Sharon Stieber

Is Securitization Right

for Microfinance?

The microfinance industry is playing a leading role in helping to alleviate poverty

by providing tiny loans to the marginalized majority of the world’s population that

lives on less than $3/day. The demand for microfinance loans, sin embargo, exceeds the current supply of capital available to microfinance institutions. Innovations in the commercial capital markets are starting to play a greater role in making more loan capital available to microfinance institutions so they can make loans to the poor. Por ejemplo, en años recientes, a growing number of microfinance institutions have issued bonds in their local capital markets to raise funds for expanding microfi- nance loan portfolios.1 This article focuses on yet another new, more structured, innovative form of financing: securitizing microfinance loan portfolios. En 2006, the world of true sale2 securitizations reached the microfinance mar- ket. In May of 2006, ProCredit Bank Bulgaria securitized 47.8 million of its Euro- denominated microfinance loans. Enhanced by guarantees provided by the European Investment Fund and Germany’s KfW, a state-supported development bank, these securities received a BBB credit rating, considered “investment grade,” from the global credit rating agency Fitch. In July of 2006, the Bangladesh Rural Advancement Committee (BRAC) closed a deal to securitize $180 million equiva-

lent of local currency microfinance loans over a six-year period, con $15 million to be disbursed in the first six months. The issuance received the highest quality credit rating (AAA) from a local rating agency, Credit Rating Agency of Bangladesh (CRAB), and succeeded in attracting two local banks as key investors. These transactions were landmark issuances for the microfinance industry. While securitizations are not new to Wall Street, they are a significant innovation in microfinance. By using this form of structured finance, microfinance institu- tions have the opportunity to attract a broader range of investors. Securitizations have existed for over 30 years in the developed world, enhanc- ing liquidity in sophisticated financial markets, but to apply this complex financial product to the world of microfinance requires new strategies, innovation, and a vision of unprecedented partnerships between the traditional banking sector and Sharon Stieber is former Vice President of Structured Transactions, Fannie Mae. In developing this article, she was ably assisted by a research assistant, Amelia Greenberg, and staff of the Grameen Foundation. 202 © 2007 Sharon Stieber innovations / invierno & primavera 2007 Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023 Is Securitization Right for Microfinance? the microfinance industry. Securitization may seem especially unlikely for an organization like BRAC, which sees financial sustainability as a primarily way to achieve its social missions of alleviating poverty and empowering the poor. BRAC is, En realidad, not a bank, but one of the world’s largest microfinance organizations with approximately 4 million outstanding loans to poor women, with loan sizes averaging about $250. ProCredit, through its local banking subsidiaries in devel-

oping countries, targets medium, small and micro-sized enterprises. Most banks

have historically ignored these kinds of borrowers, yet around the globe microfi-

nance institutions (MFIs) have shown, through their millions of clients and very

high repayment rates, that the microfinance industry is viable. Securitized micro-

finance receivables could thus provide real returns for a broad array of investors,

while MFIs could use the increased liquidity provided by securitizations to multi-

ply the number of loans they can make to microentrepreneurs in the developing

world.

Transferring securitization techniques to the world of microfinance also raises

several challenges. To ease them, the next natural innovation would be to develop

a microfinance secondary market agency that could play a role in the microfinance

industria, as Fannie Mae and Freddie Mac do in the U.S. mortgage securitization

market.

This article is organized as follows. Primero, I describe a “true sale” securitization

and then chart the history and evolution of securitizations in the U.S. market and

más allá de. Next I explore what makes securitizations attractive to issuers and why

they are of interest to a broad array of investors. This leads to a discussion of how

securitization can be transferred to the world of microfinance, and how the secu-

ritization structure is likely to pose challenges to microfinance institutions. I con-

clude with a description of how a microfinance secondary market agency could

help a growing number of microfinance institutions make use of securitizations.

WHAT IS SECURITIZATION?

Securitization occurs when assets (such as microfinance loans or receivables) son

transferred from the originator of the loans or receivables to a special-purpose

vehicle (SPV), which is often formed as a trust. The SPV is bankruptcy remote3; es

only functions are to hold the transferred loans, ensuring that they are adminis-

tered, or “serviced,” in accordance with the agreed-upon terms, and to issue its own

securities for which these loans serve as collateral The securities, or bonds, issued

by the SPV represent a beneficial interest in the transferred loans, and are often

referred to as “asset-backed securities” (called here ABS).4 The SPV sells the secu-

rities to investors, generally with the assistance of an investment banker, who gen-

erally maintains a secondary market5 for the bonds. Bonds purchased in a securi-

tization typically are liquid, making them very attractive to the investment com-

munity. The proceeds from the sale of these securities are passed back to the loan

originator, who now no longer owns the loans. The transaction is treated as a “sale

of assets,” meaning that the originator removes the securitized loans from its bal-

innovaciones / invierno & primavera 2007

203

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Sharon Stieber

ance sheet and they are replaced with cash that the bank or MFI can use to offer

additional loans. Each month the servicer—often the same entity as the loan orig-

inator—passes the principal and interest payments it receives on the securitized

loans to the SPV trustee6 who in turn allocates the funds to the SPV’s bond

investors.

HISTORY OF SECURITIZATION

The practice of securitizing loan portfolios began in 1970 when the Government

National Mortgage Association (GNMA), an entity created by the U.S. gobernar-

mento, issued securities that used government mortgages as collateral. These secu-

rities had virtually no credit risk, since they were guaranteed by the U.S. gobernar-

mento.

Later in the 1970s, securitization expanded to include non-guaranteed mort-

gages as the government created two quasi-government agencies, Fannie Mae and

Freddie Mac. These agencies readily and continuously securitize conventional

mortgage loans (those not guaranteed by the government) from banks and other

financial institutions and then issue securities that use these mortgage loans as col-

lateral. Although they do not carry government guarantees, conventional mort-

gage loans tend to be of relatively solid credit quality. Además, Fannie Mae and

Freddie Mac were created by the U.S. Congress to support housing for low- a

moderate-income families; thus their securities trade as if they had an implicit

government guarantee. Because Fannie Mae and Freddie Mac are providing this

robust secondary market for mortgage loans, banks can continuously recycle their

capital to make additional new mortgage loans; this process has contributed to a

A NOSOTROS. mortgage securitization market that is now comparable in size and liquidity

to the U.S. Treasury market.

Banks, savings and loans organizations, and mortgage companies soon saw the

appeal of these instruments and began issuing mortgage-backed securities with

various forms of credit enhancement.7 The vast majority of mortgages in the

United States are now securitized. This has been a crucial factor in increasing the

flow of funds into the American housing market and producing one of the high-

est rates of home ownership in the world. In the late 1980s, mortgage-backed secu-

rities structures became more complicated. The cash flows from principal and

interest payments could be allocated in more complex patterns and two more

structures were born: the Collateralized Mortgage Obligation8 (CMOs) y el

REMICs.9 They made it possible to issue short-, intermediate- and long-term

mortgage-backed bonds that could better meet the differing needs of a wider vari-

ety of investors. Banks became major buyers of the short-term securities that pro-

vided a good asset match with their short-term deposit liabilities. Insurance com-

panies and pension funds that had long-term liabilities found medium- and long-

term bonds attractive. As time passed, financial organizations further customized

the allocation of cash flows to meet the very specific requirements of particular

investors (who were also willing to pay more for these highly tailored securities).

204

innovaciones / invierno & primavera 2007

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Is Securitization Right for Microfinance?

As investors became more comfortable with securitization, they began to use

as collateral various receivables and loans other than mortgages, and structures

were modified to better suit the cash flows of these new types of assets. En 1987,

banks first issued the first securitizations of credit card receivables to diversify their

funding sources and free up capital. Ahora, nearly every type of loan or receivable in

the United States can be securitized: commercial mortgages, trade receivables,

manufactured housing loans, auto loans, auto leases, student loans, and credit

cards. Securitization has greatly expanded the funds available to homeowners,

small businesses, and consumers. In the past decade, these instruments spread to

Europe and the rest of the world. Microfinance loans, which are similar to credit

card receivables in terms of amounts and maturities, have now been added to this

long list of receivable and loan types that can serve as collateral for a securitization.

WHAT MAKES SECURITIZATION ATTRACTIVE TO ISSUERS

Most businesses securitize their assets for two reasons: doing so provides addition-

al funding, and transfers to the SPV the various risks associated with the assets

being securitized (credit, prepayment, interest rate, etc.)

Probably the major reason that MFIs want to securitize their loan portfolios is

to find additional funding. Many MFIs have historically relied primarily on phil-

anthropic funding, which is far from sufficient to meet the estimated demand for

microfinance credit and services. Globally, this demand is pegged as somewhere

entre $250 billion and $300 billion; according to some estimates, only 7%—$17 to $20 billion—is available today. Securitization opens the door for MFIs to obtain

funding directly from local and international capital markets, which today are

flush with available funds. Fixed-income investors looking to diversify their port-

folios may be attracted to MFI portfolio securitizations.

Besides providing an additional source of funding, securitization generally

allows an issuer to transfer to the investors or to a credit enhancer all or some of

the credit, interest rate, prepayment, and operational risks attached to the loans or

receivables being securitized. When the SPV buys a loan, it also takes on the asso-

ciated credit and prepayment risks. The issuer often continues to service the port-

folio (and has a responsibility to execute that role well), but any losses or unexpect-

ed prepayments among the securitized loans will not have an impact on the issuer’s

financial statements. (Por supuesto, if losses are significantly higher than expected, el

issuer may have difficulty transacting securitizations in the future.)

Securitizations can also free up capital that is used to support new loans. If an

issuing MFI is a regulated entity (eso es, subject to its country’s bank regulatory

standards), it must maintain minimum levels of reserve capital (also called “risk-

weighted capital”) to support its loan portfolio. Some countries require regulated

MFIs to hold more risk-weighted capital than local banks, because microfinance

loan portfolios are seen as more volatile. Como resultado, fast-growing MFIs can quick-

ly become stretched, without sufficient reserve capital to keep up with their fast-

growing microfinance loan portfolios. Securitization provides an opportunity to

innovaciones / invierno & primavera 2007

205

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Sharon Stieber

move these assets (microfinance loans) off the MFIs’ balance sheets, thereby reduc-

ing the need to increase the MFIs’ capital reserves. Put differently, when loans are

sold to an SPV in a securitization, the originator transfers the loans to the SPV and

is allowed to release the reserve capital supporting those particular assets. De este modo,

securitization successfully provides regulatory capital relief.

Además, issuers who frequently use securitizations as a funding tool also

often find their profits are increasing, since the security should generate a profit

when it is sold. The issuer can also make it more profitable by retaining the serv-

icing function.

Issuers that securitize generally do so when it will let them lower their overall

cost of funds. Issuers work with their investment bankers to carefully estimate the

costs of issuance and the proceeds from the sale of the bonds.

Over time, securitizations can be profitable, but an entity’s first securitization

transaction can be quite costly, and is usually much more expensive than later

transactions. Drafting all the legal agreements from scratch is expensive, y el

initial research into the legal and accounting viability of various structures can also

be time-consuming and costly. Sometimes new issuers find they also need to

upgrade their servicing and investor reporting capabilities to meet the standards

required for a successful securitization.

WHY INVESTORS LIKE SECURITIZATIONS

It is quite an easy decision to purchase an issuing company’s ABS in a securitiza-

tion transaction—often much easier than a decision to invest directly in the issuer

or even purchasing that issuer’s loan portfolio. The essence of a securitization is

distilled in legal documents and much, if not all, of the necessary review of credit

and operational risks has been delegated to the credit rating agency, whose rating

readily identifies for the investor the level of risk imbedded in the investment. Un

investor in a highly rated security will need to do minimal additional research to

become comfortable with the investment. The rating agency will review the legal

framework of the issuing country, the structure of the deal, the underwriting stan-

dards and credit risk of the loans, as well as the servicing and loss mitigation oper-

ations. One reason it was possible for Fitch to rate the ProCredit transaction in

Bulgaria was that the country already had the necessary legal framework for secu-

ritizations in place.

The rating agency will also monitor the performance of the portfolio over the

life of the transaction. If the quality of the portfolio begins to deteriorate, the rat-

ing agency will reassess the issuer to better understand the cause of the problem

and the steps being taken to mitigate the issue. If the rating agency thinks the risk

is significantly higher than initially estimated, it will put all or some of the bonds

on its Watch List, which is publicly available and monitored by investors.

Legal issues and operational processes must be defined and documented in a

securitization. Both the issuer and the investment banker will have legal counsel

for security and tax issues that arise while the transaction is being structured. Un

206

innovaciones / invierno & primavera 2007

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Is Securitization Right for Microfinance?

independent accounting firm will review the transaction to ensure that projected

cash flows are accurate and that the collateral is correctly described, while internal

accountants will review the transaction to ensure it receives the desired treatment

designating a true sale of assets. The legal documents will spell out the servicing

and loss mitigation processes for review by the credit rating agencies. This over-

sight at all levels is reassuring to investors.

The investment bank has an implied obligation to make a market in the ABS

for the life of the securities. Investment banks have no legal obligation, but bond-

holders expect that if they purchase a bond from an investment banking firm, eso

firm will buy the security back from them in the future at the then-current market

price. To continue to make a market in a security, the investment bank will need to

have updated information on the securitized portfolio; eso es, it will need detailed

loan (or loan pool) information to maintain its model of the transaction and to be

able to quickly provide prices to a potential investor interested in selling the secu-

rity.

IS SECURITIZATION APPROPRIATE FOR MFIS?

While a MFI can materially benefit from a securitization, executing such a trans-

action will be neither easy nor fast, y, as mentioned above, for a first-time issuer

the process can be particularly labor-intensive and expensive.

But securitization offers many benefits for microfinance, and they may well

outweigh the challenges. The benefits accruing to MFIs are the same as to other

issuers: most important, securitization can increase the amount and improve the

terms of available funding, greatly expanding the MFI’s capacity to provide life-

changing credit products to poor borrowers in its markets. Securitization can alle-

viate a MFI’s dependence on donor and less than optimal bank financing.

For investors, securitizing microfinance loans may provide a higher yielding

instrument than those currently available with similar short maturities, which typ-

ically are issued by governments. While microfinance loans tend to mature any-

where between six months and three years, other asset-backed securities tend not

to mature earlier than five years after the date of issue. As more microfinance loans

are securitized, investors will be able to diversify the risk associated with their

international investments by including microfinance receivables from diverse

countries in their portfolio.

While the advantages to securitizing an MFI’s loan portfolio seem compelling,

an MFI—or any other issuer—must address several issues in the process, así como

some additional factors specific to a MFI. Primero, as a general rule, MFIs contemplat-

ing a securitization will need a sizeable microfinance loan portfolio, a robust man-

agement information system, and an enabling legal environment. They must also

consider several other factors, described here.

innovaciones / invierno & primavera 2007

207

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

The Servicing Function

Sharon Stieber

For an MFI to successfully sell assets, it must legally transfer those assets to the SPV.

Y, since the MFI loan originator is no longer the owner, it must have no effec-

tive or indirect control over these transferred assets. This has significant implica-

tions for the continued servicing of the securitized loan portfolio. In most cases the

MFI that originated the securitized loans will retain its role as servicer of these

loans. In this function the MFI must abide by the procedures set out in the trans-

action’s pre-agreed sale and servicing agreement, so the MFI loses any ability to re-

finance or restructure the transferred microfinance loans. MFIs may feel uncom-

fortable when they cannot create new policies and procedures to respond to their

borrowers if they are impacted by unexpected events such as an economic down-

turn or even a natural disaster.10

Microfinance loans generally involve high levels of close interaction with the

borrowers and often a focus on rural and often widely dispersed borrowers. Este

means these loans generally require more labor-intensive—and more costly—

servicing, which the MFI must address as it structures the transaction. Good serv-

icing is one key to a well-performing loan portfolio, so savvy investors will want

servicers to be compensated well enough to devote adequate resources to the serv-

icing function, particularly during an economic downturn.

Reporting to Investors

An originator and servicer of loans to be securitized must compile detailed

descriptions and payment statistics on the loans, both when it initially distributes

the securities sale prospectus, and continuing into the future. This benefits

investors, rating agencies and the investment bank. Securitized portfolios are typ-

ically categorized by loan size, date of issuance, interest rate, ubicación, loan pur-

pose, initial and remaining maturity and underwriting criteria (the credit analysis

performed on the borrower). Each MFI needs a powerful management informa-

tion system (MIS) to compile this data in the form required by investors; sin

uno, it may be nearly impossible. This is why MIFOS, an open source MIS that

aims to serve providers of microfinance, is in the process of developing a securiti-

zation module that can respond to investors’ reporting needs.11

The servicer will also need to provide timely and accurate information on the

performance of the loans over the life of the securitization transaction, y el

trustee of the SPV will require accurate and detailed cash flow information to pro-

duce the bond payments. Finalmente, investors will demand information so they can

effectively monitor their investments.

Representations and Warranties

Typically, the originator of loans for securitization will be required to represent

that the loan information it provides in the initial offering prospectus and in the

sale and servicing agreement is correct. If a securitized loan goes into default and

208

innovaciones / invierno & primavera 2007

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Is Securitization Right for Microfinance?

the data on this loan is found to be inaccurate, the trustee of the SPV can demand

that the originator make up any lost payments or repurchase the loan. Loan files

are most likely to be reviewed when a loan goes into default, and repurchases are

generally called for when an issuer is least able to afford them. While a defaulted

loan is worth a fraction of its original value, the originator will be asked to pay 100

percent of the remaining balance on the loan. In a recession or natural disaster,

when defaults swell, the repurchase obligation can be a crushing blow to an origi-

nator if it is discovered that the disclosed loan information is not correct. Este

reinforces the issuer’s requirement for strong MIS capability and the collection of

correct loan data.

Expenses

Several fees and expenses are involved in any securitization: the investment bank,

rating agency and regulatory agency all require fees, along with the lawyer and

accountant; other fees may be charged for credit enhancement or printing.

Sometimes MFIs need funds to enhance their MIS and investor reporting depart-

mentos.

Organizations issuing securities can find significant economies of scale. Para

ejemplo, issuing one $200 million transaction is far more cost effective than issu- ing four $50 million transactions. MFIs may consider retaining their microfinance

loans over a longer period of time in order to build a larger portfolio to be securi-

tized, or they can even aggregate loan portfolios with other MFIs to structure a

more cost-effective transaction.

Credit Enhancement

Most asset-backed securities have some form of credit enhancement, internal or

externo. The recent ProCredit securitization in Bulgaria utilized external credit

enhancements, in which an entity with a relatively high-quality credit rating guar-

antees all or some of the bonds in a securitization transaction. Por ejemplo, if the

parent of the loan originator has a single A credit rating (considered high credit

quality), and the bonds would otherwise be rated BBB (lesser credit quality),

obtaining a guarantee from the parent would raise the credit rating on the securi-

tization to the higher single A rating.

While external credit enhancements provide comfort to investors, they are not

without risk. Por ejemplo, if the guarantor’s credit rating is downgraded for any

reason, the bonds being guaranteed are also downgraded, and will drop in value.

This devaluation will occur even though the securitized loans are performing as

esperado.

A surety company can also provide a guarantee on some or all of the bonds in

a securitization. Such a company’s sole business is to assess the risk embedded in a

transaction and guarantee it for a fee. These companies are generally rated AAA

(considered to be the highest credit quality) by all three of the global credit rating

agencias, and they bring this AAA rating to the table in a transaction. Because sure-

innovaciones / invierno & primavera 2007

209

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Sharon Stieber

ty companies are very prudent in selecting the transactions they guarantee,

investors are typically more comfortable with this type of external credit enhance-

mento, and are willing to reflect that comfort in requiring a lower yield on the cred-

it-enhanced bonds.

While surety companies, or potentially an issuer’s parent company, puede pro-

vide an external form of credit enhancement for a securitization, this enhancement

can also be provided on an “internal” basis. In the most commonly used forms of

internal credit enhancement, the issuer makes available to investors excess collat-

eral, reserve funds or interest; in subordination, it issues both senior (highest cred-

it quality) and junior (lesser credit quality) securities. Often more than one form

of credit enhancement is used in a transaction; internal and external forms can

also be combined in one transaction.

Internal credit enhancements also can be used in a securitization. Por ejemplo,

the recent BRAC securitization in Bangladesh utilized over-collateralization to

enhance its credit. Over-collateralization occurs when the unpaid principal bal-

ance of the securitized loan pool is larger than the balance of the bonds collateral-

ized by the securitized pool. The over-collateralization can be established at the

time of issuance, or it can be built up over time when the interest payments

received on the securitized loans are in excess of the aggregate of interest paid to

the bond holders plus ongoing transaction fees. If this extra cash flow is not need-

ed to cover losses it can be used to pay down the principal on the bonds, que lo hará

result in over-collateralization. Another internal means of enhancing credit is to

use a reserve fund, a pool of cash designated to be available to cover losses in the

securitized loan portfolio.

The most popular internal form of internal credit enhancement in today’s

market is subordination, but this option also has the most complex structure.

Typically, a bank will issue bonds with varying levels of credit risk ratings, de

highest to lowest (and possibly some with no rating at all). Then it makes its prin-

cipal payments to all levels of bonds below those with the highest credit rating—

the “senior” bonds—only after it has made the payments it owes to the senior

bonds. Thus this transactional, or structural, subordination effectively provides an

internal credit enhancement to the senior bonds.

Process Management

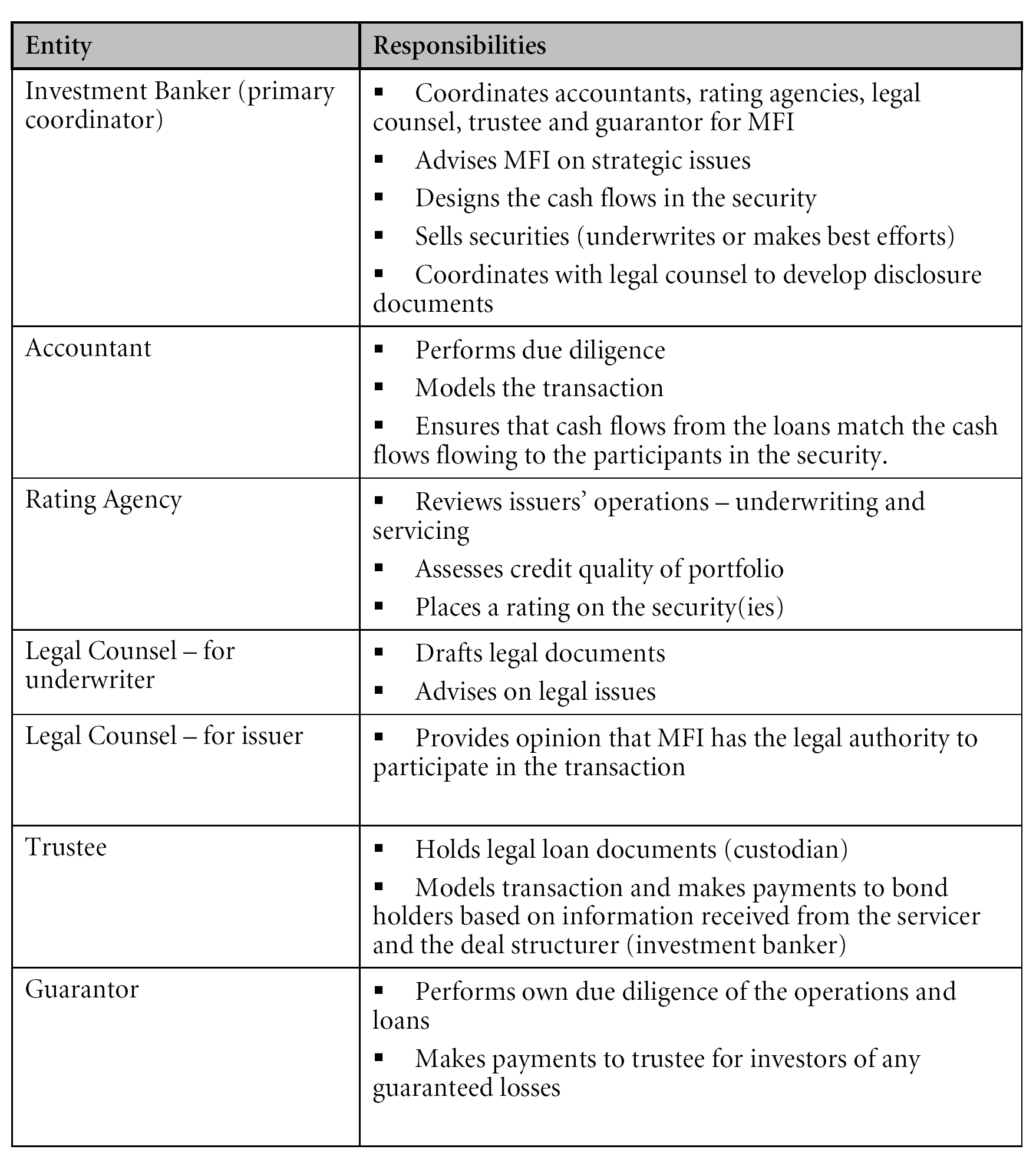

Coordinating all the players and steps required to securitize a loan portfolio can be

a daunting process. Besides the investment bank, the MFI must select and coordi-

nate legal counsel, accountants, rating agencies, the trustee for the SPV, printers,

and potentially a guarantor. Probably the most important relationship will be that

with the investment bank, which will need an adequate track record and experi-

ence to successfully execute the securitization. For first-time issuers it is especially

critical to have a high level of comfort and trust with the investment bank, desde

the issuer will rely on it for advice during every step of the process. It is prudent to

interview several investment bankers before making a final selection. The invest-

210

innovaciones / invierno & primavera 2007

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Is Securitization Right for Microfinance?

Mesa 1. Institutional and professional roles and responsibilities in the process of

securitization.

ment bank plays an extensive role in a securitization: it will recommend and coor-

dinate the rating agency, the trustee, legal counsel and accountants. It will also esti-

mate the profitability of a potential transaction, recommend the optimal form of

credit enhancement, and structure the deal to maximize profit to the issuer.

Besides selecting an appropriate investment bank, securitization issuers must

also engage legal counsel with the appropriate experience and knowledge of the

local legal framework.

The roles and responsibilities of the participants in a securitization are sum-

marized in Table 1.

innovaciones / invierno & primavera 2007

211

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Sharon Stieber

AN INNOVATION TO ADVANCE THE SECURITIZATION OF

MICROFINANCE LOANS

As described above, MFIs that want access to the benefits of securitization must

deal with several issues that may be particularly challenging for them, and they are

likely to be tackling this kind of transaction for the first time. One way to provide

MFIs with easier access to securitization would be to create an entity that could

develop a regional or even global secondary market agent for microfinance loans.

This would dramatically accelerate the growth of this market and benefit both the

MFI issuer and the investor in securitized MFI loan portfolios.

This “microfinance secondary market agency” could play a role comparable to

that of Fannie Mae and Freddie Mac in the U.S. mortgage securitization market.

Such an agency would have several specific roles:

• establish underwriting standards;

• develop servicing requirements;

• create a security platform in which large and small originators can deposit

loans;

• create disclosure documents;

• act as trustee or arrange for the trustee;

• process the data from servicers and provide reports for investors;

• monitor the performance of servicers;

• and market the loans to investors.

Investors would probably find such an agency attractive because they could

rely on it to set and maintain high standards of underwriting and servicing.

Investor reporting would be centralized, consistent, and readily available.

International investors could easily build a regionally diverse portfolio of microfi-

nance securities. This program could make use of a syndicate of investment

bankers to promote a wider and more liquid market for the securities.

For MFI issuers, such an agency would provide many benefits. Transaction

costs would be lower since several MFIs could participate in one larger securitiza-

ción, spreading the costs across many entities. Smaller microfinance loan portfo-

lios also would become more cost-effective to securitize, so many more MFIs

would be able to participate in the process. Loan underwriting and servicing poli-

cies could be standardized for all participants, and while strong information sys-

tems would still be needed to report accurate data, the secondary market agency

would process the data and create the investor reports. This agency would also be

responsible for disseminating this information to investors and other interested

Participantes. The sizable program enabled by the existence of a secondary market

agency would allow several investment banks to participate, expanding the second-

ary market and liquidity for these bonds and thus increasing their value.

A secondary market agency for MFI loans could rapidly facilitate securitiza-

tion in the microfinance sector, providing an attractive asset for investors and a

potentially life-changing credit product for an ever-increasing number of poor

borrowers.

212

innovaciones / invierno & primavera 2007

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023

Is Securitization Right for Microfinance?

1. For information about recent bond offerings in the microfinance industry, see “Microfinance:

Commercial Returns at the Base of the Pyramid” in this issue

2. A “true sale” securitization refers to a structured transaction in which the underlying assets are

kept off the balance sheet.

3. “Bankruptcy remote” is a special characteristic of true sale securitizations that isolates the risk of

the transaction to the underlying assets placed in the trust (SPV) as a result of off-balance sheet

treatment.

4. The terms “securities,” “ABS,” “bonds,” and “certificates” are used interchangeably in this paper

(and often in the marketplace).

5. Investment bankers underwrite bonds issued by the SPV and also ensure secondary market liq-

uidity by purchasing and selling bonds on behalf of other investors or for their own trading

cuenta.

6. The trustee facilitates payments (principal and interest payment on underlying assets) desde el

loan originator to investors.

7. Credit enhancements provide additional security to investors by covering all or a portion of the

losses on the underlying assets in the SPV.

8. A Collateralized Mortgage Obligation (CMO) is a type of mortgage security in which different

classes of investors receive principal and interest on varying schedules. This security is a debt

instrument that allows for time tranching.

9. A Real Estate Mortgage Investment Conduit (REMIC) is a structure created by the Tax Reform

Act of 1986. It issues mortgage-backed securities whose cash flows are similar to those of a CMO

but for tax purposes, it is treated as a sale of an asset. .

10. This inflexibility in loan servicing can be overcome by building into the agreements the ability

for the MFI to repurchase certain loans from the SPV, although this requires the MFI to main-

tain sufficient cash reserves in order to do so.

11. More information about MIFOS is available at the Grameen Foundation website at

www.grameenfoundation.org.

innovaciones / invierno & primavera 2007

213

Descargado de http://direct.mit.edu/itgg/article-pdf/2/1-2/202/704157/itgg.2007.2.1-2.202.pdf by guest on 08 Septiembre 2023