THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

Han Bleichrodt and Paul van Bruggen*

Abstract—Higher-order risk preferences are important determinants of eco-

nomic behavior. We apply insights from behavioral economics: we measure

higher-order risk preferences for pure gains and losses. We find a reflec-

tion effect not only for second-order risk preferences, as did Kahneman

and Tversky (1979), but also for higher-order risk preferences: we find risk

aversion, prudence and intemperance for gains and much more risk-loving

preferences, imprudence and temperance for losses. These findings are at

odds with a universal preference for combining good with bad or good

with good, which previous results suggest may underlie higher-order risk

preferences.

I.

Introducción

WHILE risk aversion has been the cornerstone of the eco-

nomic analysis of decision making under risk since the

1950s, only relatively recently have higher-order risk pref-

erences been receiving the attention they arguably deserve.

Although prudence as a concept has been used in the anal-

ysis of intertemporal risk preferences since Leland (1968),

Sandmo (1970), and Drèze and Modigliani (1972), specifi-

cally as a precautionary savings motive, the use of the term

comes from Kimball (1990). Temperance was introduced

even more recently, as a concept by Pratt and Zeckhauser

(1987) and as a term by Kimball (1992). Model-free defi-

nitions of prudence and temperance proposed by Eeckhoudt

and Schlesinger (2006) are illustrated in figure 1.1 Prudence is

equivalent to aversion to downside risks (Menezes, Geiss, &

Tressler, 1980), and temperance relates to whether the pres-

ence of background risk makes a person more risk averse

(Gollier & Pratt, 1996).

The importance of these preferences has been shown in

such different contexts as insurance in the presence of back-

ground risks (fei & Schlesinger, 2008), auctions (Es˝o &

Blanco, 2004), and probabilistic insurance (Eeckhoudt &

Gollier, 2005; Peter, 2017). Prudence also plays an impor-

tant role in explaining several macroeconomic consumption

puzzles through the precautionary savings motive it induces

(Caballero, 1990). Evidence of higher-order risk preferences

has been found with field data (Browning & Lusardi, 1996;

Received for publication October 25, 2018. Revision accepted for publi-

cation July 27, 2020. Editor: Brigitte C. Madrian.

∗Bleichrodt: Erasmus School of Economics and University of Alicante,

Departamento de Economía; Van Bruggen: Tilburg University, Departamento

of Economics.

We are grateful to Aurélien Baillon, Olivier l’Haridon, Gijs van de Kuilen,

and Peter Wakker for their comments on the manuscript; the editor, Brigitte

Madrian, and two anonymous referees for their suggestions and comments;

and Jingni Yang and Victoria Granger for helping us conduct the experiment.

The experiment reported in this paper was partially funded by contributions

from the Erasmus Research Institute of Management and the Tinbergen

Instituto.

A supplemental appendix is available online at https://doi.org/10.1162/

rest_a_00980.

1Higher-order risk preferences have been extended to multivariate risk

preferences (Eeckhoudt, Rey, & Schlesinger, 2007), to ambiguity (Baillon,

2017), and to time (Ebert, 2020). For an introduction to higher-order risk

preferences, see Eeckhoudt and Schlesinger (2013).

Carroll & Samwick, 1998), as well as in experiments (see the

review article by Trautmann & Van de Kuilen, 2018).

en este documento, we apply insights from behavioral economics

to the study of these higher-order risk preferences. Daniel

Kahneman called reference dependence “the core of prospect

theory” (kahneman, 2003, pag. 1457). Yet reference depen-

dencia, which leads to a reflection of risk aversion over the

gain and loss domain, has not been thoroughly investigated

or controlled for in existing studies. We measure higher-order

risk preferences while directly controlling the reference point

to separate gains and losses. We control the reference point

by giving subjects an endowment before the experiment.2

Separating gains and losses allows us to investigate

whether higher-order risk preferences, like risk aversion, re-

flect between the gain and loss domains. This is important

for two reasons. The first is external validity. Preferences

measured under gains in an experiment may be a poor pre-

dictor for choices that naturally involve losses, such as in-

surance and self-protection decisions. Decision makers may

purchase insurance that involves nonperformance risk despite

a prediction based on prudence observed under gains that

they would not demand such insurance (Eeckhoudt & Gol-

lier, 2005). Asimismo, prevention efforts are closely related to

prudence, and basing health policy on estimates of prudence

under gains may be suboptimal.

The second reason is that the domain will influence deci-

sions dependent on higher-order risk preferences. In a finan-

cial crisis, when their portfolios are deeply in the loss domain,

investors may come to prefer downside risks, and greater

volatility on the financial markets may lead investors to de-

mand insurance against unrelated risks where under more

normal circumstances, greater volatility on financial markets

has no such effect.

Separating gains and losses means we measure preferences

without loss aversion, which affects choices for lotteries that

mix gains and losses. Por ejemplo, if subjects take the high-

est possible outcome they are sure to get (the MaxMin) como

the reference point, loss aversion will bias responses toward

risk aversion, prudence, and temperance.3 Thus, we can test

the hypothesis of a preference for combining good with bad

or for combining good with good without the confounding

effects of loss aversion. Eeckhoudt, Schlesinger, and Tsetlin

(2009) and Crainich, Eeckhoudt, and Trannoy (2013) espectáculo

that these simple preferences may underlie higher-order risk

preferences, in which case decision makers who are risk

2Deck and Schlesinger (2010) and Maier and Rüger (2012) also had treat-

ments to investigate the influence of the domain on higher-order risk pref-

erences. We discuss these studies in section V.

3With such a reference point, the worst outcome between two lotteries is

perceived as a loss. This is always an outcome of the option that indicates

risk-loving preferences, imprudence, or intemperance. Loss aversion then

decreases the relative attractiveness of this option.

La revista de economía y estadística., Julio 2022, 104(4): 705–717

© 2020 The President and Fellows of Harvard College and the Massachusetts Institute of Technology. Publicado bajo una atribución Creative Commons 4.0

Internacional (CC POR 4.0) licencia.

https://doi.org/10.1162/rest_a_00980

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

mi

s

t

_

a

_

0

0

9

8

0

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

706

THE REVIEW OF ECONOMICS AND STATISTICS

FIGURE 1.—DEFINITIONS OF RISK AVERSION, PRUDENCE, AND TEMPERANCE

Risk aversion (arriba), prudence (abajo a la izquierda), and temperance (bottom right), based on Eeckhoudt and Schlesinger (2006), for all k, r > 0 and all zero-mean random variables ˜ε, ˜ε1, and ˜ε2.

averse should be temperate, whereas those who are risk lov-

ing should be intemperate, and both should be prudent.

We also measure higher-order risk preferences with lotter-

ies for which the branches in figure 1 involve probabilities

menor que 0.5.4 We extend the definitions of Eeckhoudt

and Schlesinger (2006) to such small probability lotteries

and show that the results of Eeckhoudt et al. (2009) apply to

a ellos.

We find a reflection effect for higher-order risk prefer-

ences: under gains, the majority of choices are risk averse,

prudent, and intemperate, whereas under losses, the majority

of choices are risk loving, imprudent, and temperate. The im-

prudence we find for losses and the combination of risk aver-

sion and intemperance for gains is at odds with the hypothesis

that a universal preference for combining good with bad or

good with good underlies higher-order risk preferences. Nosotros

find similar behavior for small probability lotteries and the

usual 50-50 lotteries.

In section II, we discuss the definitions of higher-order risk

preferences in detail and how these may be derived from pref-

erences for combining good with bad or good with good. Nosotros

also extend the definitions of higher-order risk preferences

so they can be used with smaller probabilities. We present

the design of our experiment in section III. In section IV, nosotros

present our results, which we discuss and relate to previous

findings in section V. Section VI concludes.

II. Theoretical Background

Eeckhoudt and Schlesinger (2006) define higher-order risk

preferences through simple lottery pairs. Dejar [X, y] denote the

lottery that gives outcome x with probability 0.5 and outcome

y with probability 0.5. Dejar (cid:3) denote the decision maker’s

preference relation. Risk aversion is defined as the prefer-

ence [−k, −r] (cid:3) [0, −k − r] for all wealth levels and for all

k, r > 0. Eeckhoudt and Schlesinger (2006) name such an at-

titude risk apportionment of order 2. A decision maker is risk

4Ebert and Wiesen (2011, 2014) use skewed zero-mean lotteries ( ˜ε in fig-

ura 1), which therefore involve probabilities smaller than 0.5, but the effect

of smaller probabilities there is confounded by a preference for skewness.

loving if the reverse preferences hold. To define prudence

(risk apportionment of order 3), the fixed deduction −r is

replaced by a zero-mean nondegenerate random variable ˜ε

(see figure 1). The decision maker is prudent if [−k, ˜ε] (cid:3)

[0, ˜ε − k] for all wealth levels, for all k > 0, and for all zero-

significar, nondegenerate random variables ˜ε. The decision maker

is imprudent if the reverse preferences hold. Temperance (riesgo

apportionment of order 4) is defined by replacing −k by an-

other independent random variable. The decision maker is

temperate if [ ˜ε1, ˜ε2] (cid:3) [0, ˜ε1 + ˜ε2] for all wealth levels and

for all zero-mean, nondegenerate, and independent random

variables ˜ε1 and ˜ε2. If the reverse preferences hold, the risk at-

titude is called intemperance. Risk attitudes of orders higher

than 4 can be defined through similar procedures, but we do

not study those attitudes in this paper.

Eeckhoudt et al. (2009) show how stochastic dominance

preferences lead to risk apportionment of any order. Ellos

show that if ˜xi dominates ˜yi, i = a, b, through ith order

stochastic dominance, then the 50-50 lottery [ ˜xa + ˜yb, ˜xb +

˜ya] dominates [ ˜ya + ˜yb, ˜xa + ˜xb] a través de (a + b)th stochas-

tic dominance. Stochastic dominance preferences thus im-

ply a preference for combining the “good” lottery with the

“bad” lottery and contain risk apportionment preferences as

defined by Eeckhoudt and Schlesinger (2006) as a special

caso. A preference for combining good with bad thus leads

to a combination of risk aversion, prudence, and temperance,

Por ejemplo.

Crainich et al. (2013) apply this logic to decision makers

who prefer combining good with good and show that this

leads to a combination of risk-loving, prudent, and intemper-

ate preferences. It follows that indifference toward combining

good with bad and good with good leads to risk neutrality,

prudence neutrality, and temperance neutrality. The results

above also hold when all final outcomes are only in the do-

main of gains (relative to some reference point) or of losses.

We can therefore test for these implications separately for

both domains to see if there are behavioral differences be-

tween them.

Because we also study preferences over lotteries involv-

ing probabilities different from 50-50, we need to extend the

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

mi

s

t

_

a

_

0

0

9

8

0

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

707

above definitions. Dejar (pag: X, pag: y, 1 − 2p: z) denote the lottery

that gives outcomes x and y with probability p and outcome

z with probability 1 − 2p. Risk aversion is then defined as

(pag: −k, pag: −r, 1 − 2p: C) (cid:3) (pag: 0, pag: −k − r, 1 − 2p: C),

prudence as

(pag: −k, pag: ˜ε, 1 − 2p: C) (cid:3) (pag: 0, pag: ˜ε − k, 1 − 2p: C),

and temperance as

(pag: ˜ε1, pag: ˜ε2, 1 − 2p: C) (cid:3) (pag: 0, pag: ˜ε1 + ˜ε2, 1 − 2p: C)

for all p ∈ [0, 1], all k, r > 0, all c, all independent zero-mean

risks ˜ε, ˜ε1, and ˜ε2 and all wealth levels. Risk-loving pref-

erences, imprudence, and intemperance are defined as the

reverse preferences. Under expected utility, these extended

definitions are equivalent to the usual definitions of risk aver-

sión, prudence, and temperance (necessity follows from the

independence axiom and sufficiency follows from their def-

inition). Además, the results of Eeckhoudt et al. (2009)

apply to these extended definitions: si [ ˜xa + ˜yb, ˜xb + ˜ya] dominación-

inates [ ˜ya + ˜yb, ˜xa + ˜xb] a través de (a + b)th stochastic dom-

inance, then the probabilistic mixture (λ: [ ˜xa + ˜yb, ˜xb +

˜ya], 1 − λ: C) also dominates (λ: [ ˜ya + ˜yb, ˜xa + ˜xb], 1 −

λ: C) a través de (a + b)th stochastic dominance (a proof is in

appendix A).

III. Diseño

We measure higher-order risk preferences in three treat-

mentos, two involving gains (with all outcomes positive addi-

tions to the initial payment) and one involving losses (con

all outcomes negative additions to the initial payment). A

induce a strong reference point, subjects face both gains and

losses relative to their initial endowment; we therefore have

a within-subject design for testing gains and losses. The two

gain treatments involve a between-subject design (subjects

were assigned randomly to either gain treatment). El 50-

50 gain treatment involves the usual 50-50 lotteries, y el

small probability gain treatment involves the small proba-

bility lotteries discussed in section II. The small probability

treatment allows us to offer the possibility of sizable gains.

For the loss treatment, we measure preferences using the

usual 50-50 lotteries. Small probabilities cannot be used to-

gether with large losses, because losses exceeding the ini-

tial endowment would lead to negative earnings. For each of

the three treatments, we measure three higher-order risk at-

titudes (risk aversion, prudence, and temperance). De este modo, nosotros

have nine treatment-risk attitude pairs in total.

To study the effects of reference-dependence, it is impor-

tant to control the reference point. Para tal fin, subjects were

given a 15 euro endowment at the start of the experiment.

They were told that this endowment was their payment for

participating in the experiment, that they could gain addi-

tional money or lose part of it, and that it was equal to the

expected value of participating. Throughout our analysis, nosotros

assume that subjects take the initial endowment as their refer-

ence point. This is a common assumption in the literature and

is consistent with a reference point based on rational expec-

taciones (K˝oszegi & Rabin, 2006) or based on the status quo.

Baillon, Bleichrodt, and Spinu (2020) find evidence that a siz-

able fraction of subjects take the status quo as their reference

punto, and Etchart-Vincent and l’Haridon (2011) find that be-

havior is similar under losses from an initial endowment and

losses out of subjects’ own pockets.

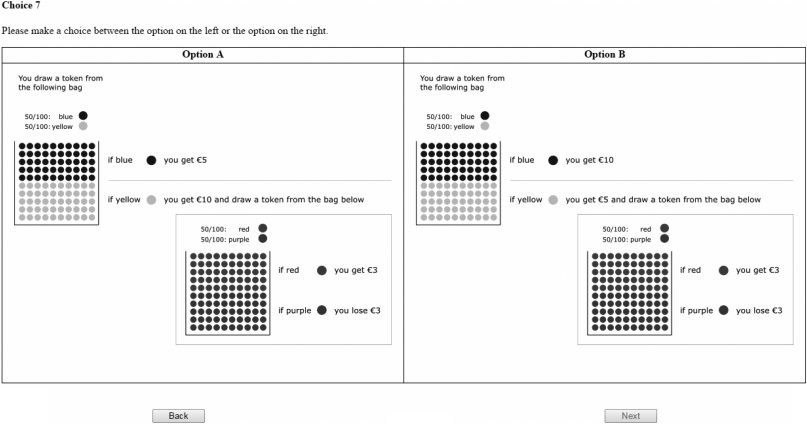

A screenshot of one of the tasks is in appendix B, y

the tasks are listed in table 6 in appendix C. Lotteries are

presented in compound form in all tasks. We use compound

lotteries because they most clearly present the choice as be-

tween combining good with bad or good with good. Haering,

Enrique, and Mayrhofer (2020) find that prudence and tem-

perance are stronger for compound lotteries than for reduced-

form lotteries. Deck and Schlesinger (2017) investigate pre-

senting lotteries in compound form and in reduced form and

find that while aggregate patterns are not much different,

individuals have different preferences between the different

formats.

Probabilities are presented as drawing a colored token from

a bag with 100 colored tokens. To avoid mixing gains and

losses, outcomes are chosen in such a way that relative to

the initial payment, they are always negative in the loss treat-

ment and always positive in the gain treatments. Hay

no zero outcomes (relative to the initial 15 euro) to prevent

possible effects such as loss and zero avoidance from influ-

encing responses. Subjects were presented with twelve tasks

for each risk attitude in a given treatment. The relatively large

number of tasks allows us to distinguish subjects who are

indifferent (or confused) from those who have a clear atti-

tude without having to measure willingness to pay. Measur-

ing willingness to pay would complicate the procedure while

the binary choices are already quite complex, especialmente para

temperance.

The experiment was performed in the ESE-econlab of the

Erasmus School of Economics. Subjects were randomly se-

lected from the ESE-econlab subject pool, which consists of

people who have registered to participate in experiments and

invited to sign up for sessions through an automated email

sistema. El 245 subjects who participated in the experiment

hecho 17,640 choices.5 Upon entering the lab, subjects were

given an envelope containing 15 euros and assigned a seat

in a cubicle. They started the experiment and left the lab at

the same time and made their choices on a computer. En el

instructions, they were informed that one of their choices in

the experiment would be implemented for real, which would

result in winning additional money or losing part of their ini-

tial payment, and that their expected earnings were equal to

5Del 245 subjects, 122 participated in sessions in January 2017, cual

was replicated with the other 123 subjects in May 2019. As the data from

both samples were very similar and no significant differences were found,

we do not distinguish between the two data sets in the main text. A discussion

is in the online appendix.

yo

D

oh

w

norte

oh

a

d

mi

d

F

r

oh

metro

h

t

t

pag

:

/

/

d

i

r

mi

C

t

.

metro

i

t

.

mi

d

tu

/

r

mi

s

t

/

yo

a

r

t

i

C

mi

–

pag

d

F

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

mi

s

t

_

a

_

0

0

9

8

0

pag

d

.

F

b

y

gramo

tu

mi

s

t

t

oh

norte

0

7

S

mi

pag

mi

metro

b

mi

r

2

0

2

3

708

THE REVIEW OF ECONOMICS AND STATISTICS

the amount they had been given. The instructions furthermore

contained an explanation of the possible outcomes of a lot-

tery similar to one of the more complicated lotteries used in

the experiment and subjects were asked three comprehension

questions that had to be answered correctly before they could

proceed to the incentivized tasks. Además, subjects were

asked to answer a (nonincentivized) practice question before

getting to the incentivized tasks to allow them to become

familiar with the interface.

Each subject was randomly assigned to either the small

probability gain treatment or the 50-50 gain treatment by the

software, and all participated in the loss treatment. Every sub-

ject thus participated in two treatments, the loss treatment and

one of the gain treatments, y 121 subjects participated in

el 50-50 gain treatment, 124 subjects in the small probability

gain treatment, and all of these subjects (245 en total) en el

loss treatment. The tasks measuring a particular higher-order

risk attitude for a given treatment were presented together,

and the order of the tasks within such a block of tasks was

randomized, as was the order of the blocks themselves. De este modo,

whether a subject first faced a loss or a gain task was deter-

mined randomly. The location, left or right, of the option that

indicates risk apportionment was randomized for each sub-

ject and each task. Subjects could go back to previous tasks

in the same block of questions and change their choices if

they so wanted.6 Subjects could continue to the next task

only after making a choice in the current one, which they

could do by clicking on the lottery they preferred. To indi-

cate the choice they had made, the selected option was then

highlighted. After participating in the treatments, subjects

were asked some background questions (on gender, edad, ya-

nacionalidad, degree program, and income); they were explicitly

allowed not to answer these questions.7

After answering all questions in the experiment, subjects

were asked one by one to come to the front desk to play one

of their choices for real. Subjects were asked to roll a six-

sided die to select one of the six blocks of tasks, three of

which measured preferences under losses and three of which

measured preferences under gains, and a twelve-sided die

to select according to which of the twelve choices in that

block they would be paid. The subject would then draw a

colored plastic token from an opaque bag with a composition

of tokens corresponding to that described in the selected task.

Composing the bag was done in full view of the first subject

in each session for whom that bag was needed, and subjects

who came thereafter could inspect the bag if they wished.

Some subjects had to draw tokens from more than one bag.

Depending on the final outcome, the subject would then be

paid in addition to their initial €15 payment or have to give

up part of it. The average earnings of subjects were €14.80,

and the total duration of a session, including the payment

procedimiento, was less than one hour.

6In the experiment, 2.5% of all choices were revised by subjects.

7Only gender was asked about in the January 2017 sessions.

IV. Resultados

A. Aggregate Behavior, Nonparametric Methods

Cifra 2 shows the number of times subjects chose in

agreement with risk aversion, prudence, and temperance in

the loss treatment and in the gain treatments. For the two gain

tratos, the patterns are very similar: we find risk aver-

sion and prudence in both gain treatments, which is consistent

with the usual findings in the literature, and weak (if signifi-

cant) intemperance, which is consistent with the findings of

Deck and Schlesinger (2010) and Baillon, Schlesinger, y

Van de Kuilen (2017) but not with the results of Ebert and

Wiesen (2014), Deck and Schlesinger (2014), and Noussair,

Trautmann, and Van de Kuilen (2014), who find modest tem-

perance in the aggregate.

Cifra 2 suggests a reflection effect for higher-order risk

attitudes: responses are markedly different for the loss treat-

ment compared to the gain treatments. For losses, we find

much more risk-loving preferences, leading to risk neutrality

in the aggregate, as well as imprudence and much temper-

ance. This reflection effect is also visible in table 1, cual

shows the proportion of choices consistent with risk appor-

tionment in each of the three treatments.8 To test the reflection

efecto, we perform a Wilcoxon signed rank test. Esto indica

that the differences in the number of risk-averse choices be-

tween the loss treatment and the 50-50 gain treatment and

the small probability gain treatment are significant, as are the

differences in the number of prudent choices between the loss

treatment and the gain treatments and the greater frequency

of temperate choices in the loss treatment compared to the

gain treatments, all with p-values smaller than 0.001.

For all risk attitudes in all treatments, the mode is either

twelve or zero choices consistent with risk apportionment

(risk aversion, prudence, or temperance), meaning fully con-

sistent choices for or against risk apportionment, and in most

casos, the second-most-common outcome is twelve choices

for the reverse higher-order risk attitude. This consistency is

reassuring considering the involved choices subjects need to

make when measuring higher-order risk preferences.

The data appear to become noisier as we go from mea-

suring risk aversion, to measuring prudence, to measuring

temperance, at least for gains. Taking the distance from six

choices for the option satisfying risk apportionment as an or-

dinal measure of consistency,9 we find a negative Spearman

rank correlation between the risk order and consistency for

50-50 gains (ρ −0.186, p-value <0.001) and small probabil-

ity gains (ρ −0.134, p-value 0.001). The small probability

gains data are more consistent than the 50-50 gains data: the

average distance from random choice is 4.71 for 50-50 gains

and 5.05 for small probability gains for second-order tasks

8When measuring types of preferences, as in this study, reflection indicates

a reversal from one type to the opposite type, that is, from risk apportionment

to the reverse preference, or vice versa.

9This is, on average, the number of choices made for the options satisfying

risk apportionment by a decision maker choosing randomly.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

709

FIGURE 2.—HISTOGRAMS OF CHOICES IN THE THREE TREATMENTS

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

TABLE 1.—AGGREGATE CHOICES BY TREATMENT AND HIGHER-ORDER

RISK PREFERENCE

TABLE 2.—RANK CORRELATIONS BETWEEN RISK-AVERSE, PRUDENT, AND

TEMPERATE CHOICES

Risk-Averse

Choices (%)

Prudent

Choices (%)

Temperate

Choices (%)

49.3

80.6***

87.8***

42.8***

60.3***

71.1***

69.4***

42.9***

46.0***

Losses (N = 245)

50-50 gains (N = 121)

Small probability gains

(N = 124)

Asterisks indicate a significant difference from 50% (binomial test) at the ∗∗5% and ∗∗∗1% level.

(Mann-Whitney U test, p-value 0.059), respectively, 4.05 and

4.74 for third-order tasks (p-value 0.008), and 3.68 and 4.36

for fourth-order tasks (p-value 0.015). For losses, we find

no relation between consistency and the risk apportionment

order of the tasks (ρ 0.050, p-value 0.177).

The percentage of choices of the risk apportionment option

are indicated in table 6 for each task. For most treatment-risk

attitude pairs, the majority of choices is for or against risk

apportionment across all tasks.

A preference for combining good with bad or good with

good leads to three possible combinations of risk attitudes

(see section II): those who are risk averse, prudent, and tem-

perate; those who are risk loving, prudent, and intemperate;

and those who are risk neutral, prudence neutral, and temper-

ance neutral. At the aggregate level, we do not find evidence

in support of a preference for combining good with bad or

good with good underlying higher-order risk preferences. In

the gain treatments, which induce the most risk aversion, we

find the least temperance, and for losses we find imprudence

in the aggregate.

Losses

Prudent choices

Temperate choices

50-50 gains

Prudent choices

Temperate choices

Small probability gains

Prudent choices

Temperate choices

p-values are in parentheses.

Risk-Averse

Choices

Prudent

Choices

0.184

(0.004)

−0.056

(0.386)

−0.031

(0.737)

−0.061

(0.505)

0.399

(<0.001)

0.181

(0.045)

−0.018

(0.775)

0.164

(0.072)

0.136

(0.133)

B.

Individual Behavior, Nonparametric Methods

Within treatments, we can test for the correlation between

the various higher-order risk preferences. Spearman corre-

lation coefficients and p-values are reported in table 2 for

the three treatments. A preference for combining good with

bad or good with good predicts that the number of temperate

choices is positively correlated with the number of risk-averse

choices, but the number of prudent choices is not. There is a

significant correlation between temperance and risk aversion

only for the small probability gain treatment, and there it is

dwarfed by the correlation between prudence and risk aver-

sion. We also find a significant correlation between prudence

and risk aversion for losses.

710

THE REVIEW OF ECONOMICS AND STATISTICS

A caveat to the tests of the correlations in table 2 is that

large numbers of indifferent subjects would push any positive

correlation toward 0. Many subjects chose the risk-averse,

prudent, or temperate option no more than two times (out

of twelve) or at least ten times, and the probability of do-

ing so when choosing randomly is slightly less than 4%. We

therefore classify subjects accordingly. The remaining sub-

jects, who chose the risk-averse, prudent, or temperate option

between three and nine times, we classify as risk neutral, pru-

dence neutral, and temperance neutral.10 The frequencies of

types are reported in table 7 in appendix D.

Using this classification, we also find little evidence that

fourth-order risk attitudes depend on second-order risk atti-

tudes. For losses and 50-50 gains, the patterns of temperance

do not appear to depend on second-order risk preferences,

and a Fisher’s exact test (p-value 0.610, respectively 0.645)

cannot reject that the patterns are the same. The distribu-

tion of fourth-order risk preferences does depend on second-

order risk preferences for the small probability gain treatment

(p-value 0.001), but this is mostly driven by the relatively

large number of temperance-neutral subjects among the

group of risk-neutral individuals.11

C. Aggregate Behavior, Maximum Likelihood Estimation

The previous results are based on an informal argument

that choices at the extremes are unlikely to be the result of

a subject choosing randomly between the options. To model

this explicitly, we perform maximum likelihood estimation

(MLE). We estimate a mixed binomial distribution for each

order of risk apportionment, with πs the proportion of deci-

sion makers who satisfy risk apportionment for that particular

order, πo the proportion of decision makers with the opposite

risk attitude, and πn the proportion of neutral or indifferent

decision makers.

We allow for types with strict preferences to make errors.

In any task, subjects who satisfy risk apportionment have a

probability η < 1/2 of choosing the option that does not in-

dicate risk apportionment, which is allowed to differ from

the error rate δ < 1/2 for those who have the opposite pref-

erence. We assume that the probability that an indifferent

decision maker chooses the option that indicates risk appor-

tionment is equal to 1/2.12 The probability of choosing the

option indicating risk apportionment x out of twelve times

can be represented by the following density for a given order,

10This classification is consistent with the maximum likelihood estima-

tions of the proportion of each type, which we present below. We also

considered the choice patterns of perfectly consistent subjects only. These

looked qualitatively similar.

11When excluding neutral types, the difference is not statistically signifi-

cant (p-value 0.117). Maximum likelihood estimation also does not indicate

significance. See section IVD.

12The position (left or right) of the lottery indicating risk apportionment

was randomized for each task, so even an indifferent subject who always

chooses the left or right option would choose the option indicating risk

apportionment with a probability of 0.5.

TABLE 3.—ESTIMATED PARAMETER VALUES FOR DIFFERENT HIGHER-ORDER

RISK ATTITUDES

Order

Treatment

2

3

4

Losses

50-50 gains

Small probability gains

Losses

50-50 gains

Small probability gains

Losses

50-50 gains

Small probability gains

ˆπs

0.32

0.79

0.85

0.27

0.46

0.63

0.57

0.18

0.31

ˆπn

0.35

0.13

0.13

0.31

0.34

0.19

0.28

0.50

0.29

ˆπo

0.34

0.08

0.02

0.43

0.20

0.18

0.14

0.32

0.39

ˆη

0.04

0.07

0.05

0.04

0.08

0.05

0.06

0.05

0.04

ˆδ

0.06

0.04

0.00

0.05

0.01

0.03

0.02

0.03

0.05

πs indicates the share of subjects satisfying risk apportionment (risk aversion, prudence, and temperance

for orders 2, 3, and 4), mistakenly choosing the reverse option with probability η. πo indicates those with

the opposite attitude and error rate δ, and πn the neutral subjects. Underlines indicate the mode.

TABLE 4.—LIKELIHOOD RATIOS AND p-VALUES FOR THE TEST THAT THE

SHARE OF SUBJECTS WHO SATISFY RISK APPORTIONMENT IS EQUAL

TO THE SHARE WHO DO NOT

Order

Treatment

2

3

4

Losses

50-50 gains

Small probability gains

Losses

50-50 gains

Small probability gains

Losses

50-50 gains

Small probability gains

LR

0.17

79.24

90.37

8.87

10.80

30.29

64.17

4.42

0.99

p-Value

0.676

<0.001

<0.001

0.003

0.001

<0.001

<0.001

0.036

0.319

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

with πs + πn + πo = 1:

(cid:2)

(cid:3)(cid:4)

f (x) =

12

x

πs(1 − η)xη12−x + πn

(cid:5)

+ πoδx(1 − δ)12−x

.

12−x

1

2

x 1

2

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

The error rates are estimated separately for each higher-

order risk preference because the lotteries become increas-

ingly complex as the order of the risk preference increases,

and it is important to be able to distinguish risk preferences

from a tendency toward random choice. Noisy behavior may

also be captured by the proportion of decision makers with

neutral risk attitudes: a decision maker who is confused or

inattentive may simply choose (almost) randomly. The pa-

rameter values, estimated using numerical methods, are pre-

sented in table 3.

The estimated proportions support the results from the

nonparametric analysis. For losses, there are slightly more

risk lovers than risk averters; there is also much imprudence

and much temperance. For 50-50 gains and small probabil-

ity gains, there is much risk aversion, much prudence, and

some intemperance. Likelihood ratio tests, reported in table

4, show that seven of these differences are statistically sig-

nificant. Only the risk-loving attitude for losses and intem-

perance for small probability gains are not significantly more

common than the opposite attitude; in these cases, we cannot

reject the null hypothesis that πs = πo against the alternative

hypothesis that πs (cid:5)= πo.

THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

711

TABLE 5.—LIKELIHOOD RATIOS AND p-VALUES TESTING THE REFLECTION

EFFECT USING MLE

FIGURE 3.—MLE, COMBINATIONS OF SECOND- AND FOURTH-ORDER RISK

ATTITUDES AND LOSS TREATMENT

Order

Treatment

2

3

4

50-50 gains

Small probability gains

50-50 gains

Small probability gains

50-50 gains

Small probability gains

LR

54.38

76.04

19.19

38.41

35.02

31.19

p-Value

<0.001

<0.001

<0.001

<0.001

<0.001

<0.001

Null hypothesis is that the proportion of those who satisfy risk apportionment relative to those who have

the opposite attitude (πs/πo) is the same for losses and the specified gain treatment.

Estimated error rates: ˆυ = 0.04 (risk-averse subjects), ˆθ = 0.06 (risk loving), ˆω = 0.06 (temperate), and

ˆζ = 0.02 (intemperate subjects).

FIGURE 4.—MLE, COMBINATIONS OF SECOND- AND FOURTH-ORDER RISK

ATTITUDES, AND GAIN TREATMENTS

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

/πl

Finally, to test the reflection effect, we test whether the

proportion of those who satisfy risk apportionment relative

to those who have the opposite preference is the same for

losses and gains. Table 5 reports likelihood ratio estimates

/πg

and p-values for the null hypothesis that πl

o,

s

where πl

o is the proportion of subjects who satisfy risk

s

apportionment for a given order relative to the proportion

of subjects with the opposite attitude for losses, and πg

/πg

o

s

has the same meaning but for either gain treatment. The re-

sults show that the greater proportion of risk-loving, impru-

dent, and temperate (relative to risk-averse, prudent, and in-

temperate) subjects for losses than for gains are all highly

significant.

= πg

s

/πl

o

D.

Individual Behavior, Maximum Likelihood Estimation

To investigate a preference for combining good with bad or

good with good further, we perform a maximum likelihood

estimation where we test the frequencies of combinations

of second- and fourth-order risk attitudes. Subjects are risk

averse and temperate if they have a preference for combin-

ing good with bad, risk loving and intemperate if they have

a preference for combining good with good, and risk neutral

and temperance neutral otherwise. There are nine possible

combinations of second- and fourth-order risk attitudes. We

denote these different types as πa,b, a, b ∈ {s, n, o}, where a

indicates whether the second-order risk attitude satisfies risk

apportionment of order 2 (risk aversion), matches the oppo-

site preference (risk-loving preferences), or is neutral toward

risk apportionment of order 2 (risk neutral) and b indicates

whether the fourth-order risk attitude satisfies fourth-order

risk apportionment (temperance), matches the opposite atti-

tude (intemperance), or is neutral (temperance neutral).

We again allow for errors, which differ across types and or-

ders of risk attitudes. A risk-averse subject is assumed to have

a probability υ of mistakenly choosing the riskier option, a

risk-loving subject has a probability θ of mistakenly choosing

the safer option, and a risk-neutral subject chooses either op-

tion with probability 1/2. Temperate subjects are assumed to

mistakenly choose the intemperate option with probability ω,

intemperate subjects mistakenly choose the temperate option

with probability ζ , and temperance-neutral subjects choose

either option with probability 1/2. The estimated proportions

are presented in figure 3 for losses and in figure 4 the gain

treatments.

712

THE REVIEW OF ECONOMICS AND STATISTICS

If subjects have a preference for combining good with bad

or good with good, then the symmetric types (πs,s, πn,n, πo,o)

should be most common. This means that most of the mass

should be on the diagonals from the top left to the bottom

right in figures 3 and 4. The data do not show such a pattern.

For losses, the most common type in fact combines temper-

ance with a risk-loving attitude. For 50-50 gains, the two most

frequent types combine risk aversion with temperance neu-

trality and risk aversion with intemperance. For small prob-

ability gains, the most common type combines risk aversion

with temperance, in agreement with a preference for combin-

ing good with bad, but the second most common type, with

a share of 31% of the subjects, combines risk aversion with

intemperance, and the difference in the proportions of these

two types is only 1 percentage point.

To formally test the hypothesis of a preference for com-

bining good with bad or good with good for gains and losses,

we test whether πs,s + πo,o = πs,o + πo,s against the alter-

native that πs,s + πo,o (cid:5)= πs,o + πo,s using a (log) likelihood

ratio test. We do not include the proportion of neutral types

in the test as subjects may be classified as indifferent be-

cause they are confused, distracted, or inattentive, and the

extent of this may depend on the order of the risk prefer-

ence measured. Neither for losses (LR 1.11, p-value 0.292),

nor for 50-50 gains (LR 2.01, p-value 0.157), nor for small

probability gains (LR 0.18, p-value 0.674) can we reject that

πs,s + πo,o = πs,o + πo,s. Thus, we do not find evidence that

risk aversion is combined more often with temperance than

intemperance or that risk lovers are more likely to be intem-

perate than temperate for gains or losses.

E. Background Characteristics and Robustness

In this section, we briefly report on tests to investigate the

influence of various factors on responses.13 First, we inves-

tigate the effects of background characteristics. As all sub-

jects participated in a gain and the loss treatment, background

characteristics cannot drive the reflection effect we find, but

nonetheless it may be interesting to see whether they play a

role. Gender in particular has been found to influence risk

preferences in various studies (see Croson & Gneezy, 2009,

for a review). Other characteristics such as age, nationality,

income, or degree program may also play a role, although ex-

perimental samples tend to be quite homogeneous, making it

difficult to detect such effects. We do not find robust evidence

of background characteristics influencing responses. See the

online appendix for details.

We also perform two robustness checks testing for ses-

sion effects and ordering effects. The results of a Kruskal-

Wallis test do not indicate that there are important session

effects. ANOVA with variables indicating whether subjects

were presented with gain or loss tasks first, whether the first

block measuring a given risk attitude did so for losses or

for gains, and the position (as the first, second, and so on) of

13We thank an anonymous referee for this suggestion.

each block of questions does not indicate significant ordering

effects. The details are provided in the online appendix.

V. Discussion

The aggregate pattern of risk aversion, prudence, and slight

intemperance we find for pure gains in our experiment mir-

rors earlier findings of Deck and Schlesinger (2010) and

Baillon et al. (2017). Deck and Schlesinger (2014), Ebert

and Wiesen (2014), and Noussair et al. (2014) also find risk

aversion and prudence in the aggregate, but they also find

moderate temperance rather than intemperance. Deck and

Schlesinger (2014) point out that the modest intemperance

of Deck and Schlesinger (2010) can be explained if there

were unusually many risk lovers in their sample but could

not verify this explanation as Deck and Schlesinger (2010)

collected no information on second-order risk attitudes. The

aggregate intemperance in our sample does not appear to be

caused by intemperate risk lovers. The number of risk lovers

is small in the gain treatments, and we do not find evidence

that fourth-order risk preferences are a function of second-

order risk preferences. Baillon et al. (2017) also have few

risk lovers in their sample while finding intemperance. The

respective temperance or intemperance is quite weak at the

aggregate level in all studies, suggesting that the observed

discrepancies may simply be the consequence of differences

in the makeup of samples combined with modest effects from

differences in presentation.

Although a preference for combining good with bad or

good with good seems to explain higher-order risk prefer-

ences for mixed lotteries, our results indicate this is not the

case for pure gains or losses. We do not find evidence at

the individual level that risk aversion is combined with tem-

perance, and the imprudence we find for losses, as well as

the combination of risk aversion and intemperance for gains,

is evidence against the hypothesis. The differences between

earlier findings and ours may be explained by loss aversion.

This is a question that deserves attention in future studies.

We find clear reference dependence of higher-order risk

preferences. As per the usual findings, the loss frame in-

duces much more risk-loving preferences. We find that pru-

dence and temperance are also affected: preferences shift

from prudence and intemperance under gains to imprudence

and temperance under losses. Thus, we have a full rever-

sal of higher-order risk attitudes: risk aversion, prudence,

and intemperance under gains and much more risk-loving

preferences, imprudence, and temperance under losses. This

is consistent with reflection (Kahneman & Tversky, 1979),

where risk preferences are reversed under losses. The differ-

ent findings suggest it should be worthwhile to investigate ref-

erence dependence further in the context of higher-order risk

preferences.

Our results contrast with those by Deck and Schlesinger

(2010) and Maier and Rüger (2012), who find no influence

of a loss frame on higher-order risk preferences. Neither of

those studies directly controls the reference point, which is

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

713

needed to separate gains and losses. Deck and Schlesinger

(2010) rewrite lotteries so fixed payments are presented as

fixed deductions. Maier and Rüger (2012) have subjects re-

turn to the lab and lose part of their earlier winnings, but they

cannot control what happens between sessions. Whether a

reference point is induced successfully is ultimately an em-

pirical question. Reproducing reference dependence of risk

aversion demonstrates that outcomes intended to be gains and

losses are perceived as such, and neither study does so.14

Prospect theory (Tversky & Kahneman, 1992) has been

suggested as an explanation of findings of higher-order risk

preferences (Deck & Schlesinger, 2010). Reference depen-

dence is an important component of prospect theory, which

can explain the differences in higher-order risk preferences

between the gain and loss treatments. The other important

component of prospect theory is inverse-S-shaped probability

weighting, which leads to risk-loving behavior for small prob-

ability gains. We do not find the predicted behavior: choices

in the small probability gain treatment closely resemble those

in the 50-50 gain treatment, meaning, in particular, that we

observe clear risk aversion. A possible explanation for the ob-

served risk aversion in the small probability gain treatment is

that the probability weighting function is convex rather than

inverse-S shaped. Convex probability weighting for gains has

been found in some experiments, including Van de Kuilen and

Wakker (2011).

Table 8 in appendix E shows the predicted choices of

prospect theory based on the functional form used in Tver-

sky and Kahneman (1992) and the parameter values they es-

timate. These imply inverse-S probability weighting. For our

tasks, the predictions are the same for all tasks in a given

treatment measuring a specific risk attitude. Besides predict-

ing that people are risk loving for our small-probability treat-

ment, prospect theory predicts prudence15 and intemperance

for losses. It predicts prudence for both losses and gains be-

cause the prudent option has both a better best and worst out-

come than the imprudent option, the probabilities of which

are overweighted with inverse-S probability weighting. Con-

vex probability weighting for losses can accommodate the

imprudence we find, as this leads to underweighting the worst

outcome.

As empirical findings point to a fourfold pattern of risk

attitudes, it would have been interesting to include a small

probability loss treatment. We did not do this for practical

considerations. Another interesting extension would be to

14Using hypothetical choices, Attema, l’Haridon, and Van de Kuilen

(2019) find risk aversion and prudence for gains and risk neutrality and

prudence neutrality for losses. Brunette and Jacob (2019) claim to find im-

prudence for losses, but their results do not support this. Their loss tasks are

the negative of their gain tasks, but this reverses which option is prudent.

Hence, their modal preference is prudence for both gains and losses. They

also pay out two tasks, one of which may involve gains, so prospects are

mixed rather than pure losses, and they do not reproduce reference depen-

dence of risk aversion.

15The utility function that Tversky and Kahneman (1992) use is prudent

(under expected utility), but this does not drive the results: with linear utility,

the same predictions follow.

test for the effects of different endowments. We leave this for

future work.

Our results indicate that it is important for policy recom-

mendations to consider whether one is measuring higher-

order risk preferences for gains, losses, or both. For exam-

ple, when investigating how demand for insurance with non-

performance risk (a type of probabilistic insurance) relates

to prudence, it will be important to measure prudence for

losses, the domain in which insurance decisions are taken.

The imprudence we find for losses indicates that demand for

probabilistic insurance may be greater than expected based

on the prudence found for gains, and policies aimed at reduc-

ing nonperformance risk (such as increasing trust in insurer

solvency) may not increase demand by as much as expected

based on an assumption of prudent consumers.

In a similar vein, prudence reduces the attractiveness of

prevention efforts, which reduce but do not take away en-

tirely the probability of a loss. Imprudence means that deci-

sion makers undertake more prevention efforts than predicted

based on prudence found for gains. This suggests opportuni-

ties for nudging; for example, by framing outcomes as losses,

people may be more willing to engage in action to reduce the

probability of catastrophic climate change.

The influence of background risks on risk-taking behav-

ior may also interact with the domain in unexpected ways: a

financial crisis may at the same time lead to increased volatil-

ity of stocks and shift the domain of investment decisions of

people with significant wealth tied to stocks to losses. Our

results indicate this would lead to greater temperance, which

means such people would become more risk averse and may,

for example, respond by purchasing insurance against unre-

lated losses (such as health insurance) or by making more

defensive investment decisions even for assets unaffected by

the increased volatility of stocks.

VI. Conclusion

It is well established that second-order risk attitudes for

gains are the mirror image of those for losses. In an exper-

iment, we observe the reflection effect also for higher-order

risk preferences. We find prudence for gains but imprudence

for losses and intemperance for gains but temperance for

losses. This reflection affects the external validity of higher-

order risk preferences measured under gains only and has

behavioral implications when choices involve losses.

The recent literature has found evidence for the hypothesis

that higher-order risk preferences are generated by a prefer-

ence for combining good with bad or good with good. Such

a preference implies risk aversion should be combined with

temperance and that all decision makers should be prudent.

We find that correlations between the number of risk-averse

choices and the number of temperate choices are small and

insignificant. Furthermore, the imprudence we find as the ma-

jority preference for losses, and the simultaneous preference

for risk aversion and intemperance on the aggregate level in

the gain domain, are at odds with this hypothesis for pure

gains and pure losses.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

714

THE REVIEW OF ECONOMICS AND STATISTICS

Appendix A Proof That Probabilistic Mixture Preserves

then

Stochastic Dominance

We follow the definition of stochastic dominance of Eeck-

houdt, Schlesinger, and Tsetlin (2009). It is assumed that all

random variables have bounded supports contained in [l, u].

With F (0)(x) the cumulative distribution function of distri-

(cid:6)

l F (i−1)(t )dt for i ≥ 1. Dis-

bution F , they define F (i)(x) ≡

tribution F weakly dominates distribution G through Nth-

order stochastic dominance if (a) F (N−1)(x) ≤ G(N−1)(x) for

all l ≤ x ≤ u and (b) F (i)(u) ≤ G(i)(u) for i = 1, . . . , N.

x

We will show that if distribution F dominates distribution

G through Nth order stochastic dominance, then the proba-

bilistic mixture F (cid:9) of distribution F and distribution H dom-

inates probabilistic mixture G(cid:9) of distribution G and distribu-

tion H through the Nth-order stochastic dominance.

The cumulative distribution function F (cid:9)(0)(x) can be

written as λF (0)(x) + (1 − λ)H (0)(x), λ ∈ [0, 1]. Similarly,

G(cid:9)(0)(x) ≡ λG(0)(x) + (1 − λ)H (0)(x). Then

(cid:7)

F (cid:9)(1)(x) = λ

l

x

F (0)(t )dt + (1 − λ)

(cid:7)

x

l

H (0)(t )dt

= λF (1)(x) + (1 − λ)H (1)(x)

and

G(cid:9)(1)(x) = λ

(cid:7)

x

l

G(0)(t )dt + (1 − λ)

(cid:7)

x

l

H (0)(t )dt

= λG(1)(x) + (1 − λ)H (1)(x)

for all l ≤ x ≤ u.

Furthermore, if

F (cid:9)(i−1)(x) = λF (i−1)(x) + (1 − λ)H (i−1)(x),

F (cid:9)(i)(x) = λ

(cid:7)

x

l

F (i−1)(t )dt + (1 − λ)

(cid:7)

x

l

H (i−1)(t )dt

= λF (i)(x) + (1 − λ)H (i)(x),

and if

G(cid:9)(i−1)(x) = λG(i−1)(x) + (1 − λ)H (i−1)(x),

then

G(cid:9)(i)(x) = λ

(cid:7)

x

l

G(i−1)(t )dt + (1 − λ)

(cid:7)

x

l

H (i−1)(t )dt

= λG(i)(x) + (1 − λ)H (i)(x).

Thus, by induction,

F (cid:9)(i)(x) = λF (i)(x) + (1 − λ)H (i)(x)

and

G(cid:9)(i)(x) = λG(i)(x) + (1 − λ)H (i)(x)

for all i ≥ 0 and all l ≤ x ≤ u.

If distribution F dominates distribution G through Nth-

order stochastic dominance, that is, F (N−1)(x) ≤ G(N−1)(x)

for all l ≤ x ≤ u and F (i)(u) ≤ G(i)(u) for i = 1, . . . , N,

then F (cid:9)(N−1)(x) ≤ G(cid:9)(N−1)(x) for all l ≤ x ≤ u and F (cid:9)(i)(u) ≤

G(cid:9)(i)(u) for i = 1, . . . , N, and distribution F (cid:9) stochasti-

cally dominates distribution G(cid:9) through Nth-order stochastic

dominance.

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

FIGURE 5.—A SCREENSHOT OF ONE OF THE PRUDENCE TASKS SUBJECTS WERE FACED WITH IN THE 50-50 GAIN TREATMENT

Appendix B Task Screenshot

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

All outcomes are in addition to the €15 subjects had been given on entering the lab.

THE REFLECTION EFFECT FOR HIGHER-ORDER RISK PREFERENCES

715

Order

2

Losses

Treatment

Task

2

50-50 gains

2

Small probability gains

3

Losses

3

50-50 gains

3

Small probability gains

Appendix C Tasks

TABLE 6.—TASKS USED IN THE EXPERIMENT

Risk Apportionment Option

[−8, −9]

[−7, −8]

[−8, −10]

[−7, −9]

[−5, −6]

[−6, −8]

[−7, −9]

[−6, −7]

[−6, −8]

[−7, −9]

[−6, −10]

[−6, −8]

[8,9]

[7,9]

[9,11]

[7,9]

[4,5]

[5,7]

[6,7]

[7,9]

[6,8]

[8,9]

[8,9]

[6,7]

(0.16: [70, 46], 0.84: 2)

(0.18: [38, 28], 0.82: 2)

(0.14: [60, 48], 0.86: 2)

(0.12: [35, 32], 0.88: 1)

(0.10: [110, 90], 0.90: 1)

(0.10: [40, 35], 0.90: 2)

(0.08: [30, 24], 0.92: 1)

(0.08: [66, 62], 0.92: 2)

(0.06: [58, 44], 0.94: 2)

(0.04: [180, 144], 0.96: 1)

(0.02: [70, 54], 0.98: 1)

(0.20: [50, 40], 0.80: 1)

[−9, −6 + [4, −4]]

[−10, −4 + [3, −3]]

[−8, −5 + [4, −4]]

[−6, −4 + [2, −2]]

[−10, −5 + [4, −4]]

[−9, −4 + [3, −3]]

[−9, −7 + [5, −5]]

[−8, −4 + [3, −3]]

[−9, −5 + [4, −4]]

[−8, −4 + [2, −2]]

[−7, −2 + [1, −1]]

[−10, −3 + [2, −2]]

[4, 11 + [3, −3]]

[3, 9 + [2, −2]]

[5, 8 + [4, −4]]

[5, 10 + [3, −3]]

[3, 8 + [1, −1]]

[5, 9 + [4, −4]]

[6, 12 + [5, −5]]

[6, 10 + [5, −5]]

[5, 10 + [4, −4]]

[4, 6 + [3, −3]]

[2, 6 + [1, −1]]

[3, 6 + [2, −2]]

(0.14: [20, 50 + [15, −15]], 0.86: 1)

(0.16: [22, 80 + [16, −16]], 0.84: 1)

(0.18: [30, 70 + [25, −25]], 0.82: 1)

(0.10: [30, 60 + [24, −24]], 0.90: 2)

(0.10: [54, 96 + [50, −50]], 0.90: 2)

(0.08: [60, 100 + [46, −46]], 0.92: 1)

(0.06: [42, 88 + [38, −38]], 0.94: 2)

(0.04: [34, 64 + [20, −20]], 0.96: 2)

(0.04: [60, 125 + [45, −45]], 0.96: 2)

Reverse Option

[−4, −13]

[−1, −14]

[−4, −14]

[−3, −13]

[−1, −10]

[−3, −11]

[−4, −12]

[−1, −12]

[−1, −13]

[−2, −14]

[−2, −14]

[−2, −12]

[1,16]

[2,14]

[4,16]

[3,13]

[1,8]

[2,10]

[3,10]

[4,12]

[3,11]

[5,12]

[3,14]

[1,12]

(0.16: [100, 16], 0.84: 2)

(0.18: [60, 6], 0.82: 2)

(0.14: [86, 22], 0.86: 2)

(0.12: [52, 15], 0.88: 1)

(0.10: [180, 20], 0.90: 1)

(0.10: [70, 5], 0.90: 2)

(0.08: [48, 6], 0.92: 1)

(0.08: [120, 8], 0.92: 2)

(0.06: [90, 12], 0.94: 2)

(0.04: [280, 44], 0.96: 1)

(0.02: [110, 14], 0.98: 1)

(0.20: [80, 10], 0.80: 1)

[−6, −9 + [4, −4]]

[−4, −10 + [3, −3]]

[−5, −8 + [4, −4]]

[−4, −6 + [2, −2]]

[−5, −10 + [4, −4]]

[−4, −9 + [3, −3]]

[−7, −9 + [5, −5]]

[−4, −8 + [3, −3]]

[−5, −9 + [4, −4]]

[−4, −8 + [2, −2]]

[−2, −7 + [1, −1]]

[−3, −10 + [2, −2]]

[11, 4 + [3, −3]]

[9, 3 + [2, −2]]

[8, 5 + [4, −4]]

[10, 5 + [3, −3]]

[8, 3 + [1, −1]]

[9, 5 + [4, −4]]

[12, 6 + [5, −5]]

[10, 6 + [5, −5]]

[10, 5 + [4, −4]]

[6, 4 + [3, −3]]

[6, 2 + [1, −1]]

[6, 3 + [2, −2]]

(0.14: [50, 20 + [15, −15]], 0.86: 1)

(0.16: [80, 22 + [16, −16]], 0.84: 1)

(0.18: [70, 30 + [25, −25]], 0.82: 1)

(0.10: [60, 30 + [24, −24]], 0.90: 2)

(0.10: [96, 54 + [50, −50]], 0.90: 2)

(0.08: [100, 60 + [46, −46]], 0.92: 1)

(0.06: [88, 42 + [38, −38]], 0.94: 2)

(0.04: [64, 34 + [20, −20]], 0.96: 2)

(0.04: [125, 60 + [45, −45]], 0.96: 2)

Choices (%)

44.5

49.8

44.9

44.5

54.3

46.9

50.6

53.9

49.8

50.2

49.8

52.2

83.5

85.1

81.0

82.6

76.0

81.0

77.7

81.0

78.5

70.2

84.3

86.0

92.7

85.5

84.7

84.7

93.5

91.1

91.1

89.5

86.3

87.1

75.8

91.1

44.1

38.4

45.3

44.9

45.7

42.0

48.2

40.4

44.9

42.0

35.5

41.6

63.6

56.2

63.6

57.9

52.9

67.8

63.6

62.8

62.8

66.1

47.1

59.5

69.4

67.7

67.7

78.2

78.2

67.7

75.8

68.5

70.2

l

D

o

w

n

o

a

d

e

d

f

r

o

m

h

t

t

p

:

/

/

d

i

r

e

c

t

.

m

i

t

.

e

d

u

/

r

e

s

t

/

l

a

r

t

i

c

e

-

p

d

f

/

/

/

/

1

0

4

4

7

0

5

2

0

3

3

3

7

3

/

r

e

s

t

_

a

_

0

0

9

8

0

p

d

.

f

b

y

g

u

e

s

t

t

o

n

0

7

S

e

p

e

m

b

e

r

2

0

2

3

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

716

THE REVIEW OF ECONOMICS AND STATISTICS

Order

Treatment

Task

4

Losses

4

50-50 gains

4

Small probability gains

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

1

2

3

4

5

6

7

8

9

10

11

12

TABLE 6.—CONTINUED.

Risk Apportionment Option

(0.02: [55, 150 + [30, −30]], 0.98: 2)

(0.20: [40, 60 + [28, −28]], 0.80: 1)

(0.12: [44, 75 + [32, −32]], 0.88: 1)

−8 + [[2, −2], [4, −4]]

−7 + [[1, −1], [4, −4]]

−6 + [[2, −2], [3, −3]]

−9 + [[2, −2], [2, −2]]

−7 + [[1, −1], [5, −5]]

−7 + [[3, −3], [3, −3]]

−9 + [[2, −2], [3, −3]]

−8 + [[1, −1], [2, −2]]

−7 + [[2, −2], [3, −3]]

−8 + [[2, −2], [3, −3]]

−6 + [[1, −1], [1, −1]]

−8 + [[1, −1], [3, −3]]

7 + [[2, −2], [4, −4]]

7 + [[3, −3], [3, −3]]

5 + [[1, −1], [2, −2]]

5 + [[1, −1], [3, −3]]

8 + [[2, −2], [3, −3]]

9 + [[2, −2], [6, −6]]

8 + [[3, −3], [4, −4]]

8 + [[2, −2], [5, −5]]

10 + [[3, −3], [6, −6]]

10 + [[4, −4], [5, −5]]

8 + [[1, −1], [6, −6]]

5 + [[2, −2], [2, −2]]

(0.08: 70 + [[20, −20], [45, −45]], 0.92: 1)

(0.10: 70 + [[28, −28], [30, −30]], 0.90: 2)

(0.10: 65 + [[24, −24], [36, −36]], 0.90: 2)

(0.12: 32 + [[14, −14], [14, −14]], 0.88: 2)

(0.12: 60 + [[22, −22], [26, −26]], 0.88: 2)

(0.14: 75 + [[25, −25], [30, −30]], 0.86: 1)

(0.16: 35 + [[10, −10], [20, −20]], 0.84: 1)

(0.06: 100 + [[30, −30], [50, −50]], 0.94: 1)

(0.04: 85 + [[34, −34], [40, −40]], 0.96: 2)

(0.02: 68 + [[18, −18], [42, −42]], 0.98: 1)

(0.20: 55 + [[5, −5], [38, −38]], 0.80: 1)

(0.08: 58 + [[14, −14], [34, −34]], 0.92: 2)

Reverse Option

(0.02: [150, 55 + [30, −30]], 0.98: 2)

(0.20: [60, 40 + [28, −28]], 0.80: 1)

(0.12: [75, 44 + [32, −32]], 0.88: 1)

−8 + [0, [2, −2] + [4, −4]]

−7 + [0, [1, −1] + [4, −4]]

−6 + [0, [2, −2] + [3, −3]]

−9 + [0, [2, −2] + [2, −2]]

−7 + [0, [1, −1] + [5, −5]]

−7 + [0, [3, −3] + [3, −3]]

−9 + [0, [2, −2] + [3, −3]]

−8 + [0, [1, −1] + [2, −2]]

−7 + [0, [2, −2] + [3, −3]]

−8 + [0, [2, −2] + [3, −3]]

−6 + [0, [1, −1] + [1, −1]]

−8 + [0, [1, −1] + [3, −3]]

7 + [0, [2, −2] + [4, −4]]

7 + [0, [3, −3] + [3, −3]]

5 + [0, [1, −1] + [2, −2]]

5 + [0, [1, −1] + [3, −3]]

8 + [0, [2, −2] + [3, −3]]

9 + [0, [2, −2] + [6, −6]]

8 + [0, [3, −3] + [4, −4]]

8 + [0, [2, −2] + [5, −5]]

10 + [0, [3, −3] + [6, −6]]

10 + [0, [4, −4] + [5, −5]]

8 + [0, [1, −1] + [6, −6]]

5 + [0, [2, −2] + [2, −2]]

(0.08: 70 + [0, [20, −20] + [45, −45]], 0.92: 1)

(0.10: 70 + [0, [28, −28] + [30, −30]], 0.90: 2)

(0.10: 65 + [0, [24, −24] + [36, −36]], 0.90: 2)

(0.12: 32 + [0, [14, −14] + [14, −14]], 0.88: 2)

(0.12: 60 + [0, [22, −22] + [26, −26]], 0.88: 2)

(0.14: 75 + [0, [25, −25] + [30, −30]], 0.86: 1)

(0.16: 35 + [0, [10, −10] + [20, −20]], 0.84: 1)

(0.06: 100 + [0, [30, −30] + [50, −50]], 0.94: 1)

(0.04: 85 + [0, [34, −34] + [40, −40]], 0.96)

(0.02: 68 + [0, [18, −18] + [42, −42]], 0.98: 1)

(0.20: 55 + [0, [5, −5] + [38, −38]], 0.80: 1)

(0.08: 58 + [0, [14, −14] + [34, −34]], 0.92: 2)

Choices (%)

64.5

71.8

73.4

72.2

68.2

70.6

67.3

61.6

71.4

71.4

70.2

73.5

73.9

63.3

69.4

45.5

43.0

41.3

47.9

43.0

40.5

42.1

41.3

43.0

42.1

39.7

45.5

46.0

45.2

43.5

50.8

44.4

44.4

48.4

46.8

46.0

46.0

44.4

46.8

Brackets indicate equal probabilities; all outcomes are in euros. Choices reported for the option satisfying risk apportionment.

Appendix D Frequency Tables

Appendix E Prospect Theory Predictions

TABLE 7.—FREQUENCIES OF COMBINATIONS OF SECOND- AND FOURTH-ORDER

RISK ATTITUDES

TABLE 8.—PROSPECT THEORY PREDICTIONS BASED ON PARAMETER ESTIMATES

OF TVERSKY AND KAHNEMAN (1992)

Attitude

Losses

Risk averse

Risk neutral

Risk loving

Total

50-50 gains

Risk averse

Risk neutral

Risk loving

Total

Small probability gains

Risk averse

Risk neutral

Risk loving

Total

Temperate

Temperance

Neutral

Intemperate Total

40

43

49

132

14

6

2

22

38

1

0

39

25

30

21

76

42

13

3