FROM HOME RUNS

TO BASE HITS

RETHINKING GREEN IMPACT INVESTING IN

EMERGING MARKETS

DUNCAN DUKE AND ERIK SIMANIS

Entrepreneurs live and breathe the Yogi Berra maxim, “When you come to a

fork in the road, take it.” Along with keen business acumen and indefatigable

persistence, the process of turning technological innovations into flourishing

industries and new markets requires vigorous opportunism. But being oppor-

tunistic is only half the game; unless entrepreneurs can quickly find new path-

ways to profits, the chances of success are slim. That’s a major reason why

entrepreneurs flock to Silicon Valley, the innovation hotspot that has produced

industry-defining businesses such as Hewlett-Packard, Apple, and Facebook.

In Silicon Valley, getting to Plan B—and

then to Plans C, D, and E—is often only a

phone call or an informal lunch meeting

weg. Robust infrastructure, dense social

Netzwerke, and a rich industry ecosystem

supply the opportunities startups need to

reframe their value propositions and

pivot to new markets.

It is these two elements—the unpre-

dictable nature of startups and the critical

supporting role of business ecosystems

and infrastructure—that underlie the

unique challenge of catalyzing the green

entrepreneurship and eco-innovation

sectors of developing countries. And in

today’s world, cultivating an army of

innovators to tackle environmental chal-

lenges across the globe is a topic worthy of

policymakers’ attention. Erste, it offers a

grassroots alternative to governments

that are already pulling all available policy

levers to combat rapidly eroding topsoils,

mounting air pollution, and other envi-

ronmental predicaments. And second,

the security and sustainability of the plan-

et depend on it. Increasing affluence and

growing populations mean that the devel-

oping world will soon surpass the CO2

emissions levels of industrialized coun-

versucht, thereby placing an unprecedented

burden on the planet’s waste sinks and

accelerating climate change.

Policymakers intent on fostering market-

based solutions to environmental chal-

lenges often look to Silicon Valley for

inspiration, given the area’s remarkable

success in spinning out transformational

IT industries. But it can also be a siren’s

call. Mimicking Silicon Valley’s approach

to investing for innovation without

accounting for the idiosyncrasies of

developing country contexts and clean-

112

Innovationen / Policy Design

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023

Rethinking Green Impact Investing in Emerging Markets

technology markets can be a recipe for

disaster. Consider E+Co, an organization

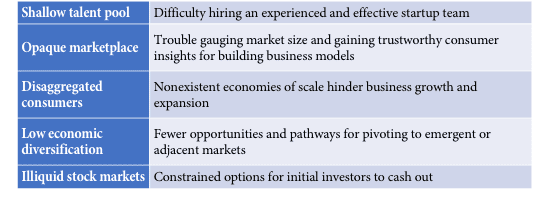

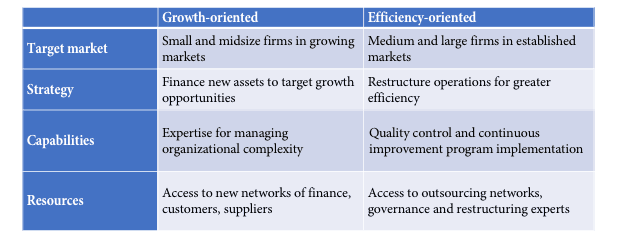

that over 18 years invested almost $40 million in more than 260 sustainable energy ventures across the developing world. It provided “patient capital,” which often is cited as the key enabler of entrepreneurship in developing coun- versucht. Despite its long-term investment horizon, wide scope, and deep experience base, E+Co was all but shuttered in 2012, writing off 83 percent of its portfolio. Our goal with this paper is to harvest les- sons from pioneering organizations like E+Co to sketch out an investment strate- gy for driving green innovation in emerg- ing markets. We begin by looking at that global innovation hub, Silicon Valley, and describing its engine and enabling condi- tionen. We then examine the clean-tech industry and the business environment in developing countries to see why the Silicon Valley investment model hasn’t worked in these arenas. We conclude by drawing insights from these analyses to flesh out a green investment approach that is tailored to the constraints and opportunities of developing countries. SILICON VALLEY: AMERICAN IDOL FOR ENTREPRENEURS Since the early 1950s, Silicon Valley has been at the forefront of the information technology revolution, accounting for one-third of all venture capital (VC) investment in the U.S. The region has spawned a stunning range of industries, from semiconductors (Intel, Nvidia), (HP, computers and Apple), and software (Oracle, Electronic Arts) to Internet services (Google, Facebook). The combined output of this ecosystem has profoundly changed the way many people around the globe work and live today. smartphones While countless studies have tried to explain why this entrepreneurial hotbed emerged, our objective is to examine how the model works: how it vets and incu- bates entrepreneurial opportunities, and then channels resources to those that meet certain parameters while killing off those that don’t. competition Think of Silicon Valley as an American Idol for entrepreneurs: scores of people with talent and ambition vying for the attention of a much smaller pool of people with money and connec- ABOUT THE AUTHORS Duncan Duke is an Assistant Professor in Strategy at Ithaca College’s School of Business. His work relates to how businesses innovate and create new business models to serve low-income markets. He also teaches and conducts research on strategic management, business sustainability, social entrepreneurship, organizational behavior, negotiations, and bottom of the pyramid (BOP) strategies. Erik Simanis is a Partner in TIL Ventures, a London-based innovation consultancy, and the former Head of the Frontier Markets Initiative at Cornell University. He is an authority on corporate entre- preneurship and market creation, having guided start-ups, green-field ventures, and corporate new business teams in Eastern Europe, Africa, Südasien, Naher Osten, and South America. © 2017 Duncan Duke and Erik Simanis innovations / Volumen 11, number 3/4 113 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Duncan Duke and Erik Simanis Table 1. Silicon Valley’s Enabling Conditions tions. It’s a “show,” where the winners are few but those who do make it “go plat- inum.” The judges in this case are the venture capitalists whose goals and strate- gies dictate the shape and form of the businesses that get chosen. Knowing how VC firms make money is therefore essen- tial to understanding the rules of the game. VC firms give money to startups in exchange for an ownership stake. Aside from money, VC firms play a key role in helping startups hire experienced talent, identify hot markets, pivot to new busi- ness models, and generate prospective sales leads. Startups, Jedoch, are highly uncertain undertakings—a 90 percent failure rate is not unheard of. VC firms invest in multi- ple startups to spread out their risk; the few ventures that do succeed must “hit a home run” to compensate for all the fail- ures. As a rule of thumb, a startup must demonstrate the potential to yield at least five times the initial investment to be con- sidered for funding. Venture capitalists readily abandon ven- tures that no longer show such promise, and redirect their resources to other opportunities. Abandoning the weak and wounded—the reason venture capitalists are often called vulture capitalists—is critical to the profitability and success of the VC model. Which raises an important contextual factor: just as having throngs of talented singers vying for a coveted spot in Hollywood improves the quality of the singing on American Idol, having a large pool of entrepreneurial talent improves the quality of the business investment opportunities VC firms can choose from. This is critical to improving the likelihood of hitting a home run. In this regard, Silicon Valley sits in a plum position, as the region has a deep pool of entrepreneurial engineering talent that is continually fed and replenished by pre- mier local universities. The region also attracts scientists and engineers from across the globe, and is home to serial entrepreneurs who have retired from ear- lier successful ventures and remain in the area looking to jump aboard new start- ups. The other critical element of the VC investment strategy is how investors real- ize their profits. VC firms usually aim to recoup their money five to ten years after making the initial investment. Given that 114 Innovationen / Policy Design Downloaded from http://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Rethinking Green Impact Investing in Emerging Markets startups typically lose lots of money early on and are unlikely to generate sufficient profits within this timeframe, venture capitalists aim to convert their ownership shares into real money through “exits”— either an initial public offering of stock (IPO), or the merger and acquisition of the venture by an existing company (M&A). In beiden Fällen, selling their own- ership stakes enables venture capitalists to monetize and capture future cash flows, rather than waiting for annual profits to accumulate. The need for “home runs” and exit options leads to two key investment parameters for venture capitalists. Erste, they invest only in businesses that target significant market demand. One of the first questions a VC fund manager asks of a prospective startup is, “What is your total addressable market?” Second, VC firms choose industries in which ventures can be scaled up quickly with minimal infrastructure build-out, especially those in which information technology (IT) plays a central role. Consider, Zum Beispiel, WhatsApp: the instant messaging service served more than 600 million users with only 55 employees when it was acquired by Facebook for $19 billion dollars.

McDonald’s, by comparison, employs

über 1.5 million people in more than

35,000 locations to achieve a market capi-

talization of about $100 Milliarde. In summary, Silicon Valley’s entrepre- neurship model is a function of the region’s enabling market and the IT- based technologies that underpin many of the ventures. To understand the applica- bility of this model to the promotion of green entrepreneurship and innovation in developing countries, we need to cross- check how these market environments and their core technologies stack up against Silicon Valley’s. FROM THE VALLEY TO THE VILLAGE Take a drive outside the capital city of any developing country and it’s immediately apparent that doing business in Africa, Asien, and Latin America is to play in a dif- ferent ballgame than in Silicon Valley and the industrialized world in general. Jedoch, beyond the overt difference in living standards, there are several under- the-surface cultural and institutional fac- tors that significantly shape the entrepre- neurial sector in the developing world. Having led startup ventures in Kenya, Ghana, Indien, and Mexico, we’ve experi- enced many of these issues firsthand. For one thing, skilled entrepreneurs and talented managers willing to work in startup ventures—particularly those based in rural areas—are in very short supply. The reason for this shortage is largely cultural, because career success means landing a steady job at a large organization, not joining a small startup in a remote village. The shallow talent pool manifests itself to investors in what the industry calls poor deal flow—there simply aren’t many high-quality startups from which to choose.1. E+Co, Zum Beispiel, was stretched thin by having to search across the developing world for promising ven- tures, from subtropical Africa to rural China to Brazil’s favelas. Recruiting sea- soned management talent for business ideas that do seem promising is an uphill battle because, apart from the status issue, there are few head-hunting firms or other labor-market intermediaries who can help in the search. Zum Beispiel, in a start- up led by one of the authors in Mexico, it took four months of intensive recruiting efforts to identify and hire just two team leaders. Locating, recruiting, and mentor- ing the local talent became the startup’s most time-consuming activity, which detracted from other urgent business development tasks. Innovationen / Volumen 11, number 3/4 115 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Duncan Duke and Erik Simanis Table 2. Emerging Market Challenges To wit, challenges on the consumer side of the emerging market equation make quantifying demand and market potential an arduous task. To start, there is limited consumer research, particularly about the lower income, mass-market segments that constitute most of the population. What does exist, such as World Bank studies on income levels and consump- tion habits, can be misleading, as it often relies on proxy measures (z.B., the pres- ence of television antennas or cooking utensils). Zum Beispiel, the team of a busi- ness effort in Ghana supported by one of the authors discovered that subsistence households (those that grow all their food) that spent on average $2 per day

and petty trading households that spent

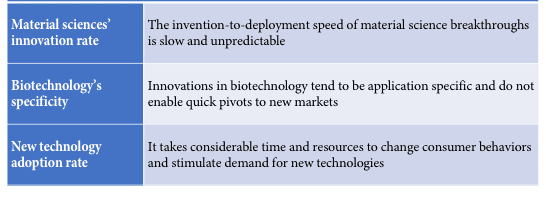

$7 per day had, in fact, similar levels of discretionary income. It turned out that the petty-trading households were spend- ing the additional cash they earned to cover their food costs. Obtaining this kind of critical insight is not easy, as consumers are often distrust- ful of outsiders or fear that information they divulge about their income—income typically made off the books in the infor- mal sector—could attract government scrutiny. Most importantly, most con- sumers don’t know exactly what they spend their money on.2. Cutting through the fog of misinformation requires getting on the ground and building rapport with the local population. In the Ghana case, it took the team two months of various immersion activities to get reliable data. Extremely poor transportation infrastruc- ture outside the Tier 1 and Tier 2 cities in developing countries also makes it diffi- cult to find opportunities that allow for the significant and rapid scale up targeted by Silicon Valley investors, as businesses are faced with highly disaggregated con- sumer populations—fragmented clusters of towns and villages that essentially func- tion as self-contained island economies. The most efficient structure for serving disaggregated consumers tends to be a decentralized business model comprised of small operating units that serve small geographic areas.3. Small operating units don’t lend themselves to rapid scaling, as a business can’t grow simply by adding central production capacity and sending salespeople out to distant areas. Instead the entire operating unit must be replicat- ed in each new area, much like a fran- chise. This takes time and capital, as it requires first systematizing all facets of the business. Consider that it took eight years to fully systematize the initial restaurant on which the McDonald’s franchise model is based. Low levels of economic diversification in emerging markets constrain startups’ 116 Innovationen / Policy Design Downloaded from http://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Rethinking Green Impact Investing in Emerging Markets Table 3. Clean Tech Challenges ability to pivot to new market opportuni- ties and business models.4. Economies dominated by single commodities (z.B., hydrocarbons) or low-value-adding agri- cultural commodities lack rich business ecosystems, thus the range of alternate pathways to pursue when Plan A goes awry is very limited. Endlich, the stock and M&A markets in emerging countries are smaller and much less liquid than those in the developed world. Zum Beispiel, there may be no trad- ing in a company stock for extended peri- ods of time in a low-liquidity stock mar- ket, which makes investor risk much higher. Mergers and acquisitions pose even greater challenges, as the availability and quality of financial data is often poor, and bringing the acquired companies up to international financial standards can be quite expensive.5. daher, IPOs and company sales are generally not viable exit options for entrepreneurs and investors in emerging markets. FROM SILICON TO SUNLIGHT The clean-tech sector—wind power, solar energy, batteries, smart meters, biofuels, carbon sequestration, HVAC efficiency, LED lighting, etc.—centers on the largest market the world: Energie. The immense size of this market, coupled with in growing awareness of climate change, led to a clean-tech investment boom in the mid-2000s. Legendary venture capitalists such as John Doerr and Vinod Khosla jumped into the game, calling attention to the need for disruptive innovations that could fundamentally move society off its collision course with environmental catastrophe, and large bets were placed on a cadre of startups. That boom, Jedoch, quickly turned to bust, as promising startups failed to achieve takeoff speed. There wasn’t a sin- gle Google-like home run to prove that these industries were, in fact, high growth. To their chagrin, VC firms dis- covered that the rate at which inventions and discoveries in materials science—one of the two core technology bases for clean tech—are converted to successful market applications is slower and more unpre- dictable than those of silicon-based tech- nologies, which have followed Moore’s Law for more than five decades.6. The problem is that there is no way to accu- rately predict when a new material or manufacturing process will be invented. Consider battery technology: it has taken 30 years for batteries’ energy density— that industry’s key performance metric— to double. Solar panel efficiency—the rate at which sunlight is converted to electric- ity—has nudged upward at a snail’s pace, Innovationen / Volumen 11, number 3/4 117 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Duncan Duke and Erik Simanis from 11 percent in the 1950s to 22 percent in today’s most efficient commercial pan- els. Im Gegensatz, the manufacturing costs of solar panels have seen a whopping 75 percent decrease in the last few years, Profi- pelled by subsidies in China that have allowed manufacturers to achieve impres- sive economies of scale. Biotechnology, the second clean tech base, has shown performance improve- ments on a par with silicon in some processes. The cost of DNA sequencing, Zum Beispiel, has decreased by orders of magnitude in just a decade. It cost $3 bil-

lion dollars to sequence the first human

genome in 2003; firms can now do it for

less than $1,000. Bedauerlicherweise, biotech- nology faces a serious lack of output flex- ibility. The production processes for bio- logical materials are specialized and idio- syncratic to the type of material, so work- ing with biological material constrains a firm’s ability to pivot quickly to new products and markets. Zum Beispiel, a firm’s R&D efforts to develop a yeast strain that efficiently converts sugarcane into bioethanol cannot easily be used to process saw grass or any other feedstock that may become available. Scaling up biotech processes has also proven devil- ishly hard and much costlier than antici- pated. The case of Amyris exemplifies this. The company was founded in 2003 to produce biodiesel and other sustainable alterna- tives to petroleum-based products using a yeast-based synthetic biology platform and a sugarcane feedstock. The startup raised more than $120 Million, set up a

demonstration plant in Brazil in 2009,

and went public in 2010 to a value of $610 Million. Amyris was in fact considered one of the safest bets in the clean-tech sec- tor because it had already “proven” its technology. Jedoch, it was simply unable to ramp up production fast and efficiently enough. Von 2012, its share price had dropped from a high of $30 to less

als $2 as it abandoned scale-up efforts and pivoted toward low-volume, hoch- margin markets such as cosmetic ingredi- ents. A third issue concerns the consumer. Most clean-tech offerings for emerging consumer markets—from clean-burning cook stoves to solar lanterns—require a moderate to significant change in con- sumer behaviors and routines. Jedoch, if there is one constant in this world, it is that consumers do not like change, even when it offers access to affordable prod- ucts that address pressing unmet needs.7. Take the case of clean-burning cook stoves for emerging markets, an industry that has seen hundreds of initiatives over the past decade but only minimal success, despite a value proposition to consumers that seems quite compelling, For a rural family that purchases firewood, the cost of a clean-burning cook stove can be recouped in just seven to ten months; it will reduce indoor air pollution and the accompanying respiratory-related dis- erleichtert, and it will reduce cooking time.8. Yet cook stove adoption rates have remained stubbornly slow, topping out at just 10 percent in some markets. The rea- son for this consumer apathy is that the stove disrupts long-held cooking prac- tices and, along with solar lanterns, water filter straws, bio-digester toilets, and other exotic clean-tech products, the stoves come across to emerging market consumers as a completely new product category that doesn’t really improve their lives that much. Given the extensive con- sumer learning and change that must accompany such products, rapid scale up is very unlikely, as it takes time and money to activate widespread consumer demand. MONEYBALL FOR EMERGING MARKETS Unfortunately, the soil in which the Silicon Valley VC model thrives isn’t 118 Innovationen / Policy Design Downloaded from http://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Rethinking Green Impact Investing in Emerging Markets Table 4. Private Equity Investment Approaches found in emerging markets or in clean- tech industries. Shallow talent pools, poor deal flows, disaggregated consumers, uncertain technology trajectories, and other factors just don’t yield enough home runs. And, as E+Co discovered, versuchen- ing to enrich the soil with only one or two nutrients isn’t enough. We instead need to start with a different investment strate- gy—one that doesn’t depend on home runs. And what better place to look for inspiration than the source of the home run metaphor itself: baseball. In his breakout book Moneyball, Michael Lewis describes how the Oakland A’s dis- rupted Major League Baseball by fielding an oddball team on a shoestring budget that outplayed wealthy teams staffed with big-name players. The key to their success was the realization that, as a relatively poor team, they could not afford to com- pete in the player market for high-profile home run hitters. Instead they signed players with high on-base averages—a proven ability to get on base one way or another, no matter how unglamorously they did it, be it by an infield bunt, taking a walk, or even being hit by a pitch. These smaller players commanded much salaries than home-run heroes and they did not provide spectacular plays. Jedoch, each one contributed marginal- ly to the team’s overall ability to score runs, and over time this difference added up to wins. In 2002, despite a budget that was one-third that of other teams, the Oakland A’s had a record 20-game win- ning streak and advanced to the playoffs. Translated into investment logic, the Oakland A’s on-base strategy relied on relatively small, consistent returns from a large percentage of a portfolio’s invest- gen, rather than on spectacular returns from one or two breakout ventures. Given what we know about emerging markets, that’s an investment logic with legs. The good news is that the investment commu- nity already applies this core logic in pri- vate equity (PE) investing. Like venture capitalists, PE investors pro- vide capital in exchange for an equity stake in a company—typically a majority stake—which entitles them to a share in the company’s profits and a hand in deci- sionmaking. A key difference from the VC industry, one that shapes the PE investor’s relationship with the investees, is how fast PE investors make money. They have shorter holding periods than venture capitalists and expect returns in three to five years.9. This reduces risk, but because risk and reward move hand in hand, the expected returns from each investee lower. Depending on geography and industry, considerably are innovations / Volumen 11, number 3/4 119 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Duncan Duke and Erik Simanis the average internal hurdle rate—the minimum rate a company expects to earn when investing in a venture—will range from 20 Prozent zu 70 Prozent. To capture low-risk opportunities, PE investors target relatively established companies with dependable cash flows. This reduces market uncertainty and downside risk so that, barring a cata- strophic event, the companies in a PE portfolio are unlikely to fail and lose the entire investment. PE investors also make their money very differently than venture capitalists. PE investors get paid directly from the improved cash flows of their investees or through a “trade sale.” In a trade sale, another company buys the PE investor’s equity stake because of long-term syner- gies and strategic reasons, such as access to a new territory or product market. Valuations for trade sales are typically based on multiples of the investee’s cur- rent earnings. In either case, the PE investor’s return depends directly on how much they help improve cash flows by increasing revenues and cutting costs. We can make a distinction between PE investors focused on growth and those focused on efficiency. PE growth funds invest in smaller companies that have proven their business model in growing industries and want to expand and advance to the “success” stage of business growth.10. The PE investment is ear- marked for specific growth objectives, such as expanding operational capacity, entering a new territory, or developing a new product line. In addition to provid- ing capital, PE investors work in close col- laboration with their investees to provide critical managerial know-how in building the formal control systems and organiza- the tional increased complexity and volume of the decisions that accompany growth. PE investors also facilitate access to new geo- graphic areas and markets, as well as to structures required for networks of suppliers, financiers, and cus- tomers. PE efficiency funds, on the other hand, target midsize to large companies in mostly stable industries that in many cases have enjoyed limited competition. These companies often have inefficient operational processes, outdated technolo- gies, underutilized assets, antiquated branding and marketing strategies, or other legacy systems that create signifi- cant drag on performance. PE efficiency funds bring in hardnosed accountants, comptrollers, and seasoned executives to unlock value by restructuring and mod- ernizing operations and imposing finan- cial discipline. Subsequent improvements in product quality may also boost sales and create new market opportunities. the significant changes Because of entailed, efficiency PEs typically acquire 100 percent of a company’s equity to gain full control and unobstructed decision- Herstellung. The appeal of both PE investment strate- gies for emerging markets is that they overcome several key structural chal- lenges to the VC approach: poor startup deal flow, the lack of new large address- able markets, and weak IPO prospects. For growth PEs, although high-growth startups are in short supply in these mar- kets, small and midsize enterprises are abundant; they account for more than 60 percent of GDP and more than 70 percent of total employment in low-income coun- tries.11. Many of these enterprises are “stuck,” as they have tapped out local demand and lack the contacts, managerial capacity, and capital to propel growth. Emerging markets also offer fertile ground for efficiency PEs. These coun- tries’ protectionist pasts and lack of a strong managerial class have generated rich pools of underperforming firms, many of them in control of natural monopolies. Außerdem, investing in firms with established markets obviates 120 Innovationen / Policy Design Downloaded from http://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Rethinking Green Impact Investing in Emerging Markets the need to discover large but previously untapped markets. zuletzt, as cash-rich corporations face slow or flat economies in developed countries and increasingly seek to enter emerging markets, the opportunity for trade sales and mergers continues to grow. In fact, the burgeoning M&A sector in emerging countries is a seller’s market, as the demand for well-run acquisition targets outstrips the supply.12. AN ON-BASE INVESTMENT STRATEGY FOR GREEN IMPACT A private equity approach provides a compelling format for investing in devel- oping markets, but it can also drive posi- tive environmental impacts. It does so the same way it generates profits: through numerous base hits rather than home runs. Each investment produces small environmental gains, but across an entire portfolio, they add up. How do these base hits relate to the natu- ral environment? Well, the essence of sus- tainability is the measured use of natural resources and ecosystem services so that the environment may remain in balance and replenish itself indefinitely—or, as the Brundtland Commission Report put it, “meeting the needs of the present with- out compromising the ability of future generations to meet their own needs.”13. The PE investment approach, which seeks to improve the productivity of existing organizational resources, also results in a more efficient use of natural resources. How a PE fund enables this depends on whether it is oriented towards efficiency or growth. Simply put, PE efficiency funds invest in high-polluting companies and make their operations cleaner, whereas PE growth funds invest in com- panies with green products and then help them grow, thereby crowding out less environmentally sound products. The focus of PE efficiency funds is, daher, on the environmental impacts that hap- pen “upstream” in a company’s value chain (activities such as raw material sourcing, manufacturing, warehousing, and distribution), while PE growth funds focus on the impacts that occur “down- stream,” once the product is in customers’ hands. Efficiency PE funds look to improve the operational productivity of midsize and large companies in stable industries. The good news is that there is a natural over- lap between improving the environmen- tal efficiency of a company and its opera- tional productivity—in other words, “greening” a company’s value chain deliv- ers significant cost savings. In fact, the dirtier a firm’s current operations, the greater the opportunities for cost reduc- tionen. Efficiency PE funds have three powerful eco-tools to simultaneously drive enhanced profitability and environ- mental performance: green supply chain management, design-for-environment programs, and environmental manage- ment systems. Green supply chain management is a set of practices designed to reduce the green- house gas and particulate emissions, physical foot print, and material use asso- ciated with the use of raw materials and other inputs. For many firms, the lion’s share of their environmental footprint occurs here. Take apparel manufacturers such as Nike, Puma, or Patagonia, Zum Beispiel. When conducting an environ- mental profit-and-loss statement, Puma famously discovered that the leather used in its shoes had the greatest environmen- tal impact due to the land and water production.14. required cattle Similarly, Patagonia realized that pesti- cide-intensive cotton growing in water- stressed regions was one of its most egre- gious environmental transgressions.15. With tools for greening their supply chains, both firms have been able resolve for innovations / Volumen 11, number 3/4 121 Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023 Duncan Duke and Erik Simanis these issues, thus continuing to grow while using fewer natural resources and ecosystem services to do so. Design-for-the-environment programs are efforts to reimagine a firm’s products and services in ways that minimize overall natural resource use. They are based on four design principles: (1) processing and manufacturing using eco-friendly materi- als and processes that minimize waste and hazardous by-products, air pollution, and energy use; (2) designing products for disposal or reuse; (3) the use of packaging with environmentally friendly and recy- cled materials; Und (4) designing products to be energy efficient across their life cycle. Products and processes that are designed for the environment often lead to cost reductions, as they tend to use fewer materials, are less complex, and are cheaper to dispose of. zuletzt, efficiency PE funds can deploy complementary environmental manage- ment programs such as ISO 14001 or EMAS (Eco-Management and Audit Scheme). These systems—which share the underlying waste-reduction and monitor- ing philosophies of Total Quality Management and Lean Manufacturing programs such as Six Sigma, HACCP, and the Toyota Production System—help for ventures uncover opportunities diminishing the negative environmental impacts of their operations in a systematic manner. As 3M discovered, these pro- grams not only reduce environmental harm, they produce significant savings. That is why 3M calls its environmental management “Pollution Prevention Pays,” which the corporation estimates have prevented over two mil- lion tons of waste and saved almost $2 bil-

lion dollars.

Programme

Growth PEs generate positive environ-

mental impacts on the opposite end of the

spectrum: by growing the sales of

young—but proven—companies whose

products reduce the overall environmen-

tal impacts of their customers. A prod-

uct’s potential environmental impacts at

the customer level are shaped by two fac-

tors: (1) the change in environmental

impacts of the customer’s existing “prod-

uct routine”; Und (2) the size of the “prod-

uct market.”

A product routine is the pattern of

Aktionen, behaviors, social relationships,

and physical objects that a consumer

activates during the purchase, use, Und

disposal of a product. Zum Beispiel, Die

product routine around a Starbucks

coffee includes not just the act of drinking

the coffee, but may also include driving

an extra mile on the way to work to pass

by a Starbucks, using unique terms when

ordering (like grande, venti, skinny),

pouring the coffee into an insulated travel

mug that fits the car’s small coffee holder,

adding two packets of sugar and stirring

with a plastic stirrer, steering with one

hand while drinking, disposing of the

paper cup in the office’s recycling bin, Und

washing out the travel mug with dish

liquid and hot water in the office’s

kitchenette.

A product market is the set of products

that—from customers’ perspective—pro-

vide the same core value proposition. A

value proposition is the so-called “job”

that a product satisfies for customers.

Using the Starbucks example, the core

value proposition may be defined as

“quick and easy artisanal coffee.” The

product market includes obvious com-

petitors, like coffee from the local coffee

shop and Dunkin Donuts. But it may also

include a Nespresso machine and its sys-

tem of easy-to-brew pods.

By defining the product routine and the

product markets in which a company’s

product sits, we can calculate the poten-

tial change in aggregate environmental

impact. As our Starbucks example sug-

gests, the environmental impacts at the

customer level can be complex. The envi-

ronmental impact of a Starbuck’s product

122

Innovationen / Policy Design

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023

Rethinking Green Impact Investing in Emerging Markets

routine includes not only the obvious

environmental impacts of making and

landfilling the disposable paper cup and

plastic stir stick but also include addition-

al automobile emissions, manufacturing

and eventual disposal of the plastic travel

mug, the production of the sugar, und das

water and energy consumed in washing

the mug.

aggregate

While there are various frameworks for

assessing

Umwelt

impact, we suggest using the ecosystems

services framework proposed in 2005 von

the United Nation’s Millenium

Ecosystems Report, as it best aligns with a

customer-level view of the world and the

notion that products satisfy jobs for the

user. Ecosystem services are the “jobs”

that humans obtain from the planet. Der

UN report identifies three main types of

ecosystem services: (1) provisioning serv-

ices (material products like lumber, wood

for fuel, or minerals); (2) regulating serv-

ices (benefits from the regulation of

ecosystem processes, like carbon seques-

tration, pest control, and water purifica-

tion); Und (3) cultural services (nonmate-

rial benefits, like recreation and spiritual

enrichment).

Consider the Starbucks product routine

described above. The physical goods used

in conjunction with the coffee—the paper

cup, the plastic stirrer, the sugar, the soap

and water to clean the travel mug—

impact the earth’s provisioning services.

The transportation to the store, welche

generates greenhouse gas emissions,

affects the earth’s regulating services. Ein

analysis of the product routine may, In

fact, conclude that the single greatest

impact of gourmet coffee shops is the

additional auto emissions created.

Now that we know how to assess a prod-

uct’s environmental impact at the cus-

tomer level, the key question is where

should a green growth PE fund invest?

The core logic mirrors that of the green

efficiency PE fund, but with a couple of

added wrinkles: target businesses that

solve the biggest customer pain points in

existing product routines that also have

high environmental impact. The logic

here is to invest in businesses selling bet-

ter solutions into established product

markets that simultaneously cut out the

worst part of the current product routine.

investment

Using the product routine as the basis for

identifying high customer and high envi-

ronmental impact potentially surfaces

Gelegenheiten.

unique

Consider again the Starbuck’s example.

Driving to Starbucks is arguably the most

inconvenient and pain-causing part of the

product routine, particularly for those

stopping by en route to work. And if

emissions are the greatest negative envi-

ronmental impact of that product rou-

tine, then a green PE investment strategy

would target businesses that solve the

transportation part of the coffee product

routine, like Uber Eats, which provides

direct-to-office delivery of meals using its

Uber network of drivers. Using Uber is

arguably a far more efficient way to get

coffee to consumers, particularly as office

workers often combine their orders. And

getting consumers high-quality coffee

directly in their place of work saves con-

sumers significant time, hassle, Und

headache in an already pressure-filled

morning routine.

Now consider an example from India,

and from a product market that has a high

impact on earth’s regulating services:

agricultural fertilizers. Farmers purchase

fertilizer to boost their crop yields.

Fertilizers, Jedoch, can negatively

impact stream and drinking water quality,

particularly when rains wash the nitrogen

and phosphorous that make up fertilizers

into nearby waters.

In developed markets, the product rou-

tine around fertilizers is quite knowledge

and technology intensive, as fertilizers are

expensive and their impacts depend on a

range of factors, including soil profile,

Innovationen / Volumen 11, number 3/4

123

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023

Duncan Duke and Erik Simanis

crop type, stage of growth, and weather.

Soil tests by local agricultural extension

offices, consultations with company rep-

resentatives, weather forecasts, crop

nutrition software, and sophisticated dis-

pensing equipment make up the product

routine. For the 100 million poor small-

holder farmers in India, that routine looks

very different: it typically starts with a

microcredit loan, then purchasing fertiliz-

er from a village store, toting the sacks out

to the farm, and applying the fertilizer

when and how their father or mother did.

If rains come unexpectedly after applica-

tion, that precious fertilizer is wasted.

A green PE growth strategy looks to com-

panies that target this part of the fertilizer

product routine, as it contributes signifi-

cantly to fertilizer pollution and is a big

pain point for farmers (it costs them

money in lost fertilizer and lost yields).

That’s precisely where

fast-growing

enterprise Reuters Market Light (RML)

sits. RML, a spinout of global mass media

and information firm Thomson Reuters,

provides a mobile-phone-based agricul-

tural information service to poor Indian

farmers. Through SMS texts in the local

Sprache, RML provides timely, crop-spe-

cific information, localized and personal-

ized weather forecasts, and local crop

prices to more than five million farmers.

The suite of services helps farmers gener-

aß $4,000 in additional profits annually and savings of $8,000.

CONCLUSION

There is one downside to the on-base PE

approach to green impact in emerging

markets that we have outlined: it’s not

sexy. Implementing ISO-1400 in a local

plastics manufacturer or helping expand

the sales of a midsize enterprise selling

crop and weather information doesn’t

hold the same cachet as investing in new

startups mounting fuel cells in rural vil-

lages. Don’t get us wrong, there are some

opportunities that do feel like break-

through innovations that will catalyze

new markets, scale explosively, und trans-

form entire industries.

A prime example is M-Kopa Solar, welche

in three years reached 50,000 households

and was acquiring 1,000 new customers a

week with only 200 people on staff. Ein

offshoot of M-Pesa—Kenya’s highly

developed and widespread mobile pay-

ment system—M-Kopa offers a simple,

user-installed solar kit that it can meter

over its mobile network. Customers pay

an up-front fee of around $10, and then pay for energy when they need it, on a daily basis, through their phone, or via scratch cards. After they have paid off the kit, they own it outright. M-Pesa and M- Kopa are allowing Kenya to leapfrog high-infrastructure industries such as wired electrification and ATMs. But M- Kopa is an exception, not the rule. As we noted, the market conditions of develop- ing countries, coupled with the con- straints inherent in clean tech, conspire to make this type of home run exceedingly rare. But in investing, optics do matter, partic- ularly when it comes to attracting impact investors. Pitching investors—whether private or public—on a green PE efficien- cy fund pitch isn’t easy in today’s climate, where flashy green innovation funds like the $1 billion Breakthrough Energy

Ventures backed by celebrities such as Bill

Gates, Jeff Bezos, Michael Bloomberg,

and Richard Branson capture investor’s

mindshare and the media’s attention with

their promise of transformational home

runs.

Our goal with this paper, in addition to

outlining a new impact investment prac-

tice, is to lay the first stone in the con-

struction of a new narrative about green

impact investing in emerging markets.

We want to redirect investors’ attention

from flashy, “save the world” moonshots

to the wealth of incremental opportuni-

ties that are ripe for the plucking in estab-

124

Innovationen / Policy Design

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023

Rethinking Green Impact Investing in Emerging Markets

Pyramid: New Approaches for Building

Mutual Value, Hrsg. T. London and S. Hart

(Oberer Saddle River, NJ: FT Press, 2011).

8. S. Bairiganjan, R. Cheung, E. Delio, F.

Fuente, S. Lall, and W. Singh, Power to the

People: Investing in Clean Energy for the

Base of the Pyramid in India (Washington,

D.C.: World Resources Institute, 2010).

9. MacArthur, H. Global Private Equity Report

2017 (Boston, MA: Bain & Co. 2017)

10. N. Churchill and V. Lewis, “The Five

Stages of Small Business Growth,” Harvard

Business Review (1983; 61(3): 30-50).

11. OECD, Promoting Entrepreneurship and

Innovative SMEs in a Global Economy:

Towards a More Responsible and Inclusive

Globalization (Paris, Frankreich: OECD

Veröffentlichungen, 2004).

12. MacArthur, H. Global Private Equity

Bericht 2017 (Boston: Bain & Co. 2017)

13. World Commission on Environment and

Development (The Brundtland

Commission) Unsere gemeinsame Zukunft (Neu

York: Oxford University Press, 1987)

14. Se, P. PUMA’s Environmental Profit and

Loss Account for the Year Ended 31

Dezember 2010. (Herzogenaurach,

Deutschland: PUMA, 2011)

15. Reinhardt, F., R. Casadesus-Masanell, Und

H. Kim. Patagonia (Boston, MA: Harvard

Business School Publishing, 2010)

16. Simanis, E., & Duke, D. 2014. “Profits at

the Bottom of the Pyramid”. Harvard

Business Review, 92, NEIN. 10: 86–93.

lished markets. By contrasting

Die

unbounded risk associated with aiming

for green home runs in developing coun-

tries with the measured risk of the private

equity approach, we hope that investors

will take a fresh look at existing markets,

uncover new opportunities, and better

allocate their green investment dollars

across a variety of ventures.16.

1. J. Freireich and K. Fulton, Investing for

Social and Environmental Impact: A Design

for Catalyzing an Emerging Industry (San

Francisco, CA: Monitor Institute, 2009); S.

Dichter, R. Katz, H. Koh, and A.

Karamchandani, “Closing the Pioneer

Gap,” Stanford Social Innovation Review

2013; 11(1): 36-43); M. Bannick and P.

Goldman, Priming the Pump: The Case for

a Sector Based Approach to Impact

Investing (Redwood City, CA: Omidyar

Netzwerk, 2012).

2. D. Karlan and J. Appel, More than Good

Intentions: How a New Economics Is

Helping to Solve Global Poverty (New York:

Dutton, 2011).

3. E. Simanis, “Reality Check at the Bottom of

the Pyramid,” Harvard Business Review

(2012; 90(6): 120-125).

4. R. Shediac, R. Abouchakra, C. Moujaes, Und

M. Najjar, Economic Diversification: Der

Road to Sustainable Development (Abu

Dhabi: Booz & Co., 2008).

5. L. Pereiro, Valuation of Companies in

Emerging Markets: A Practical Approach

(New York: John Wiley & Sons, 2002).

6.Moore’s Law refers to the observation made

by Gordon Moore in 1965 that the number

of transistors per square inch on integrated

circuits had doubled every year since their

invention. Moore’s Law predicted that this

trend would continue into the foreseeable

future. C. Mack “Fifty Years of Moore’s

Law,” IEEE Transactions on

Semiconductor Manufacturing (2011;

24(2): 202-207).

7. E. Simanis, “Needs, Needs Everywhere, Aber

Not a Market to Tap,” in Next Generation

Business Strategies for the Base of the

Innovationen / Volumen 11, number 3/4

125

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/11/3-4/112/705246/inov_a_00260.pdf by guest on 08 September 2023