ADVANCES IN REAL

TIME

CHALLENGES AND SOLUTIONS IN INTEROPERABLE

PAYMENT SYSTEMS

KOSTA PERIC, MILLER ABEL, AND MATT BOHAN

Finance can be very complex, but at its core it’s about exchanging value

between parties. In a word, payments. Making payments is a fundamental

financial action for most people around the globe, whether they use cards, cash,

or SMS to make them.

In terms of financial infrastructure,

Dann, a payments platform is a fundamen-

tal piece, the anchor that tethers the daily

financial actions of customers to the daily

holdings of financial providers. Such plat-

forms commonly have a national scale

because of country-specific currencies

and regulations. Jedoch, they also can

be regional, as we see in the EU and the

South African Development Community,

und international, as we see with credit

card systems. International platforms will

become more necessary as digitization

continues to put the common citizen in

touch with others far beyond the borders

of their home country.

In fact, the rise of digital financial

services has changed the nature of pay-

ments and payment platforms in many

ways. Customers can transfer money

across great distances with a few taps on

their mobile phones, with low or no asso-

ciated fees. Providers can reach customers

they weren’t able to before—namely, peo-

ple with very limited assets who are either

In

services.

unbanked or underserved by predigital

financial

emerging

economies, telecoms and other non-bank

institutions are stepping in to take advan-

tage of this opportunity by offering digital

payment services, such as mobile money.

This new dynamic between cus-

tomers and providers, and the opportuni-

ties this evolution presents, has raised

some compelling questions about how

payment platforms exist and interact at

the system level. Because of the positive

impact digital accounts and payments can

have on the lives of the poor, the Bill &

Melinda Gates Foundation has explored

these questions in great detail.

The outcome of that exploration was

the development of the Level One Project

(L1P), an initiative to promote the cre-

ation and evolution of inclusive, interop-

erable digital payment platforms. At the

center of this initiative are the L1P princi-

ples (see box), which list the attributes

essential to making payment systems

accessible to poor customers and support-

70

Innovationen / Blockchain for Global Development

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

ive of various financial service providers

(see http://leveloneproject.org for more

Einzelheiten).

In this article, we explore some of

those principles and the challenges of

implementing them. We also explore how

modern technologies related to distrib-

uted ledgers were adapted to support a

reference implementation (see below) von

the L1P principles. Released in October

2017, this reference implementation

demonstrates the viability of pro-poor

payment platforms and offers govern-

ments and commercial providers a flexi-

ble way of developing such platforms.

Before we look at specific design

principles and solutions, Jedoch, Wir

should understand why they are impor-

tant.

DIGITAL PAYMENTS AND

FINANCIAL INCLUSION

Cash may be accepted everywhere, Aber

it’s often expensive to use, as informal

couriers and lenders charge high fees.

Trotzdem, people who don’t have a lot

of money still use cash constantly, Und

making transactions by hand is extremely

risky and time intensive for them.

For someone who has only used cash,

making payments in a formal manner

using a banking or digital payment sys-

tem—whether by check, card, or digital

transaction—is nothing short of revolu-

tionary. Time is saved. Funds are secured.

And, in the best cases, fees are reduced.

High fees have long been one of the

biggest obstacles to the world’s poor mak-

ing formal payments. With the advent of

ABOUT THE AUTHORS

Kosta Peric is Deputy Director for the Financial Services for the Poor initiative at the Bill &

Melinda Gates Foundation, where in charge of payments. Previously he was the chief archi-

tect of SWIFTNet, SWIFT’s global secure network that connects 10,000 financial institutions

and corporations in the world, and co-founder of Innotribe, SWIFT’s initiative to enable col-

laborative innovation in financial services. He is the author of The Castle And The Sandbox,

a book on how to innovate in conservative companies using open innovation.

Matt Bohan serves as a Senior Program Officer at the Bill & Melinda Gates Foundation, mit

a specific focus on the Financial Services for the Poor. Matt supports the program’s Level One

Project, where he’s working to bring mobile payment and other financial services to the two

billion people in the world who live on less than two dollars a day. Prior to working at the

Gates Foundation, Matt was Senior Director at Alvarez & Marsal.

Miller Abel is a Principal Technologist for the Financial Services for the Poor team at the Bill

& Melinda Gates Foundation. He has more than 35 years of experience in the software and

services sector, where he has held a variety of positions in both small and large systems com-

panies. Miller specializes in fast-changing Internet and mobile businesses where ambiguity

and uncertainty must be overcome by solid strategy and converted into business results. Müller

hat 30 patents issued and pending (not including foreign equivalents) in a variety of technol-

ogy areas including contactless proximity communications.

© 2018 Kosta Peric, Miller Abel, Matt Bohan

Innovationen / Volumen 12, number 1/2

71

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Kosta Peric, Miller Abel, and Matt Bohan

LEVEL ONE PROJECT PRINCIPLES

The attributes essential to making payment systems accessible to poor customers

and supportive of financial service providers include:

(cid:2)(cid:1)An open-loop system that is available to any licensed digital financial service provider

(DFSP) in the country, including banks and licensed non-banks.

(cid:2)(cid:1) Real-time and “push” payments, and payments that are irrevocable, which remove

many of the risks and costs inherent in batch-processed and “pull” payment systems.

(cid:2)(cid:1) A system that is governed by the DFSPs that use it and regulated by a government

financial authority. This well-tested model creates a feeling of fairness among partic-

Ipants.

(cid:2)(cid:1)A system that allows same-day settlement or better among participants.

(cid:2)(cid:1)A system that operates on a “not-for-loss” or “cost-recovery-plus-investment” basis.

This does not preclude DFSPs—or other service providers in the ecosystem—from

earning profits through use of the platform.

Siehe https://leveloneproject.org.

digital financial services, providers finally

have a way to reach a large number of cus-

tomers with very low overhead. Für

Beispiel, the cost of facilitating a digital

payment from mobile phone to mobile

phone is negligible, as are the fees

providers need to charge to serve their

customers profitably. Digital financial

services finally give poor customers the

speed and security of formal banking at a

price they can afford.

This has helped drive a boom in

mobile money products and providers

across the world’s emerging economies.

The first mobile money service hit the

market in 2004, and by 2016 there were

277 active services and more than half a

billion registered accounts worldwide.1. In

Uganda and other countries, mobile

money customers outnumber traditional

banking services customers.2.

Building individual financial resilien-

cy is a slow process, but mobile money

has been around long enough to have a

measurable effect on poverty. Last year,

researchers from MIT showed that

194,000 households in Kenya emerged

from extreme poverty because they had

access to the M-Pesa mobile money serv-

ice.3. Other studies have shown that digi-

tal accounts help mothers buy healthier

food for their families and help farmers

save and invest in future harvests.4.,5.

Heute, mobile money is at an inflec-

tion point. Established providers contin-

ue to thrive, but new ones have a hard

time entering the market. Person-to-per-

son payments are common among the

poor, who regularly lend and transfer

money among friends and family, Aber

other forms of payments are extremely

important as well, such as government

social disbursements and transactions

with merchants. The integration of these

kinds of payments into the mobile/digital

milieu has so far been limited.

Cash still has one remaining advan-

tage over mobile money: universality. Nicht

everyone wishes to transact with mobile

money, and parties wishing to transact

may not use the same mobile money serv-

ice. Everyone will, Jedoch, accept cash.

This gives would-be customers a persua-

sive reason to hold on to their cash and

think twice about signing up for digital

accounts.

The current point of inflection, Dann,

rests on interoperability among services.

72

Innovationen / Blockchain for Global Development

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

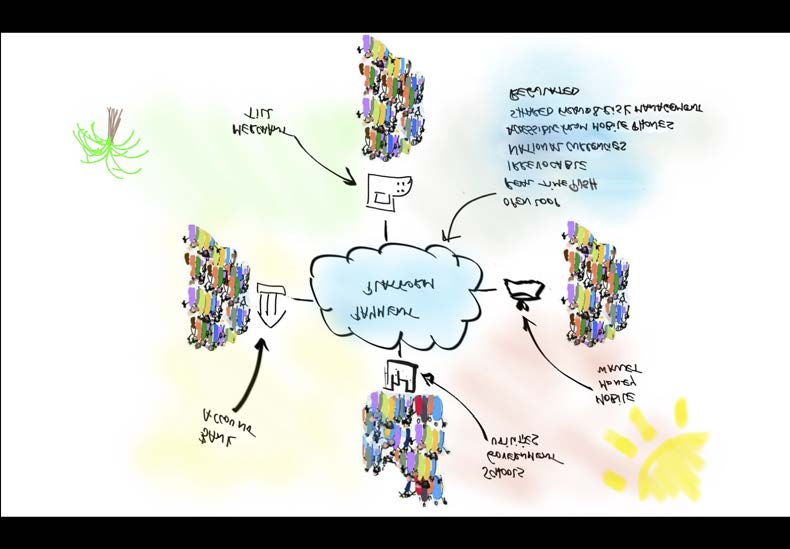

Advances in Real Time

Figur 1. Level One Project Vision and Principles

For mobile money to continue its growth

in terms of both the number of customers

the number and diversity of

Und

providers, services cannot continue to

function as closed loops, wherein sub-

scribers of one service are unable to trans-

act with subscribers of a different one. Für

customers to get the full benefits of digital

finance, they must be able to transact with

anyone, not just the random cross-section

of the population that happens to have an

account with the same provider.

Interoperability will also help extend

mobile money into merchant and bulk

payments. With interoperability, mer-

chants and employers will be able to use a

single service to issue and accept money

to and from all their customers and

employees. Without interoperability, Sie

must either choose one service, welche

excludes customers and employees using

other services, or subscribe to them all.

It’s a similar dilemma for government-to-

person payments, though on a much larg-

er scale, often millions of citizens each

month.

Endlich, interoperability based on a

shared central service will make it easier

for new providers to enter the market.

Building a customer base is something

every provider needs to do quickly in

order to achieve solvency. It’s difficult to

do when they can only offer new cus-

tomers the ability to transact with a few

hundred or thousand fellow subscribers;

most customers will prefer to sign up with

established providers who already have

sizable loops. If transactions were possible

across all services, all customers would

exist in the same loop, and new providers

could compete based on cost and features

rather than the size of their subscriber

base.

The L1P principles offer a vision for

how an interoperable payments platform

can serve the poor. Figur 1 shows this

Innovationen / Volumen 12, number 1/2

73

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Kosta Peric, Miller Abel, and Matt Bohan

vision, along with the underlying design

principles.

BUILDING L1P-ALIGNED

PLATFORMS: KEY

BARRIERS TO OVERCOME

Building an interoperable payment plat-

form on a national or regional scale is no

small feat. It requires focusing clearly on

the ultimate objectives, providing strong

governance and oversight, and having a

solid understanding of the barriers ahead.

From our experience so far, interop-

erability poses two key technological bar-

riers that projects need to overcome: Die

lack of efficient clearing and settlement of

payments across different financial serv-

ice providers, and the lack of standardiza-

tion in connecting these providers to a

common platform. The L1P principles

and reference implementation address

beide.

In terms of clearing and settlement,

L1P offers three basic principles: (1) pay-

ments should be initiated and authorized

by the payer not the payee; (2) payments

should be completed and verified in real

Zeit; Und (3) payments should be irrevo-

cable. The first principle specifies that as

with cash, an end user initiates a payment

by pushing value to the receiver; Und,

unlike direct debits or checks, money

never leaves an end user’s account with-

out direct authorization at the time of the

transaction. The second principle states

that when one person sends money to

another, the sending account is debited

and the receiving account is credited

simultaneously and immediately, ob

or not the counterparties use the same

provider. As with the first principle, this is

necessary for making digital money func-

tion similarly to cash, which will make it a

meaningful and comfortable user alterna-

tiv. The third principle states that pay-

ments are final when they are cleared;

they can’t be recalled by the person mak-

ing the payment. This is a hallmark of

cash that is essential to adoption.

Im Gegensatz, the most common exam-

ple of a pull payment is a check: Wann

processing a check, the receiver’s account

requests that money be pulled from the

account of the sender, who has pre-

approved this request by signing the

check. Checks are not cleared immediate-

ly. It often takes several days from the

time the commitment to pay is made and

when funds are credited to the receiver.

And during this time before the check is

cleared, it remains revocable because the

sender may stop payment of the check

before it clears. In this case, the request

for payment is revoked by the payer—in

other words,

the check bounces.

Darüber hinaus, because a pull payment like a

check is a request for money and is not

cleared in real time, there may not be ade-

quate funds in the payer’s account to ful-

fill the request. The sender is likely

charged a fee for pre-approving a pay-

ment that couldn’t be fulfilled.

Push payments are

irrevocable

because the sender’s provider will only

push money that is available in the

sender’s account. There is no way to cause

an overdraft. And because push payments

are cleared in real time, there is no ability

to revoke. Zusamenfassend, the payment becomes

final when it is authorized.

L1P principles prescribe these pay-

ments because they are technically sim-

pler, which makes them more affordable,

and because they are immediate. Mit

pull payments, the receiver has to wait

while the sending account verifies that the

request for money is legitimate and can be

fulfilled. With push payments, sender and

receiver get instant confirmation. Making

payments irrevocable enables them to

happen in real time. Jedoch, to achieve

real-time payments in an interoperable

System, another issue must be addressed:

the timing of transactions between

providers.

74

Innovationen / Blockchain for Global Development

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Advances in Real Time

When a user of one service sends

money to a user of another service, eins

service provider ends up in debt to the

andere. Both customers’ accounts must be

credited and debited, as must the ledgers

belonging to each provider. daher, A

payment transaction must occur at some

point between the providers.

Settlements between financial service

providers already occur within the estab-

lished banking systems in every country.

Banks in this system usually settle their

transactions with each other once every

business day. This means that all the cus-

tomer transactions for the settlement

period are tallied up and cleared at once,

in a single bulk transaction. This is anoth-

er case where customers must sometimes

wait for funds to be available, welche

results in payments that are not real time.

This can be a problem for mobile

money and other non-bank providers in

an interoperable system because they also

depend on these once-a-day deposits with

banks. To guarantee all the digital money

reflected in the accounts of their end

Benutzer, non-bank providers are required to

have an equal supply of “real” funds saved

with a bank so that, Zum Beispiel, if a

provider’s customers all decide to with-

draw their funds on the same day, Das

provider is able to give each one their full

account value in cash.

In an interoperable system, non-bank

providers need an additional reserve of

funds specifically designated to cover

cross-platform transactions. When a cus-

tomer sends money to someone who uses

a different provider and the first provider

becomes indebted to the second provider,

that debt is paid using this designated

account.

To keep pace with its users’ cross-

platform transactions, a provider will

periodically move money into its desig-

nated account. While these deposits typi-

cally settle only once per business day,

customer transactions happen much

more frequently. This means that the

amount of digital money transacted

across platforms by customers and the

amount of cash a provider has on deposit

to cover these transactions can easily fall

out of sync. In other words, if there is a

sudden surge in cross-platform transac-

tions over the course of a day, eins

provider could end up owing another

provider more than it has set aside to pay.

One solution is to make a customer

wait for cross-platform transactions to

clear. As stated earlier, obwohl, this is

unacceptable, because it fails to mimic the

performance of cash and thus fails to

meet the customer’s needs.

daher, the time window for set-

tling provider-to-provider transactions

must be reduced. In systems aligned with

L1P principles, this time window is

reduced from a full business day to hours

or even seconds. Provider ledgers are

therefore updated and kept accurate mul-

tiple times throughout the day, daher

reducing the capital requirements for

supporting interoperability.

The other key barrier we encountered

in deploying the L1P principles is the lack

of appropriate standards to connect a

financial service provider’s system to the

payment platform. Systems aligned with

these principles fall into the category of

real-time retail payments (RTRP) sys-

Systeme. Other systems—such as real-time

gross settlement systems, which cover

bank-to-bank payments that are high in

value but low in volume, and automated

clearing houses, which deal with low

value-batch

payments—traditionally

come from the banking world and tend to

be served by messaging standards, wie

ISO 20022. The RTRP space is more tech-

nologically demanding, and platforms

aligned with L1P principles tend to con-

nect a variety of providers in addition to

banks, such as mobile money providers,

microfinance

institutions, payment

aggregators, and merchant networks.

Innovationen / Volumen 12, number 1/2

75

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Kosta Peric, Miller Abel, and Matt Bohan

von

Die

Weil

technological

demands and diversity of players, ein

application programming interface (API)

design principle offers a viable solution.

APIs can accommodate the deeper and

more efficient integration required by a

high volume of transactions while placing

a relatively low development burden on

individual providers—certainly much

lower than constructing their own plat-

forms or connections.

Jedoch, there is as yet no pervasive

standard for this type of integration.

daher, one challenge to overcome in

deploying platforms aligned with L1P

principles will be to settle on an API stan-

dard that will enable easy and rapid inte-

gration of financial providers.

MOJALOOP: THE OPEN-

SOURCE REFERENCE

IMPLEMENTATION OF L1P

As efforts to deploy systems modeled on

L1P principles in actual country markets

progressed from 2013 Zu 2015, it became

apparent that the barriers described above

were slowing them down. Deployments

require expertise in designing and con-

structing payment systems—a resource

that is difficult to procure, especially in

the African and Asian countries where

L1P principles were being considered.

We realized that we needed to sup-

port these deployment efforts by provid-

ing additional guidance and examples of

plans and designs, and even of software

Code, to make sure the projects could

progress according to plan. The team then

commissioned a reference implementa-

tion for L1P, which took the form of

open-source software that embodied the

architecture and design principles of L1P

and demonstrated how to overcome the

barriers described earlier.

Publishing the reference implemen-

tation as an open-source asset was impor-

tant for a few reasons. Since its inception,

all materials and knowledge gained from

the L1P principles have been shared on

the project’s website.6. This is consistent

with the open, collaborative spirit that led

to the development of these materials,

and with the goal of enabling anyone to

use the assets and to create L1P-aligned

platforms without direct involvement

with the Gates Foundation. As open-

source software, the reference implemen-

tation remains available for adaptation

and adoption, like all previous L1P assets.

Called Mojaloop—building on the

word “moja,” which means “one” in

Swahili—the software was developed by

Ripple, Dwolla, The Software Group,

ModusBox, and Crosslake Technologies.

In October 2017, it was made available on

GitHub and on

its own website

(mojaloop.io) under the Apache 2.0

Lizenz.

Mojaloop covers many of the essen-

tial uses end users find for real-time pay-

gen: person-to-person, merchant

point-of-sale, payroll and bulk payments,

multiple accounts and users, and fraud

Überwachung. Four central components

enable these uses:

(cid:2)(cid:1) A central directory service, welche

routes each payment to the correct

service/provider in the ecosystem

(cid:2)(cid:1) A central ledger service, which tracks

transactions for compliance and settle-

ment among providers

(cid:2)(cid:1)A fraud service, which allows providers

to share transaction information to val-

idate and secure payments

(cid:2)(cid:1)A central rules service, which sets policy

across the system

Of special interest in this article is

how Mojaloop enables faster clearing and

settlements between providers. Dort

were several iterations in the architecture

and design. The first of these considered a

public blockchain. The idea was that the

clearing and settlement would occur as

transactions on the single distributed

76

Innovationen / Blockchain for Global Development

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Advances in Real Time

ledger connecting all financial service

providers in the ecosystem. The design

accommodated the actual movement of

money between providers (d.h., direct set-

tlement using central bank money),

which is clearly superior to managing set-

tlements outside the platform. The design

also could assign the job of clearing to the

distributed ledger, with settlement still

occurring on a periodic basis (using a set-

tlement bank) for the regulatory environ-

ments where this is mandated.

While it satisfied our objective of

faster settlement, this architecture pre-

sented two key drawbacks when consid-

ered in the context of a national payment

platform:

(cid:2)(cid:1)Lack of national-level data control and

confidentiality. Because it used a pub-

lic blockchain, the design would repli-

cate national payment data across the

entire Internet. This obviously conflicts

with the natural sovereignty regulators

typically require. A country-level

blockchain could have been considered

as an alternative, but this was not pur-

sued, as other more practical solutions

existieren (siehe unten).

(cid:2)(cid:1) Lower capacity for transaction vol-

ume. The design could accommodate

hundreds of transactions per second

(depending on the nature of the

blockchain used), which is impressive,

but it falls well short of the thousands

per second required for real-time retail

payment platforms.

The team thus looked for other solu-

tionen. In the end they chose to use the

Interledger protocol, along with specific

code implementing a central ledger in the

platform.

The Interledger protocol is itself an

open-source specification, invented by

Ripple and developed through a broad

collaboration under the World Wide Web

Consortium.7. The protocol enables cryp-

tographically assured ledger synchroniza-

tion. The major advantages of the proto-

col are the low level of requirements to

conform with it, and the extreme efficien-

cy and scale in processing transactions.

These aspects make it especially useful in

high-volume, low-value retail payments

systems—that is, in systems that millions

of poor customers will use to make lots

and lots of transactions in very small

amounts.

Mojaloop’s current design places a

central ledger within the payment plat-

form and uses the Interledger protocol to

synchronize the ledgers of all the financial

providers involved in a given transaction.

This securely synchronizes payment

transactions within the system. Der

design provides for immediate settlement

between providers or a separate clearing

and settlement in a separate bank at very

high transaction rates—meanwhile pre-

serving the privacy and sovereignty

requirements of the entire system.

The second barrier mentioned above

was the lack of standards for connecting

financial service provider systems with

the payment platform. The Interledger

protocol provides easy use and fertile

ground for such a standard. Daher, while

the Mojaloop platform was being

designed,

the Gates

Foundation engaged another team of

developers to work on an API.

team at

Die

The mobile money platforms of

Huawei, Ericsson, Mahindra Comviva,

and Telepin provide the majority of

mobile money operators with the key

technologies needed to meet their cus-

tomers’ needs. These four companies

agreed to collaborate on creating an API

standard for industry interoperability.

They also agreed to upgrade their prod-

ucts to meet this standard, which auto-

matically gave all their customers the

option of using it. The latest update to the

API (available at mojaloop.io.) provides a

layer of semantic interoperability and can

be deployed over the Interledger protocol.

Innovationen / Volumen 12, number 1/2

77

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023

Kosta Peric, Miller Abel, and Matt Bohan

There is potential for such ecosystems

to become common around the world,

starting in the emerging economies,

where the size of the unbanked popula-

tion and the zeal for financial innovation

are both quite high. From there these

ecosystems can blossom into regional and

even continental platforms. As they do,

Mojaloop may again be useful in solving

the new challenges that arise, such as how

to facilitate payments across borders and

currencies.

1. GSM Association. 2017. “State of the

Industry Report on Mobile Money: Decade

Edition (2006-2016).” Available at

https://www.gsma.com/mobilefordevelop-

ment/wp-

content/uploads/2017/03/GSMA_State-of-

the-Industry-Report-on-Mobile-

Money_2016-1.pdf.

2. World Bank Group. 2014. “Global Findex.”

Verfügbar um:

https://globalfindex.worldbank.org/

3. Suri, T, Jack, W. “The Long-Run Poverty

and Gender Impacts of Mobile Money.”

2016. Wissenschaft, 354: 1288-1292. Verfügbar um

http://science.sciencemag.org/content/354/63

17/1288.full.

4. Doepke, Matthias, and Michèle Tertilt.

“Does Female Empowerment Promote

für

Economic Development?” Centre

Economic Policy Research discussion paper

NEIN. 8441, Juni 2011.

5. Brune, Lasseet al. Facilitating Savings for

Landwirtschaft: Field Experimental Evidence

from Malawi. NBER working paper number

20946, Februar 2015.

6. See http://leveloneproject.org.

7. See http://Interledger.org.

As stated earlier, everything pro-

duced or enabled by L1P is available in

the public commons. While the essential

challenges are the same, every market will

have its own regulatory and technical

Umfeld. The assets aligned with L1P

principles are designed to be flexible, Und

to reflect the needs and intentions of their

adopters rather than their creators.

CONCLUSION

Numerous governmental and nongovern-

mental bodies have codified principles of

financial inclusion. These include the

Maya Declaration from the Alliance for

Financial Inclusion and the High Level

Principles for Digital Financial Inclusion

put forth by the G20. The Level One

Project principles are unique in that they

are specific. Rather than pointing to the

broad strokes necessary to make progress,

such as infrastructure and government

leadership, the L1P principles identify the

particular aspects and functions a digital

financial platform must include in order

to be inclusive.

Technology inspired by distributed

ledger technology can help resolve the

challenge of real-time settlement across

an array of diverse,

interoperabel

providers and ledgers. This is borne out in

the Mojaloop example, which applies the

Interledger protocol to achieve multilat-

eral net settlement in a digital financial

ecosystem consisting of mobile money

providers, banks, and merchant account

Inhaber.

By laying out key components, Die

L1P principles provide a valuable tool for

increasing and sustaining digital financial

inclusion. By manifesting these compo-

nen, with the help of DLT-inspired

strategies, Mojaloop and the mobile

money API make the vision of an interop-

erable ecosystem much more possible to

realize.

78

Innovationen / Blockchain for Global Development

Von http heruntergeladen://direct.mit.edu/itgg/article-pdf/12/1-2/70/705263/inov_a_00268.pdf by guest on 07 September 2023