., for dividend income among audited tax-

payers), this can be attributed to noncompliance, although

we cannot identify which individuals are the ones underre-

porting. Because declines are faster for less autocorrelated

income sources, this suggests the importance of information

provision. This is something we know to be important from

other settings (Kleven et al., 2011; Pomeranz, 2015), although

the value of audits as a potential source of information about

future tax has not previously been recognised.

One caveat to this interpretation is that falls in reporting

could alternatively be driven by changes in actual income.

For example, those who are audited might sell shares to pay

fines, reducing dividend income. Whilst this is possible, it

seems unlikely. In cash terms, the peak additional income

reported for those who have dividend income is £414. As-

suming a high-end estimate for the dividend yield of 10%

implies £4,140 of undeclared shares. Conservatively assum-

ing also that individuals are on the higher rate of income

tax, this implies an additional £135 of tax owed. The abso-

lute maximum penalty for misreporting is 100% of the tax

due (on top of paying the tax). So selling all these shares

(and hence looking like the control group) would be needed

only for an individual who is found to have misreported for

at least fifteen years, and receives the maximum fine. While

such cases might exist, it seems extreme to assume that this

is occurring on average. Hence we think it is unlikely that

the observed pattern represents changes in real behavior,

rather than reporting, though we cannot definitively rule it

out.

V.

Impacts by Audit Outcome

We next consider how dynamic effects vary depending on

the outcome of audit. This is important for policy, as it helps

distinguish whether merely the process of being audited is

enough to impact reported income and tax. We find that those

who were found to be correct do not respond, while those for

whom errors were found increase reported tax. Being audited

per se does not appear to increase reported tax—that is, there

is no change in behavior among compliant taxpayers—but

those found to have underpaid are 18 percentage points more

likely to report higher tax owed after audit. We first describe

the approach taken to study this question, because our pre-

vious control group cannot help us study effects by audit

outcome. We then describe the findings highlighted above.

A. Empirical Approach

Since we now wish to study audit impacts separately by au-

dit outcome, we cannot use the earlier identification strategy.

In the “placebo audit” group, we cannot observe what audit

outcomes would have been, so we cannot construct separate

control groups for each audit outcome. Gemmell and Ratto

(2012) studied this question by comparing each treatment

group to the original control group containing people with a

mix of possible outcomes, implicitly assuming that audit out-

comes are exogenously assigned. More recently, Beer et al.

(2020) used a matched difference-in-difference approach, al-

lowing for observable differences in audit outcome.

We take an event study approach to answer this question.

Our sample for each regression is the set of observations for

individuals who are audited and found to have some particular

outcome (e.g., found to be compliant). Within that sample,

the timing of audit is random—there is nothing systematic

that led individuals to be selected in a particular year within

the sample. Hence we can compare the outcome for some-

one audited and found to have a particular status (e.g., to be

compliant) with someone who will be audited and found to

have the same status.

For our variable of interest, we now focus on a binary

variable measuring whether tax paid increases, rather than

on the sizes of the increase, as in Pomeranz (2015). In par-

ticular, we estimate a linear probability model in which the

outcome is whether tax paid in year t is larger than in the

year before audit. Our interest now is understanding which

individuals—when split by audit status—respond. This out-

come is therefore preferred because it compares individuals

to their own history, and it is equally responsive to increases

for individuals across the distribution of taxes owed. It is

also less sensitive to relatively extreme observations, which

is more important in our event study approach because the

sample size is now much smaller. Whereas previously we

had a treatment group of 53,000 individuals, and could draw

a large sample of controls from the nonaudit population, now

the entire sample is those selected for audit. That sample

is then further split into subsamples by audit outcome status,

making results more sensitive to outliers and reducing power.

Use of a binary variable removes this sensitivity without lim-

iting our ability to study which groups respond.

In our specification we control for a number of key covari-

ates: sex, age, industry, region, and years filing, as well as

calendar-year fixed effects. Many of these individual char-

acteristics have been shown to be predictive of noncompli-

ance (Advani, 2022), so if responsiveness to audit also differs

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1