Indonesien, Malaysia, and Thailand

Indonesien, Malaysia, and Thailand

Don Hanna

Citigroup Global Markets

388 Greenwich Street, 11th

Floor

New York, New York 10013

USA

don.hanna@citigroup.com

Indonesien, Malaysia, and Thailand: Neu

Administrations, New Policies, Neu

Performance?

Abstrakt

The administrations in Indonesia, Malaysia, and Thailand have all

put in place economic policies designed to increase growth, Re-

duce poverty, and improve governance. In Thailand, the govern-

ment is taking a more activist role, a change from the previous,

more hands-off approach. In both Indonesia and Malaysia, neu

policies reduce the activist role of the state, creating greater pre-

dictability and transparency. Better governance remains a key to

Wachstum, with many reforms within governments’ reach. Während

many of the policies focus on the medium term, there is an ac-

ceptance of the need for prudent short-term management. Der

open question is whether progress on structural changes can per-

sist when the short-term macroeconomic picture becomes more

challenging.

1. Einführung

ASEAN has a new crop of leaders. In the last three years,

both Malaysia and Indonesia have seen new administra-

tions come to power. In Thailand, Prime Minister Thaksin

had ªve years in power, with a resounding electoral vic-

tory in 2005 returning him to ofªce, before protests and an

annulled snap election this year prompted a coup that top-

pled him.1 The shift in Malaysia, with the appointment of

Abdullah Badawi was the ªrst change in prime minister in

über 20 Jahre. President Susilo Bambang Yudhoyono is the

ªrst Indonesian president ever directly elected. Thaksin

1 The analysis in this paper was written before the coup. Singa-

pore also has a new prime minister, Lee Hsien Loong, and Glo-

ria Macapagal Arroyo has been formally elected to ofªce in the

Philippinen, but this paper does not address Singaporean or

Philippine economic performance.

Asian Economic Papers 5:3

© 2007 The Earth Institute at Columbia University and the Massachusetts

Institute of Technology

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

may yet remain in ofªce if, as expected, his Thai Rak Thai party wins a majority in

the planned October election.

All these administrations represent a break with the past. All have touted new poli-

cies. This paper looks at what the distinct features of these new policies are and how

they may affect their respective economies going forward. In Thailand, Thaksin’s

longer time in ofªce does allow for some empirical analysis. Because of the short

time involved in Malaysia and Indonesia, the judgments here rely more on the bi-

ases of the author than empirical analysis. Time will tell whether those biases reºect

Wirklichkeit.

The analysis proceeds in two stages. Erste, I lay out my understanding of the key ele-

ments of the policies espoused by the Yudhoyono, Badawi, and Thaksin administra-

tionen, relying for this on their published policy statements. Zweite, I assess the long-

term issues against the yardstick of work done across a range of emerging markets

on the relevance of the themes espoused by the administrations to economic

Wachstum. I also make some preliminary assessments of the effectiveness of policies to

Datum.

2. New policies, new outcomes?

Any understanding of the effects of the policy agenda of any administration re-

quires an understanding of just what policies it is undertaking. We look at each of

the three administrations in turn, comparing them with the past agendas in each

country and with each other.

2.1 Indonesien: Frieden, justice, and prosperity

Over the last eight years, a degree of turmoil has marked Indonesia’s economic per-

formance that is greater than any seen in the country since the 1960s. After a period

of growth in per capita income that was surpassed by only a few countries in the

Welt, the crisis that followed the 1997 Thai baht devaluation and the ensuing end

of the 30 years of rule by Suharto was a rude exposure of the weaknesses of “growth

with stability,” the catchphrase of Suharto’s economic policy.

Natürlich, the very phrase “growth with stability” is on one level contradictory.

Something growing is, by deªnition, changing, at a minimum in size. One could

think of the phrase, obwohl, as the description of a stable dynamic solution in the

manner of the now-classical growth theory of the 1960s. There was much in

Suharto’s policies that bore the hallmarks of the 1960s, especially a technocratic ap-

129

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

Figur 1. Geographic concentration of Indonesia’s GDP, 1996–2004 (Prozent)

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Quelle: CEIC Data Company Limited, Citigroup calculations.

proach to economic policy that sought to isolate economics from politics.2 The more

usual distinction in the “growth with stability” catchphrase was the split between

economics and politics. Suharto sought a growing economy and a stable polity (eins

led and controlled by him). Jedoch, while Suharto envisioned stable growth in the

economy, he seemed to favor absolute stability in the level of politics.

One can argue that it was the conºict between pursuing stable economic growth

and static politics that undermined Suharto’s regime and unwound, at least tempo-

rarily, some of the regime’s economic beneªts. The effort at avoiding political

change in leadership did bring change, a centralization of authority under Suharto

as alternative centers of power were emasculated (the military, political parties, Die

parliament [Dewan Perwakilan Rakyat]).3 The centralization of political authority

under Suharto may have tended to concentrate economic activity in Jakarta as busi-

ness sought to inºuence the president and his administration (certainly, the demise

of Suharto’s presidency has tended to rebalance GDP away from Jakarta) (see ªgure

1). By the 1990s problems of pollution and congestion in the Jakarta metropolitan

area were becoming severe (World Bank 1996). The bureaucracy, zu, was heavily

concentrated in Jakarta, reinforcing the economic concentration. With centralized

2 For a discussion of Suharto’s economic policies, see Glassburner, Nasution, and Woo (1994).

3 For a discussion of politics under Suharto, see Schwarz (1999).

130

Asian Economic Papers

Indonesien, Malaysia, and Thailand

Figur 2. Country scores on Corruption Perception Index, 2005, and Heritage Foundation

Index of Economic Freedom Index, 2006

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Sources: Heritage Foundation (2005) and Transparency International (2005).

political decision making, regions got short shrift, feeding simmering tensions on

the fringes of the far-ºung archipelago, in Aceh, in Papua (then Irian Jaya), und in

northern Kalimantan.

Centralized decision making and the absence of checks on government authority

not only undermined political growth, but also promoted corruption. It is perhaps

not a coincidence that Transparency International’s rankings of the most corrupt

countries bear a direct relationship to the Heritage Foundation’s Index of Economic

Freedom (see ªgure 2). Unbridled corruption undermined justice in Indonesia, cre-

ating an environment in which justice was bought.

This backdrop is important for understanding the themes that President Yudhoyono

emphasizes in his approach to governing Indonesia. In einem 2005 speech he summa-

rized his policy agenda: „. . . to change Indonesia for the better. To make Indonesia

more democratic, more prosperous, more just, more peaceful (Yudhoyono 2005, empha-

sis added). These watchwords—democracy, prosperity, and peace—go beyond the

typical range of economic policies toward areas that the profession has termed

“governance.” Only in prosperity do we have the typical set of economic policy is-

131

Asian Economic Papers

Indonesien, Malaysia, and Thailand

Tisch 1. Key elements of Yudhoyono’s 100-day plan

Ziele

Key Actions

Ensuring security and

peace

Promoting justice and

democracy

Speedily resolve conflicts in Aceh and Papua and prevent escalation of conflicts in Poso, Maluku,

and North Maluku.

To facilitate the above, focus on rehabilitating infrastructure and ensuring adequate autonomy

laws.

Ban exports from illegal logging and fishing.

Combat corruption and demonstrate commitment by empowering the Anti-Corruption Court and

concluding a few high-profile corruption cases expeditiously.

Focus on poverty reduction, complete a strategic document on poverty reduction, and prepare a

comprehensive poverty map to guide future interventions.

Strengthen public services in education and health (through scholarships for books, teacher

Ausbildung, more staff and free services to the poor at health facilities, and adoption of a law on

medical practice).

Promoting prosperity Put in place a business-friendly tax system, with the focus on an accelerated depreciation schedule,

investment allowances, extending the carry-forward period for losses, and reducing tax on

dividends.

Ensure budgetary needs in 2004 are met, through tighter tax collection and divestment of minority-

share ownership of the government in some banks, and review 2005 budget to align priorities with

resources.

Improve labor regulations related to recruitment, wages, layoffs, and separation pay.

Support the small and medium-sized enterprise sector through debt forgiveness from state-owned

banks and other support mechanisms through state-owned enterprises.

Quelle: Coordinating Ministry of Economic Affairs, as quoted by Asian Development Bank, www.adb.org/Documents/CERs/INO/

2004/ino0300.asp

sues. Within each broad category is a set of initial actions that the government com-

mitted to as part of its 100-day program (see table 1).

2.2 Malaysia: A national performance culture

Understanding the policies of Malaysian Prime Minister Badawi is also easier if one

considers those of his predecessors, Tun Abdul Razak and Mahathir Mohamed, WHO

governed Malaysia for 35 years prior to Badawi. The dominant policy agenda of

much of that period was the “New Economic Policy” (NEP) adopted in 1970 in re-

sponse to serious race riots in 1969. The objectives of the policy were to eradicate all

poverty and to redistribute wealth to the bumiputera, largely Malay, with a goal of

having 30 percent of national wealth in bumiputera hands by 1990. In practice this

meant institutionalized discrimination in favor of other Malaysians against the Chi-

nese, the chief holders of wealth in Malaysia, in owning businesses, in education,

and in job placement.

Favored by the state, bumiputera citizens did increase their relative incomes and

their control of wealth in part by preferential access to state privatization deals as

well as favorable quotas at universities and in the civil service.4 But a culture of

cronyism also set in, with opportunities allocated not on merit, but on race. Crony-

4 For an analysis of the NEP, see Sundaram (2004).

132

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

ism was reinforced by Prime Minister Mahathir’s preference of favoring particular

bumiputera businessmen as a means of creating a new business class rather than a

strategy of distributing stakes in state assets widely through the Malay community.

Like that of Indonesia, Malaysia’s economic performance through the NEP years

was among the best in the word. Per capita income soared from US$370 in 1970 to US$2,400 in 1990. The incidence of poverty slipped, life expectancy lengthened, Und

infant mortality plummeted. By the 1990s Prime Minister Mahathir was focused on

“Vision 2020,” a plan to push Malaysia to developed-country status by that date.

Achieving this goal was complicated, obwohl, by the Asian crisis and the weakness

in Malaysia’s corporations and banks that it exposed. Favored, state-connected, Und

previously high-ºying institutions like Renong defaulted as many of the bumiputera

managers, who had not seen a recession since the mid-1980s, found themselves un-

able to cope with the country’s economic downturn. Banks’ balance sheets were rid-

dled by bad loans, threatening their solvency.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Five years later, as Prime Minister Mahathir gave way to Prime Minister Badawi,

the criticisms of the discrimination inherent in government policies had risen, nicht

just among those who had been discriminated against, but also among Malays

who had begun to resent the stigma of favoritism, rather than personal achieve-

ment, that clung to accomplishments.5 Against this backdrop, Prime Minister

Badawi, shortly after assuming ofªce in October 2003, proclaimed his new economic

policy agenda:

Let us now enter into a “performance contract.” The public sector hereby com-

mits to maintaining strong ªscal discipline and growth-supporting policies, Und

at the same time strives to overhaul the levels of bureaucracy and red tape to

achieve higher levels of efªciency and transparency. Im Gegenzug, the corporate sec-

tor commits to leading the growth effort, by improving productivity and interna-

tional competitiveness, while capitalizing on focused investments in key sectors

to build our future economic growth engines. Zusätzlich, we will collectively

commit to upgrading the quality of our human capital. (Badawi 2004)

Notable in this enumeration was the total lack of any racial or religious references.

Performance, rather than race, has become the watchword.

2.3 Thailand: 21st-century global populism

Thai Prime Minister Thaksin’s economic policies, as announced in his March 2001

policy speech, also reºect a response to the aftermath of Thailand’s 1997 wirtschaftlich

5 For an insightful personal view of the NEP period, see Rashid (1993).

133

Asian Economic Papers

Indonesien, Malaysia, and Thailand

crisis (Shinawatra 2001), to a sluggish economy and rising poverty, and to perceived

decaying moral values, epitomized by rising corruption and drug use. As the crisis

has receded and economic performance has improved, the emphasis has shifted to

eliminating poverty and building a “sustainable” Thailand.

Tellingly, the Thaksin administration attributes the weak performance of Thailand’s

economy immediately after the 1997 crisis to “heavy dependence on foreign mar-

kets” (see Shinawatra 2005, 1). Hence the policy prescription at heart attempts to

build Thai resilience in the face of greater global competition, rather than simply

shielding the economy from that competition. Zu diesem Zweck, the government’s “Dual

Track” policy pronouncements have tended to focus on building rural, “grassroots”

Thailand (the revolving Village Fund, the farmer debt moratorium, the “One Vil-

lage, One Product” campaigns). They have also tended to emphasize advantages to

Thai business integral to Thailand due to its geography or culture (tourism and agri-

culture again are prominent). Endlich, there has been a willingness to use the state

more actively in promoting economic growth (the consolidated asset management

company, clusters of state-owned enterprises).

Gleichzeitig, Thailand has pursued a policy of promoting trade, negotiating for

a free trade agreement with the United States, and pushing to expand the ASEAN

Free Trade Agreement. These efforts are constrained, obwohl, by a desire to promote

local business interests. This again, comes across very clearly in the 2001 Politik

statement of the trade agreement: “Support free trade in the international arena, tak-

ing into full consideration the level of preparedness and national interests of the

country as well as the interest of domestic entrepreneurs” (Shinawatra 2001, section

4.3(1)). The tension between national and foreign interests in trade and production is

also evident in a more recent policy speech: „. . . industrial manufacturing continues

to be run by placing orders or according to the pattern developed by the foreign in-

tellectual property owners, welche, im Gegenzug, makes the country deeply dependent on

the imports of raw materials, capital and technological expertise from abroad”

(Shinawatra 2005).

Some observers have attributed this bias to Thaksin’s own background as a Thai

entrepreneur whose telecom businesses beneªted from Thailand’s initially protected

regulatory environment and from government contracts. The popularity of the

policy may also be a backlash by domestic business against the sale of assets,

largely to foreigners, instituted by the Democratic administration that preceded

Thaksin.6

6 See Phongpaichit and Baker (2002) for an espousal of this view.

134

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

There has also been a tension between the Thaksin administration’s desire to pro-

mote grassroots development and the somewhat newer emphasis on providing so-

cial protections from “cradle to grave.” The interesting issues are how to strike the

balance between absorbing the technology and prowess of the rest of the world and

being absorbed by it, and how the state can promote risk taking while sheltering

those who fall behind.

Endlich, there is little said in Prime Minister Thaksin’s policy statements about the

conduct of macroeconomic policy. There was a commitment in Thaksin’s ªrst ad-

ministration to reducing the ªscal deªcit as Thailand’s economy rebounded, wie-

mitment that was met. Because of concerns about the faltering economy, the admin-

istration has now pledged to keep public debt below 50 percent of GDP and debt

service to under 15 percent of public spending, even as it announced a July 2005

ªscal package of Bt$50 billion, oder 0.7 percent of GDP, and infrastructure spending of US$63 billion over the next ªve years.

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

On monetary policy, obwohl, little has been said, even as inºation picked up in 2005.

Thaksin’s original 2001 policy statement commits the administration to “implement

monetary policies that facilitate the extension of credits to the real sector”

(Shinawatra 2001, section 2.2, paragraph 1). There is no mention of price stability.

Natürlich, this could simply represent the independence of the Bank of Thailand,

though the ouster of the previous governor seems to imply limits on the effective

independence of the bank.

2.4 Parallels across the region

There are echoes in Thaksin’s economic policies of those of former Malaysian Prime

Minister Mahathir.7 The willingness to remain open to trade, while harboring suspi-

cions about the motives and consequences of foreign trade, is very reminiscent of

Mahathir. Also, zu, is a willingness to use the state as an agent of change. But with

Thaksin having just begun the process of political and economic consolidation, Dort

is less of the performance contract/transparency theme inherent in the Badawi

administration policies.

Like his fellow leaders in neighboring countries, Thaksin is also emphasizing the

need to root out corruption. This goal was one of the key planks of his ªrst adminis-

tration and repeated in the second. Against this goal, it is ironic that the sale of his

7 Phongpaichit (2004) argues that there are also political echoes of Mahathir in Thaksin, partic-

ularly his willingness to use the state as an engine of reform and his penchant for concentrat-

ing authority in his party, the Thai Rak Thai.

135

Asian Economic Papers

Indonesien, Malaysia, and Thailand

family’s ºagship company in early 2006, in a manner that avoided any tax pay-

gen, sparked the current political turmoil in the country.

There is an interesting evolution, obwohl, in the government’s position on democ-

racy and transparency and civil society: “That the Government received the people’s

trust so overwhelmingly in the last election has given rise to a new dimension in the

Thai political system: a strong government. Jedoch, the Government fully recog-

nized that in a democratic society, there must be checks on the administration of

public affairs, through a strong civil society” (Shinawatra 2005, section 7). Diese

comments seem at odds with other observers’ concerns about the human rights of

southern Muslims and of drug trafªckers and about press freedom. They are consis-

tent, obwohl, with Thaksin’s decision to temporarily step down from the position of

prime minister, holding the position now only in a caretaker capacity until new elec-

tions can be arranged.

There are echoes in Thaksin’s Thailand of the pro-domestic-business stance evinced

by Indonesian Vice President Jusuf Kalla and his chosen Economic Coordination

Minister, Aburizal Bakrie. Both countries focus on calls for reduced poverty and

greater decentralization. Prime Minister Thaksin, obwohl, with a stronger ªscal and

political base, seems more willing to use state authority for his aims than President

Yudhoyono has been to date. Both countries have plans for a large expansion of in-

frastructure: in Thailand’s case, some US$63 billion over the next ªve years, in Indo- nesia’s case, US$25 billion.8 In Thailand’s case, obwohl, there is a greater emphasis

on state-driven projects, while Indonesia has tried to focus on a better enabling envi-

ronment and less direct state funding.

Other elements of Thaksin’s agenda appear in the 100-day plan of the Yudhoyono

administration: ensuring peace (Aceh and the Malukus versus southern Thailand),

lessening corruption, reducing poverty, support for small and medium-sized enter-

prises, and more effective decentralization and public infrastructure. The similarity

in ends, obwohl, seems to mask some differences in means, insbesondere, the willing-

ness to use the state as a catalyst rather than focusing on removing governmental

obstacles. This in turn may simply reºect the differences in the effectiveness of ad-

ministrations in the two countries, evident in the World Bank data on governance

(see appendix 1).

8 According to a presentation made by Raden Pardede, the head of the Indonesian govern-

ment’s task force for infrastructure ªnancing, the total amount needed for infrastructure ad-

justment is as much as US$149 billion in the next ªve years. This includes Aceh/Nias recon- struction. Jedoch, only US$25 billion of that will come out of the national state budget.

136

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

3. Policy evaluation: Current and likely effects

3.1 Indonesien

One way of assessing President Yudhoyono’s economic program in the ªrst year is

simply to enumerate how much of the 100-day program has actually been carried

out. The answer to that is straightforward: there has been a good start on some

structural measures, but the record on short-term policy management and on the

infrastructure initiative is very mixed.

Enhancing peace and security The tsunami that devastated western Aceh pro-

vided an opportunity for progress on peace negotiations with the Free Aceh Move-

ment. Both sides agreed to a cease-ªre as they focused on the need to prioritize di-

saster relief. Several rounds of talks in Helsinki ended with a peace agreement in

July that is now being put in place. Along with peace negotiations, infrastructure re-

building in Aceh has begun, with billions of dollars in aid ºows beginning to be felt

in the province, and a one-year debt moratorium from the Paris Club to provide

some US$4.5 billion in temporary cash ºow relief. Progress on autonomy laws or on conºicts elsewhere around Indonesia, obwohl, has suffered as the government’s at- tention and capacity is occupied by tsunami relief. Combating corruption In regard to ªghting corruption, zu, there has been some progress, largely with the Corruption Elimination Commission bringing cases against 10 prominent government ofªcials and opening investigations into 16 others as of May. Five cases have been decided, but four are still under appeal.9 President Yudhoyono has also publicly acknowledged police and army connivance in illegal logging in Papua and Kalimantan, a major source of corrupt income for both enti- Krawatten. Under new scrutiny from the president, customs has reduced bribe taking to such an extent that exporters are now complaining that imports of components are being held up as ofªcials demand proper bills of lading and tariff payments. Struc- tural changes in public sector compensation, obwohl, remain unaddressed. A much- awaited reshufºing of senior civil servants designed to root out corruption and also increase the effectiveness and competence of the civil service is still pending. Promoting prosperity Promotion of prosperity is perhaps the area most closely tied to immediate economic performance. It is also one where the items identiªed in the 100-day plan remain largely works in progress. The most contentious issue has 9 See article by the Deputy of Prevention of the Corruption Elimination Commission, Kneipe- lished by the Independent Commission Against Corruption of Hong Kong in the Interna- tional Anti-Corruption Newsletter, 2005, NEIN. 2, cited at http://www.icac.org.hk/newsl/ issue22eng/frame.htm 137 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / Direkte . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 5 3 1 2 8 1 6 8 2 2 8 6 a s e p 2 0 0 6 5 3 1 2 8 p d . . . . . f by gu e s t o n 0 8 S e p e m b e r 2 0 2 3 Indonesien, Malaysia, and Thailand been implications of the steady rise in oil prices and its ªscal and inºationary conse- quences. Poverty reduction efforts and ªscal coherence got a boost from the 1 Marsch 2005 announcement of a 29 percent average hike in the price of fuels in Indonesia. Roughly half the expected subsidy cut of Rp20 trillion was earmarked for the 16 pro- cent of Indonesia’s population living under the poverty line. To avoid the misuse of these funds, as occurred after a similar effort in 2001, the government has also funded a commission to monitor and report any corruption or abuse in the use of the funds. The money will largely be used for rural infrastructure and health pro- grams and for subsidizing rice purchases, thus addressing some of the public ser- vice issues on the government’s agenda. Initial gains from this measure, Jedoch, were quickly stripped away by rising in- ternational oil prices that threatened to drive the domestic fuel subsidy to 5 percent of GDP. Even netting out higher revenues from oil production, domestic demand at Indonesia’s low prices was enough to generate a ªscal deªcit of about 0.5 percent annually. In part this reºected the fall in domestic production to under 1 million bar- rels a day from 1.5 million pre-crisis, welche, im Gegenzug, was a result of Indonesia’s un- certain investment climate and a paucity of exploration and development. The most visible example of this is the case of the Cepu oil ªeld in central Java, currently oper- ated by Exxon. In order to invest the money needed to add some 15–20 percent to Indonesia’s annual oil production, Exxon had asked for a lease extension. A long and contentious negotiation was necessary, with only the intervention of President Yudhoyono moving the issue forward in the summer of 2005. With Pertamina’s oil demands rising, and Bank Indonesia lagging behind on interest rate adjustments (siehe unten), the nominal exchange rate on the rupiah moved through 10,000 to the U.S. dollar in late August 2005 and quickly moved through 11,000 (see ªgure 3). Faced with a crumbling currency and slumping equity and bond prices, President Yudhoyono ªnally moved, promising a fuel price hike in October. Bank Indonesia joined in the stabilization effort, pushing up policy rates by 125 basis points in two weeks. While this initially stabilized asset markets, greater market conªdence was engendered by the passage of a new 2005 budget in Septem- ber that implied an 80 percent increase in domestic fuel prices. An 1 Oktober, Wie- immer, the government actually surpassed market expectations by boosting fuel prices 110 Prozent. Since then world oil prices have continued to rise, without further do- mestic adjustments. Jedoch, the effects on Indonesia’s oil product imports from the 2005 price moves have been so dramatic that currently higher oil prices posi- tively affect both the balance of payments and the ªscal accounts. The whole episode surrounding the fuel subsidy and monetary policy highlights some key points about macroeconomic management in Indonesia. Under Suharto, 138 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / Direkte . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 5 3 1 2 8 1 6 8 2 2 8 6 a s e p 2 0 0 6 5 3 1 2 8 p d . . . . . f by gu e s t o n 0 8 S e p e m b e r 2 0 2 3 Indonesien, Malaysia, and Thailand Figure 3. Indonesia rupiah/U.S. dollar nominal exchange rate and the Jakarta Stock Exchange Source: Haver Analytics. short-term macro stability was generally protected, while progress on long-term, structural reforms, especially in the 1990s, was painfully slow. Megawati’s economic team has restored short-term macro stability, as evidenced by the declining ªscal deªcit, a strong trade balance, and stronger currency and falling inºation (see table 2). Jedoch, it has not been very successful at boosting investment. In the ªrst year of Yudhoyono’s term, just the opposite was the case, at least as far as inºation, the rupiah, and investment were concerned. The minicrisis surrounding the rupiah has served to focus attention again on short- term management and has led to changes in Yudhoyono’s economic team, with the well-respected former ªnance minister, Boediono, brought back in to coordinate eco- nomic policy, helped by a more decisive new ªnance minister, Sri Mulyani. Part of the problem in Indonesia, obwohl, has not been so much poor ªscal policy as it has been easy monetary policy that does not respond to a changing environment (see ªgure 4). Bank Indonesia seemed mired in a debate over which interest rates to fol- niedrig, deposit or lending rates. Some argued that because lending rates were very high, monetary conditions were tight, and the weaker rupiah was just due to oil prices. Others looked at near-zero short-term interest rates, accelerating GDP growth, and a shrinking trade surplus and concluded that monetary policy needed to tighten. Certainly 30 percent credit growth, more than double nominal GDP growth, didn’t seem to jibe with lending rates’ being “too high.” 139 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / Direkte . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 5 3 1 2 8 1 6 8 2 2 8 6 a s e p 2 0 0 6 5 3 1 2 8 p d . . . . . f by gu e s t o n 0 8 S e p e m b e r 2 0 2 3 Indonesien, Malaysia, and Thailand e c n a l a b e d a r T * ) P D G f o % ( e c n a l a b l a c s i F a ) P D G f o % ( r a l l o d e t a r t s e r e t n i l a e R e t a r * I B S l e u f d n a s d o o f P D G y l l a n o s a e s e g a r e v A – n o s a e s e g a r e v A . . S U r e p h a i p u R h t n o m – e e r h T h s e r f g n i d u l c x e I P C e c n a m r o f r e p o r c a m s ’ a i s e n o d n I f o y r a m m u s e v i t a r a p m o C . 2 e l b a T y t i l i t a l o V d r a d n a t s ( y t i l i t a l o V d r a d n a t s ( y t i l i t a l o V d r a d n a t s ( y t i l i t a l o V d r a d n a t s ( y t i l i t a l o V d r a d n a t s ( y t i l i t a l o V d e t s u j d a y t i l i t a l o V d e t s u j d a y l l a d r a d n a t s ( l a i t n e u q e s d r a d n a t s ( h t w o r g l a i t n e u q e s ) n o i t a i v e d . g v A ) n o i t a i v e d . g v A ) n o i t a i v e d . g v A ) n o i t a i v e d . g v A ) n o i t a i v e d . g v A ) n o i t a i v e d e t a r h t w o r g ) n o i t a i v e d e t a r 4 4 . 3 6 . 3 0 . 4 . 2 (cid:2) 3 2 7 3 6 8 , 7 4 2 . . 0 4 1 . . a n . A . N 8 0 8 1 6 2 , 9 8 0 . 0 . 9 7 0 . 5 . 0 (cid:2) 7 9 3 2 6 6 , 9 2 . 9 6 . 1 1 . 2 6 . 4 4 . 3 2 . 1 (cid:2) 9 . 0 1 5 . 9 1 6 . 3 7 . 2 1 5 . 2 6 . 9 1 . 0 2 . 0 0 . 0 2 . 0 4 . 0 2 . 0 7 . 2 6 . 0 6 . 0 . s e t a m i t s e p u o r g i t i C d n a s c i t y l a n A r e v a H : e c r u o S . s m u s h t n o m – 2 1 g n i l l o R . A . a i s e n o d n I k n a B t a k i f i t r e S * . e l b a l i a v a t o n . A . N 5 . 1 f o n o i t a l l a t s n i o t r o i r P n o i t a r t s i n i m d a s u o i v e r p 1 . 1 n o i t a r t s i n i m d a s u o i v e r P ) 4 0 – p e S o t 1 0 – l u J ( 3 . 1 n o i t a r t s i n i m d a t n e r r u C ) 4 0 – t c O m o r f ( 140 Asian Economic Papers l D o w n o a d e d f r o m h t t p : / / Direkte . m i t . / e d u a s e p a r t i c e – p d / l f / / / / / 5 3 1 2 8 1 6 8 2 2 8 6 a s e p 2 0 0 6 5 3 1 2 8 p d . . . . . f by gu e s t o n 0 8 S e p e m b e r 2 0 2 3 Indonesien, Malaysia, and Thailand Figure 4. Indonesia’s short-term interest differential and rupiah/dollar exchange rate changes (Prozent) Quelle: Haver Analytics and Citigroup calculations. Notiz: Upward direction in the “IDR/USD appreciation” line denotes a devalued IDR vis-à-vis the U.S. dollar. With Bank Indonesia independent, Jedoch, there is more limited means for the ad- ministration to inºuence monetary policy. It took the minidebacle surrounding the rupiah to shift the argument sharply in favor to those pushing for tighter monetary policy. This mistake was not lost on Bank Indonesia, Jedoch, which has kept nomi- nal and real interest rates high as the inºationary effects of the fuel price adjustment subside. Trotzdem, the episode underscores how important accountability, as well as au- tonomy, is to the success of an independent central bank. Aus 100 days to 1,825 Tage: Possible growth effects over time The general market reaction to President Yudhoyono’s administration had been positive prior to the August 2005 debacle and has largely recovered to the levels prior to the debacle. The combination of shifting policies and personalities has seen a dramatic strength- ening of the rupiah on the back of higher capital ºows and falling month-to-month inºation (siehe Abbildung 3). International reserves have reached all-time highs, as Indo- nesia now is grappling with the problem not of capital ºight, but of capital excess driving up the real exchange rate. Rating agencies, having upgraded the country’s sovereign rating in 2005, saw no reason to change their ratings, and bond markets have tightened the spread to U.S. Treasuries on Indonesia’s dollar-denominated bonds, with Indonesia issuing the largest trade in 30-year dollar paper of any Asian sovereign, US$600 million, during the ªrst week of October 2005. This despite an-

other in a string of fall bombings, the second episode to strike Bali.

141

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

Whether these market judgments prove correct will depend on two things: the po-

tential impact of the policies on stated objectives and the actual effects. Given the

general scope of the policy agenda, and our limited expertise as economist, Wir

choose to focus on the gains to economic growth that could potentially accrue to the

policy agenda if implemented.

One strategy is to simply look at the gains to GDP that would accrue from either

larger or more effective use of resources in Indonesia commensurate with the policy

objectives. A growth-accounting framework is one way of carrying out such an exer-

cise.10

The Indonesian government has a medium-term projection for reducing unemploy-

ment and poverty—by 2009—cutting open unemployment to 5.1 percent from

9.7 Prozent in 2004. What would that mean for GDP growth? We use an expected la-

bor force growth rate of 2.3 Prozent, derived by taking the moving-average growth

in the working-age population over the six years to 2004 and a modest increase in

the labor participation rate from the 2003 value of 65.7 percent to the recent peak

value of 68.6 achieved in 2001. Assuming that the reduction in unemployment oc-

curs smoothly over the next ªve years means an effective gain in the labor force of

1 percent year each year. This in turn should boost GDP growth by the same

amount, assuming constant labor productivity.

But Indonesia plans other changes that should affect growth through both the capi-

tal stock and educational attainment. A dramatic surge in infrastructure is one of the

key elements of the new policy program within the promoting-prosperity agenda.

At the infrastructure summit held in Jakarta in January 2005, the country argued

that it would need to roughly double infrastructure investment from 2.3 percent of

GDP to 5 percent of GDP. Assuming an incremental capital output ratio of four, Die

average of the last two years, would imply a boost in GDP growth as a result of

higher infrastructure investment of 0.7 percent each year.

There are no quantitative increases in educational attainment yet speciªed. Gegeben

the lags between improving educational attainment and quality and moving people

into the workforce, it is unlikely that changes instituted now would have an appre-

ciable effect over the next ªve years, even if successfully implemented. There is,

10 Bosworth and Collins (2003) looked at growth accounting across the world from 1960

durch 2000 using information on labor quantity, labor quality and capital. Their underly-

ing production function in intensive form assumed constant factor share ratios of 0.65 für

human capital (educational attainment over the labor force) Und 0.35 for physical capital

(capital stock over the labor force). Total factor productivity was taken as a residual.

142

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

Jedoch, growth regression work that relates improvements in educational attain-

ment and quality to GDP across a wide cross-section of countries. Bosworth and

Collins (2003), Zum Beispiel, work with a human capital share of 0.65, meaning that

for every 1 percent gain in educational attainment, output per worker would rise by

0.65 Prozent. Their empirical work, Jedoch, casts some doubts on the magnitude of

the effects of educational attainment on growth (see table 3).

In a regression in which the contribution from physical capital is constrained to the

assumed 0.35 share, educational attainment is signiªcant, but when initial condi-

tions or educational quality is included, the magnitude and the signiªcance of the

relation breaks down (see columns 3–5 of table 3). None of this should be taken to

mean that human capital is not a crucial input to growth, only that quantifying its

effect is tough.

President Yudhoyono’s policy agenda goes beyond better labor markets that lower

unemployment and higher infrastructure spending that boosts investment and

Wachstum. There is also a focus on improving the investment climate through improv-

ing security and revamping the regulatory and legal environment, especially as it re-

lates to establishing a business, enforcing contracts, or closing businesses. On mea-

sures of these areas, Indonesia rates poorly (see table 4).

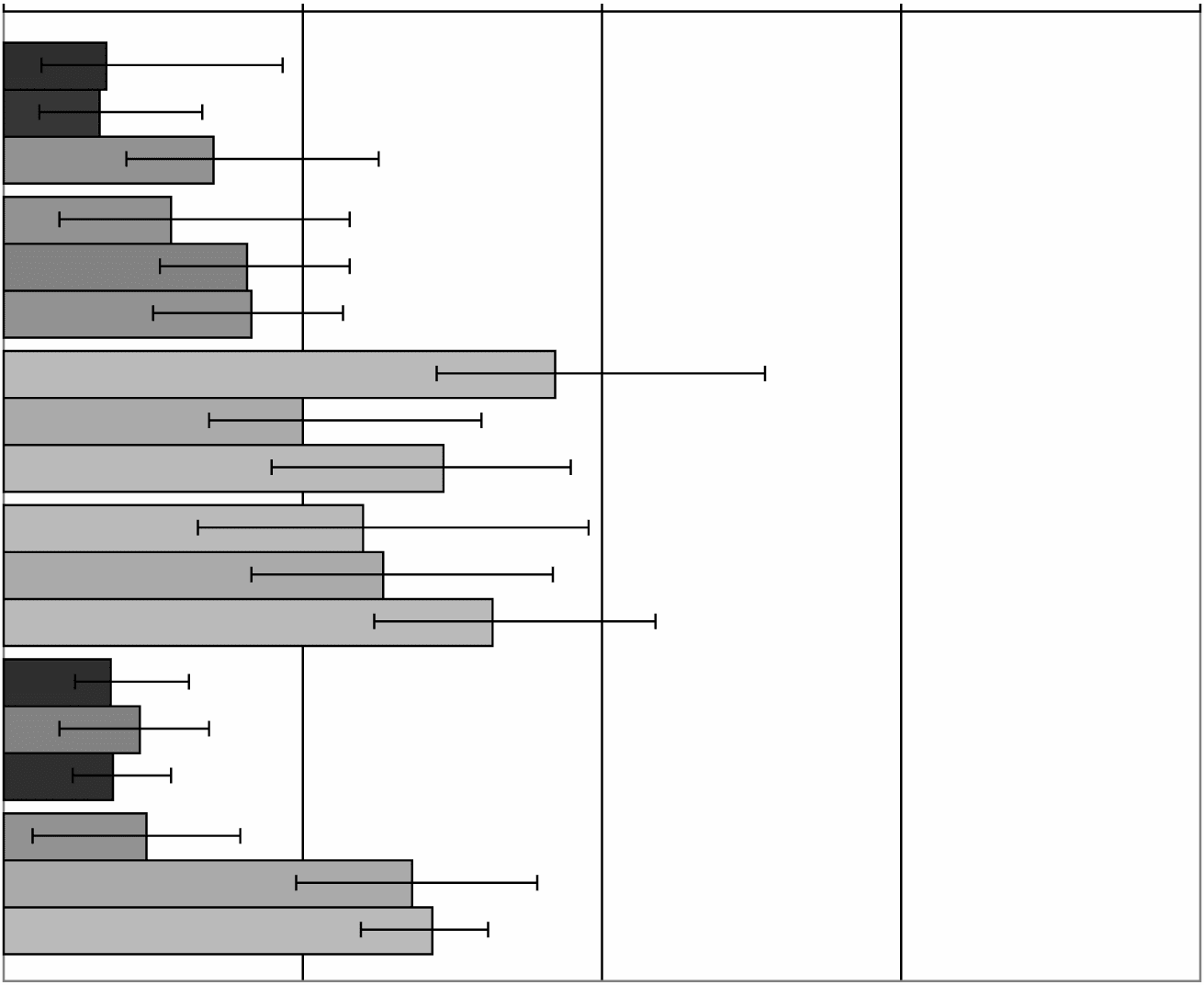

The peace and democracy aspects of policy may also have important effects on In-

donesia’s growth. Issues of governance and growth have been examined in

Kaufmann, Kraay, and Mastruzzi (2005). Indonesien, at least in 2002, ranked very

poorly (see appendix 1). Kaufmann identiªes six facets of governance: voice and ac-

countability, political instability and violence, government effectiveness, regulatory

burden, rule of law, and control of corruption. Each of these indicators is positively

correlated with per capita income growth. While correlation is not causality, the pos-

itive correlation between governance and growth holds out hope for President

Yudhoyono’s policies.

So far the goals and focus of President Yudhoyono’s new policies appear, according

to our examination, aligned with economic evidence supporting higher growth—

one measure of the prosperity that Indonesia seeks. If that judgment is right, Dann

the real change isn’t the objectives of the policy, but rather their implementation.

Then–Planning Minister Sri Mulyani echoed as much in a 2005 public speech in

which she cited implementation of policy, not its formulation, as the biggest chal-

lenge facing the administration. There are clearly huge beneªts to lifting investment,

improving governance, and maintaining monetary and ªscal prudence. Capturing

those beneªts will depend on the execution. Success for President Yudhoyono

143

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

e

G

A

R

e

v

A

)

5

(

7

2

0

.

0

6

.

3

5

0

.

3

.

1

7

0

0

.

0

.

1

1

0

.

0

7

0

.

D

R

A

D

N

A

T

S

(

j

T

ich

l

ich

T

A

l

Ö

V

)

N

Ö

ich

T

A

ich

v

e

D

j

l

l

A

N

Ö

S

A

e

S

e

G

A

R

e

v

A

l

A

ich

T

N

e

u

Q

e

S

D

e

T

S

u

J

D

A

e

T

A

R

H

T

w

Ö

R

G

–

N

A

T

S

(

j

T

ich

l

ich

T

A

l

Ö

V

)

N

Ö

ich

T

A

ich

v

e

D

D

R

A

D

j

l

l

A

N

Ö

S

A

e

S

e

G

A

R

e

v

A

l

A

ich

T

N

e

u

Q

e

S

D

e

T

S

u

J

D

A

e

T

A

R

H

T

w

Ö

R

G

8

4

.

0

5

.

0

1

2

8

.

0

6

.

1

7

0

.

0

8

.

1

2

0

.

0

2

.

2

)

4

(

7

2

.

0

2

.

6

5

5

.

0

3

.

1

8

0

.

0

4

.

1

)

3

(

—

—

5

3

.

0

—

)

2

(

5

5

.

1

0

.

3

3

1

.

0

7

.

3

—

—

1

5

.

0

5

.

1

1

4

7

.

0

4

.

1

1

1

.

0

5

.

3

)

1

(

—

—

.

3

5

4

(cid:2)

.

9

3

(cid:2)

S

e

Y

9

.

0

(cid:2)

5

.

2

(cid:2)

Ö

N

5

2

.

4

(cid:2)

9

.

3

(cid:2)

S

e

Y

1

5

.

0

(cid:2)

6

.

1

(cid:2)

Ö

N

1

4

.

0

(cid:2)

4

.

1

(cid:2)

Ö

N

4

8

.

0

4

8

2

7

.

0

4

8

4

8

.

0

4

8

7

.

0

4

8

1

7

.

0

4

8

l

A

T

ich

P

A

C

l

A

C

ich

S

j

H

P

N

ich

H

T

w

Ö

R

G

l

A

T

ich

P

A

C

N

A

M

u

H

N

ich

H

T

w

Ö

R

G

e

G

A

R

e

v

A

F

Ö

l

e

v

e

l

l

A

ich

T

ich

N

ICH

j

T

ich

l

A

u

Q

l

A

N

Ö

ich

T

A

C

u

D

E

G

N

ich

l

Ö

Ö

H

C

S

F

Ö

S

R

A

e

j

R

e

k

R

Ö

w

R

e

P

R

e

k

R

Ö

w

R

e

P

e

l

B

A

ich

R

A

v

T

N

e

D

N

e

P

e

D

N

ICH

D

e

D

u

l

C

N

ich

S

N

Ö

ich

T

ich

D

N

Ö

C

l

A

ich

T

ich

N

ICH

T

N

A

T

S

N

Ö

C

.

)

3

0

0

2

(

S

N

ich

l

l

Ö

C

D

N

A

H

T

R

Ö

w

S

Ö

B

:

e

C

R

u

Ö

S

S

N

Ö

ich

T

A

v

R

e

S

B

Ö

F

Ö

R

e

B

M

u

N

S

C

ich

T

S

ich

T

A

T

S

j

R

A

M

M

u

S

2

R

D

e

T

S

u

D

A

J

0

0

0

2

–

0

6

9

1

,

H

T

w

Ö

R

G

C

ich

M

Ö

N

Ö

C

e

D

N

A

,

j

T

ich

l

A

u

Q

,

T

N

e

M

N

ich

A

T

T

A

l

A

N

Ö

ich

T

A

C

u

D

e

N

Ö

S

T

l

u

S

e

R

N

Ö

ich

S

S

e

R

G

e

R

.

3

e

l

B

A

T

.

j

T

ich

l

A

u

Q

l

A

N

Ö

ich

T

u

T

ich

T

S

N

ich

D

N

A

,

j

H

P

A

R

G

Ö

e

G

,

T

N

e

M

u

R

T

S

N

ich

e

D

A

R

T

,

0

6

9

1

N

ich

N

Ö

ich

T

A

l

u

P

Ö

P

G

Ö

l

,

0

6

9

1

N

ich

j

C

N

A

T

C

e

P

X

e

e

F

ich

l

,

0

6

9

1

N

ich

A

T

ich

P

A

C

R

e

P

P

D

G

e

D

u

l

C

N

ich

S

N

Ö

ich

T

ich

D

N

Ö

C

l

A

ich

T

ich

N

ICH

.

S

C

ich

l

A

T

ich

N

ich

e

R

A

S

C

ich

T

S

ich

T

A

T

S

–

T

:

e

T

Ö

N

.

e

l

B

A

l

ich

A

v

A

T

Ö

N

:

—

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

144

Asian Economic Papers

Indonesien, Malaysia, and Thailand

A

G

N

ich

S

Ö

l

C

G

N

ich

C

R

Ö

F

N

E

S

S

Ö

R

C

A

G

N

ich

D

A

R

T

G

N

ich

j

A

P

G

N

ich

T

C

e

T

Ö

R

P

G

N

ich

T

T

e

G

G

N

ich

R

e

T

S

ich

G

e

R

D

N

A

G

N

ich

R

ich

H

H

T

ich

w

G

N

ich

l

A

e

D

A

G

N

ich

T

R

A

T

S

G

N

ich

Ö

D

F

Ö

e

S

A

E

S

S

e

N

ich

S

u

B

S

T

C

A

R

T

N

Ö

C

S

R

e

D

R

Ö

B

S

e

X

A

T

S

R

Ö

T

S

e

v

N

ich

T

ich

D

e

R

C

j

T

R

e

P

Ö

R

P

G

N

ich

R

ich

F

S

e

S

N

e

C

ich

l

S

S

e

N

ich

S

u

B

S

S

e

N

ich

S

u

B

j

M

Ö

N

Ö

C

E

2

7

1

4

1

1

7

3

3

4

3

1

5

9

5

5

9

2

3

1

6

1

1

8

1

1

1

1

0

1

6

1

3

9

4

1

6

8

1

7

2

7

4

2

0

1

9

8

5

4

1

8

3

1

6

7

1

6

2

2

1

9

8

6

3

6

1

4

5

8

4

3

8

3

3

9

4

0

3

1

9

2

0

3

0

5

4

3

9

1

4

4

2

3

9

1

1

7

0

1

0

8

8

1

1

3

0

1

2

7

4

4

1

3

3

5

7

8

5

6

0

0

1

3

4

1

2

3

1

8

5

9

2

8

2

5

1

8

1

9

5

6

5

2

8

5

3

1

1

6

0

1

1

2

1

3

6

4

8

4

1

2

1

0

7

6

3

2

2

3

5

4

6

6

2

4

2

9

3

2

9

7

0

1

1

0

1

7

6

3

0

2

3

2

4

3

5

0

1

8

0

1

7

8

2

2

1

2

8

0

2

1

6

1

1

7

7

1

7

7

5

8

1

0

1

5

2

6

2

1

6

3

1

8

1

1

9

7

0

1

4

2

1

5

3

6

1

8

9

2

7

5

7

9

9

7

6

2

1

2

8

9

8

0

9

4

4

1

2

3

7

0

1

0

2

1

2

7

2

5

3

1

9

9

9

3

1

1

5

1

1

6

1

1

A

N

ich

H

C

,

G

N

Ö

K

G

N

Ö

H

S

e

T

A

T

S

D

e

T

ich

N

U

e

R

Ö

P

A

G

N

ich

S

A

N

ich

H

C

,

N

A

w

ich

A

T

S

e

N

ich

P

P

ich

l

ich

H

P

A

ich

S

e

N

Ö

D

N

ICH

A

ich

D

N

ICH

M

A

N

T

e

ich

V

A

N

ich

H

C

D

N

A

l

ich

A

H

T

A

ich

S

j

A

l

A

M

N

A

P

A

J

A

e

R

Ö

K

0

1

e

H

T

F

Ö

H

C

A

e

N

Ö

S

G

N

ich

k

N

A

R

e

l

ich

T

N

e

C

R

e

P

j

R

T

N

u

Ö

C

F

Ö

e

G

A

R

e

v

A

e

l

P

M

ich

S

e

H

T

N

Ö

G

N

ich

k

N

A

R

e

H

T

S

A

D

e

T

A

l

u

C

l

A

C

S

ich

X

e

D

N

ich

e

H

T

.

T

S

e

H

G

ich

H

e

H

T

G

N

ich

e

B

1

H

T

ich

w

,

5

5

1

Ö

T

1

M

Ö

R

F

S

e

ich

M

Ö

N

Ö

C

e

S

k

N

A

R

X

e

D

N

ICH

S

S

e

N

ich

S

u

B

G

N

ich

Ö

D

F

Ö

e

S

A

E

e

H

T

:

e

T

Ö

N

.

S

R

Ö

T

A

C

ich

D

N

ich

T

N

e

N

Ö

P

M

Ö

C

S

T

ich

N

Ö

S

G

N

ich

k

N

A

R

e

l

ich

T

N

e

C

R

e

P

e

H

T

F

Ö

e

G

A

R

e

v

A

e

l

P

M

ich

S

e

H

T

S

ich

C

ich

P

Ö

T

H

C

A

e

N

Ö

G

N

ich

k

N

A

R

e

H

T

.

6

0

0

2

N

ich

S

S

e

N

ich

S

u

B

G

N

ich

Ö

D

N

ich

D

e

R

e

v

Ö

C

S

C

ich

P

Ö

T

.

)

/

S

G

N

ich

k

N

A

R

j

M

Ö

N

Ö

C

E

/

G

R

Ö

.

S

S

e

N

ich

S

u

B

G

N

ich

Ö

D

.

w

w

w

/

/

:

P

T

T

H

(

k

N

A

B

D

l

R

Ö

W

:

e

C

R

u

Ö

S

S

e

R

u

S

A

e

M

e

T

A

M

ich

l

C

S

S

e

N

ich

S

u

B

N

Ö

j

l

R

Ö

Ö

P

S

e

T

A

R

A

ich

S

e

N

Ö

D

N

ICH

.

4

e

l

B

A

T

145

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

would be a bigger milestone than the peaceful election process that brought him to

power. Stories of the corruption of Indonesian ofªcials and their antipathy to busi-

ness go back at least to the 16th century.11

3.2 Assessing Malaysia’s new performance contract

As with Indonesia, there has been little time since the announcement of Badawi’s

policies, making an empirical assessment of their impact difªcult, though some par-

tial indicators are available. Fiscal discipline looks improved, mit dem 2004 deªcit

running at 4.5 percent of GDP, budgeted to fall to 3.8 percent of GDP in 2006, obwohl

this remains much worse than the average under Mahathir (see table 5 and ªgure 5).

The ratio of public debt to GDP is also falling, with ratings agency upgrades in 2004

lauding the country’s economic management.12

These policies reverse the expansionary ªscal policy pursued to stabilize the econ-

omy after the 1997–98 debacle. Trotzdem, the Malaysian government has not returned to

the surpluses it was running in the 1990s.

The history of ªscal adjustment in Malaysia is encouraging. Past surplus gave the

government considerable room to operate countercyclical ªscal policy during the

Asian crisis downturn. Although the country’s budget balance is improving, there is

probably greater room to steer a more aggressive ªscal consolidation path in meet-

ing the commitment to “strong ªscal discipline.” Malaysia’s tax effort compares well

regionally (see ªgure 6).

But an increasing need for a lighter direct tax burden to cope with growing interna-

tional competition for foreign direct investment and to stimulate domestic private

investment implies that policymakers need to broaden the country’s revenue base to

pave the way for a cut in direct taxes. Recent ªscal consolidation has relied mainly

on the scaling back of development spending. Jedoch, there is also greater scope

for tighter discipline in regard to operating expenditures, such as a partial hiring

freeze in the public sector to reduce the public sector wage bill.

With the government dedicated to fostering entrepreneurship, in addition to a low

tax burden, an important driver is the ease of opening a business. If establishing

a business is too expensive or cumbersome, potential entrepreneurs may decide

11 See Milton (2000) for a description of an early encounter between English spice traders and

Indonesian locals.

12 Moody’s upgraded its rating of Malaysia one notch to A(cid:3) in December 2004; Fitch also

moved its rating up one notch to A3 in November 2004.

146

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

5

3

1

2

8

1

6

8

2

2

8

6

A

S

e

P

2

0

0

6

5

3

1

2

8

P

D

.

.

.

.

.

F

B

j

G

u

e

S

T

T

Ö

N

0

8

S

e

P

e

M

B

e

R

2

0

2

3

Indonesien, Malaysia, and Thailand

e

C

N

A

l

A

B

e

D

A

R

T

A

)

P

D

G

F

Ö

%

(

e

C

N

A

l

A

B

l

A

C

S

ich

F

A

)

P

D

G

F

Ö

%

(

R

A

l

l

Ö

D

e

T

A

R

e

T

A

R

R

Ö

B

ich

l

k

l

e

u

F

D

N

A

P

D

G

.

.

S

U

R

e

P

T

ich

G

G

N

ich

R

T

S

e

R

e

T

N

ich

l

A

e

R

H

T

N

Ö

M

–

e

e

R

H

T

S

D

Ö

Ö

F

H

S

e

R

F

G

N

ich

D

u

l

C

X

e

ICH

P

C

e

C

N

A

M

R

Ö

F

R

e

P

Ö

R

C

A

M

A

ich

S

j

A

l

A

M

F

Ö

j

R

A

M

M

u

S

e

v

ich

T

A

R

A

P

M

Ö

C

.

5

e

l

B

A

T

j

T

ich

l

ich

T

A

l

Ö

V

D

R

A

D

N

A

T

S

(

j

T

ich

l

ich

T

A

l

Ö

V

D

R

A

D

N

A

T

S

(

j

T

ich

l

ich

T

A

l

Ö

V

D

R

A

D

N

A

T

S

(

j

T

ich

l

ich

T

A

l