Dylan Higgins, Jake Kendall, and Ben Lyon

Mobile Money Usage Patterns of

Kenyan Small and Medium Enterprises

Some people expect to see small and medium enterprises (SMEs) benefit substan-

tially from using mobile money (MM). SMEs are often seen to process large num-

bers of payments and can have a surprising amount of money flowing through

a ellos. Al mismo tiempo, their need for payment and transactional services are not

always well served by traditional banks. They do not always find it easy or cost

effective to adopt a full-featured package of banking services as a larger business

might. Anecdotal evidence seems to confirm that many small businesses use MM

intensively in markets where it is available; sin embargo, the phenomenon is not well

documented or researched. En respuesta, in late 2011, we conducted a survey of 865

SMEs in Kenya to better understand MM adoption patterns in one of the most

active markets in the world.

We found that whether Kenyan SME owners use MM to pay utility bills or

salaries or suppliers, they are driving higher volumes of both MM adoption and

transactions. Our data show that of the 865 SME owners who responded, 861

(99.5%) used MM in their personal or business dealings, y 67% used it for busi-

ness. SMEs are intensive users compared to consumers; 80% report using MM

once per week or more, whereas the average usage in Kenya is closer to twice a

mes. SMEs also appear to promote viral adoption along the supply chain; muchos

say they adopted it because clients or suppliers asked them to. For these reasons

SMEs should be a critical market segment for mobile network operators who seek

to make MM usage pervasive across the value chain from consumers, to mer-

chants, to suppliers.

We also found that while MM use by SMS is widespread, it is not yet deep and

SMEs are not yet “closing the e-loop.” Most SMEs use MM on a one-off basis and

do not actively promote MM at the point of sale. En particular, SMEs are not yet

Dylan Higgins is the CEO and Cofounder of Kopo Kopo, a merchant aggregator for

mobile money systems.

Jake Kendall is the Program Officer managing the research strategy in the Financial

Services for the Poor initiative at the Bill & Fundación Melinda Gates.

Ben Lyon is the Head of Product and Cofounder of Kopo Kopo.

© 2012 Dylan Higgins, Jake Kendall, and Ben Lyon

innovaciones / volumen 7, number 2

67

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

closing the e-loop by receiving large volumes of retail transactions electronically

and then paying out to employees in electronic value – both retail transactions and

wage payments were predominantly cash. We did find that 28% reported accept-

ing MM retail payments, a figure we found higher than expected given the high

pricing of transactions and lack of a convenient interface. Enticing SMEs and other

businesses to close the loop will be a major part of the endgame for MM operators

who hope to move toward a cash-light world.1

Finalmente, our survey found several barriers that have prevented people from

using MM. Específicamente, respondents cited high tariffs and inadequate access to

record-keeping and payment-management interfaces as main barriers to adoption.

In order to make MM ubiquitous, MM providers and their partners will need to

keep an eye on cost and convenience and offer value-added services beyond the

transaction.

CONTEXT

Three recent studies document how MSMEs (micro, pequeño, and medium enterpris-

es) are using MM, but the data sets are limited.2 In general, this work shows that

MSMEs are using MM more intensively than regular consumers, but it also shows

that MSMEs are not “going digital” and using MM extensively for a large percent-

age of their business transactions.

One study of users of MTN MM in and around Kampala, Uganda, was con-

ducted in 2009 by Ali Ndiwalana, Olga Morawczynski, and Oliver Popov.3 They did

not set out to investigate business users, but when they asked their survey respon-

dents what they were using MM for, aside from airtime purchases, they found that

cerca de 33% of transactions were to purchase or sell goods or services, while the

remaining two thirds were for money transfers. Larger formal businesses in

Uganda do not usually accept MTN MM as a means of payment, so it’s likely that

most of these purchases and sales transactions were conducted by entrepreneurial

individuals or small businesses on one side or the other. This is a significant level

of usage, given that MM has never been marketed for retail or business payments.

It speaks to the high level of need in this group.

In another study, Lennart Bångens and Björn Söderberg4 interviewed 110

MSEs in Tanzania about their use of MM. (These were just micro and small enter-

tomado, not medium-sized ones). They found that, in Tanzania, business owners use

MM much more than the national average, and that many report significant ben-

beneficios. The main benefit these entrepreneurs reported was increased efficiency,

because of time saved and improved logistics. Most find MM much easier than

banks: the locations are more accessible, customer service is better, transactions

are quicker, and it’s much easier to sign up for an account. dicho eso, agents often

didn’t have the float to meet the larger transaction sizes that SMEs require and

some reported having to visit two or three agents to get the cash or float they need-

ed. The authors also believe that SMEs may help “diffuse” MM by prompting cus-

68

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

tomers and suppliers to sign up—yet another reason they may be of high value to

mobile network operators as early adopters. Our data also support this claim.

In a more recent study, Ignacio Mas and Amolo N’gweno5 investigated how

businesses in Kenya use the M-PESA product, focusing on medium and large busi-

nesses rather than on micro and small businesses. They found that formal busi-

nesses were very slow to adopt MM. In discussions, such businesses identified

multiple barriers to integrating MM more fully into their payment systems. Ellos

say MM is hard to integrate into corporate IT systems, and it is impossible to move

money quickly between bank accounts and M-PESA accounts; they also see chal-

lenges with adapting legacy paper-based processes to a new system. También, the sys-

tem offers no options for paper receipts or transaction confirmation, and has no

way to handle misidentified transactions. Y, without any arbitration process,

they fear fraud and transaction reversals. The product’s existing features are limit-

ed: web interfaces are inflexible, application program interfaces (APIs) are inade-

quate, and they experience too much system downtime. Finalmente, Safaricom does

not target its sales, marketing, and services to this segment.

Given all these barriers, most formal businesses rely on checks, bank transfers,

and cash to make payments. The authors do note that many small and informal

businesses—like those our survey focuses on—do not have ready access to these

opciones, so they use MM more frequently out of necessity.

This is the point of departure for our survey; we seek to understand how this

segment uses MM and to diagnose the barriers to greater use and integration.

OUR SURVEY: SAMPLE SIZE, DATA, SECTORS, CONNECTIVITY

Our goal in this study was to collect data to answer three questions: Do SMEs

leverage MM for business purposes, and if so, cómo? What challenges do they face

al hacerlo? And how can commercial providers better serve this important mar-

ket segment?

Our survey team approached 1,000 SMEs throughout Kenya: 600 in Nairobi,

200 in Mombasa, 100 in Nakuru, y 100 in Kisumu. SMEs were selected at ran-

dom from Mocality.com, a database of over 160,000 Kenyan SMEs. By necessity,

our sample focused on urban and semi-urban businesses that had registered with

Mocality. Thus our sample is biased toward larger, formal businesses and away

from the large pool of informal single-person businesses that dominate the land-

scape in much of Africa. Sin embargo, 50 percent of our sample was small busi-

nesses engaged in various lines of work (p.ej., airtime vendor, salon, restaurant,

etc.); 13.6 percent of them, o 127 respondents, were one-person businesses. El

remaining 50 percent were medium-sized businesses. We received quality respons-

es from 932 negocios.

El 932 Kenyan SMEs in our sample had a total of 13,000 employees. El

average number of employees per business across all cities was 14.3, with a medi-

an of 5; 13.6 percent were sole proprietorships. The mean was significantly higher

than the median because several businesses employed over 100 gente. Though

innovaciones / volumen 7, number 2

69

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

Cifra 1. Do you have regular access to the Internet?

small by definition (bajo 50 percent had five employees or fewer), the SMEs in

our sample were likely larger on average than a fully representative national sam-

por ejemplo, given that we did not sample in rural areas and may have missed many infor-

mal, one-person businesses since we used the Mocality database.

The SMEs in our sample were highly connected. Of the SMEs that responded,

94.1 percent own a mobile phone, compared to the national average of 74 percent.6

Como figura 1 muestra, Internet connectivity was also high; 60.6 percent of respondents

have regular Internet access via either a mobile phone or a PC. The fact that the

SMEs in the sample were highly connected highlights the opportunity to reach

them with properly-designed mobile and Internet-enabled services.

The SMEs in our sample did a significant volume of business daily, a total of

about Kenya Shillings (KSE) 49METRO (US$515,000). Though most of them have only a few employees—or only one—their average daily revenue was KSE 56,825 ($600)

with a median of KSE 10,000 ($105). Del 617 respondents who were willing to supply revenue information, the sum of revenues was KSE 36.7M ($390,000) por

día. This high turnover indicates many payments and much cash moving in and

out of businesses.

Services and retail were by far the dominant business activities. Of these busi-

nesses, 50% classified themselves as services, 33% as retail or trading, 12% as man-

ufacture, y 5% as other. Thus this sample is biased more toward services and

retail than the Kenyan economy as a whole; encima 20% of the Kenyan GDP comes

from industry or manufacturing. This is to be expected for a sample of SMEs, como

manufacturing firms tend to be larger. These are businesses with large unmet

needs for payment services, especially in the retail sector.

70

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

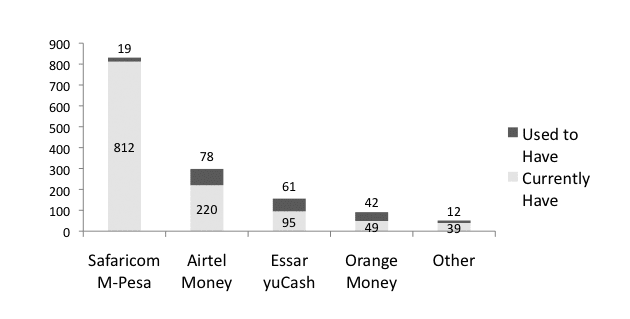

Cifra 2. Do you use any of the following MM services?

How Has Mobile Money Spread to Small and Medium Enterprises?

In our sample of SMEs, rates of MM adoption are extremely high. All but one of the

865 SMEs that responded to the question on MM usage had used MM; four had

used it but stopped. De este modo 99% of those who responded had at least one active MM

cuenta. Además, 67% of respondents reported using MM for business pur-

poses while the others reported personal uses. Of the users, 72% had one account

y 28% had more than one. Cifra 2 shows which services they reported using.7

While Safaricom is clearly the leader in total numbers, it also seems to have a lower

churn rate, as evidenced by the smaller proportion of users who are former users.

Many businesses used MM quite intensively. A total of 80.3% of respondents

claimed to use MM at least once a week; 25.1% use it every day, 43.8% use it a few

times a week, y 11.4% use it once a week. Data from Safaricom in 2010 presentado

that the average M-PESA user was making two transactions a month;8 this indi-

cates that SMEs are quite intensive users of the MM service compared to the rest

of the population. dicho eso, many were still making many of their payments in

cash, as Table 1 muestra. This indicates that MM still has some way to go to displace

cash significantly within Kenyan SMEs.

MM usage by SMEs may promote viral adoption. Most respondents said they

use MM either because customers ask to pay with it (47.8%), or because sales

agents or suppliers ask to be paid with it (38.6%)—and many (13.7%) indicated

that requests from both customers and suppliers were a factor. Most of those who

responded “other” indicated that convenience and safety were their paramount

reasons for choosing MM over other methods. The fact that customers value the

ability to pay with MM and that SMEs’ business partners prompt each other to take

up the service shows it spreads virally up and down the supply chain. This indi-

innovaciones / volumen 7, number 2

71

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

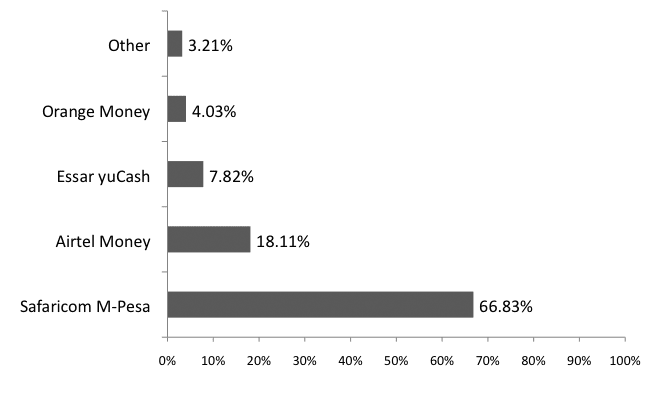

Cifra 3. Which (if any) do you use for business?

cates that MM operators may wish to target SMEs to encourage the viral adoption

ciclo.

SMEs are more frequent adopters and more intensive users than other cus-

tomers and they appear to promote viral adoption to their customers and along the

supply chains. De este modo, SMEs would appear to be a very important segment for MM

schemes to target.

How Do Small and Medium Enterprises Currently Use Mobile Money?

The idea that MSMEs use MM should come as no surprise, since they have a lot to

gain from it’s use. As our data shows, they need to pay and be paid frequently,

sometimes in quite large amounts or over long distances. This implies that they

could lower their costs and save time with a cheaper and more convenient way to

pay electronically. They also need to manage their working capital to get the most

from it, which means turning it over as often as possible: speeding up the cycle

from cash to inventory to receivables and back to cash, but replacing cash with

electronic value. SMEs also find it useful to have a record of transactions, as they

often do not keep formal records but do deal with many customers and suppliers.

Thus they often hold many ledgers, receipts, and debts in their head.

MM is gaining ground against cash for many types of payments

While cash is still king for all types of receipts and payments, MM has made sig-

nificant progress, especially in the areas of paying suppliers and paying bills: two

areas where more sophisticated counterparties may ask or even require MM pay-

mentos, as compared to employees and customers. Differences in the level of adop-

72

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

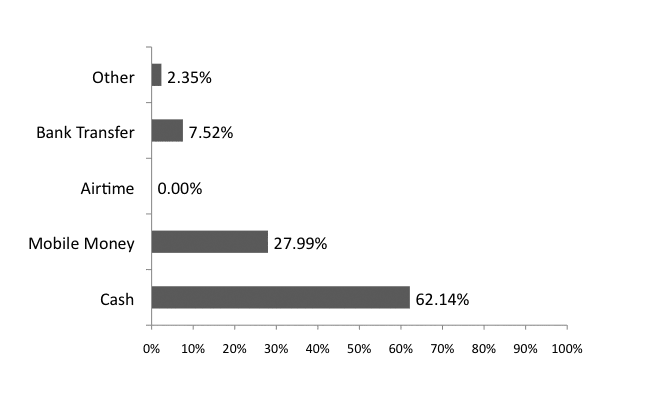

Cifra 4. How do Customers pay?

tion for bill-paying between Mombasa and Nairobi illustrate this trend.

Respondents in Mombasa use MM the least (24.22%) and those in Nairobi use it

the most (34.15%). The fact that SME owners in Mombasa use MM to pay suppli-

ers suggests that bill providers there may have less access to corporate MM

accounts than their counterparts in Nairobi where penetration in the corporate

sector is greater.

Cash, MM, and bank transfers are the most common ways businesses pay bills,

en 38.21%, 30.8%, y 26.95% respectivamente, as shown in Table 1.

Respondents across all cities prefer to use cash and MM to pay suppliers, con

bank transfers accounting for only 18.34% of responses. En cambio, it appears that

cash and bank transfers remain the most popular methods for paying employees,

con solo 11.39% of respondents using MM. Paying rent is the one area where cash

does not dominate all other forms of payment; aquí, bank transfers are the most

common way to pay, across all four cities.9

Given the potential benefits of converting their various payment streams to

electronic forms of payment, it is no surprise that SMEs are converting to MM,

despite the lack of convenient interfaces, ways to track transactions and manage

records, and limited pricing options. Being able to receive MM payment from

clients more quickly allows them to more quickly convert receivables to cash; sim-

ilarly, being able to arrange delivery and pay over the phone increases efficiency on

the other end by moving cash into inventory more quickly and making arrange-

ments at lower cost. Al mismo tiempo, because business owners can more quickly

order more supplies, they can reduce the inventory they hold and not wait to run

innovaciones / volumen 7, number 2

73

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

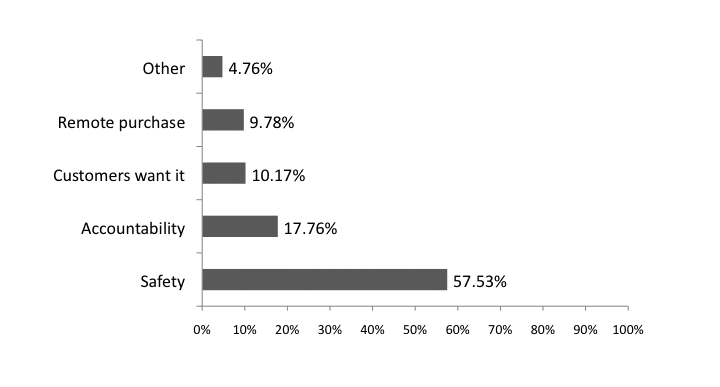

Cifra 5. What is the main benefit of receiving mobile payments?

out before ordering more, which also speeds turnover. In this sense they are mov-

ing toward the just-in time style of production practiced by many larger firms.

Mobile Money penetration for retail payments is surprisingly high

Como se esperaba, cash remains king at the point of sale: 62.14% of respondents across

all cities said their customers use cash. Sin embargo, 28% of respondents across all

cities claim that customers pay them with MM. While these respondents receive

payments in other forms, it is striking that so many report receiving some pay-

ments via mobile, especially given the lack of a convenient interface for retail pay-

ments and pricing geared toward money transfer.

Mobile Money is safer and helps with record keeping and tracking

When asked about the benefits of accepting MM, respondents across all cities said

safety was the paramount benefit, followed by better accountability, as the SMS

receipt leaves a paper trail. This paper trail helps reduce leakage and error, si

by employees or customers, and makes business owners more confident that their

books are accurate. This point is especially salient for businesses that sell services,

which cannot be easily accounted for in the same way that payments can be

tracked against inventory for retail and manufacturing businesses.

Barriers to Adoption

MM is becoming a prominent method of transaction for business purposes. Still,

it is clear that several impediments, especially tariffs and the user interface, prevent

MM from becoming even more prominent.

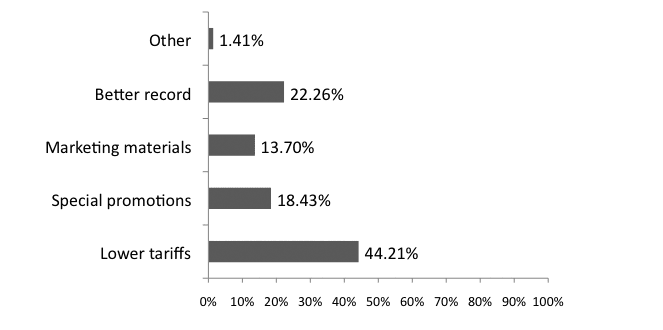

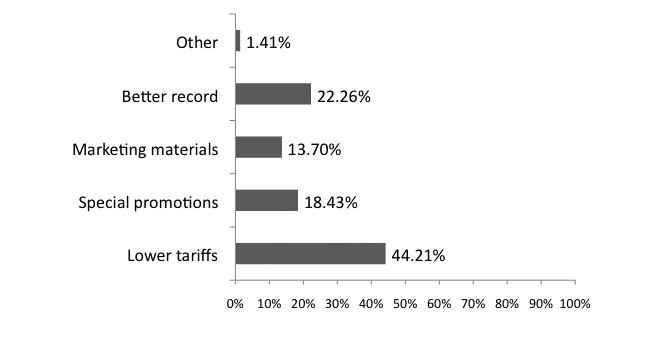

As Figure 6 muestra, tariffs are the biggest impediment to more businesses

adopting MM. The high cost of person-to-person transfers and the lack of differ-

74

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

Cifra 6. What would make it easier to accept mobile payments?

entiated pricing for different types of bulk users or for different types of transac-

ciones (p.ej., in-store retail payments) is a significant barrier to market growth. El

customer and/or business pays a variable tariff, depending on the kind of transac-

ción: p.ej., Send Money, Buy Goods, or Pay Bill. If a business sells inexpensive

goods, the relative tariff is either prohibitively high to the customer, the margin less

the tariff is prohibitively high to the business, or both. De este modo, the existing tariff

structure is not compatible with most common transactions–the small, frecuente

payments for daily servings of fast-moving consumer goods.

A second barrier is the lack of a user-friendly interface to facilitate business

uses and record-keeping. While M-PESA has a limited interface where users can

check their transaction history, it is very basic and lacks the kind of record man-

agement and other functionality that would make it easy for businesses to use it.

So, while many MSMEs do report relying on their SMS history from M-PESA as a

crude form of electronic record-keeping, the lack of functionality here is a clear

barrier.

These two barriers were echoed in two recent studies on new financial prod-

ucts that leverage the MM platform in Kenya. Both found that pricing and poorly

performing APIs are significant barriers to developing products that leverage

MM.10

Solo 17 respondents (1.94 por ciento) said they do not accept MM because no

agent is nearby. This is not to say that agent service is not a major concern of SMEs;

instead it shows how successfully Safaricom has blanketed the Kenyan landscape,

with over 30,000 agents. Other services, in Kenya and abroad that have significant-

ly fewer agents have experienced significant churn among SMEs (ver figura 2).11

We asked the respondents who do not accept MM or who discourage their cus-

tomers from paying with it for their reasons. Across all cities, 38.47 percent of

innovaciones / volumen 7, number 2

75

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

Mini-case: Dennis, furniture business

Dennis is 35 years old. He is one of the five partners who operate Sakaki

Enterprise, located at the Githurai 45 roundabout. Githurai is a mixture of slums

and suburbs in the eastern part of Nairobi. Sakaki makes and sells furniture—

sofa sets, tables, chairs, etc.—at prices that range from KES 3,000 to KES 30,000

($34.76 a $347.60). Dennis says their business operates with mostly cash. Ellos

use no accounting software, and they keep their records in paper notebooks.

Sakaki relies heavily on M-PESA for most of its transactions. It buys raw

materials every week from the Gikomba market, using M-PESA. “We usually

pay the supplier with M-PESA in advance so that he can deliver the raw materi-

als to us once or twice every week,” says Dennis. Dennis pays the suppliers

between KES 10,000 and KES 20,000 ($116 y $232) every week using M-

PESA. Sakaki also pays its employees with M-PESA. This is very convenient for

Sakaki; it saves them time.

Many of Dennis’s customers ask to pay with M-PESA, especially those who

buy furniture worth KES 20,000 or more. Dennis says that Githurai is a very

insecure area and that paying with M-PESA is the best option for his customers

and for Sakaki too.

Dennis says that the greatest challenge he and his partners face is lack of cap-

ital to expand and grow their business.

Thanks to Peter Gakure-Mwangi

respondents said, “I prefer cash,” and 28.54 percent said the tariffs are too high.

The responses above were corroborated by those to our Question 11—“What

would make it easier for you to accept MM?”—to which 44.21 porcentaje de respuesta-

dents chose lower tariffs. It is worth noting that 22.26 percent of respondents said

they would like an electronic record of MM transactions. If respondents use indi-

vidual MM accounts to accept business payments, this response makes sense as

few MM systems enable users to access a transaction statement.

How can mobile money schemes and service providers best reach small and

medium enterprises?

Our analysis and discussions with SME owners have uncovered a few possible

ways that commercial players could target SMEs as an MM user group. To drive

adoption, MM players need to understand the unique needs of SMEs that tend to

be intensive users, in terms of both volume and number of counterparties.

To manage their relationships and higher volume, SMEs need good tools for

records management and tracking. Paper record-keeping remains the status quo

for many SMEs in Kenya. The electronic record associated with an MM transac-

tion presents a unique opportunity to incentivize SMEs to adopt electronic record-

keeping for the first time. Específicamente, electronic records allow SMEs to reduce the

76

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

Cifra 7. Why do you NOT accept mobile payments?

“cost of cash”: seguridad, counterfeit and leakage risks, transport, customer

anonymity, etc..

Because SMEs have varied needs, mobile operators can avoid the cost of pro-

viding these record-keeping tools by offering data interfaces such as application

programming interfaces, which can be leveraged by the software community. El

challenge will lie in finding the market-appropriate tools and processes that nudge

an SME to adopt an electronic method to replace existing mental or paper records.

Our findings indicate that a significant step driving adoption would be to improve

both the content of the transaction record, by including the source and purpose of

payments, and to improve access to the record in the form of an online or SMS-

based interface.

In addition to better record-keeping, SMEs need a set of features that motivate

them to adopt MM. These features include the ability to manage the reversal of

transactions and to accept retail payments with fees that are at or below credit card

tarifas, and flexible and speedy bank settlement options.

Perhaps more than anything, SMEs need to be offered a platform to change

their consumers’ perspective on MM. Customers are still forced to inquire whether

an SME accepts MM payments. To reach scale, they must be able to assume that

every merchant does so—just as many merchants now assume that every individ-

ual has an MM account.

When the two-sided payment market is in place, Kenya will be well on its way

to becoming a cash-light society. Consumers will not be forced to convert MM

value into cash in order to transact with businesses. Similarmente, businesses will be

able to use their electronic value to pay their suppliers and avoid the need to deliv-

er cash payments in person. Along the way, these different payments will be bet-

innovaciones / volumen 7, number 2

77

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

ter managed and tracked by all of the parties in the payment value chain because

of the electronic records associated with these transactions.

Fast forward. Imagine a Kenya where MM has fully saturated the SME value

cadena: merchants use it to pay suppliers, suppliers use it to pay employees, employ-

ees use it to pay merchants, etcétera. That is the “endgame” for MM providers: a

system whereby MM is issued, cycled, and retained within a closed loop. The same

ubiquity that made M-PESA the preferred way to send money home would then

become the impetus for using MM on a daily basis for (mostly) frecuente, pequeño

transactions. Operators would benefit from a virtuous circle resulting in higher

average revenue per user, consumers would benefit from increased security and

convenience, and merchants would benefit from increased business intelligence

and accountability.

To achieve the endgame, our results indicate that operators will need to keep a

close eye on cost and convenience and should focus on developing tools in-house

and through partnerships that offer market-appropriate solutions to SMEs.

CONCLUSIONS

SMEs are a valuable market segment for mobile operators and their service

providers but they have special needs.

Primero, SMEs may be especially valuable as nodes in driving the viral uptake of the

MM product or product features. As we noted above, they tend to adopt MM

because their customers and/or suppliers do. And because they are just as often

customers and suppliers of other small or large firms, they are likely to be strong

propagators of the product along the value chain.

Similarmente, because SMEs are often in the retail business, they also represent an

opportunity to begin to drive customers to adopt MM for retail payments; for that

to happen, it will have to become a ubiquitous form of payment that is both con-

venient and affordable.

Businesses want to use MM, and many do. Pero, many more would do so if the

tariffs were lower and if the service quality and product features associated with

M-PESA fit the special needs of SMEs. Mas and N’gweno12 list seven ways the M-

PESA platform could be improved to serve business better: features to assure ver-

ification of the sender/receiver, easier process for reversing payments sent to the

wrong number, a paper receipt option, secure APIs to allow business integration,

easy sweeping of funds to/from bank accounts, an integrated interface for paying

and receiving and records management, and efficient dispute resolution.

Most of these features would be useful for MSMEs too. Además, MSMEs

have special needs that should be taken into account. En particular, an MM offer-

ing for merchants should incorporate ways to access these features through limit-

ed interfaces like web and smartphone, rather than integrating them into back-end

IT systems that few MSMEs have.

78

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

Given that a majority of the Kenyan economy operates informally, at low mar-

gins, for small value purchases, the tariffs alone are a significant impediment to

more MSMEs adopting MM. In order to take MM to the next step—retail and

value chain payments—it is imperative that tariffs be reduced.

Businesses also want marketing materials in order to educate customers that

they can pay with MM—in the same way that VISA, MasterCard, and Amex pro-

vide stores with logos and other signage to show which merchants accept their

cards. Mobile operators are particularly adept at marketing and should launch

campaigns to encourage people and organizations to pay with MM.

At the heart of any successful business lies a strong record-keeping system.

Mobile operators should recognize that they can help businesses grow through bet-

ter communication and better payments, and also by enabling them to improve

their accounting. Many MSMEs could benefit from even rudimentary Internet- o

smartphone-based record-keeping and customer relationship management sys-

tems to manage payments and cash flow. Such functionality could induce them to

take up mobile payments.

Smart regulations are required to protect existing players and allow new ones

to flourish.

Regulators have enabled innovation to flourish in Kenya. Ahora, many of the pay-

ment innovators are well established and it is time to level the playing field.

Regulators should facilitate healthy competition between MM providers and

encourage new market entrants by reducing barriers to entry. They should be espe-

cially careful to ensure that MM players do not abuse their control of the commu-

nications channels (voice, SMS, or USSD) that facilitate mobile financial transac-

tions and thus disadvantage other entrants, like banks, that could also offer finan-

cial products and services over the network.

Además, regulators and policymakers should take a market-level view of

encouraging the transition to electronic “cash light” by engaging with operators

and other players around issues of pricing, service quality, and the platform func-

tionality to enable the widest range of uses, and thereby greater innovation.

New and unique business models will need to be tested to serve the Kenyan

market. These models will be tested by banks, mobile operators, and third parties,

and no party should be given an unfair advantage over the others.

Empowering SMEs empowers the economy: SMEs are major drivers of

employment and economic activity.

M-PESA revolutionized the Kenyan market and inspired a global industry. Tiene

slashed the transport and opportunity costs associated with domestic remittances,

lowered the cost of distributing airtime, and helped millions access basic financial

tools for the first time.

innovaciones / volumen 7, number 2

79

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Dylan Higgins, Jake Kendall, and Ben Lyon

Mini-case: Juma, shopkeeper

Juma is 34 and operates a mini shop (duka) at Dandora Phase 2 estate. Dandora

is a populous low-income estate in the Eastlands area of Nairobi. He runs the

shop with his wife and they have two small children.

Juma serves an average of 30 customers each day; most are neighbors. Él

sells mostly foodstuffs like milk and bread, and detergent in small packets. Su

most common transaction size is KES 200 ($2.30).

Juma says that very few of his customers ask to pay him with M-PESA. “My

customers always pay me with cash. They mostly buy small quantities of things

like sugar, soap, and bread, so there is no point in them paying with M-PESA.”

But Juma says that some customers pay with M-PESA. “The customers who

pay me with M-PESA are only the ones that I know and trust. Some take goods

on credit and they pay with M-PESA at the end of the month.” However, Juma

says that he cannot turn away a customer who has only M-PESA and has no cash

at hand. He says he would accept M-PESA plus an additional withdrawal

amount. “But in a case where I don’t know the customer, I have to withdraw the

money immediately, or just hope that the customer will not reverse the transac-

tion.”

He explains, “I pay my supplier with M-PESA in advance so he can deliver

the goods to my shop. That way I don’t have to leave my business to go and buy

cosas. It saves me a lot of time.” Juma says for other products like milk and

bread, he has an arrangement in which the supplier delivers the goods but he

only pays for them at the end of the day, after selling them. He uses M-PESA to

make the payment. “Initially the suppliers used to come to my shop to collect the

money but nowadays I just ‘M-PESA them.’”

When I ask Juma what one thing he needs most to expand his business, él

tells me it is capital. “I would love to expand my business but I do not have the

capital to do that.”

Thanks to Peter Gakure-Mwangi

As our survey found, most businesses and consumers want to use MM more

regularly. They find it to be safer, más eficiente, and convenient than other pay-

ment channels.

Most mobile operators define an “active user” as someone who uses MM sev-

eral times a month. By facilitating the broader payment ecosystem, from utility and

value chain payments to payments at the point of sale, MM providers could enable

customers to use MM several times a day. This would give customers the potential

to benefit from lower transport and opportunity costs, as well as increased securi-

ty.

Moving informal cash-based transactions to an electronic medium will also

benefit financial institutions and governments. Consumer transactions can be fed

into credit reference bureaus, enabling banks to properly assess the credit worthi-

80

innovaciones / Entrepreneurial Ecosystems

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023

Mobile Money Usage Patterns of Kenyan SMEs

ness of customers and adjust interest rates accordingly. Governmental bodies

would be able to pay workers and welfare recipients more efficiently and at lower

costo.

Cash is the enemy of financial inclusion. By fostering the widespread use and

acceptance of MM, financial services will continue to become more accessible and

affordable for consumers at the base of the pyramid.

1. See David Porteous and Ignacio Mas, “A LiFi World,” CGAP Technology Blog, Enero 11, 2012.

Available at http://technology.cgap.org/2012/01/11/a-lifi-world/.

2. Jake Kendall summarized two of these pieces in “Small Business Might Be Big Business for

Mobile Money,” Next Billion blog, Marzo 23, 2011. Available at http://www.nextbillion.net/blog-

post.aspx?blogid=2216.

3. Adi Ndiwalana, Olga Morawczynski, and Oliver Popov, “Mobile Money Use in Uganda: A

http://scholar.mak.ac.ug/andiwalana/files/m4d-

Disponible

Study.”

en

Preliminary

mobilemoney.pdf.

4. Lennart Bångens and Björn Söderberg, “Mobile Money Transfers and Usage among Micro and

Small Businesses in Tanzania.” Available at

http://www.southcliff.se/docs/SME_AND_MMT_FINAL_DRAFT.pdf.

5. Ignacio Mas and Amolo N’gweno, “Why Doesn’t Every Kenya Business Have a Mobile Money

Account? A Study of the Business Uses of Mobile Money in Kenya,” paper presented at 8th

Research Colloquium, hosted by FSDK, Nairobi, Abril

en

http://www.fsdkenya.org/pdf_documents/12-04-20_Business_uses_of_M-PESA.pdf.

2012. Disponible

6. Pew Research Center, Global Digital Communication: Texting, Social Networking Popular

Worldwide. Available at http://www.pewglobal.org/2011/12/20/global-digital-communication-

texting-social-networking-popular-worldwide/.

7. Non-users may have been less likely to respond to a question about whether or not they use MM;

this would imply an actual rate of usage among SMEs somewhat lower than 99 percent but it

would still be quite high.

8. Ignacio Mas and Dan Radcliffe, “Mobile Payments Go Viral: M-Pesa in Kenya.” Available at

http://www.microfinancegateway.org/gm/document-1.9.43376/Mobile%20Payments%20Go%20

Viral_M-PESA%20in%20Kenya.pdf.

On rent, Nakuru is a significant outlier: 22.47 percent of respondents chose “other” and wrote in

“cheques” when asked to explain.

9. See Jake Kendall, Bill Maurer, Phillip Machoka, and Clara Veniard, “An Emerging Platform: De

Money Transfer System to Mobile Money Ecosystem,” Innovations 6, No. 4 (2011): 49-64; Mukesh

Sadana, George Mugweru, Joyce Murithi, David Cracknell, and Graham A. norte. Wright, “Analysis

de

en

http://www.microsave.org/research_paper/analysis-of-financial-institutions-riding-the-m-pesa-

rails.

the M-PESA

Instituciones

Financial

Disponible

Riding

Rails.”

10. Por ejemplo, Bångens and Söderberg document the frustrations many Tanzanian SMEs face in

getting quality service from agents.

11. Mas and N’gweno, “Why Doesn’t Every Kenya Business.”

innovaciones / volumen 7, number 2

81

Descargado de http://direct.mit.edu/itgg/article-pdf/7/2/67/704905/inov_a_00129.pdf by guest on 07 Septiembre 2023