Christine Eibs Singer

Impact Investing in Energy Enterprises:

A Three-Act Play

Innovations Case Narrative:

E+Co

En 1994, E+Co (pronounced “E and Co”) was formed to pioneer a differ-

ent approach to the global energy problem.

—Baron and Weinmann1

My colleagues and I became involved in impact investing in the early 1990s, first as

an activity of the Rockefeller Foundation, eventually continuing this work through

the launch of E+Co in 1994. Our focus on supporting clean-energy enterprises in

developing countries has presented us with an array of challenges throughout the

años, all of which stem from a core question: how can we use public (philanthrop-

ic or government) funds to create “envelopes of investment” for the private sector

that will have an impact on the environment (such as slowing climate change), y

on development (such as access to a modern energy supply)?

By some measures, we have succeeded. Eight million people have access to a

modern energy source as a result of E+Co’s investments in two hundred enterpris-

es. US$280 million of new capital has been mobilized, and five million tons of car- bon have been offset. “Energy through enterprise” and “energy poverty” are now well-known terms, and the connection between energy and climate change—and the implications for development—is firmly established. We have a community of current and former E+Co staff who have demonstrated a great commitment to the design and implementation of energy through enterprise—without them we would not have reached our level of success nor had such a great impact.2 But we have just scratched the surface. The world’s energy consumption will rise by 59 percent between 1999 y 2020 a 607 quadrillion BTUs. Most of the growth will occur in the rapidly developing parts of the world.3 Energy poverty— Christine Eibs Singer, Cofounder and CEO of E+Co, is a frequent contributor to the social capital markets debate, regularly presenting lessons learned from E+Co’s 17 years of experience in clean energy enterprise development and investment in the developing world. En 2011 she was awarded the Keystone Leadership Award for the Environment, as well as an Honorary Doctorate of Humane Letters from NJ City University. © 2011 Christine Eibs Singer innovations / volumen 6, number 3 55 Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Christine Eibs Singer people worldwide who lack access to electricity or other modern energy—is extremely large and continues to grow, and climate change is and will remain a major issue. The chances of improving other problems that are linked to the avail- ability of clean-energy access—lung disease, child mortality, education, and so on—remain dismal. So while we have moved one step toward scale and impact, the size and understanding of the problem has grown. As E+Co evolves to address this problem, this article reflects back on our experience that has informed and led us to our way forward. Rockefeller Foundation Incubation PRELUDE E+Co began as a program within the Rockefeller Foundation, which in the early 1990s was looking for high-impact innovations to address environmental issues. Peter Goldmark and Kenneth Prewitt, the foundation’s president and vice presi- mella, conceived and led a “Global Bargains” program initiative that was based on the thesis that private capital providers from the global north would be willing to generate environmental benefits in the global south. In their search, they veered from the foundation’s historically science-based development approach, which pointed to traditional solutions, and instead asked a small group with different experience and expertise—in this case, economic development led by the public sector—to examine the problem and the possibilities. Phil LaRocco and I brought more than 30 years of that experience with us from a large public authority with a track record of infrastructure development, pur- chasing contracts, and long-term financing with public funds.4 Such long-term financing led to subsequent commercial investments by shipping companies, aire- líneas, manufacturers, and service firms, which then repaid the initial public invest- ments through leases, loans, and revenue sharing. The Global Bargains idea was to use public capital to create envelopes of investment for private capital, the aim being to have an impact on economic development and produce financial returns—in short, to bring the Port Authority model to bear on the problems of energy poverty and climate change. Four Core Statements Our initial thinking within the Rockefeller Foundation, which later translated into the thesis that launched and still underpins E+Co, can be summarized in four statements that would become conventional wisdom a decade later: • If you care about the global environment, you need to care about energy. • If you care about energy, then you have to care about developing countries because of the forecasted growth in energy consumption in these markets. • If you care about economic development and quality of life improvements in developing countries (which were the core of the Rockefeller Foundation’s strategy then and now), you need to focus on energy. 56 innovaciones / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Impact Investing in Energy Enterprises: A Three-Act Play • If you care about energy in developing countries, you need to focus on private- sector initiatives because there is insufficient public capital available to meet the forecasts by the World Bank on the levels of energy poverty. In terms of strategic planning and value proposition, what we have learned is that energy drives environmental and economic change. Energía, a necessary but not sufficient element of development, was beyond the scope of business as usual and development as usual. In more optimistic terms, we realized that both a large market—energy serv- ices for those unserved and poorly served—and a large untapped resource—local entrepreneurs—existed. And while the environmental movement was in full throt- tle at the time, its focus was more on lobbying against this or that cause, often with the mantra of “think globally, act locally.” We too found value in the global-local focus, but latched on to two of its elements in particular. Primero, to act locally, local resources are needed. Segundo, under the prevailing development paradigm, previo- ities and plans were being made anywhere but locally—national capitals, regional organization headquarters, and institutions in Washington, CORRIENTE CONTINUA., were “the deciders.” We also noted the role small businesses play in driving economic growth in the industrialized world, and the sector’s virtual absence in models used in developing countries. What emerged from these ideas was a working hypothesis: public funds could prepare local enterprises to deliver life-enhancing energy services to a grow- ing unserved population, eventually leading to commercial investments or what we characterized as a “third way”—the public-private funded, or hybrid, model of investing. Not Exactly Mainstream These views could hardly be considered mainstream at the time, 1994. That year marked the heavily hyped Rio Climate Summit and the rollout of the Global Environment Facility (GEF), which is comanaged by the World Bank-United Nations Development Program-United Nations Environment Program. Big push- es from the top down were not just the prevailing strategies, they were the only strategies. Trying to squeeze even a minor request for resources for bottom-up business development into the conversation elicited a patronizing dismissal from most institutions. Fortunately, Peter Goldmark and Kenneth Prewitt saw the value in experimen- tation and diversification. As this was long before the Millennium Development Goals and well before conversations included terms such as “blended value,” “impact investing,” “scale” (now used as a verb meaning something other than climbing a mountain), “public-private partnerships,” and “triple bottom line,” there was a lot of explaining to be done and a lot of pushback. It was a lonely time. innovaciones / volumen 6, number 3 57 Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Christine Eibs Singer ACT ONE: 1994-2000 Services Plus Seed Capital Plus Handoff Our thesis reflected our belief that a combination of technical assistance (what we called enterprise development services, or EDS) and early stage, patient capital would set the stage for energy enterprises to first prove their worth, and then go on to attract later-stage growth capital from third parties. While our public authority experience and the track record of venture capital showed this strategy to be a well- established model in other sectors, in the development arena we were one of the first entities to combine the two under one services-delivery model. E+Co’s EDS encompasses a variety of activities, including business plan development, market assessment, and accounting and financial modeling. Ultimately what we learned was that the public sector wanted to build capaci- ty and the private sector wanted investment-ready opportunities. The question remained how to link the two. For the public sector, which in this case meant most- ly capacity-building and training entities, our pitch emphasized that delivering business-planning services without capital was akin to job training for nonexistent jobs. For private-sector players, we didn’t stress the capacity-building or the need for the core idea to be supplemented by outside expertise (a nosotros). We realized instead that this extensive hand-holding was an excellent risk-mitigation tactic that would offset the inexperience of local entrepreneurs. Investors understood and valued this form of risk mitigation. A few organizations understood our integration of both products; the Multilateral Investment Fund of the Inter-American Development Bank (Don Terry and Sandra Darville) and the United Nations Foundation (Tim Wirth and Gary Nakarado) were two early stakeholders that pro- vided catalytic funding for both EDS and investment. Al mismo tiempo, USAID launched a program that focused on the enterprise development aspects of renewable energy finance. FENERCA,5 a multiyear, multi- country program, was the archetype of our thesis that public capital could set the stage for investment and impact. In partnership with José María Blanco of the Biomass Users Network–Central America (BUN-CA), our implementation of FENERCA produced 62 business plans, mobilized US$36 million of investor cap-

ital, and launched the $17 million Central American Renewable Energy and Cleaner Production Facility in Central America. Something Borrowed, Something Blue Although there were lots of variables to manage in proving this hypothesis, we knew that little of it was truly original and that we were borrowing parts of what had worked well in the past. Our idea simply reflected a merging of different sec- tores. (My colleague Phil LaRocco likes to say our approach was “as original as dirt.”) From the venture capital world, we borrowed an emphasis on the entrepreneur and the team, and the notion that more hands-on activities are worth the cost. From the public finance world (our Port Authority roots), we took the blending of 58 innovaciones / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Impact Investing in Energy Enterprises: A Three-Act Play public good with private enterprise, and the idea of using public finance to fill early stage capital gaps. From the project finance and corporate finance worlds, we took the importance of underlying fundamentals and cash flow, adopting the phi- losophy that getting paid predictably was superior to getting paid a large return “someday.” We even borrowed from the nascent microfinance sector to reduce the emphasis on track record and collateral. Long before the term “mash-up” existed, we had a mash-up, hybrid business model. Entrepreneurs and Local Grounding Something else borrowed (from Business 101) was an emphasis on the local deliv- ery of goods and services. El critico, essential relationship was, and is, between the energy enterprise and its customer, whether that customer is a household, a business, or a national utility.6 The enterprise is the multiplier in our equation: a single enterprise, properly prepared and financed, can readily touch 5,000 cus- Tomeros. Whether a sole proprietorship or the end of a complex, multiheaded value chain rooted in China or the U.S. or Europe or Japan, “doorstep delivery” is the glue that binds together all the other variables.7 While organizations like E+Co might play the next multiplier role—one intermediary touching 200 enterprises reaches 1.6 million customers and benefits eight million people—the sustainabili- ty of this approach, and therefore its growth, is dependent on the strength and nature of the enterprise-customer connection. Enterprises, not Projects Our thesis required solid project fundamentals, but we knew at the outset that projects, while more easily financed and copied, would be growth inhibiting and would have less of an impact than a focus on enterprises. We also struggled with funders who understood projects as having a beginning and an end and a tidy final report. It was challenging for some funders to structure engagements that planned to continue, hopefully for years, beyond the funding cycle. Desafortunadamente, it remains so today. Along with our emphasis on portfolios rather than transactions, this has been one of the hardest mountains to scale (pun intended). During the first several years of E+Co’s operations, the general consensus about venture capital was that it only applied to technology companies. Everything else, mientras tanto, was viewed within the framework of a project-finance debt model. We had to describe how the project-finance model could be applied to startups. Former E+Co board chair Nick Parker described what we were doing as “ven- ture debt.” Our ability to do this required not just enormous faith in our underly- ing assumptions but hands-on knowledge of the market—we had to be close to our customer and their culture of business. This critical need directed the decen- tralization of our operations into the markets where we were investing. How else could we learn but by doing and building credibility? Our decentralization was an organic process driven by several factors. We conducted research on where we innovations / volumen 6, number 3 59 Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Christine Eibs Singer could find the investment opportunities and talent, and assessed the markets where our portfolios were growing in order to deepen our impact in those markets and bring some efficiency to our operations. We also analyzed the value chains of the sectors we were supporting to improve access to products/supplies for our portfolio companies and/or support end-user finance. Sin embargo, we were also inevitably guided down the paths where our donor funds led us. We began by establishing our first regional office in San Jose, Costa Rica, en 1995, which was soon followed by offices in Zimbabwe and Nepal. We then expanded to South Africa, Brasil, Ghana, Porcelana, and Tanzania. We eventually relocated our Asia regional office to Thailand. Portfolios, not Transactions While the focus on open-ended enterprises and businesses pointed in a clear direc- ción, it also posed a significant problem: picking winners that satisfied our inter- linked criteria—financial sustainability, environmental benefits, and social impact. The solution—again, not a very mainstream thought at the time or even today— was to focus on heterogeneous enterprises and markets, and on the portfolio effect at the benefits level. This is another portfolio lesson learned in our Port Authority days, when the investments and revenues of profit centers like the John F. Kennedy Airport and the World Trade Center offset the losses of the PATH transit system and industrial parks. We learned rather early on that certain enterprises and technologies—lighting for example—produced easily defined and substantial social benefits: job creation, educational opportunity, and improved health. Other applications, such as con- verting waste to gas to produce heat, have enormous and readily quantifiable envi- ronmental benefits—elimination of liquid waste, cutting greenhouse gases—but they were often technology heavy and light on jobs and social benefit. De este modo, organ- izing a portfolio of projects by placing a learning challenge on E+Co’s growing staff became the obvious solution. In those early days we were often advised to focus on narrow markets and tech- nológico. While doing so seemed logical, we weren’t sure where success and inno- vation would occur. What model or research activity would highlight the cutting- edge solar payment work being done by Rich Hansen in rural parts of the Dominican Republic? While it probably seemed “scatterized”—a Peter Goldmark term—we needed to chase what was happening, not wait for a model that predict- ed what would happen where. Tecnosol. Recall our thesis: services plus seed capital lead to handoff to third parties. Let’s visit an early case that proved our thesis was at least two-thirds cor- recto. Tecnosol is a solar energy retail company started in 1998 in Nicaragua, dónde 45 percent of the population lacks basic energy services. Founder Vladimir Delagneau, an electrical engineer, built a steady reputation for quality by selling systems and accessories primarily for cash, then installing the systems and stand- 60 innovaciones / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Impact Investing in Energy Enterprises: A Three-Act Play ing behind his products. Tecnosol had all the elements of a business that could grow, but it lacked a lending track record and access to credit. After more than a year of working with Vladimir on his market assessment and business plan, E+Co provided a $100,000 loan to this company that at the time had

sold only a few hundred solar home systems. E+Co has been engaged with the

company since 2001, advising it on aspects of business that include inventory con-

trols and growth planning. E+Co also helped Tecnosol grow to the point where it

was able to repay its loan on time and meet its clearly articulated business goals.

From our perspective, the support services plus working capital loan had

enabled Vladimir and Tecnosol to put in place formal business practices and the

beginning of a network to cover rural Nicaragua. Encima 90 percent of the people in

Tecnosol’s market territory were without modern energy, y 60 percent of those

surveyed were interested in what was a demonstrably affordable product. Ahora, todo

that was needed to validate our thesis was for local or regional financial institu-

tions to step in and fund Tecnosol’s scale-up plan—in other words, to move the

company into the mainstream.

In the interest of making a long and often replicated story short, this local or

regional financial institution was not to be found. Our thesis was naïve; in a telling

example of what we would experience worldwide, early stage success did not open

doors for growth financing. Even if there were interested funds or specialized pro-

gramos, they had their own opinions about the conditions under which an invest-

ment was appropriate; none embraced the philosophical or investment criteria we

had followed to achieve early success. One-third of our thesis was simply wrong.

When we tried to probe why larger investors were hesitant, we were bombard-

ed with what in hindsight we realize was a litany of platitudes, most of which had

been disproved in the marketplace by pioneers such as Vladimir, Rich Hansen,8

and Harish Hande. These included the small size of the transactions, the cus-

tomers’ poverty, the weakness of the market, the macro-economic conditions of

the country and region, the newness of the technologies, y, most of all, the lack

of a track record and collateral.

Numerous well-meaning efforts floundered because the line between the pub-

lic sector and the private sector became a mountain range, despite the evidence

that this approach had well more than a 100-year history in public authorities. El

well-intentioned efforts of a number of U.S. foundations, the World Bank, y el

International Finance Corporation (IFC), which began at a July 1996 retreat in

Leesburg, Virginia, led to the creation of the Solar Development Group, an effort

that concluded in 2004, which is just one example of this stressful and unsuccess-

ful journey. Most disheartening were the repeated mistakes of programs and

investors who tried to pick individual “winners” rather than assembling portfolios,

and the dismissal of what we were doing by one well-placed former manager at the

IFC as “just” character investing.

innovaciones / volumen 6, number 3

61

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Christine Eibs Singer

ACT TWO: 2000-2009

Incorporating Growth Capital, or “Abandoning 1, 2, and Beg”9

Faced with a strategy that we felt created small, successful enterprises but could

also inhibit their ultimate growth and therefore their impact—not to mention

their ability to repay E+Co’s investment—choices had to be made. These included

sourcing larger amounts of funding, making larger commitments to individual

enterprises, learning how to document nonfinancial returns, and possibly walking

away from our underwriting criteria that allowed for untried entrepreneurs in new

markets (for some, a logical consequence of thinking bigger).

We had spent an inordinate amount of time trying to solicit third-party capi-

tal and had not succeeded; acknowledging the error of a core thesis is not the eas-

iest thing for management to do. But the disconnect of one too many last-minute

changes of mind by next-stage investors and the failure of a number of large-tick-

et items told us it was time to change. There was going to be no easy road to fund-

ing the soft and the hard costs, seed and growth capital.

We adopted a strategy of seeking low-cost debt or performance-based capital

and donor funding that matched the requirements of our core business develop-

ment services. It was at this point that it hit us: if we were going to be seeking

below-market debt, we had better be able to tell our investors what was happening

as a result of investing in local energy enterprises. Even while the term “blended

value” was making the rounds, we determined that there was no real way or stan-

dard by which to organize impact information. One of our founding staff, Gina

Rodolico, took it upon herself to invent our own “triple bottom line” reporting sys-

tema. It became our guiding principle to count everything, as we just didn’t know

what was important to whom. As you can imagine, and as has now become pretty

generally accepted, this is an expensive proposition that few donors or investors are

willing to pay for. Fortunately, the Citi Foundation was embracing enterprise

development and wanted to understand what the impact was of working with local

negocios, thus they became an early supporter of these impact indicator efforts.

We also took some baby steps with the IFC to polish our experience and cre-

dentials in managing institutional funds. When a large-scale, multiparty fund

failed, we were positioned to pick up part of the transaction and were able to con-

clude an agreement with the IFC to establish the Sustainable Energy Facility (SEF),

un $18 million facility for EDS and seed and growth capital. SEF would turn out to be pivotal in our ability to prove the concept of the energy enterprise investment model. Let’s return to Tecnosol and Vladimir. Tecnosol, now with 10 branch offices, had repaid its initial $100,000 loan, and in 2004 we provided it with a growth

investment of $200,000. With the closing of SEF we had increased liquidity, and in 2007 we disbursed a $1 million loan to Vladimir, allowing him to expand further,

diversify his product line, and deepen his market. Following through on its busi-

ness goals, Tecnosol closed a $1.3 million private equity investment in 2009. E+Co followed this by making a fourth loan to the company of $1 million in 2010, y

62

innovaciones / Impact Investing

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Impact Investing in Energy Enterprises: A Three-Act Play

by the end of the year, Tecnosol had launched its first international efforts in El

Salvador and Panama, with plans to expand into Honduras and Guatemala in

2011-2012. E+Co’s serial investment enabled Tecnosol to reach more than 30,000

Nicaraguan households with clean energy, offset more than two million gallons of

kerosene, and displace close to 64,000 tons of carbon dioxide. Moving forward,

Tecnosol plans to install up to 8,000 systems a year that will provide clean energy

access to approximately 30,000 people annually.

“But you are so expensive . . ."

Integrating local service delivery alongside investment was hard for many funders

to comprehend. Many asked us, “Why do you need grant funding when you are

borrowing money? Aren’t I just subsidizing someone else’s return?” It apparently

was easier for donors to fund separate technical assistance or EDS entities than to

see what our experience was showing: the efficient integration of services plus cap-

ital. We had a hard time making the case that having both under one umbrella

actually was representing the true cost of the investment.

If the EDS was required, but not from the same checkbook, someone still had

to pay for it—we were very transparent. Experience—by then we had made more

than 100 investments—showed us that there was an initial cost of about 30 por ciento

to launch a series of investments in a company such as Tecnosol. What that meant

was that even with a nominal 8 por ciento a 12 percent return at the enterprise level,

the real net return (after losses, direct expenses, and general and administrative

costos) was about 3-4 por ciento. Given the capital requirements of the space, especial-

ly the length of time it took some enterprises to mature, we—silly us!—thought

this was pretty good, especially when we layered in the number of people served

and the reduction in carbon emissions.

En ese tiempo, our five-year business plan set forth a need for $100 million of 4 percent capital and $20 millones en subvenciones. Even before the impact investing focus,

we thought that such capital was in the market and would eagerly seek out an

investment model that combined financial returns with a social and environmen-

tal impact. We created a standardized private offering memorandum for our

“People and Planet” note to attract this capital.

What followed was a stunning revelation: investors would talk the talk of sin-

gle-digit financial returns with robust triple bottom lines and they would applaud

the discipline required in such a model, but the pool of interested dollars was small

and attention was shifting. Without a platform on which to market our People and

Planet note, we were not able sell a sufficient volume of notes to capitalize our

investment budget. We turned our attention back to the development finance

institutions.

By now we were students of this space (whatever its nom de jour). We may not

have been the first to refer to the “missing middle,” but we definitely personified it

and built the metaphor out as follows.

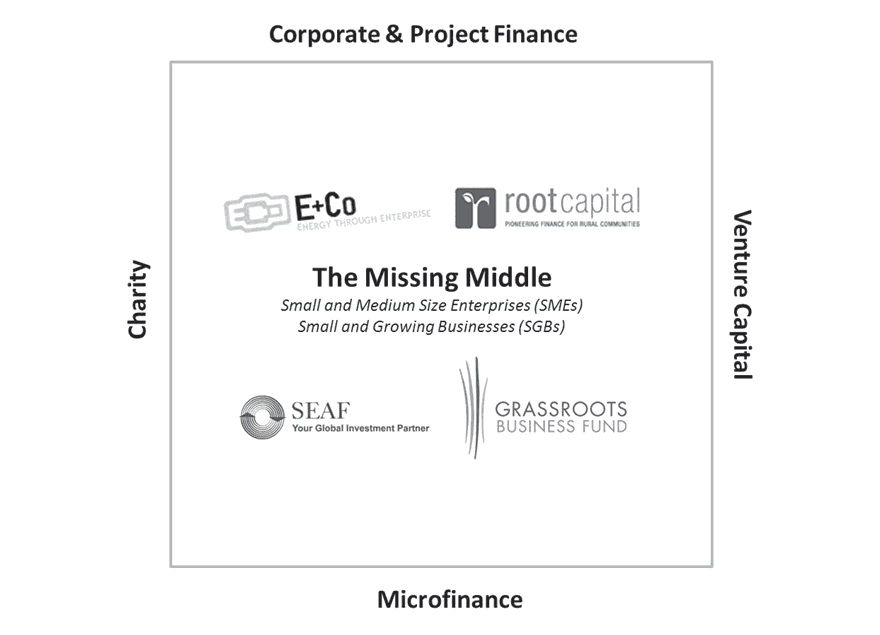

• Imagine a two-dimensional drawing of a box

innovaciones / volumen 6, number 3

63

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Christine Eibs Singer

Cifra 1. Defining the Space

• For the top line, insert “Corporate and Project Finance”

• At the bottom, insert “Microfinance”

• Label the right side “Venture Capital”

• Label the left side “Charity”

• The empty area described by these four lines delineates the space where E+Co

and other intermediaries work (See Figure 1 above.)

This empty space has been given numerous names over the last two decades,

but it has never achieved a real identity or become an asset class. Tal como, it does

not have its own rules. It always needs to beg or steal from other disciplines (el

four sides). This makes it unpredictable, which makes life in this space very untidy

for organizations that borrow or manage money and then invest it. What began as

a conversation in 2004 at a Socially Responsible Investment in the Rockies confab

with David Wood, who at the time was with the Institute for Responsible

Investment at Boston College, about the opportunity to organize this “space” as an

asset class similar to microfinance has now evolved into the near-sector status

called small and growing businesses—contributing to the related launch of the

Aspen Network of Development Entrepreneurs, of which I am a cofounder and

serve on the executive committee.10

64

innovaciones / Impact Investing

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Impact Investing in Energy Enterprises: A Three-Act Play

Innovation versus Bankable

When we added growth capital to our product line, we realized that there was a

natural conflict between the new, the exciting, and the innovative on the one hand,

and that which could secure predictable cash flow or be considered commercial on

the other. Donors and foundations want the breakthrough. Lenders and investors

want the predictable. Everyone tends to speak of “their” focus and exhibit discom-

fort with the focus of others. “Innovation” is a word with so many varied meanings

that it is as vague and subjective today as its for-profit counterpart, “commercial.”

We would ask, “Isn’t something being done for the first time in a new market

that is capable of producing a steady 3 percent return both innovative and com-

mercial?” The answer was rarely even a “maybe” on both counts. If it is commer-

cial, we are told, it should produce higher returns; if it works and is considered

comercial, it is not innovative. In conversations with stakeholders seeking to

increase their investment in energy and development, we found ourselves asking

for the creation of a “fund for things that work” as they sought to establish the next

new thing.

Next New Thing versus What Works

There is a subcategory of this innovation versus commercial problem within the

donor community itself. Donors tend to take the early success of an intervention

as a sign that the problem has been solved (“All that’s required is a few decades of

implementation”). This hits specialist intermediaries especially hard, such as

E+Co, ROOT Capital, and the Small Enterprise Assistance Fund, which have built

a niche but need to keep growing in order to be sustainable. Even what works con-

sistently faces a challenge that is captured by two simple words: working capital.

Events do not roll out evenly. While predictable rates of return exist, the tim-

ing of those returns is in the hands of numerous exogenous as well as controllable

factores. I have often said that E+Co faces the same challenge as our enterprises—

we need up-front working capital that will allow us to implement our business

plan. For a nonprofit organization, this is where the decreasing numbers of core

funders hits hard. Donors want specific projects and activities and will only rarely

support organizational growth and development. So, until the social capital mar-

kets are no longer broken, or until business as usual reflects a value chain that has

smoothly connected the dots, these specialized intermediaries are necessary to

bridge the gap and do the dot connecting. Specialized knowledge and experience

can produce a desired impact at a reasonable cost.

Do a Fund

The fascination with closed-ended funds grows and shrinks predictably. It is on the

rise again as our markets appear ready for equity capital. Such funds alone have the

potential to grow a slice of a market to enhance part of the growth process for the

space and sector. Sin embargo, such funds are overemphasized as being The Answer

cuando, like many things, they are simply part of an answer. There are two weak ele-

innovaciones / volumen 6, number 3

65

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Christine Eibs Singer

ments in the argument that funds are the answer. Primero, despite discussion to the

contrary, funds have yet to integrate the searching and nurturing and experimen-

tation needed to create investment-ready enterprises.11 Thus the “fund” universe

has a limited impact as a magnet to the sector.

Segundo, to date, E+Co’s mission is to empower entrepreneurs, the vehicle

through which energy access is delivered. This differs from traditional funds whose

mission is to maximize financial returns to investors. Enterprises (deal flow) y

investors (capital providers) are critical to both. In the case of the latter, sin embargo,

“exit” is the most important four-letter word in the fund vocabulary. This creates

real conflict between the objective of cash flow versus sector and enterprise

growth, the goal of return on investment versus the goal of energy through enter-

prise. Act three of E+Co finds us firmly immersed in managing this conflict.

ACT THREE. 2010 AND BEYOND…

ENERGY FOR DEVELOPMENT: √

ENERGY AND CLIMATE CHANGE: √

SMALL AND GROWING BUSINESSES: √

HYBRID INVESTMENT MODELS: ??

So here we are. Having worked in and studied the field for two decades, learned a

broad set of skills, and carried out what we believe is a value-added toolkit of serv-

ice and capital, plus a serial investment and portfolio impact approach that works,

we find ourselves at a crossroads. What informs us about the direction we should

llevar?

The importance of energy access remains undiminished. The Millennium

Development Goals are de facto unachievable without energy access; business as

usual has little to report about progress toward a significant increase in energy

access by 2035, and that was before the population forecasts were recently revised

upward . . .Hay 1.5 a 2.5 billion poor people in the world who lack electric-

idad, are cooking with dirty, dangerous fuel, and are unable to afford modern sub-

stitutes, and this number will likely be the same or even larger in 2035. Business as

usual has no tricks up its sleeve to bend that curve. Pequeño, empowered local entre-

preneurs, alone or as a part of networks, larger corporations, or multinational cor-

porations, are an enormous but largely untapped and profitable resource.

Por lo tanto, we will stay true to our mission of seeking access to cleaner affordable

energy through local, market-based enterprises.

A balancing act is needed. With the lack of acceptance of the “missing middle”

as an investment category, entities such as E+Co must blend the commercial with

the catalytic and capitalize on specialized knowledge. Por qué? Because the aggrega-

tion of large amounts of single-digit return on investment capital seems unattain-

capaz, even as the lure of impact investing takes off. We again need to acknowledge

the error of a core thesis. The “all in one pot” message has not gained traction,

despite the recognition that business development and technical assistance are

necessary to produce the very pipeline that impact investors claim is a barrier to

66

innovaciones / Impact Investing

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Impact Investing in Energy Enterprises: A Three-Act Play

investing. We know that our model of investing in energy enterprises must increase

by an order of magnitude if we are to achieve the desired energy access. Thus we

are now facing the more difficult task of disaggregating services and capital and

reaggregating in separate units, which requires an enormous amount of time. I am

optimistic that this decoupling of enterprise development from investment and

the resulting clarification of E+Co’s message will resonate with donor and govern-

ment entities as being unapologetically philanthropic.

The opportunity to commercialize clean energy in developing countries is

immense, and currently largely unmet. While access to energy is now the dominant

global call to action for E+Co, the demand for our investment remains as strong as

ever from the climate change side. It is now known and accepted that the global

energy system is the most significant contributor to climate change, representing

aproximadamente 60 percent of total greenhouse gas emissions.12 The growth of clean

energy technologies in the developing world is one immediate response to the

urgent need to reduce the global energy system’s carbon intensity. El

International Energy Agency projects that $756 billion of additional financing, o $36 billion a year, is needed to achieve universal energy access by 2030.13 Mientras que la

need is immense, the current investments in the space are meager—only approxi-

mately $10 billion in developing countries.14 There is a growing recognition that the capacity to commercialize clean ener- gy needs to be developed locally, and that increasing access to energy often requires decentralized and off-grid solutions, both of which fall within the range of small and growing businesses. Además, larger investors such as traditional private equity funds see constraints in the number of large clean energy deals available, putting further attention on those that target this market niche. Obviamente, this is where E+Co has operated for the last 17 años, and it will remain the target of our future enterprise development and investment activities. De hecho, our first entry into private equity fund development will be focused on this market niche in Southeast Asia. It’s still about the entrepreneur and still local. We must incorporate the supply lines of energy products and other sources of capital, but the enterprise-customer framework is still key.15 While focusing on the eight factors within this framework will not guarantee success, failing to focus on them will likely spell disaster. Focusing on these factors within a traditional fund structure is a challenge, but one that must be tackled through an integrated strategy of services, or what the ven- ture capital industry calls “smart money,” plus capital: Customer Side: Demand + Knowledge + Services + Finance Enterprise Side: Tecnología + Entrepreneur + Services + Capital Innovation remains key. There is enormous room for continued innovation in the energy-for-development space. This is not primarily in the energy gadgets themselves or the production of better stoves, cheaper lights, etcétera. Affordable and accessible technology solutions already exist in emerging markets, so the ener- gy poor don’t need to wait for these. It is mechanisms for end-user finance and innovations / volumen 6, number 3 67 Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Christine Eibs Singer entrepreneur empowerment that sit on the doorstep of innovation. We perceive that the key innovations will occur in mobile payment systems that make products more affordable, and in capacity-building that prepares more entrepreneurs to accept capital and roll out sustainable businesses. The Success Versus Scale Conundrum E+Co will continue to prove our thesis that scale can be achieved through innova- tion and replication. Our work with Harish Hande and the SELCO India team on replicating their success through local energy enterprise development is indicative of this path forward. Our portfolio approach has allowed us to show that replica- tion and the expansion of what is working is innovation. We will continue to make the voice of what works equal to the voice of the next new thing. We believe this is an essential message for the broadly defined impact investment community to hear. To build on success and scale, we will continue our portfolio approach and will seed multiple businesses, rather than picking scalable winners on Day 1. Por qué? The track record of picking winners is poor, and exogenous events trump business plans every time. There are many routes to scale and impact; replicating success along a value chain of clean energy distribution channels in a country can be game changing and can meet the scale test. We need to keep all of these routes robust. For E+Co, three different organizational priorities have emerged. Primero, we must continue to prove the energy enterprise model and the triple bottom line impact it delivers through the strong performance of our portfolio of more than 135 active companies. We have $35-plus million of debt placed in these companies

that we are obligated to repay. The money we now have invested is not philanthro-

py but impact-oriented capital from development finance institutions (70 por ciento)

and from foundations and social investors (30 por ciento). Hasta la fecha, the financial per-

formance of our portfolio is strong: we’ve repaid $12.5 million to lenders through December 2010. At the time of this article’s writing, we are restructuring and establishing a portfolio management unit that will focus exclusively on the triple bottom line performance of these assets, thereby assisting these companies with growth and follow-on investment, from E+Co’s new investment vehicles and from others. We will drill down into this portfolio, evaluating patterns of performance among energy enterprises and extracting lessons learned, and offer structuring and operational benefits to existing and new investment opportunities. Segundo, we will evolve our investment activity out of the nonprofit structure to commercial platforms and embrace specialized funds and investment vehicles, but the investment strategy will reflect our experience of integrating services with seed and growth capital. Depending on the market, these funds will satisfy the appetite of those commercial investors leading with double-digit returns. Our investment experience in Asia accomplishes this. In other markets, the requisite blending of return and risk profiles will be necessary—in Africa, Por ejemplo. As we do this, we will present our lessons learned and the market realities to a funder 68 innovaciones / Impact Investing Downloaded from http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023 Impact Investing in Energy Enterprises: A Three-Act Play pool that right now is quite comfortable with the “8 and 20, double-digit return, plain vanilla” checklist (nota: I did not state the standard 2 percent management fee in that formula, so of course we will have months of negotiations around this). We will stay on the fundraising treadmill and hope for a day when the missing middle is supplied adequately with appropriate capital. While time-consuming and frustrating, it will also be necessary until the private sector’s reluctance to place large amounts of capital into this energy-access investment arena is behind us. Our third priority is to tackle E+Co’s two decades of learning and focus on innovations for energy access. Específicamente, we will combine technology advances of the last 10 years—in mobile technology, in distance learning, and in Internet col- laboration—with our energy enterprise development knowledge to create a sys- tematized process to grow an enterprise pipeline of hundreds, then thousands, of bankable enterprises each year. True to our antipathy for job training without a job, we plan to connect this energy through enterprise learning platform to the universe of financial providers and product suppliers and innovators, fine-tuning the service-plus-capital equation. This is our response to the size of the problem, and the need, and the demands of the impact investing community that there be a big enough pipeline of bankable deals to put their money to work. You’ve been heard; now you must support the efforts necessary to create that pipeline. We all must move past a time of accepting a world where one-third of the people are liv- ing in homes filled with cooking smoke, and then left staring at the darkness in the night. Let’s hope that the grand finale of this play called E+Co is universal energy access being delivered by tens of thousands energy entrepreneurs. Now that’s impact investing. 1 En 2003-2004, two University of Michigan graduate students, Scott Baron and George Weinmann, prepared a profile of E+Co and the landscape of energy poverty in the form of a case study pub- lished in the late C. k. Prahalad’s Fortune at the Bottom of the Pyramid. This profile is rich in back- ground and what were then “forward looking statements” and quotes. C. k. Prahalad, The Fortune at the Bottom of the Pyramid (Upper Saddle River, Nueva Jersey: Wharton School Publishing, 2010), pag. 358. 2. International accolades, such as the Ashden Awards for Sustainable Energy and the Schwab Social Entrepreneur of the Year, are more and more often recognizing as game changers companies that address energy poverty through market-based approaches—including, to our delight, some of E+Co’s portfolio companies. E+Co was also honored as the Financial Times Sustainable Investor of the Year in 2008 and runner-up in 2009. In January 2011, E+Co was runner-up for the Zayed Future Energy Prize, which recognizes vision, leadership, and outstanding work in renewable energy and sustainability. 3. Via study detailed in endnote 1. 4. Phil LaRocco was director of World Trade and Economic Development, and I was manager of the World Trade Institute for the Port Authority of New York and New Jersey. 5. The Increased Use of Renewable Energy Resources Program, known as FENERCA—the Spanish acronym for Financiamiento de Empresas de Energía Renovable en Centro America—was a US$5.3 million, five-year USAID Leader with Associates Cooperative Agreement that was award-

ed to E+Co and initiated in April 2000. FENERCA’s objective was to promote the development of

renewable energy enterprises and projects, while increasing the capacity of financial institutions,

innovaciones / volumen 6, number 3

69

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023

Christine Eibs Singer

empresarios, and NGOs to support the advancement of the region’s renewable energy sector.

6. The definition of an enterprise includes rural energy service companies or project developers; para

ejemplo, a company building a hydroelectric project powered by the “run of the river” rather than

through dam construction and selling its kWh to the grid.

7. Coined by Dr. Harish Hande, cofounder and managing director of SELCO India and a member

of E+Co’s board of directors. Having established a company that is dedicated to servicing the

energy needs of the poor through financial innovations, Harish and the SELCO team lead by

ejemplo, generously sharing their experiences and lessons “open source” with all who inquire.

Harish is the recipient of the Ashden Award for Sustainable Energy and its Outstanding

Achievement Award; en 2008, he was named one of the 50 pioneers for change in India by India

Hoy. I am a director on the SELCO board.

8. Richard Hansen, the founder and CEO of Soluz, Cª, is one of the earliest pioneers in the imple-

mentation of a market-based approach to solar photovoltaics for rural electrification. We began

working with Rich, John Rogers, and Steve Cunningham (who later joined E+Co’s investment

staff, becoming CFO in 2005) en 1993 through a “recyclable grant” from the Rockefeller

Foundation for the launch of a photovoltaic company in the Dominican Republic.

9. 1=Services, 2=Seed Capital, and Beg was what we felt like we did for third-party capital.

10. See http://www.aspeninstitute.org/policy-work/aspen-network-development-entrepreneurs.

11. Eric Usher and UNEP have launched the GEF funded Seed Capital Access Facility as a way to

counter this.

12. UN Secretary-General’s Advisory Group on Energy and Climate Change, “Energy for a

Sustainable Future: Report and Recommendations," Abril 28, 2010, pag. 7.

13. International Energy Agency, Energy Poverty: How to Make Energy Access Universal? (París:

Author, 2010), pag. 7.

14. Gordon Browne, “The Road to Copenhagen: The Challenge of Climate Change and

Desarrollo,” speech delivered June 26, 2009; Project Catalyst, “Scaling Up Climate Finance,"

finance briefing paper, Septiembre 2009.

15. For a full discussion and example of this framework, ver

http://energyaccess.wikispaces.com/Toolkit+for+Increasing+Energy+Access.

70

innovaciones / Impact Investing

Descargado de http://direct.mit.edu/itgg/article-pdf/6/3/55/704696/inov_a_00082.pdf by guest on 07 Septiembre 2023