Usman Ahmed, Thorsten Beck,

Christine McDaniel, and Simon Schropp

Filling the Gap

How Technology Enables Access to Finance

for Small- and Medium-Sized Enterprises

Pequeño- and medium-sized enterprises (SMEs) account for more than one-half of

the world’s GDP and employ two-thirds of the global workforce.1 The number one

barrier to growth faced by SMEs around the globe is access to financing.2 This is

not a new issue, as the onerous information, administración, and collateral

requirements associated with traditional loans have inhibited SMEs from seeking

or securing financing.

El 2008 financial crisis only exacerbated the problem, as many local retail

banks (often the primary providers of SME financing) closed their doors and the

appetite for taking on high-risk SME loans was quelled. The International Finance

Corporation estimated that SMEs faced a $2 trillion global credit gap in 2010.3 Online business lending may be stepping in to fill this gap by resolving many of the barriers associated with traditional SME financing. It does so by leveraging new business methods and targeted data analysis generated from past transac- ciones, social interaction data, and back-end financial data (taxes, receivables, etc.). Big data analysis enables modern lenders to better understand the credit risk of an individual SME and provide it with targeted funding in a timely manner with a flexible repayment schedule, and it often can do so without requiring collateral. Online business lending comprises a number of different models. This paper analyzes data from PayPal Inc., a company best known for its global online pay- ment system, and from Kiva, a crowdsourcing platform. Our objective is to under- stand how technology is impacting SMEs’ ability to access financing. PayPal Working Capital (PPWC) launched in late 2013; it is a product that enables SMEs to apply for and obtain short-term credit. PayPal Working Capital loans are fund- Usman Ahmed is the Head of Global Public Policy at PayPal Inc. and an adjunct professor of law at Georgetown University. Thorsten Beck is professor of banking and finance at Cass Business School in London. Christine McDaniel is a Senior Economist at Sidley Austin LLP. Simon Schropp is a Managing Economist at Sidley Austin LLP. © 2016 Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp innovations / volumen 10, number 3/4 35 Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023 Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp ed by a state-chartered industrial bank. En octubre 2015, PayPal announced that the product had reached $1 billion in funding to entrepreneurs in the U.S., Reino Unido,

and EU.4 The dataset we analyze here consists of 60,000 PPWC loans disbursed to

more than 18,000 SME owners in the United States between October 2014 y

Marzo 2015. Kiva, which was launched in 2005, enables people to lend money to

entrepreneurs through an easy-to-use Internet platform. A marketplace that con-

nects lenders and borrowers, Kiva has loaned nearly $800 million since it was launched, and the company boasts a community of more than 1 million lenders and nearly 1.8 million borrowers.5 One of Kiva’s cofounders is a former PayPal employee, and Kiva maintains a close partnership with PayPal. The Kiva dataset we analyze comes from Kiva Zip, a program through which lenders make loans with zero-percent interest directly to borrowers in the U.S.6 Key findings from our analysis of these two online business lending services include the following: (cid:2)(cid:1)Online business loans seem to have stepped in to fill the SME funding gap left in the wake of the 2008 financial crisis. A high proportion of PPWC loans are dis- bursed in zip codes that have experienced a relatively steep decline in the num- ber of traditional retail banks, cerca de 25 percent of PPWC loans were disbursed in the 3 percent of counties that have lost ten or more banks since the 2008 financial crisis. (cid:2)(cid:1)Young and minority-owned businesses with low and moderate income benefit particularly from online business loans. Nearly 35 percent of PPWC loans go to low- and moderate-income businesses, compared to 21 percent of retail bank loans, mientras 61 percent of PPWC loans go to entrepreneurs and young firms that have been in business for less than five years. More than half (53 por ciento) of Kiva Zip’s loans go to women-owned businesses and 63 percent to minority- owned businesses; this compares to 36 percent and 14.6 por ciento, respectivamente, of traditional retail bank loans. (cid:2)(cid:1)Online business loans can boost the growth of SMEs in underserved counties. PPWC recipients in counties that have lost ten or more bank branches since the 2008 financial crisis saw their PayPal sales soar by 22.4 percent from one year to the next, while comparable retail businesses in the U.S. grew by only 1.72 por- cent over the same period.7 (cid:2)(cid:1)Online loan products have potentially significant economic benefits. Based on increased sales of businesses that have received PPWC loans, we estimate that programs like this have the potential to boost economic activity in the U.S. por $697.95 billion, o 3.98 percent of the country’s 2015 PIB.

This paper will begin by describing the challenges SMEs have traditionally

faced in securing access to financing. It will then provide an analysis of the data

that have led us to our conclusion about online business lending stepping in to fill

the gap. The paper will then analyze the demography of the businesses securing

online business loans and the economic opportunity online business lending pres-

36

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Filling the Gap

ents. The paper concludes with a discussion of the policy issues associated with

online lending products.

ASSESSING THE SME FINANCING GAP

Financial institutions have traditionally been the primary source of SME financing

around the world. In the U.S., Por ejemplo, the overwhelming majority of SMEs

report that commercial retail banks (regional or community) are their primary

financial institutions.8 SMEs in Europe obtain 85 percent of their loans from retail

banks.9

En 2014, SME lending by the ten largest U.S. banks was down 38 percent from

its peak in 2006.10 The number of bank branches in the U.S. decreased from 97,274

en 2007 a 94,725 en 2014, and some regions were disproportionately affected by

this shake-out.11 The global market for SME financing has yet to fully recover

from the crisis; en 2013, outstanding SME loans and the number of new loans

issued remained low in much of the developed world.12

SMEs have far more difficulty with access to finance than larger firms. Ellos

often face higher interest rates, shorter maturity, and more stringent collateral

requirements.13 The smaller a firm, the more difficulty it has obtaining financ-

ing.14 A survey of European businesses found that large SMEs (50+ employees) son

more likely than micro-SMEs (1-9 employees) to apply for bank loans and less

likely to be concerned about rejection.15 A Federal Reserve Bank study confirmed

this trend in the U.S., noting that financial institutions have traditionally viewed

micro-SMEs as high-risk and expensive to do business with (es decir., high transaction

costs and low returns).16 The study also found that 20 percent of all SMEs are dis-

couraged from applying for loans in the first place, due to prohibitive application

costs and low loan prospects. Por lo tanto, it is not surprising that SMEs no longer

look to traditional bank loans as a likely credit source.17

Research has provided a number of explanations for why SMEs have tradi-

tionally struggled to obtain capital, incluido:

(cid:2)(cid:1)Poor record-keeping

(cid:2)(cid:1)High risk and turnover in the sector

(cid:2)(cid:1)Overreliance on internal financing

(cid:2)(cid:1)Weak management

(cid:2)(cid:1)Lack of assets to use for collateral

(cid:2)(cid:1)Lack of a track record

(cid:2)(cid:1)Lack of connections in the financial system

(cid:2)(cid:1)Poor knowledge of financing options

(cid:2)(cid:1)The high cost of finding a loan product that fits their needs18

Además, lenders often lack access to third-party information regarding

SME borrowers’ credit profiles and histories. SME financing was further con-

strained in the wake of the financial crisis, as brick-and-mortar financial institu-

tions were increasingly reluctant to engage in high-risk and relatively low-yield

SME loans.19 Many workers who lost their jobs in the course of the crisis launched

innovaciones / volumen 10, number 3/4

37

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp

businesses to make ends meet, and they faced tremendous credit constraints

because they lacked the track record required to secure financing.20 Existing SMEs

were left vulnerable during the credit crisis, as shocks to their companies could not

be absorbed due to the lack of access to short-term financing.21

ONLINE LENDING MAY FILL THE FINANCIAL GAP

The Internet is an interconnected global network that enables a seamless transfer

of information among its more than three billion global users. In the last few years,

this global communications network, combined with advanced analytics, ha sido

leveraged to resolve some common barriers associated with SME lending. Como nosotros

demonstrate below, technological developments in data capture, data analysis,

and reporting have unleashed the potential for online lending to fill the SME

financing gap.22

New technologies can be applied to SME lending in a number of ways: SMEs

can be assessed using new sources of first- and third-party financial information;

forms can be simplified and accessed online; credit assessments can be conducted

in short order, using objective criteria; funding can be disbursed in real time; y

repayment schemes can be adjusted to the individual SME borrower’s situation.

Además, online loans can be tailored to the needs of SMEs. These businesses

typically do not have large cash reserves, so small working-capital loans can

address the cash-flow problems they commonly experience.23 Jesse Hagen, a for-

mer vice president of the U.S. Bank Small Business Division, stated that 82 por ciento

of businesses fail due to poor cash-flow practices.24 In the United States,

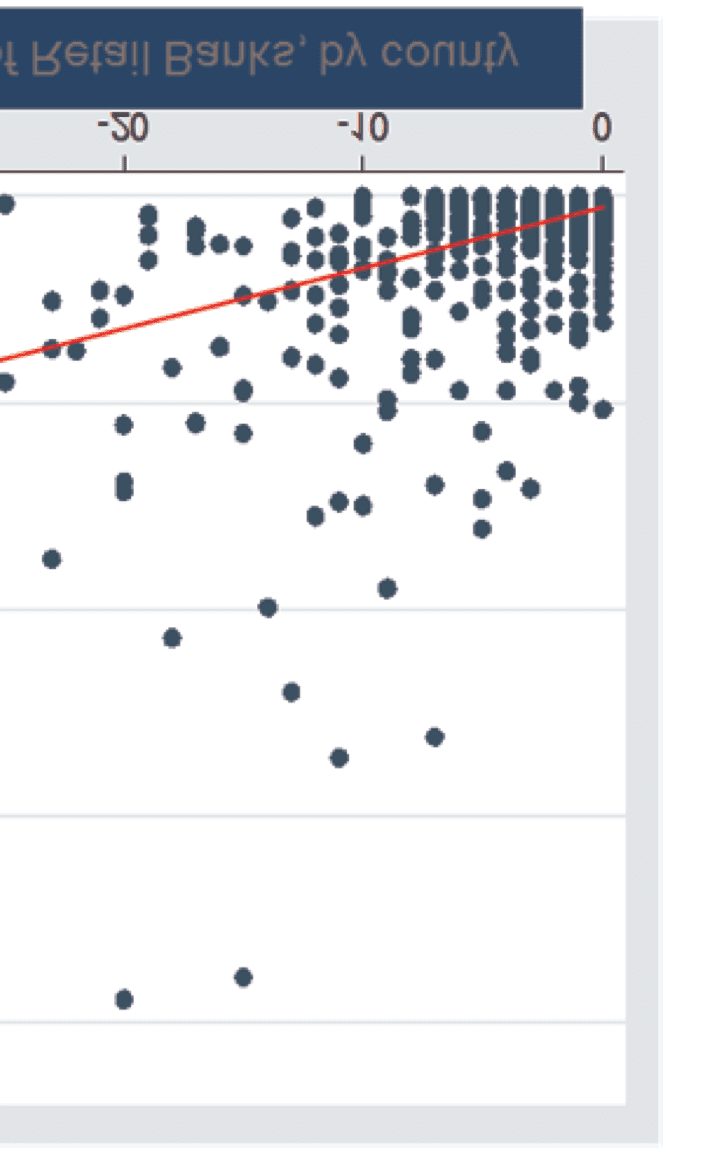

microloans ($100,000 and under) account for 90 percent of SME loans.25 Indeed, the need for small working-capital loans, which a traditional retail bank often con- siders too risky or low profit, can be filled by an online lender that can leverage technology and scale to overcome these difficulties.26 Many firms that obtain financing online report having faced borrowing con- straints that precluded them from obtaining traditional bank loan financing.27 A survey by the National Endowment for Science, Technology and the Arts found that 33 percent of online borrowers said they likely would not have gotten funds through traditional bank loans.28 Traditional loans often require the potential borrowers to provide secure col- lateral before obtaining financing, which can be difficult for smaller businesses, particularly those engaged in intangible products.29 Thirty percent of businesses that responded to a recent survey by the Federal Reserve Bank of New York reported having insufficient collateral as the reason they were unable to obtain funding.30 Lifting collateral requirements has been shown to increase access to credit, which has led to increased hiring and aggregate fixed assets for the busi- nesses that receive financing.31 Traditional brick-and-mortar financial institutions continue to be extremely reluctant to lift collateral requirements, but not so online products. A significant percentage of online business loans are unsecured, significar- ing they do not require collateral. 38 innovaciones / Financial Inclusion II Downloaded from http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023 Filling the Gap Figure 1. Online borrowing and bank departures Source: PayPal data, Federal Deposit Insurance Corporation Lifting the traditional barriers associated with SME financing may lead to pos- itive developments in lending. Cifra 1 plots two sets of data: the change in the number of U.S. bank branches between 2007 y 2014, by county (eje horizontal), and the number of PPWC loans made in the U.S. en 2014, by county (eje vertical). The red line reveals the relationship between the two data series, which is negative, with a correlation coefficient of -0.23. This relationship indicates that a higher proportion of PPWC loans are being disbursed in counties that lost the highest percentage of their traditional retail banks. The data also reveal that nearly 25 percent of PPWC loans were disbursed in the 3 percent of the counties that have lost ten or more banks since the 2008 financial crisis. Technology companies and startups are not the only firms innovating in an effort to fill the SME financing gap. Wells Fargo, a retail bank with more than 6,000 retail branches in the U.S., Por ejemplo, revamped its previously miniscule SME lending product to become the second largest SME lender in the country. As a result, 70 percent of Wells Fargo’s revised data-enabled loan product went to businesses that employ five or fewer people, with an average loan size of just $15,000.32 Además, collaborations between banks and technology companies are

rapidly developing, which could lead to tremendous efficiencies in reaching

underserved SMEs.33

innovaciones / volumen 10, number 3/4

39

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp

S

oh

tu

r

C

mi

:

PAG

a

y

PAG

a

yo

d

a

t

a

,

F

mi

d

mi

r

a

yo

D

mi

pag

oh

s

i

t

I

norte

s

tu

r

a

norte

C

mi

C

oh

r

pag

oh

r

a

t

i

oh

norte

F

i

gramo

tu

r

mi

2

.

l

oh

a

norte

s

metro

a

d

mi

t

oh

yo

oh

w

–

a

norte

d

metro

oh

d

mi

r

a

t

mi

–

i

norte

C

oh

metro

mi

F

i

r

metro

s

40

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Filling the Gap

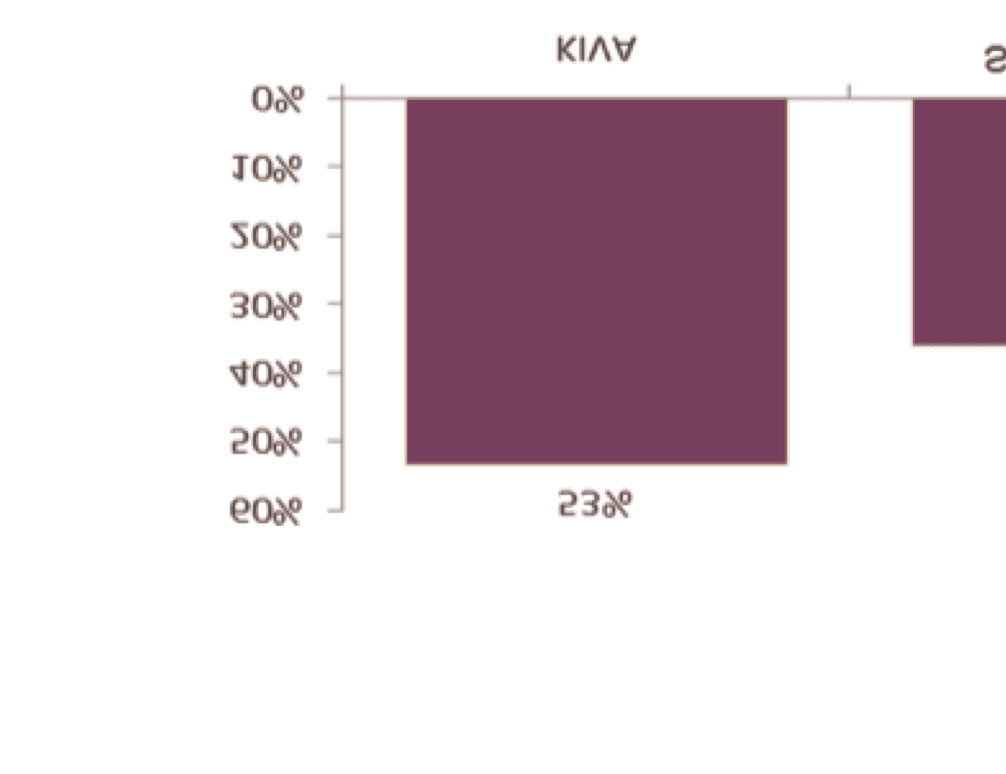

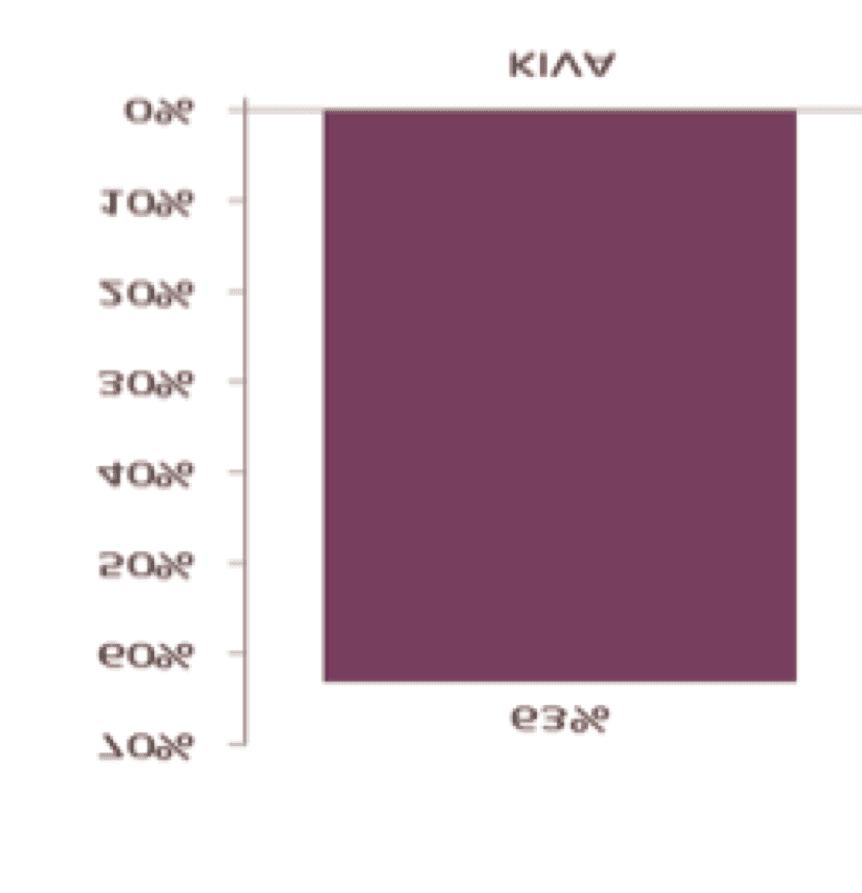

Cifra 3. Lending to young firms

Fuente: PayPal, Kiva Zip

THE DEMOGRAPHY OF ONLINE BORROWERS

SME borrowers that use online channels to access financing come from nearly

every sector and experience level. Hay, sin embargo, some interesting character-

istics unique to the SMEs that use online lending services. Online business loans

disproportionately serve low-income, young, women-owned, and minority-

owned firms.

Data from the Federal Deposit Insurance Commission indicate that approxi-

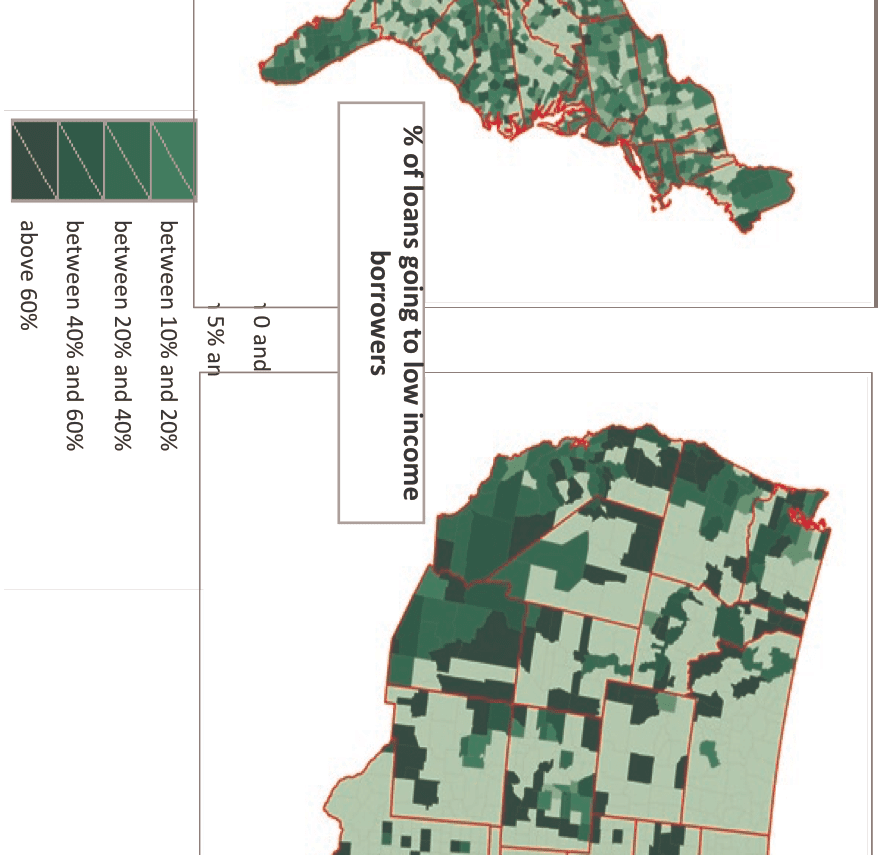

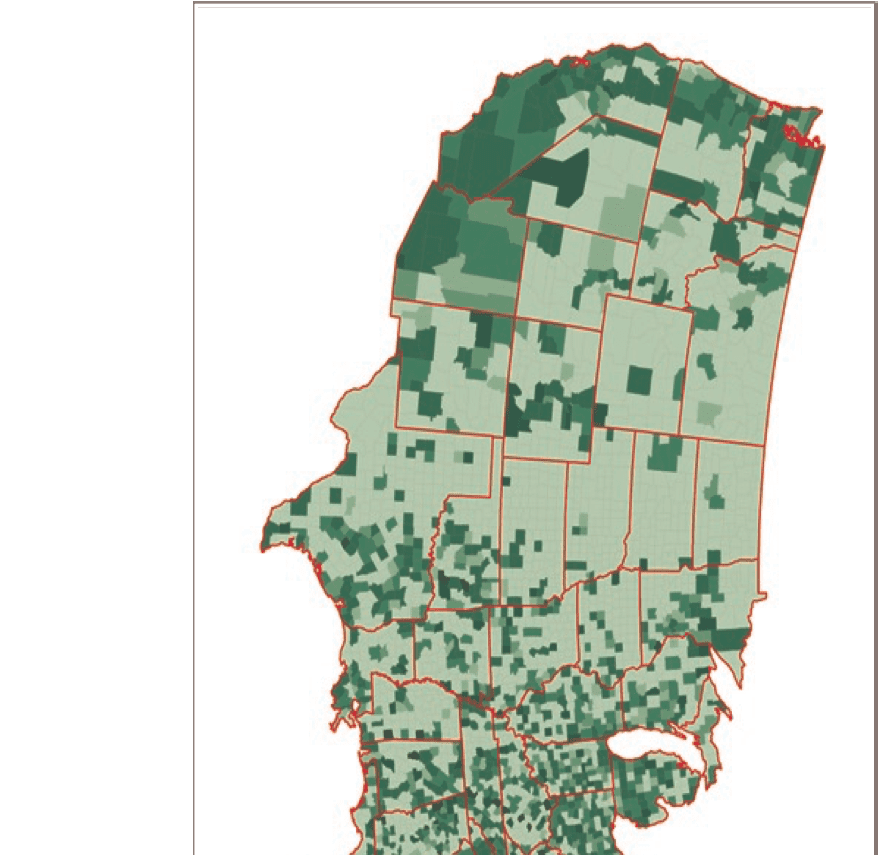

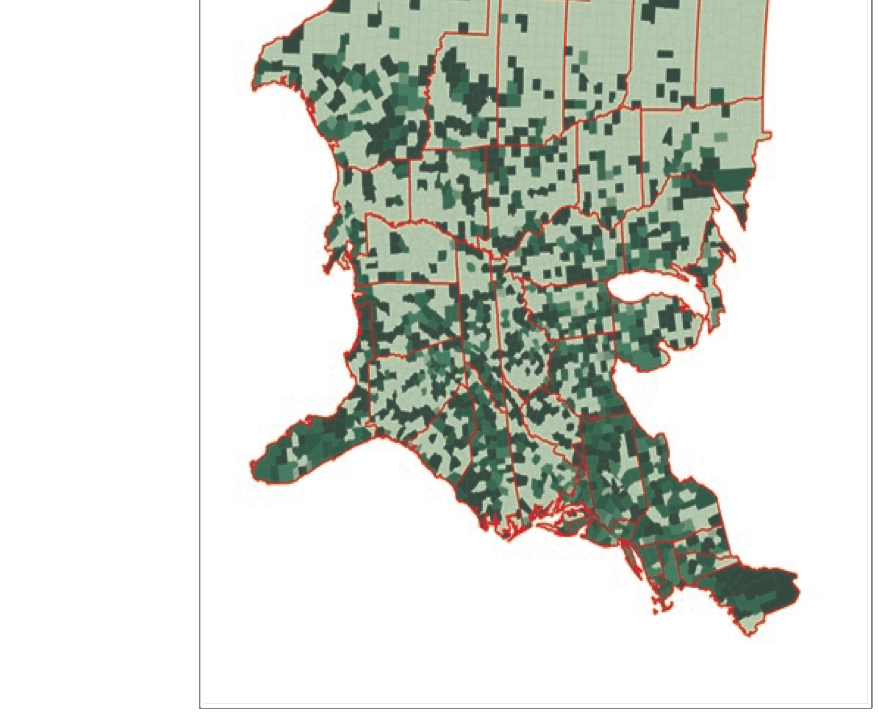

mately 21 percent of the retail bank loans under $100,000 are taken out by low- and moderate-income businesses in the United States, compared to 33.7 percent of PPWC loans of the comparable amount. Bajo- and moderate-income business- es are rarely eligible for traditional loan products, due to the collateral and admin- istrative requirements of traditional bank loans. A recent working paper by the National Bureau of Economic Research demonstrates that the credit expansion created by governments and financial institutions in the wake of the 2008 financial crisis did not serve borrowers with low-FICO scores (often low-income borrow- ers) effectively, but they did benefit those with high FICO scores (often high- income borrowers).34 Cifra 2 compares the U.S. loan activity by county between low-income businesses and traditional brick-and-mortar banks, and between these businesses and the PPWC product. The darker areas indicates that more loans were made to low-income borrowers. Over the last decade, traditional bank financing has been more available for large established firms than small young firms, which has left the latter harder hit by the credit gap.35 A recent survey by the Federal Reserve shows that the majority of small firms (less than $1 million in revenues) and startups (fewer than five years

in operation) en los EE.UU.. are unable to secure credit.36 Newer and younger firms

were three times more likely than established firms to be fully or partially denied

fondos, and this discrepancy is not unique to the United States.37 As a result,

innovaciones / volumen 10, number 3/4

41

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp

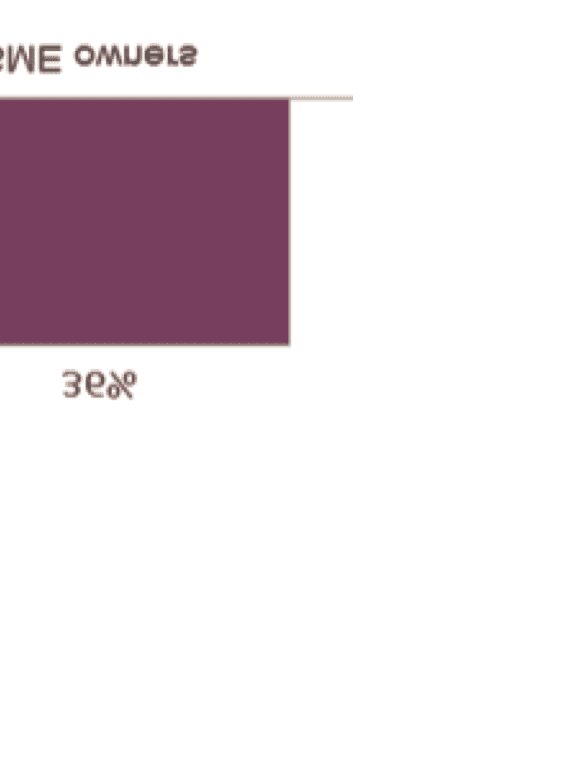

Cifra 4. Women-owned businesses

Fuente: Kiva Zip data (2014) and Small Business Administration (2012)

younger firms that have struggled to secure financing now prefer to pursue the

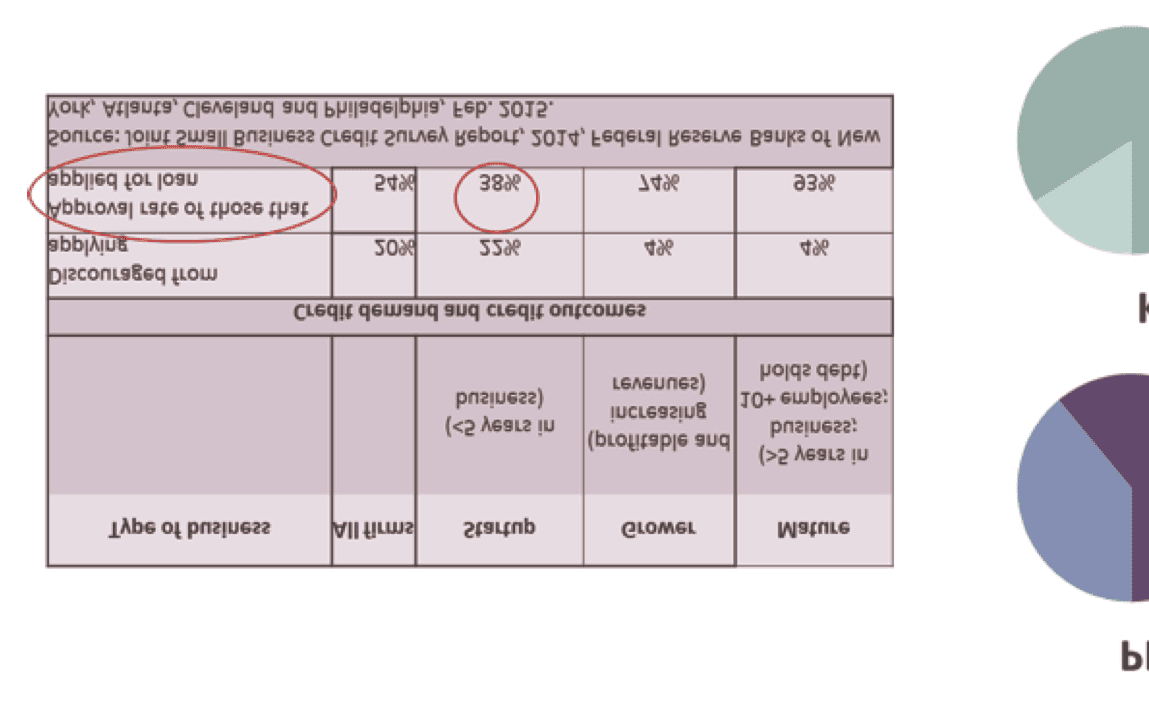

online alternatives. Cifra 3 presents official U.S. data demonstrating the difficulty

young firms face when trying to secure financing—only 38 percent are approved

for loans. It also shows that 61 percent of PPWC loans and 84 percent of Kiva Zip

loans go to young firms.

Women around the globe consistently have less access to financial resources

than men.38 Using U.S. Census Bureau data, the Economics and Statistics

Administration reports that women are half as likely to start or acquire a firm

using a business loan acquired from a traditional financial institution.39

Mientras tanto, women entrepreneurs are disproportionately represented among

Kiva Zip borrowers: 36 percent of SMEs are female-owned, mientras 53 por ciento de

Kiva Zip borrowers are women (see figure 4).

En los Estados Unidos, women-owned firms grow at more than double the rate

of other firms, and they are expected to create more than half of the new jobs in

the U.S. en 2018.40 If the financing issues of women-owned businesses are

resolved, these numbers could be even greater.

Firms operated and/or owned by minorities have traditionally struggled to

secure financing, and they tend to be younger and smaller than the average busi-

ness. This puts them at an immediate disadvantage when accessing financing.41

Census Bureau data indicate that minorities are denied loans at 2.5 times the rate

of non-minorities.42 Black, asiático, and Hispanic businesses have also struggled to

secure loans since the 2008 financial crisis, particularly loans backed by the Small

Business Administration, which has traditionally catered to minority-owned

firms.43 The Small Business Administration reports that only 14.6 percent of

SMEs are minority owned, mientras 63 percent of the Kiva Zip loans go to minor-

ity-owned businesses (see figure 5).

42

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Filling the Gap

Cifra 5. Minority-owned firms

Fuente: Kiva Zip data (2014) and Small Business Administration (2012)

THE ECONOMIC IMPACT

The World Economic Forum’s 2015 Inclusive Growth and Development Report

finds that access to financing is a key link between economic opportunity and out-

comes.44 Financing provided by the private sector can be powerful. A doubling of

the amount of private-sector credit is associated with a two percentage point

increase in the rate of GDP growth.45

SMEs’ access to online lending has resulted in strong growth trends for the

participating companies. Research demonstrates that the most favorable growth

rates result from having access to financing. One study finds that a 10 por ciento

increase in funds is associated with a 14.68 percent increase in firm growth for a

financially constrained firm, but only 3.82 percent for a financially unconstrained

firm.46 We analyzed the growth of firms receiving PPWC loans, which originated

en el 3 percent of U.S. counties that have lost ten or more banks since the 2008

financial crisis. We found that sales by these businesses grew 22.4 percent between

2014 y 2015. Estados Unidos. Census Bureau reports that similarly situated retail busi-

nesses across the U.S. only grew 1.72 percent in that same timeframe.47 If the jump

in sales spurred by an online business loan were extended to every underserved

SME in the U.S., the nation’s economic activity could increase by as much as

$697.95 billion, o 3.98 por ciento de 2015 PIB. We arrive at that number by taking a jump in sales following receipt of an online loan (20.68 por ciento) and multiplying it by the total sales generated by U.S. SMEs in 2015 ($11.38 trillion). We only

innovaciones / volumen 10, number 3/4

43

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp

looked at SMEs the Federal Reserve Bank found were too discouraged to apply for

traditional funding or had already been rejected (29.6 por ciento). To arrive at that

last percentage, we consulted a recent Federal Reserve survey, which shows that 22

percent of SMEs applied for credit and 44 percent of them were not able to secure

funding.48 Moreover, 20 percent of SMEs are too discouraged to even apply.

Together this suggests that 29.7 percent of SMEs (22% de 44% = 9.7%, plus the 20%

just mentioned) are either rejected for a loan or too discouraged to apply for one.

We note further that online lending not only results in economic growth for

SMEs, it benefits consumers through, Por ejemplo, increased product selection

and lower costs.

Online lending also provides economic value to SMEs by bringing competi-

tion to the market for corporate lending, a sector that was sorely in need of new

entrants, particularly in the wake of the financial crisis. Through consolidation

and closings, the number of community banks in the United States has declined

de 14,000 in the mid-1980s to just 7,000 hoy, and only three new commercial

banks have opened in the United States since 2010.49 Before the financial crisis,

SMEs traditionally secured financing from community banks and thus have been

disproportionately affected by these changes.50

Information asymmetry has traditionally plagued SME financing. The lack of

public information about the performance of SMEs can make it difficult to assess

their creditworthiness. Increased competition among lenders could help to pro-

mote innovative solutions to information asymmetry, as well as to alleviate finan-

cial constraints for the SME sector.51 Because the lending market has traditionally

failed to meet demand, governments around the world have stepped in to provide

SME financing, particularly during financial crises, when constraints on borrow-

ing are exacerbated.52 The benefits of increased competition brought on by online

financing might obviate the need for these government programs, which tend to

operate at less than optimal efficiency.53

Finalmente, competition from online lending may reduce systemic risk. El

Organization for Economic Cooperation and Development has found that firms

that solely have access to capital through traditional bank loans are more vulner-

able during crises.54 SMEs have largely been tied financially to a select group of

institutions—namely, community banks—and when these banks started to disap-

pear, SMEs were greatly affected. Online lending provides more diversified lend-

ing options, which can reduce borrowers’ exposure while also spreading the risk

across a broader ecosystem.

Online business lending is still in its infancy; most providers started within the

past decade. Sin embargo, recent Federal Reserve Bank studies have found that 20

percent of SMEs have attempted to secure credit from an online lender.55 A

Greenwich Associates survey of 218 SMEs found that nearly 25 porcentaje de respuesta-

dents had obtained credit from an online provider in the past 18 meses. The eco-

nomic impact of online business lending is likely to grow in the future.

44

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Filling the Gap

POLICY ISSUES

Policymakers must recognize that a multitude of business models are being

employed in the online business lending space, some of which warrant more

scrutiny than others. If the interests of a lender and a borrowing business are

aligned and the lender is invested in a borrower’s success, then there may be less

need for government scrutiny.56 Moreover, risk assessment and collection prac-

tices differ across the online business lending industry. Models that assess risk

without sound data and collection practices should be scrutinized, since they con-

tain inefficiencies and hence result in higher fees. Many of the new types of finan-

cial services have links with existing regulated financial institutions. Por lo tanto, a

the extent that regulators look to propose additional rules for new financial serv-

ices, it is essential to understand the existing landscape and avoid redundant and

inefficient regulations.

It is also worth noting that a host of regulations already govern the online

business space. In the U.S., Por ejemplo, online lenders are subject to Section 5 de

the Federal Trade Commission Act (prohibiting unfair or deceptive practices) y

the Equal Credit Opportunity Act (prohibiting lenders from issuing credit based

on race, sexo, edad, religión, etc.).57 Además, a significant portion of online busi-

ness loans are originated by traditional financial institutions, which are already

subject to a host of regulations.

Policymakers must understand the difference between online business lending

products and traditional lending products. Online SME loans are often short-term

financial products, and the total cost of the loan can be calculated using an annu-

alized percentage rate (APR) or a fee-based model (the loan amount includes

additional fixed costs). Policies regulating traditional loan products often center

around APRs, but this annualized measure often makes no sense for a product

that might have a term of three months. Por lo tanto, an SME may understand the

actual costs of the fixed-fee better than an APR. Policymakers should analyze the

differences between online loan offerings to determine which may be harmful to

SMEs.

Finalmente, although this paper focuses largely on the U.S., the global nature of the

Internet means that online business loans can be made across international bor-

ders. Sin embargo, the differing regulations between countries, and even within coun-

intentos, temper the wide reach of these online platforms. In the U.S., divergent state

banking rules on licensing, interest rates, consumer protection, and due diligence

threaten the ability of online business lenders to provide a uniform experience.58

Policymakers should work to harmonize online business lending rules across

intra- and inter-country boundaries.

CONCLUSIÓN

Traditional financial services are rapidly being reformed by technology. An esti-

acoplado $20 billion in venture capital was expected to be invested in financial tech- nology businesses in 2015, a 66 percent increase over the previous year.59 Startups, innovaciones / volumen 10, number 3/4 45 Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023 Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp large financial institutions, and technology companies are adapting to these changes and creating new financial services solutions that have the potential to fill the gap in SME financing that developed in the wake of the 2008 financial crisis. Además, the impact these new products could have for the broader economy, in particular for financially underserved firms, is noteworthy. Policy interventions that affect new SME financing products must be carefully considered. Acknowledgments The authors wish to thank Olim Latipov, Kornel Mahlstein and Pierre-Louis Vézina for their valuable input, and Jegan VelappanPillai for his data expertise. All opinions expressed in this paper are the authors’ and should not be attributed to the institutions they are affiliated with, nor with the clients they represent. As usual, any errors, flaws, or lapses remain solely the authors’ responsibility. 1 World Economic Forum, The Future of Fintech: A Paradigm Shift in Small Business Finance, 2015; Federal Reserve Banks of New York, Atlanta, Cleveland, and Philadelphia, Joint Small Business Credit Survey Report 2014. 2 International Labour Office, Small and Medium-Sized Enterprises and Decent and Productive Employment Creation, Report IV, 2015; WEF, What Companies Want from the World Trading System, 2015. 3 Peer Stein, Tony Goland, and Robert Schiff, Two Trillion and Counting, 2010. 4 Harriet Taylor, PayPal Has Lent More Than $1 Billion to Small Biz, CNBC, Octubre 27, 2015.

5 See www.kiva.org/about/stats.

6 See http://www.kiva.org/zip.

7 A NOSOTROS. Census, advance monthly sales for retail and food service, not seasonally adjusted, 2013-

2015.

8 Kennickell et al., Small Businesses.

9 European Commission, 2013 SMEs Access to Finance Survey; Mills and McCarthy, The State

of Small Business Lending.

10 Ruth Simon, “Big Banks Cut Back on Loans to Small Business”, Wall Street Journal,

Noviembre, 26 2015.

11 Summary of Deposits Database, Federal Deposit Insurance Corporation.

12 Financing SMEs and Entrepreneurs 2015, OECD, 2015.

13 Financing SMEs and Entrepreneurs 2015, OECD, 2015; Bataa Ganbold, Improving Access to

Finance for SME: International Good Experiences and Lessons for Mongolia, 2008; Thorsten

Beck and Asli Demirguc-Kunt, Small and Medium-Size Enterprises: Access to Finance as a

Growth Constraint, Journal of Banking & Finanzas, 2006.

14 Veselin Kuntchev, Rita Ramalho, Jorge Rodríguez-Meza, and Judy S. Cual, What Have We

Learned from the Enterprise Surveys Regarding Access to Credit by SMEs? 2013.

15 European Commission, 2013 SMEs Access to Finance Survey.

16 Federal Reserve Banks, Joint Small Business Credit Survey; Malhotra et al., Expanding Access

to Finance: Good Practices and Policies for Micro, Small and Medium Enterprises, 2007.

17 Barbara J. Lipman and Ann Marie Wiersch, Alternative Lending Through the Eyes of “Mom

46

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Filling the Gap

& Pop” Small-Business Owners: Findings from Online Focus Groups, 2015.

18 The Economic Impact of OnDeck’s Lending, prepared by Analysis Group, Noviembre 17,

2015; WEF, What Companies Want; Karen Gordon Mills and Brayden McCarthy, The State

of Small Business Lending: Credit Access during the Recovery and How Technology May

Change the Game, Harvard Business School working paper 15-004, 2014; What Works

Centre for Local Economic Growth, Evidence Review, Access to Finance 4, 2014; Malhotra

et al., Expanding Access to Finance; John Rigby and Ronnie Ramlogan, Access to Finance:

Impacts of Publicly Supported Venture Capital and Loan Guarantees, Nesta working paper

13/02, 2013; Ernst and Young, Funding the Future, produced for the G20 Young

Entrepreneur Summit, Junio 2012; Stijn Claessens, Access to Financial Services: A Review of

the Issues and Public Policy Objectives, prensa de la Universidad de Oxford, 2006.

19 Governor Lael Brainard, At the Community Banking in the 21st Century, Third Annual

Community Banking Research and Policy Conference, Calle. luis, Misuri, Septiembre 30,

2015; Community Banks, Small Business Credit, and Online Lending.

20 Arthur B. Kennickell, Myron L. Kwast, and Jonathan Pogach, Small Businesses and Small

Business Finance during the Financial Crisis and the Great Recession: New Evidence from the

Survey of Consumer Finances, 2015.

21 Wehinger, SMEs and the Credit Crunch.

22 Accountants for Businesses, Innovations in Access to Finance for SMEs, 2014.

23 Federal Reserve Bank of Cleveland, Alternative Lending; Lipman and Wiersch, Alternative

Lending; Kuntchev et al., What Have We Learned?

24 Bryan Bodhaine, The Importance of Cash Flow Management for Small and Mid-Size

Businesses, Signature Analytics, Febrero 5, 2015.

25 Federal Reserve Banks, Joint Small Business Credit Survey; European Commission, 2013

SMEs Access to Finance Survey.

26 Lipman and Wiersch, Alternative Lending.

27 The Economic Impact of OnDeck’s Lending.

28 World Economic Forum, The Future of Fintech: A Paradigm Shift in Small Business

Finanzas, 2015.

29 Fleisig et al., Reforming Collateral Laws to Expand Access to Finance, 2006.

30 Federal Reserve Banks, Joint Small Business Credit Survey.

31 Mauricio Larrain and Murillo Campello, Enlarging the Contracting Space: Collateral

Menus, Access to Credit, and Economic Activity, Review of Financial Studies, Noviembre

2015.

32 Malhotra et al., Expanding Access to Finance.

33 Brainard, At the Community Banking.

34 Sumit Agrawal, Souphala Chomsisengphet, Neale Mahoney, and Johannes Stroebel, Do

Banks Pass Through Credit Expansions? The Marginal Profitability of Consumer Lending

During the Great Recession, NBER working paper, Agosto 30, 2015.

35 Leon, Bank Competition and Credit Constraints; Ruth Simon, Big Banks Cut Back on Loans

to Small Business, Wall Street Journal, Noviembre 26, 2015.

36 Federal Reserve Banks, Joint Small Business Credit Survey.

37 Kennickell et al., Small Businesses; Ernst and Young, Funding the Future; Mirjam Schiffer

and Beatrice Weder, Firm Size and the Business Environment: Worldwide Survey Results,

IFC, 2001.

innovaciones / volumen 10, number 3/4

47

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023

Usman Ahmed, Thorsten Beck, Christine McDaniel, and Simon Schropp

38 International Finance Corporation and Global Partnership for Financial Inclusion,

Strengthening Access to Finance for Women-Owned SMEs in Developing Countries, Octubre

2011.

39 Women-Owned Businesses in the 21st Century, A NOSOTROS. Department of Commerce, Ciencias económicas

and Statistics Administration, Octubre 2010, pag. 18.

40 International Finance Corporation & Global Partnership, Strengthening Access to Finance.

41 David G. Blanchflower, Phillip B. Levin, y David J.. Zimmerman, Discrimination in the

Small-Business Credit Market, La revista de economía y estadística., 85(4) 2003: páginas. 930-

943.

42 Access to Capital for Women- and Minority-Owned Businesses: Revisiting Key Variables,

Small Business Administration, issue brief number 3, Enero 2014, pag. 2.

43 Ruth Simon and Tom McGinty, Loan Rebound Misses Black Businesses, Wall Street

Diario, Marzo 14, 2014.

44 World Economic Forum, Inclusive Growth and Development Report, 2015.

45 Stijn Calessens, Access to Financial Services: A Review of the Issues and Public Policy

Objectives, prensa de la Universidad de Oxford, 2006.

46 Rahaman, Access to Financing and Firm Growth.

47 A NOSOTROS. Census, Monthly and Annual Retail Trade, non-seasonally adjusted; these calculations

are based on the 12-month period November 2013-October 2014 and November 2014-

Octubre 2015.

48 See Board of Governors of the Federal Reserve System, Availability of Credit to Small

Businesses, Septiembre 2012, Mesa 7, Overall credit application experience, 2009-2011.

49 Heather Long, Weird: Solo 3 New US Banks Opened Since 2010, CNN, Julio 29, 2015; Mills

and McCarthy, The State of Small Business Lending.

50 Kuntchev et al., What Have We Learned?; Federal Reserve Bank of Cleveland, Alternative

Lending.

51 Leon, Bank Competition; R. METRO. Ryan et al., Does Bank market power affect SME financing

constraints?, Journal of Banking & Finanzas 49, 2014; Id.; Terence Tai-Leung Chong, Liping

Lu, and Steven Ongena, Does Banking Competition Alleviate or Worsen Credit Constraints

Faced by Small and Medium Sized Enterprises? Evidence from China; Beck and Demirguc-

Kunt, Small and Medium-Size Enterprises Across the Globe, Small Business Economics,

2007.

52 Wehinger, SMEs and the Credit Crunch.

53 What Works, Centre for Local Economic Growth, Evidence Review, Access to Finance 4,

2014.

54 Wehinger, SMEs and the Credit Crunch.

55 Lipman and Wiersch, Alternative Lending; Federal Reserve Banks, Joint Small Business

Credit Survey.

56 Joe Valenti, Sarah Edelman, and Julia Gordon, Lending for Success, Center for American

Progress, 2015.

57 Chapman and Chapman, The Regulation of Marketplace Lending: A Summary of the

Principle Issues, 2015.

58 Id.

59 KPMG and H2 Ventures, Fintech 100: Leading Global Fintech Innovators Report 2015.

48

innovaciones / Financial Inclusion II

Descargado de http://direct.mit.edu/itgg/article-pdf/10/3-4/35/705146/inov_a_00239.pdf by guest on 08 Septiembre 2023