CAP AND GAP: THE FISCAL EFFECTS OF

PROPERTY TAX LEVY LIMITS IN NEW YORK

Phuong Nguyen-Hoang

School of Planning and

Public Affairs & Público

Policy Center

University of Iowa

Iowa City, IA 52242

phuong-nguyen@uiowa.edu

Pengju Zhang

School of Public Affairs and

Administration

Rutgers University, Nueva York

Nueva York, Nueva Jersey 07102

pengju.zhang@rutgers.edu

Abstracto

This is the first study to examine the fiscal effects of the New York

property tax levy limit, using variation from the degree of fiscal

stringency across school districts and over time in its first five

years of implementation. Based on a difference-in-differences es-

timator, coupled with an event study specification, we find that the

tax limit has imposed a real cap on many school districts; eso es,

at-limit districts’ total current expenditures per pupil are signif-

icantly lower than what they would have spent absent the limit.

For those affected school districts, this expenditure gap does not

come from spending on teacher salaries or fringe benefits but

rather from other instructional salaries/expenses, central admin-

istración, transportation, interfund transfers, and undistributed

spending. We also find heterogeneity in the constraining effects of

the tax limit across different need-based groups of school districts.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

F

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

1

https://doi.org/10.1162/edfp_a_00327

© 2020 Asociación para la política y las finanzas educativas

Cap and Gap: Tax Limits in New York

INTRODUCCIÓN

1 .

Under Chapter 97 of the Laws of 2011, the state of New York (Nueva York) established a property

tax levy limit (herein referred to as the tax limit) that affects all local governments with

property taxing power, including school districts. Effective in fiscal year 2013, the tax

limit basically restricts the annual growth of property tax levies to 2 percent or the rate

of inflation, whichever is less. The tax limit has been criticized for limiting NY school

districts’ ability to raise property taxes—their largest revenue source—for educational

services (Yinger 2019). Recent data from the NY State Education Department (NYSED)

seem to support this criticism. In fiscal years 2017 y 2018, 369 (55 por ciento) y 328

(49 por ciento) of the districts, respectivamente, proposed to raise taxes by every dollar they

could within the limit. A few districts (es decir., 36 districts in 2017) even proposed to over-

ride the tax limit. Despite criticisms, the NY State Senate and Assembly recently made

permanent the limit, which had been scheduled to expire in 2020 (NYSDTF 2020).

The tax limit in NY is one of the most recent examples of state-imposed tax and

expenditure limitations (TELs) that have been adopted in many states in the United

Estados (Downes and Figlio 2015; Lincoln Institute of Land Policy and George Washing-

ton Institute of Public Policy 2020).1 Applied public finance scholars have extensively

investigated the intended efficacy and unintended consequences of TELs. The literature

demonstrates two contrasting perspectives: The “institutional irrelevance view” holds

that fiscal rules can be strategically circumvented by local governments in many ways,

whereas the “public choice view” suggests that fiscal rules represent important and

effective constraints on the behavior of local political actors (Poterba 1996).

Empirical research on the fiscal impact of TELs on local general-purpose govern-

ments basically buttresses the “institutional irrelevance view” by pinning down mul-

tiple strategies that localities have used to escape the constraint of TELs (Mullins

and Joyce 1996; Shadbegian 1999; Skidmore 1999; Hoene 2004; Cheung 2008;

McCubbins and Moule 2010; Sol 2014; zhang 2018; Eliason and Lutz 2018; Zhang and

Hou 2020). Sin embargo, when it comes to school districts, studies on the fiscal impact of

TELs provide mixed findings. Based on seventeen empirical articles, a meta-regression

analysis finds that TELs have a complex effect on education financial resources, y

recent studies are more inclined to support the “public choice view” when compared

to studies conducted in the past (Ballal and Rubenstein 2009).

To provide new evidence on the effect of TELs on school finance, this study focuses

on the most recent tax limit in NY and seeks to answer three closely related research

preguntas. Considering that not all TELs are fiscally constraining, the first question

is whether the tax limit has a constraining effect, or has put an effective cap, on NY

school districts’ total current expenditures per pupil. The second research question is

whether the tax limit may have differential expenditure-stifling effects on different dis-

trict groups. Tercero, this study asks which expenditure categories and subcategories bear

the brunt of this constraint; eso es, how districts under fiscal constraint make spending

cuts across different functions.

1. En 2018, thirty-six states and Washington, DC imposed TELs on local governments’ property tax levy, though not

all of the TELs apply to school districts (Lincoln Institute of Land Policy and George Washington Institute of

Public Policy 2020).

2

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

By definition, a property tax levy limit is fiscally constraining or binding when it

prevents a school district from reaching the level of total spending desired or preferred

by local voters (or determined by the local median voter). This definition suggests that

“at-limit” school districts—those that exhaust the limit—are most likely constrained

by the tax limit. We adopt a difference-in-differences (DID) estimation approach by ex-

ploiting unaffected or far-from-limit districts as comparison districts for at-limit school

districts. We also utilize an event study specification to support causal links between

the tax limit and changes in school districts’ spending behaviors. Based on a data panel

de 666 school districts in NY between 2011 y 2017, we find strong evidence to support

the public choice view that the tax limit has put an effective cap or constraint on at-limit

school districts in the first five years of implementation.

Our study makes three contributions to the literature. Primero, we investigate both

average and heterogeneous fiscal effects of the tax limit, the latter of which has not been

adequately explored in the literature. Segundo, this is the first study to take full advantage

of the finely disaggregated expenditure data from NY. Our estimations provide a holistic

picture of cutback strategies adopted by different district types in response to the limit-

induced constraint. Tercero, this study evaluates the latest ongoing TEL measure, eso es,

the tax limit in NY and, por lo tanto, our findings can inform in a timely manner current

debates on its extension and potential changes in design.

The remainder of the paper proceeds as follows. The next section provides technical

details of the tax limit, followed by a review of the literature. We then present a simple

theoretical framework on the effect of the tax limit, discuss empirical challenges, y

present our empirical strategies. The next section briefly describes data and provides

a descriptive analysis, followed by a discussion of regression results. The last section

concludes with policy implications and suggestions for future research.

2 . B AC K G RO U N D

The property tax levy limit in NY imposes a percentage limit on total property tax levies

set by local governments, not on assessed property values or tax rates. Basically, local

governments may not adopt a budget funded by a property tax levy that exceeds the prior

year’s levy by more than 2 percent or the rate of inflation, whichever is less. The tax limit

on school districts does not apply to fiscally dependent large-city school districts (Nuevo

York City, Buffalo, Rochester, Siracusa, and Yonkers).

Property Tax Limit Formula

To calculate a school district’s tax limit, the formula starts with the district’s prior-

year property tax levy and then adds a prior-year reserve offset, from which the re-

serve amount (including interest earned) needs to be deducted, como se muestra en la figura 1.

It is multiplied by a district-specific tax base growth factor determined by the NY State

Department of Taxation and Finance (NYSDTF). Prior-year payments in lieu of taxes

(PILOTs) receivable are then added to the resulting product, while the prior-year capital

tax levy and tort exclusions are subtracted, leading to an adjusted prior-year tax levy.

The adjusted prior-year tax levy is multiplied with the allowable levy growth factor,

which is the lesser of either 2 percent or the inflation rate. The levy growth factor was 2

por ciento en 2013 y 2014, but fell to 1.46 por ciento, 1.62 por ciento, e incluso 0.12 por ciento en

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

/

F

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

F

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

3

Cap and Gap: Tax Limits in New York

Nota: Information on this formula, district-specific annual tax base growth factor, and statewide annual allowable levy growth

is available at https://www.osc.state.ny.us/local-government/property-tax-cap/real-property-tax-cap-local-governments. PILOT =

payments in lieu of taxes.

Cifra 1. Property Tax Limit Formula

2015, 2016, y 2017, respectivamente. After subtracting PILOTs receivable in the coming

year and adding available carryover, a school district will subsequently obtain its tax levy

limit for the coming or current fiscal year.

Sin embargo, the tax levy limit can be higher because of three excludable property tax

levies—namely, levies for court orders or judgments exceeding 5 percent of the prior-

year tax levy, a levy for an increase of over 2 percentage points in the rate of state-

mandated contributions to district pension funds, and the current-year levy for capital

projects. Además, a school district can still legally override the tax levy limit with

exclusions when there is 60 percent voter approval.

Property Tax Levy Limit and School District Budgeting Process

To examine whether the tax limit is binding or not, one also needs to understand lo-

cal budgeting processes in NY. The school districts’ fiscal year begins on 1 Julio. Every

año, the NYSDTF calculates a tax base growth factor for each school district, and by 15

Febrero, notifies those with a positive change in the factor. School districts can then

incorporate this growth factor, which is part of the tax limit formula, into the coming

year’s budget. Por 1 Marzo, school districts must report their proposed budget (incluido

levy) and data necessary to compute their property tax levy limit (as in figure 1) via the

Property Tax Report Card to the state comptroller, the commissioner of education, y

the NYSDTF. In this report card, the difference between the tax levy limit and the total

proposed tax levy is calculated. If the proposed levy is higher than the tax levy limit, el

budget, as explained above, must be approved by 60 percent or more of local voters to

override the limit (whereas regular budgets only need a 50 percent majority). In late

Abril, districts must transmit the report card to the NYSED and to local newspapers for

general circulation. Shortly after a public hearing, districts will mail budget notices to

eligible voters who cast their vote on the proposed budget sometime in May.2

A school district’s budget is not always successfully passed. The failure of budget

passage is not uncommon, especially before the enactment of the tax limit. In NY, if a

school district’s initial override budget is defeated, it has only one additional chance to

gain voter approval. In the second vote, the school board has three budget vote options:

2. A timeline of annual budget votes and school board elections since 2008 can be found on the Web site of NY

State School Boards Association at nyssba.org/news-media/school-budget-votes/.

4

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

the original failed budget; a revised budget that is lower than the original but still higher

than the levy limit and therefore requires 60 percent approval; and finally, a revised

budget that is lower than or equal to the levy limit and needs only 50 percent voter

approval. Given that the school year commences on 1 July for school districts, budget

revote activities must be completed in June.

If a second budget vote is again defeated, the district must operate under a con-

tingency budget no greater than its prior-year levy. (Alternately, the district can adopt

the contingency budget right after the first budget defeat.) Voting records show that

defeated budgets have dramatically decreased to less than 5 por ciento desde 2013, y

the number of cases adopting contingency budgets has become extremely rare—only

a single district adopted a contingency budget in two of the post-tax limit years.

3 . REVISIÓN DE LITERATURA

Because the tax limit under investigation is imposed by the state on local governments,

this review focuses on state-imposed TELs.3 The effect of state-imposed TELs has been

extensively studied by public finance scholars (Rose 2010). An empirical consensus in

the literature is that state-imposed TELs have little effect on the overall size of local

general-purpose government budgets (Mullins and Joyce 1996; Shadbegian 1999; Sol

2014; Eliason and Lutz 2018). Localities subjected to property tax limitations, both in

the United States and in some European countries, are found to tap into other un-

constrained revenue sources (other taxes and fees), establish special districts or home-

owners’ associations, and issue more nonguaranteed debt (Shadbegian 1999; Skidmore

1999; Hoene 2004; Cheung 2008; McCubbins and Moule 2010; Blom-Hansen, Houl-

berg, and Serritzlew 2014; zhang 2018; Kioko and Zhang 2019).

School districts differ from other local, general-purpose governments, possibly lead-

ing to a different impact of TELs on school districts’ fiscal behaviors. Primero, escuela

districts are not authorized to create special districts through enabling legislations. Sec-

ond, property taxes constitute the lion’s share of own-source revenue for most school

districts in the United States. Por lo tanto, when confronted with a constraining limit on

property taxes, they are less able to raise adequate, other own-source revenues to off-

set the shortfall, as confirmed by the historical analysis in Downes and Killeen (2014).

También, the constraining effects of TELs on school districts may become stronger over

tiempo (Dye, McGuire, and McMillen 2005). Ballal and Rubenstein (2009) argue that

studies with more recent data tend to consistently find a negative association between

TELs and local spending on education, although empirical findings are more incon-

sistent across studies analyzing older data. Extant studies also explore whether state

governments may help fill the gap when local revenues decline. Shadbegian (2003),

Blankenau and Skidmore (2004), and Shadbegian and Jones (2005) all find that TELs

result in increased state aid, suggesting the reduction of local spending is, to some

extent, offset by the growth of state fiscal transfers.

Two studies examine previous TELs in New York. Ebdon (1997) analyzes the impact

of constitutional property tax levy limits on small city school districts in NY and finds the

limit reduced spending in small city school districts by 2 percent from 1984 a 1986.

3. Kioko (2011) and Brooks, Halberstam, and Phillips (2016) provide reviews on state-level TELs and city-level self-

imposed TELs, respectivamente.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

5

Cap and Gap: Tax Limits in New York

Nguyen-Hoang (2013) examines the effects of the 1986 repeal of these constitutional

limits and finds that the repeal had no effect on school operating expenditures in NY

durante 1980 a través de 1994. Sin embargo, the repealed constitutional tax levy limit differs

from the tax limit in our study for two major reasons. Primero, a constitutional limit is

harder to change than a statutory one, like the tax limit. Segundo, el 2013 tax limit starts

with the prior-year levy, and the constitutional limit restricts school operating levies to

a maximum 2 percent of a five-year average of the full value of taxable property.

In addition to the effects of TELs on school funding sources and total expenditures,

some studies also examine whether school districts respond to TELs by changing their

expenditure structure or reallocating educational inputs. Dye and McGuire (1997) find

that the property tax cap enacted in 1991 in the Chicago metropolitan area decreased

operating expenditures but had no effect on instructional expenditures in the short

run. Downes and Figlio (2015) suggest that the protection of instructional spending at

the expense of noninstructional spending found in Dye and McGuire (1997) is prob-

ably related to Tiebout’s (1956) theory of competition through which unaffected dis-

tricts could put competitive pressure on affected districts. Dye, McGuire, and McMillen

(2005), sin embargo, find that, in the long run, growth rates in both operating and instruc-

tional expenditures are slower in districts subject to the same Chicago tax cap. Figlio

(1998) also finds the reduction of school district resources caused by Measure 5 in Ore-

gon was borne more heavily by instruction than by administration. Además, Figlio’s

(1997) study on school-level data from forty-nine states finds schools subject to prop-

erty tax levy limitations did not reduce administrative costs but lowered instructional

services. As an explanation for the stronger expenditure effects of TELs on instruction

than administration, Downes and Figlio (1999, 2015) argue that a larger cut in instruc-

tional spending is consistent with administrative rents (defined as use of resources to

benefit those in control of resources) and with TEL provisions’ lack of incentives for

administrators to improve efficiency. Considerándolo todo, the literature seems to reveal mixed

evidence that TELs reduce resources for instruction or administration.4 Also, none of

the existing studies explores whether or how fiscally constrained school districts, in re-

sponse to a TEL, cut subcategories of instructional expenditures and other spending cat-

egories beyond instruction and administration—a literature gap that our study seeks to

fill.

The current study also supplements the education finance literature on how school

districts respond to the fiscal impacts of a major economic bust. The Great Recession,

which started in 2007, induced most states to cut education aid (Oliff and Leachman

2011) and shrank their property tax base (Collins and Propheter 2013). Without a prop-

erty tax levy limit, school districts could raise property taxes (by levying higher tax rates

on their smaller tax base) to buffer the impact of decreased state aid (Chakrabarti, Liv-

ingston, and Roy 2014; evans, Schwab, and Wagner 2019). Sin embargo, had a property

tax levy limit similar to NY’s current limit been in place during the Great Recession

4. Another strand of relevant research examines the effects of TELs on educational outcomes. Figlio (1997) finds

that TELs are associated with lower student performance, which is partly explained by the findings that tax limits

systematically reduce the quality of new teacher hires (Figlio and Rueben 2001), whereas Downes, Dye, y

McGuire (1998) find only limited evidence that student performance declines in districts subject to TELs. De este modo,

the literature does not provide clear guidance on the relationship between TELs and student performance, either.

A recent literature review on this can be found in Downes and Figlio (2015).

6

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

/

F

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

años, school districts’ ability to stabilize their budgets via raises in property taxes would

have been seriously undermined. A recent official report sounded a grim warning of

the ongoing COVID-19 pandemic’s implications for NY schools. The state’s pandemic

response includes substantial cuts to state aid; coupled with school districts’ tax cap-

induced inability to shore up local revenue, the reduction in state aid could have dra-

matic effects on NY school districts’ resources (Office of the New York State Comptroller

2020). This study’s findings give credence to that warning.

4 . T H E O R E T I C A L F R A M E WO R K

This section presents a conceptual framework for how the tax limit may exert fiscal con-

straint on school districts. Districts are constrained when the tax limit prevents them

from achieving the spending level desired, or determined, by the majority of local vot-

ers (or by the median voter). Tal como, constrained districts refer to the those who spend

less than what they would have spent absent the tax limit.

The first cause for the possible constraining effect of the tax limit is associated with

the important role that property taxes play in funding school districts’ operations. Como

with most school districts in the United States, NY school districts rely primarily on

two major revenue sources: property taxes and state aid. In the three-year period before

2013, the percentage share of state aid in total revenue sources experienced a slight

decline, de 37.9 por ciento en 2010 a 37.5 por ciento en 2012, whereas property taxes on

average accounted for an increasingly large share of all school district revenues (de

41.5 por ciento en 2010 a 44.2 por ciento en 2012). Given the important role of property taxes,

a limit on this revenue source may translate into fiscal constraint on some districts.

The constraint may be felt particularly strongly by districts that rely heavily on prop-

erty taxes. Statewide averages mask substantial variation in districts’ reliance on prop-

erty taxes. To present this variation clearly, we rely on the state official classification

of school districts based on the need/resource capacity (NRC) índice: low NRC, aver-

age NRC, urban–suburban high NRC, and rural high-NRC districts.5 Given that the

NRC index—a ratio of a school district’s standardized poverty percentage to its com-

bined wealth ratio—indicates the district’s ability to meet the needs of students through

local resources, these groups are, for ease of presentation, hereinafter referred to as low-

need, average-need, urban high-need, and rural high-need districts. Columna 2 de mesa 1

shows that 85 percent of low-need districts’ total revenue comes from property tax levy,

followed by average-need districts (55 por ciento). Logically, these two groups of districts

with higher reliance on property taxes are more likely to be constrained by the tax limit.

Por el contrario, rural high-need districts with relatively much lower reliance on property

taxes (31 por ciento) are less likely to be constrained.

Beyond the degree of reliance on property taxes, the fiscal impact of the tax limit

may be offset by how much state aid and federal aid a district receives during the limit

5. A measure for need used in the NRC index is the share of eligible free or reduced-priced lunch students, y

capacity is measured partly by full property valuation. While table A.1 (available in a separate online appendix that

can be accessed on Education Finance and Policy’s Web site at https://doi.org/10.1162/edfp_a_00327) proporciona

more information on how each group is officially defined, columnas 3 y 4 de mesa 1 show that low-need districts

have only 11 percent of economically disadvantaged students (con $3.8 million full property value per pupil), whereas urban high-need districts are relatively property-poor ($434,669 full property value per pupil), con

a much higher share of economically disadvantaged students (64 por ciento). Our data also show that districts

retained their NRC-based classification during our sample period.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

7

Cap and Gap: Tax Limits in New York

Mesa 1. Basic Information on Four District Groups

Average Total Current

Expenditure per

Pupil ($) Average Share of Property Tax Levy to Total Revenue (%) Average Share of Free or Reduced-Priced Lunch Students (%) Average Total Full District Valuation per Pupil ($)

District Groups

Low-need

Average-need

Urban high-need

Rural high-need

(1)

30,264

20,388

20,373

21,005

(2)

84.8

54.7

41.3

31.0

(3)

11.2

34.7

64.1

52.2

(4)

3,808,624

760,233

434,669

538,832

Nota: The averages come from our sample period between 2011 y 2017.

years.6 A district that has been hit hard by the limit may receive more intergovernmen-

tal aid, which offsets the shortfall of property taxes. Because the amount of intergov-

ernmental aid that a district receives is usually outside its control, we allow aid to fully

play this offsetting role by leaving out aid variables in our empirical models. De este modo, nosotros

compare the results from models with and without aid variables to diagnose the size of

the offsetting effects of intergovernmental aid, if any.

A district may attempt to escape limit-induced constraints by overriding the limit, como

mentioned before. Sin embargo, for two reasons, overriding the limit successfully is neither

easy nor tantamount to permission for the district to spend at the level desired absent

the limit. Primero, the required 60 percent voter approval for overriding is a more diffi-

cult hurdle to overcome than a 50 percent majority for regular budgets. Segundo, a levy

limit serves as a reference levy. According to the theory on reference-dependent pref-

erences (Ashworth and Heyndels 1999), when voters are more readily able to compare

the difference between a proposed levy and the levy limit, they are more likely to reject

the override. The combination of the supermajority threshold and reference-dependent

preference enhances the likelihood of failed budgets. The consequence of two consec-

utive failed proposed budgets is the adoption of a contingency budget (cual, de nuevo,

will be no greater than the prior-year levy). This consequence may induce the district

to be more conservative in its proposed overriding amount, which suggests, absent the

limit, this district could still have spent more than the overriding level.

Finalmente, one can expect that constrained districts do not cut spending equally across

all categories; some categories receive fewer resources or get cut whereas resources for

other categories remain intact. Expenses that school districts are legally and contrac-

tually bound to incur may be hard to reduce or cut. Examples of these expenses are

teacher salaries and benefits, including retirement, that result from union agreements.

School districts are, sin embargo, more likely to spend less on expenditure items that are

non-core to their operations (p.ej., support staff, paraprofessionals, undistributed funds,

interfund transfers) or less contractually binding (p.ej., school supplies, materiales). Nosotros

use the detailed expenditure data to provide by far the most nuanced picture of how

at-limit districts across district groups change their spending patterns in response to

the tax limit.

6. Other revenue sources for NY school districts include user charges, and sales and use taxes. But our data show

that school districts received less than 2 percent of total revenue from those two sources in 2013.

8

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

5 . E M P I R I C A L C H A L L E N G E S A N D S T R AT E G I E S

A Measure of the Fiscal Stringency of Property Tax Limit

Multiple measures can be used to capture TELs. The most common approach is to

use a dichotomous indicator to identify the existence of a TEL law (p.ej., Shadbegian

1999). The indicator approach makes sense when the event of interest is simply the

occurrence of a TEL law with little consideration of heterogeneity in TEL law designs.

A second approach is to construct a continuous index of TEL degrees of stringency by

assigning weights to different components in each TEL law (p.ej., Deller, Stallmann,

and Amiel 2012). This approach quantifies TEL laws and allows for engaging more

advanced econometric tools in TEL analysis.

Our measure deviates from those two approaches for two reasons. Primero, both ap-

proaches are more appropriate for cross-state analyses. As the tax limit formula in NY

applies identically to all districts, adopting either of those two measures would lead

to zero cross-district variation for our study. Segundo, of our interest is not whether NY

adopts a limit, but rather whether the tax limit really exerts binding constraints on some

districts, and how the tax limit changes the spending behaviors of those constrained or

affected districts. En otras palabras, we need a working measure of fiscal stringency for

the tax limit in NY.

Conceptually, a district’s limit-induced fiscal constraint can be measured by distance

to limit (DL), defined as the percentage gap between the maximum property levy legally

allowed by the limit (or levy limit, LL) and the district’s proposed property tax levy (PL).

Eso es,

DL = (LL − PL)/LL.

(1)

By definition, DL in equation 1 is continuous, and a large positive DL indicates that

a district does not have to tap all available property tax levy allowed—an indication of

nonconstraint. Por el contrario, a district is more likely to be fiscally constrained when it

overrides the limit (DL < 0), exhausts the limit (DL = 0), or raises almost every property

tax dollar it can under the limit (0 < DL (cid:2) ε, where ε is a very small positive number).

All districts with DL (cid:2) ε are referred to in this study as at-limit districts.7

Note that DL is not a sound direct measure of fiscal constraint. A unit increase in

DL does not necessarily indicate a unit decrease in the degree of constraint; that is,

DL is not linearly correlated with the degree of constraint. Additionally, what really

concerns us is not the limit-induced fiscal behaviors of the average-DL district, but

of constrained districts. Thus, instead of using DL directly, we use DL to develop a

dichotomous variable of being at limit, D. D is coded 1 for at-limit districts with DL (cid:2) ε,

where ε is a numeric positive benchmark, and 0 otherwise. As indicated, ε must be very

small. For instance, Bradbury, Mayer, and Case (2001) consider a school district to be at

limit in a year when its proposed levy is within 0.1 percent of its levy limit in that year,

that is, when ε is 0.1 percent. This small value of ε is consistent with our definition of an

at-limit district and we therefore adopt this ε, 0.1 percent, as our preferred benchmark

as well.

7. At-limit districts may be theoretically unconstrained when their maximum levy limits happen to equal exactly the

amount needed to fund their desired spending levels. We suspect that, in practice, the probability at-limit districts

are not constrained is very low.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

f

/

/

e

d

u

e

d

p

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

e

d

p

_

a

_

0

0

3

2

7

p

d

.

f

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

9

Cap and Gap: Tax Limits in New York

Admittedly, this chosen value of ε may not be perfect. For instance, a district that is

actually constrained by the tax limit could be classified as a control unit in our research

design when its DL is just slightly larger than ε, leading to an attenuation of estimated

tax limit effects on at-limit districts. This attenuation suggests that our estimated effects

are conservative, and the true effects could be even stronger when at-limit districts are

perfectly identified.

It may not be a good idea to choose a relatively larger ε. With a relatively larger ε,

an at-limit district would have considerable untapped property taxes. This is logically

self-contradictory because an at-limit district would not have much excessive revenue

slack if they were really at limit or constrained. Regardless, we start with ε = 0.1 percent

and increase ε to 1 percent and 2 percent to test the robustness of our measure.

Empirical Models

Difference-in-Differences Estimator

To examine whether and how the tax limit affects the fiscal behaviors of at-limit school

districts in NY, we start with a DID framework and estimate a model of the following

form:

ln Eit = τt + μi + αDit + (cid:5)it,

(2)

where E stands for total current expenditures per pupil, i and t index school districts

and years, and τ and μ are year- and school district–fixed effects, respectively.8 As dis-

cussed earlier, D in equation 2 is coded as 1 for at-limit school districts with DL (cid:2) 0.1

percent—districts that are most likely constrained by the tax limit—and 0 otherwise.

The coefficient of this variable, α, indicates how much more or less spending (in per-

centage terms) would, on average, have changed for at-limit school districts.

A key identifying assumption underlying a DID estimator is that the pre-limit trend

in total current expenditures per pupil of at-limit school districts parallels that of coun-

terfactual school districts. Similar to Lafortune, Rothstein, and Schanzenbach (2018),

school districts not at limit in a particular year serve as the counterfactual for at-limit

school districts in that year. To test the common pre-trend assumption, we add the lin-

ear pre-trend variable (P), as shown in equation 3, to capture differences in E between

at-limit and counterfactual districts during the years before a district is first at limit (in

year t*). Of note, not all school districts are at limit immediately in 2013 when the tax

limit comes into effect. Therefore, the initial at-limit year, t*, varies from one district

to another. P equals (t − t0) before t* (where t0 is the baseline year that immediately

precedes t*, or t0 = t* − 1), and 0 otherwise. A small insignificant coefficient of P, β, is

expected, should the common pre-trend assumption hold.

ln Eit = τt + μi + αDit + βPit + δTit + βWit + (cid:5)it.

(3)

According to the tax limit formula, a school district’s current levy will factor into the

calculation of the proposed levy in the following year, suggesting a dynamic effect of

8. The tax limit may affect capital spending. However, capital investment tends to be lumpy (i.e., not spreading

evenly across the years). Therefore, a valid investigation of a policy or intervention’s effect on capital spending

usually requires a long data panel and a different methodological approach than that used to investigate current

expenditures (Wang, Duncombe, and Yinger 2011).

10

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

/

/

f

e

d

u

e

d

p

a

r

t

i

c

e

-

p

d

l

f

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

e

d

p

_

a

_

0

0

3

2

7

p

d

f

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

the tax limit during its post-initial (t > t*) período. To capture this post-initial effect, nosotros

include the post-trend variable (t) in equation 3. Específicamente, T captures whether, encima

tiempo, the expenditure change associated with D stays constant (δ is insignificant), dis-

sipates (δ is significantly positive), or increases (δ is significantly negative). Por lo tanto,

T equals (t − t*) for at-limit districts when t > t*, y 0 de lo contrario. For school districts

that are never at limit, P and T are set to zeros during the entire sample period.9

Following the education cost-function literature (Duncombe and Yinger 2011), equa-

ción 3 also includes a series of control variables (W.), such as student characteristics (es decir.,

logged enrollment as well as the percentages of English Language Learner students,

special education students, economically disadvantaged students, and African Ameri-

can students), and factors influencing efficiency and demand for school expenditures

(es decir., logged median household income, logged median tax share, logged state and fed-

eral aid per pupil, the percentages of owner-occupied housing units, and population

aged 25 years and over with a four-year college education). The median tax share is de-

rived as the ratio of a district’s median housing value to its total taxable property value

per pupil.

We also estimate equation 3 separately with ε = 2 percent and ε = 1 por ciento. Como

discussed earlier, a larger ε is more likely to produce nonnegative and insignificant

effects of the limit because more far-from-limit and plausibly unconstrained districts

are treated as at-limit constrained districts in those scenarios.

Event Study Specification

A major empirical challenge of equation 3 is that even with school district and year fixed

efectos, as well as all controls in W, the key variable D is still potentially biased, as are

its derived variables P and T. The more a school district would like to spend, the more

likely it is to be at limit, leading to a reverse causation or a positive bias in the estimate

of α. Eso es, the negative coefficient of D is likely to be attenuated toward zero. Uno

way to address this endogeneity is to use instrumental variables. Sin embargo, it is hard

to find three or more instrumental variables that are time-varying (because of district

efectos fijos), exogenous of equation 3, and strongly correlated with D, PAG, and T.

Another way to diagnose and reduce the bias is to use nonparametric event-study

modelos. The use of event-study specifications is also warranted when there is variation

in treatment timing (Goodman-Bacon 2021), as in the current study. An event occurs in

a year when a district is at limit (DL ≤ 0.1 por ciento). We estimate models of the following

forma:

ln Eit = τt + μi +

5(cid:2)

k=−4

θkTk,él + βWit + (cid:5)él,

(4)

where τ , μ, and W are defined as in equation 3; Tk equals 1 for at-limit districts when

t = t0 + k, where k represents the number of years before (k < 0) or after (k > 0) el

baseline year, t0. While year 5 is the farthest year after t0 in our dataset, −4 represents

four or more years before t0. También, t0 is excluded and serves as the reference year. Cuando

9. Year fixed effects obviate the need for a general trend variable (coded 1 para 2011, 2 para 2012, etcétera) for all school

districts. Including such a general trend variable would require a drop of a year dummy while the results stay

sin alterar.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

F

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

F

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

11

Cap and Gap: Tax Limits in New York

k > 0, the coefficient for a Tk, θk, indicates the effect of an event in t0 on outcomes k

años después. Compared to parametric estimations, the θ coefficients with k > 0 captura

dynamic effects of the tax limit on at-limit districts. Similar to the DID design, an event-

study design requires, for a causal interpretation, a common pre-trend of treatment (en-

limit) and comparison (not-at-limit) districts. This assumption is statistically supported

when the series of lead indicators (θ−4 to θ−1) are not significant.

There are two important issues related to equation 4. Primero, as explained earlier, un

at-limit school district may receive federal and state aid to meet their desired spending

nivel. Por lo tanto, in addition to the models with aid variables, our preferred specification

is one without these variables so that intergovernmental aid is allowed to offset property

tax shortfall. Segundo, as with the standard event-study design, equation 4 accounts only

for the first event of being at limit. Sin embargo, a school district may experience subse-

quent events, in subsequent years, after the first. There is no established econometric

method to account for multiple events. Following Lafortune, Rothstein, and Schanzen-

bach (2018), we replicate the data for school districts with multiple events; Por ejemplo,

a district with three at-limit events has three copies (or cohorts). We then stack all repli-

cated cohorts with no-event districts. Each cohort of the same multiple-event district

now has only one event in this stacked dataset. The coding method for Tk in equation

4 is the same as before, and μ now represents district-cohort fixed effects.

Additional Analyses

To explore the second research question, which concerns the differential effects of

the tax limit, we estimate equation 4 using four NRC-based district groups: low-need,

average-need, and urban and rural high-need districts. Específicamente, we allow each

district group, gramo, to have a separate series of Tk for the five-year limit period (es decir.,

(cid:3)

θkgTkg), where Tkg captures the average within-g effect of an event in t0 on

outcomes k years later.10 This flexibility allows us to see how districts in four groups

respond differently to the limit. Finalmente, for the third research question on cutback

estrategias, we use equation 4 with Tkg for disaggregated expenditure categories and

subcategories as dependent variables.

5

k=1

4

g=1

(cid:3)

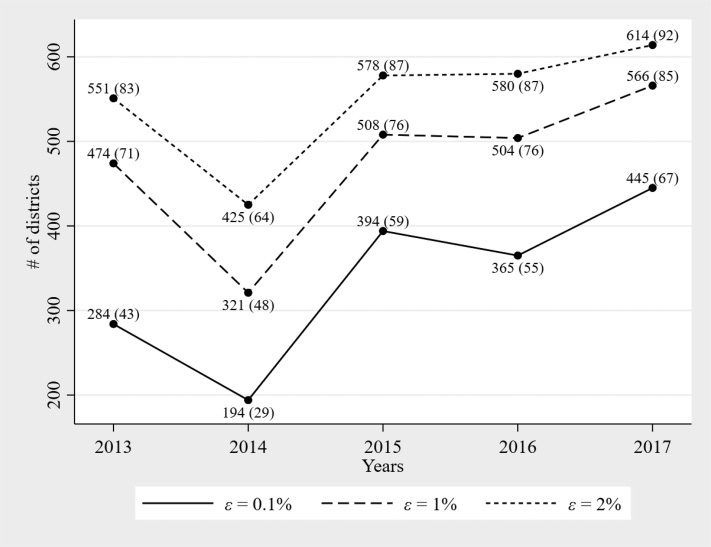

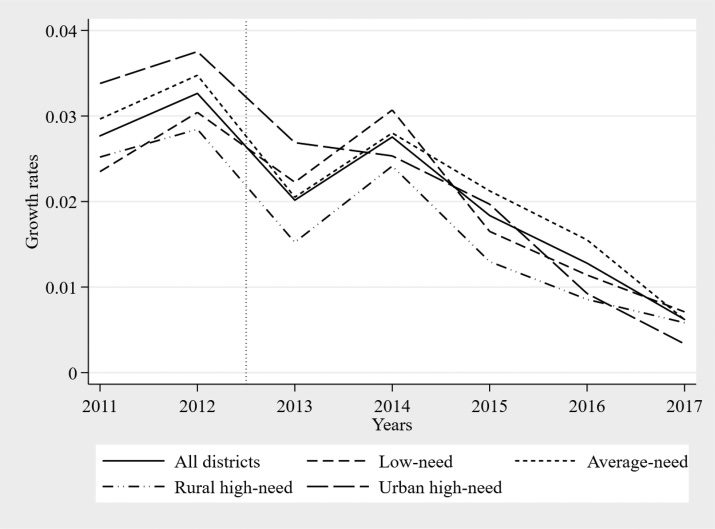

6 . DATA A N D D E S C R I P T I V E A N A LY S I S

Datos

The data panel consists of all school districts, except for Buffalo, Nueva York,

Rochester, Siracusa, and Yonkers.11 The sample period is between 2011 y 2017.12 Mayoría

of our data come from NYSED. We also take some data from the American Commu-

nity Surveys, a saber, median house value (to calculate tax share), median homeowner

10.As shown in table 3, the number of comparison districts that are never at limit is quite small (only six low-need and

θkTk,

nine urban high-need districts). Por lo tanto, all district groups have the same pre-trend variables, o

to maximize pre-trend variation.

(cid:3)−1

k=−4

11. These five large city school districts, called the “Big Five,” are not subject to the tax limit. Education budgets for

these fiscally dependent school districts are included in their respective municipal budgets. Además, each city,

including the Big Five cities, is subject to an individual constitutional tax limit; education in each city is funded

within that set limit (New York State Office of the State Comptroller 2018). Constitutional tax limits do not apply

to the independent school districts that comprise our sample.

12. We do not extend the data further back beyond 2011 to head off potential effects of the Great Recession years on

school districts’ resources.

12

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

F

/

/

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

Mesa 2. Summary Statistics

Variables

Key variables

Total current expenditures per pupil, $ D (= 1 if DL (cid:2) 0.1 y 0 de lo contrario) Control variables Enrollment Percent of free or reduced-price lunch students Percent of special education students Percent of ELL students Percent of black students Median homeowner income Tax share Mean SD Minimum Maximum Data Source 22,247 9,246 11,368 279,812 0.4 0.5 2,267 35.9 13.9 2.2 4.9 2,306 18.9 3.0 4.3 8.9 0 16 0 4.1 0 0 1 19,457 100 32.3 37.1 79.7 78,794 30,856 37,930 250,000 0.33 0.15 0.004 1 1, 3 1 1 1 1 1 2 1, 2, 3 2 2 1 1 Percent of adults with college education Percent of owner-occupied housing units 29.2 77.2 15.0 12.3 Intergovernmental aid Staid aid per pupil Federal aid per pupil 9,018 779 4,711 606 6.1 5.0 816 0 1.04 89.1 100 47,613 13,082 Notas: Hay 4,630 observaciones. This table summarizes fiscal, económico, and demographic information for 666 New York school districts between 2011 y 2017. SD = standard deviation; ELL = English language learner. income, and district-level information on percent of college-educated population and owner-occupied housing units. Mesa 2 provides summary statistics and sources of the variables used in our estimations. We follow the NYSED categorization of current ex- penditure categories and subcategories, and table 4 provides the definitions of all cate- gories and subcategories we use for our estimations. Descriptive Analysis New York state’s property tax limit law’s primary objective is to combat the growth of property tax revenue. In figure 2, we delineate the trends of the average annual growth rates of property tax levy by four district groups. Basically, all district groups exhibit a similar declining pattern in the growth rate of property tax levy. Of note, urban high- need districts had the highest levy growth rate before 2013, experienced the fastest de- clining trend, and had the lowest levy growth rate five years after the limit enactment. Cifra 3 presents the number of at-limit districts as a share of total districts by different values of ε. When ε is set at 2 por ciento, 551 districts (o 83 percent of all) would be counted as at-limit districts in 2013, and this number increases to 614 (o 92 por ciento) en 2017. When using ε = 1 por ciento, the number of at-limit districts increases from 474 (o 71 por ciento) en 2013 a 566 (o 85 por ciento) en 2017. Finalmente, with ε = 0.1 por ciento (our preferred benchmark), at-limit districts number 284 (42 por ciento) en 2013 y 445 (67 por ciento) en 2017. Cifra 3 provides two takeaways. Primero, the annual number of at-limit districts in NY increases substantially with larger ε. Starting with ε = 0.1 por ciento, the number of at- limit districts in 2013 expands by 67 percent with ε = 1 percent and by 94 percent with ε = 2 por ciento. Segundo, all ε options illustrate the substantial temporal upward trend in the frequency of at-limit districts. This trend is consistent with findings in other states. l D o w n o a d e desde h t t p : / / directo . mi t . F / / e d u e d p a r t i c e – pdlf / / / / / 1 7 1 1 1 9 7 7 6 2 4 e d p _ a _ 0 0 3 2 7 pd . f f b y g u e s t t o n 0 7 septiembre 2 0 2 3 13 Cap and Gap: Tax Limits in New York Figure 2. The Average Annual Growth Rates of Total Property Tax Levy by District Groups l D o w n o a d e d f r o m h t t p : / / directo . mi t . / / partícula alimentada – pdlf / / / / / 1 7 1 1 1 9 7 7 6 2 4 e d p _ a _ 0 0 3 2 7 pdf . f por invitado 0 7 septiembre 2 0 2 3 Nota: The numbers in parentheses indicate the percentage shares of total school districts. Cifra 3. The Numbers and Shares of At-Limit School Districts Over Time by Different Values of ε 14 Phuong Nguyen-Hoang and Pengju Zhang Table 3. Distribution of School Districts by the Number of Times Being at Limit (with ε = 0.1%) and by Need Groups Number of Times at Limit Low-Need Average-Need Urban High-Need Rural High-Need All Districts 0 1 2 3 4 5 Total 6 (5) 12 (9) 30 (23) 21 (16) 45 (34) 19 (14) 133 29 (9) 59 (18) 66 (20) 90 (27) 55 (16) 37 (11) 336 9 (20) 8 (18) 7 (16) 11 (25) 5 (11) 4 (9) 44 33 (22) 35 (23) 33 (22) 26 (17) 19 (12) 7 (5) 153 77 (12) 114 (17) 136 (20) 148 (22) 124 (19) 67 (10) 666 Nota: The numbers in parentheses indicate at-limit districts as a percent of all districts within a group. Por ejemplo, Dye, McGuire, and McMillen (2005) find the binding effect of the tax limit in Illinois becomes stronger over time. Mesa 3 shows the distribution of at-limit districts by instances of being at limit and by type of need. Of all districts, 77 (12 por ciento) are never at limit and the number of these districts is sufficiently large to serve as a comparison group. Being at limit three times during the five-year limit duration, as occurs for 148 districts, is the mode. Three in- stances of being at limit is also the mode for average-need and urban high-need groups. As many as 67 (10 por ciento) districts are at limit in all five years. Mesa 3 indicates sub- stantial within- and across-district variation for our estimations. Our data show that only 8.9 percent of all at-limit cases needed budget overrides (es decir., DL < 0). Finally, in over two thirds of no-override at-limit cases, the proposed limit exactly equals levy limit (DL = 0). The primary dependent variables are total current expenditures per pupil defined as ([total district expenditures − debt service]/enrollment).13 Table 2 shows the mean cur- rent expenditure per pupil is $22,247 with a standard deviation of nearly $9,246. The last four columns of table 4 also show three spending patterns from the group-based shares of each expenditure category in their total current expenditures, and the group- based shares of each subcategory in their respective category. First, the two largest categories are instruction and benefits, while the smallest expenditure categories are, in ascending order, interfund transfers, undistributed, administration, and transporta- tion. These categories represent only 0.5 percent to 5.6 percent of total current expen- ditures, far less than the second highest category of benefits (23 percent to 25 percent). Of note, the share of administration in total current expenditures is lower than that of transportation. Second, one expenditure subcategory dominates across instruction, benefits, and administration. Teacher salary constitutes the largest shares of districts’ instructional budget, 54 percent to 60 percent, followed by other instructional expenses (24 percent to 35 percent), and other instructional salaries (13.3 percent to 15.4 percent). Central ad- ministration and other fringes account for at least 76 percent of total administration and benefits, respectively. Finally, there is some expenditure variation in both categories and subcategories across district groups. There is a six percentage point difference between 13. Once logged enrollment is controlled for on the right-hand side, the results with either logged expenditures or logged expenditures per pupil are the same. l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / / f e d u e d p a r t i c e - p d l f / / / / / 1 7 1 1 1 9 7 7 6 2 4 e d p _ a _ 0 0 3 2 7 p d f . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 15 Cap and Gap: Tax Limits in New York . ] 8 3 5 [ . ] 3 3 1 [ . ] 9 2 3 [ . ) 5 1 6 ( . ] 9 2 2 [ . ] 1 7 7 [ . ) 4 2 ( . ) 8 4 ( ) 2 2 ( . ) 5 0 ( . ] 1 2 [ ] 9 7 [ . ) 8 2 2 ( p u o r g t c i r t s i d h c a e . ] 9 1 5 [ . ] 5 3 1 [ . ] 6 4 3 [ . ) 3 5 5 ( . ] 8 7 1 [ . ] 2 2 8 [ ) 8 3 ( . ) 5 5 ( . . ) 1 3 ( . ) 4 1 ( . ] 5 7 1 [ . ] 5 2 8 [ . ) 7 4 2 ( d e e N - h g i H n a b r U d e e N - h g i H l a r u R d e e N - e g a r e v A d e e N - w o L s n o i t i n fi e D s e i r o g e t a c b u S . ] 2 7 5 [ . ] 0 4 1 [ . ] 3 0 6 [ . ] 4 5 1 [ i n e t r a g r e d n k e r p , s e s r u n , s r e k r o w l i a c o s l , s t s i g o o h c y s p , s r o e s n u o c l l o o h c s o t i d a p s e i r a a S l s e i r a a s l l a n o i t c u r t s n i r e h t O s r e h c a e t 2 1 — K o t i d a p s e i r a a S l y r a a s l r e h c a e T . ] 8 8 2 [ . ] 3 4 2 [ ) S E C O B ( s e c i v r e S l a n o i t a c u d E e v i t a r e p o o C f o s d r a o B , n o i s i v r e p u s d n a l t n e m p o e v e d m u u c i r r u C l s e s n e p x e f f a t s t r o p p u s r e h t o d n a , s d a i r e h c a e t , s l a n o i s s e f o r p a r a p , s n a i r a r b i l , s r e h c a e t , . g . e ( s e r u t i d n e p x e l a n o i t c u r t s n i l y r a a s n o n d n a , s n o i t i u t t c i r t s i d r e t n i , s e c i v r e s l a n o i t c u r t s n i l a n o i t c u r t s n i r e h t O . ) 4 6 5 ( . ] 4 0 2 [ ) 9 5 ( . ] 8 2 2 [ . ] 6 9 7 [ . ] 2 7 7 [ . ) 1 3 ( . ) 6 5 ( ) 4 2 ( . . ) 3 1 ( . ] 8 9 1 [ . ] 2 0 8 [ . ) 8 4 2 ( . ) 1 3 ( . ) 7 4 ( . ) 9 1 ( . ) 4 1 ( . ] 7 3 2 [ . ] 3 6 7 [ ) 3 2 ( c i l b u p , t n e m e g a n a m s d r o c e r s t n e g a l a c s fi r o f s e e f ; s e c i v r e s d n a , n o i t a m r o f n i , l e n n o s r e p , g n i s a h c r u p , s s e n i s u b f o s e c fi f o e h t ; r e c fi f o l o o h c s i f e h C n o i t a r t s i n m d a i l a r t n e C n o i t a r t s i n m d a i l a t o T , k r e c l t c i r t s i d f o s e c fi f o e h t ; s e c i v r e s l a g e l d n a g n i t i d u a ; g n i t e e m t c i r t s i d ; n o i t a c u d e f o d r a o B n o i t a c u d e f o d r a o B n o i t a r t s i n m d A i ) s e i t i v i t c a l r a u c i i r r u c , t n e m p u q e , s l a i r e t a m , s e i l p p u s n o i t c u r t s n i l a t o T r o t c e l l o c x a t d n a , r e r u s a e r t ) s e s n e p x e l a t i p a c i g n d u c x e ( l g n d i l i u b e g a r a g d n a s e s u b l o o h c s i g n d u c n l i s e c i v r e s n o i t a t r o p s n a r T l e b a l i a v a s e u d i n o i t a c o s s a l o o h c s , g n i s s e c o r p a t a d , g n i l i a m , g n i t n i r p , m o o r e r o t s l a r t n e C l e b a l i a v a s d n u f l a t i p a c d n a e c i v r e s d o o f l o o h c s o t r e f s n a r T l e b a l i a v a t o N t o N t o N s r e f s n a r t d n u f r e t n I n o i t a t r o p s n a r T d e t u b i r t s i d n U s t fi e n e b e e y o p m e l r e h t o , s e e y o p m e l r o f e g a r e v o c l a t n e d d n a l i a c d e M s e g n i r f r e h t O s t fi e n e b l a t o T m e t s y s t n e m e r i t e r r e h c a e t n i s l a u d i v i d n i r o f s t n e m y a P t n e m e r i t e r r e h c a e T s t fi e n e B s e i r o g e t a C n o i t c u r t s n I d n a s e i r o g e t a c e r u t i d n e p x e l l a r o f l a u m r o f t n e t s i s n o c a s e s u D E S Y N . p u o r g t c i r t s i d h c a e i n h t i w s e i r o g e t a c e r u t i d n e p x e n i s e i r o g e t a c b u s e r u t i d n e p x e f o s e r a h s t n e c r e p e h t e t a c d n i i s t e k c a r b n i s r e b m u n e h T . d o i r e p l e p m a s e h t g n i r u d l e b a t e h t n i d e t r o p e r t o n e r a ) e c i v r e s y t i n u m m o c d n a , e c n a n e t n a m d n a i n o i t a r e p o , y l e m a n ( s e i r o g e t a c e r u t i d n e p x e o w t m o r f s e r u t i d n e p x e t n e r r u c l a t o t f o t n e c r e p 7 n a h t s s e l , y n o m i s r a p r o F . d o i r e p l e p m a s e h t g n i r u d s e i r o g e t a c b u s l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / / f e d u e d p a r t i c e - p d l f / / / / / 1 7 1 1 1 9 7 7 6 2 4 e d p _ a _ 0 0 3 2 7 p d . f f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 . m e h t n o t c e f f e y n a e v a h o t n w o h s t o n s i t i m i l x a t e h t e s u a c e b i n h t i w s e r u t i d n e p x e t n e r r u c l a t o t n i s e i r o g e t a c e r u t i d n e p x e f o s e r a h s t n e c r e p e h t e t a c d n i i s e s e h t n e r a p n i s r e b m u n e h T . ) 9 1 0 2 D E S Y N ( t n e m t r a p e D n o i t a c u d E e t a t S k r o Y w e N n o d e s a b e r a s n o i t i n fi e d e h T : s e t o N s e i r o g e t a c b u S d n a s e i r o g e t a C e r u t i d n e p x E f o s e r a h S d n a s n o i t i n fi e D . 4 e l b a T 16 Phuong Nguyen-Hoang and Pengju Zhang Table 5. Parametric Results ε = 2% ε = 1% ε = 0.1% Current Expenditure Current Expenditure Current Expenditure with Benefits Excluded Key variables (1) (2) (3) (4) (5) (6) D (= 1 if DL (cid:2) ε and 0 otherwise) Pre-trend (P) Post-trend (T) With aid 0.0029 (0.003) 0.0026 (0.005) 0.0033 (0.005) Yes −0.0017 (0.002) 0.0011 (0.003) 0.0010 (0.003) Yes −0.0026 (0.002) −0.0020 (0.002) −0.0041* (0.002) −0.0023 (0.002) −0.0018 (0.002) −0.0038* (0.002) −0.0053* (0.002) −0.0030 (0.002) −0.0070** (0.002) −0.0050* (0.002) −0.0028 (0.002) −0.0068** (0.002) Yes No Yes No Notes: There are 4,630 observations. The dependent variables are the logged total current expenditures per pupil in columns 1 to 4 and non-benefit current expenditures (total current expenditures − benefits defined in table 4) per pupil in columns 5 and 6. Estimates are obtained with year and district fixed effects as well as all control variables in table 2. Robust standard errors clustered at the school district level are reported in parentheses. *p < 0.05; **p < 0.01. the groups with the highest and lowest instructional shares of total current expendi- tures: urban high-need at 61.5 percent versus rural high-need at 55.3 percent. Another difference of similar size comes from the shares of teacher salary in instruction: 60.3 percent for low-need districts versus 53.8 percent for urban high-need districts. 7 . R E G R E S S I O N R E S U LT S Table 5 reports the DID regression results for the first research question. The results in columns 1 through 3 are obtained with state and federal aid per pupil and with different values on ε. Column 1 shows that when at-limit districts are defined as those with ε = 2 percent, the coefficient on D is positive but not statistically significant. When ε = 1 percent, D is still not statistically significant, but it becomes negative (column 2). Also, the post-trend variable, T, is not significant with these values of ε. Columns 3 through 6 report results when our preferred value of ε is 0.1 percent, or a proposed levy within 0.1 percent of the limit is used to define at-limit districts. In columns 3 and 4, while the negative coefficients of D remain insignificant, T becomes negative and significant. Its coefficient in column 3 indicates that an at-limit district spends 0.4 percent less each year in the wake of first exhausting their limit than what they would have spent absent the tax limit. Districts may find it hard to reduce spending on benefits, the major contractually binding category. With non-benefit current expenditures per pupil as the dependent variable, both D and T are significant in columns 5 and 6. The coefficients of D indicate that absent the limit, at-limit districts would have annually spent approximately 0.5 percent more on non-benefit current categories. Columns 4 and 6 show that state and federal aid have a negligibly offsetting effect on the property tax shortfall among at- limit districts, evidenced by slightly smaller (in absolute value) coefficients of D and T relative to those in columns 3 and 5, respectively. Finally, the insignificance of the pre-trend variable, P, provides statistical evidence that the common trend assumption holds for all six columns. l D o w n o a d e d f r o m h t t p : / / d i r e c t . m i t . / / f e d u e d p a r t i c e - p d l f / / / / / 1 7 1 1 1 9 7 7 6 2 4 e d p _ a _ 0 0 3 2 7 p d f . f b y g u e s t t o n 0 7 S e p e m b e r 2 0 2 3 17 Cap and Gap: Tax Limits in New York Table 6. Nonparametric Results with the Event-Study Design ε = 0.1% ε = 1% Current Expenditure Current Expenditure Current Expenditure with Benefits Excluded Current Expenditure with Stacked Data Current Expenditure Key Variables Four or more years before t0 (T−4) Three years before t0 (T−3) Two years before t0 (T−2) One year before t0 (T−1) One year after t0 (T1) Two years after t0 (T2) Three years after t0 (T3) Four years after t0 (T4) Five years after t0 (T5) With aid Observations (1) 0.0082 (0.009) 0.0036 (0.006) 0.0006 (0.004) −0.0017 (0.002) −0.0066* (0.003) −0.0080* (0.004) −0.0122* (0.005) −0.0135* (0.007) −0.0245** (0.009) Yes 4,630 (2) 0.0068 (0.009) 0.0031 (0.006) 0.0001 (0.004) −0.0019 (0.002) −0.0062* (0.003) −0.0073 (0.004) −0.0112* (0.005) −0.0121 (0.007) −0.0234* (0.009) No 4,630 (3) 0.0096 (0.010) 0.0070 (0.007) 0.0031 (0.005) −0.0003 (0.003) −0.0096** (0.003) −0.0124** (0.005) −0.0198** (0.007) −0.0233** (0.008) −0.0376** (0.011) No 4,630 (4) 0.0090 (0.006) 0.0057 (0.005) 0.0033 (0.003) 0.0018 (0.002) −0.0042* (0.002) −0.0060 (0.003) −0.0089 (0.005) −0.0110 (0.006) −0.0174* (0.008) No 12,121 (5) −0.0098 (0.016) −0.0013 (0.012) −0.0044 (0.008) −0.0066 (0.004) −0.0041 (0.004) −0.0033 (0.007) −0.0003 (0.011) −0.0014 (0.014) −0.0010 (0.017) No 4,630 Notes: The dependent variable is the logged total current expenditures per pupil for all columns, except for column 3, where the dependent variable is non-benefit current expenditures per pupil. An event is defined as when a district’s property tax levy is at limit with ε = 0.1 percent. Estimates are obtained with year and district fixed effects as well as all other control variables in table 2. Robust standard errors clustered at the district-cohort level for column 4 and at the school district level for other columns are reported in parentheses. *p < 0.05; **p < 0.01. As discussed earlier, the DID regression results in table 5 are likely to be biased by endogeneity. Table 6 shows event-study results to address the endogeneity. With ε = 0.1 percent, similar to the results in table 5, columns 1 and 2 in table 6 report little dif- ference in the coefficients estimated with or without intergovernmental aid. A major reason for such a minor difference could be the current state education aid formula en- acted in 2007 does not factor in potential fiscal effects of a state-imposed TEL measure on school districts.14 Column 2 (without aid) shows that at-limit districts’ total current expenditures are reduced by 0.6 percent in the first event year and the reduction in- creases in size over the next four years. By year 5, the tax cap results in a cumulative reduction of 2.3 percent in at-limit districts’ expenditures.15 Column 3, where the depen- dent variable is non-benefit current expenditures per pupil, shows a similar declining trend but with larger reductions. Figure 4 visualizes the increasingly constraining ef- fects of the tax limit on total current expenditures and non-benefit expenditures over the years. 14. In fact, during the period of 2013–17, the average annual change in state aid per pupil for at-limit districts in year t > t0 is $477, which is even lower than that for never-at-limit districts and at-limit districts in year t ≤ t0 ($496).

This difference is not statistically significant, aunque.

15. We also test whether the tax cap has differential effects on school districts that were at limit in all five years (2013–

17) and on those that were at limit less than five years. The coefficients of T1 to T5 in this test are similar in size

and significance both for these two at-limit district groups and to those in column 2 de mesa 6.

18

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

/

F

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi

d

pag

_

a

_

0

0

3

2

7

pag

d

.

F

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

Phuong Nguyen-Hoang and Pengju Zhang

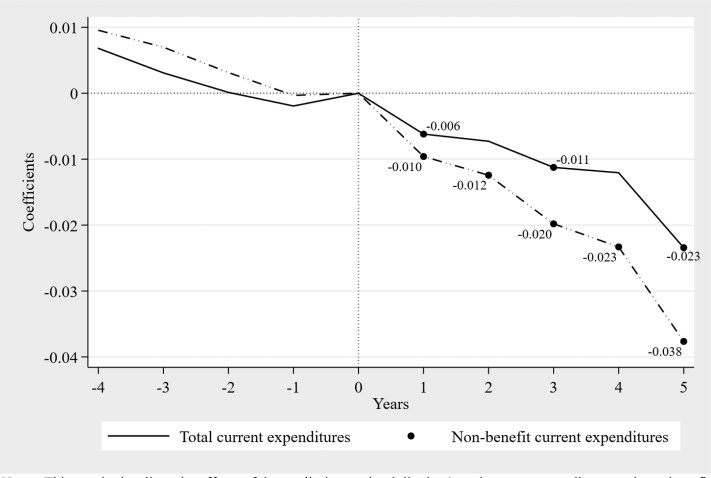

Notas: This graph visualizes the effects of the tax limit on school districts’ total current expenditures and non-benefit current expen-

ditures per pupil, reported in columns 2 y 3 de mesa 6. A black circle indicates a significance level of at least 5 por ciento.

Cifra 4. The Effects of the Tax Limit on Total Current Expenditures and Non-Benefit Current Expenditures

We conduct two additional robustness tests by using stacked data and ε = 1 por ciento.

The results prove to be robust to a certain degree when within-district multiple events

are taken into account with stacked data. Compared with column 2, the coefficients of

T1 through T5 in column 5 de mesa 6 are slightly smaller in absolute value, and those

of T2 through T4 are significant only at 10 por ciento (although not indicated by any aster-

isk). Given ε = 1 por ciento, none of the coefficients is significant (columna 5 de mesa 6),

providing evidence that the 1 percent distance to limit is so large as to include many

unconstrained districts. In all columns, the pre-trend variables (T−4 to T−1) are not sig-

nificant, providing statistical evidence to support the common pre-trend assumption.

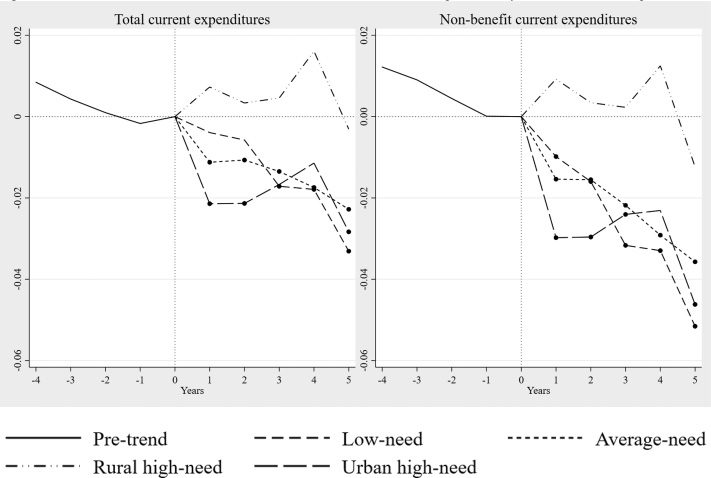

Mesa 7 reports empirical results for the second and third research questions. Columna-

umn 1 shows the differential effects of the tax limit on the total current expenditures of

four district groups. Of the four groups, only rural high-need districts are not affected

by the tax limit. This finding makes sense given these districts rely the least on property

tax levy (31 percent of their total revenue, as shown in column 2 de mesa 1). Por el contrario,

the tax limit has expenditure-stifling effects on the other three district groups. Absent

the tax limit, at-limit average-need districts’ annual total current expenditures would

have been from 1.1 por ciento a 2.3 percent higher in all five limit years. The tax limit,

sin embargo, reduces total current expenditures for at-limit low-need and urban high-need

districts in only three of the years. The left panel of figure 5 clearly depicts the declining

trends for the three limit-affected district groups.

Columna 2 de mesa 7, which is visually represented in the right panel of figure 5,

shows the size and significance of the effects of the tax limit on non-benefit current

expenditures are stronger for the three top-panel groups. In the first two years, urban

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

/

/

F

mi

d

tu

mi

d

pag

a

r

t

i

C

mi

–

pag

d

yo

F

/

/

/

/

/

1

7

1

1

1

9

7

7

6

2

4

mi