BLOCKCHAIN AND

PROPERTY IN 2018

AT THE END OF THE BEGINNING

j. MICHAEL GRAGLIA AND CHRISTOPHER MELLON

Before considering the evolution of blockchain for land governance, it is

important to consider wider developments in the blockchain ecosystem of

which it is a part. Many of the technical and legal obstacles highlighted in this

paper, such as the lack of interoperability and legal recognition of digital signa-

turas, are being addressed for other use cases. The widespread adoption of

blockchain is not only a question of technical development, but of the degree

to which society embraces the sort of decentralized governance models that it

can orchestrate. Blockchain is unusual in that it is a social technology, designed

to govern the behavior of groups of people through social and financial incen-

tives. It is therefore inherently political in a way that few other technologies are.

This quality has swept blockchain into the growing debate over reforming the

power structures that govern the digital world.

It was the Russian interference in the

2016 A NOSOTROS. presidential election that elevat-

ed this previously obscure issue to a

prominent place in the public discourse.

The fundamental problem that has been

identified is that the consolidation of

power in the hands of a few tech giants

has become socially and politically dan-

gerous. Proponents of this idea point to a

variety of ills arising from the centralized

control of data and of the attention econ-

omy in which it is generated, collected,

and sold. These include the exploitation

of social media marketing by political

influence operations, the promulgation of

extremist content, algorithmic bias,1. y

the monetization of attention.2.

A few companies, notably Facebook

and Google, effectively control the online

marketplace of ideas. Como resultado, they find

themselves responsible for, among other

cosas, policing speech on their platforms.

But despite having accumulated powers

previously diffused amongst the media,

gobierno, and civil society, these plat-

forms are privately governed. And as for-

profit enterprises, their interests are

aligned not with those of the public, pero

with those of the shareholders to whom

they are accountable.

Además, the problem is inherently

difficult to correct. The ubiquity of these

platforms makes it hard for even the most

socially-conscious users to “vote with

90

innovaciones / Blockchain for Global Development

Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023

their feet” by choosing alternatives that

better reflect their values. For many peo-

por ejemplo, the cost of leaving Facebook is pro-

hibitive, as they would have to leave

behind the data that comprise their

online social connections and identity. Él

is similarly difficult for regulators to

address the problem, as increasing com-

pliance costs could lock the dominant

companies into a permanent hegemony.

At a recent New America event, “Who’s

Afraid of Online Speech?” Sen. Amy

Klobuchar and Rep. Ted Lieu discussed

the difficulty of legislative solutions. Como

Rep. Lieu noted, the U.S. gobierno

could require social media platforms to

review posts and ads for fake news and

extremist content, but while Facebook

and Google could bear the subsequent

hiring costs, startups would be priced out

of the market.3.

One clear solution would be to

decentralize control of the information

economía, beginning with open protocols

for personal ownership of digital identi-

ties and user data. This would make per-

sonal data portable, allowing users to

bring their data to the platforms of their

choosing. More importantly, current

advertising-based revenue models would

be upended. Further decentralization of

the Internet, including the Domain Name

System and file storage, would have addi-

tional advantages, including increased

privacy,

y

resilience against data breaches (p.ej., el

Equifax breach) and Distributed Denial

of Service attacks.

censorship-resistance,

Though the movement to decentral-

ize the Internet has existed for some

time—and has prominent advocates

including Sir Tim Berners-Lee, inventor

of the World Wide Web, Internet pioneer

Vint Cerf,4.

y

Foundation—it has suffered from a lack

of resources, both financial and techno-

logical. In the decade since its introduc-

ción, blockchain has emerged as the best

candidate to solve these problems by

attracting investment and enabling open,

the Mozilla

ABOUT THE AUTHORS

Michael Graglia is the Director of the Future of Property Rights program at New America.

Graglia comes from a career in international development and strategy that has seen him in

finance at the Gates Foundation, program evaluation at BCG, developing a global tertiary

education network at the World Bank Group, managing a national refugee program for the

International Catholic Migration Commission in Zimbabwe, and teaching math in Peace

Corps Namibia, where he founded a scholarship program to fund women’s education.

Graglia has an MBA from Columbia University, where he was a Bronfman Fellow, an MA in

Southeast Asian studies from Johns Hopkins SAIS, where his studies were supported by the

Pablo & Daisy Soros Fellowship for New Americans. Graglia studied mathematics and comput-

er science at Gonzaga University, S.J.

Christopher Mellon is a Policy Analyst with the Future of Property Rights program at New

America. Previously, he was a researcher with New America’s International Security pro-

gram, where his work focused on international hostage-taking. Prior to New America, Mellon

worked as an IT contractor for the U.S. Department of Defense. He is a graduate of St. John’s

College, Annapolis.

© 2018 j. Michael Graglia and Christopher Mellon

innovaciones / volumen 12, number 1/2

91

Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023

j. Michael Graglia and Christopher Mellon

decentralized applications. As Steven

Johnson wrote in a January 2018 Nuevo

York Times Magazine article, “right now,

the only real hope for a revival of the

open-protocol

el

ethos

blockchain.”5.

lies

en

Decentralizing the Internet would

involve solving some of the most chal-

lenging prerequisites outlined in this

paper, including digital identity. It would

also require a great deal of investment in

blockchain infrastructure and standards,

the lack of which is commonly cited as the

greatest obstacle to the creation of an

Internet of Value. Además, it would

necessarily be accompanied by an attitude

shift towards comfort and familiarity with

decentralized governance structures.

It is not certain that the open, decen-

tralized ethos will prevail.6. The repeal of

net neutrality protections may be taken as

a sign that the current political climate

does not favor a move away from corpo-

rate control. And in 2017, Google became

the largest corporate lobbyist in the

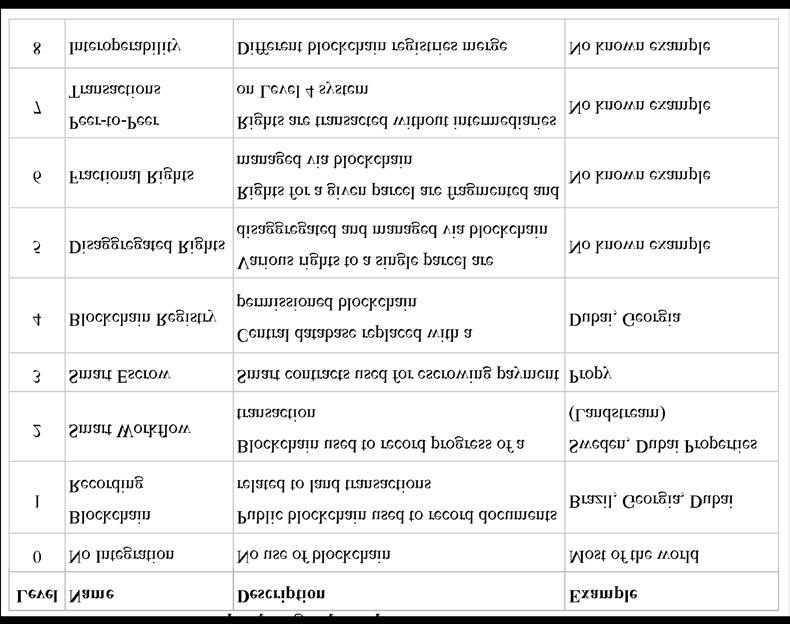

United States, “allocating more than $18 million to lobby Congress, federal agen- cies and the White House on issues such as immigration, tax reform, and antitrust. It also spent money to weigh in on an effort by lawmakers and regulators to reg- ulate online advertising, which is at the core of Google’s business, according to disclosures filed to the Senate Office of Public Records.”7. On the other hand, these trends are a powerful argument for accelerating the development of open protocols and decentralized applications. Concern over the negative influence of the Internet giants is creating some pressure to change their business models. In February 2018, Europe’s seventh- largest company, Unilever, announced it would stop advertising on that Facebook and Google if they did not take steps socially -responsible.8. In a speech at the IAB Annual Leadership Meeting in Palm become more to Desert, California, Unilever CMO Keith Weed said, “it is acutely clear from the groundswell of consumer voices over recent months that people are becoming increasingly concerned about the impact of digital on wellbeing, on democracy— and on truth itself,” and that “2018 is either the year of techlash, where the world turns on the tech giants—and we have seen some of this already—or the year of trust. The year where we collec- tively rebuild trust back in our systems and our society.”9. This rhetoric accompanied the announcement that Unilever and IBM were partnering on “the first Blockchain solution for media buying,”10. but its invo- cation of trust is still significant. It is true that the information economy is under- going a crisis of trust. The question is whether trust will be restored by the tech giants reforming themselves to suit the demands of the current political climate, or if it will be created by the blockchain “trust machine.”11. If it is the latter, and it is decided that the digital world—in which our time, our money, and our increasingly social relationships are invested—must be governed in accor- dance with the sort of open and demo- cratic values we insist upon in the non- virtual world, then the result will be an environment that is better prepared to accommodate the more radical scenarios described in this paper. BLOCKCHAIN MAKES SENSE FOR REAL ESTATE Driven primarily by private-sector invest- mento, blockchain-based technologies are being developed to address a number of land and property related challenges. This paper examines how those technologies have been applied to land registries and real estate to date and considers how blockchain and registries may evolve going forward.12. 92 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning High-friction transactions are hard- wired into the structure of modern real estate markets. As a result, legacy infra- structure in the sector is slow, expensive, and brittle. For the median home sold in the United States, transaction costs can constitute up to 10% of the total sales price. Entire industries have emerged for the sole purpose of capitalizing on the inefficiencies of property transfers. The situation in less developed markets is often even more cumbersome. Real estate transactions currently depend on a number of intermediaries, including brokers, government property databases, title companies, escrow com- empresas, attorneys, inspectors, appraisers, and notaries. In the short term, sharing contracts and approvals in real time will reduce delays caused by mailing and delivery. En efecto, Goldman Sachs estimat- ed that blockchain technologies could lead to an annual savings of $2-$4 billion in the real estate title insurance market alone.13. It would also eliminate the need for parties to reconcile documents, as all parties maintain an identical, immutable copy. and smart In addition, many time-consuming, expensive functions can be replaced with blockchain contracts. Payments of rent, deposits, and fees could be automated. Escrow accounts could be redesigned around smart contracts and multisig wallets. The same infrastructure could be harnessed for other transactions that occasionally require resolution by a neutral party, such as disputes over rent deposits. In the longer term, blockchain-based registries could allow peer-to-peer asset transfers, reducing transaction times from months or weeks to minutes. Transaction costs could come down from thousands of dollars per sale to a modest service fee. The ease and security of transactions efficient14. also permit the could unbundling of property rights. A landowner could sell an easement to a neighbor quickly and cheaply. Investors could buy small shares in a rental proper- ty and receive their portion of the rent via an automated payment. This could allow individuals that cannot afford to buy entire parcels to invest relatively small amounts of money in real estate. This trend could have vast implications for financial inclusion, creating an interna- tional market for small real estate invest- ments spread across multiple jurisdic- ciones. Cross-border real estate investment is already projected to grow to over 50% of all real estate investment by 2020, and the emergence of blockchain could ampli- fy this trend by introducing a class of real estate investors not limited by geogra- phy.15. Because it is decentralized, fault toler- ant, and virtually immutable, blockchain offers security and resilience advantages over traditional transaction and record- keeping systems. Records could be more resilient, as there would be no single, cen- tralized repository vulnerable to destruc- ción, as occurred in Haiti when “an untold number of title deeds and land registry records” were destroyed in the 2010 earthquake.16. Fraud and error created by new transactions could also be reduced with an immutable ledger that tracks all trans- comportamiento. This opportunity will have signif- icant implications for national land reg- istries and title insurance. The need for title insurance will be reduced, as proof of ownership can be established indelibly on the blockchain. The creation of more complete and reliable property records will provide a hugely valuable tool foran- alysts, regulators, and land-management officials. Por último, we believe the ability to promote property rights formalization, registry modernization, and the collection and analysis of land-related data makes blockchain a disruptive technology for innovations / volumen 12, number 1/2 93 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon land governance. PREREQUISITES FOR BLOCKCHAIN INTEGRATION As we wrote in 2017, there are a number of prerequisites that need to be in place before blockchain can be integrated into a registry.17. These are: • • • An identity solution Digitized records Multiple signature (“multisig”) wal- lets A private or hybrid blockchain18. Accurate data Connectivity and a tech-aware pop- • • • ulation • A trained professional community Below we briefly review these points with some updates from the initial writing. Those already familiar with this work are encouraged to turn to page 98, where we introduce the levels of integration we anticipate once these prerequisites are satisfied. An identity solution Registries tell us who has what rights to which asset, so knowing the “who” is crit- ical. Land and buildings can be tied to a registry via maps, deeds, and surveys. Those documents can be connected to the chain via hashes, but how to validate identity? At the moment, we are only aware of one blockchain-based national ID system, SecureKey in Canada, which launched in 2017.19. Certainly, with Ukraine and Dubai’s stated intentions of having their entire government “on chain,” they may also be developing something.20. Decentralized blockchain-based identity platforms are being developed and may soon be viable options for reg- istries. These include uPort, Civic, y, for those without personal devices, EverID. We do not suggest waiting for these systems; bastante, a registry must leverage an existing digital identity sys- tema. In the Swedish pilot, Por ejemplo, the large telecom company Telia provided the digital keys to verify identity.21. In India, the Aadhaar identity platform is a logical choice.22. Estonia also has a robust non- blockchain system.23. In the U.S., one could imagine Login.gov, the Social Security Administration, or a state’s DMV providing verification of identity to a registry.24. It is far better to use an existing, vali- dated identity system than to create a new one just for a registry. This is both because identity management is a separate skill set and because using an established system or systems (if a federated identity verifica- tion approach is used) will result in higher quality information. Noel Taylor points out that, while “verification of identity is certainly a paramount requirement for the system to work, imposing a digital ID requirement on all who transact in the system will impede progress into develop- ing is not if addressed.”25. We agree, but insist that digital identity must be solved first. SDG 16.9 aims to provide everyone with a legal identity by 2030.26. We hope this goal is met because it will get us closer to more people enjoying increased tenure security. countries equality Registries must be digitized A hash “is a mathematical algorithm that maps data of arbitrary size to a bit string of a fixed size (a hash) and is designed to be a one-way function, eso es, a function which is infeasible to invert.”27. One of the properties of hashing is collision resist- ance, where it is hard to find two inputs that produce the same hash.28. Another quality of hashing is that even the slightest change to a digital file will produce a dif- ferent hash—even file format has to be consistent.29. By hashing a document and posting that hash to a public chain, it is 94 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning verifiably timestamped without being published. You cannot hash a paper doc- umento, though.30. You can scan a docu- ment and hash the scan; any subsequent scan, sin embargo, would have a different hash, due to minute differences. Everyone would need the same copy in the same format in order for the hashes to agree. And that empowers blockchains to mitigate against the alter- ation of records. So we recommend that a registry be completely digital before blockchain is integrated. Note that both Sweden and Georgia had fully digitized systems before incorporating block- chain.31. is hashing it Multiple Signature Wallets What happens if someone steals your key? What if you lose your key? What if someone holds a gun to your head and makes you sign over your house to them digitally without actually taking the key? The public-private encryption keys built into blockchain ensure that only those holding the associated keys can register or transfer a property. But if keys are lost or stolen, there must be recourse to recover the property associated with them. The issue of legal recourse is discussed in an upcoming prerequisite, but one clear mit- igation, if not solution, is multiple signa- tura (“multisig”) wallets. These wallets require verification by a minimum num- ber of keys, rather than a single key, before a transaction is completed. Instead of a seller simply pressing a “sell” button, a registry could require both a seller and a banker (or registrar) to sign off on the transaction. Multisig can be configured in any number of ways, requiring, for exam- por ejemplo, two of two, two of three, or three of five designated signers. Some suggest a notary should be used as a second signer, but we disagree. There is no reason to shackle blockchain-based platforms to outdated systems already in decline.32. Notaries are part of the system of middlemen and gatekeepers that is receding in the face of technical innova- ción. In the United States, por ejemplo, notaries were historically used to vouch for identity, which modern identity sys- tems may not require. Other stakeholders who have a vested interest in valid trans- actions—bankers and registrars, for instance—can act as second signers. Once identity is confirmed and all transactions are put in an immutable ledger, there is no need for a human notary in a blockchain-enabled process, much less a justification for the associated costs. Those who excitedly envision direct, peer-to-peer exchanges of real estate and unbundled property rights may groan at the suggestion of multisig wallets, but for most homeowners that dream is more like a nightmare.33. Despite the Parity multisig hacks, which were due to poor coding, we believe that multisig wallets will be secure and will prevent more prob- lems than they will cause by the modest delays associated with their use.34. Use a private or hybrid blockchain format is no universal There for blockchain-based registries, at least not yet, but we expect that they will all employ a private blockchain in some form. There are at least three good reasons for thi s:35. a. The judiciary and registrar must be able to adjust the ledger On a public chain (BTC, ETH) there is only a record of the transactions by two willing parties identified by their public keys,36. as well as any comments appended to their transaction. Generally, if fraudu- lent data was entered and discovered, the only recourse for correction is another transaction reversing the prior entry. If a court rules that one spouse gets the house, innovaciones / volumen 12, number 1/2 95 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon but the other spouse does not want to transfer ownership, what happens? If someone loses their key or dies without communicating their key to another, how is ownership reallocated? What about expropriation of privately held lands for construction of public infrastructure? On a public chain, all of these questions are difficult to answer. But in a hybrid chain—where decisions are tracked on a private chain with hashes of key docu- ments recorded on a public chain—they can be addressed by granting appropriate authorities to the registrar and judiciary, which is critical when managing real assets.37. This could take the form of a spe- cial kind of multisig wallet where an ombudsman has a key allowing it to cre- ate reverse transactions on the private chain. Accenture has made a similar observation in the context of financial services.38. What happens if these authorities are abused? While this is a risk, one of the appeals of the blockchain is that it is a reg- istry of all transactions. So while we advo- cate for exceptional authorities to issue new keys and create reversing (rather than overwriting) transactions where mandated by law, we do not suggest that this should be done in secret. Since all transactions will be recorded to the pri- vate chain and be visible to those with access, if configured appropriately, it will be far easier to identify and correct any abuse of authority. b. Public chains cannot handle the volume of data involved Registries contain deeds, títulos, maps, planes, etc.. All of these documents must be stored somewhere. Public blockchains cannot viably store such large amounts of data. Decentralized storage and transfer systems like IPFS, Swarm, Sia, Storj, and Maidsafe may solve the problem in the future, but they are still in the early stages of development and therefore are not ready to be entrusted with a property reg- istry.39. Registries can store the documents on a regular server and post the associated hashes to a public blockchain, but if a blockchain-based record of the actual data is desired, registries will need to use a private blockchain. C. Anonymity is not an option Registries need to know who is registering or transferring property records. Public blockchains allow anyone with the correct keys to broadcast valid transactions, regardless of who or what they are. A pri- vate blockchain is needed if registries want to ensure that only parties who have validated their identity to the satisfaction of the authorities are transacting. If noth- ing else, in jurisdictions with property tax, the tax authority may want more than a public key to hold liable for taxes. Registries should be as accurate as possible One of the merits of a blockchain is its ostensible immutability, so it is important to make sure that any existing data that is transferred onto the blockchain is accu- rate.40. Jurisdictions looking to implement digital solutions are in one of three situa- ciones: they have a paper registry, a digital registry, or a registry that was destroyed. All existing registries, whether digital or on paper, contain inaccuracies. Most causes of error are benign, but fraud and corruption always pose a risk. Simple administrative errors and property own- ers forgetting—or avoiding for tax opti- mization—to register changes also quick- ly cause outdated registries. Idealmente, the registry should be cleaned and current before it is put onto an immutable platform. The reality is that stopping to clean a registry risks creating disputes that would hinder a transition 96 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning for years. How bad is it if messy data is imported into a blockchain? Pulling a reg- istry into a platform that allows for more transparency and lower transaction costs could expedite and facilitate clean up. This is particularly true in the case of a paper registry. It is often challenging to find errors in the registry or cadastre until it is digitized—with a poorly managed registry it is difficult to cross-check claims. If a registry is in use, and functioning as the public record, it should be on the best available technology. If transitioning to a new technology surfaces erroneous or conflicting records, they can be addressed in a systematic manner. Records can be flagged, and a process giving all parties a voice can be initiated without delaying implementation. Si, sin embargo, the registry is riddled with errors, resources may be better utilized to address those errors before incorporating blockchain into the registry. Digital registries require connectivity and a tech aware population Before a registry adopts a digital platform, it should consider the costs and support requirements. An initial response may be that these additional costs make a project unattractive, but the counterargument is that a new system should eliminate a number of prospective operating costs. Blockchain software is complex, and the hardware requirements substantial. It is hard to imagine that most public agen- cies could take these responsibilities in- house. This is well-understood beyond the world of registries, hence the prolifer- ation of Infrastructure and Software as a Service models (IaaS & SaaS).41. These models allow parties to purchase servers and software on a subscription basis instead of making substantial initial capi- tal investments. We are seeing the same with Blockchain as a Service (BaaS),42. but this change in support model has budget implications, namely that while the upfront costs are avoided, they are replaced with recurring costs. The main- tenance and troubleshooting costs, cómo- alguna vez, shift to the vendor, which must be able to guarantee a very low rate of failure. And while proof-of-work public blockchains have proven robust, segundo- ary software like wallets, exchanges, and smart contracts can be soft targets for hackers. A professional level of quality assurance and quality control will there- fore be required. In jurisdictions where connectivity is limited or consumers are not comfortable with digital transactions, a blockchain registry may not be optimal. If the system is not already digitized, we suggest start- ing there and then revisiting blockchain later. Registry digitization alone is a chal- lenge. The Jamaican registry had to retrain employees and transform its office culture to make their new digital system work, and moving to a blockchain-based system will likely face similar chal- lenges.43. Train the professional community that interacts with the registry In the long run, some envision blockchain disintermediating many parties. In the near term, this is unlikely. Lawyers will still bring suits, judges will hear them, and real estate agents will offer value added services to clients who would prefer expert assistance. All of these parties will need to be trained on the new system in order for it to function properly. The importance of engaging the professional communities who will interact with the blockchain early on in the transition can- not be overlooked. Blockchain lawyers such as Andrew Hinkes remind us that lawyers will need to understand a number innovations / volumen 12, number 1/2 97 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon Table 1. Blockchain Property Registry Adoption Levels Source: Future of Property Rights program, New America of issues, including how to present records from the blockchain, how to interpret records, and how to harmonize evidence rules with output from the blockchain. To do any of those things, they will first need to be trained in the fundamental concepts, capacidades, and vocabulary of the blockchain. Even with a clear picture of the technical and structur- al requirements for a blockchain registry, a great deal of work will remain in the form of education and capacity-building. FRAMEWORK FOR BLOCKCHAIN-REGISTRY ADOPTION Once these prerequisites are satisfied, what does integration actually look like? How will it evolve? What does it mean to put a registry on the blockchain? There are different ways to integrate or apply blockchain to an immovable real property registry. Instead of enumerating each of these scenarios, we propose a progressive framework for how we see blockchain integrating with property registries over time. This progression is not envisioned due to limitations of the available tech- nology—whether blockchain or a tradi- tional database. Bastante, it is the complex- ity and resulting inertia of existing processes, compounded by implementa- tion costs, that makes a progressive approach most likely. In January 2014, SAE International launched the standard J3016 Taxonomy and Definitions for Terms Related to On- 98 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning technologies Road Motor Vehicle Automated Driving Systems.44. According to Car and Driver, this was done to allow “automakers, sup- pliers, and policymakers to classify a sys- tem’s sophistication,” because, “no two automated-driving are exactly alike.”45. A similar framework will benefit the developers and policymakers who are active in the space defined by the intersection of blockchain and land reg- istries. The progression is not as clear in this case as it is with autonomous vehi- cles, and it is unlikely to proceed in as lin- ear a fashion as the numbering may sug- gest. The levels represent increasing sophistication or complexity, as perceived by the authors. We propose eight levels. The first four envision the two most commons forms of and transactions: property lease/rental. Starting with level five, blockchain is seen as facilitating the dis- aggregation of different types of rights as well as their fractionalization. sale Level 0—No Integration Here we include all non-blockchain sys- tems, from informal land where there are no legal titles, to paper registries, to com- puterized registries that rely on a central- ized database. Level 1—Blockchain Recording This is useful in situations where notaries are not available, or where trust in the existing system is limited.46. Hashing is the process of taking any digital input— from a string of characters to a scan of a legal document like a deed or lease—and creating a unique output of fixed length.47. The hash of a document is often referred to as the digital fingerprint, a unique identifier. By storing this hash on a public chain—such as BTC or ETH—one creates an independently verifiable record of the existence of the document, in a specific condition, exactly when it was recorded via timestamps and ownership (or at least association) via public and private keys. In other words, the document has been virtually notarized and publicly record- ed.48. Some existing intermediaries are concerned by this practice; a group of European surveyors and notaries docu- mented some of these concerns at the World Bank in March 2017.49. Despite their concerns, we believe that the use of public blockchains to record key docu- ments is likely to continue. In jurisdic- tions where corruption is a concern, introducing a public record of hashes can make it significantly harder to falsify records. On the other end of the spec- trum, in countries where there are strong open data movements (Suecia, Estonia) or high degrees of transparency (Los países bajos), a public document registry may also be welcomed. Examples: Brasil (Ubitquity) and Georgia (Bitfury) are using the Bitcoin blockchain to notarize the sale of proper- ties.50. The Netherlands is also using blockchain for leases. The Dubai Land Authority has the most advanced use case we are aware of. Per the Gulf News, the Dubai Land Department: has created its blockchain system using a smart and secure data- base that records all real estate contracts, including lease regis- trations, and links them with the Dubai Electricity & Water Authority (Dewa), the telecom- munications system, and various property related bills. Dubai’s blockchain’s secure, electronic real estate platform incorporates databases, personal tenant Identity including Emirates Cards and the validity of residen- cy visas, and allows tenants to make payments electronically to write the need without innovations / volumen 12, number 1/2 99 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon cheques or print any papers. The entire process can be completed electronically within a few min- utes at any time and from any- where in the world, removing the need to visit any government entity.51. Level 2—Smart Workflow This is useful as a way to both speed up existing work processes and make them more transparent. Real estate develop- ment and transactions are often complex, involving numerous intermediaries and elaborate processes. By publishing the completion of each step of the transaction on a permissioned chain and making those events visible to other participants in the transaction, timelines can be com- pressed dramatically. Along with mid- transaction transparency, hand-offs between parties become easier since everyone is using the same workflow rather than integrating numerous existing systems, which often introduces errors. In the case of a real estate transaction, the steps—bank-approved credit line, offer accepted, deposit received, contract signed, etc.—involve numerous entities who need to interact and be certain that each has done their part. Collaborating via a blockchain will allow them to col- lapse the timeline and realize significant efficiencies. Another benefit of this appli- cation is that more members of an ecosys- tem engage with blockchain and as a result may become more comfortable with the technology, building support for deeper levels of adoption. In the case of real estate development, the documents required to develop a proj- ect—sales and purchase agreements, progress reports, and master plans—need to move back and forth between develop- ers and approving agencies.52. Having a trustless blockchain that can track these documents and increase visibility to all parties will expedite the process and reduce confusion. Examples: Sweden with ChromaWay are using the Bitcoin blockchain to nota- rize transaction documents.53. Australian banks Westpac and ANZ are working with IBM to use blockchain technology for commercial leases. Their white paper on the project is informative.54. For proj- ect development, Dubai Properties and ConsenSys have developed a proof of concept for a product called Landstream. It was presented at the Arab Land Conference in February 2018 and went into production in March 2018.55. Level 3—Smart Escrow Smart contracts replace escrow agents in level 3. An escrow is “a deposit of funds, a deed or other instrument by one party for the delivery to another party upon com- pletion of a particular condition or event.”56. When smart contracts were envisioned in 1995 by Nick Szabo, he defined them as “a set of promises, speci- fied in digital form, including protocols within which the parties perform on these promises.”57. So instead of buyers, sellers, and banks depositing deeds, down pay- mentos, and mortgage payments with a professional escrow firm, all of those things are digitized and entrusted to a small program that lives on a blockchain and transfers ownership when all condi- tions are satisfied. Aside from the clear implications of replacing a set of professionals with code, nivel 3 blockchain integration is signifi- cant because, as Andrew Hinkes argues, the impact of blockchains on contract law may minimize litigation exposure as well.58. Hinkes points out that oracles— external data sources upon which smart contacts may rely—remain a vulnerabili- ty. Oracles are susceptible to fraud or manipulation and although many proj- ects seek to address oracle information 100 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning sources, they have many moving parts where they can break, be faked, or be manipulated. Smart contracts open a Pandora’s box of legal issues if they do not behave appropriately. Ejemplo: Propy.com has used this approach to facilitate the purchase of an apartment in Ukraine by a buyer in California paying with Ether and PRO tokens.59. A detailed walkthrough of the transaction has been published.60. Level 4—Blockchain Registry In all the previous instances, we imagined that the property registries existed as independent, centralized databases, which are supplemented in some way by the blockchain: in level 1 as a time- stamped signature, in level 2 as a shared source of truth regarding a process, in level 3 as smart escrow. In level 4, we imagine that a private permissioned blockchain replaces the central database and stores the actual records.61. A private blockchain would be used to store the data for reasons of security, costo, selective privacy, and efficiency. The recording function, sin embargo, would still be per- formed on a public blockchain. This is not to say that all information would be private. Selective information from all transactions could made visible to a large number of participants, reducing the like- lihood of fraud or other undesirable behavior. These observers could also be given permission to suggest edits or updates to the data-set, creating a better- curated data set over time. This arrange- ment could include built-in incentives to reward useful contributions. Examples: Dubai is doing exactly this for their real estate documents.62. Georgia is in the process of implementing such a system.63. Level 5—Disaggregated Rights From levels 1 a través de 4, the rights in question will be ownership and occupan- cy, but once a blockchain becomes the registry, other possibilities present them- selves. In level 5, rights can be disaggre- gated and discretely managed via a blockchain. Various rights associated with a property would be freely negotiat- ed, using a blockchain system to track those transactions. Examples of other rights include, but are not limited to air, agua, subsurface, mineral, grazing, and easements. Level 6—Fractional Rights Fractional rights are when a specific right is shared or divided between multiple users. This is frequently brought up in discussions about blockchain and real estate, but it would be more difficult in practice without level 5 integration in place. Fractionalization of rights allows for numerous scenarios. In addition to rights of ownership or occupancy, rights to revenues resulting from different uses of the property could also be fractional- ized and traded. Fractional ownership in this context could be defined as multiple parties shar- ing the rights and responsibilities of own- ing a real asset (es decir., a house, a condomini- um, or a commercial building), much like multi-investor leases. Fractional occupancy could mean a number of things, depending on whether the right is divided in terms of space, tiempo, or both. Examples of fractional rights include rights to a room in a house, or a bed in a room, or a time slot for a bed in a room, or rights to occupy an apart- mento, water rights being shared by multi- ple companies, or other third parties shar- ing the water on a land with owners, etc.. Beyond dividing how a property is used, both the governance and invest- ment aspects can be allocated via innovations / volumen 12, number 1/2 101 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon blockchain. Buyers will purchase shares in an asset, which translate to a stream of payments, assuming the asset is leased (investment), and also provides certain rights or decision-making abilities (gobierno- ernance). This is technically possible without blockchain—see the Australian example of Brickx.com—but with blockchain, the costs of allocating, recording, and trading these rights would be considerably lower.64. Por lo tanto, we should expect various models for mint- En g, trading, and discarding these shares. Blockchains may also facilitate the scaling of the Brickx.com model. Ejemplo: ConsenSys has announced a project called Pangea (now Meridio), which will do what Brickx.com is doing via the Ethereum public chain.65. In the long term, this service may expand to allow fractional ownership of properties rather than shares of derived products. Level 7—Peer-to-Peer Transactions These exchanges can occur only after the adoption of a blockchain and the clarifi- cation of legal rights. En general, until levels 1-6 materialize, it is difficult to envision genuine peer-to-peer transactions with- out the presence of intermediaries. In the case of Brickx.com, the use of a blockchain to facilitate their model, instead of a centralized internal system, could offer a similar user experience but with faster clearing and lower fees. The real potential for this model becomes clear, sin embargo, when it is applied without an intermediary. Por ejemplo, if a home- owner desires capital, instead of securing a home equity line of credit (HELOC) from a bank, they could simply fractional- ize the rights to rent their house and enter into a long-term lease with themselves. The homeowner could then offer a frac- tion of the right to rental payments to any willing buyer via a smart contract. They would then be obliged to make payments to the owner of those rights (interés) until they paid off the initial cost (princi- pal). Said differently, a level 7 registry with fractional rights would allow for a DIY HELOC or a crowd-sourced, peer- to-peer mortgage. In both cases it remains to be seen how these fractionated rights will be treated by the courts when failure to meet an obligation triggers a conflict. Level 8—Interoperability This would be something of a Holy Grail—interoperability between multiple blockchain-enabled registries and levels of jurisdiction—whether it is Santa Clara and San Mateo counties, the Netherlands and Spain, or China and the U.S. It is important here to distinguish that we are not talking about level 3. Bastante, nivel 8 would be an actual peer-to-peer transac- tion between two blockchain-enabled registries. From a technology perspective, this would require some standardization of what defines a property on a blockchain between registries and blockchain firms in order to have a uni- fied definition for a physical space and its associated rights. The political and legal challenges to such transactions would be significant. The vision here entails the world’s property being managed on a large hybrid blockchain that came togeth- er by virtue of its interoperability. Another scenario could involve someone creating a blockchain that is capable of managing all the property in the world. BEYOND COLORED COINS The higher levels of our integration framework also require an appropriate digital instrument for conveying owner- barco. One solution for public blockchains is to use colored coins, cryptocurrency 102 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning tokens marked with metadata linking them to off-chain assets. The transfer of colored coins can in theory be used to represent transfer of the assets associated with them, but some legal scholars have concerns. An analysis by Rod Thomas published in the European Property Law Journal identifies two major obstacles to trading property with colored coins in common law jurisdictions.66. Primero, he argues that colored coins may be unable to convey ownership of a specific property because they are based on currencies, which are fungible. Thomas argues that incorporeal interests, like easements or rights-to-rent charges, could be transferred by coin, but property ownership should not. He argues further that there would be no adequate process for redressing loss of a specific asset like a house because if a transaction went wrong, damages could be claimed but ownership of the property could not be reassigned. The second issue Thomas identifies is that “competing claims” and “off-chain interests” would need to be recorded in the colored coin in order for it to allow secure transactions, and the owner of the coin cannot be trusted to be the gatekeep- es. An additional problem is that, depend- ing on the implementation, colored coins may only store a very limited amount of data. Some of the objections mentioned above are also mitigated by the use of pri- vate or hybrid chains with multisig wal- lets, which we argued in the prerequisites section were the best structure for blockchain registries. Similarmente, given that the higher levels introduce some com- plejidad, we believe it would be preferable to create a standardized, purpose-built digital instrument for representing and conveying property ownership on chain. Instead of colored coins, such a system might be a robust digital identity system that gave identities to humans, parcels, and buildings, and the blockchain and smart contracts to record the relationships between them. then used WHAT IS THE FUTURE OF BLOCKCHAIN FOR REAL ESTATE? that power There are a number of well-known tech- nical and legal obstacles to overcome in order for blockchain to be widely adopted in the real estate and land sectors. These include the lack of standard protocols for interoperability and the fact that the dom- inant public chains may perish, for a vari- ety of reasons, including regulation of the cryptocurrencies them. Transaction speeds must increase without compromising data security. If we foresee a world with numerous micro-transac- ciones, there must be adequate throughput speed to maintain it. This will depend in part on consensus mechanisms. Proof of Work has been very successful in large public chains, but it is slow and energy intensive. Ethereum’s Proof of Stake mechanism remains unproven. More U.S. states are moving to recognize smart con- tracts and blockchain records, but early bills are occasionally compromised by the inability of lawmakers to define those technologies with sufficient accuracy. The difficulty of these challenges should not be understated, but none of them is insurmountable and the potential for blockchain to improve land adminis- tration has generated a great deal of inter- est. In this section we explore the impact of blockchain on five areas: title insur- ance, legal reform, financial inclusion, grandes datos, and regulation. Each of these topics is too large to be explored in a single paper, so we have kept our remarks brief and focused only on key issues. innovaciones / volumen 12, number 1/2 103 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon What does blockchain mean for title insurance? Title insurance differs from other com- mon forms of insurance in that it insures against past, rather than future, events. It can be expected, por lo tanto, that if the his- torical property record can be made more reliable, risk will be diminished corre- spondingly.67. This makes title plants a very natural blockchain use case. A widely cited analysis published by Goldman Sachs in May 2016 concludes that the impact of blockchain on title insurance will be to make title plants more efficient, reducing the cost of premi- ums.68. Moat of the cost of title insurance comes not from actuarial risk but from fixed personnel costs, which “represent nearly 75% of industry premiums.”69. Title insurance companies can reduce these costs by using blockchain to create thorough and accurate records databases, enabling more efficient title searches and reducing the number of defective titles they have to correct. Goldman estimates that total cost savings created by blockchain will result in 30% lower pre- miums for consumers. Curiosamente, they project that this will bring premiums across the U.S. in line with those in the state of Iowa, which is unique in having a state-run title insurance monopoly.70. While the Goldman report acknowledges that the use of blockchain will “clean” property registries over time, it does not envision a scenario in which title insur- ance becomes unnecessary. The question of whether a sufficiently comprehensive and reliable registry—for example, a blockchain registry that had been in place for decades—could eventu- ally remove the need for title insurance altogether is interesting. This seems unlikely to happen in the U.S. without significant legal reforms, because in most U.S. jurisdictions there are documents that affect security of title but do not have to be recorded. Además, documents can contain defects because they are not reviewed and validated by a responsible party prior to recording. As long as off- chain information can impact security of title, professional intermediaries will be required to perform due diligence and mitigate against risk, which is a barrier to peer-to-peer transactions. Under these circumstances, disintermediation is not desirable for the transacting parties, who would assume the risk themselves. The situation is different in Torrens jurisdic- ciones, where the registration of a certifi- cate of title is guaranteed by the state as proof of ownership and title insurance is usually not required. According to the American Land Title Association, Estados Unidos. title insurance industry “generated $14.3 billion in title

insurance premiums during 2016 com-

pared to $13.2 billion during 2015.”71. While there is broad agreement that blockchain will make the operations of title insurers more efficient, it is not clear what impact that efficiency will have on competition in the industry. The market is currently dominated by a handful of underwriters, with the top five companies having a 75% combined market share in the third quarter of 2017.72. Early adop- tion by a major player could lead to con- solidation in the industry as it out-com- petes and acquires its rivals. Though it seems likely that early adoption will be by established companies migrating their existing title plants to the blockchain, it is also conceivable that private blockchain registry and workflow management providers could eventually compete with them. A company providing a parallel registry and managing document exchange between the buyer, seller, banks, registry, attorneys, escrow agent, notary, and brokers might accumulate enough records to start its own title plant over time and offer title insurance through its platform. 104 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning Is Torrens a better legal framework for a blockchain registry? Most of the early blockchain-based real estate products have been oriented toward abstract title recording jurisdic- tions.73. Complex tasks like recording transactions, managing workflows, and researching chain of title create obvious opportunities for cost savings from increased efficiency. It could therefore be argued that there is currently less of an economic incentive for Torrens jurisdic- tions to adopt blockchain. But the oppo- site may be true when it comes to the higher levels of blockchain integration proposed in our framework, which involve increased decentralization and liquidity of assets. At those later stages the security and simplicity of Torrens title may offer significant advantages. In the short term, blockchain could reduce the time required to approve new title certificates in Torrens jurisdictions. In the long term, the adoption of blockchain registries could allow them to benefit from a greater degree of liquidity than could be achieved in abstract title jurisdictions, which include the majority of U.S. states and counties. Greater security of title is the primary advantage of the Torrens system. A cer- tificate of title is a government-backed guarantee of ownership, and it includes all encumbrances on the title document. This makes it easier to transfer ownership securely, and can greatly reduce the num- ber of title disputes that burden the legal system, especially in places with unreli- able or incomplete property records.74. This security would be especially signifi- cant for peer-to-peer transactions. The indefeasibility of Torrens titles would allow buyers to know the validity of the seller’s title and of their own claim once the transfer was registered, allowing digi- tal title certificates to function more like bearer instruments. When a legal claim is brought suc- cessfully against the holder of a Torrens title, the claimant receives monetary com- pensation from an indemnity fund and ownership of the property remains with the certificate holder.75. This means that there must be a pool of money set aside for the purpose of compensation. In places like Australia, where the Torrens system originated, the government col- lects this money from title registration fees.76. A blockchain-based registry could automate this function, collecting money for the compensation fund with transac- tion fees. It is not clear that these potential advantages would be enough to drive adoption of the Torrens system in the U.S. It is used to a limited extent in a number of states, including Minnesota, Washington, and New York, but was never widely adopted after its introduc- tion in the nineteenth century. This is largely because the expense of migrating a property in the U.S. to the Torrens system has been too great to justify. A sufficiently compelling justification may develop if property transactions become increasing- ly decentralized. Because of the cost and complexity of converting properties to Torrens title, this transition could not be done all at once. A more reasonable approach would be to move properties over to a parallel, blockchain-based registry over time. This could be achieved through incentivizing property owners to make the transition voluntarily, Por ejemplo, to gain access to an international market for fractionalized property or peer-to-peer sales to foreign investors. Alternativamente, the transfer could be prompted by a triggering event speci- fied by the registrar. The latter has been done in the United States before, if on a small scale. In Hennepin County, Minnesota, the registrar converts proper- innovaciones / volumen 12, number 1/2 105 Descargado de http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 j. Michael Graglia and Christopher Mellon ties to Torrens when they are repossessed for tax liens.77. For our purposes, the trig- gering event is less important than the effect, which would be to produce a grad- ual transition to Torrens titles on a blockchain registry. The idea that Torrens titles could be transferred and registered more easily and securely on a blockchain-based sys- tem depends on the willingness and abili- ty of the registrar to approve and register documents in a timely fashion. In their examination of the advantages and disad- vantages of Torrens title in the United States, the authors of The Earthen Vessel point out that because the registrar’s office is not particularly sensitive to mar- ket forces, the inherent delays of the time consuming review of the documents for legal sufficiency by the registrar’s office can be an unacceptable burden for those engaged in transactions. On the other hand, for the registration of records system, where the exam- ination of title is completed by private representatives of the parties to the transaction, market forces are a factor, and where necessary, the attorneys can complete the examination of title and the closing on a transaction, based upon the needs and expec- tations of the client, in a very short period of time.78. It should also be noted that jurisdictions may be reluctant to embrace the Torrens system because of the cost of assuming liability and maintaining the indemnity fund. But as is the case in the title insur- ance industry, this risk would be reduced by improving the quality of property records. We should also reiterate that the argument presented here in favor of Torrens title is predicated on the idea that more liquid property transfers will be a great enough economic incentive to justi- fy the disruption and expense of legal reforms. There are a number of reasons why this might not come to pass. It is pos- sible, Por ejemplo, that the overwhelming majority of blockchain-based transac- tions will be of property-backed invest- ments in which ownership is not trans- ferred. The broader question raised is whether some jurisdictions will stand to benefit more than others based on the degree to which their land laws map onto the characteristics of blockchain. Will blockchain and land drive financial inclusion? We should begin by emphasizing that, as Aanchal Anand, Matthew McKibbin, and Frank Pichel wrote in 2016, blockchain registries do not become significant for land governance until after land rights have been formalized: Simplemente pon, blockchain does not resolve the primary challenge of land administration faced in many emerging economies— how to bring citizens and prop- erties into the formal system. Blockchain will not help to iden- tify who has what right and to where. It will not resolve proper- ty rights disputes as properties are brought into the formal sys- tema. Most importantly it won’t resolve the tedious and time con- suming process of collecting, ver- ifying and bringing data into the system in the first instance.79. This is an important point, and as we described earlier, there are other prereq- uisites to blockchain registry adoption in addition to the existence of formal records. We do see the potential, howev- es, for commercially oriented real estate platforms to speed up the formalization process indirectly through the promise of 106 innovaciones / Blockchain for Global Development Downloaded from http://direct.mit.edu/itgg/article-pdf/12/1-2/90/705267/inov_a_00270.pdf by guest on 09 Septiembre 2023 Blockchain and Property 2018: At the End of the Beginning financial inclusion.80. Low-transaction- costo, low-barrier-to-entry platforms for accessing international property markets offer a powerful incentive for both gov- ernments and private companies to invest in the creation of modern and reliable property registries. Real estate investment would be a major addition to the list of inclusion opportunities enabled by blockchain, which include remittance services, mobile money, and economic identity. A 2016 market overview by the technology services company Cognizant estimated the “revenue generated by banks by 2020 within emerging markets from unbanked populations” at $380 bil-

lion.81. If blockchain-based real estate

markets can help to activate dead capital

in those markets, this number will be rad-

ically increased.

en

a

the company. According

There are already several companies

positioning

bring

ellos mismos

blockchain-based real estate solutions to

the developing world. The most ambi-

tious of these ventures may be De Soto

Cª, though little has been made public

acerca de

a

Overstock founder Patrick Byrne, a part-

ner in the venture, their goal is to put

títulos

the developing world on

blockchain in a format that will allow

them to be used as collateral for loans,

with the resulting capital being traded on

a tokenized market called tZERO.82. It is

unclear whether this is practicable, pero

does indicate that serious business inter-

ests in the developed world are aware of

the opportunity formalization represents

and see blockchain as a key enabling tech-

nología. Byrne has even considered selling

Overstock, which has a total market capi-