Digital Transformation and Risk

Differentiation in the Banking Industry:

Evidence from Chinese Commercial Banks

Xinran Cao

Institute of Digital Finance

National School of Development and China Center for Economic Research

Peking University

xrcao2019@nsd.pku.edu.cn

Boyu Han

School of Economics

Peking University

hanboyu1998@163.com

Yiping Huang

Institute of Digital Finance

National School of Development and China Center for Economic Research

Peking University

yhuang@nsd.pku.edu.cn

Xuanli Xie

Institute of Digital Finance

National School of Development and China Center for Economic Research

Peking University

xxl@nsd.pku.edu.cn

Abstrakt

This paper studies the impact of digital transformation on the ex post risk differentiation of large and

small banks, measured by nonperforming loan (NPL) ratios. It uses the Digital Transformation Index

of Commercial Banks compiled by the Institute of Digital Finance of Peking University, which contains

data on three dimensions—cognition, organization and products—for 97 banks from 2011 Zu 2018.

The three main findings are: (1) the digital transformation of cognition and organization only affects

the NPL ratio through the digital transformation of products; (2) the digital transformation of products

only increases the NPL ratio of small banks, but not large banks; Und (3) the reason for the above results

is that, in fulfillment of the mandatory requirement of lending to the micro-, small, and medium-sized

enterprises (MSMEs), digital transformation makes it easier for large banks to discount commercial

bills held by MSMEs, thereby pushing small banks to extend corporate loans to MSMEs, welche haben

higher risks.

1. Einführung

The banking industry is undergoing digital transformation, and risk is one of the most im-

portant indicators for banking businesses. In the process of technological progress, Dort

is sometimes a lag in the devising and implementation of relevant rules and regulations,

Asian Economic Papers 21:3

© 2022 by the Asian Economic Panel and the Massachusetts Institute of

Technologie

https://doi.org/10.1162/asep_a_00853

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

which frequently leads to the accumulation of financial risks. Digital transformation may

be no exception. China is one of the world’s leading countries in the development of finan-

cial technology, and it is also a country where the banking industry dominates the financial

System. As lending is the core business of banks, it is of great importance to understand the

impact of digital transformation on the loan-side risks in the Chinese banking industry.

The existing literature tentatively concludes that the application of digital finance can

strengthen banks’ ability to resist and control risks (Jin et al. 2020; Li and Yang 2020).

DeYoung et al. (2004) find that due to technological progress, the advantages of small

banks in commercial loans, payment services, customer financing, and customer invest-

ment have been weakened. In terms of risk control, Li and Yang (2020) find that the level

of financial technology development in banks is negatively correlated with the level of

risk borne by banks, and there is a U-shaped relationship between bank market power

and bank risk. Zhao et al. (2021) find that for banks with a high level of digital transfor-

mation, digital transformation is negatively related to their nonperforming loan (NPL) ra-

tio, and for banks with a low level of digital transformation, it is positively related to their

NPL ratio.

The literature provides correlation analysis of the relationship between digital transfor-

mation and risk in the banking industry. Jedoch, it fails to reveal the difference in the

changes in loan risks of large and small banks in the process of digital transformation, Und

it also fails to unveil the essential causes for the changes in banks’ loan risks. Starting from

the ex post risk of bank loans, we study the heterogeneous impact of the digital transfor-

mation of the banking industry on the loan-side risk of large and small banks, as well as the

fundamental reasons for the difference. Daher, this study makes three new contributions to

the literature.

Erste, this study proposes that the digital transformation of banks will lead to differentia-

tion between the ex post risks of the loans of large and small banks. The analysis uses the

Digital Transformation Index of Commercial Banks (Phase 1), constructed by the Institute

of Digital Finance of Peking University (Xie and Wang 2022) with data from banks’ annual

reports from 2011 Zu 2018, to show that the NPL ratio of small banks will increase, und das

NPL ratio of large banks will remain unchanged.

Zweite, this study uses instrumental variables for the digital transformation of banks to

address the potential endogeneity problem. This approach contrasts with the existing

research on digital technology and bank risk, which mainly discusses correlation. Der

analysis here uses the average closest distance between the local city and the cities in the

province along the “eight horizontal and eight vertical” optical fiber trunk network, Die

number of mobile phone users, and a joint instrumental variable that combines them. Daher,

the purpose of using instrumental variables is to identify causality.

2

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Dritte, this paper also explores the mechanism through which digital transformation affects

the ex post risks of the loans of large and small banks differently. The analysis finds that

the cause of the differentiation between large and small banks’ NPL ratios is that digital

transformation has differentiated the loan-side structure of large and small banks.

Policies mandate all banks lending to micro-, small, and medium-sized enterprises

(MSMEs) to improve small firms’ funding conditions.1 Both bill discounting and corpo-

rate loans are loans to companies, as well as to MSMEs. Banks can use bill discounting and

corporate loans to fulfill the policy requirements. Jedoch, the risk implications of these

two types of loans are quite different. Bills held by MSMEs are endorsed by the credit of

large companies or banks.2 Assessing the risk of bill discounting is straightforward: A bank

only needs to check whether the bill is real or not. In der Zwischenzeit, bill discounting has a much

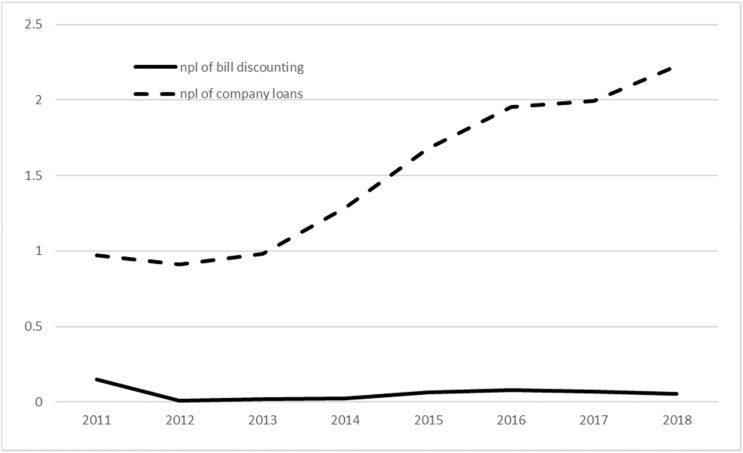

lower risk and, daher, implies a lower NPL ratio.3

Im Gegensatz, corporate loans to MSMEs are dependent purely on MSMEs’ credit worthi-

ness. The risk assessment of a corporate loan is much more complicated: A bank needs to

perform comprehensive due diligence before making a loan.4 The NPL ratios of corporate

loans to MSMEs are relatively high.5 In this way, as long as a bank can use bill discounting

to fulfill the MSME lending target required by the authorities, it would be reluctant to issue

corporate loans endorsed by MSMEs to fulfill the policy requirement.

To fulfill the policy requirements of lending to MSMEs, large banks would first choose bill

discounting. Because MSMEs are scattered across the country, Jedoch, in the traditional

banking environment it is not easy for large banks to conduct bill discounting businesses,

given their limited branch networks. Digital transformation has eased this constraint

because most of the information can now be available online. This allows large banks to

1 Since the CPC National Congress, the Central Bank has always taken serving small and micro

enterprises as the top priority of its work, and financial support for small and micro enterprises

has been increasing overtime. Zum Beispiel, the China Banking Regulatory Commission proposed

a “three no lower than” policy that efforts should be made to achieve the following three goals:

(1) The growth rate of the loans to small and micro enterprises should not be lower than the av-

erage growth rate of all items of loans. (2) The number of small and micro enterprise who receive

loans should not be lower than that in the same period of the previous year. (3) The loan acqui-

sition rate of small and micro enterprises applying for loans should not be lower than that of the

same period last year.

2 We use an example to explain bill discounting. Zum Beispiel, when large company A owes com-

pany B some money, it issues a bill to company B by which company B can get cash from large

company A on the maturity date of the bill. Company B needs to get this money before the matu-

rity date, so it gives the bill to bank C and receives money from bank C, which means that bank C

discount commercial bill (or bill loan) held by company B. Then on the maturity date of the bill,

bank C receives cash from large company A by the bill.

3 As is shown in Figure 1.

4 Due diligence includes checking the balance sheet, spot research, und so weiter.

5 Loans to MSMEs are often risky because of the lack of collateral.

3

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

serve more companies across the country, through bill discounting, given their large pools

of cheap funds (since bill discounting businesses, mostly backed by credit worthiness of

large corporations, have relatively low risks). Expansion of the large banks’ bill discount-

ing business does not necessarily increase their loan risks. In der Zwischenzeit, the small banks

are pushed to extend corporate loans to firms, as the large banks cream-skimmed better

quality businesses from them. Their loan risks could increase as a result.

The rest of the paper is structured as follows. Abschnitt 2 provides a literature review and

points out some directions where this study could make contributions. Abschnitt 3 intro-

duces the data and methodology. Abschnitt 4 presents the regression results and also con-

ducts some robustness tests. Abschnitt 5 offers some concluding remarks.

2. Literature review

2.1 Impact of digital finance on bank risks

As it is a new market force, researchers have focused on the impact of digital finance on

commercial bank risks. Guo and Shen (2015) find that the development of Internet finance

has an impact on the risk-taking of commercial banks. In the early stage of development,

Internet-based finance helps commercial banks to reduce management costs and risk tak-

ing. Jedoch, Internet finance increases capital costs, which intensifies risk taking. Guo

and Shen show that compared with non-systemically important banks, systemically impor-

tant banks have responded more prudently to the development of Internet finance. Some

scholars point out that Internet finance improves depositors’ perception of banks’ risk tak-

ing (Hou et al. 2016). Some have studied the impact of digital finance on banks’ risk taking

from the perspectives of the liability and asset sides. Wang (2015) shows that digital finance

and commercial banks compete directly in the field of business liabilities, dislocate compe-

tition in the field of asset business, and compete in the field of intermediate business, welche

force banks to increase their risk appetite. Konkret, the development of digital finance

has promoted the marketization of deposit interest rates in disguised form, changing the

structure of bank liabilities, which made commercial banks more reliant on interindustry

lending, thereby driving up financing costs (Guo and Shen 2019; Qiu et al. 2018). From the

asset side, the rising cost of the liability side prompts banks to choose higher-risk assets

to make up for the loss caused by the rising cost of the liability side (Qiu et al. 2018). Der

previous literature used the data constructed by the Peking University Digital Financial

Inclusion Index and Baidu searches of words related to “Internet finance,” emphasizing the

use of Alipay and the impact of the Internet finance industry in a broad sense on bank risks.

2.2 Impact of the development of digital finance on bank risks

Most scholars believe that banks’ use of digital finance has a positive impact on their op-

erations (Berger 2003), which is mainly due to the banks’ operational capabilities and risk

Kontrolle. In terms of bank operations, the application of digital finance can greatly reduce

4

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

the temporal and spatial distance between banks and customers and help banks to maxi-

mize customer coverage. Gleichzeitig, digital finance can support the diversification of

commercial banks’ business, Kanäle, and product innovation (Huang and Huang 2018);

optimize customer experience (Xing 2016); improve operational efficiency; and increase

banks’ total factor productivity (Casolaro and Gobbi 2007; Shen and Guo 2015).

DeYoung et al. (2004) describe the past and present of commercial banks through a series

of descriptive statistics and envision their future. They find that changes in technology

and deregulation have intensified competition in the banking industry, threatening the

survival of some banks. With technological progress, small banks have tended to become

more involved in commercial loans, payment services, customer financing, and customer

investment. The advantages of small banks have weakened, and the market share of large

banks has gradually increased with the advance of technology. In 1986, the total assets

of the top ten banks in the United States by assets accounted for 28 percent of all bank

assets. In 2001, this share had increased to 76 Prozent. From this, DeYoung et al. (2004)

infer that future technological advances and deregulation will differentiate large and

small banks. Xie and Gao (2021) use the index compiled by Xie and Wang (2022) to find

that the higher the degree of digital transformation of commercial banks, the better is the

bank performance, especially when banks carry out transformation in the cognitive and

organizational dimensions.

In terms of risk control, with the application of digital finance, commercial banks can better

describe customer profiles and serve “long-tail customers.” This alleviates the information

asymmetry in the traditional banking industry, increasing banks’ market power and ability

to resist and control risks (Jin et al. 2020; Li and Yang 2020). Li and Yang (2020) crawled all

the relevant fintech news in the Advanced Search page of Baidu Information and added

up the number of news articles searched by all the key words at each bank level each year

to obtain the annual total news articles of the sample banks. Using this information, Sie

measure the level of banks’ financial technology development over time. They find that

the level of a bank’s financial technology development is negatively correlated with the

level of risk undertaken by the bank, and there is a relationship between a bank’s market

power and risk. With the strengthening of bank market power, bank risk presents a trend

of “first fall and then rise.” Zhao et al. (2021) use data from company annual reports and

the index compiled by Xie (2020). They find that the relationship between bank digital

transformation and NPL ratio is nonlinear. When the degree of digital transformation is

hoch, the bank digital transformation index and NPL ratio is negatively correlated. Wann

the degree of digital transformation is low, the bank digital transformation and NPL ratio

is positively correlated.

Most existing analyses on the relationship between digital transformation and bank risk

mainly rely on correlation analysis. They have neither reached a consistent conclusion nor

5

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

provided a credible analysis of the mechanism of the impact of digital transformation on

different types of bank risks. In this paper we use the index compiled by Xie (2020) Und

data from banks’ annual reports from 2011 Zu 2018. We first propose that the digital trans-

formation of banks will lead to ex post risk differentiation of the loans of large and small

banks, which is consistent with the Matthew effect. Zusätzlich, we examine the mecha-

nism by which digital transformation differentiates the ex post risks of large and small

banks’ loans, and put forward specific policy recommendations.

3. Data and variables

3.1 Dependent variables

The analysis uses three dependent variables: (1) bank risk (especially the NPL ratio of bank

loans); (2) proportions of bill discounting and corporate loans in all loans; Und (3) average

yield of bill discounting and corporate loans. The data sources are bank annual reports

and the Wind Economic Database, and the data time range is 2011–18. The NPL ratio is

generally used as a proxy variable to measure bank asset-side risk, which is bank ex post

risk measurement.

3.2 Explanatory variables

We use the Digital Transformation Index of Commercial Banks (Phase 1) (hereinafter re-

ferred to as the “Index”) compiled by the Institute of Digital Finance of Peking University

(Xie and Wang 2022) to measure the level of digital transformation of commercial banks.

The time span of the Index is 2011–18. The Index comprises 97 commercial banks, inkl-

ing five large state-owned commercial banks, 12 joint stock commercial banks, Und 80 city

commercial banks.

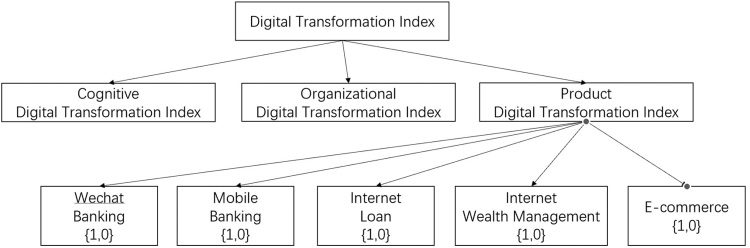

The Index has three sub-indexes: the Cognitive Digital Transformation Index, the Organi-

zational Digital Transformation Index, and the Product Digital Transformation Index. In

Figure A.1, a brief view of the Index is shown.

The Cognitive Digital Transformation Index refers to the commercial banks’ understand-

ing of and emphasis on the “technological change of digital finance,” “digital,” “digital

finance,” and other key words.

The Organizational Digital Transformation Index includes the setting of relevant depart-

ments of digital finance in banks, the setting of directors and executives with information

technology backgrounds, and the banks’ investment related to digital finance.

The Product Digital Transformation Index covers four major sectors: e-banking (mobile

banking/Wechat banking), Internet wealth management, Internet credit, and e-commerce.

6

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Tisch 1. Descriptive statistics

Variable name

Nummer

Mean

SD

Min

Max

Symbol

INDEX

PROFI

ORG

Digital Transformation Index

Product Digital Transformation Index

Organizational Digital Transformation

Index

COG

WECHAT

Cognitive Digital Transformation Index

Cognitive digital transformation–Wechat

NPL

SIZE

ROA

CAR

DGDP

LGDP

COM

MOBILE

DIS

banking {1,0}

Nonperforming loan ratio

Total assets, logarithm

Return on assets

Capital adequacy ratio

Deposits/GDP

Loans/GDP

Competition in the province

Number of mobile phone users

Average shortest distance from the

“eight horizontal and eight vertical”

optical fiber trunk line network to the

cities in the province where the

bank’s headquarters is located

5BIG

Proportion of the number of branches of

LP_COMPANY

LP_BILL

LR_COMPANY

LR_BILL

the five major banks

Proportion of corporate loans

Proportion of discounted bills

Corporate loans yield

Bill discounting yield

667

668

668

667

670

667

631

669

668

648

648

669

527

672

632

232

231

146

99

2.8296

2.2769

1.6295

6.3338

0.8015

1.3621

19.4658

0.9988

0.1287

1.9776

1.5482

0.9431

958.9315

76188.81

2.1411

1.6020

1.4068

6.5200

0.3992

0.8571

1.6435

0.3844

0.0316

4.0478

3.5320

0.0413

711.9078

63510.52

0

0

0

0

0

0.0200

16.6249

0.0200

0

0.4987

0.1655

0.8210

55.7

933.038

11.7667

5

8

39.8337

1

13.2500

24.0447

2.7000

0.6

103.4023

90.1567

1

4076

216477

0.3686

0.0964

0.1793

0.8043

68.6145

4.1173

5.8071

5.1161

8.0334

3.6227

0.9406

1.6164

40.1403

0.0284

3.99

2.06

87.1252

22.0081

7.79

10.61

The Product Digital Transformation Index is the most direct and core part of measuring

the digital finance strategy of commercial banks (Xie and Wang 2022). The Product Dig-

ital Transformation Index reflects banks’ activity in product digital transformation and

is divided into six levels: none = 0, very low = 1, low = 2, medium = 3, high = 4, Und

very high = 5.

3.3 Control variables

We control for the individual bank-level factors and city-level factors. The bank-level fac-

tors include the return on assets, capital adequacy ratio, and total assets. The city-level

controls are the degree of local economic development (province gross domestic product

[BIP]), the degree of local financial development (deposits/GDP and loans/GDP), und das

degree of local financial competition at the prefecture-level city level (the proportion of the

number of branches of the five largest banks). Zusätzlich, because the research objective

of this paper is to analyze the digital transformation of banks, we use the Digital Financial

Inclusion Index (Fintech) of the Peking University Digital Financial Inclusion Index to rep-

resent the local level of digital financial development and the level of local competition in

digital finance. The analysis also controls time and province-level fixed effects, to control

for changes at the policy level and other factors.

Tisch 1 provides the descriptive statistics of the variables. We drop the sample whose core

variables are missing and outliers.

7

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

4. Empirical analysis

4.1 Model setting

We focus on the impact of bank digital transformation on bank risk. Referring to

Demirgüc-Kunt and Huizinga (2010), we construct the relationship between banks’ NPL

ratio and banks’ Digital Transformation Index.

Yit

= β

0

+ β

1tranit

+ β

2Xit

+ λ

T

+ δ

ich

+ ε

Es

,

(1)

where Yit is banks’ NPL ratio; tranit is the bank Digital Transformation Index; and Xit is

the control variables, including the asset-liability ratio, capital adequacy ratio, total assets

(logarithm), GDP per capita (logarithm), deposits/GDP, loans/GDP, proportion of the

number of branches of the five largest banks, and the overall Digital Financial Inclusion

Index. λ

i is the province fixed effect or the bank fixed effect.

t is the time fixed effect, and δ

The following methods are adopted to solve the endogeneity problem.

Erste, the next period of the NPL ratio is used as the dependent variable to estimate the

impact of the digital transformation of banks on the NPL ratio.

Zweite, the number of mobile phone users at the prefecture level at the end of the year

and the average closest distance to cities in the province along the “eight horizontal and

eight vertical” optical fiber trunk line in the province where the bank’s headquarters is lo-

cated are respectively used as instrumental variables for the digital transformation index of

banks, and the two are used as a joint instrumental variable for the digital transformation

index of banks.

The equations for the mechanism analysis are the following:

RATIOit

RETURNit

= β

= β

0

0

+ β

1TRANit

+ β

2Xit

+ λ

T

+ δ

ich

+ ε

Es

,

+ β

1TRANit

+ β

2Xit

+ λ

T

+ δ

ich

+ ε

Es

,

(2)

(3)

where RATIOit represents the proportion of discounted bills, corporate loans, und persönlich

loans to total loans, jeweils; RETURNit represents the average yields of discounted

bills, corporate loans, and personal loans, jeweils; TRANit is the digital transforma-

tion index of the bank; Xit is the control variables, including the asset-liability ratio, cap-

ital adequacy ratio, total assets (logarithm), GDP per capita (logarithm), deposits/GDP,

loans/GDP, proportion of loans from the five major banks, and digital financial inclusion

aggregate index. λ

fixed effect.

i is the province fixed effect or the bank

t is the time fixed effect, and δ

8

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Tisch 2. Benchmark regression with the full sample: Impacts of

the overall Bank Digital Transformation Index and sub-indexes

on banks’ ex post risk

Digital Transformation Index

Product Digital Transformation Index

Organization Digital Transformation Index

Cognitive Digital Transformation Index

Bank control variables

City control variables

Province fixed effect

Year fixed effect

Robust standard error

Number of observations

R2

(3)

(2)

(1)

Nonperforming loan ratio

Full sample

−0.0229

(0.0290)

0.0446**

(0.0226)

Ja

Ja

Ja

Ja

Ja

633

0.3977

Ja

Ja

Ja

Ja

Ja

634

0.3991

0.0630***

(0.0232)

−0.0150

(0.0238)

−0.0128*

(0.0076)

Ja

Ja

Ja

Ja

Ja

633

0.4031

Notiz: Standard errors are in parentheses. ***Statistically significant at the 1 percent level;

**statistically significant at the 5 percent level; *statistically significant at the 10 percent level.

4.2 Benchmark regression without sample division

Tisch 2 presents the results of the benchmark regression, showing how the Digital Trans-

formation Index and its sub-indexes (Product Digital Transformation Index, Organiza-

tional Digital Transformation Index, and Cognitive Digital Transformation Index) affect

the NPL ratio, which represents banks’ ex post risk. The table shows the results of the full

sample regression, which indicates that the overall Digital Transformation Index, the Orga-

nizational Digital Transformation Index, and the Cognitive Digital Transformation Index

do not affect banks’ NPL ratio.

The Product Digital Transformation index has direct and indirect effects on the NPL ratio.

In column (2), which includes all the sub-indexes, when the Product Digital Transforma-

tion Index increases by 1 unit, the NPL ratio increases by 0.0446 unit. In column (3), welche

includes only the Product Digital Transformation Index, when it increases by 1 unit, Die

NPL ratio increases by 0.0630 unit. Mit anderen Worten, on average, the NPL ratio of the bank

with the most active product digitization was 0.315 percent higher than that of a bank with-

out product digitization. Tisch 2 shows that from the perspective of the whole sample, bei

this stage, only the digital transformation of products has increased the NPL ratio, Und

the digital transformation of organizations and cognitive digital transformation can only

increase banks’ NPL ratio through the digital transformation of products.

This may be because only the digital transformation of products will change the banks’

main deposit and loan-related behavior, while organizational digital transformation and

cognitive digital transformation may not directly affect banks’ behavior through channels

other than product digital transformation. This also may be because it takes less time for

9

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Tisch 3. Benchmark regression of large and small banks: Nonperforming loan ratio,

bank size, and Product Digital Transformation Index

(2)

(1)

Nonperforming loan ratio

Large banks

Small banks

Product Digital Transformation Index

0.0444

(0.0403)

0.0593**

(0.0298)

Wechat bank {1,0}

Bank control variables

City control variables

Province fixed effect

Bank fixed effect

Year fixed effect

Robust standard error

Number of observations

R2

Ja

Ja

NEIN

Ja

Ja

Ja

80

0.9102

Ja

Ja

NEIN

Ja

Ja

Ja

554

0.5348

(3)

(4)

Large banks

Small banks

0.0011

(0.1246)

Ja

Ja

Ja

NEIN

Ja

Ja

80

0.8112

0.2593***

(0.0887)

Ja

Ja

Ja

NEIN

Ja

Ja

556

0.4189

Notiz: Standard errors are in parentheses. ***Statistically significant at the 1 percent level; **statistically significant at the

5 percent level.

product digital transformation to affect banks’ risk, while the organization and cognitive

digital transformation may take longer. The total duration of the digital transformation of

banks is currently only 11 Jahre, so this impact cannot be obtained from the existing data.

4.3 Benchmark regression with large and small banks

Banks of different size may have different ways to conduct business. daher, digital

transformation may have different effects on large banks and small banks. In diesem Abschnitt,

we divide banks into subsamples for further analysis.

Tisch 3 divides the sample into large and small banks. We use two methods to separate

large and small banks, with the second method creating the samples for the robustness test

of the first method. For the first division method, the top ten banks in asset size are large

banks and the others are small banks; for the second method, the top 15 banks in asset size

are large banks. The results of the second division method are similar to those of the first

division method, so only the regression results of the first division method are discussed

in the text. The second division method is regarded as a robustness test, and the results are

provided in Table A.2.

In Table 3, the explanatory variable in columns (1) Und (2) is the Product Digital Trans-

formation Index.6 The explanatory variable in columns (3) Und (4) is whether a bank has

Wechat banking (yes = 1, no = 0). The regression results show that when the product digi-

tization index increases by one unit, the NPL ratio of small banks increases by 0.0593 unit.

6 Product Digital Transformation Index has five sub-indexes: the existence of Wechat banking {1,0},

the existence of mobile banking {1,0}, the existence of Internet loan products {1,0}, the existence of

Internet wealth management products {1,0}, and the existence of e-commerce {1,0}. More detailed

aspects of the regression can be seen in Table A.1 and Table A.2.

10

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

In terms of the direct effect, compared with large banks without Wechat banking, Dort

is no significant change in the NPL ratio of large banks with Wechat banking. Compared

with small banks without Wechat banking, the NPL ratio of small banks with Wechat

banking increases by 0.2593 unit. We also test the impacts of other four variables: the ex-

istence of mobile banking (yes = 1, no = 0), the existence of Internet loan products (yes =

1, no = 0), the existence of Internet wealth management products (yes = 1, no = 0), Und

the existence of e-commerce (yes = 1, no = 0). We find that the impacts of these four vari-

ables on the NPL ratios of large and small banks are neither stable nor significant, as is

shown Table A.1.

The heterogeneity analysis in Table 3 shows that the digital transformation of products did

not increase the NPL ratio of large banks, but it increased the NPL ratio of small banks.

In Table A.2, the regression includes province fixed effects, and the results are still ro-

bust. To sum up, from the perspective of the whole sample, the general digital transfor-

mation of banks, the first-level cognitive digital transformation, and the digital transfor-

mation of organizations do not affect banks’ NPL ratios; only the digital transformation

of products affects banks’ NPL ratios. The digital transformation of products has not in-

creased large banks’ NPL ratio (ex post risk), but has increased small banks’ NPL ratio

(ex post risk).

4.4 Robustness test

So far, the analysis has assumed that the digital transformation of banks is exogenous with

respect to the disturbance term after adding fixed effects and other control variables. Al-

though the bank characteristic variables, city characteristic variables, and fixed effects

have been controlled as much as possible, it is still difficult for the model to ensure that

the above fixed effect regression controls all the variables that may affect the digital trans-

formation of banks and bank risks at the same time. An endogeneity problem caused by

omitted variables or reverse causality would affect the consistency of the fixed effect re-

Ergebnisse. daher, we conduct further robustness tests on the benchmark regression results

for small and large banks.

To solve the endogeneity problem, we adopt the following strategy.

We use instrumental variables to solve the endogeneity problem. We use three instrumen-

tal variables. The first is the average closest distance between the city where the bank’s

headquarters is located and the cities in the province along the “eight horizontal and eight

vertical” optical fiber trunk network. The second is the number of mobile phone users at

the prefecture level at the end of the year, as the instrumental variables for the banks’ digi-

tal transformation. The third is the joint instrumental variable of the two variables above.

The launch and use of digital banking products rely on fast and stable mobile Internet

Signale. The National Development and Reform Commission (the former State Planning

11

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Commission) and the Ministry of Industry and Information Technology (the former Min-

istry of Posts and Telecommunications) built the “eight horizontal and eight vertical” large

capacity optical fiber communication trunk network covering cities above the provincial

capital and 90 percent of the prefectures in the country from 1986 Zu 2000. The rapid devel-

opment of the communications industry in the 1990s laid a solid foundation for the rapid

popularization of mobile networks and the development of digital finance. To a certain ex-

tent, the distance between the city where a bank’s headquarters is located and the optical

fiber communication trunk network reflects the level of convenience and cost for the bank,

local residents, and companies to obtain fast and stable Internet services.

Allgemein, the closer the city is to the optical fiber trunk line, the higher are the stability and

quality of its Internet services, which is more conducive to the digital transformation of

local banking products. In addition to affecting the NPL ratio of banks through the digital

transformation of banks, the optical fiber network may also affect the behavior of residents

and companies through the use of Alipay and other digital inclusive financial services,

thereby affecting the NPL ratios of banks. Jedoch, our control variables already include

the Peking University Digital Financial Inclusion Index, which excludes this possible chan-

nel. It is unlikely that the fiber communication trunk network, which was built as early as

the 1990s, could affect banks’ NPL ratios through other channels.

Ähnlich, mobile phones, as the most important tool for the use of digital banking prod-

Produkte, are closely related to the digital transformation of banking products. Zusätzlich, nach

controlling for the local economic development level, financial development level, and dig-

ital financial inclusion index, there is no direct correlation channel between the number of

mobile phone users at the prefecture level and bank risk, which make it possible to become

an effective instrumental variable. Zweite, the NPL ratio in the next period is used as the

dependent variable, the instrumental variables of the bank’s digital transformation remain

unchanged, and a robustness test is performed.

Bedauerlicherweise, because large banks are spread all over the country, we cannot find in-

strumental variables for the digital transformation of large banks. The best way is to

use explanatory variables to regress the next period of the dependent variables for large

banks. The results are shown in Table A.3, and they are consistent with the benchmark

regression results.

Tisch 4 reports the results of the endogeneity analysis, including the regression using lag of

the explanatory variable and the instrumental variable regression.

In columns (1) Und (2), the dependent variable is the lag of the NPL ratio. Columns (3)–

(5) are instrumental variable regressions, and the dependent variable is the NPL ratio.

The instrumental variable for column (3) is the average shortest distance from the “eight

horizontal and eight vertical” optical fiber trunk line network to the cities in the province

12

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Tisch 4. Endogeneity: Large banks (dependent variable in the next period) and small banks

(dependent variable in the next period and instrumental variables, jeweils)

Product Digital Transformation Index

(Wechat bank)

Bank control variables

City control variables

Province fixed effect

Year fixed effect

Robust standard error

Number of observations

R2

First-stage F

Prob > F

χ 2

Prob > χ 2

(1)

NPL_lag

Big banks

−0.0865

(0.0657)

Ja

Ja

NEIN

Ja

Ja

70

0.9130

(2)

Small banks

(3)

NPL

Small banks

(4)

(5)

Small banks

Small banks

0.1543*

(0.0912)

Ja

Ja

NEIN

Ja

Ja

485

0.5709

2.1655**

(0.9425)

Ja

NEIN

Ja

Ja

Ja

556

0.0406

9.7011

0.0019***

1.4569**

(0.6767)

Ja

NEIN

Ja

Ja

Ja

507

0.2863

12.2319

0.0005***

1.7646***

(0.6564)

Ja

NEIN

Ja

Ja

Ja

507

0.2075

8.8161

0.0002***

0.4852

0.4861

Notiz: Standard errors are in parentheses. ***Statistically significant at the 1 percent level; **statistically significant at the 5 percent level;

*statistically significant at the 10 percent level. The control variables include the digital financial inclusion index at the prefecture level.

where the bank’s headquarters is located. The instrumental variable for column (4) ist der

number of mobile phone users at the prefecture level at the end of the year. The instru-

mental variable for column (5) is the joint instrumental variable of the two instrumental

Variablen. Due to space limitations, we do not report the regression results for the first

stage, but we report the Kleibergen-Paap rk F-statistic and its p-value. The F-statistic of

the first stage-regression is high. Bei der 1 percent level, the null hypothesis of the problem

of weak instrumental variables is rejected, indicating that the instrumental variables are

not weak. Zusätzlich, referring to Dinger and von Hagen (2009), we partially demonstrate

the exogeneity of the joint instrumental variable using the overidentification test, Bericht-

ing the Wald statistic and its p-value. Daher, there is no overidentification problem, welche

partially proves the exogeneity of the joint instrumental variable. Tisch 4 shows that the

digital transformation of products through Wechat banking indeed increases the NPL ratio

of small banks.

4.5 Mechanism analysis

The previous analysis showed that the digital transformation of banks’ products can in-

crease the NPL ratio of small banks, but it does not increase the NPL ratio of large banks.

These results are statistically and economically significant. This section proposes and tests

a hypothesis for the mechanism for the relationship between digital transformation and the

NPL ratio.

4.5.1 Proposition of the hypothesis

Our hypothesis is as follows.

(1) Digital transformation increases the proportion of large banks’ bill loans or the yield

of large banks’ bill loans, which means that large banks extended the user group of

bill discounting.

13

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Figur 1. Fact 1: Discounted bills have a lower NPL ratio compared with corporate loans

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

(2) Digital transformation increases the proportion of small banks’ corporate loans or the

yield of small banks’ corporate loans, which means that small banks extended the user

group of corporate loans.

(3) Digital transformation decreases the proportion of small banks’ bill loans and de-

creases the proportion of large banks’ corporate loans.

There are two types of bank loans to companies. One is bill discounting, which is loans to

other companies that are endorsed by large company credit or bank credit. The other type

is corporate loans, which are loans to companies that are endorsed by their own credit.

The average NPL ratio of bill discounting is higher than that of corporate loans (Figur 1).

Against the background that banking sector policy mandates that all banks extend their

user group of loans, both bill discounting and corporate loans are ways to fulfill the pol-

icy requirements. It is easier to check whether companies will default on bill discounting

loans because it is only necessary to verify the authenticity of the bills. What’s more, Die

NPL ratio of bill accounting is lower. Jedoch, corporate loans are endorsed by the credit

of MSMEs and require complex prior risk assessment, such as due diligence. daher, als

long as a bank can use bill discounting to fulfill the MSME loan target required by the pol-

icy, it is reluctant to issue corporate loans endorsed by small business credit to fulfill the

policy requirement.

14

Asian Economic Papers

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Tisch 5. Fact 2: In prefecture-level cities with low GDP, the proportion of large bank

branches is low

Number of branches of the five major banks in prefecture-level cities

Number of all bank branches in prefecture-level cities

Log (BIP) (prefecture level)

Time fixed effect

0.4436***

(0.1798)

NEIN

2.0881***

(0.1984)

Ja

Notiz: Standard errors are in parentheses. ***Statistically significant at the 1 percent level.

Tisch 6. Robustness check of the mechanism

(2)

(1)

Bill discounting/

Total loans

Groß

banks

(4)

(3)

Corporate loans/

Total loans

Groß

banks

Small

banks

(6)

(5)

Bill discounting

yield

Groß

banks

Small

banks

(8)

(7)

Corporate loans

yield

Groß

banks

Small

banks

Product Digital

Transformation Index

Bank control variables

City control variables

Bank fixed effect

Year fixed effect

Robust standard error

Number of observations

R2

0.8648***

(0.2277)

Ja

Ja

Ja

Ja

Ja

80

0.5925

Small

banks

−0.7668*** −1.4903**

(0.6615)

(0.2291)

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

80

150

0.9287

0.7340

0.3734

(0.3414)

Ja

Ja

Ja

Ja

Ja

151

0.8136

0.2853**

(0.1407)

Ja

Ja

Ja

Ja

Ja

56

0.9314

0.1650

(0.2152)

Ja

Ja

Ja

Ja

Ja

43

0.9528

0.0371

(0.0515)

Ja

Ja

Ja

Ja

Ja

66

0.9768

0.0807***

(0.0380)

Ja

Ja

Ja

Ja

Ja

79

0.9699

Notiz: Standard errors are in parentheses. ***Statistically significant at the 1 percent level; **statistically significant at the 5 percent level.

To fulfill the policy requirements for lending to MSMEs, large banks prioritize bill dis-

counting. Jedoch, against the background of using traditional financial methods, Dort

is a major obstacle to extend the large bank bill discounting user group: In “poor places,”

the ratio of large bank branches to small bank branches is relatively small and cannot cap-

ture all the local customers, as is shown in Table 5, which has become an obstacle to extend

the bill discounting business of large banks. Digital transformation makes it unnecessary

for large banks to rely on branch offices for bill discounting business, which is beneficial

for large banks extending bill discounting business, thereby pushing small banks to the

corporate loan business—the harder and riskier one.

4.5.2 Validation of the hypothesis

regression results in Table 6 verify hypotheses (1) Zu (3), using the samples of large and

small banks.

The following regressions test our hypothesis. Der

According to Table 6, the regression results show that when the Product Digital Transfor-

mation Index increases by 1 unit, large banks’ proportion of corporate loans decreases by

1.49 Prozent, large banks’ proportion of discounted bills increases by 0.86 Prozent, small

banks’ proportion of corporate loans is relatively stable, and small banks’ proportion

of discounted bills decreases by 0.77 Prozent. Das ist, on average, compared with large

15

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

banks without digital transformation, among large banks with a high degree of digital

transformation, the proportion of corporate loans decreases by 7.45 Prozent, und das

proportion of discounted bills increases by 4.3 Prozent. Transformed small banks, mit

a high degree of digital transformation, decrease their proportion of discounted bills

von 3.85 Prozent.

When the Product Digital Transformation Index increases by 1 unit, the corporate loan

yield of small banks increased by 0.0807 Prozent, and the discounted bill yields of large

banks increases by 0.2853 Prozent. Das ist, on average, compared with large banks without

product digitization, the discount rate of bills of large banks with a high degree of product

digitization increases by 1.427 Prozent. Compared with small banks without product digi-

tization, small banks with a high degree of product digitization had a 0.404 percent higher

loan yield.

Table A.3 provides the results of a robustness check, in which we use the second method to

define “large banks.”

5. Concluding remarks

We use the Digital Transformation Index of Commercial Banks and data from the annual

reports of 97 banks, with a time span of 2011–18, to study the effect of commercial banks’

digital transformation on the NPL ratios of large and small banks.

Das finden wir:

(1) At this stage, out of three dimensions of banks’ digital transformation—cognition, oder-

ganization, and products—only transformation of products has significant impacts on

banks’ current NPL ratios. Changes in organization and cognition are effective only

through their influence on changes in products. This may be because only changes in

products represent material adjustments in banking businesses, while changes in orga-

nization and cognition can only have real impacts if they affect banks’ financial prod-

Produkte. This may also be because it takes less time for new products to affect banks’ risk,

while changes in organization and cognition may take a longer time to be effective. Der

study covers a period of 11 Jahre, which is probably too short for examining the real

impact of digital transformation of the banks, let alone that most banks started digital

transformation only in recent years.

(2) The digital transformation in terms of the products of large banks did not change their

NPL ratios, while that of small banks increased their NPL ratios. This confirms that the

digital transformation of banks had an important difference in terms of risk implica-

tions between large and small banks.

16

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

(3) The broad story of risk differentiation between large and small banks is that all banks

are required by the authorities to increase their lending to MSMEs every year—and

they all try hard to fulfill this requirement. Against this institutional background, groß

banks take advantage of digital transformation to expand their bill discounting busi-

nesses. One of the consequences of digital transformation is that more information

about bills held by MSMEs becomes available online. This allows large banks to ex-

tend bill discounting services to more MSMEs than before, using their advantages of

large pools of cheap funds. Because the bills are often backed by large corporations’

credit worthiness, this expansion of bill discounting businesses by the large banks does

not increase loan risks. Since the large banks now serve more MSMEs with relatively

higher quality, the small banks have to reach more and lower-quality MSMEs by of-

fering corporate loans, to satisfy the policy requirement. But this inevitably leads to

higher loan risks for the small banks.

Gesamt, it is not a bad outcome for the whole economy, as large banks increase their bill

discounting business, and therefore push small banks to extend corporate loans to firms

who have higher risks. Gesamt, MSMEs receive more funding, as a result. The logic of

the large and the small banks’ lending to small businesses is different: Large banks are

more distant from the MSMEs, in general, and therefore, do not have enough soft infor-

mation to support uncollateralized loans to MSMEs (Williamson 1967). Andererseits,

small banks tend to have much closer relationships with the owners of the small banks,

or even the owners themselves. As a result the owner of the bank may allow the lender

to use more soft information (information on local businesses and business owners, usw.)

in lending decisions. In this way, small banks rely more on soft information for making

loans (Cole 2004). This gives small banks a natural comparative advantage in lending to

small businesses. Im Gegensatz, large banks have comparative advantages in the bill dis-

counting business. This is because part of the business in bill discounting is the loan en-

dorsed by the credit of large companies. Compared with small banks, large banks often

have stronger relationships with large companies. daher, development of the bill dis-

counting business by large banks will help more MSMEs to obtain short-term financing

through bill discounting. Daher, we believe that the rise of NPL itself may not totally be a

bad thing, since more entities can have access to financial resources after bank digital trans-

Formation. Gleichzeitig, the differentiation of NPL ratio may be a good phenomenon,

because it means that both large banks and small banks do the business where they have

comparative advantages.

The NPL ratio is an important indicator for monitoring bank risks, but its role is limited.

Zum Beispiel, the NPL ratio cannot monitor off-balance-sheet risks. The NPL ratio of bill

discounting must be lower. Jedoch, this does not mean that the off-balance-sheet risks

and financial system risks brought by bill discounting are lower than those of corpo-

rate loans. Discounted bills are short-term loans, generally no more than 180 Tage, Und

17

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

essentially money market funds, which may lead to problems such as the term mismatch.7

At the State Council executive meeting on 20 Februar 2019, Li Keqiang said: The rise of

bill financing and short-term loans may not only cause “arbitrage” and “fund idling,” but

also may bring new potential risks.

Based on these findings, we also offer some policy recommendations.

Erste, it is important to look objectively at the optimization of the real economic services

behind the risk differentiation of large and small banks, and not to carry out blind control

on the differentiation of NPL ratio and the rise of NPL ratio of small banks.

Zweite, we recommend targeted prevention of possible systemic financial risks in the pro-

cess of digital transformation of the banking industry. As mentioned herein, bill discount-

ing can cause risks off the balance sheet. This requires regulators to pay special attention

to where the funds of MSMEs obtained from large banks go. The government can use dig-

ital technology to integrate the information of logistics, capital flow, information flow, Und

other information on MSMEs and connect them to the digital bill discounting business of

large companies. In this way, the digital bill discounting business of large banks is not just

an online discount of traditional bills, but also allows for better supervision of the flow of

funds from large banks to MSMEs, which can improve the quality of large banks’ services

for financing private and MSMEs through discounted bills.

Dritte, we recommend scientific guidance of the banking industry to use digital technology

to serve the real economy. Both discounted bills and corporate loans are essentially ways

to expand loans to MSMEs. Regulators should think about how to guide the future pattern

of the banking industry, in terms of the method for achieving the goal of enabling digital-

ization to assist in financing MSMEs. It is not necessary for regulators to impose the same

requirements on large and small banks. Stattdessen, the requirements should comply with the

comparative advantages of large and small banks.8 For example, regulators should not

require large and small banks to lend to MSMEs in the same way. What’s more, regula-

tors should not only look at the NPL ratio as a general indicator. Stattdessen, they can set “red

lines” for the NPL ratios of bill discounting and corporate loans separately. Regulators can

tolerate higher NPL ratios of small banks, thus encouraging them to give more corporate

loans to MSMEs, which uses soft information.

7 In many cases, companies use short-term company loans to finance for their long-term investment

and research and development expenditure.

8 As we have mentioned above, small banks have a natural comparative advantage in lending to

MSMEs because they can rely more on soft information for making loans (Cole 2004). Im Gegensatz,

the large banks have comparative advantages in the bill discounting business.

18

Asian Economic Papers

l

D

Ö

w

N

Ö

A

D

e

D

F

R

Ö

M

H

T

T

P

:

/

/

D

ich

R

e

C

T

.

M

ich

T

.

/

e

D

u

A

S

e

P

A

R

T

ich

C

e

–

P

D

/

l

F

/

/

/

/

/

2

1

3

1

2

0

5

0

0

9

2

A

S

e

P

_

A

_

0

0

8

5

3

P

D

.

F

B

j

G

u

e

S

T

T

Ö

N

0

7

S

e

P

e

M

B

e

R

2

0

2

3

Digital Transformation and Risk Differentiation in the Banking Industry: Evidence from Chinese Commercial Banks

Verweise

Berger, Allen N. 2003. The Economic Effects of Technological Progress: Evidence from the Banking

Industry. Journal of Money, Credit and Banking 35(2):141–176. 10.1353/mcb.2003.0009.

Casolaro, Luca, and Giorgio Gobbi. 2007. Information Technology and Productivity Changes in the

Banking Industry. Economic Notes 36(1):43–76. 10.1111/j.1468-0300.2007.00178.x.

Cole, Matthew A. 2004. Trade, the Pollution Haven Hypothesis and the Environmental Kuznets

Curve: Examining the Linkages. Ecological Economic 48(1):71–81. 10.1016/j.ecolecon.2003.09.007.

Demirgüç-Kunt, Asli, and Harry Huizinga. 2010. Bank Activity and Funding Strategies: The Impact

on Risk and Returns. Journal of Financial Economic 98(3):626–650.

DeYoung, Robert, William C. Hunter, and Gregory F. Udell. 2004. The Past, Present, and Probable

Future for Community Banks. Journal of Financial Services Research 25(2):85–133. 10.1023/B:FINA

.0000020656.65653.79.

Dinger, Valeria, and Jurgen von Hagen. 2009. Does Interbank Borrowing Reduce Bank Risk? Zeitschrift für

Money, Credit and Banking 41(2-3):491–506. 10.1111/j.1538-4616.2009.00217.x.

(cid:2)

Guo, Pin, and Yue Shen. 2015. Does Internet Finance Increase Commercial Banks

ical Evidence from Chinese Banks [in Chinese]. Nankai Economic Studies 4:80–97.

Risk-taking? Empir-

Guo, Pin, and Yue Shen. 2019. Internet Finance, Deposit Competition, and Bank Risk-Taking [in Chi-

nese]. Journal of Financial Research 8:58–76.

Hou, Xiaohui, Zhixian Gao, and Qing Wang. 2016. Internet Finance Development and Banking Mar-

ket Discipline: Evidence from China. Journal of Financial Stability 22:88–100. 10.1016/j.jfs.2016.01.001.

Huang, Yiping, and Zhuo Huang. 2018. Digital Finance Development in China: Present and Future

[in Chinese]. Economics (Quarterly) 17(4):1489–1502.

Jin, Hongfei, Hongji Lin, and Yinlu Liu. 2020. FinTech, Banking Risks and Market Crowding-Out

Effect [in Chinese]. Journal of Finance and Economics 5:52–65.

Li, Xuefeng, and Panpan Yang. 2020. Fintech, Market Power and Bank Risk [in Chinese]. Modern

Economic Science 1:45–57.

Qiu, Han, Yiping Huang, and Yang Ji. 2018. How Does FinTech Development Affect Traditional

Banking in China? The Perspective of Online Wealth Management Products [in Chinese]. Zeitschrift für

Financial Research 11:17–29.

Shen, Yue, and Pin Guo. 2015. Interest Finance, Technology Spillover and Commercial Banks TFP [In