Jake Kendall, Bill Maurer, Phillip Machoka,

and Clara Veniard

An Emerging Platform:

From Money Transfer System to

Mobile Money Ecosystem

In the past, the emergence of new network infrastructures (canals, railroads, elektr-

tricity, telecommunications, the Internet, usw.) has had a profound effect on the

world economy.1 New ways of moving people and goods, Energie, and information

often led to waves of innovation, and over the centuries these innovations have

transformed markets as existing firms restructure and new firms emerge to cap-

ture new opportunities. Mobile money, while often described as a money-transfer

product, is in fact a network infrastructure for storing and moving money that

facilitates the exchange of cash and electronic value between various actors,

including clients, businesses, the government, and financial service providers.

As with many other types of network infrastructure, mobile money displays

the characteristics of a platform, as it brings together financial service providers

and clients and provides them with a core functionality they can use to transact,

and which can be incorporated into various financial products.2 Platforms such as

the Internet, Facebook, iPods, smart phones, video games, and financial and com-

mercial exchanges also have great power to stimulate innovation and change exist-

ing business models. As a network infrastructure and a platform for financial serv-

ices innovation, mobile money appears to have the potential to radically reconfig-

ure how retail finance is handled in developing countries.

There are a number of fundamental challenges to reaching the poor with

financial services that have blocked market growth in the past. Perhaps the key

Jake Kendall is Program Officer with the Bill & Melinda Gates Foundation.

Bill Maurer is Professor of Anthropology and Law at the University of California,

Irvine, and Director of the Institute for Money Technology and Financial Inclusion.

Phillip Machoka is a Lecturer in Information Systems and Technology at the United

States International University, Nairobi.

Clara Veniard is Associate Program Officer at the Gates Foundation.

The views expressed herein should be considered the personal views of the authors

alone and may not reflect the views of the Gates Foundation.

© 2012 Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

Innovationen / Volumen 6, number 4

49

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

Mobile Money Players in Kenya

Mobile operators in Kenya have launched mobile money services similar to

Safaricom’s M-PESA during the past two years, including Yu (YuCash), Orange

(Orange Money), and Zain (Zap). Jedoch, M-PESA remains the most widely

used mobile money service and is the focus of our study.

challenge is that the vast majority of the poor lives in a cash economy and is paid

in cash. In developed economies, banks usually receive clients’ salaries via direct

deposit, and the money can either be moved to longer term savings products or be

withdrawn and spent through channels like ATMs and point-of-sale devices. In

developing economies, the poor lose the natural connection to the financial system

that stems from having income born in electronic form. They require a deposit-

taking infrastructure to even get their money into the bank in the first place, Und

to make matters worse, the poor often earn money unpredictably and need to

deposit whenever small windfalls come their way. In der Zwischenzeit, banks and other

financial service providers are loath to deploy deposit-taking banking infrastruc-

tur (d.h., branches and two-way ATMs) as intensively as they might require to

service poor clients’ greater deposit needs, since the revenue these clients generate

does not justify the investment. Tatsächlich, even clients who do not require intensive

deposit services (z.B., those who might receive direct government transfers or mil-

itary pensions) are rarely seen as profitable customers by banks, given the low bal-

ances they hold and the high transaction costs of traditional banking infrastruc-

tur.

Mobile money appears to have the potential to solve many of these issues. Von

giving banks and other financial service providers a cheap way to outsource cash

handling and deposit and withdrawal transactions, mobile money can enable

providers to serve clients at a lower cost per transaction and with a reduced invest-

ment in physical infrastructure. Darüber hinaus, by unbundling and outsourcing trans-

action handling, banks may be able to get more value out of their existing branch-

es and branch staff. They can refocus them on more value-adding and complex

tasks, such as wealth and risk management advisory services and cross-selling

Produkte. Mobile money also helps clients by giving them a dense network of

transaction outlets where they work and live, reducing the cost to clients of access-

ing financial services. Once clients are in the financial system and able to transact

at low cost with banks and other financial service providers, the platform enables

the provider to offer a new set of services and delivery models that were not previ-

ously possible or profitable.

The excitement over mobile money in the financial inclusion field is driven by

the possibility of providers offering savings, Kredit, insurance, and other products

to the poor at low cost. But whether mobile money will achieve this lofty vision

depends on a number of factors. First and foremost is that networks and platforms

usually require scale to have a significant impact. Zweite, even if mobile money

50

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

reaches the poor, other barriers might inhibit innovation in financial services for

this population segment. Endlich, mobile money may simply not lower clients’ and

providers’ costs enough to be truly transformative.

In Kenya, Safaricom’s M-PESA has managed to overcome the “last mile” prob-

lem

the difficulty of delivering a service over the very last leg of its journey to a

remote client by creating a network that connects over 70 percent of Kenyan

households to the financial system (13.3 million people, etwa 60 Prozent

of all adults in Kenya).3 The M-PESA network handles more transactions in a year

than Western Union does globally, and the value of transactions represents more

als 15 percent of Kenya’s GDP.

Unlike other deployments around the world that are struggling to achieve

scale, penetration is no longer the barrier limiting the benefits of this platform.

Trotzdem, having only been launched in 2007, M-PESA is still in its early stages

Und, while the uptake of M-PESA has been spectacular, it is not yet clear what the

final effect will be on the wider retail market or on the number of poor people who

access the financial system. Some in the financial inclusion field suggest there is an

“innovation gap” and that M-PESA is failing to live up to its original promise, Aber

it is too early to tell whether innovation is simply not there or is still gaining

momentum as the market comes to grips with a new way of doing business.4 It is

also too early to tell who will drive innovation—will it be M-PESA, or new and

existing players riding on the M-PESA wave? If others build products and plat-

forms on top of the M-PESA platform, the possibilities for innovation will expand

greatly.

In diesem Papier, we present the results of some initial probes into understanding

how market players are harnessing M-PESA as a platform for new services, und zu

gauge the emerging ecosystem of these services enabled by M-PESA.

We looked for existing financial institutions that are integrating M-PESA into

their service offerings, and for startups and new ventures that are launching new

“pure-play”services, das ist, services that operate primarily through the M-PESA

platform (analogous to pure-play e-commerce services that operate exclusively

through the Internet). In addition to a basic survey to provide a landscape of this

space and to measure the level of activity in the space, we sought to understand

some of the motivations for using mobile money within a new wave of financial

services and some of the challenges these new and existing financial service

providers face in doing so. We conducted the survey through Internet research and

phone calls, and then had a mini-conference in Nairobi on January 14, 2011, bei

which we brought together some financial service providers and information tech-

nology service firms that have begun to specialize in M-PESA product integration.

We also incorporate results from a recent study conducted by Microsave for

the Bill & Melinda Gates Foundation, which assesses new mobile money-enabled

products and services using information available from desk research, Interviews

with the implementers and users, secret shoppers, and focus groups.

Our investigations document the significant integration of mobile money into

the products and services offered by existing financial institutions in Kenya. Wir

Innovationen / Volumen 6, number 4

51

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

Application Programming Interfaces for Mobile Applications

Application Programming Interfaces (APIs) are sets of instructions that allow

different software applications to interface with one another. Well-designed APIs

are powerful because they allow the development of new applications that seam-

lessly incorporate the functionality of the original system into their workings.

APIs are a recent innovation: their origin is in TCP/IP network architecture, Aber

their use for user-oriented application development dates to the mid-1990s. Der

invention of M-PESA corresponds in time to the explosion of interest in APIs for

third-party application development, itself propelled by the mobile revolution,

so it can hardly be blamed for having a poor API (PayPal, Zum Beispiel, launched

APIs in 2010).

find that numerous technology firms have sprung up to facilitate this integration

between financial service providers’ back-end systems and new mobile money

platforms. We also find a number of innovative new businesses and pure-play

startups that offer financial services that operate solely via mobile money.

Institutions integrating with existing products and those launching new ones both

frequently cite improved outreach and lower costs, especially with poor clients, als

motivations for adopting the mobile money platform. That said, significant barri-

ers remain that block the development of a fully integrated ecosystem, einschließlich

the high price of person-to-person transfers and the difficulty of integrating with

the M-PESA application programming interfaces (APIs; see text box 2). From our

conversations with providers, we also infer that those wishing to outsource their

day-to-day cash transactions with clients may face a new challenge, as they must

find new opportunities for interactions with their clients to create rapport, build

trust, educate, and cross-sell new products.

MARKET ACTIVITY IN BROAD STROKES

Even though we were not able to conduct a complete census of the market, unser

search identified over 300 formal businesses that are integrated with M-PESA and

other mobile money services. All of these businesses are large enough and formal

enough to have a web presence. We did not seek to assess whether smaller or infor-

mal businesses are using M-PESA, although many also appear to be doing so.

Außerdem, we found almost 90 formal financial institutions that have integrat-

ed their operations with mobile money (primarily M-PESA) and few providers

that do not have mobile money integrations completed or under way. Financial

service providers range from traditional banks, savings and credit cooperatives

(SACCOs), and insurance providers to newer mobile-based credit, insurance, Und

mobile savings offerings.

Many of these integration efforts and products are still in an early stage, Und

some of the new products have few active customers. More detail on the market

activity we found follows.

52

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

LANDSCAPE OF “INNOVATORS,” “INTEGRATORS,”

AND “BRIDGE-BUILDERS”

For the purposes of our study, we developed a shorthand. We call financial service

providers “integrators” when they add mobile money as a service delivery channel

for an existing line of products, and “innovators” when they offer new entrepre-

neurial products or ventures launched around a purely mobile money-based busi-

ness model. We call application developers that specialize in mobile money inte-

grations for financial and payment services “bridge-builders.”

Integrators

Most financial service providers in Kenya are joining mobile money platforms as a

channel through which their clients can make deposits and withdrawals from bank

accounts and other financial products. Financial service providers integrate with

mobile money platforms using a variety of mechanisms that vary according to the

institution. These linkages are often difficult and expensive to create, and many

providers we spoke to are wrestling with the process. In our analysis below we

focus on M-PESA, since it is by far the dominant platform, although other mobile

money providers exist.

No official API exists that service providers can use to integrate with M-PESA.

With the exception of the M-KESHO product described below, financial service

providers typically adapt two different one-way mechanisms to move money to

and from clients. M-PESA’s Pay Bill function allows clients to send deposits from

their M-PESA account to the financial service provider, whereas most providers

use custom built “screenscraping” programs that connect to M-PESA’s bulk pay-

ments web page to automate the sending of large numbers of withdrawals. Der

screenscraping programs capture data from terminal display screens. Banks can

avoid the bulk pay screenscraping by using a SIM card, which is activated directly

by the bank’s server. Jedoch, these integrated SIM cards are extremely slow and

not suitable for sending more than a few dozen transfers per minute, so they are

rarely used. In some cases, financial service providers opt to use a third-party

“middleware” software application to facilitate integration with M-PESA, although

these also use the bulk payments channels to activate payments.

Most providers offer clients two separate interfaces for making deposits and

withdrawals. Deposits are done through the normal Bill Pay option in the M-PESA

menu on their phone. Clients must then use a USSD-based interface (described

below) that allows them to trigger withdrawals to their M-PESA account. Here we

describe how some of the integrations work.

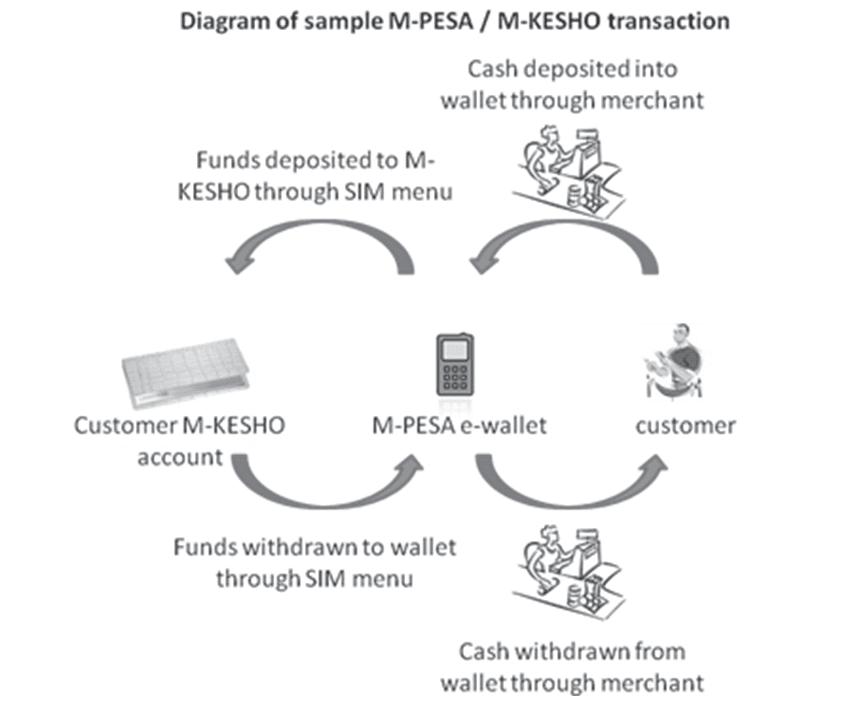

M-KESHO link with M-PESA. Equity Bank, with over six million bank

accounts that constitute 55 percent of all accounts in Kenya, is perhaps the most

active in the mobile money space and has the strongest link with M-PESA. In May

2010, Equity partnered with Safaricom to launch the M-KESHO product. M-

KESHO is the first bank product with a real-time link to M-PESA for deposits and

withdrawals via an easy-to-use SIM-based menu. It is branded by both Equity

Innovationen / Volumen 6, number 4

53

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

Figur 1. Diagram of Sample M-PESA/M-KESHO Transaction

Bank and M-PESA and can be opened directly at an M-PESA agent. The two main

elements that differentiate the M-KESHO product from others is that both

deposits and withdrawals can be initiated through the SIM-based menu, als

opposed to relying on the less user-friendly USSD menu. Figur 1 shows the

mechanics of M-KESHO’s interface with M-PESA. Zusätzlich, and perhaps more

importantly, the product was marketed and branded as a joint effort, which prob-

ably boosted initial uptake substantially.5 In November 2010, Equity partnered

with the mobile operator Orange and launched its own mobile money product to

try to increase competition with M-PESA. Along with the cash merchant network

Orange plans to develop, Equity will establish its own cash merchants, thereby fur-

ther increasing customers’ access to financial services through mobile money.

No financial services provider other than Equity Bank has managed to inte-

grate directly with M-PESA. No formal interface exists for the others, und sie sind

forced to adapt the Pay Bill function to facilitate deposits and the bulk payments

web menu for withdrawals, as described below.

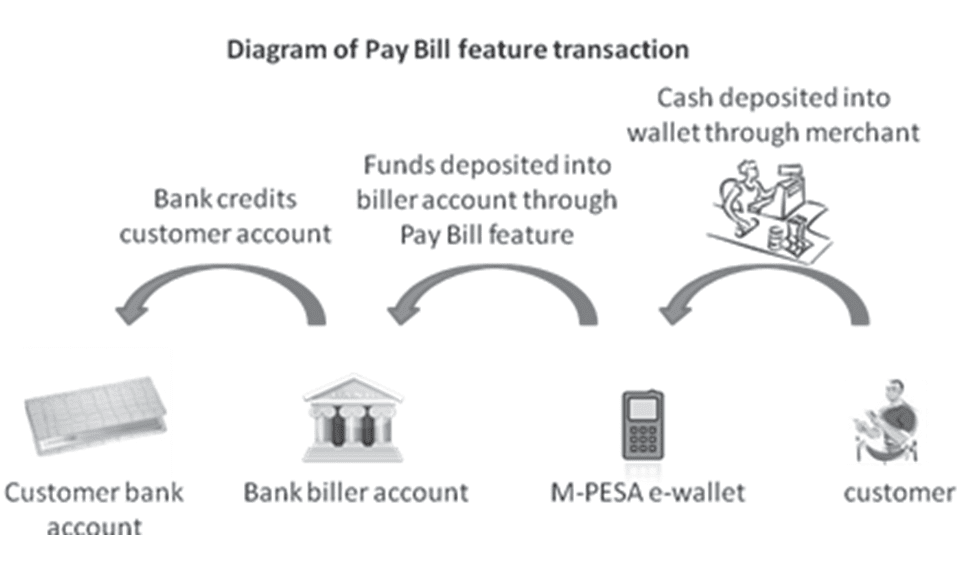

Deposits through the Pay Bill feature. Pay Bill can be accessed from the M-PESA

SIM menu. It allows customers to transfer money from M-PESA to their bank

54

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

account, although they are not able to withdraw funds. The customer experience

is similar to paying a bill: she selects Pay Bill, enters the short code for the recipi-

ent, which M-PESA calls a “business number,” as well as her own account number,

as she would, Zum Beispiel, with an account number at the power company. Das

directs a transfer to be made from her electronic “wallet” to the bank’s biller

account. Most banks allow deposits through the Pay Bill channel, even if they have

not yet managed to facilitate withdrawals through M-PESA.

The Pay Bill feature can also be used to connect to other financial accounts.

Kenya Women Finance Trust bank, Zum Beispiel, is a microfinance institution that

leverages M-PESA’s Pay Bill feature to enable customers to make loan payments.

The CIC Insurance Company uses M-PESA’s Pay Bill to allow customers to pay

insurance premiums using a mobile phone. Customers can save Ksh 140

(US$1.75) every seven days, earn interest, and access immediate life insurance cov- erage of Ksh 50,000 (US$625), which increases to Ksh 100,000 (US$1,350) by the twelfth year. The company absorbs the remittance charges that M-PESA places on Pay Bill transactions. Figur 2 (following page) shows the mechanics of a Pay Bill feature transaction. Withdrawals using bulk pay and USSD. A subset of financial institutions enables customer transactions through M-PESA in the other direction (d.h., mit- drawals) using a bank-run USSD menu. Institutions pursuing this approach include Barclays Bank of Kenya, Kenya Commercial Bank, Co-operative Bank, NIC Bank, Family Bank, K-rep Bank, Kenya Post Office Savings Bank, and Faulu Kenya. In order to process a withdrawal, customers have to link to their bank’s m-bank- ing platform by dialing a USSD code (Zum Beispiel, *498# for Kenya Post Office Savings Bank). Funds are then transferred from the bank account to Safaricom and into the customer’s M-PESA wallet. Once the funds are deposited into the wallet, the customer receives a message that funds are available. Banks typically automate the high volume of withdrawals using M-PESA’s web-based interface for bulk payments. Since this web interface is designed to be used manually and no API exists to integrate with this page, financial institutions typically write a custom built screenscraping application. This application manip- ulates the web page like a real user, uploading payments in real or near real time and sending them to clients who have requested a withdrawal. Screenscraping techniques are notoriously unstable, and many providers’ interfaces have broken down when Safaricom made even minor changes to the web interface. Figur 3 shows a diagram of the mechanics of a transaction using the USSD channel. Neither the Pay Bill deposits nor the bulk payment withdrawals need to be real time because the bank does not have to credit the client account immediately. Stattdessen, providers typically send the bulk pay transactions in a batch on a set fre- quency; Jedoch, most do this every few minutes. Leveraging bridge-builders. Some financial institutions also leverage bridge- builders to facilitate connections with M-PESA, either by building custom applica- tions to facilitate integration or by offering middleware applications that automate the integration process for multiple smaller institutions. Zum Beispiel, Meru innovations / Volumen 6, number 4 55 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023 Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard Figure 2. Diagram of Pay Bill Feature Transaction Mwalimu SACCO integrated its products with the M-PESA platform through Spotcash, a service that allows members of SACCOs and microfinance institutions to withdraw and deposit their money from and to their savings account, bzw- aktiv, through SMS, USSD, IVR (interactive voice response), or WAP (wireless application protocol)6. Once the withdrawal request has been received, the money is transferred to the member’s M-PESA account. The cost is Ksh 10 per transaction (US$0.12), not including SACCO fees or Safaricom withdrawal fees. Ein anderer

example is Celullant, which has developed integration solutions for many banks,

including a platform for the World Council of Credit Unions, that will enable

SACCO to connect with M-PESA.

Innovators

Innovators are new entrepreneurial ventures or products with a purely mobile

money-based business model for financial services.7 They fall into two categories:

existing providers developing new types of products that only operate through the

mobile money channel, and new entrepreneurial ventures launched around

mobile money-based products. In both cases, the new products facilitate transac-

tions through the mobile phone and mobile money agents, rather than through

legacy channels like retail bank outlets or sending money by check or money order.

Savings and insurance seem to be particularly popular financial products in this

Raum, probably as a result of the need for frequent small-value transactions that

would be expensive to facilitate through normal retail channels—both for clients

who would have to travel further and for institutions that would have to maintain

a retail channel.

56

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

Figur 3. Diagram of USSD Transaction

Examples of innovators. Our research uncovered a number of newly launched

savings, Kredit, and insurance products for which mobile money is integral to their

delivery model. These products run on the mobile money platform and help low-

income Kenyans save for retirement, Gesundheitspflege, and other needs, to borrow, oder zu

open small-value insurance contracts. Many are targeted at customers who do not

have steady incomes and cannot afford to make regular monthly lump-sum pay-

ments and thus appreciate a service that allows them to make small-value pay-

gen. A few sample products include:

• Zimele asset management offers a new pension scheme in which clients can

remit a deposit of as little as Ksh 250 (US$3.13) on a regular basis via the Pay Bill feature and earn interest at a rate of 8.5 percent quarterly. Zimele started this in late 2008 and claims it is getting a good response from depositors who want to avoid traveling to the head office to pay installments. • The Jua Kali Association (an association of self-employed informal workers) offers a new pension product that can be funded through mobile money, inkl- ing M-PESA. Users can save for retirement via the Pay Bill feature starting at Ksh 20 (US$0.24). This product has allowed Jua Kali to more than double the num-

ber of pension accounts in only six months.

• Changamka Microhealth, Ltd., offers a medical savings plan for out-patient and

maternity health care for expectant mothers. Customers use M-PESA’s Pay Bill

function to save small contributions to a smart card, where the money is locked

in for use when one falls ill or needs maternity care. In selected clinics, customers

can pay for medical services at a discounted rate using the smart card.

Innovationen / Volumen 6, number 4

57

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

Contributions to the smart card can also be made via M-PESA from family

members, friends, and other community members.

• UAP insurance company partnered with the Syngenta Foundation for

Sustainable Agriculture and Safaricom to help farmers insure against drought

when they buy certified seeds and fertilizers through a program called Kilimo

Salama (safe farming). This scheme offers a micro-insurance policy to small-

scale farm holders who plant on as little as one acre. It covers them from finan-

cial losses caused by drought or excess rain. Dealers are equipped with a camera

phone that scans a bar code at the time of purchase and immediately registers

the policy with UAP Insurance through Safaricom. An SMS confirming the

insurance policy is sent to the farmer through the mobile phone. When data is

transmitted through the Safaricom network from a particular weather station

indicating that extreme weather conditions are going to cause crop failure, all the

farmers within the region of that station automatically receive a payout via M-

PESA. Im September 2010, rain shortfall in the Embu region allowed over 100

farmers to receive an insurance payment via M-PESA. This was the first crop

insurance claim to be paid through a mobile payment system.

• M-PESA has also enabled the launch of entirely new service providers, einschließlich

a virtual microfinance institution named Musoni. Musoni only offers credit

services, although they hope to provide deposit services in the future, and all

operations are cash free, with disbursements and repayments done through M-

PESA’s Pay Bill feature. Zusätzlich, Musoni has developed a server that creates

reports based on data provided by Safaricom and facilitates lending operations.

Musoni customers are not charged for repaying through M-PESA or for the loan

disbursement through M-PESA. The customer is only responsible for paying the

cash-out fee from their M-PESA wallet.

Bridge-Builders

As financial service providers and other businesses struggle to integrate with M-

PESA, a mini-industry of software developers and integrators has started to spe-

cialize in M-PESA platform integration. A number have also built and begun mar-

keting their own middleware applications, which usually specialize in facilitating

certain types of integrations. These bridge-builders fall into two broad categories:

those that are strengthening M-PESA’s connections with financial institutions for

the delivery of financial products, and those that are strengthening M-PESA’s abil-

ity to interoperate with other mobile and online payment systems. The lack of

functional M-PESA API is hindering bridge-building, but several companies have

nonetheless devised tools for new financial functions and online payments.

Connectors with financial service providers. A number of technology companies

are facilitating mobile money’s connections with financial institutions, especially

small financial institutions struggling to integrate with M-PESA. Tangazaletu, für

Beispiel, is developing a set of tools to integrate financial systems with M-PESA

through an application called Spotcash, which allows members of SACCOs and

58

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

microfinance institutions to deposit and withdraw money to and from their sav-

ings accounts through the Pay Bill or a USSD menu at a cost of Ksh 10 (US$0.12) per transaction. A number of other providers are building or offering similar con- nections to M-PESA for small financial institutions, such as Kopo Kopo and Coretech Systems. Zege Technologies has developed an M-PESA integration, automation, and aggregation solution called MPAYER, which eases the process of frequent payments to and from M-PESA by processing payments on demand. Pay Bill transactions are currently manually processed in batches at scheduled times, thereby causing delays and resulting in errors. Connectors with other mobile and online payments. Other technology compa- nies are strengthening mobile money’s ability to interoperate with online payment systems. Webtribe’s Jambopay, Symbiotics’ Moca, Intrepid Data System’s iPay, and Pespal are a few examples of payment services that allow buyers to pay for goods and services over the Internet using their phones. We found mention of over 20 companies that were performing this type of integration or writing their own middleware applications to facilitate it. Although not all of them operate in the financial services space, a significant number are pre- senting strong evidence that there is sustained demand from financial services players to adopt the mobile money platform. MOTIVATIONS FOR ADOPTION AND PERCEIVED BENEFITS FROM MOBILE MONEY In surveying the landscape of financial service providers that are harnessing the mobile money platform and the software development firms that are facilitating integrations, a few common themes emerge. Providers state a number of different reasons to adopt mobile money, most of them related to expanding geographic outreach and facilitating payments more cheaply. Some benefits accrue mainly to clients, some to suppliers, but there are also several mutually beneficial features of mobile money integrations. From the client perspective, integrating with mobile money increases the den- sity of access points and the reach of access points in new areas, transforming the geographical distribution of delivery channels. Many financial service providers cite the lower cost in time and money for clients who want to make payments and deposits or receive insurance payments, withdrawals, or loan disbursements. Smaller institutions in particular lack widespread distribution networks (some have only a single branch) and thus can benefit from plugging into an ubiquitous, low-cost retail delivery channel. Some institutions also report that the existing ATM network is not well situated for the poor. Zum Beispiel, Nayndarua Teachers SACCO notes that ATMs are clustered around wealthier and urban areas far away from their low-income and rural clientele. Providers may also gain from behavioral and other benefits. Savings clubs can have more efficient meetings because more time can be spent attending to business and less to counting the money that members brought in for payments.8 innovations / Volumen 6, number 4 59 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023 Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard Furthermore, because the mobile money platform provides real-time remittance transactions and feedback (including instant SMS receipts), it can help build trust and promote savings and repayment behavior. There may be additional benefits to clients’ having all their financial relationships and transactions available through a unified interface that is with them at all times—that is, their mobile phone. From the supplier perspective, there are a number of benefits afforded by the reduced need to deal with cash. Several providers suggest that keeping money in electronic form with clear records of every transaction is valuable in reducing the risk of theft and misappropriation by employees. Providers are also able to save on cash-handling and collection costs. By removing the need to keep retail locations and field agents stocked with cash, many costs and risks are removed for both sav- ings and lending operations. Zum Beispiel, with its purely mobile-based business model, Musoni hopes to maintain very low-cost operations. This not only reduces costs for the provider, it can also enable previously unprofitable small-value trans- actions—although M-PESA’s transaction fees are still too high to generate this benefit in significant amounts. Not having to handle cash also frees up staff time to focus on sales and other important tasks. This is especially valuable for smaller financial institutions, such as SACCOs and other small financial services that value individualized sales and customer service for low-income customer segments (through their closer connec- tion with this client base) but that are poor at service delivery. CHALLENGES PROVIDERS FACE INTEGRATING WITH MOBILE MONEY IN KENYA Many providers report that building mobile money into new and existing products has posed challenges at all levels, from the operational to the strategic. The most common complaints are as follows: Cost of transactions is the main barrier to integration with mobile money, espe- cially M-PESA. The high cost of M-PESA transactions, which can amount to more than US$1.00 for a round-trip deposit and withdrawal transaction (though clients

and institutions usually split this cost in some way), is a significant barrier for

offerings where frequent small payments are necessary. Providers are excited about

the ability of M-PESA to facilitate low-value transactions—many of the innovative

products linking to M-PESA allow very small transactions—but M-PESA’s fees are

still too high to be viable for the client, especially the person-to-person fee of more

than US$0.40. Many providers cite this as a key barrier to reaching lower income

clients, who prefer to risk storing the money at home or saving through other

informal means than to pay these fees. Infolge, some providers, such as Kenya

Bankers Sacco Society, Musoni, and Zimele Asset Management, cover all or a por-

tion of the fees charged by M-PESA. Although M-PESA transaction fees were cost-

effective when building the business, especially when compared with traditional

retail channels, they are limiting the viability of smaller value transactions and thus

limiting outreach to the poor. With Equity Bank/Orange entering the market and

60

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

Airtel Mobile money currently relaunching the ZAP product, Safaricom may even-

tually face some pressure to reduce prices on transfers.

Integration costs and poorly performing M-PESA APIs are a key challenge. Ein

equally common complaint is that integrating with mobile money is difficult and

M-PESA has no real API to speak of. As detailed above, most providers have to

hack together a system whereby clients access a session-based phone menu (USSD)

to enable withdrawals via the web interface and use M-PESA’s Pay Bill function to

send money back the other way. Neither mechanism is optimized for the tasks they

are performing, and the Pay Bill function actually requires most financial service

providers to have a custom integration to collect client data, link it to information

received from M-PESA, and input both sets of information directly into their

back-end systems. The poor API functionality causes many institutions to incur

large integration costs, and they suffer from poor performance and system down-

time whenever Safaricom’s interfaces change.9 This is especially problematic for

smaller institutions with limited in-house software development capability, Und

whose lower scale of operations combined with often older (even Excel spread-

sheet-based) back-end systems make integration a challenge.

While M-PESA’s API was considered the worst, other mobile money APIs in

Kenya are not much better. Yu-cash is lauded as having the best API, although its

extremely limited agent footprint and client base make it of little use to banks seek-

ing to reach the mass market.

Challenges of building and maintaining relationships with clients when offering a

service indirectly. While clients’ low levels of literacy, lack of familiarity with tech-

nology, and limited exposure to financial products are challenges many financial

institutions cite in dealing with the poor, these are exacerbated when mobile

money is used, as it implies less face-to-face contact with clients. Infolge, Die

large savings to banks and to clients from having fewer transactions with the teller

come at the expense of reduced client contact. This may make client outreach,

trust-building, Ausbildung, and cross-selling more challenging, especially for

providers that do not have brand recognition. Mamakiba, Zum Beispiel, is an early

stage venture that offers pre-paid prenatal care and childbirth services to allow

mothers to save for births rather than borrow. Given the lack of face-to-face con-

tact and the unknown brand, clients were at first skeptical that these services would

actually be available when they were ready to give birth. Mamakiba had to count-

er this with extra client outreach to establish trust.

We believe reduced direct client contact is a fundamental challenge that is cre-

ated by the efficiency-enhancing separation of the cash transaction service func-

tion from the customer service and sales functions. These functions used to be

combined in one retail outlet where they overlapped, facilitating client contact and

client relationship management whenever someone came in to deposit or with-

draw cash. Now they are separated, challenging providers to develop new models

for fostering positive interactions with customers. One potential bright spot is that

while mobile money is a payment service, it comes through a mobile phone, welche

Innovationen / Volumen 6, number 4

61

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

facilitates new ways to communicate with customers via text and voice messages.

Some providers are already experimenting in this area.

Other issues reported included lack of phones among some of the poorest

Kenyans—many poor Kenyans borrow phones from others, making it difficult for

financial service providers to confirm a client’s identify before allowing them to

withdraw money or receive funds—and poor service, including lack of float at the

agent or downtime of the mobile operator’s network.

CONCLUSIONS

M-PESA was launched only four years ago, and its rate of uptake in the population

has taken even Safaricom by surprise: über 70 percent of households and 60 pro-

cent of adults in Kenya use it regularly.10 Existing financial service providers offer-

ing new or enhanced products and entrepreneurs seeking to hatch new ventures

have had little time to develop and test business models. Trotzdem, our prelim-

inary investigations in Kenya reveal a growing demand from banks, microfinance

institutions, and SACCOs and other financial service providers to connect their

products to the platform provided by M-PESA. We found few financial institutions

that did not have some form of mobile money integration completed or under

Weg, and documented 90 specific cases that did.

We also uncovered a number of new entrepreneurial ventures that exist solely

on the mobile money platform, although none of these startups had yet generated

a significant volume of business. While the level of transactions going to and from

the financial system through these newly enabled mobile money channels is still

relatively low, according to anecdotal evidence, and it does not yet seem likely that

large numbers of new poor clients are being reached because of mobile money,

these are nonetheless the early days, and the level of activity is already striking.

Aus diesem Grund, we believe mobile money has great potential to become a “cat-

alytic platform.” The variety of new models and approaches being tried could por-

tend a fairly fundamental realignment of the cash-based financial sector—a move

from all cash transactions being mediated by expensive retail infrastructure to

greater use of electronic payments through cell phones. Outsourcing cash han-

dling not only will allow financial service providers to serve their clients at lower

cost per transaction but also will allow them to get more value out of their exist-

ing front-office infrastructure and staff as they focus on more sophisticated tasks,

such as customer service, cross-selling, risk evaluation, usw. On the client side, cus-

tomers will gain access to a dense network of transaction points, greatly reducing

their costs to access financial services. Darüber hinaus, once clients are in the financial

system and able to transact at a low cost with financial service providers, the plat-

form enables them to access a whole new set of services and delivery models that

were not previously possible or profitable.

Jedoch, whether mobile money will achieve this vision in Kenya depends on

operators’ and financial service providers’ ability to overcome three major chal-

Längen:

62

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

An Emerging Platform: From Money Transfer System to Mobile Money Ecosystem

• Prices on transfers, especially through M-PESA, must be reduced

• Mobile money providers, especially M-PESA, must lower integration costs and

develop a useful set of APIs

• Financial service providers must develop fundamentally new models for foster-

ing relationships with customers when face-to-face cash transactions and the

retail infrastructures associated with them are a thing of the past

If mobile money and financial service providers can overcome these chal-

Längen, Kenya’s retail financial services market will be poised for a transformation.

1. Historians of technology have long noted the economic and social changes wrought by new infra-

Struktur, such as electrical power and rail. See Thomas P. Hughes, Networks of Power:

Electrification in Western Society, 1880-1930, Baltimore: Johns Hopkins University Press, 1992. Für

a cautionary tale, see Wolfgang Schivelbusch, The Railway Journey: The Industrialization and

Perception of Time and Space, Berkeley: University of California Press, 1987.

2. Economists often refer to mechanisms that bring together multisided markets as a platform.

Multisided markets are those where each side benefits the more the other sides participate. Ein

example would be video game consoles, which bring together game players and game producers,

and where players benefit from a wider variety of game producers and game producers earn more

when there are more players.

3. For more on the history of the M-PESA products, see Ignacio Mas and Daniel Radcliffe, Mobile

payments go viral: M-PESA in Kenya, The Lydian Journal. Available at http://pymnts.com/mobile-

payments-go-viral-m-pesa-in-kenya/ 2010; for more on the mechanics of how M-PESA’s retail

network works, see Frederik Eijkman, Jake Kendall, and Ignacio Mas, “Bridges to cash: the retail

bei

end of M-PESA,” Savings & Development

http://ssrn.com/abstract=1655248 2010.

(2010). Verfügbar

34, NEIN. 2

4. See http://technology.cgap.org/2010/03/08/mobile-money-takes-off-where-is-the-innovation-in-

product-design/.

5. It’s not clear whether this interest will be sustained, Jedoch, as the rate of uptake slowed signifi-

cantly after the product launch. There were approximately 600,000 accounts opened in the few

months after launch in May 2010, but the rate of activations dropped dramatically in the fall of

2010. The high price of deposits and withdrawals and difficulties in the relationship between

Equity and Safaricom have contributed to the stagnant growth of the product.

6. SMS refers to the Short Message Service/text message functionality of the phone. SMS messages

are processed via a store-and-forward system and are not real-time transactions. SMS is linked to

the phone’s SIM and are thus carrier dependent. USSD is Unstructured Supplementary Service

Data sent by all phones to towers and are carrier independent. IVR is Interactive Voice Response

voice-recognition and activation functionality, and WAP is the wireless application protocol for

accessing web pages on mobile phones.

7. Most of the innovators link to M-PESA using one or more of the integration options outlined in

the Integrators section.

8. Anecdotally, practitioners report that monthly savings group meetings can be hours long, Und

much of the time is taken up by publicly counting cash to verify that records and bookkeeping are

accurate.

9. We feel there are two main features of a “good” API: predictability of API management from the

provider and ease of use, which may or may not be related to degree of openness or adherence to

industry standards; a user-friendly API might still be a walled garden or adhere to its own set of

Standards, Zum Beispiel. It is hard to program when the system might change without warning and

when the system is not designed to be open to third-party programmers. Safaricom has no formal

API management process, and when changes are made to the interface, financial institutions are

left scrambling to fix them, regularly leaving their systems down for up to days at a time.

Innovationen / Volumen 6, number 4

63

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023

Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard

10. See Tavneet Suri and Billy Jack, “Mobile Money: The Economics of M-PESA” [NBER Working

Paper No. 16721], 2011.

64

Innovationen / Inclusive Finance

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/6/4/49/704824/inov_a_00100.pdf by guest on 08 September 2023